ASEAN EV Battery Pack Market Size and Share

Market Overview

| Study Period | 2017 - 2029 |

|---|---|

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2017 - 2022 |

| Market Size (2024) | USD 0.33 Billion |

| Market Size (2029) | USD 1.47 Billion |

| Growth Rate (2024 - 2029) | 34.68% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN EV Battery Pack Market Analysis by Mordor Intelligence

The ASEAN EV Battery Pack Market size is estimated at 0.33 billion USD in 2024, and is expected to reach 1.47 billion USD by 2029, growing at a CAGR of 34.68% during the forecast period (2024-2029).

The ASEAN electric vehicle battery pack industry is experiencing transformative growth driven by declining battery costs and technological advancements. Battery prices have witnessed a significant reduction of approximately 80%, reaching USD 220 per kWh by 2023, making electric vehicles more accessible to consumers across the region. This price reduction has been accompanied by improvements in battery chemistry and energy density, enabling longer driving ranges and faster charging capabilities. The industry is also benefiting from increasing environmental consciousness and supportive government policies aimed at reducing carbon emissions across the transportation sector.

Manufacturing capabilities in the region are expanding rapidly through strategic investments and partnerships. In 2023, Banpu NEXT established a lithium-ion electric vehicle battery manufacturing facility in Thailand with an initial production capacity of 1 GWh annually, demonstrating the region's commitment to localizing battery production. Similarly, Chinese battery manufacturer Gotion High Tech announced a joint venture with Thailand's PTT Group in late 2023 for electric vehicle battery pack production and export operations. These developments are strengthening the regional supply chain and reducing dependency on imports.

Technical innovations and evolving battery chemistries are reshaping the market landscape. NMC (Nickel Manganese Cobalt) batteries have emerged as the dominant chemistry, commanding over 60% market share in Thailand as of 2023, due to their superior energy density and performance characteristics. In terms of form factor, prismatic batteries have gained significant traction, accounting for 47.12% of the market share in 2023, owing to their efficient space utilization and thermal management capabilities. This trend reflects the industry's focus on optimizing electric car battery design for improved performance and safety.

Government support and infrastructure development are catalyzing market growth across the ASEAN region. The Thai government's announcement of a USD 689 million subsidy program in February 2023 for EV battery cell manufacturers exemplifies the strong public sector commitment to developing domestic battery production capabilities. Major international players are also recognizing the region's potential, as evidenced by CATL's USD 5 billion investment in an Indonesian battery factory. These investments are complemented by expanding charging infrastructure networks and standardization efforts, creating a more conducive environment for EV adoption and consequently driving demand for EV battery pack solutions.

ASEAN EV Battery Pack Market Trends and Insights

The ASEAN region has several EV manufacturers, but Wuling, Tesla, and BYD were the primary demand generators for battery packs in 2022

- In several ASEAN countries, the demand for electric cars has risen sharply during the last few years. The interest in purchasing EVs varies by location and country. However, in the ASEAN region, SUVs are the most popular EVs. The rising popularity of SUVs as a practical and spacious alternative to sedans is driving the demand for electric SUVs throughout the ASEAN region.

- The demand for compact sport utility vehicles (SUVs) among ASEAN customers has increased dramatically in recent years. Several key ASEAN countries have made the Tesla Model Y one of their top picks due to the vehicle's all-electric powertrain, 5-star NCAP safety certification, room for up to 7 people, long range, and other attributes. The BYD Song DM's plug-in hybrid engine has been well-accepted by consumers in numerous ASEAN nations as well, owing to the vehicle's low price and high fuel economy.

- The Model 3 was one of Tesla's best-selling cars in ASEAN countries in 2022. This is because it has a fully electric engine and several features that make it appealing to buyers. There are also electric SUVs and sedans from different foreign brands in the ASEAN EV market. The Haval H6, Nissan Licks, is a popular car that sold well in 2022. Other cars in the ASEAN EV market that are in competition include the Toyota Innova and Hyundai Ionic.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Growing adoption of electric vehicles in the ASEAN region is driven by government initiatives and infrastructure development

- The dominance of NMC batteries, the growing popularity of LFP batteries, and adoption of NCA batteries

- Foreign investments will boost domestic battery production in APAC

- Growing electrification of vehicles in the ASEAN region is driven by technological advancements and increasing battery capacity and efficiency

- The market is majorly based on imported vehicles and is dominated by Chinese brands

- Electric vehicle sales in New Zealand have been on the rise because of falling battery prices

- Downward price trend in ASEAN battery chemistries: factors driving the decline and future outlook for the electric vehicle industry

- International automakers are entering the Thai EV market with new models, thus driving EV and battery pack demand.

Segment Analysis: Body Type

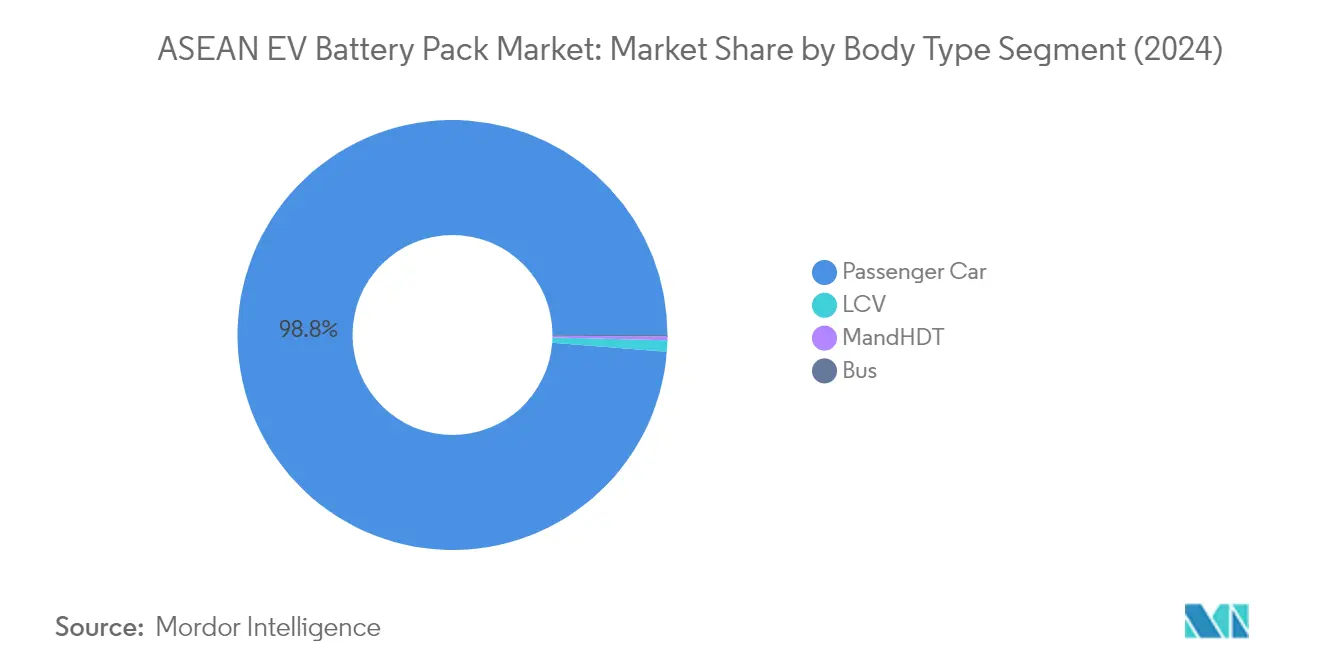

Passenger Car Segment in ASEAN EV Battery Pack Market

The passenger car segment dominates the ASEAN EV battery pack market, commanding approximately 99% market share in 2024. This overwhelming dominance can be attributed to several factors, including increasing consumer awareness about environmental sustainability, government incentives for electric passenger vehicles, and the expanding charging infrastructure across ASEAN countries. Thailand, being the largest EV market in the region, has significantly contributed to this segment's growth through its strong focus on passenger electric vehicles. The segment's robust performance is further supported by the entry of major global automakers and their growing investment in electric passenger vehicle production facilities across ASEAN nations. The integration of EV battery module and EV battery cell technologies has been pivotal in enhancing the performance and efficiency of passenger cars.

Bus Segment in ASEAN EV Battery Pack Market

The bus segment is emerging as the fastest-growing segment in the ASEAN EV battery pack market, projected to grow at approximately 143% CAGR from 2024 to 2029. This exceptional growth is driven by increasing government initiatives to electrify public transportation systems across ASEAN countries. The surge is particularly notable in countries like Indonesia, where major transportation companies are actively expanding their electric bus fleets. The growth is further accelerated by advancements in battery technology specifically designed for heavy-duty applications, making electric buses more viable for public transportation. Rising urbanization and the push for sustainable mass transit solutions are also contributing to the segment's rapid expansion.

Remaining Segments in Body Type

The LCV and M&HDT segments, while currently holding smaller market shares, play crucial roles in the ASEAN EV battery pack market's diversification. The LCV segment is gaining traction in urban logistics and last-mile delivery applications, particularly in developed ASEAN markets. Meanwhile, the M&HDT segment is emerging as a significant player in the commercial transportation sector, with increasing adoption in logistics and construction industries. Both segments are benefiting from technological advancements in battery capacity and charging infrastructure, making electric commercial vehicles more practical for business operations. The role of EV battery component and battery management system technologies is crucial in optimizing the performance of these segments.

Segment Analysis: Propulsion Type

BEV Segment in ASEAN EV Battery Pack Market

Battery Electric Vehicles (BEVs) have emerged as the dominant force in the ASEAN EV battery pack market, commanding approximately 100% of the market share in 2024. This overwhelming dominance can be attributed to several factors, including the superior performance characteristics of BEVs, their lower maintenance requirements, and zero direct emissions. The segment's growth is further bolstered by supportive government policies across ASEAN nations, particularly in Thailand and Indonesia, where substantial incentives and infrastructure development initiatives are driving BEV adoption. The segment is experiencing remarkable growth, with projections indicating a robust expansion at a rate of nearly 50% from 2024 to 2029. This growth trajectory is supported by increasing consumer awareness, expanding charging infrastructure, and the entry of major automotive manufacturers into the ASEAN BEV market. Additionally, the declining costs of battery technology and improving energy density of BEV batteries are making these vehicles increasingly attractive to consumers across the region. The integration of traction battery pack systems is enhancing the efficiency and range of BEVs.

PHEV Segment in ASEAN EV Battery Pack Market

The Plug-in Hybrid Electric Vehicle (PHEV) segment currently shows minimal market presence in the ASEAN EV battery pack market. This limited market penetration can be attributed to various factors, including higher vehicle costs due to the complexity of dual powertrains, limited model availability, and stronger market preference for pure electric vehicles. The segment faces challenges in gaining traction despite the potential advantage of range anxiety mitigation, as consumers in the ASEAN region increasingly favor full electric solutions. Market dynamics suggest that while PHEVs offer a transitional solution between conventional vehicles and full electric vehicles, the direct shift to BEVs appears to be the predominant trend in the ASEAN market.

Segment Analysis: Battery Chemistry

NMC Segment in ASEAN EV Battery Pack Market

The NMC (Nickel Manganese Cobalt) battery chemistry dominates the ASEAN EV battery pack market, commanding approximately 61% market share in 2024. This significant market position can be attributed to NMC batteries' superior characteristics including high energy density, lighter weight, and enhanced charging capabilities. The segment's dominance is particularly evident in Thailand, which represents the largest EV market in the ASEAN region. Major automakers are increasingly adopting NMC batteries for their electric vehicle models due to their optimal balance of performance, cost, and reliability. The growing consumer preference for electric vehicles with longer range and faster charging capabilities has further strengthened the position of NMC batteries in the market.

LFP Segment in ASEAN EV Battery Pack Market

The Lithium Iron Phosphate (LFP) battery segment is emerging as the fastest-growing segment in the ASEAN EV battery pack market, projected to grow at approximately 54% annually from 2024 to 2029. This remarkable growth trajectory is driven by several factors including LFP batteries' cost-effectiveness, enhanced safety features, and extended lifespan. The segment is witnessing increased adoption particularly in commercial vehicle applications and mass-market electric vehicles. Manufacturers are investing heavily in LFP technology development and production capacity expansion across various ASEAN countries, particularly in Thailand and Indonesia. The growing emphasis on safety and reliability in electric vehicles, coupled with the decreasing costs of LFP battery production, is expected to maintain this segment's strong growth momentum.

Remaining Segments in Battery Chemistry

The remaining battery chemistry segments in the ASEAN EV battery pack market include NCA (Nickel Cobalt Aluminum) and other emerging chemistries. NCA batteries are gaining traction in premium electric vehicles due to their high energy density and superior performance characteristics. These segments play a crucial role in serving specific market niches and applications where their unique properties provide distinct advantages. The diversity in battery chemistry options allows manufacturers to optimize their electric vehicle offerings based on different performance requirements, cost considerations, and target market segments. The continuous research and development in these battery chemistries contribute to the overall advancement of the ASEAN EV battery ecosystem.

Segment Analysis: Battery Form

Prismatic Segment in ASEAN EV Battery Pack Market

The prismatic battery form continues to dominate the ASEAN EV battery pack market, commanding approximately 47% market share in 2024. This significant market position can be attributed to several advantages that prismatic batteries offer, including their cost-effectiveness in manufacturing, excellent safety ratings, ease of production, and high energy density. The prismatic form factor is particularly popular among major automotive manufacturers in the region due to its efficient space utilization and thermal management capabilities. Additionally, prismatic batteries have demonstrated superior performance in various electric vehicle applications, from passenger cars to commercial vehicles, making them the preferred choice for many OEMs operating in the ASEAN market. The segment's strong position is further reinforced by established supply chains and manufacturing infrastructure specifically designed for prismatic battery production across key ASEAN markets like Thailand and Indonesia.

Pouch Segment in ASEAN EV Battery Pack Market

The pouch battery segment is emerging as the fastest-growing form factor in the ASEAN EV battery pack market, projected to expand at an impressive rate between 2024 and 2029. This remarkable growth trajectory is driven by several key advantages that pouch cells offer, including their high energy density, enhanced flexibility in design and packaging, and cost-effective manufacturing processes. Automotive manufacturers across ASEAN are increasingly adopting pouch batteries for their new electric vehicle models, particularly in applications where space optimization and weight reduction are crucial factors. The segment's growth is further supported by ongoing technological advancements in pouch cell manufacturing, improved safety features, and enhanced thermal management capabilities. Additionally, significant investments in pouch battery production facilities across the region, coupled with increasing collaboration between battery manufacturers and automotive OEMs, are expected to sustain this segment's rapid expansion through 2029.

Remaining Segments in Battery Form

The cylindrical battery form represents another significant segment in the ASEAN EV battery pack market, offering unique advantages that complement the broader market landscape. Cylindrical batteries are particularly valued for their streamlined manufacturing processes, high output capabilities, and enhanced uniformity in production. These batteries have established a strong presence in specific electric vehicle applications where their form factor provides optimal performance characteristics. The standardized nature of cylindrical cells makes them particularly attractive for certain vehicle designs and applications, while their proven track record in terms of reliability and performance continues to drive their adoption across various electric vehicle platforms in the ASEAN region. The segment maintains its relevance through continuous innovations in cell chemistry and manufacturing processes, ensuring its important role in the overall battery form ecosystem.

Segment Analysis: Method

Laser Segment in ASEAN EV Battery Pack Market

The laser method has emerged as the dominant technology in the ASEAN EV battery pack market, commanding approximately 56% market share in 2024. This method has gained significant traction due to its superior capabilities in creating high-quality connections, particularly beneficial for high-current batteries. The laser welding technique offers distinct advantages including improved joint strength, reduced resistance, and enhanced thermal management capabilities. The technology enables precise control over weld parameters, ensuring consistent and reliable connections between battery components. Manufacturers across ASEAN are increasingly adopting laser welding for its ability to work effectively on irregular surfaces and its suitability for high-volume production environments. The segment's growth is further bolstered by its ability to provide robust and durable connections, making it particularly valuable for electric vehicle applications where reliability is paramount. Additionally, the laser method's capability to maintain high precision while operating at increased production speeds has made it the preferred choice for many battery manufacturers in the region.

Wire Method in ASEAN EV Battery Pack Market

The wire bonding method represents a traditional yet reliable approach in the ASEAN EV battery pack market, particularly favored in low to medium-power applications. This method utilizes ultrasonic or thermocompression bonding techniques to establish connections between battery cells, offering a cost-effective solution for manufacturers. The wire method's popularity stems from its proven track record in creating dependable connections, with factors such as wire material selection, diameter optimization, and bonding parameters playing crucial roles in ensuring efficient performance. The technique's adaptability to various battery configurations and its relatively straightforward implementation process make it an attractive option for certain market segments. While the wire method may not offer the same level of precision as laser welding, it continues to maintain its relevance in specific applications where cost considerations and simpler manufacturing processes are prioritized over high-power requirements.

Segment Analysis: Component

Cathode Segment in ASEAN EV Battery Pack Market

The cathode segment dominates the ASEAN EV battery pack market, accounting for approximately 50% of the total market value in 2024. This significant market share can be attributed to cathodes being one of the most critical and expensive components in battery cell manufacturing, constituting about 52% of all battery cell components across ASEAN countries. The segment's dominance is further strengthened by its crucial role in determining battery performance, range, and thermal safety characteristics. Cathodes are integral to all battery chemistries, including LFP, NMC, and NCA, which are widely used across the region. The growing adoption of electric vehicles, particularly in countries like Thailand, Indonesia, and Singapore, continues to drive the demand for high-performance cathode materials. Manufacturers are increasingly focusing on developing advanced cathode materials to enhance battery efficiency and performance, further solidifying the segment's market position.

Separator Segment in ASEAN EV Battery Pack Market

The separator segment is emerging as the fastest-growing component in the ASEAN EV battery pack market, projected to grow at a robust rate between 2024 and 2029. This growth is primarily driven by the increasing adoption of electric vehicles and the subsequent demand for high-quality battery components. Separators, while accounting for only about 7% of the overall battery cost, play a crucial role in ensuring battery safety and performance by facilitating ion transport while preventing electrical shorts. The segment's growth is further supported by technological advancements in separator materials and manufacturing processes, leading to improved battery performance and safety features. Major battery manufacturers in the region are investing in separator technology development to enhance battery efficiency and longevity. The segment is also benefiting from the establishment of local battery manufacturing facilities across ASEAN countries, particularly in Thailand and Indonesia.

Remaining Segments in Component Segmentation

The anode and electrolyte segments also play vital roles in the ASEAN EV battery pack market. The anode segment, being a fundamental component of lithium-ion batteries, continues to evolve with new materials and technologies being developed to improve battery performance and charging capabilities. Anodes, typically made from materials like graphite and silicon, are crucial in determining the battery's capacity and charging speed. The electrolyte segment, while relatively smaller in terms of cost contribution, is essential for ion transport between electrodes and plays a critical role in battery functionality and safety. Both segments are witnessing significant technological advancements and innovations, particularly in terms of material development and manufacturing processes, contributing to the overall growth of the EV battery pack market in the ASEAN region.

Segment Analysis: Material Type

Natural Graphite Segment in ASEAN EV Battery Pack Market

Natural graphite has emerged as the dominant material in the ASEAN EV battery pack market, driven by its crucial role as a key anode material in various battery types including LFP, NMC, NCM, and NCA batteries. The material accounts for approximately 77% of the total material volume in 2024, highlighting its fundamental importance in battery production. Natural graphite's popularity stems from its high energy density, cost-effectiveness, and superior performance characteristics in EV batteries. The segment is experiencing remarkable growth with a projected growth rate of around 50% from 2024 to 2029, driven by increasing EV adoption across ASEAN nations, particularly in Thailand, Indonesia, and Malaysia. The material's widespread adoption is further supported by its abundant availability, established supply chains, and continuous technological improvements in graphite processing and battery manufacturing techniques. The demand is particularly strong in the passenger car segment, where natural graphite-based anodes are preferred for their reliability and performance characteristics.

Remaining Segments in Material Type

The ASEAN EV battery pack market encompasses several other critical materials including lithium, cobalt, manganese, and nickel, each playing vital roles in battery chemistry and performance. Lithium serves as the fundamental component in all lithium-ion batteries, essential for ion transport and energy storage. Cobalt is crucial for providing structural stability and enhancing the battery's energy density, particularly in NMC and NCA chemistries. Manganese contributes to thermal stability and safety features while helping reduce overall battery costs. Nickel is instrumental in improving energy density and extending driving range, particularly important in high-performance EVs. These materials collectively contribute to the advancement of battery technology, with their usage patterns influenced by factors such as cost, availability, and specific performance requirements of different EV applications across the ASEAN region.

ASEAN EV Battery Pack Market Geography Segment Analysis

ASEAN EV Battery Pack Market in Thailand

Thailand has established itself as the dominant force in the ASEAN EV battery pack market, with its robust automotive manufacturing infrastructure and supportive government policies. The country has successfully positioned itself as a major manufacturing hub for electric vehicles and electric vehicle battery packs in the region, accounting for approximately 50% of the total ASEAN EV battery pack market volume in 2024. The Thai government's commitment to electrification is evident through its comprehensive incentive programs, including excise tax reductions of up to 50% for locally assembled EVs and up to 80% for imported vehicles. The country's strategic focus on developing its EV ecosystem has attracted significant investments from both domestic and international players in the battery manufacturing sector. Thailand's strong automotive supply chain, skilled workforce, and established quality control standards have made it an attractive destination for automotive battery pack manufacturers. The presence of major automotive OEMs and their supplier networks has further strengthened Thailand's position in the regional EV battery pack market.

ASEAN EV Battery Pack Market in Indonesia

Indonesia has emerged as a significant player in the ASEAN electric vehicle battery market, leveraging its vast natural resources, particularly nickel reserves, which are crucial for battery production. The country's strategic approach to developing its EV battery ecosystem includes establishing partnerships with global battery manufacturers and automotive companies. Indonesia's government has implemented comprehensive policies to attract investments in the EV battery sector, including tax incentives and simplified licensing procedures. The country's commitment to becoming a global EV battery hub is evident through its focus on developing integrated battery production facilities. Indonesia's abundant raw material resources, combined with its large domestic market potential, have attracted significant investments from international battery manufacturers. The country's efforts to develop its battery manufacturing capabilities are supported by collaborations with established global players in the battery industry. The government's push for local content requirements has also stimulated the development of a domestic battery supply chain.

ASEAN EV Battery Pack Market in Malaysia

Malaysia has positioned itself as a key player in the ASEAN automotive battery pack market through its focus on high-technology manufacturing and research capabilities. The country's well-developed semiconductor industry and expertise in electronics manufacturing provide a strong foundation for electric car battery pack production. Malaysia's strategic location and established trade relationships have facilitated its integration into the regional EV battery supply chain. The government's commitment to sustainable mobility is reflected in its comprehensive National Automotive Policy, which emphasizes the development of EV-related technologies. The country's advanced manufacturing capabilities and skilled workforce have attracted investments in battery pack assembly and testing facilities. Malaysia's focus on developing charging infrastructure and promoting EV adoption has created a conducive environment for battery pack manufacturers. The country's strong intellectual property protection and research institutions have fostered innovation in battery technology development.

ASEAN EV Battery Pack Market in Singapore

Singapore has carved out a unique position in the ASEAN EV battery pack market by focusing on research and development, quality control, and high-value manufacturing activities. The city-state's advanced technological infrastructure and strong intellectual property protection have made it an attractive location for battery innovation centers. Singapore's emphasis on sustainable urban mobility has created opportunities for specialized battery pack applications. The country's expertise in precision engineering and quality control has positioned it as a center for battery testing and certification in the region. Singapore's strong financial sector and supportive regulatory environment have facilitated investments in battery technology startups. The country's focus on developing smart mobility solutions has driven innovation in battery management systems and charging technologies. Singapore's role as a regional trading hub has enabled efficient distribution of battery components and finished products throughout ASEAN.

ASEAN EV Battery Pack Market in Other Countries

The EV battery pack market in other ASEAN countries, including Vietnam, the Philippines, Brunei, Cambodia, Laos, and Myanmar, is at various stages of development, each presenting unique opportunities and challenges. These markets are characterized by growing awareness of electric mobility and increasing government support for sustainable transportation solutions. While some countries are focusing on assembly operations, others are developing their capabilities in specific components of the battery value chain. The varying levels of infrastructure development and market maturity across these countries create diverse opportunities for battery pack manufacturers and suppliers. Regional cooperation initiatives and technology transfer programs are helping these markets develop their EV battery capabilities. The growing emphasis on reducing carbon emissions and promoting sustainable transportation is driving the adoption of EVs and, consequently, the demand for EV energy storage and automotive energy storage solutions in these markets.

Competitive Landscape

Top Companies in ASEAN EV Battery Pack Market

The ASEAN EV battery pack market is characterized by intense innovation and strategic developments among key players like CATL, BYD Company, Deutsche ACCUmotive, Samsung SDI, and LG Energy Solution. Companies are heavily investing in research and development to improve battery chemistry, focusing particularly on NCM and LFP technologies to enhance energy density and performance. Operational agility is demonstrated through rapid capacity expansion initiatives, with many players establishing new manufacturing facilities across Thailand, Indonesia, and other ASEAN countries. Strategic partnerships with automotive manufacturers and local enterprises have become increasingly common, enabling better market penetration and technology transfer. Companies are also emphasizing sustainable production methods and circular economy principles, including battery recycling programs and green manufacturing practices, to maintain a competitive advantage.

Market Dominated by Global Battery Specialists

The ASEAN EV battery pack market exhibits a high level of consolidation, with Chinese and South Korean manufacturers holding significant market share. These global players leverage their advanced technological capabilities, established supply chains, and economies of scale to maintain their dominant positions. The market structure is characterized by a mix of pure-play battery manufacturers and diversified technology conglomerates, with the former leading in terms of market share and innovation. Local players are gradually emerging, particularly in Thailand and Indonesia, supported by government initiatives and partnerships with global leaders.

The market is witnessing increased merger and acquisition activity as companies seek to strengthen their regional presence and technological capabilities. Joint ventures between global battery manufacturers and local automotive companies are becoming more prevalent, facilitating technology transfer and local manufacturing capabilities. Companies are also pursuing vertical integration strategies, securing raw material supplies and establishing end-to-end production capabilities within the region. This consolidation trend is expected to continue as players seek to achieve economies of scale and enhance their competitive positioning in the rapidly growing market.

Innovation and Localization Drive Future Success

Success in the ASEAN EV battery pack market increasingly depends on companies' ability to combine technological innovation with local market understanding. Incumbent players must focus on continuous product innovation, particularly in areas such as fast charging capabilities, energy density improvements, and cost reduction through manufacturing efficiency. Building strong relationships with local governments and automotive manufacturers is crucial for maintaining market share. Companies must also invest in local research and development facilities to adapt their technologies to regional requirements and weather conditions.

For new entrants and smaller players, differentiation through specialized battery solutions for specific vehicle segments or applications offers a viable path to market share growth. Success factors include developing robust supply chain networks within ASEAN, establishing strategic partnerships with local automotive manufacturers, and maintaining compliance with evolving regulatory standards. The regulatory landscape is becoming increasingly supportive of domestic battery production, with various governments offering incentives for local manufacturing and technology development. Companies must also address environmental concerns through sustainable production practices and end-of-life battery management systems solutions to maintain their competitive edge.

ASEAN EV Battery Pack Industry Leaders

BYD Company Ltd.

Contemporary Amperex Technology Co. Ltd. (CATL)

Deutsche ACCUmotive GmbH & Co. KG

LG Energy Solution Ltd.

Samsung SDI Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2023: CATL announced that it will launch its sodium-ion battery in Chery models first. In addition, the two parties will jointly build the new ENER-Q battery brand, covering all application scenarios of all power types and all material systems.

- March 2023: Contemporary Amperex Technology Co., Ltd. (CATL) announced that it signed a strategic cooperation agreement on business cooperation and advanced technology development with Beijing Automotive Group Co., Ltd. (BAIC Group).

- March 2023: Contemporary Amperex Technology Co., Ltd. (CATL) announced that it has established a joint venture (JV) named Jiefang Shidai New Energy Technology Co., Ltd. with FAW Jiefang Automotive Co., Ltd. (FAW Jiefang). The JV has a registered capital of CNY 90 million, with CATL and FAW Jiefang each holding a 50% share.

ASEAN EV Battery Pack Market Report Scope

Bus, LCV, M&HDT, Passenger Car are covered as segments by Body Type. BEV, PHEV are covered as segments by Propulsion Type. LFP, NCA, NCM, NMC are covered as segments by Battery Chemistry. 15 kWh to 40 kWh, 40 kWh to 80 kWh, Above 80 kWh, Less than 15 kWh are covered as segments by Capacity. Cylindrical, Pouch, Prismatic are covered as segments by Battery Form. Laser, Wire are covered as segments by Method. Anode, Cathode, Electrolyte, Separator are covered as segments by Component. Cobalt, Lithium, Manganese, Natural Graphite, Nickel are covered as segments by Material Type. Thailand are covered as segments by Country.| Bus |

| LCV |

| M&HDT |

| Passenger Car |

| BEV |

| PHEV |

| LFP |

| NCA |

| NCM |

| NMC |

| 15 kWh to 40 kWh |

| 40 kWh to 80 kWh |

| Above 80 kWh |

| Less than 15 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Laser |

| Wire |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| Cobalt |

| Lithium |

| Manganese |

| Natural Graphite |

| Nickel |

| Other Materials |

| Thailand |

| Body Type | Bus |

| LCV | |

| M&HDT | |

| Passenger Car | |

| Propulsion Type | BEV |

| PHEV | |

| Battery Chemistry | LFP |

| NCA | |

| NCM | |

| NMC | |

| Capacity | 15 kWh to 40 kWh |

| 40 kWh to 80 kWh | |

| Above 80 kWh | |

| Less than 15 kWh | |

| Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| Method | Laser |

| Wire | |

| Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator | |

| Material Type | Cobalt |

| Lithium | |

| Manganese | |

| Natural Graphite | |

| Nickel | |

| Other Materials | |

| Country | Thailand |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 1

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms