API Observability And Testing Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

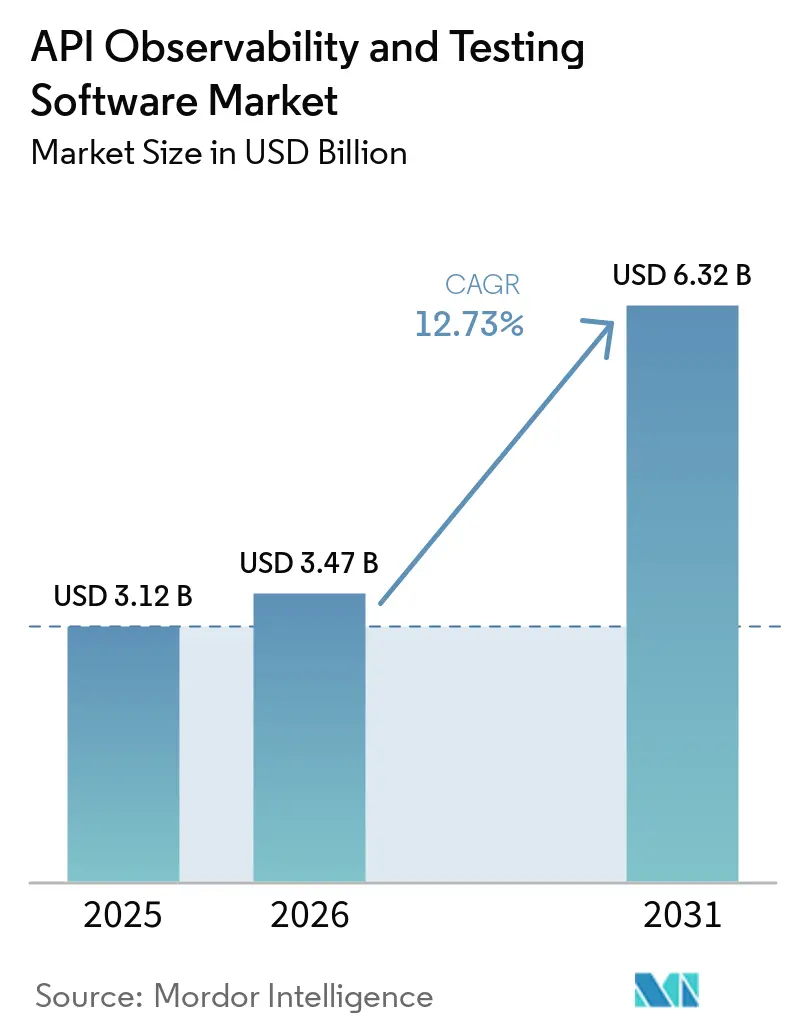

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 6.32 Billion |

| Growth Rate (2026 - 2031) | 12.73% CAGR |

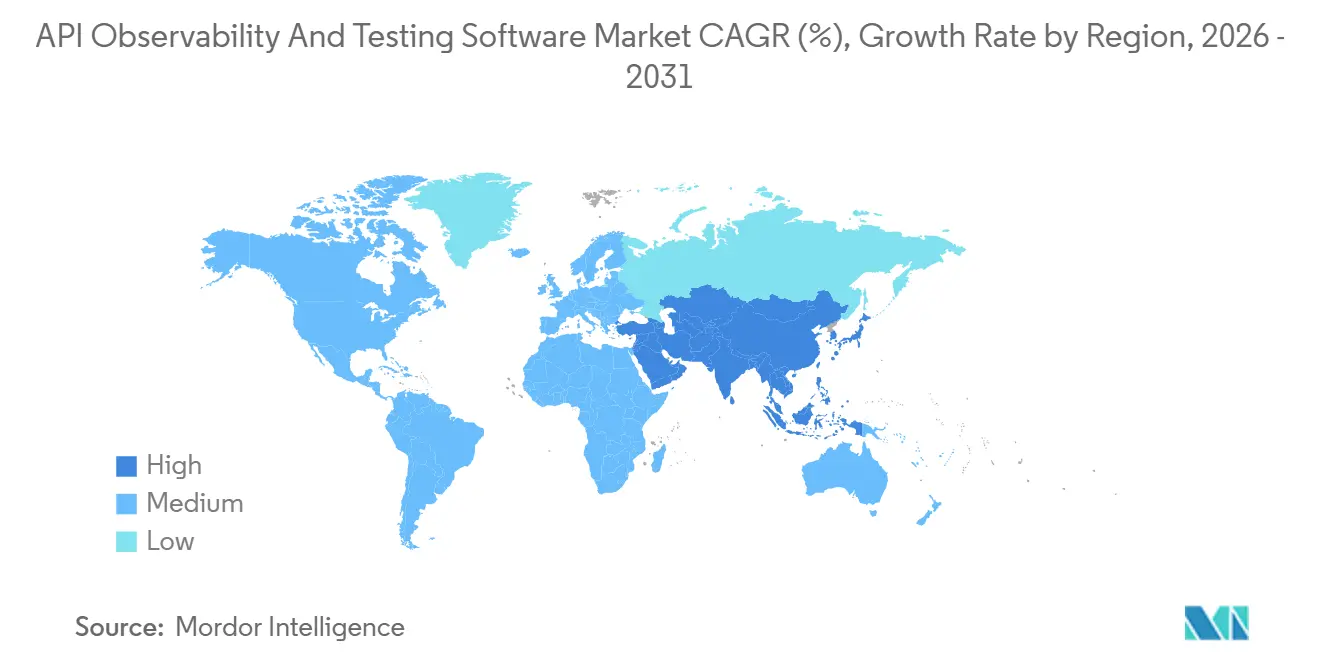

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

API Observability And Testing Software Market Analysis by Mordor Intelligence

The API observability and testing software market size is expected to grow from USD 3.12 billion in 2025 to USD 3.47 billion in 2026 and is forecast to reach USD 6.32 billion by 2031 at 12.73% CAGR over 2026-2031. Heightened exposure of microservices, rapid CI/CD cadences, and a doubling of endpoint-oriented breaches in 2025 have elevated automated validation from a developer convenience to a board-level risk-mitigation priority. Platform vendors are responding with AI-assisted test generation, per-endpoint consumption pricing, and tight integration with API gateways, helping enterprises compress release cycles without sacrificing quality. Small and medium enterprises are flocking to free tiers and low-code workflows, while heavily regulated verticals, notably healthcare and financial services, are treating API conformance as a compliance prerequisite. These converging forces sustain double-digit expansion even as tool sprawl, observability data inflation, and talent shortages remain structural headwinds.

Key Report Takeaways

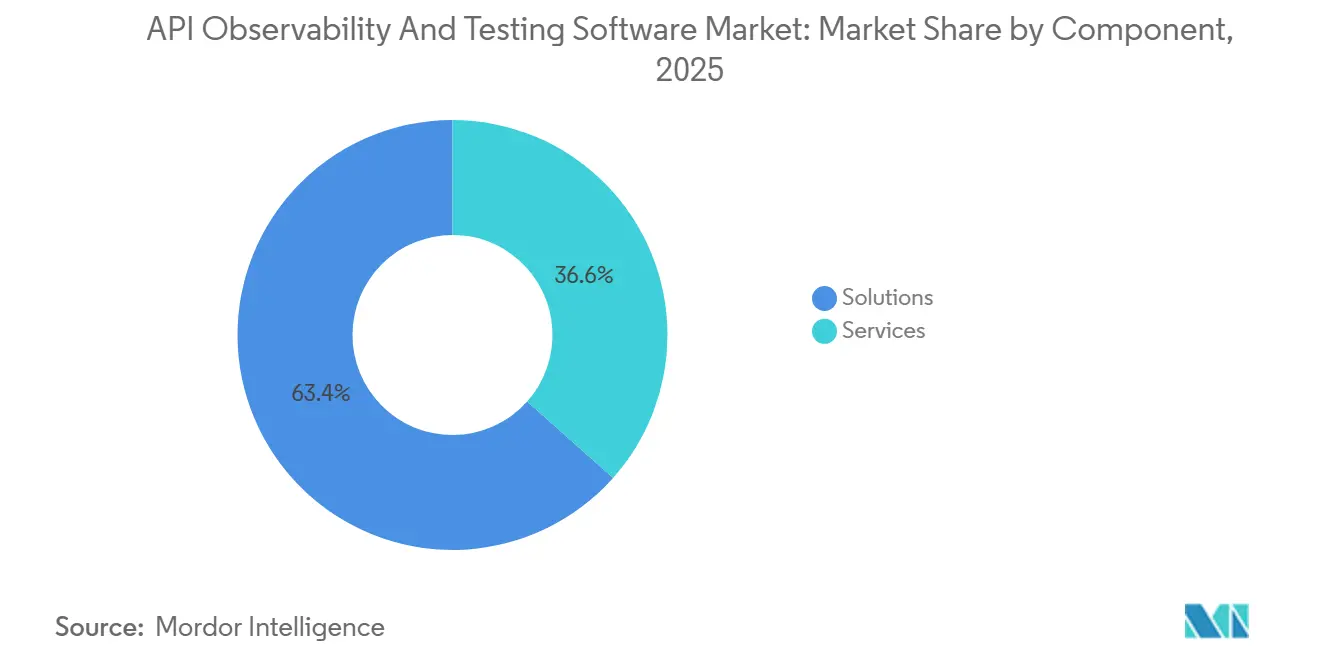

- By component, solutions led with 63.42% share in the API observability and testing software market in 2025, while services are projected to expand at a 13.57% CAGR through 2031.

- By deployment mode, cloud-based offerings accounted for 65.21% of 2025 revenue and are advancing at a 14.57% CAGR through 2031.

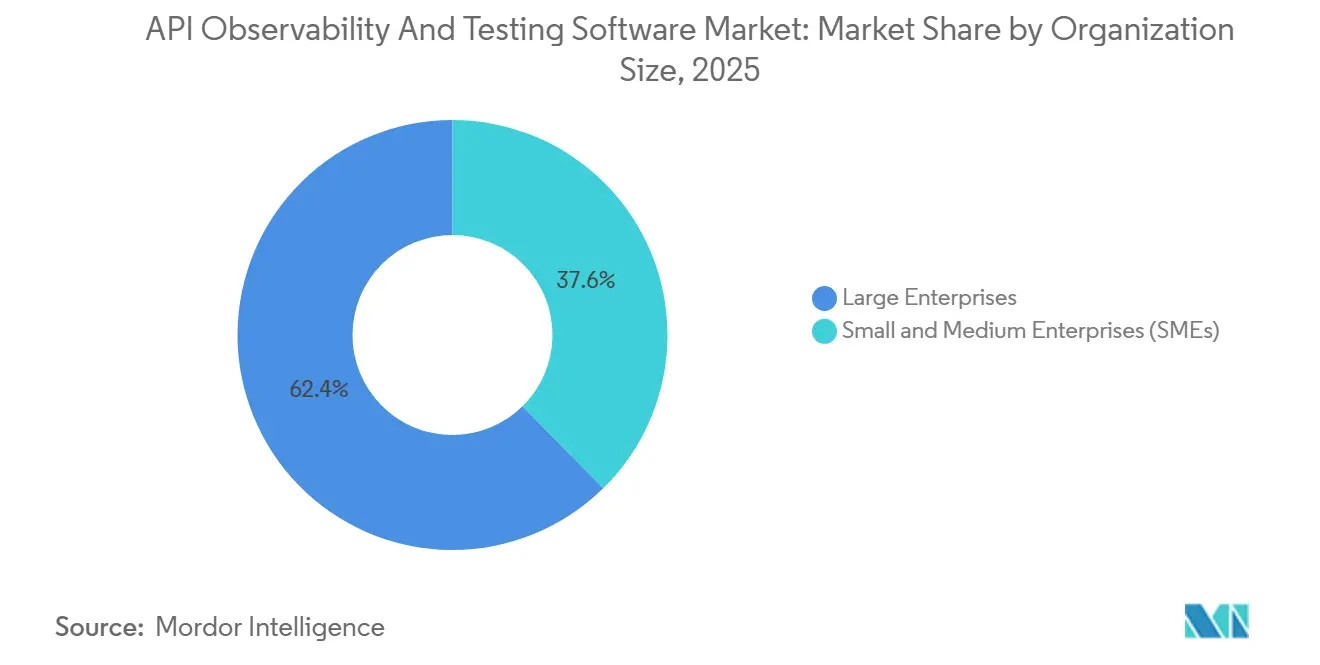

- By organization size, large enterprises held 62.3% share in 2025, yet small and medium enterprises are set to climb at a 16.15% CAGR through 2031.

- By end-user industry, IT and telecommunications contributed 23.11% of 2025 spending, whereas healthcare is forecast to grow fastest at a 15.37% CAGR.

- By geography, North America retained 34.70% share in 2025, while Asia-Pacific is poised for the highest regional growth at a 13.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global API Observability And Testing Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Microservices Architectures | +3.20% | Global, high in North America and Europe | Medium term (2-4 years) |

| Acceleration of CI/CD and DevOps Pipelines | +2.80% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising API Security Incidents and Compliance Mandates | +2.50% | Global, heightened in Europe and North America | Short term (≤ 2 years) |

| Expansion of Cloud-Native and Serverless Workloads | +2.10% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Low-Code and No-Code Test Automation Platforms | +1.20% | Global, faster uptake in SME-heavy regions | Long term (≥ 4 years) |

| Per-Endpoint Pricing Models Driving SME Uptake | +0.90% | Global, strongest in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Microservices Architectures

Organizations are decomposing monolithic architectures into hundreds of loosely coupled services, each exposing multiple endpoints that require automated contract testing, schema validation, and distributed tracing. A single digital transaction can traverse 15-20 internal APIs, increasing system complexity and interdependencies. To manage this, development teams deploy service mesh integrations to detect latency spikes and error cascades in real time. Industries such as financial services, retail, and media streaming consider deep observability essential, as system downtime directly impacts customer trust, operational continuity, and revenue generation.[1]GitLab Inc., “2025 DevSecOps Survey,” ABOUT.GITLAB.COM

Acceleration of CI/CD and DevOps Pipelines

DevSecOps toolchains enable multiple daily code releases, requiring API testing cycles to complete within minutes rather than hours. Automated regression suites, contract testing, and security scans function as mandatory checkpoints across each pipeline stage, ensuring early detection of breaking changes before production deployment. This shift embeds quality and security directly into the development lifecycle. Additionally, compliance mandates from federal and defense agencies reinforce this approach by prohibiting deployments that fail pre-production API security validations, increasing the criticality of robust, automated testing frameworks within continuous integration and delivery environments.[2]Akamai Technologies, “State of the Internet Security Report 2025,” AKAMAI.COM

Rising API Security Incidents and Compliance Mandates

Attackers increasingly exploit APIs to bypass user interface controls, driving a rise in breach frequency and associated costs. In response, regulators enforce stricter requirements, such as quarterly penetration testing, detailed audit trails, and defined uptime thresholds, which necessitate continuous runtime monitoring. Organizations must demonstrate both security and operational resilience. In parallel, healthcare payers advancing toward Fast Healthcare Interoperability Resources compliance are investing in solutions to validate secure, reliable data exchange, further reinforcing the need for robust API monitoring, testing, and governance frameworks across production environments.[3]Amazon Web Services, “AWS re:Invent 2025 Keynote,” AWS.AMAZON.COM

Expansion of Cloud-Native and Serverless Workloads

Serverless functions, event-driven architectures, and Kubernetes clusters create highly dynamic execution patterns that legacy agent-based monitoring tools cannot effectively track. To address this, vendors deploy lightweight sidecars and OpenTelemetry collectors that continuously stream metrics, logs, and traces into centralized observability platforms. This approach enables real-time visibility across ephemeral workloads. As a result, factors such as cold-start latency, burst concurrency, and autoscaling thresholds emerge as critical performance indicators, directly influencing system reliability and end-user experience in distributed, cloud-native environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity with Legacy Systems | -1.8% | Global, acute in Europe and North America | Medium term (2-4 years) |

| Shortage of Skilled API Test Engineers | -1.5% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Observability Data Cost Inflation in Large-Scale Deployments | -0.9% | Global, concentrated in large enterprises | Medium term (2-4 years) |

| Tool-Sprawl Leading to Governance Challenges | -0.7% | Global, prevalent in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy Systems

Enterprises operating hybrid environments must manage REST, SOAP, GraphQL, and gRPC payloads across mainframes, middleware, and cloud native services. Only a minority use a unified platform to correlate such heterogeneous telemetry, forcing teams to rely on protocol-specific monitoring tools that increase operational overhead and extend mean time to recovery. Additionally, translating legacy COBOL copybook data structures into modern JSON formats introduces latency and new failure points. These complexities require dedicated monitoring pipelines, further fragmenting observability and making end-to-end performance tracking and incident resolution more difficult.

Shortage of Skilled API Test Engineer

Demand for contract-aware test automation talent exceeds supply by more than 3 times, driving salary inflation and delaying critical release cycles. This talent gap constrains organizations' ability to scale reliable API testing practices. At the same time, only a small share of enterprises conduct chaos experiments on APIs, despite their effectiveness in uncovering systemic vulnerabilities before they impact end users. While low-code testing platforms help reduce dependency on specialized skills, they still require structured onboarding and governance, limiting their ability to fully offset the shortage of experienced testing professionals.[4]Enterprise Strategy Group, “API Management Survey 2025,” ESG-GLOBAL.COM

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Complexity Outpaces In-House Capacity

Solutions accounted for 63.42% of API Observability And Testing Software Market revenue in 2025, indicating strong enterprise preference for platform-led adoption embedded within DevOps pipelines. Buyers prioritize scalability, integration with CI/CD workflows, and centralized governance, which favors licensed tools over fragmented approaches. In parallel, the services segment is expanding at a 13.57% CAGR, driven by demand for outsourced test-case development, execution, and continuous monitoring. Managed service providers are consolidating consulting, environment provisioning, and compliance oversight into subscription-based models, reducing internal resource constraints. For instance, Katalon introduced its 2026 MSP Program, accelerating onboarding timelines through AI-generated test libraries and pre-configured deployment frameworks.

The solutions ecosystem remains structurally fragmented across low-code platforms, enterprise-grade suites, and open-source tools, each targeting distinct user maturity levels. Low-code environments address skill gaps by enabling non-technical teams to design and execute tests, while enterprise platforms from IBM and SmartBear emphasize governance, observability, and lifecycle integration. Open-source tools such as Postman continue to serve as entry points for developers, but are increasingly commercialized via service providers offering SLA-backed support and customization. This layered ecosystem is expanding adoption across both large enterprises and mid-market digital-native firms, thereby increasing overall market penetration and spend.

By Deployment Mode: Cloud-Based Dominance Shows Elastic Value

Cloud-based deployment accounted for 65.21% of API observability and testing software market revenue in 2025 and is projected to expand at a 14.57% CAGR, driven by structural shifts toward SaaS consumption models. Cloud-native tools remove the need for upfront hardware investment, enable globally distributed load testing, and align pricing with actual API usage volumes, improving cost transparency. Despite this, on-premises deployments remain relevant in regulated sectors such as financial services, healthcare, and defense, where data sovereignty and compliance requirements mandate localized execution. Hybrid models are gaining traction as enterprises split workloads, running functional and scalability tests in the cloud while retaining sensitive data validation on-site to comply with frameworks such as DORA and FedRAMP.

Ecosystem integration with hyperscalers is further accelerating cloud adoption. Services like AWS API Gateway, Azure API Management, and Google Apigee provide native integrations that streamline authentication, reduce latency, and simplify deployment pipelines. Additionally, IBM API Connect enables centralized governance across multi-cloud environments through a federated runtime model, increasing platform stickiness. While legacy on-premises tools persist in niche use cases, the ongoing decline of enterprise-owned data centers and a broader shift toward OpEx-driven IT spending models are expected to sustain cloud dominance in the API observability and testing software market.

By Organization Size: SMEs Benefit From Per-Endpoint Pricing

Large enterprises accounted for 62.3% of the API observability and testing software market revenue in 2025, reflecting their ability to invest in integrated platforms and absorb higher licensing costs. These organizations prioritize governance, scalability, and compliance, often consolidating fragmented DevOps stacks comprising 7 or more tools into unified environments with embedded API testing capabilities. This consolidation reduces operational complexity and improves observability across distributed systems. In contrast, SMEs are emerging as the fastest-growing segment, expanding at a 16.15% CAGR, supported by consumption-based pricing models that significantly lower entry barriers and bypass lengthy procurement cycles.

Startups and mid-sized firms are leveraging freemium and low-cost tiers from tools such as Insomnia and qAPI to validate live API traffic at minimal cost, often below USD 100 monthly. This trend is particularly evident in high-growth digital ecosystems such as India’s fintech sector and Latin American e-commerce markets, where lean teams favor low-code interfaces and rapid deployment. The resulting bifurcation, with enterprises consolidating and SMEs experimenting, is expanding the total addressable market by driving adoption across both high-value and high-volume customer segments.

By End-User Industry: Healthcare Accelerates on Interoperability Rules

IT and telecommunications accounted for 23.1% of API observability and testing software market revenue in 2025, supported by early adoption of API-first architectures and mature DevOps practices. These organizations require continuous validation across high-volume, low-latency environments, sustaining consistent demand for testing and observability tools. Healthcare is the fastest-growing vertical, with a 15.37% CAGR, driven by regulatory enforcement on interoperability. Frameworks from the Centers for Medicare & Medicaid Services and the Office of the National Coordinator for Health Information Technology, alongside tools such as the Inferno conformance suite, are making API validation a compliance requirement. Payers and providers must now submit standardized test reports to maintain reimbursement eligibility, effectively linking API performance to licensure.

Banking and insurance are also scaling adoption due to open banking mandates and operational resilience requirements under DORA, which necessitate rigorous failure simulation and recovery testing. Retailers intensify API testing ahead of demand spikes to ensure transaction stability, while public sector agencies expand secure data exchange frameworks requiring OAuth-based validation, supported by bodies such as the United States Environmental Protection Agency. Manufacturing is integrating API testing into Industrial IoT environments to maintain synchronization between connected devices and MES platforms. As compliance obligations broaden across sectors, API testing is transitioning from a technical function to a regulatory and operational necessity, structurally increasing market depth and recurring spend.

Geography Analysis

North America accounted for 34.70% of the API observability and testing software market revenue in 2025, supported by mature DevOps adoption, high hyperscaler concentration, and strict regulatory frameworks such as the Health Insurance Portability and Accountability Act that elevate API quality standards. Federal agencies are expanding validation mandates, while Canadian financial institutions continue strengthening open-banking infrastructure. However, growth is moderating due to vendor consolidation as large enterprises rationalize supplier bases. Despite this, underpenetrated segments, including defense, state government, and industrial manufacturing, offer incremental opportunities, particularly as legacy systems transition to API-driven architectures.

Asia-Pacific is the fastest-growing region, with a 13.72% CAGR, driven by the rapid expansion of digital infrastructure and high API transaction volumes. India’s Unified Payments Interface, which processed over 100 billion transactions in 2025, underscores the scale of API dependency, underscoring the need for scalable, cloud-based testing solutions. China’s sovereign cloud policies favor domestic vendors, although international providers are entering through localized deployments and joint ventures. Meanwhile, Japan and South Korea are embedding API validation within smart manufacturing initiatives, and Australia is advancing compliance under its Consumer Data Right framework. Fragmentation in standards and localization requirements introduces execution complexity but sustains long-term demand.

Europe’s market trajectory is shaped by regulatory enforcement under DORA and stringent data governance requirements linked to the General Data Protection Regulation. Financial institutions across the United Kingdom, Germany, and France are investing in advanced testing frameworks to simulate cyber disruptions and validate recovery SLAs. Switzerland and Nordic countries are supporting cross-border payment integration, increasing demand for latency-sensitive API testing. South America, the Middle East, and Africa remain smaller in absolute terms but are scaling through SaaS-based pricing models. Initiatives such as Brazil’s Pix and Saudi Arabia’s digital government programs are reinforcing sustained adoption of API testing.

Competitive Landscape

The competitive landscape remains fragmented, with no single provider achieving dominant control, resulting in a landscape shaped by two distinct strategic approaches. Developer-centric platforms prioritize ease of use, rapid onboarding, and seamless integration into CI/CD pipelines, enabling faster adoption among engineering teams. In contrast, enterprise-focused vendors embed observability and testing capabilities within broader API management suites, appealing to organizations seeking centralized governance, unified billing, and tighter integration across the full API lifecycle.

AI-driven anomaly detection is emerging as a key differentiator across vendors, enabling correlation between request-level latency and backend system performance. This capability allows faster identification of bottlenecks and improves incident resolution efficiency. At the same time, specialized vendors are focusing on niche capabilities, such as service-mesh-native routing and advanced schema inspection, positioning themselves as complementary solutions rather than direct competitors to large enterprise platforms. This dynamic is accelerating consolidation as larger vendors expand integrated observability capabilities.

Edge computing and industrial IoT represent underpenetrated opportunities within the market. Lightweight monitoring agents designed for constrained environments are enabling observability at remote and distributed endpoints, including industrial equipment and retail infrastructure. As enterprises increasingly deploy workloads closer to end users, demand for decentralized monitoring solutions is expected to rise. Vendors that optimize for low latency, minimal resource consumption, and interoperability across edge environments are likely to gain early competitive advantage in these emerging deployment scenarios.

API Observability And Testing Software Industry Leaders

Postman, Inc.

SmartBear Software, Inc.

Tricentis GmbH

Micro Focus International plc

Parasoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Postman released an AI-based test-generation engine that mines historical traffic to propose high-coverage regression suites, cutting authoring time by 60%.

- February 2026: Kong finalized its purchase of Insomnia to bundle API design, testing, and runtime telemetry into one interface.

- January 2026: SmartBear unveiled ReadyAPI 4.0, adding live contract validation against OpenAPI and secure secret storage via HashiCorp Vault.

- December 2025: IBM teamed with Red Hat to auto-instrument APIs inside OpenShift Service Mesh clusters.

Global API Observability And Testing Software Market Report Scope

The API Observability and Testing Software Market comprises solutions that enable organizations to monitor, test, and optimize API performance, reliability, and security across development and production environments. These tools provide capabilities such as automated testing, distributed tracing, real-time monitoring, and analytics, supporting modern architectures, including microservices and cloud-native systems. The market also includes integrated platforms and services that help enforce API governance, ensure compliance, and improve system resilience across diverse deployment models, including cloud, hybrid, and on-premises environments.

The API observability and testing software market report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Retail and E-commerce, Government, Manufacturing, and Other End-User Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare |

| Retail and E-commerce |

| Government |

| Manufacturing |

| Other End-User Industries |

| North America | United States | |

| Mexico | ||

| Canada | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Switzerland | ||

| Benelux | ||

| Russia | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Kingdom of Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premises | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-User Industry | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare | |||

| Retail and E-commerce | |||

| Government | |||

| Manufacturing | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Mexico | |||

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Switzerland | |||

| Benelux | |||

| Russia | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| South America | Argentina | ||

| Brazil | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Kingdom of Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected revenue for the API observability and testing software market in 2031?

The API observability and testing software market is forecast to reach USD 6.32 billion by 2031 based on current growth trajectories.

How fast is the sector expanding between 2026 and 2031?

The market is set to grow at a 12.73% CAGR during the 2026-2031 period.

Which deployment mode is growing the quickest?

Cloud-based API testing platforms lead expansion with a 14.57% CAGR thanks to elastic scaling and consumption pricing.

Why is healthcare driving new demand for API testing?

U.S. interoperability mandates require payers and health IT vendors to run routine FHIR and SMART conformance tests, making validation a certification prerequisite.

What challenges slow wider adoption of API test automation?

Integration complexity with legacy SOAP systems and an ongoing shortage of skilled API test engineers both act as significant restraints on market growth.

Which regions offer the strongest future growth potential?

Asia-Pacific, propelled by India’s payments ecosystem and China’s sovereign cloud policies, is expected to record the highest regional CAGR at 13.72% through 2031.

Page last updated on: