Argentina Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

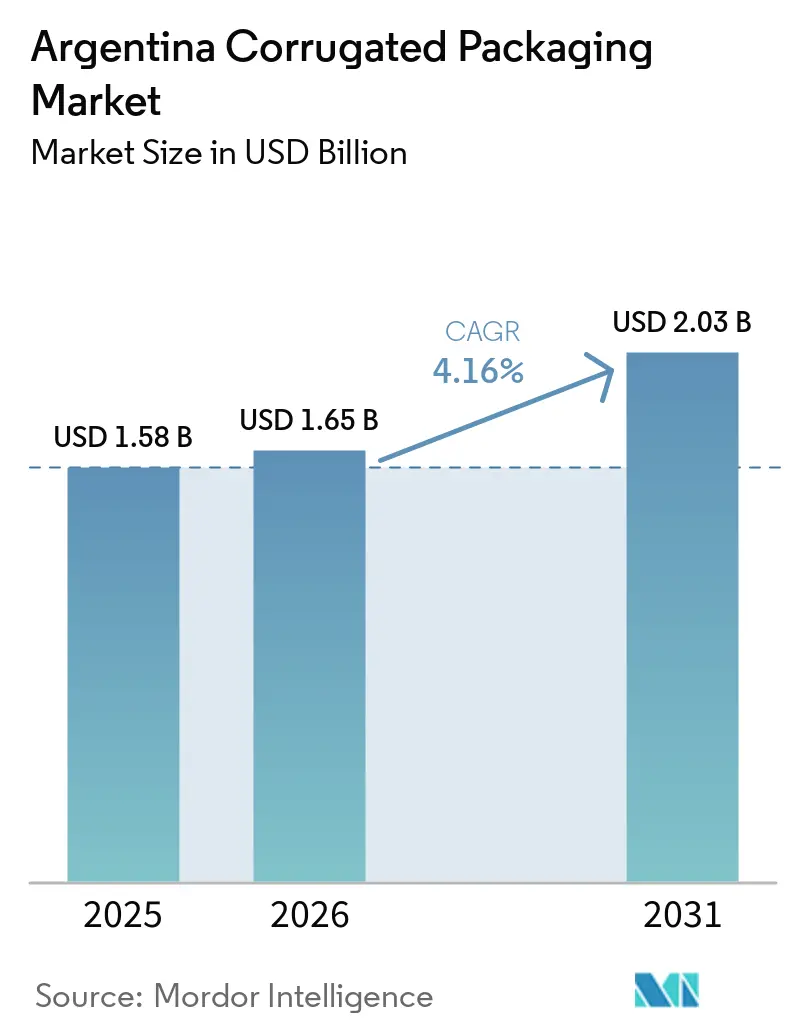

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 2.03 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Corrugated Packaging Market Analysis by Mordor Intelligence

The Argentina corrugated packaging market size is expected to grow from USD 1.58 billion in 2025 to USD 1.65 billion in 2026 and is forecast to reach USD 2.03 billion by 2031 at a 4.16% CAGR over 2026-2031. A gradual rebound in household spending, a sizable agro-export pipeline and the country’s e-commerce boom combine to lift baseline demand. Recycled fiber continues to displace virgin grades because of cost and sustainability advantages, even as import liberalization keeps Brazilian kraftliner competitive. Logistics players now specify lighter micro flute and die-cut formats to cut freight charges, while processed food companies call for retail-ready cases that speed shelf replenishment. Converter margins remain sensitive to diesel-led transport inflation, pushing vertically integrated suppliers to expand renewable-power sourcing and lightweight paper innovations.

Key Report Takeaways

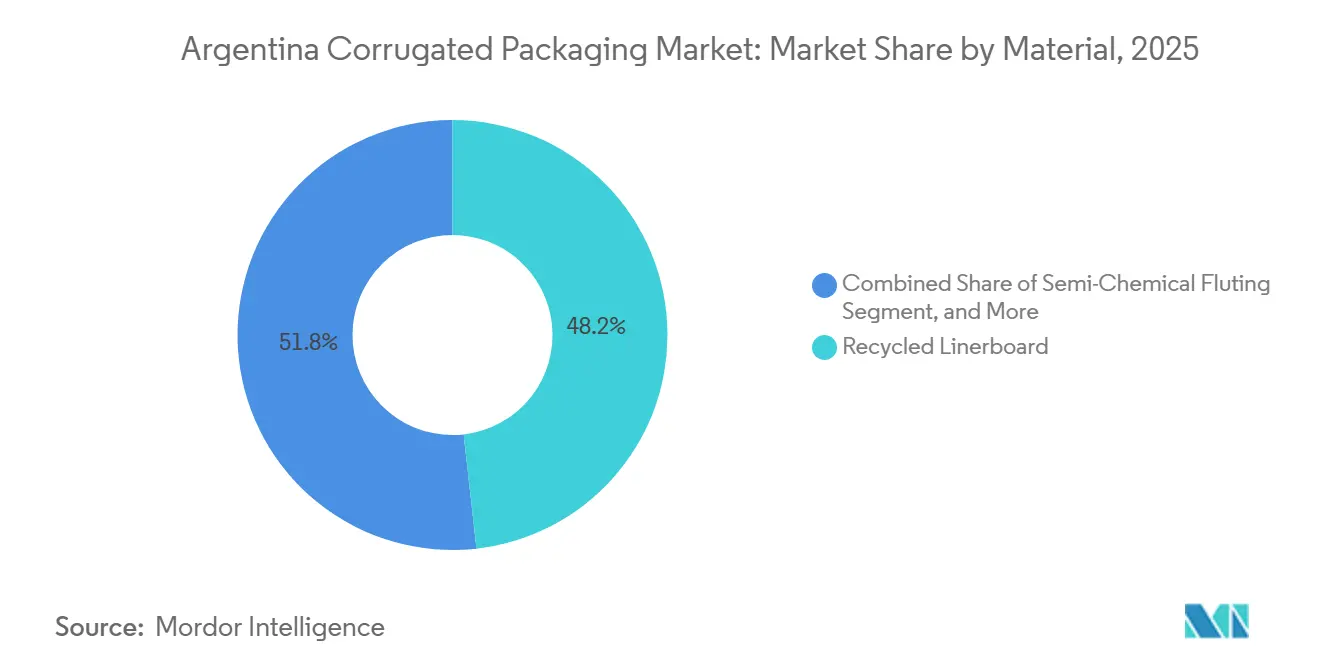

- By material, recycled linerboard captured 48.22% of the Argentina corrugated packaging market share in 2025.

- By flute type, the Argentina corrugated packaging market size for the F flute segment is forecast to advance at a 5.13% CAGR through 2031.

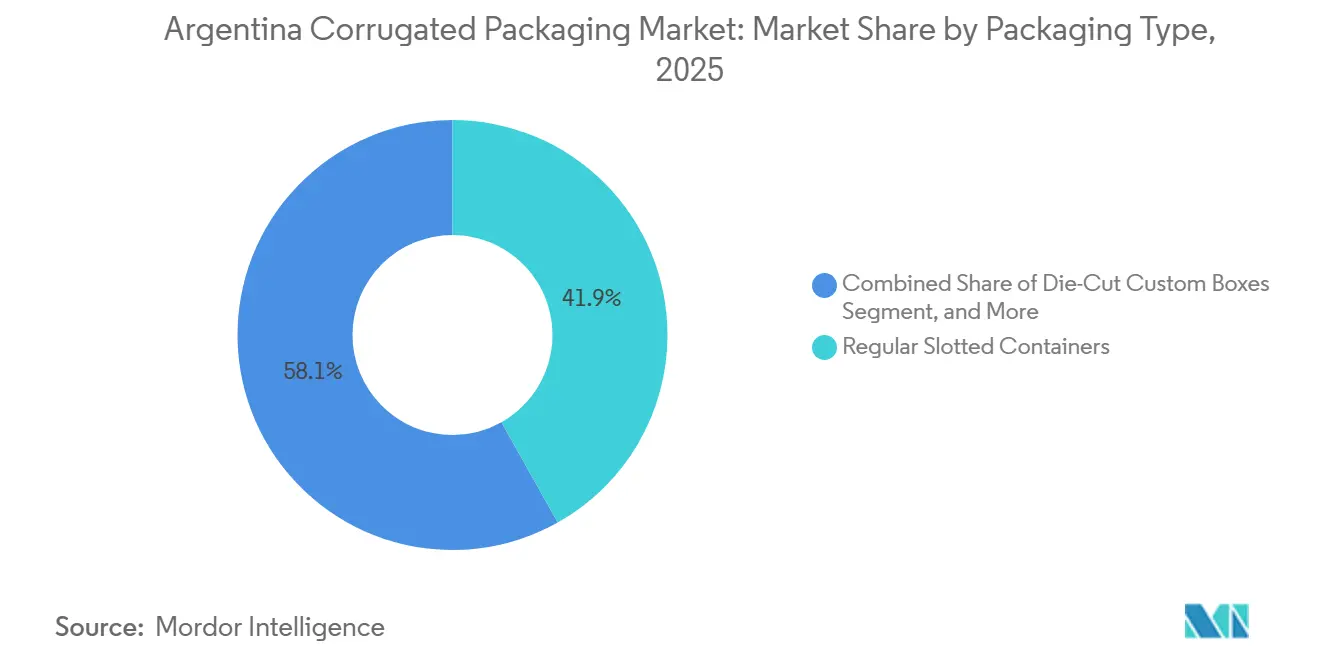

- By packaging type, regular slotted containers captured 41.86% of the Argentina corrugated packaging market share in 2025.

- By wall type, the Argentina corrugated packaging market size for the triple-wall structures segment is forecast to advance at a 5.01% CAGR through 2031.

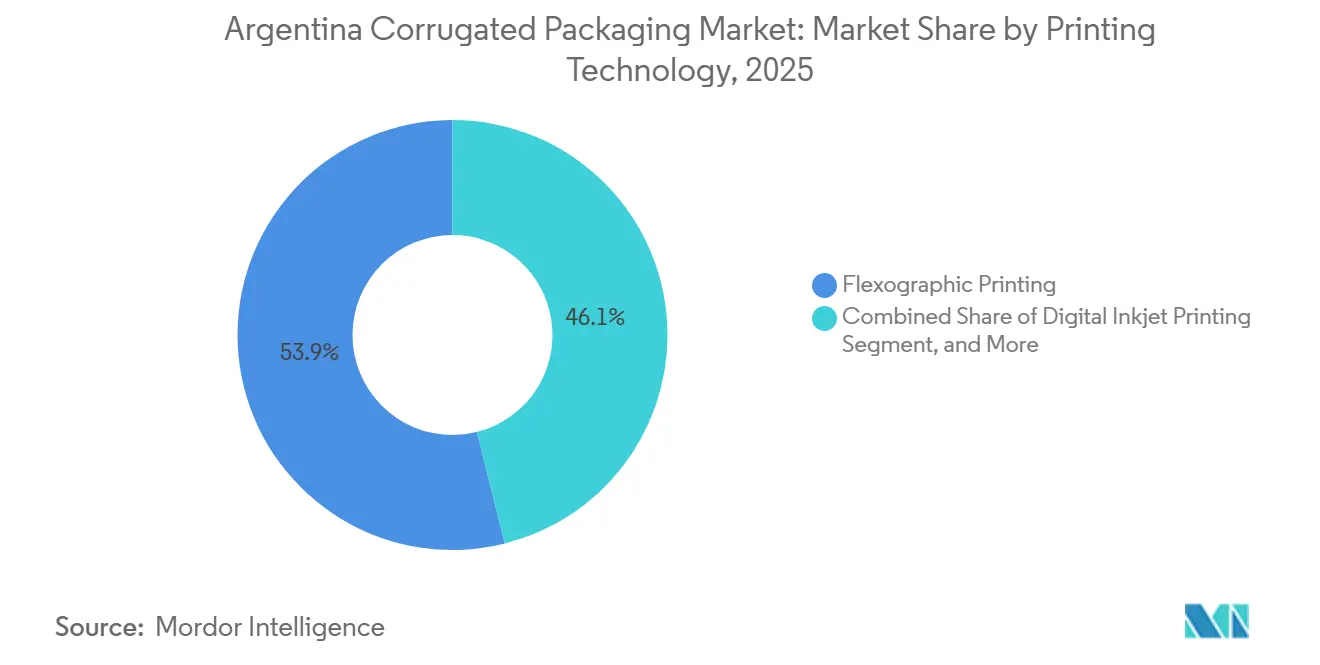

- By printing technology, flexographic printing captured 53.91% of the Argentina corrugated packaging market share in 2025.

- By end-user, the Argentina corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at a 5.09% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-commerce Penetration in Argentina | +1.20% | Greater Buenos Aires and Córdoba | Short term (≤ 2 years) |

| Government Incentives for Sustainable Packaging | +0.80% | Buenos Aires and Salta provinces | Medium term (2-4 years) |

| Expansion of Domestic Processed Food Industry | +0.70% | San Luis, Buenos Aires and Balcarce | Medium term (2-4 years) |

| Growth in Fresh Produce Export Corrugate Demand | +0.60% | Río Negro, Tucumán and Mendoza corridors | Short term (≤ 2 years) |

| Technological Adoption of Digital Printing | +0.30% | Greater Buenos Aires converters | Long term (≥ 4 years) |

| Shift Toward Lightweight Recycled Fiber | +0.40% | Provinces with long inland transport distances | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising E-commerce Penetration In Argentina

MercadoLibre’s USD 3.4 billion capital plan for 2026 underpins near-term corrugated growth, including a 100,000 m² Escobar hub capable of sorting 130,000 parcels per day.[1]Rodrigo Campos and Andre Romani, “MercadoLibre to Invest USD 3.4 Billion in Argentina This Year,” Reuters, reuters.com Fulfillment models now favor right-sized, die-cut cartons compatible with automated picking, increasing the SKUs that converters must stock. Thin F flute formats help sellers shave dimensional-weight fees, and branded graphics heighten the unboxing experience that drives repeat purchases. Rapid delivery promises require local corrugator footprints near last-mile depots spreading across 40 cities.[2]Redacción, “Mercado Libre Anunció la Construcción del Mayor Centro Logístico del País,” Punto Biz, puntobiz.com.ar Demand is therefore migrating from a Buenos Aires-centric base toward provincial nodes.

Government Incentives For Sustainable Packaging

Decreto 779 operationalized national EPR rules that oblige brand owners to finance post-consumer recovery, pushing box makers to certify recycled content.[3]Presidencia de la Nación, “Volumen Récord de las Exportaciones Agroindustriales Durante el Primer Bimestre de 2026,” argentina.gob.ar Salta’s circular-economy statute sets aggressive recycled-content tiers for plastics, indirectly positioning corrugated as a substitute.[4]Cámara de Senadores de la Provincia de Salta, “Expte. 90-33.413/2025 - Economía Circular de los Plásticos,” senadosalta.gob.ar The Economy Ministry’s BIOPRODUCTO seal rewards biobased substrates, giving virgin-fiber corrugators a premium niche. Multinational FMCGs increasingly require ISO 14001 compliance in supplier audits, driving investments in energy-efficient corrugators and closed-loop water systems. Early adopters market these credentials to capture higher-margin export orders.

Expansion Of Domestic Processed Food Industry

McCain is channeling USD 100 million into its Balcarce potato plant, with a share earmarked for state-of-the-art packaging lines that raise throughput. Arcor’s new San Luis site adds confectionery capacity and creates 300 early jobs, locking in steady carton volumes for biscuits and candy. Food processors are downsizing pack formats to meet inflation-hit wallets, so converters must supply high-graphic retail-ready cases that preserve shelf presence in crowded supermarkets. Frozen and chilled SKUs require moisture-resistant liners to maintain cold-chain integrity, while export consignments require double-wall strength for Brazilian routes. These specifications spur capital upgrades in printing and coating.

Growth In Fresh Produce Export Corrugate Demand

Fruit exports rebounded to 770,000 tonnes in 2025, led by lemons and pears, lifting orders for ventilated double-wall trays that endure 1,000+ km truck hauls to Buenos Aires ports. January 2026 agro-exports rose 17 % YoY to 10.63 million tonnes, extending peak season for rural corrugators. Long cold-chain transits spur trials of wax-free moisture barriers that ease recycling overseas. Triple-wall cases protect machinery and sugar sacks bound for Asia, illustrating a dual-track demand for strength and stackability. Regional packhouses in Tucumán and Río Negro now co-locate mini corrugators to cut empty-box freight backhauls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Recycled Paper Prices Due to Import Restrictions | -0.90% | Buenos Aires converters | Short term (≤ 2 years) |

| Inflationary Pressure on Packaging Costs | -0.70% | Provincial converters with lengthy routes | Short term (≤ 2 years) |

| Limited Availability of High-quality Virgin Fiber | -0.50% | Producers of high-strength kraft boxes | Medium term (2-4 years) |

| Competitive Threat from Flexible Plastic Alternatives | -0.30% | Food and personal-care segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Recycled Paper Prices Due To Import Restrictions

Cardboard prices plunged from ARS 300/kg to ARS 163/kg after the government eased controls on imported kraftliner, eroding margins for cartoneros supplying domestic mills. Waste-collection volumes fell 8.3 % in 2025, starving recyclers of feedstock. New IRAM 3130 quality rules tighten contamination thresholds, raising rejection rates at customs. Converters with foreign-currency credit lines import pulp to hedge, but smaller players face liquidity crunches and output cuts. The mismatch between falling domestic supply and cheaper imports heightens price volatility, disrupting production planning.

Inflationary Pressure On Packaging Costs

The FADEEAC index shows transport costs up 37% in 2025, as diesel jumped 45%. Fuel-tax deferrals cloud price visibility, complicating long-term freight contracts. Rising logistics bills compress converter spreads because pass-through is limited in a market running 60 % excess capacity. Provincial plants shipping boards from Buenos Aires incur the steepest surcharges, nudging brand owners to dual-source from nearby corrugators. Fleet upgrades to Euro VI trucks and route-optimization software are mitigating measures, but capex payback stretches when inflation runs high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fiber Consolidates Cost Leadership

Recycled linerboard anchored 48.22% of 2025 shipments in the Argentine corrugated packaging market. Semi-chemical fluting, expanding at 5.26% CAGR, reflects brand owners’ drive to shed grammage without sacrificing stacking performance. Virgin Kraft remains vital for export-grade triple-wall crates, but supply tightened after Celulosa Argentina’s bankruptcy, increasing reliance on Brazilian mills. Integrated players such as Arcor arbitrage between self-collected OCC and imported kraft rolls, enabling agile pricing when peso swings widen. The Argentina corrugated packaging market size for semi-chemical fluting is therefore poised for above-average expansion as converters tune recipes to counter freight inflation.

Liberalized scrap imports lower fiber costs for mills that clear IRAM 3130 checks, but most SMEs lack the paperwork expertise, locking them into volatile domestic feedstock. Renewable power deals signed by Smurfit Westrock cut Scope 2 costs, reinforcing recycled fiber’s low-carbon appeal among multinational FMCGs. Net-net, recycled grades will likely top 50% share before 2028, cementing their role in the Argentine corrugated packaging industry’s circular-economy narrative.

By Flute Type: Micro Flute Formats Gain Retail Momentum

B flute sustained a 37.55% share in 2025, balancing cushioning with economics for mass FMCG shipping. F flute’s 5.13% CAGR outpaces all, spurred by MercadoLibre’s automation specs favoring thin profiles. The resulting dimensional-weight savings satisfy e-tailers’ courier contracts, especially on cross-province legs. A flute retains niche appeal for heavy fruit boxes shipped in refrigerated containers, preserving the Argentina corrugated packaging market size linked to agricultural exports.

Micro flute adoption demands tighter process control and higher-grade starch adhesives, raising entry hurdles for smaller corrugators. Capex in precision corrugators is clustering among metro-Buenos Aires plants that can amortize volumes, leaving provincial peers to secure toll-conversion deals. Over the horizon, joint R&D between paper mills and machinery vendors aims to expand F flute grammage windows so producers can switch grades without downtime.

By Packaging Type: Displays And Custom Boxes Outshine Commodity SKUs

Regular slotted containers still accounted for 41.86% of revenues in 2025, yet display units will chart the highest 5.97% CAGR as brand marketers battle for in-store attention. Die-cut cartons underpin the e-commerce unboxing push, enabling converters to capture value-added margins despite raw-material swings. The Argentina corrugated packaging market share held by displays will edge up as supermarkets mandate shelf-ready cartons that cut restocking labor.

Sustainability rules in Buenos Aires City encourage mono-material solutions, giving corrugated displays an edge over laminated plastics. Meanwhile, pallet-box pilots using reinforced corners aim to displace wooden crates in intra-Mercosur flows, illustrating continuous innovation even in mature SKUs. Printers therefore invest in high-line-count flexo plates to deliver photo-real graphics at run lengths below litho thresholds.

By Wall Type: Export Growth Propels Triple-Wall Uptick

Single-wall cartons made up 60.14% of 2025 volume thanks to domestic FMCG and parcel traffic. Triple-wall units, set to grow 5.01% CAGR, serve sugar, wheat and machinery exporters facing rough maritime handling. The Argentina corrugated packaging market size tied to single-wall will still rise, but its mix skews lighter as converters adopt semi-chemical mediums.

Transport-fuel inflation intensifies the quest for lighter yet stiffer constructions, prompting research into nano-fibrillated cellulose strengthens. Exporters of frozen crustaceans now trial hybrid double-wall liners coated with plant-based resins to survive blast-freezer moisture. Such niche adaptations illustrate how wall-type strategy balances structural integrity, cost and recyclability.

By Printing Technology: Digital Inkjet Crosses The Adoption Chasm

Flexo held 53.91% share in 2025 on the back of mature workflows and low unit costs. Digital inkjet is forecast for 5.31% CAGR because e-retailers demand serialized prints for order tracking and campaign personalization. The Argentina corrugated packaging industry still wrestles with the USD 1 million ticket price of single-pass inkjet presses, but early adopters leverage premium margins on short runs.

Brand compliance with upcoming post-consumer labeling laws in Buenos Aires City will likely compel wider variable-data capability, shortening the ROI on digital presses. Flexo will not fade; instead, hybrid lines combining inkjet modules with high-speed flexo units are emerging, marrying speed and customization. Converters that master workflow integration will outpace peers tethered to legacy platemaking queues.

By End-User Industry: Fulfillment Centers Emerge As Volume Catalyst

Processed foods delivered 28.58% of 2025 demand, anchored by bakery, confectionery, and frozen potato products. Yet e-commerce fulfillment centers will post the leading 5.09% CAGR as MercadoLibre and competitors replicate hub-and-spoke models beyond Greater Buenos Aires. The Argentine corrugated packaging market, driven by e-commerce, therefore outstrips GDP growth, cushioning the sector from cyclical dips in consumer goods.

Fresh-produce packers in Tucumán and Río Negro sustain double-wall box orders aligned with rising pear and lemon exports, while electronics importers lean on E flute cartons for mobile-phone drop shipments. Pharmaceutical firms are requesting tamper-evident secondary boxes with QR authentication, a niche that dovetails with the uptake of digital printing. This diversified end-user mix insulates the sector from single-segment shocks.

Geography Analysis

Greater Buenos Aires dominates the Argentine corrugated packaging market, clustering the nation’s largest converters, its busiest seaport, and the bulk of e-commerce parcel flows. The new Escobar fulfillment campus cements this primacy, giving box makers within 100 km unrivaled volume visibility. Córdoba and Santa Fe host satellite plants that feed processed-food corridors, while Mendoza corrugators cater to wine exporters whose fragile glass requires precision die-cuts.

Transport-fuel inflation, running 37% in 2025, is incentivizing on-site corrugator installations in agro-export hubs like Tucumán’s lemon belt, trimming empty-box hauls that once stretched 900 km to port. Nevertheless, most imported kraftliner still lands in Buenos Aires and Rosario, binding provincial converters to the river Parana logistics. Provincial demand is also rising because MercadoLibre’s 40 mini-hubs distribute order fulfillment, diffusing carton consumption toward mid-sized cities.

Policy developments mirror these spatial shifts. Salta’s circular-economy mandate spurs local box makers to ramp post-consumer content, while Buenos Aires City’s draft EPR law could impose city-specific labeling that only nearby printers can meet at 24-hour lead times. Overall, the Argentine corrugated packaging market maintains a core-periphery dynamic, yet investments in regional capacity suggest moderating concentration over the next decade.

Competitive Landscape

Market concentration is moderate. Smurfit Westrock, Cartocor, and Grupo Zucamor headline, but over 800 smaller firms supply niche runs. Smurfit Westrock’s full switch to renewable electricity in 2025 cuts operating risk from volatile grid tariffs and gives its cartons a low-carbon badge coveted by global FMCGs. Cartocor’s control of 23,000 ha of forestry and 170,000 tpy of recycled paper shields it from fiber price gyrations, allowing it to make aggressive bids on long-term supply contracts.

Import liberalization widened the price gap between integrated and non-integrated converters, as the former leverage bulk kraftliner buys from Klabin’s new Piracicaba plant. Digital print remains a white-space; less than 5% of the national installed base can run variable-data jobs at scale, so early movers can capture high-margin promotional SKUs. Smurfit Westrock’s PPAs with 360Energy underpin carbon-neutral claims, while provincial SMEs pool OCC collections to secure BIOPRODUCTO certification.

M&A potential looms as smaller converters, squeezed by 45% diesel hikes, may offload assets to cash-rich leaders. Still, antitrust regulators monitor share thresholds to keep the Argentine corrugated packaging market contestable. Foreign entrants eye regional platforms rather than greenfield mills, evident in Klabin’s cross-border box exports that undercut local kraft substitutes when the peso slides.

Argentina Corrugated Packaging Industry Leaders

Smurfit Westrock plc

Grupo Zucamor SA

Cartocor SA (Arcor Group)

International Paper Company

Papelera San Andrés de Giles SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: MercadoLibre began building a USD 115 million, 100,000 m² logistics hub in Escobar, slated to open Nov 2026 with capacity for 130,000 daily parcels and 2 million bulky items, quadrupling its domestic handling capacity.

- March 2026: McCain Foods announced a USD 100 million, five-year modernization at Balcarce, channeling USD 3 million into new packaging automation and USD 2 million into logistics upgrades.

- March 2026: MercadoLibre confirmed a USD 3.4 billion national investment program for 2026, a 30 % rise over the prior year, targeting logistics, fintech and platform technology expansion.

- December 2025: Smurfit Westrock achieved 100% renewable electricity across Argentine plants after signing multi-year PPAs with 360Energy and Energeia.

Argentina Corrugated Packaging Market Report Scope

The Argentina Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Argentina Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Argentina corrugated packaging market size and its growth outlook?

The sector stood at USD 1.65 billion in 2026 and is projected to reach USD 2.03 billion by 2031, reflecting a 4.16% CAGR over 2026-2031.

Which material segment will see the fastest growth in Argentina's box sector?

Semi-chemical fluting is forecast to rise at a 5.26% CAGR as shippers pursue lightweight yet strong boards.

How is e-commerce reshaping demand for corrugated solutions in Argentina?

MercadoLibre's multi-billion-dollar fulfillment buildout is driving micro flute adoption and rapid-cycle, custom die-cut boxes for parcel networks.

What sustainability measures influence packaging choices among Argentine brand owners?

Extended producer responsibility rules and ISO 14001 supplier audits are pushing converters toward recycled fiber, renewable energy and BIOPRODUCTO certification.

Which printing technology is gaining share in Argentina's box market?

Digital inkjet is the fastest-growing technology thanks to short-run customization and variable data needs linked to e-commerce promotions.

How exposed are corrugated producers to input-price swings?

Volatile recycled-paper prices and a 45 % diesel surge in 2025 squeezed margins, favoring vertically integrated firms with import options and renewable-energy hedges.

Page last updated on: