Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

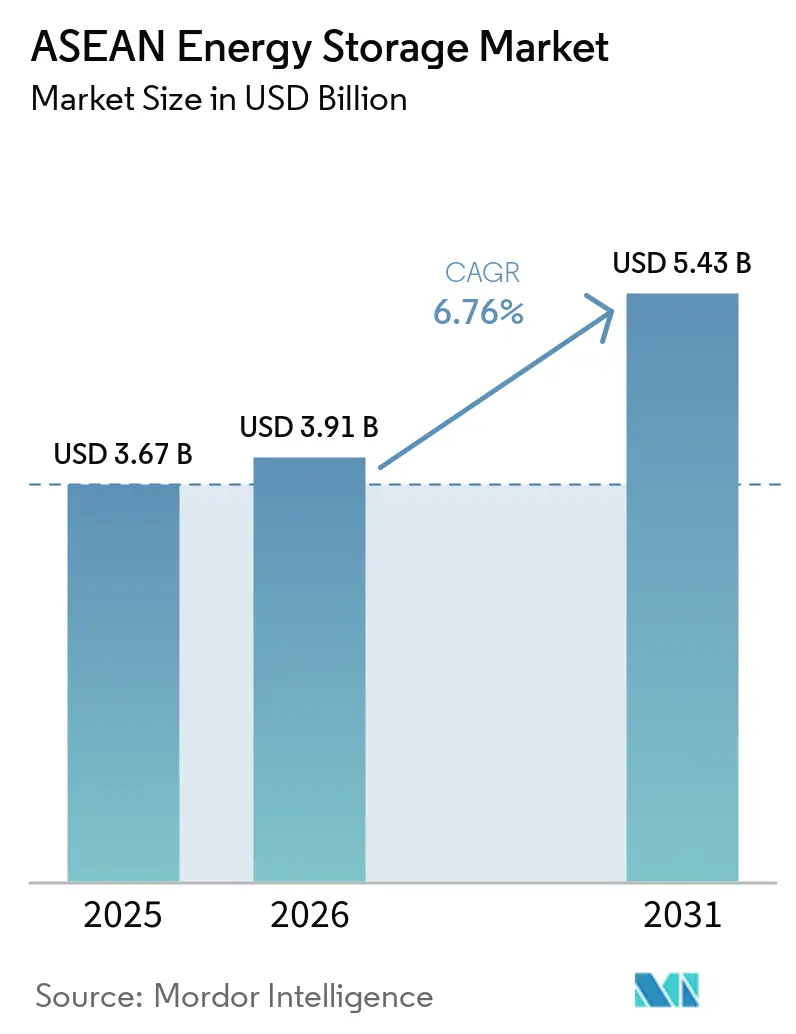

| Base Year Market Size (2025) | USD 3.67 Billion |

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Energy Storage Market Analysis by Mordor Intelligence

The ASEAN Energy Storage Market size is projected to expand from USD 3.67 billion in 2025 and USD 3.91 billion in 2026 to USD 5.43 billion by 2031, registering a CAGR of 6.76% between 2026 and 2031. The ASEAN energy storage market still leaned heavily on large infrastructure in 2025, with pumped-storage hydroelectricity holding 80.9% of storage technology demand and on-grid systems accounting for 79.1% of total deployments. Regional power demand rose by more than 7% in 2024, while ASEAN adopted a 30% renewable share in primary energy and a 45% share in installed power capacity by 2030 under APAEC 2026-2030, which lifted the need for storage across balancing, reserve, and capacity use cases. The ASEAN energy storage market is also being pushed by state utility programs in Indonesia, Vietnam, and Thailand, while grid-scale utility applications already held a 47.2% share in 2025, and data centres and critical facilities are set to expand at the fastest application CAGR of 10.3% through 2031. Within the ASEAN energy storage market, Indonesia led with a 29.1% regional share in 2025, while Vietnam is forecast to grow the fastest at 9.3% through 2031 as planning reforms and mandated storage additions move into execution.[1]Tạp chí Năng lượng Việt Nam, “Việt Nam Tăng Tốc Lộ Trình Phát Triển Lưu Trữ Năng Lượng,” Tạp chí Năng lượng Việt Nam, thuongtruong.com.vn Regulatory uncertainty around standalone storage and uneven financing conditions still slow larger projects, which keeps the ASEAN energy storage market on a two-speed path where off-grid and behind-the-meter projects often move faster than long-duration utility assets.

Key Report Takeaways

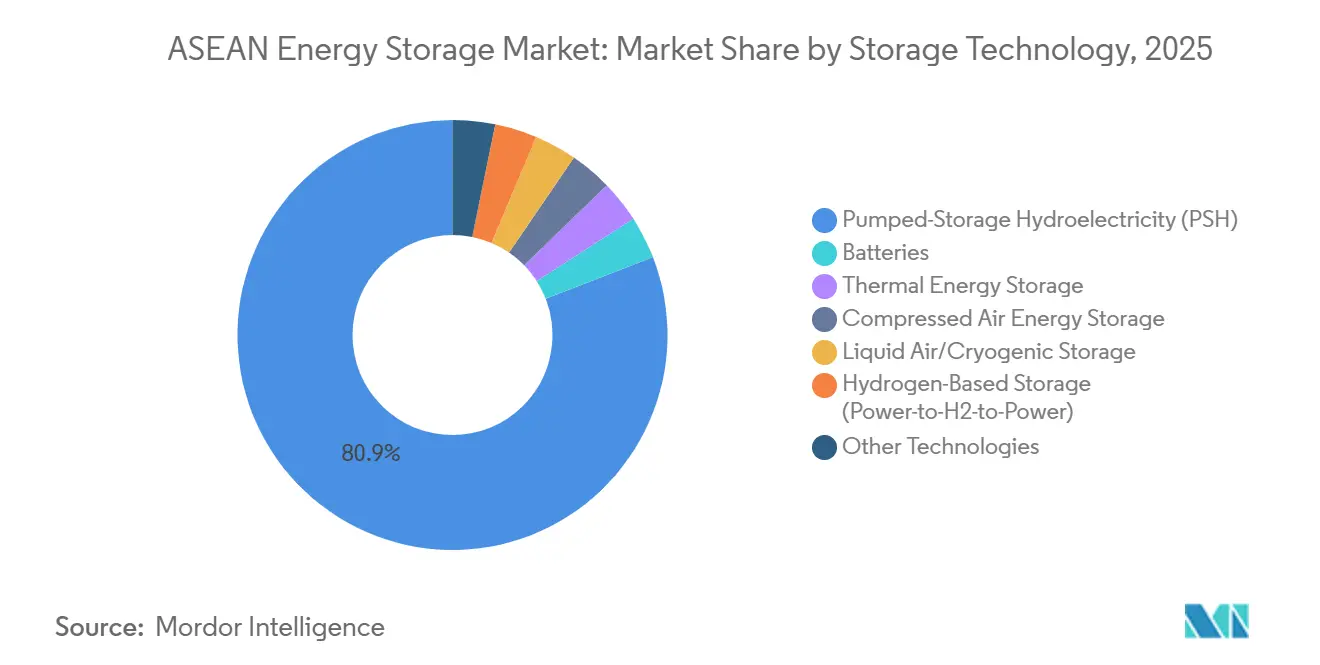

- By storage technology, Pumped-Storage Hydroelectricity held 80.9% of the ASEAN energy storage market share in 2025, while hydrogen-based storage is forecast to expand at an 11.1% CAGR through 2031.

- By connectivity, on-grid storage held 79.1% of the ASEAN energy storage market share in 2025, while off-grid storage recorded the highest projected CAGR at 9.1% through 2031.

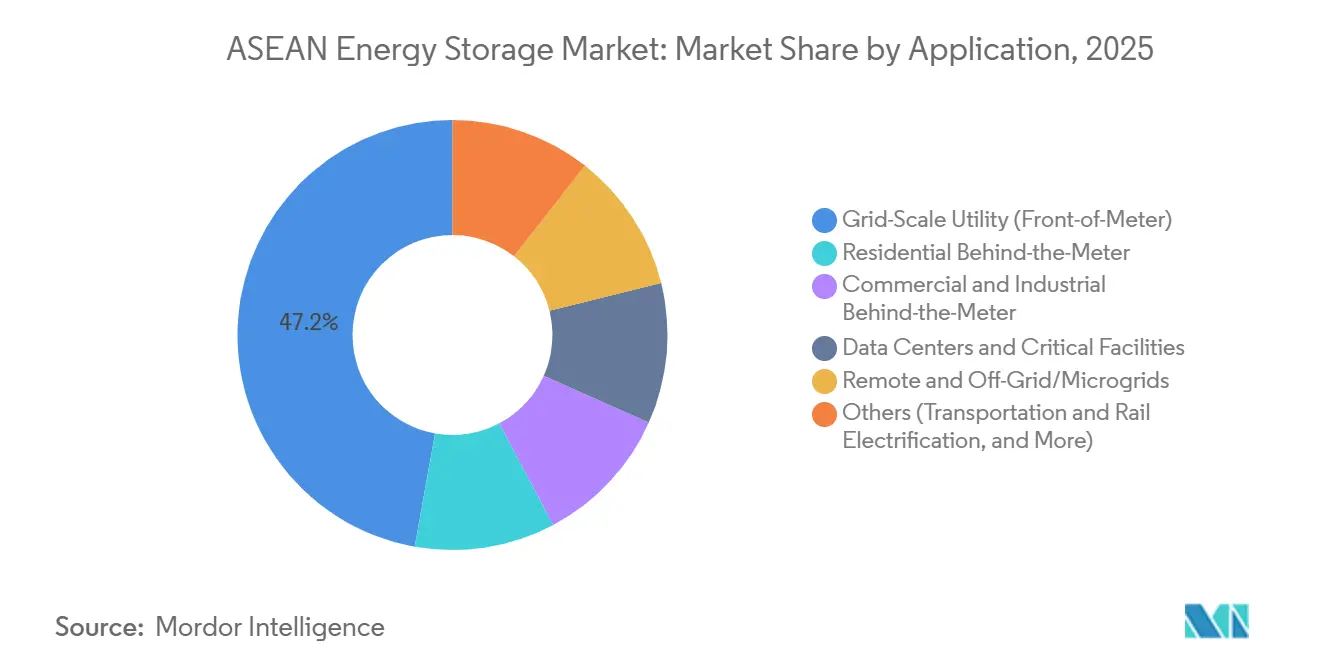

- By application, grid-scale utility storage accounted for 47.2% of the ASEAN energy storage market size in 2025, while data centres and critical facilities are expected to advance at a 10.3% CAGR through 2031.

- By geography, Indonesia held 29.1% share of the regional market in 2025, while Vietnam recorded the highest projected CAGR at 9.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

ASEAN Energy Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Electricity Demand from C&I Sector | +1.5% | Vietnam, Indonesia, Thailand, with spill-over to the Philippines and Malaysia | Short term (≤ 2 years) |

| Grid Stability Issues and Outage Mitigation Needs | +1.0% | Vietnam, the Philippines, and Indonesia | Short term (≤ 2 years) |

| ASEAN Renewable Portfolio Targets Acceleration | +1.8% | Regional, with stronger concentration in Vietnam, Indonesia, and the Philippines | Medium term (2-4 years) |

| Falling Li-ion Battery Costs | +1.2% | Regional, with stronger uptake in Malaysia, Thailand, and Singapore | Short term (≤ 2 years) |

| Digital Twin Enabled Optimisation of Storage | +0.4% | Singapore, Thailand, and Malaysia | Medium term (2-4 years) |

| Island Grid Resiliency and Diesel Offset Programmes | +0.7% | Indonesia, the Philippines, and the rest of ASEAN | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ASEAN Renewable-Portfolio Targets Accelerating Storage Deployment

The ASEAN energy storage market is being shaped by a higher regional renewable ambition under APAEC 2026-2030, which raised the 2030 target to 30% of primary energy and 45% of installed power capacity. Vietnam’s adjusted Power Master Plan VIII moved this shift into project design by requiring centralised solar projects to install BESS equal to at least 10% of installed capacity for 2-hour storage. Indonesia’s RUPTL 2025-2034 also gave storage a planned role by assigning 15% of new capacity additions to storage assets alongside a wider renewable build-out. These changes matter because they shift storage from a discretionary balancing tool into a utility procurement category with direct links to renewable auctions and grid planning. The IEA’s integration roadmap for Southeast Asia also shows that faster solar and wind additions will need more system flexibility between 2025 and 2028, which keeps storage near the center of regional power policy.[2]International Energy Agency, “Integrating Solar and Wind in Southeast Asia,” IEA, iea.org

Electricity Demand from C&I Sector Creating Behind-the-Meter Storage Markets

The ASEAN energy storage market is also gaining support from industrial users that need more stable power and better control over outages, curtailment, and operating costs. Grid-scale systems still take the largest application share, but data centres and critical facilities are the fastest-growing application block at 10.3% CAGR through 2031, which shows how strongly reliability-led demand is rising across the region. In Vietnam, storage is moving closer to factories and industrial parks as new planning rules and the formal recognition of storage in the power framework create a clearer path for deployment. This part of the ASEAN energy storage market is important because manufacturers and digital operators value continuity and power quality even when wholesale flexibility markets remain immature. That makes commercial and industrial storage demand more durable in countries where policy is still catching up with system needs.

Grid-Stability Issues and Outage Mitigation as an Immediate Procurement Signal

The ASEAN energy storage market is responding to a grid problem that is immediate rather than theoretical, because renewable additions are already moving ahead of network reinforcement in several countries. The IEA identified the 2025-2028 period as critical for building flexibility procurement mechanisms across Southeast Asia, which makes storage one of the few technologies that can address balancing, reserves, and integration at the same time. The Philippines has moved further than most regional peers in turning this need into contracted capacity, while Singapore is using battery systems to support renewable imports and grid balancing across a tightly managed power system. Vietnam’s storage push is also linked to curtailment and dispatch challenges, which is why both pumped hydro and battery systems are now appearing in parallel project pipelines. For utilities, this makes storage less of a technology option and more of a grid-loss prevention and service continuity tool.

Island-Grid Resiliency Creating a Parallel Off-Grid Storage Economy

The ASEAN energy storage market has a second growth lane in island systems where diesel replacement often offers a clearer business case than large on-grid arbitrage. Off-grid storage is forecast to grow at 9.1% through 2031, which is faster than the on-grid segment because project economics are tied more directly to fuel savings and service reliability. Indonesia’s current rollout of solar-plus-BESS projects to replace diesel units shows how storage is becoming part of basic electrification and supply security across dispersed systems. The Philippines is following a similar path through hybrid microgrids and island service contracts that combine solar, batteries, and backup capacity to stabilize local supply. This side of the ASEAN energy storage market often advances faster because projects do not depend on a fully liberalised ancillary services framework to justify investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital Intensity and Limited Project Finance | -0.8% | Regional, with stronger pressure in Indonesia, Vietnam, and Cambodia | Medium term (2-4 years) |

| Ambiguous Storage Asset Class Regulation | -0.6% | Indonesia, Vietnam, and Malaysia | Medium term (2-4 years) |

| Community Push Back on Pumped Hydro | -0.3% | The Philippines, Indonesia, and Vietnam | Medium term (2-4 years) |

| Nickel Manganese Supply Chain Volatility | -0.4% | Regional, with higher concentration in NMC and NMCA supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital-Intensity and the Project Finance Gap

High upfront costs remain one of the clearest brakes on the ASEAN energy storage market, especially for long-duration assets and large standalone battery projects. Vietnam shows this clearly because multiple BESS projects remained stalled into early 2026 while pricing rules for standalone storage, ancillary compensation, and capacity payments were still being finalised under Circular 62/2025/TT-BCT. Large pumped hydro projects are moving forward, but many depend on concessional or multilateral funding rather than broad commercial bank participation, as seen in Bac Ai’s financing structure and Indonesia’s wider state-backed pipeline. This slows the conversion of announced targets into contracted and commissioned capacity across the ASEAN energy storage market. It also leaves smaller developers at a disadvantage because domestic lenders still treat many storage structures as unfamiliar risk.

Ambiguous Storage Asset-Class Regulation

Regulatory ambiguity still delays investment across the ASEAN energy storage market because project developers need clear rules on ownership, compensation, grid connection, and service stacking. The IEA identified 2025-2028 as the decisive period for building flexibility markets in Southeast Asia, yet the region still moves unevenly on the treatment of storage as a distinct asset class. Singapore and the Philippines remain ahead in market design, while other countries are still refining pilot mechanisms, interconnection procedures, and payment structures for non-energy services. Vietnam’s recognition of storage in law is an important step, but implementation details still matter for bankability and project timing. Until these rules become more predictable, the ASEAN energy storage market will keep favoring projects backed by utilities, public plans, or clear captive demand rather than fully merchant business models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: PSH Retains Scale Dominance as Battery Technologies Diversify

Pumped-Storage Hydroelectricity held 80.9% of the ASEAN energy storage market size in 2025, which shows how strongly the region still depends on long-established civil infrastructure for bulk storage. That position is reinforced by major project pipelines in Indonesia, Vietnam, and Thailand, where state utilities continue to treat pumped hydro as a strategic balancing asset rather than a niche technology. Vietnam’s 1,200 MW Bac Ai pumped storage project entered its main construction phase in 2026 and remains central to the country’s effort to absorb more renewable output from high-curtailment regions. Thailand also plans 2,472 MW of additional pumped hydro under PDP 2024 through the Chulabhorn, Vajiralongkorn, and Krathun projects, which confirms that PSH will stay important well beyond the current forecast period.

Battery technologies, however, are where most incremental diversification is taking place in the ASEAN energy storage market. Hydrogen-based storage is the fastest-growing technology segment at 11.1% CAGR from 2026 to 2031, which reflects growing interest in longer-duration flexibility and island-grid applications. Lithium-ion systems remain the main battery choice across utility and behind-the-meter projects, with LFP, NMC, and emerging sodium-ion chemistries shaping the procurement mix. Lower global battery costs are improving the case for utility-scale BESS, while thermal stability and safety are becoming more important in tropical operating conditions. Flow batteries, thermal systems, and compressed air are still early in the region, but they address storage durations that lithium-ion does not serve as efficiently. Safety certification is also becoming a stronger buying factor, which gives structured system integrators a clearer advantage in public and utility tenders.

By Connectivity: On-Grid Scale Anchors Market, Off-Grid Accelerates on Island Economics

On-grid storage held 79.1% of the ASEAN energy storage market size in 2025, reflecting the dominance of regulated procurement, utility planning, and sovereign-backed projects. Indonesia’s RUPTL 2025-2034 alone includes 10.3 GW of storage, made up of 6.0 GW of pumped hydro and 4.3 GW of BESS, which gives the on-grid segment a scale base that private developers cannot easily match. Similar state-led programs in Vietnam, Thailand, Malaysia, and the Philippines keep on-grid storage at the center of near-term capital deployment. This part of the ASEAN energy storage industry is more bankable because long project life, public procurement, and multilateral finance lower risk compared with purely commercial storage models.

Off-grid storage is moving faster in percentage terms and is projected to grow at 9.1% through 2031. The demand case is strongest in island systems where storage directly replaces diesel consumption and improves supply continuity without waiting for a full ancillary services market. Indonesia’s current solar-plus-BESS rollout across 21 projects in 7 provinces is designed to replace 741 diesel units, which gives the off-grid segment a strong policy and operating cost foundation. In the Philippines, hybrid microgrid programs are extending the same logic to remote service areas through combinations of solar, batteries, and backup generation. As a result, the ASEAN energy storage market is developing one stream around regulated grid assets and another around diesel offset economics in remote systems.

By Application: Grid-Scale Utilities Lead, Data Centres Emerge as High-Growth Outlier

Grid-scale utility storage accounted for 47.2% of the ASEAN energy storage market size in 2025 and remains the anchor application because utilities are still the largest and most reliable buyers. This lead is supported by large procurement programs such as the Philippines’ solar-plus-storage pipeline, Singapore’s utility battery expansion, and Malaysia’s utility-scale BESS rollout under MyBeST. MTerra Solar energised its first 250 MW of solar and 450 MWh of BESS in the Philippines in 2026, showing that integrated front-of-meter projects in the region are now reaching global scale. Singapore’s storage expansion also shows that batteries are becoming a core firming layer for renewable imports and grid frequency control rather than a peripheral balancing resource. Long-duration project pipelines in pumped hydro add another layer of depth to the utility application base across the ASEAN energy storage market.

Data centres and critical facilities are the fastest-growing application segment with a 10.3% CAGR through 2031. Their rise reflects the need for uninterrupted supply, better voltage quality, and cleaner backup strategies in markets where digital loads are expanding quickly. Commercial and industrial behind-the-meter demand is also rising because storage helps facilities manage reliability and align power use more closely with captive solar or contracted renewable supply. Residential behind-the-meter systems are growing steadily as lower system costs improve viability, while remote microgrids continue to expand in locations where storage substitutes diesel rather than merely shifting energy. Other uses, including transport charging and grid deferral, remain smaller today, but they give the ASEAN energy storage market a broader demand base for the next investment cycle.

Geography Analysis

Indonesia held 29.1% of the ASEAN energy storage market size in 2025 and remains the largest country market because it combines utility-scale need, island-grid demand, and a growing domestic battery chain. PLN is now executing 21 solar-plus-BESS projects across 7 provinces with 513 MWp of solar capacity and 9.03 GWh of storage to replace 741 diesel power units, which ties storage directly to system efficiency and fuel import reduction. An integrated USD 6 billion battery manufacturing project backed by PLN, Indonesia Battery Corporation, ANTAM, and HYD Investment Limited is also expected to support domestic cell production capacity and create a local supply base for future BESS deployment. Indonesia’s 17,000-island geography means storage often substitutes for transmission links that will not be built at the national scale. The country’s nickel base remains a major upstream advantage as well, with Indonesia accounting for 45% of global refined nickel production in 2024, even though foreign ownership in refining still shapes supply chain dependence.

Vietnam is the fastest-growing geography in the ASEAN energy storage market and is forecast to expand at 9.3% CAGR from 2026 to 2031. The policy stance has become more concrete because Vietnam’s amended Electricity Law now recognises storage, while a March 2026 directive pushed BESS deployment for grid regulation across capacity levels. EVN’s system plans include 305 MW of BESS by June 2026 and a broader 1,200 MW deployment program through 2030, which gives storage a defined place in system operation rather than only future planning. Fluence’s 35 GWh manufacturing facility in Bac Giang, opened in August 2025, also signals a shift from simple import dependence toward regional manufacturing participation. Vietnam’s continuing curtailment pressures and the construction of Bac Ai keep both battery and pumped hydro investment relevant at the same time.

The Philippines, Malaysia, Thailand, and Singapore broaden the ASEAN energy storage market through different policies and system needs rather than one common model. The Philippines remains one of the most advanced BESS markets in the region because auctions, ancillary services, and large integrated solar-plus-storage projects are already translating policy into operating assets. Thailand’s PDP 2024 includes 10,000 MW of BESS and 2,472 MW of new pumped hydro by 2037, while Singapore is building storage as the firming layer for its target of 6 GW of low-carbon power imports by 2035. The rest of ASEAN is still earlier in grid-scale deployment, but the ASEAN Power Grid and wider clean power trade will raise the need for storage at interconnection points over time.

Competitive Landscape

The ASEAN energy storage market is moderately fragmented in system integration and project execution, but cell supply and core technology sourcing are more concentrated. CATL, Sungrow, and BYD hold a strong position in major utility-scale procurement because they combine cell manufacturing, systems capability, and delivery scale in one package. That integrated model has made price and lead time harder for Western and Korean rivals to match across Indonesia, Vietnam, Thailand, and the Philippines. CATL’s corridor deals tied to the Indonesia-Singapore renewable chain in 2025 show how early anchor agreements can secure volume, support local manufacturing, and raise barriers for later entrants. Because on-grid procurement still dominates the ASEAN energy storage market, vendors with strong balance sheets and proven execution remain best placed in near-term tenders.

Fluence has made the largest Western manufacturing response so far through its 35 GWh Bac Giang facility in Vietnam, which gives it a deeper local footing even as Chinese competition intensifies. Wärtsilä, Siemens Energy, and Hitachi Energy are taking a different route by focusing on grid services integration, controls, and hybrid architecture rather than competing only on cell cost. LG Energy Solution and Samsung SDI also remain relevant where buyers value advanced chemistry performance and high-temperature cycling resilience. Safety and certification are gaining importance in public tenders, which means the competitive field is no longer defined only by the lowest upfront system cost. In this setting, the ASEAN energy storage market increasingly rewards suppliers that can pair hardware with stronger controls, service coverage, and bankable performance commitments.

White space still exists in long-duration storage, hydrogen-linked systems, and software-led asset optimization. Hydrogen-based projects for island systems remain early, but the pipeline already includes HDF Energy’s planned power projects in the Philippines and wider hydrogen-linked investment themes in Indonesia and Malaysia. A 2025 MDPI Computers study also showed that digital twin guided battery management can extend usable capacity by up to 5% and improve grid battery efficiency by 5 percentage points over a 10-year asset life, which gives software-enabled operators a practical margin advantage. Legacy references, such as NEC Energy Solutions, no longer reflect the active ASEAN field as clearly as current participants, such as Wärtsilä and Vena Energy, which better match the region’s present project pipeline.

ASEAN Energy Storage Industry Leaders

BYD Co Ltd

CATL

Fluence Energy Inc

Wärtsilä Oyj Abp

LG Energy Solution

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: PT PLN (Persero) confirmed execution of 21 solar-plus-BESS projects across 7 Indonesian provinces, with a combined solar capacity of 513 MWp and 9.03 GWh of storage, targeting COD from 2026 to 2028 as part of the government's programme to replace 741 diesel power units

- February 2026: PLN signed a framework agreement with Indonesia Battery Corporation (IBC), ANTAM, and HYD Investment Limited Consortium for a USD 6 billion integrated battery manufacturing project in Indonesia, targeting up to 20 GWh of annual production capacity.

- February 2026: PLN announced plans to construct the 1,000 MW Pacitan Pumped Storage project in East Java, which would become the second-largest pumped-hydro facility in Indonesia, supporting the East Java-Bali grid's renewable integration under RUPTL 2025–2034

- January 2026: Vietnam's Bac Ai Pumped Storage project (1,200 MW, USD 780 million in World Bank and AIIB financing) entered its main construction phase after exceeding early construction targets in 2025 for tunnelling, earthworks, and access infrastructure. First unit commissioning is targeted for December 2029.

ASEAN Energy Storage Market Report Scope

Energy storage is the capture of energy produced at one time and used at a later time to keep a balance between energy demand and energy production. With the world's renewable energy capacity reaching record levels, storage technologies are fundamental to smoothing out peaks and dips in energy demand without resorting to fossil fuels.

The ASEAN Energy Storage Market is segmented into storage technology, connectivity, application, and geography. By storage technology, the market is segmented into batteries (lithium-ion, solid-state lithium, sodium-ion, lead-acid, sodium-sulfur, and flow batteries including vanadium and zinc-bromine technologies), pumped-storage hydroelectricity (PSH), thermal energy storage (sensible heat storage such as molten salt and water, latent heat storage including phase-change materials, and thermochemical storage systems), compressed air energy storage, liquid air/cryogenic storage, hydrogen-based storage, and other technologies (flywheel energy storage, gravity-based storage, iron-air, and zinc-air systems). By connectivity, the market is segmented into on-grid and off-grid systems. By application, the market is segmented into grid-scale utility (front-of-meter), residential behind-the-meter, commercial and industrial behind-the-meter, data centers and critical facilities, remote and off-grid/microgrids, and others, including transportation and rail electrification, EV-charging infrastructure, and transmission and distribution deferral. The report also covers the market size and forecasts for the ASEAN energy storage market across 6 major countries in the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Storage Technology

| Batteries (Lithium-ion, Solid-State Li, Sodium-ion, Lead-acid, Sodium-Sulfur, and Flow Batteries (Vanadium, Zinc-Bromine)) |

| Pumped-Storage Hydroelectricity (PSH) |

| Thermal Energy Storage (Sensible Heat (Molten Salt, Water), Latent Heat (Phase-Change Materials), Thermochemical) |

| Compressed Air Energy Storage |

| Liquid Air/Cryogenic Storage |

| Hydrogen-Based Storage (Power-to-H2-to-Power) |

| Other Technologies (Flywheel Energy Storage, Gravity-Based Storage, Iron-Air, Zinc-Air) |

By Connectivity

| On-Grid |

| Off-Grid |

By Application

| Grid-Scale Utility (Front-of-Meter) |

| Residential Behind-the-Meter |

| Commercial and Industrial Behind-the-Meter |

| Data Centers and Critical Facilities |

| Remote and Off-Grid/Microgrids |

| Others (Transportation and Rail Electrification, EV-Charging Infrastructure, Transmission and Distribution Deferral) |

By Geography

| Indonesia |

| Vietnam |

| Philippines |

| Malaysia |

| Thailand |

| Singapore |

| Rest of ASEAN |

| By Storage Technology | Batteries (Lithium-ion, Solid-State Li, Sodium-ion, Lead-acid, Sodium-Sulfur, and Flow Batteries (Vanadium, Zinc-Bromine)) |

| Pumped-Storage Hydroelectricity (PSH) | |

| Thermal Energy Storage (Sensible Heat (Molten Salt, Water), Latent Heat (Phase-Change Materials), Thermochemical) | |

| Compressed Air Energy Storage | |

| Liquid Air/Cryogenic Storage | |

| Hydrogen-Based Storage (Power-to-H2-to-Power) | |

| Other Technologies (Flywheel Energy Storage, Gravity-Based Storage, Iron-Air, Zinc-Air) | |

| By Connectivity | On-Grid |

| Off-Grid | |

| By Application | Grid-Scale Utility (Front-of-Meter) |

| Residential Behind-the-Meter | |

| Commercial and Industrial Behind-the-Meter | |

| Data Centers and Critical Facilities | |

| Remote and Off-Grid/Microgrids | |

| Others (Transportation and Rail Electrification, EV-Charging Infrastructure, Transmission and Distribution Deferral) | |

| By Geography | Indonesia |

| Vietnam | |

| Philippines | |

| Malaysia | |

| Thailand | |

| Singapore | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the current outlook for ASEAN energy storage through 2031?

The ASEAN energy storage market is valued at USD 3.91 billion in 2026 and is forecast to reach USD 5.43 billion by 2031 at a 6.76% CAGR.

Which storage technology currently leads in Southeast Asia?

Pumped-storage hydroelectricity remains dominant with an 80.9% share in 2025 because many countries still rely on large utility-backed infrastructure.

Which application is expanding the fastest in the region?

Data centres and critical facilities are the fastest-growing application segment, with a projected 10.3% CAGR through 2031.

Which country leads the regional landscape today?

Indonesia leads with a 29.1% share in 2025, supported by utility procurement, island-grid demand, and domestic battery manufacturing plans.

Which country is expected to grow the fastest by 2031?

Vietnam is forecast to grow at 9.3% CAGR from 2026 to 2031 as storage moves from planning targets into mandated deployment.

Why are off-grid systems gaining momentum in ASEAN?

Off-grid storage is projected to grow at 9.1% CAGR because island systems can justify batteries through diesel displacement and reliability gains without waiting for mature power markets.

Page last updated on: