Argentina Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

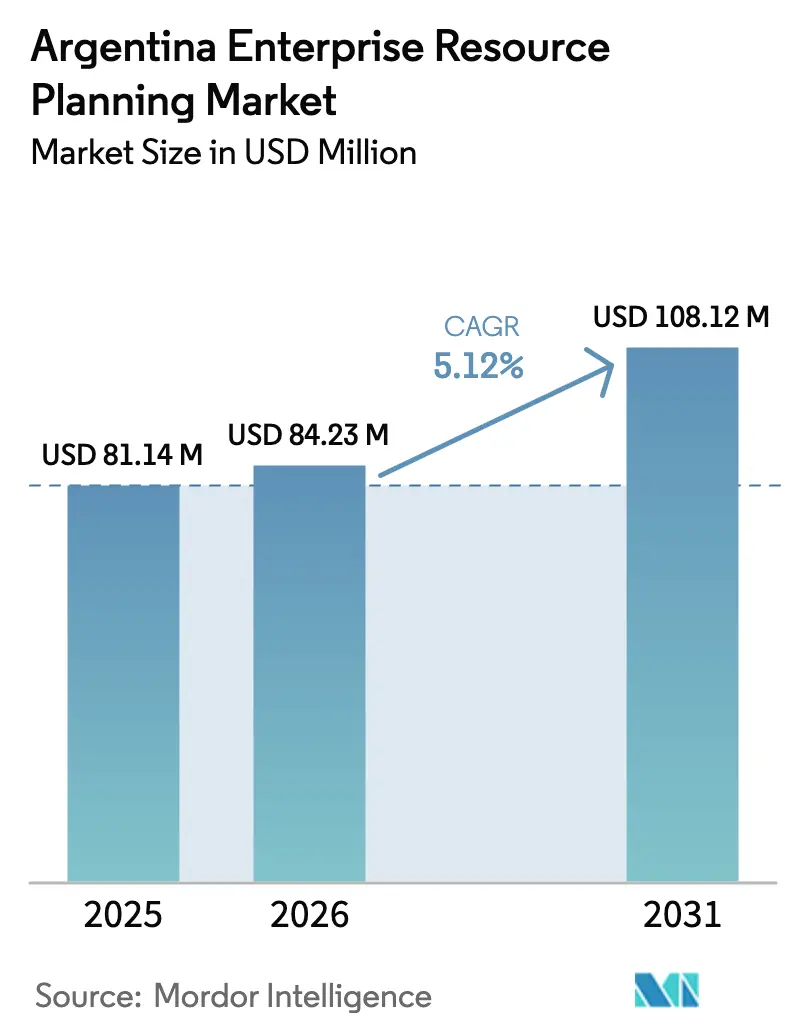

| Base Year Market Size (2025) | USD 81.14 Million |

| Market Size (2026) | USD 84.23 Million |

| Market Size (2031) | USD 108.12 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

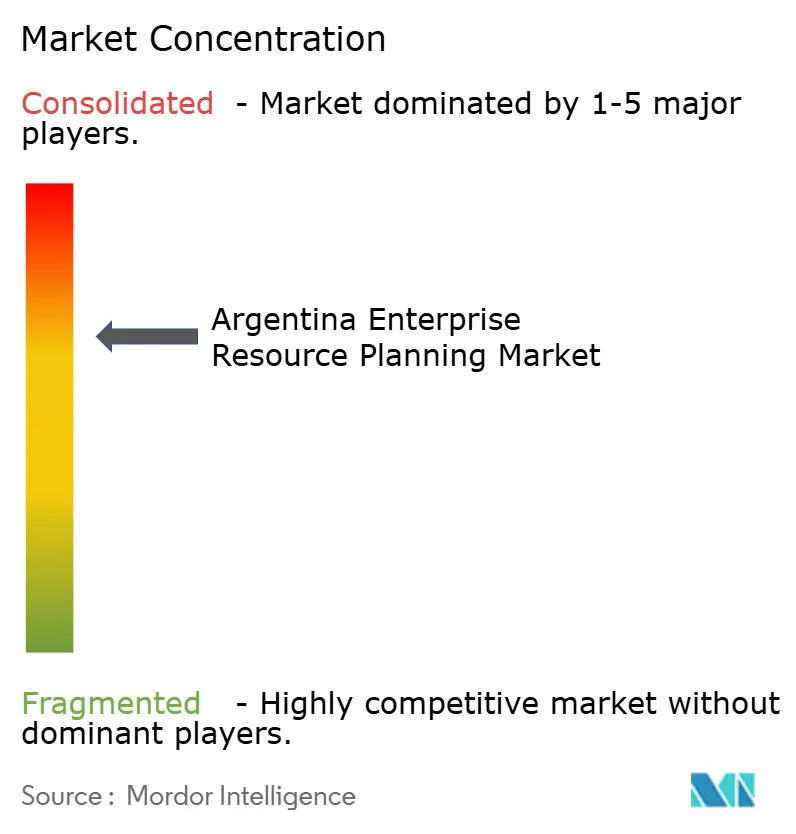

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Argentina enterprise resource planning market size is expected to grow from USD 81.14 million in 2025 to USD 84.23 million in 2026 and is forecast to reach USD 108.12 million by 2031 at a 5.12% CAGR over 2026-2031. Commercial buyers are prioritizing solutions that convert lump-sum capital outlays into predictable operating expenses, a shift that favors cloud subscriptions denominated in pesos. Stricter e-invoicing mandates, a gradual slowdown in monthly inflation, and nearshoring investments under the RIGI incentive framework are converging to sustain steady but not spectacular spending on integrated finance, supply-chain, and human-capital modules. Large enterprises continue to anchor demand because they can hedge currency risk through peso-linked service contracts, whereas small and medium enterprises are still evaluating subsidized adoption programs that began disbursing funds in 2024. Competitive positioning now hinges on localization depth, in-country data-center presence, and Spanish-language AI assistants that lower training costs for non-technical staff.

Key Report Takeaways

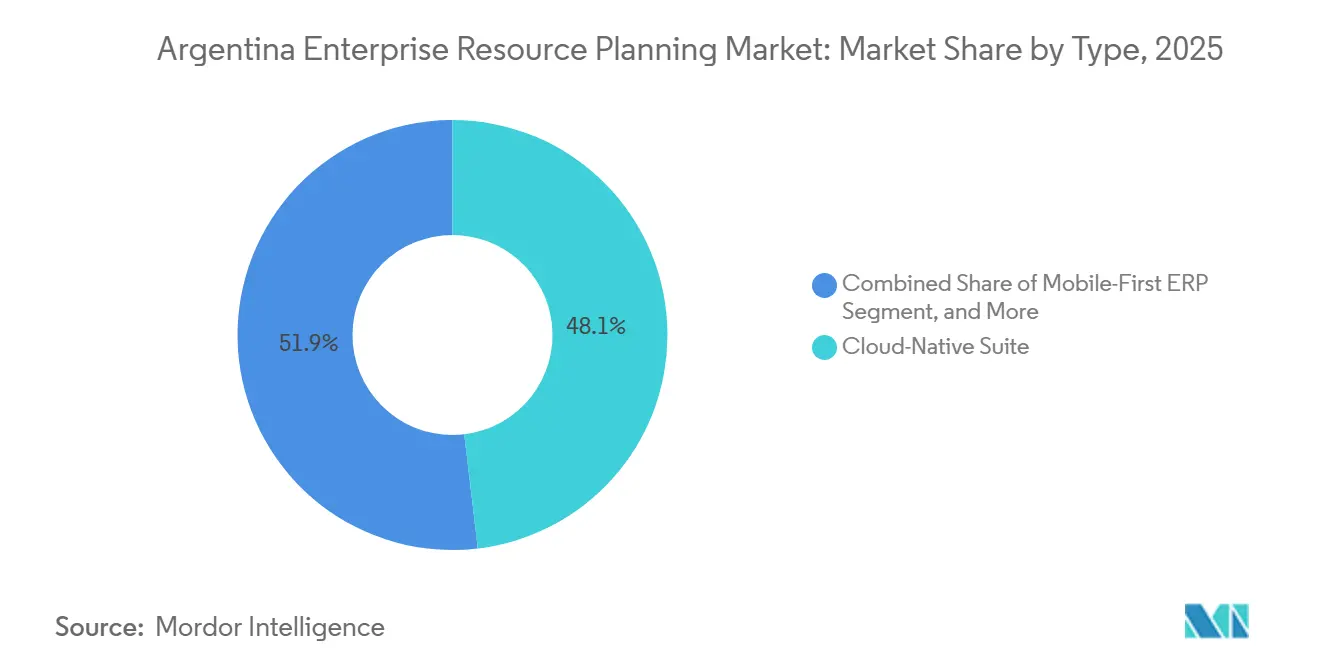

- Cloud-native suites accounted for 48.12% of Argentina's enterprise resource planning market share in 2025, while the mobile-first ERP segment is anticipated to grow at a CAGR of 5.96% during 2026-2031.

- Finance and accounting modules represented 33.97% of the Argentine enterprise resource planning market by business function in 2025, with the human capital management segment expected to achieve the highest CAGR of 6.14% through 2031.

- Cloud deployments contributed 65.17% of revenue in 2025 by deployment model and is projected to grow at a CAGR of 5.57% through 2031.

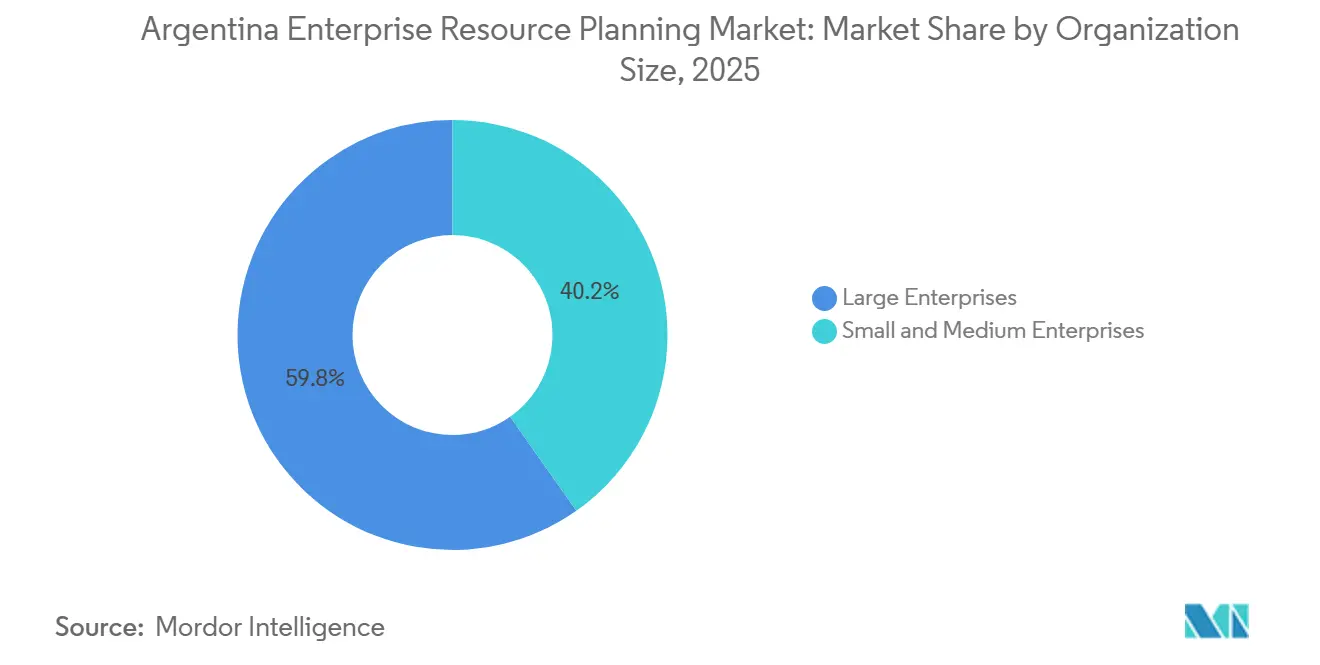

- Large enterprises held 59.77% of the market share in 2025 by organization size, while small and medium enterprises is projected to experience the fastest growth at a CAGR of 5.78% over the forecast period.

- The manufacturing sector accounted for 29.84% of revenue in 2025, the largest share by industry vertical, while the retail and e-commerce segment is expected to grow at a CAGR of 6.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for Real-Time Financial Visibility Due to Inflation Volatility | +1.8% | National, highest urgency in Buenos Aires, Córdoba, Rosario | Short term (≤ 2 years) |

| Integration of ERP with E-Invoicing and Tax Compliance Mandates | +1.5% | National, mandatory for financial institutions, insurance, credit cards from July 2026 | Medium term (2-4 years) |

| Rising Adoption of Cloud Computing Among Argentine Enterprises | +1.2% | National, concentrated in metro areas with reliable connectivity | Medium term (2-4 years) |

| Emergence of Spanish-Language AI Co-Pilots Accelerating User Adoption | +0.9% | National, early uptake in large firms and tech-forward SMEs | Long term (≥ 4 years) |

| Growing Nearshoring of Manufacturing to Argentina Boosting ERP Demand | +0.7% | RIGI-eligible provinces | Long term (≥ 4 years) |

| Government Digital Transformation Incentives for SMEs | +0.5% | National, focused on underserved provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Need for Real-Time Financial Visibility Due to Inflation Volatility

Argentine treasurers must update cash-position dashboards daily because peso depreciation erodes working capital within weeks, not quarters. Enterprises are therefore automating bank-feed ingestion, continuous reconciliation, and multi-currency revaluation so that finance managers can reprice products, accelerate collections, and lock hedges within 48 hours. A state-controlled energy major trimmed year-end closing time by half after migrating its SAP estate to a hyperscale cloud platform, proving that real-time processes yield measurable efficiency gains.[1]SAP Help Portal – Argentina Localization for SAP S/4HANA,” SAP, help.sap.com Government loans aimed at micro and small enterprises require beneficiaries to adopt software that interfaces with AFIP’s electronic invoicing web services, further linking liquidity oversight to ERP adoption. The result is a structural preference for cloud modules that push transactional data into analytic workspaces with minute-level latency, a capability largely absent from legacy on-premise systems.

Integration of ERP with E-Invoicing and Tax Compliance Mandates

ARCA Resolution 5824/26 obliges banks, insurers, and card processors to issue XML invoices containing CAE authorization codes and to archive them digitally for ten years. Spreadsheet workflows cannot meet those requirements, so even cautious institutions are layering finance modules that automatically fetch CAE numbers from AFIP during posting. Tier-one vendors responded with Argentine localizations that embed provincial gross-receipts rules, QR codes, and monthly tax-perception updates. Early adopters report 30% shorter invoice-to-cash cycles because digital documents pass auditor checks without manual edits. Compliance depth has thus become a primary scoring criterion in RFPs, overtaking pure functional breadth for the first time.

Rising Adoption of Cloud Computing Among Argentine Enterprises

Cloud spending converts lump-sum license fees into operating leases, making them easier to budget for in volatile currencies. Data-center expansions by regional colocation providers and fiber-backbone rollouts have lowered latency for SaaS applications by double-digit milliseconds, enabling warehouse and field teams to transact on mobile devices without VPN bottlenecks. To meet residency requirements for financial data, hyperscalers are planning in-country regions or partnering with local hosts that replicate ledgers to Argentine soil. The Universal Service Fund is financing last-mile fiber to 258 underserved localities, which will gradually unlock fresh demand from provincial distributors that today rely on intermittently synced on-premise servers

Emergence of Spanish-Language AI Co-Pilots Accelerating User Adoption

Natural-language assistants embedded in ERP screens eliminate the need for arcane transaction codes. Finance clerks now ask in Spanish, Which bill needs to be paid this week and receive live S/4HANA data inside Microsoft Teams. SMEs lacking dedicated IT staff value these features because they shorten onboarding by weeks and cut report customization fees. Outcome-based pricing models charge customers only when an AI-generated purchase order converts to a sale, aligning vendor incentives with user productivity. Adoption is fastest in large enterprises but is forecast to diffuse to mid-market firms as pricing tiers broaden.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Currency Instability Deterring Long-Term IT Investment | -1.2% | National, acute on dollar-indexed SaaS contracts | Short term (≤ 2 years) |

| Skills Gap In Advanced ERP Customization And Integration | -0.8% | National, most severe outside major metros | Medium term (2-4 years) |

| Data Sovereignty Concerns Limiting Public Cloud ERP Uptake | -0.5% | National, mandatory in finance sector | Medium term (2-4 years) |

| Fragmented Internet Connectivity Outside Major Urban Centers | -0.4% | Patagonia, Northwest, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Currency Instability Deterring Long-Term IT Investment

According to Buenos Aires Times, a 31% peso slide against the dollar in 2025 raised the effective cost of multi-year, dollar-denominated SaaS contracts, prompting CFOs to request peso pricing with quarterly indexation. Vendors have experimented with hybrid billing that pegs licenses to U.S. currency, but prices consulting services in pesos, yet smaller firms still hesitate because their revenue streams are local. Some large industrials hedge by splitting workloads between a São Paulo cloud region and an Argentine colocation site paid in pesos, but SMEs often lack the treasury tools needed to replicate that strategy.

Skills Gap in Advanced ERP Customization and Integration

Argentina’s universities graduate generalist developers, yet ABAP, Power Platform, and API specialists remain scarce, especially outside Buenos Aires, Córdoba, and Rosario. Mid-level consultants are wooed by offshore gigs that pay in hard currency, creating churn that drives up daily rates for domestic implementations.[2]SAP Help Portal – Argentina Localization for SAP S/4HANA,” SAP, help.sap.com Local integrators therefore invest heavily in bootcamps to build captive pipelines, but those programs will take years to close the supply-demand gap. Meanwhile, projects stall or scale back scope, trimming overall license growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud-Native Suites Dominate Amid Peso Volatility

Cloud-native suites captured 48.12% of the Argentine enterprise resource planning market share in 2025, a lead rooted in their subscription billing that shields buyers from abrupt capital outlays. The Argentina enterprise resource planning, as mobile interfaces, elastic compute, and automatic tax table updates become indispensable for finance chiefs battling weekly currency swings. Two-tier architectures appeal to manufacturers with patchy bandwidth because lightweight edge nodes can run production or retail modules offline and sync later, preserving transaction integrity without continuous connectivity. Mobile-first platforms also thrive in the distribution and field-service sectors, and the segment is projected to expand at a 5.96% CAGR through 2031, where handheld devices are the primary workstations. Social or collaborative add-ons that surface ERP approval flows inside chat applications help dispersed project teams operate across Argentina’s vast landmass.

At an implementation level, early adopters use mixed models in which core financials run in the public cloud, while specialized shop-floor modules remain on-premises until bandwidth improves. Vendors tout this phased roadmap because it stabilizes revenue while accommodating regulatory or connectivity constraints. Open-source alternatives, particularly Odoo, gain traction among SMEs that value license flexibility and a thriving local extension ecosystem. Yet, for mission-critical workloads, tier-one providers still dominate RFP shortlists because they combine uptime SLAs, audit-ready security certifications, and embedded Spanish-language AI skills that small code bases cannot match.

By Business Function: Finance Modules Lead As Compliance Complexity Rises

Finance and accounting applications accounted for 33.97% of the market share in 2025, the largest slice of the Argentina enterprise resource planning market. The driver is clear; AFIP’s e-invoicing APIs, provincial gross-receipts regimes, and ten-year archival mandates punish manual workflows that misreport tax triggers. Automated CAE retrieval, multi-currency valuation, and real-time ledger postings thus top every functional wish list. Supply-chain modules rank next, as nearshoring projects under RIGI require end-to-end material visibility; manufacturers cannot afford buffer inventories when inflation erodes carrying value month to month.

The human capital management segment is expected to achieve the highest CAGR of 6.14% through 2031. The segment grows because payroll tax tables change frequently, and embedded compliance templates cut audit risk. Customer-relationship components integrate e-commerce storefronts and physical stores, a necessity for retailers pursuing omnichannel strategies after pandemic-era habits stuck. Manufacturing execution and quality management remain niche but strategic among automotive and life sciences players that must trace every batch or VIN across multi-plant networks. Gradually, buyers are bundling discrete modules into holistic suites, but finance remains the gateway purchase that anchors vendor relationships.

By Deployment Model: Cloud Gains Despite Data-Residency Constraints

Cloud implementations accounted for 65.17% of the market share in 2025 and continue to grow at a 5.57% clip, proving that subscription economics outweigh skepticism about off-premise hosting. Financial institutions, however, must replicate ledgers to servers physically located in Argentina under data-sovereignty statutes, prompting a hybrid architecture in which compute runs in a São Paulo or Santiago region while write-once storage resides in Buenos Aires. Vendors wishing to win regulated-sector deals either open local regions or partner with colocation firms that can certify sovereign hosting.

Telecom Argentina's 2024 Integrated Report disclosed that the company operates 16 data centers with plans to upgrade capacity to 10 megawatts, positioning itself as a managed-cloud provider for enterprises seeking Argentine-hosted ERP instances without the capital expenditure of building private infrastructure.[3]Integrated Report 2024,” Telecom Argentina, telecom.com.ar On-premise share declines but persists in provinces where fiber backbones remain under construction or where companies prefer to amortize legacy hardware already on the books. The IDB-financed expansion of the federal fiber network will slowly level the playing field, yet until those trenches are dug, companies in Patagonia and the Northwest operate mirrored databases that sync during nighttime maintenance windows, ensuring regulatory reports reach AFIP even when primary links drop.

By Organization Size: Large Enterprises Anchor Market Amid SME Digitization Push

Large enterprises held a 59.77% revenue share in 2025 because they wield sufficient bargaining power to negotiate peso-indexed contracts and can finance multi-year rollout projects. Their average implementation includes finance, logistics, and HR modules across multiple legal entities, often supported by managed-service agreements that hedge currency risk. The small- and medium-sized enterprise segment is expected to grow the fastest, with a CAGR of 5.78% over the forecast period. SMEs hesitate to sign multi-year, dollar-denominated subscriptions, but IDB-backed vouchers are beginning to offset setup fees for firms outside urban cores.

Localized SaaS bundles that combine e-invoicing, payroll, and inventory under a single, low-seat offering appeal to wholesalers and agro exporters in second-tier cities. Implementation partners now package templates that cut go-live timelines to 90 days, reducing the window during which currency devaluation can inflate project cost. Over the forecast horizon, the SME segment’s CAGR remains below that of large enterprises but will climb as incentive disbursements accelerate and fiber availability improves.

By Industry Vertical: Manufacturing Leads as RIGI Nearshoring Accelerates

Manufacturing accounted for 29.84% of the Argentina enterprise resource planning market in 2025. Automotive, energy, and heavy-equipment OEMs committing USD 16 billion under RIGI need synchronized production, procurement, and treasury functions that legacy systems cannot handle. ERP suites, therefore, integrate MES data with financial ledgers, enabling real-time variance analysis and predictive maintenance. Retail and e-commerce are projected to expand at a 6.54% CAGR, the highest among all verticals, as chains build unified order-to-cash workflows that collapse storefront, marketplace, and last-mile delivery data into a single ledger.

Banking, financial services, and insurance providers face hard deadlines for electronic invoicing by July 2026, pushing them toward finance modules that automatically generate XML files containing CAE codes. Public-sector entities lag but are explicitly targeted by national transparency programs that condition budget increases on adopting digital procurement. Telecom operators embed billing engines capable of processing millions of daily events, and healthcare groups evaluate solutions with serialized product tracking to comply with drug-traceability norms.

Geography Analysis

Greater Buenos Aires, Córdoba, and Rosario jointly accounted for roughly 70% of Argentina's enterprise resource planning market installations in 2025 because those metros enjoy dense fiber rings, 5G coverage, and deep consultant pools. Edge providers expanded routes that cut SaaS latency by 18 milliseconds, making real-time dashboards viable for logistics fleets that previously worked offline. Nevertheless, Patagonia and the Northwest still rely on mixed deployments that batch-sync during off-peak hours, a compromise dictated by spotty connectivity rather than user preference.

Federal programs budgeted approximately USD 60 million for new 5G sites and USD 40 million for last-mile fiber in 2025, aiming to link 258 underserved municipalities by 2027. Progress is visible along national highways where fresh ducts carry multi-core cables, yet many provincial towns will not see enterprise-grade bandwidth until 2028. In the interim, distributors maintain on-premise instances behind satellite links or microwave relays and push consolidated ledgers to cloud repositories during scheduled maintenance windows.

Nearshoring incentives also shape the map. Automotive and energy projects gravitate toward Buenos Aires, Córdoba, Santa Fe, and Mendoza where supply chains, ports, or shale deposits cluster. Those same provinces therefore attract consultants and managed-service providers, reinforcing network effects that leave peripheral regions playing catch-up. Private carriers have laid 1,200 kilometers of new backbone since 2024, connecting secondary hubs like Neuquén and Salta to a Buenos Aires internet exchange, but economic feasibility keeps the most remote districts at the back of the rollout queue.

Competitive Landscape

Argentina's enterprise resource planning market competition is moderately concentrated. SAP, Oracle, and Microsoft remain entrenched in the top tier due to broad functional scope, Local GAAP support in Argentina, and the ability to host data within sovereign facilities. SAP deepened local roots by co-founding an AppHaus with Globant and launching AI-enhanced agriculture templates that resonate with grain cooperatives and seed developers.[4]Source: “SAP + Microsoft 365: A Unified AI Experience,” Microsoft, techcommunity.microsoft.com Microsoft counters with ARFinances, a turnkey localization for Dynamics 365 Business Central that embeds AFIP invoicing and provincial tax logic out of the box, cutting mid-market deployment time by a third.

Regional challenger, TOTVS, leverages peso pricing, Spanish-language interfaces, and a 70,000-company Latin American client base to undercut global rivals on total cost of ownership. Open-source vendor Odoo, distributed through Argentine partners, targets SMEs that want modular adoption and short learning curves. Local integrators such as Baufest, Calipso, and Axoft differentiate by bundling payroll or agribusiness extensions unavailable in off-the-shelf SaaS catalogs and by offering peso-denominated managed services that hedge currency swings for domestic clients.

Strategic moves increasingly revolve around AI-infused productivity. SAP’s Joule assistant and Dynamics 365 Copilot now interoperate, allowing cross-suite natural-language queries in Spanish. TOTVS signaled similar ambitions by previewing autonomous procurement agents that trigger MRP suggestions without user clicks. Compliance and residency credentials are table stakes, so vendors that cannot demonstrate ISO 27001 alignment or local data-center capacity find themselves locked out of regulated tenders. Taken together, the top five suppliers controlled comfortably above 60% of 2025 turnover, leaving ample white space for niche vertical specialists but few slots for generic newcomers.

Argentina Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

TOTVS S.A.

Infor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: ARCA issued Resolution 5824/26 mandating electronic invoicing for banks, insurers, and card processors from July 2026, creating immediate demand for compliant ERP modules.

- February 2026: TOTVS reported 2025 revenue of BRL 5.75 billion (USD 1.1 billion) and announced plans to embed predictive analytics across its suite.

- January 2026: SAP and Microsoft released bi-directional integration between SAP Joule and Microsoft 365 Copilot, enabling Spanish-language natural-language queries across both environments.

- January 2026: SAP and Syngenta partnered to deploy SAP S/4HANA Cloud Private Edition with AI-assisted agriculture modules tailored for Argentine growers.

- November 2025: Microsoft launched ARFinances localization for Dynamics 365 Business Central, providing out-of-the-box AFIP compliance and peso-denominated pricing.

Argentina Enterprise Resource Planning Market Report Scope

Argentina enterprise resource planning (ERP) is a suite of integrated applications that organizations use to manage and automate core business processes across functions such as finance, supply chain, human resources, customer relationship management, and manufacturing. The ERP market offers solutions tailored to businesses of all sizes and industries, with deployment options ranging from on-premises to cloud-based.

The Argentina enterprise resource planning report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and Social/Collaborative ERP, and Two-Tier/Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, and Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Other Industry Verticals |

| By Type | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Other Industry Verticals |

Key Questions Answered in the Report

How fast is the Argentina enterprise resource planning market expected to grow through 2031?

It is forecast to advance at a 5.12% CAGR from 2026 to 2031, reaching USD 108.12 million by the end of the period.

Which deployment model leads current spending?

Cloud implementations held 65.17% of 2025 revenue, driven by peso-denominated subscriptions that shield buyers from large up-front capital outlays.

Why are finance modules the largest functional segment?

AFIP e-invoicing mandates and multi-year digital-archival rules require automated CAE retrieval, pushing enterprises to prioritize finance and accounting suites.

How do data-residency laws affect cloud adoption in banking?

Financial institutions must store original ledgers on Argentine soil, forcing a hybrid model that replicates data to in-country servers even when compute runs abroad.

Page last updated on: