Arthroscopy Fluid Management Disposables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 6.76% CAGR |

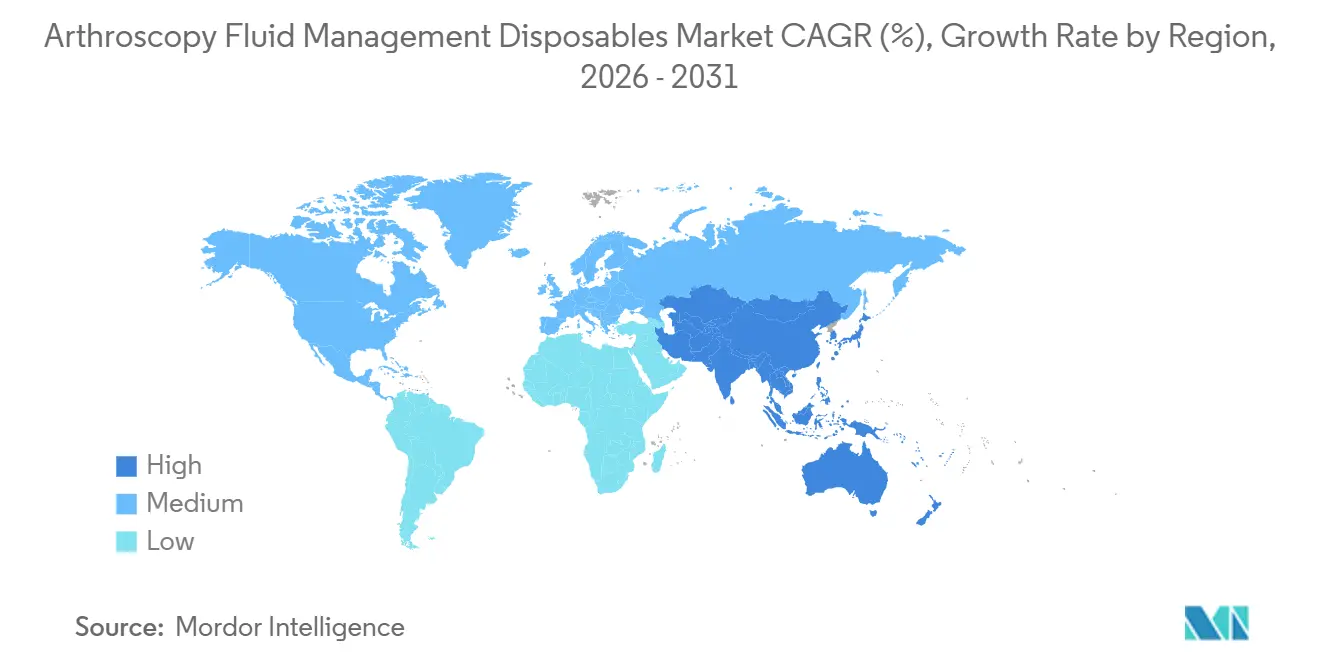

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

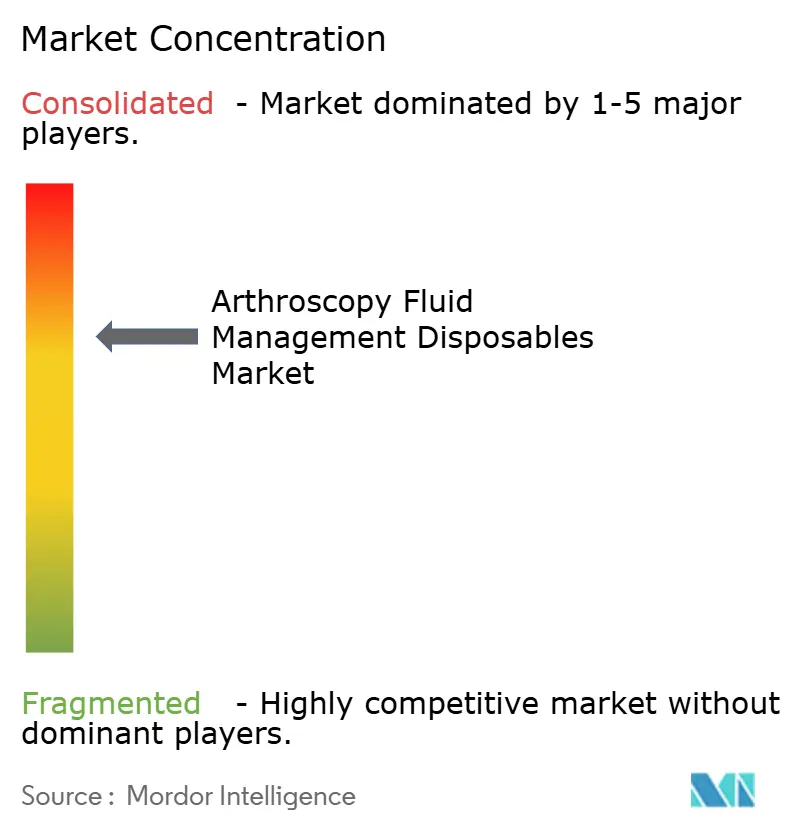

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Arthroscopy Fluid Management Disposables Market Analysis by Mordor Intelligence

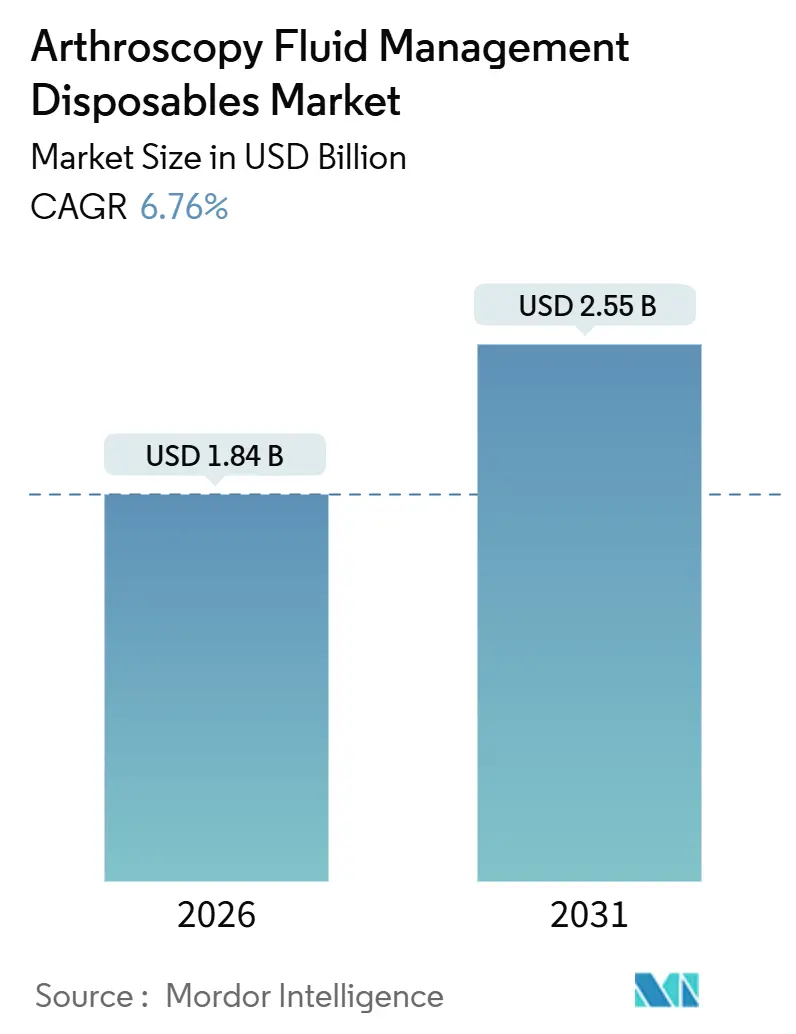

The Arthroscopy Fluid Management Disposables Market size is estimated at USD 1.84 billion in 2026, and is expected to reach USD 2.55 billion by 2031, at a CAGR of 6.76% during the forecast period (2026-2031).

The arthroscopy fluid management disposables market benefits from a clear preference for pump-based irrigation, which shortens cases and improves joint visualization. Pump management disposables already account for more than half of global revenue and are growing faster than gravity options as hospitals upgrade to pressure-controlled systems. Demand also tracks the migration of routine knee and shoulder procedures to ambulatory surgery centers, which perform a larger volume of day-case arthroscopies and favor standardized, single-use kits that reduce turnover time. Regionally, North America remains the largest contributor, thanks to high procedure volumes and supportive reimbursement, while Asia-Pacific is the fastest-growing region as China and India expand orthopedic capacity to manage aging populations and rising sports injuries. Persistent infection-control protocols that mandate sterile, disposable tubing further reinforce recurring sales of consumables.

Key Report Takeaways

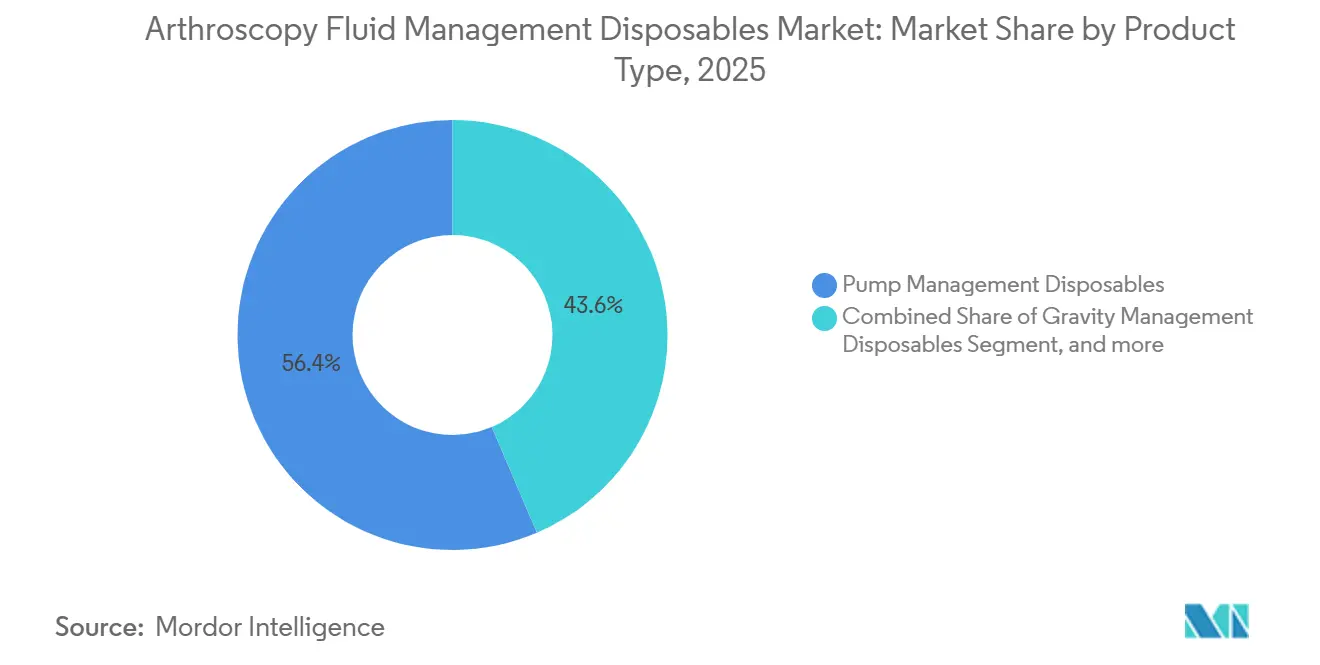

- By product type, pump management disposables captured 56.43% arthroscopy fluid management disposables market share in 2025, while the same segment is projected to expand at an 8.76% CAGR through 2031.

- By end user, hospitals led with 64.56% of the arthroscopy fluid management disposables market size in 2025, whereas ambulatory surgery centers are forecast to post the highest 9.76% CAGR to 2031.

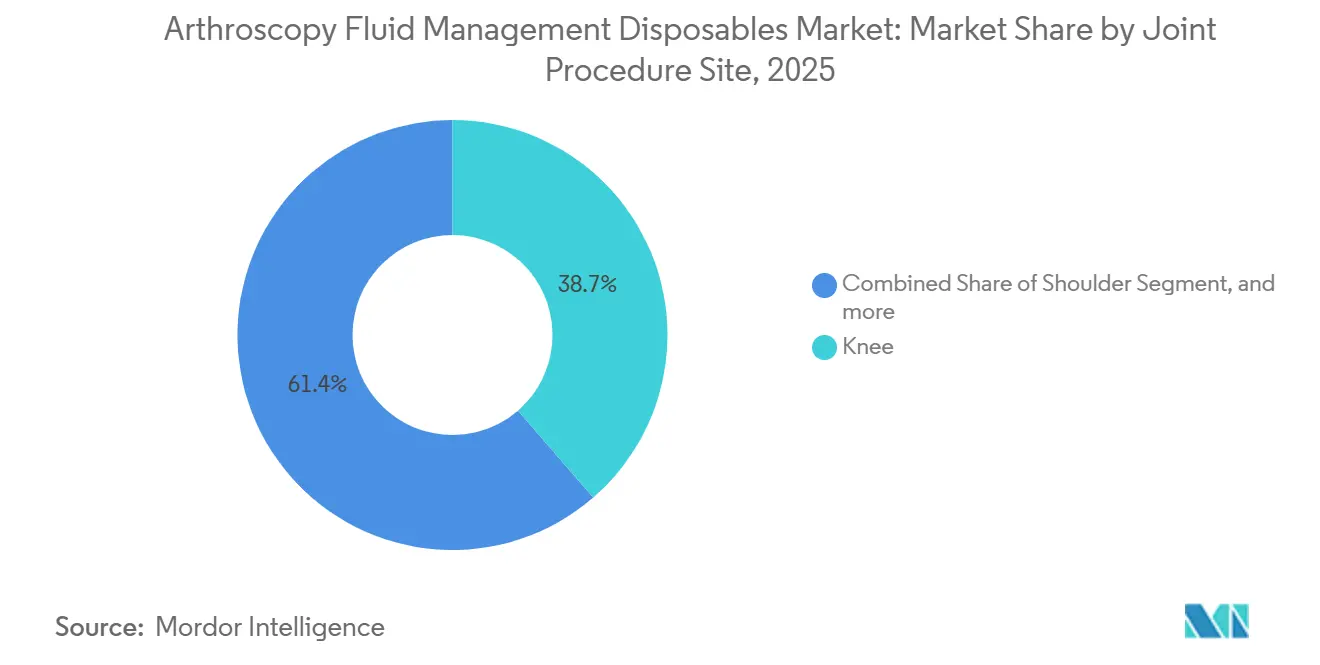

- By procedure site, knee arthroscopy dominated at 38.65% of 2025 volume, yet hip arthroscopy is advancing at an 8.43% CAGR through 2031.

- By sales channel, direct hospital procurement accounted for 44.56% of global revenue in 2025, but distributor and dealer channels are growing at 9.54% CAGR through 2031.

- By geography, North America held 42.12% arthroscopy fluid management disposables market share in 2025, while Asia-Pacific is expanding at a 7.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Arthroscopy Fluid Management Disposables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Burden Of Musculoskeletal Disorders | +1.8% | Global, with acute pressure in APAC and North America | Long term (≥ 4 years) |

| Shift Toward Day-Case Orthopedic Surgeries | +1.5% | North America & EU, spreading to urban APAC | Medium term (2-4 years) |

| Technological Integration Of Smart Fluid Systems | +1.3% | North America, Western Europe, urban China | Medium term (2-4 years) |

| Expansion Of Orthopedic Capacity In Emerging Economies | +1.0% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Hospital Preference For Infection-Control Single-Use Lines | +0.9% | Global, strongest in North America and EU | Short term (≤ 2 years) |

| Regulatory Push For Minimally Invasive Procedures | +0.3% | North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Burden of Musculoskeletal Disorders

Musculoskeletal conditions affected 1.71 billion people in 2025, and knee osteoarthritis alone accounted for 365 million cases, a 15% increase since 2020. Aging demographics and growing obesity are accelerating joint degeneration, driving more arthroscopic interventions that each consume multiple disposable tubing sets. Recreational sports participation among adults aged 50 and older climbed 22% in North America and Europe during the same period, adding sports-injury cases to the pipeline. China reported 4.2 million arthroscopies in 2025, up from 3.1 million in 2022, underscoring demand in populous emerging markets. Every procedure requires 3–15 liters of sterile irrigation, so rising volumes directly translate into higher consumable sales. Regulatory oversight from agencies such as the FDA protects quality, cementing the shift away from reusable components.

Shift Toward Day-Case Orthopedic Surgeries

Ambulatory surgery centers performed 68% of all U.S. knee arthroscopies in 2025, up from 52% in 2020, as payers push routine cases to lower-cost venues. The Centers for Medicare & Medicaid Services added shoulder and hip procedures to the ASC-approved list in 2024, lending further momentum. ASCs average 8.3 arthroscopy cases per room per day compared with 4.7 in hospitals, so they demand pre-packaged disposables that minimize setup time. The United Kingdom followed suit by piloting 14-day surgery hubs equipped with standardized pump systems that cut per-case costs by 18%[1]National Health Service England, “Orthopedic Hub Pilot Report,” nhs.uk. Manufacturers have answered with procedure-specific kits that align with high-throughput workflows and support the arthroscopy fluid management disposables market.

Technological Integration of Smart Fluid Systems

Arthrex introduced the Synergy HD3 pump in 2025, embedding real-time pressure control that holds intra-articular pressure between 40 and 60 mm Hg. Stryker’s FLOW Pump links irrigation to its 1688 AIM camera, letting surgeons toggle flow rates via foot control. Smith & Nephew added RFID-tagged tubing that automatically sets pump parameters, reducing setup errors by 23% during multi-surgeon trials. These innovations generate pressure data that hospitals feed into quality dashboards, creating switching costs that anchor the arthroscopy fluid management disposables market. Compliance with IEC 60601-1 and cybersecurity standards raises the bar for development but differentiates premium systems in tenders.

Expansion of Orthopedic Capacity in Emerging Economies

India earmarked USD 1.2 billion in 2025 to open 87 district orthopedic centers featuring dedicated arthroscopy suites[2]Ministry of Health and Family Welfare India, “District Hospital Expansion Plan,” mohfw.gov.in. China’s Healthy China 2030 plan subsidizes arthroscopy equipment for hospitals serving more than 500,000 people, expanding capacity beyond Tier 1 cities. The Gulf Cooperation Council intends to build 40 specialty orthopedic hospitals by 2028 under Saudi Vision 2030. These investments enlarge the install base for pumps and tubing, especially where policy mandates single-use lines. Local regulatory hurdles, however, extend launch timelines, so multinational suppliers with ISO 13485 systems are favored.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity In Budget-Constrained Healthcare Systems | -0.7% | South America, MEA, Southeast Asia, Eastern Europe | Medium term (2-4 years) |

| Environmental Scrutiny Of Single-Use Plastics | -0.4% | European Union, select North American jurisdictions | Long term (≥ 4 years) |

| Interoperability Gaps With Legacy Arthroscopy Towers | -0.3% | North America, European Union, Japan | Medium term (2-4 years) |

| Talent Shortage Of Skilled Arthroscopy Staff | -0.2% | Emerging APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Budget-Constrained Healthcare Systems

Public hospitals in Argentina, South Africa, and Indonesia limit disposable spending to USD 80–120 per case, one-third of North American levels, steering procurement toward gravity tubing sets. Thailand imposes a THB 3,500 (USD 100) ceiling per arthroscopy, hampering the adoption of premium smart pumps. Poland negotiated a 12% price reduction in its 2025 framework contract, squeezing margins and discouraging the adoption of advanced features. Rising polypropylene costs, up 18% between 2024 and 2025, further erode profitability on entry-level lines. Sites without stable electricity rely on gravity systems, slowing uptake in rural markets.

Environmental Scrutiny of Single-Use Plastics

The EU’s Single-Use Plastics Directive now covers medical devices, obligating manufacturers to provide recycling pathways by 2027. Johnson & Johnson launched a collection program in Germany and the Netherlands to recycle used tubing into non-medical pellets. Stryker invested USD 15 million to develop sugarcane-based polymer lines, but must secure regulatory clearance before commercial launch. A 2025 U.K. survey found that 64% of surgeons were concerned about the strength of biodegradable tubing, citing incidents of rupture at high pressure. Compliance with ISO 14001 and detailed lifecycle audits increases overhead, particularly for mid-tier vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pump Systems Dominate as Precision Demands Rise

Pump management disposables accounted for 56.43% of 2025 revenue, and their share of the arthroscopy fluid management disposables market is projected to grow at 8.76% through 2031. Hospitals value automated pressure control that maintains visibility and limits extravasation, trimming case time by up to seven minutes. Gravity sets still appeal to cost-constrained facilities but are ceding ground as reimbursement models reward efficiency.

Continued upgrades to smart pumps create pull-through demand for proprietary inflow and outflow tubing, cannulas, and waste bags. Manufacturers bundle these consumables into leasing packages that stabilize annual cash flows and lock customers in for 5-year terms. Innovations such as low-profile NanoScope cannulas reduce soft-tissue trauma, opening micro-joint indications and expanding the market for arthroscopy fluid management disposables.

By End User: Ambulatory Centers Capture Outpatient Migration

Hospitals generated 64.56% of 2025 demand, reflecting their dominance in complex reconstructions that require extended stays. Ambulatory surgery centers, however, are expanding at 9.76% CAGR as insurers reimburse more day-case arthroscopies, adding volume to the arthroscopy fluid management disposables market share in outpatient settings.

Physician-owned clinics invest in small arthroscopy suites to capture elective work. Many choose modular pump platforms that accept third-party tubing to avoid single-vendor lock-in, widening opportunity for disruptors. Sports-medicine clinics treating elite athletes also prefer premium disposable kits that permit same-day return-to-training protocols.

By Joint / Procedure Site: Hip Arthroscopy Gains as Indications Expand

Knee arthroscopy accounted for 38.65% of global procedures in 2025, the largest slice of the arthroscopy fluid management disposables market size[3]American Academy of Orthopaedic Surgeons, “2025 Procedure Utilization,” aaos.org. Hip arthroscopy, though smaller, posted the fastest 8.43% CAGR, enabled by improved traction tables and flexible cannulas that simplify access to the central compartment.

Shoulder volumes continue to rise on degenerative pathology tied to population aging in Western economies. Ankle, wrist, and elbow cases remain niche yet benefit from miniaturized pumps that safely irrigate small joints. The growing diversity of joint indications underpins steady demand across the tubing portfolio.

By Sales Channel: Distributors Gain as GPO Contracts Standardize Procurement

Direct hospital procurement retained 44.56% of 2025 sales, but group purchasing organizations are bundling capital and disposables into multi-year deals that shift price leverage away from manufacturers. Distributor and dealer channels are advancing at 9.54% CAGR as smaller hospitals and ASCs outsource logistics.

Regional distributors in India and Southeast Asia offer consignment models that reduce inventory costs, boosting uptake of mid-tier tubing lines. Digital marketplaces launched by firms like Medline shorten lead times to 48 hours, a key factor for high-volume ambulatory centers. The resulting channel mix spreads demand more evenly and supports global growth in the arthroscopy fluid management disposables market.

Geography Analysis

North America remained the largest contributor with 42.12% arthroscopy fluid management disposables market share in 2025. The United States alone performed 3.8 million arthroscopies, supported by Medicare and private insurers that reimburse smart pump disposables. Canada adopts gravity systems in rural hospitals to manage budgets, yet urban centers pilot value-based sourcing tied to complication reduction. Mexico’s private sector serves medical tourists seeking lower-cost sports-medicine surgery and relies on mid-tier kits that balance price and quality.

Europe is more fragmented but collectively large. Germany, the United Kingdom, France, Italy, and Spain account for two-thirds of procedures, funded by a mix of public and private sources. The United Kingdom’s NHS seeks a 15% cost cut through centralized procurement, favoring vendors that offer standardized pump-tubing bundles. Eastern European hospitals tap EU modernization funds to upgrade arthroscopy suites, yet often choose gravity disposables until pump prices fall.

Asia-Pacific is the growth engine, with a 7.54% CAGR through 2031. China logged 4.2 million arthroscopies in 2025, driving volume for local and imported tubing. India is building district orthopedic centers with government subsidies that specify single-use lines for infection control. Japan maintains a stable demand but restrains prices through national fee schedules, limiting premium penetration. Australia, South Korea, and Southeast Asian nations are expanding capacity through post-pandemic healthcare programs, though regulatory fragmentation is slowing multinational rollouts.

The Middle East and Africa expand from a low base, led by Saudi Vision 2030 projects that require ISO-certified disposables. South America grows steadily, but price pressure keeps gravity systems relevant. Across regions, local regulatory approvals and currency volatility influence launch timing and profitability.

Competitive Landscape

The top five suppliers—Arthrex, Stryker, Smith & Nephew, DePuy Synthes, and Zimmer Biomet—held roughly 62% of global revenue in 2025, giving the arthroscopy fluid management disposables market a moderately consolidated profile. Their integrated towers bundle pumps, cameras, and proprietary tubing, encouraging hospitals to sign multi-year agreements.

Mid-tier companies such as ConMed, Karl Storz, and Olympus compete on open architecture that interfaces with third-party pumps, attracting cost-sensitive ASCs. Startups pursue biodegradable polymers to satisfy environmental mandates, but regulatory testing slows commercialization.

Regionally, North America and Western Europe adopt data-enabled pumps that feed metrics to electronic health records. Emerging markets focus on cost, favoring gravity kits or hybrid pumps that accept low-cost tubing. Compliance with ISO 13485 and FDA post-market surveillance raises fixed costs, limiting new entrants and reinforcing incumbent advantage.

Arthroscopy Fluid Management Disposables Industry Leaders

Arthrex

Stryker

Smith & Nephew

DePuy Synthes (J&J)

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Arthrex, one of the global leader in minimally invasive surgical technology launched Synergy Power, a versatile and reliable battery-powered system designed for a wide variety of orthopedic applications.

- January 2024: Arthrex launched a new patient-focused resource, TheNanoExperience.com, highlighting the science and benefits of Nano arthroscopy, a modern, least-invasive orthopedic procedure that may allow for a quick return to activity and less pain.

Global Arthroscopy Fluid Management Disposables Market Report Scope

As per the scope of the report, arthroscopy fluid management disposables are single-use medical devices designed to control and monitor the flow of fluids during arthroscopic surgeries. They help maintain joint distension, improve visualization, and reduce the risk of infection. These disposables enhance surgical efficiency and patient safety by providing sterile, ready-to-use solutions.

The Arthroscopy Fluid Management Disposables Market is Segmented by Product Type (Pump Management Disposables, Gravity Management Disposables, Inflow/Outflow Tubing Sets, Cannulas & Valves, and Waste Collection & Floor-Suction Accessories), End User (Hospitals, Ambulatory Surgery Centers, Specialty Orthopedic Clinics, Sports-Medicine Clinics, and Other End Users), Joint/Procedure Site (Knee, Shoulder, Hip, Ankle, Wrist & Elbow, and Other Procedures), Sales Channel (Direct Hospital Procurement, Group Purchasing Organisations, and Distributors/Dealers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Pump Management Disposables |

| Gravity Management Disposables |

| Inflow/Outflow Tubing Sets |

| Cannulas & Valves |

| Waste Collection & Floor-Suction Accessories |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Orthopedic Clinics |

| Sports-Medicine Clinics |

| Other End Users |

| Knee |

| Shoulder |

| Hip |

| Ankle |

| Wrist & Elbow |

| Other Procedures |

| Direct Hospital Procurement |

| Group Purchasing Organisations (GPOs) |

| Distributors / Dealers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Pump Management Disposables | |

| Gravity Management Disposables | ||

| Inflow/Outflow Tubing Sets | ||

| Cannulas & Valves | ||

| Waste Collection & Floor-Suction Accessories | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Orthopedic Clinics | ||

| Sports-Medicine Clinics | ||

| Other End Users | ||

| By Joint / Procedure Site | Knee | |

| Shoulder | ||

| Hip | ||

| Ankle | ||

| Wrist & Elbow | ||

| Other Procedures | ||

| By Sales Channel | Direct Hospital Procurement | |

| Group Purchasing Organisations (GPOs) | ||

| Distributors / Dealers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is the arthroscopy fluid management disposables market in 2026?

In 2026, global sales reach USD 1.84 billion on the back of high procedure volumes in the United States, Europe, and China.

What value will the market reach by 2031?

Forecast models show revenue rising to USD 2.55 billion in 2031, supported by wider adoption of smart pump systems and growing outpatient surgery capacity.

How much revenue do pump-management disposables generate today?

Pump-based kits account for 56.43% of total 2025 sales, translating to roughly USD 1 billion and widening their lead as hospitals shift to pressure-controlled irrigation.

What share of global revenue comes from North America?

North America contributes 42.12% of worldwide sales in 2025, or just over USD 770 million, thanks to high procedure counts and favorable reimbursement.

How quickly is Asia-Pacific demand growing in dollar terms?

Regional revenue is advancing at a 7.54% CAGR; at that pace, Asia-Pacific climbs from about USD 420 million in 2026 to nearly USD 605 million by 2031.

Which end-user segment delivers the largest spending, and how big is it?

Hospitals remain the top buyers, representing 64.56% of 2025 global revenue, equal to nearly USD 1.1 billion, because they handle complex reconstructions that consume more disposables.

Page last updated on: