Argentina Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

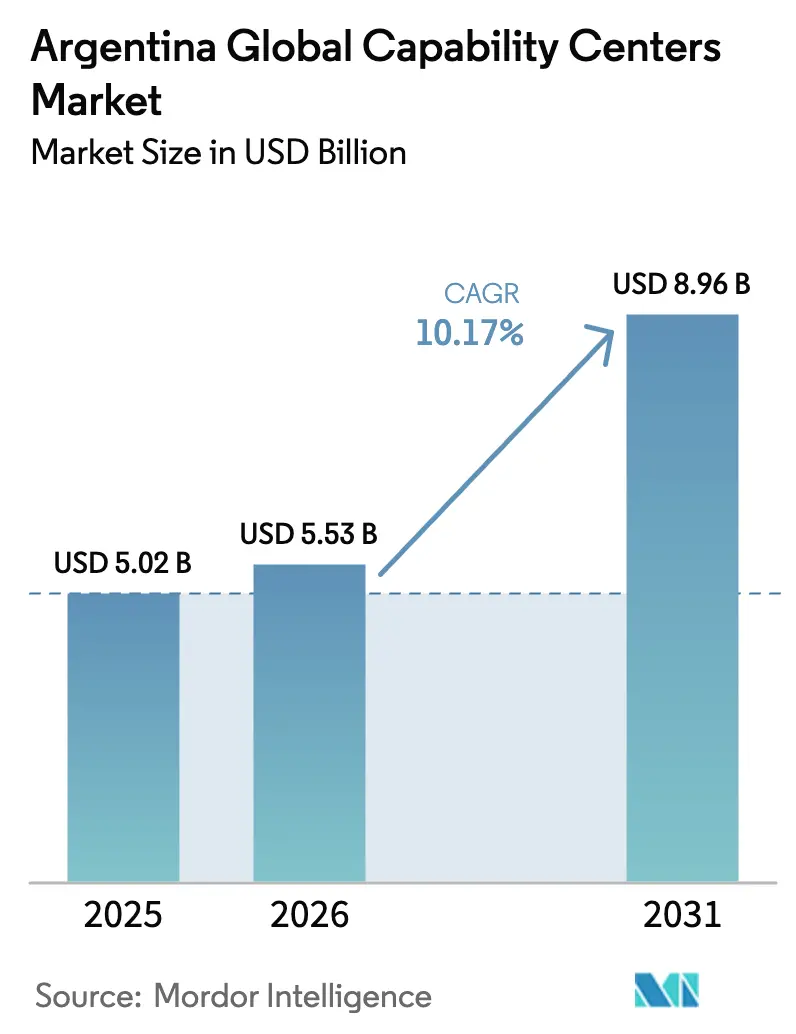

| Base Year Market Size (2025) | USD 5.02 Billion |

| Market Size (2026) | USD 5.53 Billion |

| Market Size (2031) | USD 8.96 Billion |

| Growth Rate (2026 - 2031) | 10.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Global Capability Centers Market Analysis by Mordor Intelligence

Argentina Global Capability Centers market size in 2026 is estimated at USD 5.53 billion, growing from 2025 value of USD 5.02 billion with 2031 projections showing USD 8.96 billion, growing at 10.17% CAGR over 2026-2031. This sustained expansion is anchored in an exceptional talent pipeline, favorable time-zone alignment with North America and Europe, and robust fiscal incentives that materially lower operating costs for new centers. Multinational corporations value the country’s English-proficient labor force, while near-real-time collaboration windows shorten project cycles and enable agile delivery models. New rules under the Large Investment Incentive Regime (RIGI) guarantee a 25% corporate tax rate and 30-year legal stability, materially improving the total cost of ownership for capability center investors.[1]Buenos Aires Herald, “Argentina launches RIGI with changes in the fine print,” buenosairesherald.com A record USD 17.1 billion in services exports in 2024, with knowledge-based activities contributing half the total, evidences Argentina’s delivery maturity. These strengths override lingering macro volatility and elevate the Argentina Global Capability Centers market as Latin America’s most compelling near-shore alternative for complex technology and business processes.

Key Report Takeaways

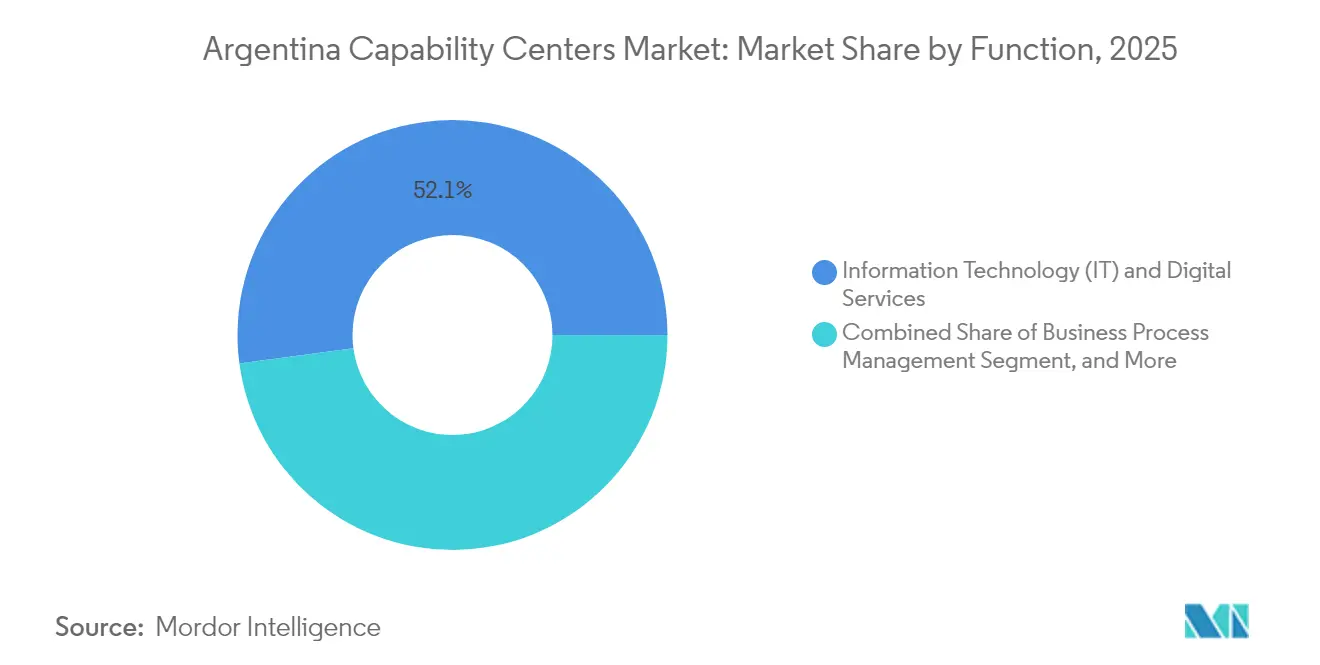

- By function, Information Technology and Digital Services held a 52.12% market share of the Argentina Global Capability Centers in 2025, while the segment is expected to advance at a 12.08% CAGR through 2031.

- By engagement model, captive centers captured 56.74% of the Argentina Global Capability Centers market in 2025, whereas Hybrid Build-Operate-Transfer arrangements are the fastest-growing model, with a 11.62% CAGR.

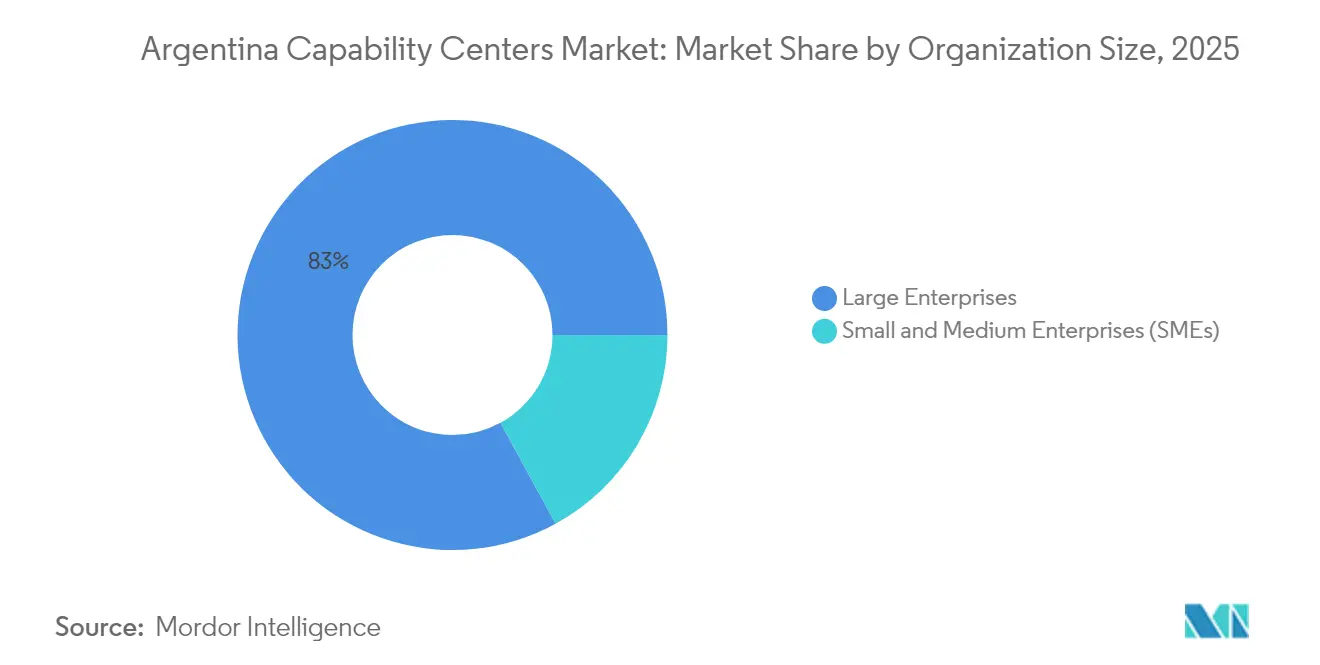

- By organization size, large enterprises accounted for 82.96% of 2025 revenue; small and medium enterprises are set to grow at a 12.14% CAGR as cloud delivery lowers entry barriers.

- By industry vertical, Telecom and IT led with 32.85% revenue in 2025; the Banking, Financial Services, and Insurance sector is projected to expand at a 11.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pool of STEM graduates and English proficiency | +2.8% | Buenos Aires, Córdoba, Rosario | Medium term (2-4 years) |

| Nearshore advantage for US and European time zones | +2.1% | Nationwide, strongest in the Buenos Aires metro | Short term (≤ 2 years) |

| Increasing government tax credits for software and knowledge exports | +1.9% | Nationwide, amplified in tech parks | Medium term (2-4 years) |

| Accelerated digital transformation initiatives post-pandemic | +1.7% | Nationwide | Short term (≤ 2 years) |

| Rising adoption of agile engineering centers by global firms | +1.4% | Buenos Aires, Córdoba, Mendoza | Medium term (2-4 years) |

| Emergence of specialized fintech and crypto GCCs | +1.1% | Buenos Aires financial district | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Pool of STEM Graduates and English Proficiency

Argentina supports 115,000-135,000 active technology professionals, supplemented by more than 20,000 new STEM graduates each year.[2]International Trade Centre, “Driving economic growth in Argentina through digital transformation,” intracen.org Combined with the region’s top English proficiency ranking, this talent depth enables centers to manage client-facing work without language barriers. The software sector alone employs 156,800 specialists across 5,500 companies, with 43.8% of external revenue exported to the United States and an additional 25.7% to Mexico and Chile. Leading universities in Buenos Aires and Córdoba channel steady cohorts into artificial intelligence, cybersecurity, and blockchain programs, ensuring a robust bench for next-generation GCC roles. This unique mix of linguistic and technical skills positions Argentina Global Capability Centers' market operations to tackle complex analytics, product development, and high-touch customer functions at scale.

Nearshore Advantage for US and European Time Zones

Operating in GMT-3 grants three to four concurrent business hours with the US East Coast and early-morning overlap with Europe, enabling real-time sprint reviews, troubleshooting, and regulatory checks. JPMorgan Chase plans to expand its staff in Buenos Aires to 5,000 by 2030, primarily to capitalize on opportunities in capital markets and risk management. Unlike Asian offshore locations that must rely on night shifts, Argentina-based teams align naturally with clients, reducing fatigue, improving staff retention, and accelerating cycle times. This alignment boosts the adoption of agile frameworks and shortens feedback loops, driving higher productivity across the Argentina Global Capability Centers market.

Increasing Government Tax Credits for Software and Knowledge Exports

The Knowledge Economy Law applies reduced corporate income tax and payroll tax relief, as well as export refunds, to qualifying services. The RIGI statute extends a 25% corporate rate and 30-year legal stability to investments exceeding USD 200 million. Knowledge-based service exports reached USD 8.5 billion in 2023, the highest level since 2006, indicating the strong effectiveness of incentives.[3]Argentina Ministry of Foreign Affairs and Worship – Centre for International Economy, “Argentina's Trade in Services in 2023,” cancilleria.gob.ar Fiscal certainty and relaxed foreign-exchange rules lower costs and de-risk large-scale commitments, making the Argentina Global Capability Centers market attractive to both Fortune 500 captives and specialist service providers.

Accelerated Digital Transformation Initiatives Post-Pandemic

A 2024 survey of 614 domestic firms found that users of digital freight and payment solutions reported twice the improvement in delivery timeliness and significantly stronger cash-flow visibility compared to non-users. Local demand for cloud migration, cybersecurity, and data analytics is rising, augmenting export-led revenue streams. Public-sector modernization programs further expand addressable workloads for GCCs specializing in e-government, identity management, and compliance platforms. This domestic momentum complements foreign contracts and raises the utilization rates of existing centers across the Argentina Global Capability Centers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic volatility and inflation impacts on Opex planning | -1.8% | National, with Buenos Aires, cost pressures are most acute | Short term (≤ 2 years) |

| Talent churn due to the high emigration of senior engineers | -1.2% | Buenos Aires, Córdoba, and technology hubs with international connectivity | Medium term (2-4 years) |

| Foreign-exchange controls are complicating profit repatriation | -0.8% | Nationwide, particularly impacting multinational GCC operators | Short term (≤ 2 years) |

| Premium office space cost pressure in Buenos Aires | -0.5% | Buenos Aires' central business districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Volatility and Inflation Impacts on Opex Planning

Allianz Trade expects 5.5% GDP growth in 2025 with inflation moderating to 18-23%, an improvement but still above peer averages. Fluctuating input costs complicate multi-year budget cycles for rent, utilities, and compensation. Although the Central Bank logged USD 6.57 billion in foreign direct investment during Q1 2024, foreign-exchange controls remain partially in place, delaying dividend repatriation.[4]Central Bank of the Argentine Republic, “Report on Foreign Direct Investment – First Quarter of 2024,” bcra.gov.ar Operators mitigate exposure with hedging programs and multi-currency pricing, yet residual policy risk persists as a drag on the Argentina Global Capability Centers market.

Talent Churn Due to High Emigration of Senior Engineers

Competitive overseas pay continues to draw seasoned architects and engineering leads to North America and Europe. New digital-nomad visas, MERCOSUR mobility rules, and investment citizenship pathways aim to offset outflows, but ramp-up times for replacement talent raise delivery risk. Global Capability Centers now embed accelerated career tracks, equity participation, and university alliances to deepen the local senior-level pool. Absent sustained retention success, wage inflation could intensify, tempering the current cost advantage enjoyed by the Argentina Global Capability Centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: Digital Services Extend Lead

Argentina Global Capability Centers' market share for Information Technology and Digital Services stood at 52.12% in 2025, confirming the segment as the principal revenue engine. Demand centers on software engineering, cloud operations, and cybersecurity assignments that align with the country’s deep STEM talent pool. Engineering and R&D follow, earning favor from automotive and industrial clients that co-locate design and simulation activities with local production footprints. Business Process Management retains a sizable niche in finance, human resources, and omnichannel customer work, while Knowledge-Process Outsourcing captures premium fees in legal analytics and compliance research.

The Argentina Global Capability Centers market size attributed to Digital Services is projected to rise at a 12.08% CAGR through 2031 as enterprises modernize legacy environments and pursue artificial-intelligence acceleration. Engineering and R&D benefit from incremental spending on digital twins and autonomous-systems testing, maintaining its share stability. Business Process Management edges toward higher-value tasks by weaving analytics into routine finance and HR workflows. Together, these shifts elevate the functional mix toward complex, technology-driven mandates that monetize Argentina’s twin advantages of language fluency and advanced engineering skills.

By Engagement Model: Captive Control with Hybrid Momentum

Captive centers commanded a 56.74% market share of the Argentina Global Capability Centers in 2025, reflecting investor preference for direct oversight of intellectual property and regulatory compliance. Multinationals anchor teams that span application development, data science, and 24-hour support, counting on Argentina’s legal protections and RIGI-backed tax certainty. Build-Operate-Transfer structures attract firms that seek local expertise during the ramp-up phase yet intend to assume full control after operations stabilize. Traditional outsourcing agreements remain present, but their share is declining as clients seek tighter governance.

Hybrid Build-Operate-Transfer arrangements are expanding at an 11.62% CAGR, outpacing other models because they couple speed-to-launch with the option to internalize mature operations later. The Argentina Global Capability Centers market size tied to Hybrid contracts is forecast to surpass USD 1.74 billion by 2031 without eroding the captive base. Service providers supply turnkey facilities, compliance stewardship, and seasoned managers, enabling investors to navigate hiring, real estate, and statutory hurdles. Once performance metrics reach target thresholds, ownership can be transferred, providing companies with long-term cost and control benefits.

By Organization Size: Enterprise Dominance, SME Upswing

Large Enterprises accounted for 82.96% of 2025 revenue, mirroring the capital intensity required for multi-thousand-seat hubs. Their global footprint favors Argentina for roles that require continuous overlap between North America and Europe, such as regulatory reporting, real-time analytics, and full-stack product development. Deep pockets allow these firms to finance Grade-A workspace, resilient connectivity, and comprehensive staff development programs. They also leverage RIGI incentives to secure tax and legal stability for commitments exceeding USD 200 million.

Small and Medium-Sized Enterprises, while smaller in absolute terms, are expanding at a 12.14% CAGR as consumption-based cloud platforms reduce entry barriers. These companies tap niche teams of 50-150 specialists for DevOps, UX design, or multilingual customer success, often integrating with venture-funded growth strategies. The resulting Argentina Global Capability Centers market share for SMEs remains modest yet growing, helped by local fintech, SaaS, and e-commerce innovators that require regional language coverage and agile product iterations. Universities and incubators funnel flexible talent into these high-velocity deployments, reinforcing momentum.

By Industry Vertical: Telecom Leadership, BFSI Acceleration

Telecom and IT led with 32.85% of 2025 turnover, grounded in Argentina’s robust fiber networks, 19 operational data centers, and decades-long carrier presence. Centers manage network operations, 5G rollouts, and multi-cloud orchestration for domestic and regional operators. Software-defined networking projects and edge-compute pilots widen the scope of work, sustaining volume even as automation trims basic tasks. Cross-border engagements with Brazilian and Chilean carriers further diversify billings.

The banking, Financial Services, and Insurance Sector is advancing at an 11.05% CAGR, riding on Buenos Aires’ 432-firm fintech ecosystem and strong cryptocurrency adoption. Global banks scale analytics, fraud detection, and regulatory technology solutions that rely on real-time data from the U.S. and Europe. Manufacturing and industrial programs benefit from engineering depth, while healthcare and life sciences rely on Argentina’s clinical research credentials for pharmacovigilance and data management. Collectively, these vertical threads broaden the Argentina Global Capability Centers market size, reduce cyclicality, and sharpen specialization.

Geography Analysis

Buenos Aires concentrates a significant share of the national workforce, thanks to its dense university clusters, reliable power grids, and direct flights to major business hubs. Grade-A office vacancies near 17% provide room for expansion at rents below those of comparable Latin American capitals. Cable landing stations and carrier-neutral data centers offer low-latency links, which are essential for capital markets, streaming, and cloud-based workloads. The metropolitan government offers additional incentives through tech-park tax rebates and streamlined permitting processes.

Córdoba hosts a prominent share of the capability centers, leveraging its automotive heritage to inform mechanical and software engineering disciplines. Cost structures run 15-20% lower than in Buenos Aires, and public-private partnerships fund STEM curricula at Universidad Nacional de Córdoba. Rosario, Mendoza, and Mar del Plata form an emerging tier-two corridor where operational costs can undercut the capital by up to 25% while still offering qualified graduates. These cities attract mid-sized GCCs that handle QA, customer experience, and localized product adaptation for Spanish-speaking markets.

Argentina’s GMT-3 slot aligns with U.S. East Coast mornings and European afternoons, enabling follow-the-sun delivery without graveyard shifts. Mercosur membership provides tariff relief on professional services sold to Brazil, Paraguay, and Uruguay. New bilateral accords with the United Arab Emirates and Qatar, under RIGI, pave the way for Middle Eastern capital to invest in Patagonia’s USD 25 billion Stargate data-center project, which expands backbone capacity for southern provinces. Digital nomad visas and investment citizenship pathways expand the national talent pool.

Competitive Landscape

The top five providers, Accenture, Globant, IBM, Tata Consultancy Services, and Cognizant, collectively command a significant share of the sector's revenue, resulting in a moderate level of concentration in the Argentina Global Capability Centers market. Each firm maintains multi-domain portfolios covering cloud, cybersecurity, and advanced analytics. Globant epitomizes local-to-global scaling, with roughly 20% of its 30,000 staff based in Argentina feeding global delivery for Fortune 500 customers. IBM leverages its Buenos Aires Client Innovation Center for hybrid-cloud integration and mainframe modernization across Spanish-speaking markets.

Strategic differentiation now hinges on high-growth niches. Accenture and TCS invest in artificial intelligence labs, while Cognizant targets healthcare tech accelerators. Local specialists capitalize on white space by focusing on blockchain, crypto-exchange compliance, and digital twin modeling for the mining and agritech industries. Mergers and minority investments are common. For example, Globant acquired two regional design studios in 2024 to strengthen its end-user experience lines, and IBM inked joint AI research agreements with the Universidad de Buenos Aires.

Legal and fiscal dynamics also shape competition. RIGI’s 30-year stability pledge draws new entrants in semiconductor design and biotech process outsourcing. Domestic boutiques secure advantage through Spanish fluency, near-court proximity, and agile pods capable of sprint starts in under three weeks. The interplay of global scale and niche depth fosters a balanced market, encourages specialization, and pushes continuous upskilling across the workforce.

Argentina Global Capability Centers Industry Leaders

Accenture Argentina SRL

Tata Consultancy Services Argentina SA

IBM Argentina SA

Cognizant Technology Solutions Argentina SRL

Capgemini Argentina SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Decree 524/2025 took full effect, providing qualifying technology investors with a streamlined route to Argentine citizenship and strengthening the country’s appeal to global talent and capital.

- July 2025: The Central Bank recorded USD 6.57 billion in foreign direct investment during Q1 2025, with technology and services leading inflows from United States, Spanish, and Dutch companies, underscoring sustained confidence in the reformed investment climate.

- May 2025: Argentina’s Ministry of Foreign Affairs confirmed that 2024 services exports reached USD 17.1 billion, up 6.3% year-over-year, with business services at 34.6% and telecommunications or IT at 16.4%, setting a solid base for 2025 growth targets.

- April 2025: The final RIGI guidelines became operational, locking in a 25% corporate tax and 30-year legal stability for technology projects exceeding USD 200 million.

Argentina Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build)/ In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

How large is the Argentina Global Capability Centers market in 2026?

Argentina Global Capability Centers market size is estimated at USD 5.53 billion in 2026 with a 10.17% CAGR outlook to 2031.

Which segment holds the largest share of Argentine capability centers?

Information Technology and Digital Services leads with 52.12% revenue share in 2025.

Why do firms favor Argentina over other Latin American locations for GCCs?

The country combines top-ranked English proficiency, a 20,000-person annual STEM pipeline, and GMT-3 overlap with US and European business hours.

What incentives does the Argentine government provide to GCC investors?

The Knowledge Economy Law offers tax credits, while the RIGI regime grants a 25% corporate rate and 30-year legal stability for projects above USD 200 million.

Which industry vertical is expanding fastest within Argentine capability centers?

The Banking, Financial Services, and Insurance sector is projected to grow at a 11.05% CAGR through 2031.

How are small and medium enterprises using GCC services in Argentina?

Cloud-native delivery and consumption-based pricing enable SMEs to tap into specialized teams, driving the segment to a 12.14% CAGR.

Page last updated on: