Arachnoid Cysts Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

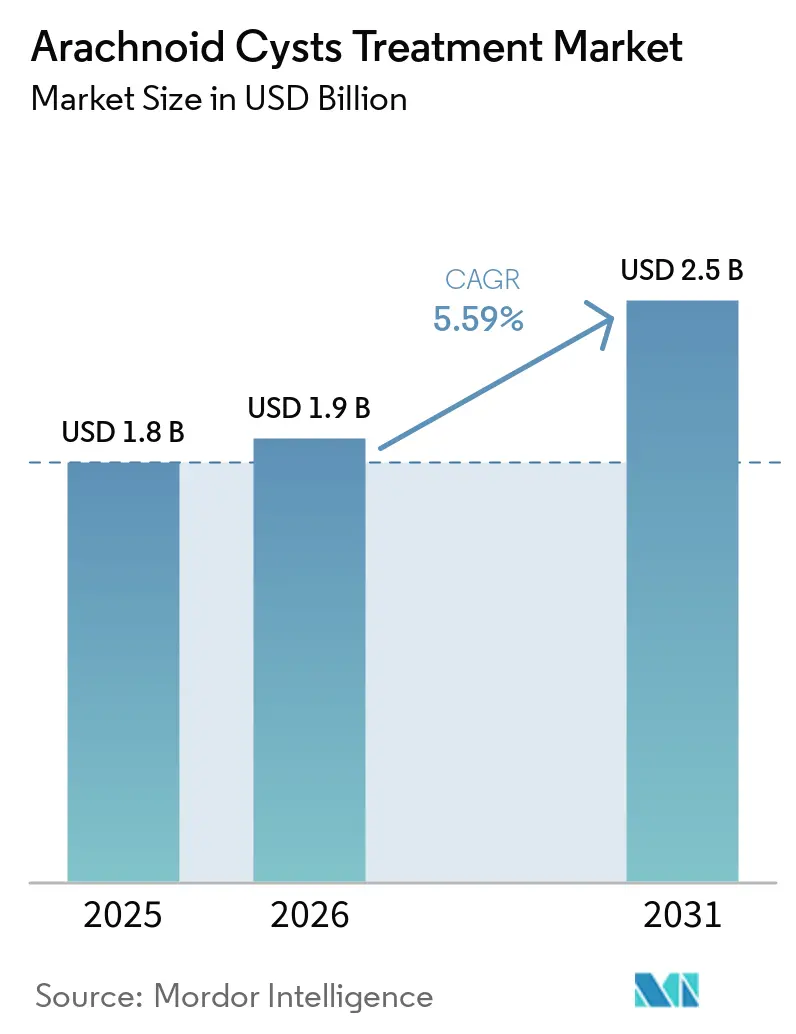

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.5 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Arachnoid Cysts Treatment Market Analysis by Mordor Intelligence

The Arachnoid Cysts Treatment Market size is projected to expand from USD 1.8 billion in 2025 and USD 1.9 billion in 2026 to USD 2.5 billion by 2031, registering a CAGR of 5.59% between 2026 to 2031.

Growing clinical confidence in endoscopic fenestration, incremental gains in programmable shunts, and steady roll-out of hybrid operating rooms are setting a measured but durable growth path. Surgeons are increasingly guided by high-resolution MRI and near-infrared fluorescence imaging, which sharpen anatomic visualization and trim operative times. Hospital capital budgets are allocating more funds to single-use neuroendoscopy sheaths that lower infection risks, while public health systems in Asia-Pacific are underwriting hybrid suites to lift surgical throughput. Competitive intensity stays moderate; device buyers prize post-operative outcomes over headline price, leaving scope for differentiated optics, miniaturized scopes, and MRI-safe programmable valves to defend margin in the arachnoid cysts treatment market.

Key Report Takeaways

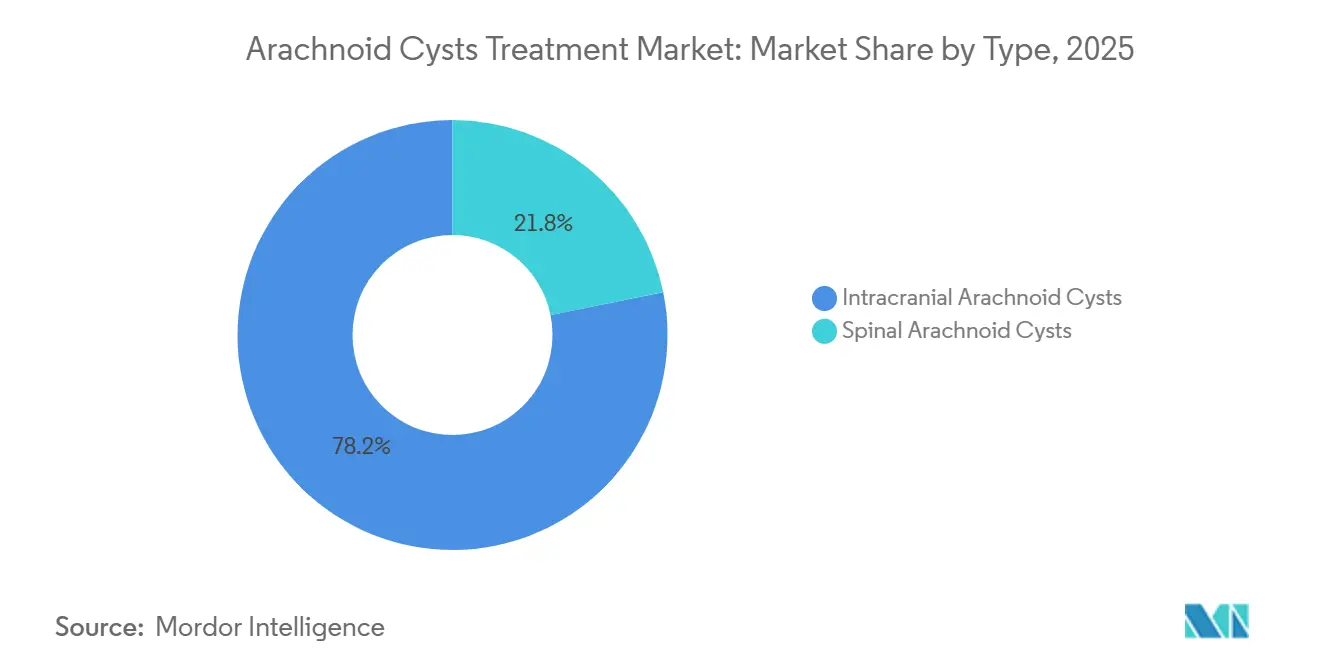

- By type, intracranial arachnoid cysts captured 78.19% of the arachnoid cysts treatment market share in 2025, whereas spinal cysts are on track for the fastest growth with a 7.30% CAGR to 2031.

- By treatment, endoscopic cyst fenestration led with 61.89% of treatment revenue in 2025, while microsurgical fenestration is set to expand at a 7.45% CAGR due to its efficacy in hemorrhagic or multiloculated lesions.

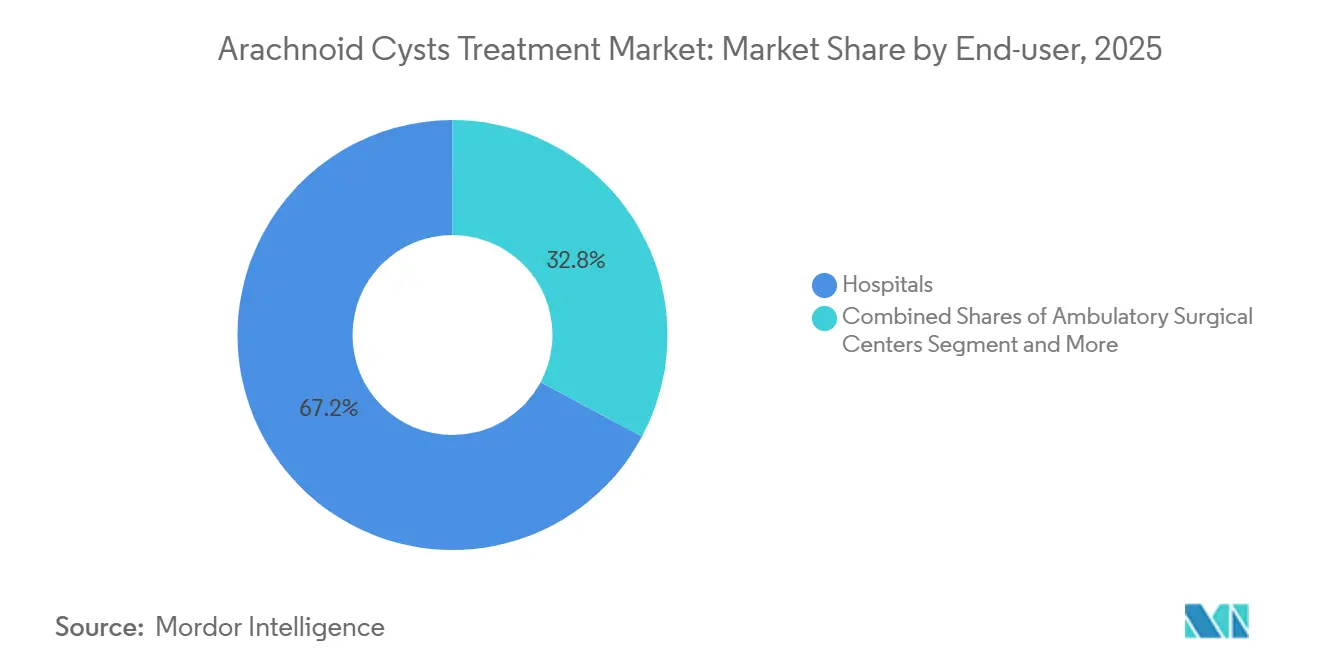

- By end users- hospitals accounted for 67.18% of the value in 2025, but specialty neurosurgery clinics represent the quickest-moving end-user segment at a 7.23% CAGR as outpatient protocols shorten length-of-stay.

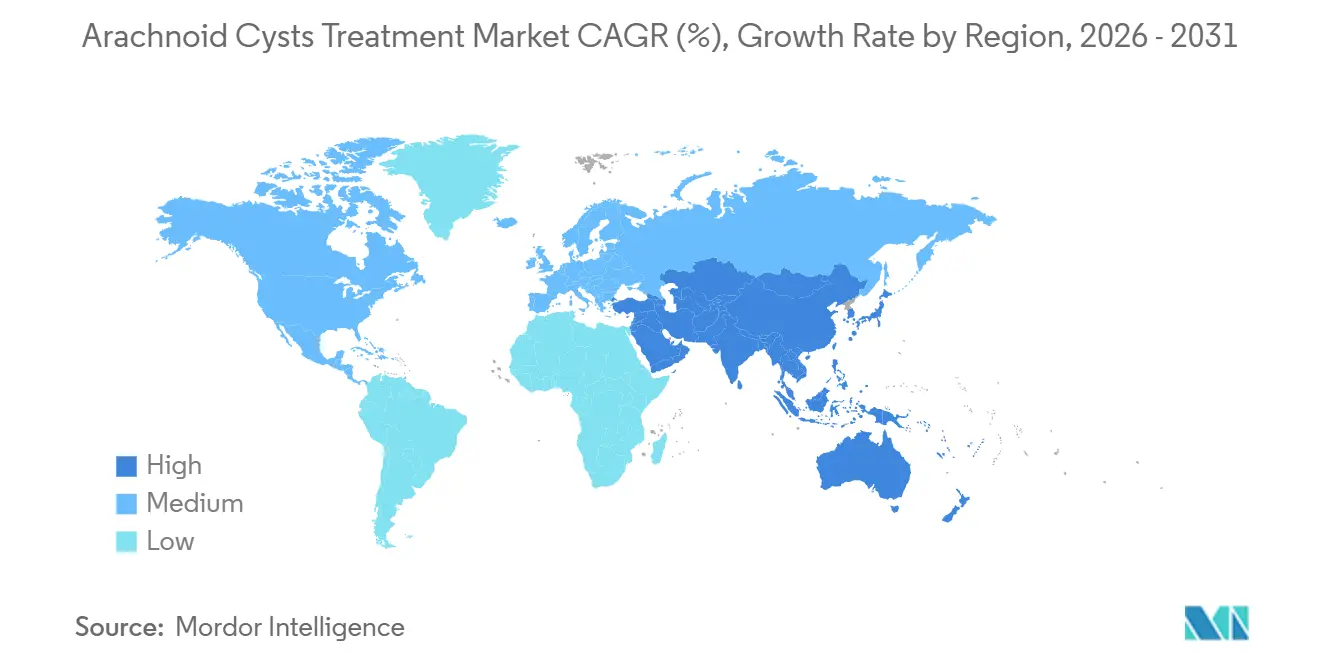

- By geography, North America commanded 47.17% regional share in 2025; Asia-Pacific is the fastest climber, advancing at a 7.45% CAGR through 2031 as public-sector projects seed hybrid operating theatres.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Arachnoid Cysts Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in minimally invasive neuroendoscopy and real-time intraoperative imaging | +1.8% | Global, with early adoption in North America, Europe, and Asia-Pacific tertiary centers | Medium term (2-4 years) |

| Expanding pediatric neurosurgery infrastructure in emerging markets | +1.5% | Asia-Pacific (India, China, Southeast Asia), Latin America (Brazil, Argentina) | Long term (≥ 4 years) |

| Improved high-resolution MRI enabling early detection of symptomatic cysts | +1.2% | Global, accelerated in regions with universal healthcare coverage (Europe, Canada, Japan) | Short term (≤ 2 years) |

| Growing adoption of programmable shunt valves with anti-siphon mechanisms | +1.0% | North America, Europe, with spillover to Middle East private hospitals | Medium term (2-4 years) |

| Improved clinical outcomes data and evidence-based guidelines driving surgical intervention | +0.9% | Global, with faster adoption in academic medical centers and tertiary hospitals | Short term (≤ 2 years) |

| Telemedicine-enabled triage and remote MRI interpretation expanding access | +0.7% | Asia-Pacific (China-Pakistan corridor), Middle East, Africa, with cross-border applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advances in Minimally Invasive Neuroendoscopy Drive Procedural Shift

Neuroendoscopic fenestration now anchors first-line therapy, propelled by FDA clearances for systems that pair 4 mm rigid scopes with near-infrared fluorescence to map subsurface vessels and avert venous injury. Integra’s single-use AURORA Surgiscope, cleared in April 2025, folds LED lighting and video into a sterile sheath, cutting reprocessing time and infection exposure [1]Integra LifeSciences, “AURORA Surgiscope System 510(k) Summary,” 510k.innolitics.com. A 2024 meta-analysis reported 75% radiographic cyst reduction and 90% headache relief after posterior fossa decompression, reinforcing confidence in endoscopy. Recurrence persists at 10-30%, steering R&D toward biodegradable stents that prop open fenestrations. Shorter average hospitalization of 1.5 days now aligns fenestration economics with ambulatory surgical center models.

Expanding Pediatric Neurosurgery Infrastructure Unlocks Emerging-Market Demand

Government-funded hybrid suites in India, China, and Southeast Asia are broadening operative capacity. Tamil Nadu’s integrated theatre, inaugurated in November 2025, merges CT, endoscopy, and ultrasound, enabling 40-50 complex cases per month and eliminating risky mid-procedure transfers. Argentina’s neurosurgery society embedded a 720-hour pediatric curriculum that includes arachnoid cyst techniques, signaling talent pipeline expansion. Telemedicine corridors linking Pakistan with Beijing Tiantan Hospital streamline pre-op triage and reserve cross-border referrals for the toughest lesions, trimming travel costs and accelerating care.

Improved High-Resolution MRI Expands Diagnostic Capture of Symptomatic Cases

Three-Tesla scanners armed with cine phase-contrast sequences show CSF flow and cyst-cistern communication, refining surgical choice between ventriculocystostomy and ventriculocystocisternostomy. Diffusion-weighted imaging distinguishes arachnoid from epidermoid cysts, minimizing misdiagnosis. Population studies peg prevalence at 1.4% in adults and 2.6% in children, yet only a slice become symptomatic, keeping surgeons vigilant against overtreatment. Earlier detection lifts the potential intervention pool, nudging up the arachnoid cysts treatment market but also loading imaging departments with follow-up scans.

Growing Adoption of Programmable Shunt Valves Reduces Overdrainage Complications

When fenestration fails or cysts coexist with hydrocephalus, MRI-safe programmable valves provide adjustable pressure settings that trim revision risk. Aesculap’s proSA Valve independently tunes upright and supine pressures to counter siphoning. Integra’s Codman Certas Plus adds a virtual-off mode, letting clinicians dial out flow without surgery. Sub-millimeter duckbill valves under development could mimic arachnoid granulations and usher in physiologic drainage solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedural costs and reimbursement complexity limiting access | -0.8% | Global, acute in developing markets without universal coverage; prior authorization delays in North America | Short term (≤ 2 years) |

| Asymptomatic presentation in 70-90% of cases limiting surgical market | -0.6% | Global, with conservative observation protocols most prevalent in Europe and Japan | Long term (≥ 4 years) |

| Surgical complication risks and recurrence rates constraining adoption | -0.5% | Global, with higher impact in centers lacking hybrid OR capabilities | Medium term (2-4 years) |

| Neurosurgeon workforce shortages constraining capacity in emerging markets | -0.4% | Asia-Pacific (excluding Japan, South Korea), Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedural Costs and Reimbursement Complexity Limit Access

Endoscopic fenestration CPT codes (e.g., 62161) often require prior authorization in the U.S., delaying therapy for most patients and tightening hospital cash flows [2]Osama Amir, “Medical Billing for Neurosurgery,” transcure.net. In many emerging economies, out-of-pocket bills between USD 3,000 and USD 5,000 keep surgery out of reach. Bundling of navigation and imaging add-on codes further clouds revenue predictability. Pediatric families without insurance frequently defer care until hydrocephalus sets in, crimping the immediately addressable portion of the arachnoid cysts treatment market.

Surgical Complication Risks and Recurrence Rates Constrain Adoption

Subdural effusion surfaced in the majority of children undergoing transtemporal fenestration, though two-thirds resolved spontaneously. Recurrence hits 10-30% across modalities, leading some surgeons to favor microsurgical excision despite higher infection odds. Re-operation risk climbs in infants, and the absence of biomarkers to predict cyst expansion forces conservative observation for borderline cases, moderating overall procedure volumes in the arachnoid cysts treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Intracranial Dominance Reflects Symptomatic Burden

Intracranial cysts commanded 78.19% of the arachnoid cysts treatment market in 2025, mainly because middle cranial fossa and retrocerebellar locations provoke headaches, seizures, or hydrocephalus that necessitate surgery. Galassi type III lesions usually bypass observation and move straight to fenestration or shunting. Spinal arachnoid cysts hold a sliver of current revenue yet are forecast at a robust 7.30% CAGR as safer laminectomy protocols extend operability.

The arachnoid cysts treatment market size attributable to intracranial surgery is projected to widen steadily through 2031, while spinal cases benefit from neuromonitoring that curbs cord-injury risk. Although spinal cysts lack a universal classification scheme, thoracic lesions that compress the dorsal columns are moving toward earlier excision, increasing the demand for low-profile retractors. Combined, these dynamics keep intracranial volume high and spinal growth brisk, sustaining product line diversification for device makers.

By Treatment Type: Endoscopy Leads, Microsurgery Scales Complexity

Endoscopic fenestration held 61.89% of treatment revenue in 2025, but microsurgical fenestration’s 7.45% CAGR underscores its appeal for multiloculated or hemorrhagic cysts. A child-focused 2025 study logged zero recurrences with partial cyst-wall excision versus three each in endoscopic and shunt cohorts, spotlighting microsurgery in difficult anatomy[3]Mohamed Amen et al., “Ventriculocystocisternostomy vs Ventriculocystostomy,” Egyptian Journal of Neurosurgery, springeropen.com. The arachnoid cysts treatment market size linked to endoscopy will still outpace peers because ambulatory suitability and short stays resonate with value-based care mandates. Yet the microsurgical subset generates a premium on operative microscopes and neuronavigation, enriching average selling prices. Cystoperitoneal shunting retains a niche for protein-rich lesions, but recurring infections and obstruction temper growth.

By End-User: Hospitals Dominate, Clinics Gain Margin Advantage

Hospitals represented 67.18% of spending in 2025, reflecting their control of hybrid ORs, intensive care, and transfusion services essential for complex cranial work. Intracranial cases needing extended monitoring keep hospitals at the center of the arachnoid cysts treatment market.

Specialty neurosurgery clinics, however, are registering a 7.23% CAGR as payers green-light outpatient endoscopic protocols. Clinics leverage low overhead and quicker prior authorization cycles to perform fenestrations with 24- to 48-hour discharge, improving margin. Still, any intraoperative hemorrhage instantly redirects patients to hospital ICUs, preserving the hospital’s role for high-acuity events.

Geography Analysis

North America generated 47.17% of 2025 revenue. Widespread insurance coverage and dense neurosurgeon networks buoy procedure volumes, although prior authorization delays continue to blur scheduling. Canada’s single-payer model ensures universal access but prolongs elective waitlists. Mexico’s private centers draw uninsured U.S. patients with package prices that undercut domestic quotes, nudging tourism inflows and adding a niche layer to the arachnoid cysts treatment market.

Asia-Pacific is projected to climb at 7.45% CAGR through 2031. India’s first government-run hybrid neurosurgery suite demonstrates how public capital can pivot regional surgical capacity upward. China’s flagship hospitals blend intraoperative CT and neuronavigation, while telemedicine links extend consult reach into Pakistan and Bangladesh. Southeast Asian growth rides pediatric demand spikes and multi-lateral training partnerships. Japan and South Korea hover near saturation, but their aging installed base will demand replacement endoscopes and valves.

Europe remains steady, its universal health systems undergirding consistent procedure counts. Germany and the United Kingdom steer volumes, with the NHS favoring conservative follow-up for asymptomatic cysts. Eastern European states are investing in hybrid theatres to stem outbound medical migration. South America is gradually assembling pediatric neurosurgery muscle, led by Brazil and Argentina, though reimbursement gaps still limit cross-border device adoption, moderating the regional share of the arachnoid cysts treatment market.

Competitive Landscape

The arachnoid cysts treatment market hosts a moderately concentrated roster: Medtronic, Integra LifeSciences, and Aesculap control most shunt and endoscope revenue, benefiting from entrenched surgeon training modules and hospital service contracts. Integra’s AURORA Surgiscope leverages single-use sterility to claim infection-control mindshare, while Aesculap’s proSA Valve capitalizes on dual-pressure programmability. Medtronic maintains reach via its global CSF management catalog and coding assistance guides.

Disruptive potential lies in pediatric-scaled 4 mm scopes, biodegradable fenestration stents, and microfluidic artificial granulation valves now in pre-clinical testing. Entry barriers stay high; FDA 510(k) and EU MDR filings require bench and animal data plus validated manufacturing quality systems. Instead of price wars, incumbents court neurosurgeons with symposium sponsorships and on-site OR training, shoring up loyalty and stabilizing average selling prices across the arachnoid cyst treatment market.

Arachnoid Cysts Treatment Industry Leaders

Medtronic Plc

Integra LifeSciences Corporation

GE Healthcare

Boston Scientific Corporation

Aesculap, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medtronic received FDA clearance to expand its Stealth AXiS platform for cranial and ENT procedures. This system integrates AI to automatically generate brain maps and visualize critical neural pathways, which is vital for planning safe access to arachnoid cysts.

- November 2025: Tamil Nadu opened India’s first public hybrid neurosurgery theatre, integrating 3D CT, microscope, ultrasound, and endoscopy in one suite.

- June 2025: Sophysa secured FDA clearance for external CSF drainage catheters, positioning the company against incumbents in temporary postoperative diversion.

Global Arachnoid Cysts Treatment Market Report Scope

As per the scope of the report, treatment for arachnoid cysts is primarily determined by whether the cyst causes symptoms or exerts significant pressure on the brain or spinal cord. Conservative treatment is generally suitable for small, asymptomatic cysts, though patients may be advised to avoid high-impact activities that could potentially cause a rare cyst rupture or hemorrhage. Surgical intervention becomes necessary when a cyst is large, growing, or symptomatic, potentially leading to complications like hydrocephalus (fluid buildup in the skull) or focal neurological deficits. Endoscopic cyst fenestration is often the preferred surgical method due to its minimally invasive nature; it involves using a tiny camera and tools through a small burr hole to create openings in the cyst wall, allowing the trapped fluid to drain and be absorbed by the body.

The arachnoid cysts treatment market is segmented by type, treatment type, end-user, and by geography. Based on type, the market is segmented into intracranial arachnoid cysts and spinal arachnoid cysts. By treatment type, the market is segmented into endoscopic cyst fenestration, microsurgical fenestration (craniotomy), cystoperitoneal shunting, and observation / conservative management. By end users, the market is segmented into hospitals, ambulatory surgical centers, and specialty neurosurgery clinics. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Intracranial Arachnoid Cysts |

| Spinal Arachnoid Cysts |

| Endoscopic Cyst Fenestration |

| Microsurgical Fenestration (Craniotomy) |

| Cystoperitoneal Shunting |

| Observation / Conservative Management |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Neurosurgery Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Intracranial Arachnoid Cysts | |

| Spinal Arachnoid Cysts | ||

| By Treatment Type | Endoscopic Cyst Fenestration | |

| Microsurgical Fenestration (Craniotomy) | ||

| Cystoperitoneal Shunting | ||

| Observation / Conservative Management | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Neurosurgery Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big will the arachnoid cysts treatment market be by 2031?

The arachnoid cysts treatment market size is forecast to reach USD 2.5 billion by 2031, advancing at a 5.59% CAGR from 2026 to 2031

Which treatment generates the most revenue today?

Endoscopic cyst fenestration accounts for 61.89% of 2025 revenue, reflecting surgeon preference for minimally invasive approaches supported by hybrid OR imaging platforms.

What is the fastest-growing treatment modality?

Microsurgical fenestration is expanding at a 7.45% CAGR through 2031 because it excels in multiloculated or hemorrhagic cysts where direct visualization prevents recurrence

Which region offers the highest growth potential?

Asia-Pacific is projected to climb at a 7.45% CAGR through 2031, driven by public investment in hybrid suites and pediatric neurosurgery programs.

Page last updated on: