Asia-Pacific Construction And Demolition Waste Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

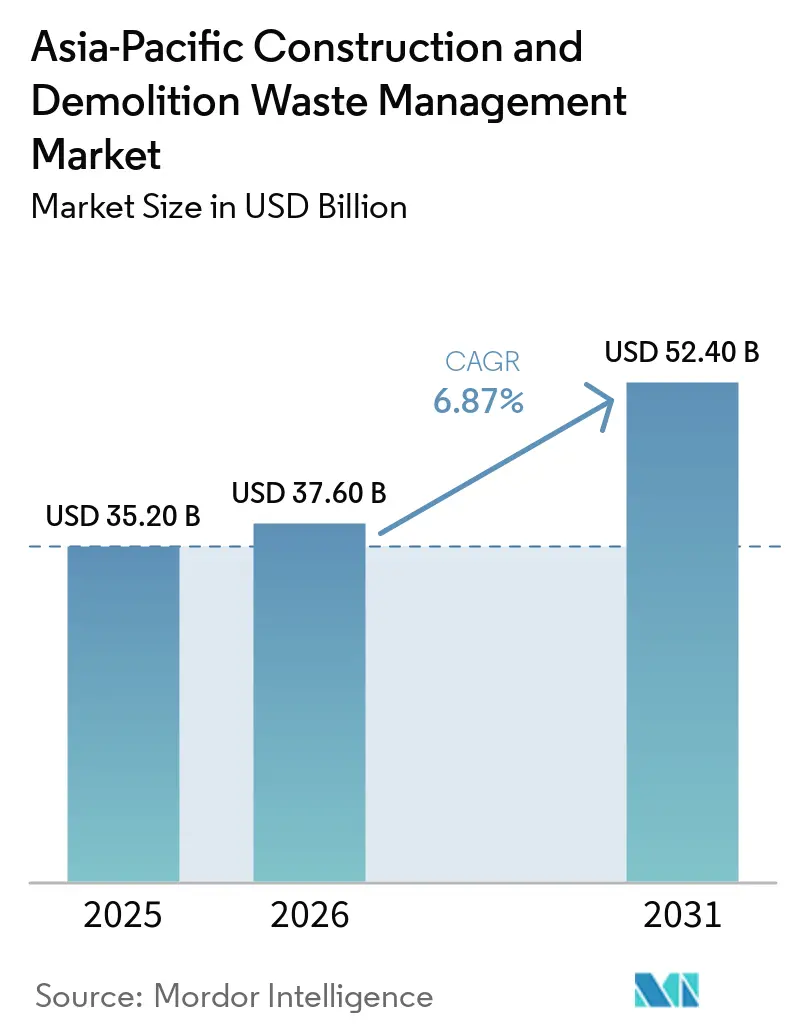

| Base Year Market Size (2025) | USD 35.20 Billion |

| Market Size (2026) | USD 37.60 Billion |

| Market Size (2031) | USD 52.40 Billion |

| Growth Rate (2026 - 2031) | 6.87% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Construction And Demolition Waste Management Market Analysis by Mordor Intelligence

The Asia-Pacific Construction And Demolition Waste Management Market size was valued at USD 35.20 billion in 2025 and is estimated to grow from USD 37.60 billion in 2026 to reach USD 52.40 billion by 2031, at a CAGR of 6.87% during the forecast period (2026-2031).

Sustained public spending on urban renewal and transportation networks supports steady demand for downstream recycling, sorting, and compliant disposal services in large cities and fast-growing secondary hubs. Tightening rules on segregation, traceability, and resource utilization are reshaping contracting models and boosting investment in material recovery infrastructure across the region. Municipal authorities are shifting to performance-based recycling targets, creating demand for operators with digital tracking and efficient processing. Aggregate scarcity in dense metros and circular procurement criteria in public works expand the addressable pool for quality-assured recycled products, especially for sub-base, backfill, and non-structural concrete applications. These shifts collectively reinforce the relevance of the Asia-Pacific Construction and Demolition Waste Management market across both mature and emerging jurisdictions.

Key Report Takeaways

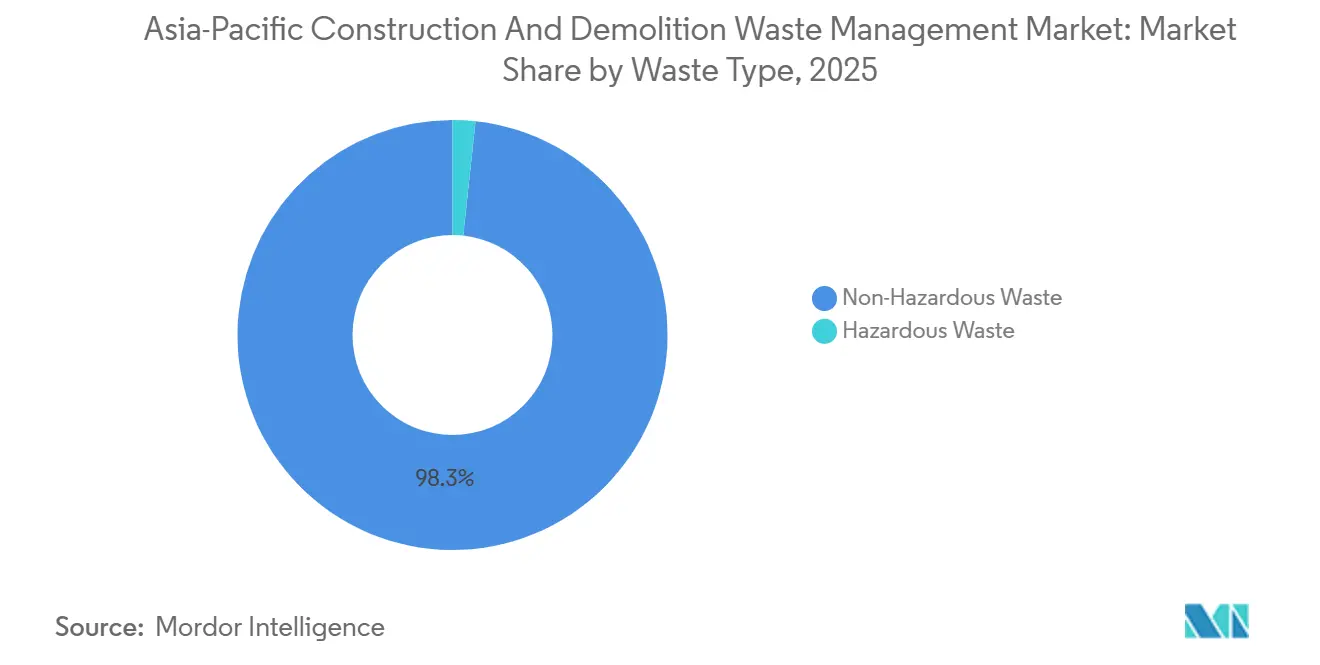

- By waste type, non-hazardous waste led the Asia-Pacific Construction and Demolition Waste Management Market size with 98.3% share in 2025, while hazardous waste recorded the fastest projected CAGR at 7.1% through 2026-2031.

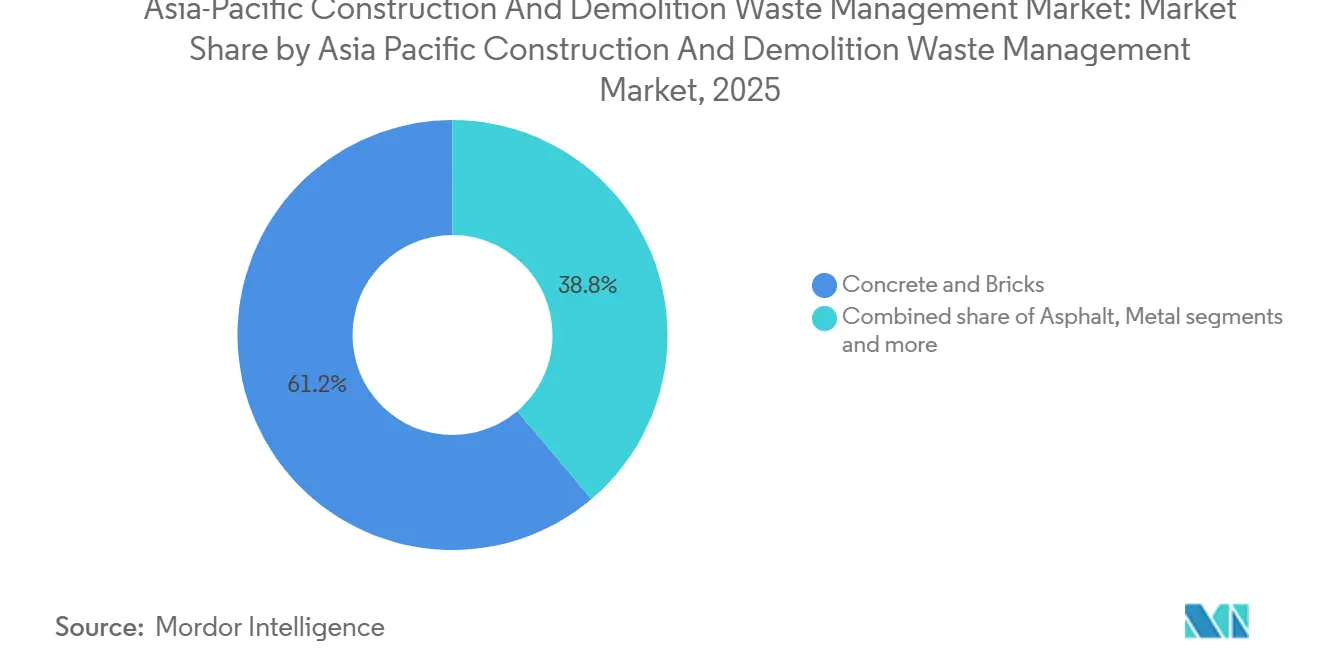

- By material, concrete and bricks held 61.2% Asia-Pacific Construction And Demolition Waste Management Market share in 2025, while the Others category grew fastest at a 7.3% CAGR through 2031.

- By service, landfilling and disposal accounted for 41.7% revenue share in 2025, while recycling and material recovery are projected to expand at a 6.9% CAGR to 2031.

- By geography, China led with 57.3% share in 2025, while India is projected to post the highest CAGR at 7.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Construction And Demolition Waste Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Urbanization and Mega Infrastructure Development | +1.8% | China's core cities, India's metros, ASEAN capitals | Medium term (2-4 years) |

| Government Circular Economy and Zero Waste Policies | +1.5% | China, Singapore, Vietnam, Taiwan | Long term (≥ 4 years) |

| Aging Building Stock Demolition in Mature Markets | +1.2% | Japan, South Korea, Australia | Medium term (2-4 years) |

| Environmental Pollution Concerns from Illegal Dumping | +0.9% | India, Vietnam, Philippines | Short term (≤ 2 years) |

| Smart City Sustainable Waste Integration | +0.7% | Singapore, China tier-1, India urban programs | Medium term (2-4 years) |

| Natural Aggregate Shortages in Dense Urban Areas | +0.8% | Singapore, India, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Mega Infrastructure Development

Urban growth across Asia is producing large amounts of demolition debris, excavation soil, and renovation waste. This increase is boosting the need for proper waste management services in the Asia-Pacific Construction and Demolition Waste Management market. Governments in major economies are encouraging waste producers to sort materials and ensure traceable transport, driven by policy-backed projects. This shift highlights the rising role of digital tools and on-site processing. In China, new rules for managing construction waste focus on sorting at the source and reusing materials during projects. This approach connects construction progress with recycling goals and uses multi-agency enforcement to prevent illegal dumping. By setting reuse targets and monitoring requirements, businesses are finding more reasons to adopt mobile crushing, screening, and precise sorting methods. These practices cut down on long-distance transport and support markets for recycled materials. As cities grow denser, limited access to active sites is making modular equipment and phased logistics more popular. These solutions help move materials quickly from job sites to approved recovery centers. This shift is aligning the growth of collection, sorting, and recycling systems with real-time monitoring, supported by national and local platforms in China. [1]State Council of the People’s Republic of China, “Notice on Printing and Distributing the Action Plan for Comprehensive Governance of Solid Waste,” State Council, gov.cn

Government Circular Economy and Zero Waste Policies

By 2030, Chinese central and municipal authorities aim to comprehensively utilize bulk solid waste and standardize construction waste governance. These initiatives bolster the long-term demand for services like recycling, sorting, and traceable hauling. The State Council's 2025 action plan, along with its operational guidance, emphasizes the classified treatment of construction waste, promotes green construction practices, and mandates the integration of waste reduction costs into project budgets. Meanwhile, Vietnam's national circular economy action plan aims for high collection rates and formalizes extended producer responsibility in sectors linked to building materials, enhancing segregation and downstream processing. In China, corporate operators are collaborating with local governments to launch digital platforms that monitor waste inflows and outflows, optimizing recovery. These collaborations establish new benchmarks for reuse rates and product conversion. Taiwan is witnessing cross-sector initiatives that enhance the recovery of inorganic resources, repurposing them for uses like asphalt aggregates and controlled low-strength material. This not only stabilizes end-use outlets for recycled content in construction but also tightens the alignment between regulatory targets, public procurement, and technology adoption. Such concerted efforts fortify the Asia-Pacific Construction and Demolition Waste Management market.

Aging Building Stock Demolition in Mature Markets

In Japan, high recycling performance for concrete, asphalt, wood, and metals is supported by long-standing laws that require separation and recovery planning for construction and demolition activities. City-scale studies show that concrete blocks dominate the material mix and that the recycling pathway for masonry, metals, and wood can reduce lifecycle emissions relative to manufacturing entirely from virgin inputs when system design and logistics are optimized. The consistent focus on selective dismantling, strict contractor obligations, and downstream quality control improves the yield of usable aggregates and feedstocks for engineered products. Hong Kong’s public sector operates a dedicated crushing plant that turns sorted concrete and rock into recycled rockfill and encourages on-site sorting through standard demolition protocols, which links urban renewal with circular material flows in a constrained land environment. The maturation of advanced processing, standardized quality benchmarks, and reliable offtake outlets sustains high diversion rates in these markets and offers models for other dense cities that seek to raise recycled aggregate penetration. These practices reinforce technology adoption and compliance-led contracting across the Asia-Pacific Construction and Demolition Waste Management market. [2]Civil Engineering and Development Department, “Recycling of Construction & Demolition (C & D) Materials,” CEDD, cedd.gov.hk

Environmental Pollution Concerns from Illegal Dumping

Municipal regulations increasingly mandate surveillance, electronic waybills, and pre-check forms at jobsite gates to deter illegal dumping and to reinforce traceability in the handling of construction debris. Shanghai codified these requirements and introduced a clear fine framework, which shifts behavior toward compliant collection, transport, and processing. As penalties tighten and multi-agency enforcement becomes more active, contractors face stronger incentives to use licensed carriers and qualified facilities. These measures reduce environmental harms linked to indiscriminate dumping, including siltation and flood risk near waterways, while improving public confidence in redevelopment programs. The policy emphasis on oversight and documented chains of custody supports the adoption of digital tools and centralized dashboards for authorities and service providers. This compliance architecture creates a more level playing field for operators that invest in sorting and recovery capabilities in the Asia-Pacific Construction and Demolition Waste Management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weak Regulatory Enforcement in Developing Nations | -0.8% | Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Low Tipping Fees Favoring Landfill Disposal | -0.6% | Malaysia, India, Thailand | Short term (≤ 2 years) |

| Limited Recycling Infrastructure in Emerging Economies | -0.9% | India, Indonesia, Philippines | Long term (≥ 4 years) |

| Cultural Preference for Virgin Materials | -0.5% | Regional intensity varies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak Regulatory Enforcement in Developing Nations

In several emerging markets, uneven enforcement of construction waste rules and licensing requirements can limit diversion and slow investment in advanced recovery lines. Authorities have started to strengthen oversight through joint inspections, electronic documentation, and penalties, but consistent implementation remains a work in progress in some provinces and municipalities. China’s recent guidance formalizes inter-departmental enforcement and the use of surveillance and e-waybills for construction waste, which illustrates how digital governance can curb leakage and improve compliance. Where digital tracking is not fully deployed, gaps may persist in first-mile collection and transfer, which reduces the capture of higher-value fractions and constrains revenues for material recovery operators. As regulators expand audits and standardize reporting, private service providers can better align capacity with policy direction and secure long-term contracts. Continued progress in monitoring and enforcement will support recovery targets and reduce illicit dumping risk in the Asia-Pacific Construction and Demolition Waste Management market.

Low Tipping Fees Favoring Landfill Disposal

Where landfill gate fees remain low relative to processing costs, project owners can default to disposal rather than invest in sorting and recycling, which dampens secondary material supply. Some jurisdictions are beginning to recalibrate incentives through higher levies on non-recoverable fractions and tighter methane controls to reflect lifecycle emissions more transparently. Local rules in China are increasing the cost of non-compliance by requiring documented handling and imposing fines for violations, which encourages a shift from disposal-first to resource-first behavior at construction sites. Digital supervision and joint enforcement also raise the likelihood of detection, which reduces illegal diversion to low-cost dumps and strengthens throughput at licensed facilities. As fee structures evolve and compliance audits become more routine, the relative economics for recycling improve, particularly where recycled products have established offtake channels in public works. These changes favor integrated operators that can combine collection, sorting, and product certification across the Asia-Pacific Construction and Demolition Waste Management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Waste Type: Infrastructure Recycling and Regulatory Enforcement

In 2025, non-hazardous waste dominated the scene, capturing a 98.3% share. This dominance, driven by materials like concrete, brick, soil, asphalt, and timber from demolition and renovation activities, continues to shape investment priorities in the Asia-Pacific Construction and Demolition Waste Management market. Assessments in Japanese cities reveal that concrete blocks lead the non-hazardous stream. Moreover, structured separation techniques boost yields for aggregates, metals, and wood. Public agencies with dedicated crushing capacities have shown that, with high-quality upstream sorting, concrete and rock can be recycled into engineered fill for infrastructure and reclamation projects. However, these recycling pathways hinge on efficient logistics management and quality assurance processes that check for gradation, contaminants, and performance standards. Mobile pre-processing at sites offers significant advantages for non-hazardous streams, cutting down haul distances and ensuring a consistent feedstock size for downstream plants. Such efficiencies bolster the Asia-Pacific Construction and Demolition Waste Management market, aligning collection, sorting, and high-volume recycling with policy-driven utilization goals.

While hazardous waste made up a mere 1.7% share in 2025, it's set to grow at a robust 7.1% CAGR through 2031. This growth is largely due to heightened enforcement on materials like asbestos, lead-based coatings, and contaminated soils in the Asia-Pacific Construction and Demolition Waste Management market. Regional regulators have tightened asbestos handling rules, with some areas outright banning it and mandating licensed contractors for its removal, transport, and disposal. Highlighting the issue, health authorities in Indonesia have pointed out the ongoing use of asbestos-containing materials and the resultant public health challenges, bolstering the case for future restrictions and the need for specialized disposal facilities. In markets with stringent compliance, practices like clear labeling, chain-of-custody controls, and dedicated landfill cells or treatment routes have become the norm. As monitoring intensifies and enforcement tightens, the identification and routing of hazardous waste volumes improve, enhancing safety and minimizing cross-contamination with non-hazardous processing lines. Such measures not only boost compliance but also open doors for specialized services in the Asia-Pacific Construction and Demolition Waste Management market.

By Material: Concrete Dominance Coexists with Others Segment Innovation

In 2025, concrete and bricks commanded a 61.2% share of materials, mirroring their dominance in Asian construction and renovation activities. This prevalence plays a pivotal role in shaping capacity planning within the Asia-Pacific Construction and Demolition Waste Management market. A city-scale study in Japan underscores concrete's prominence in incoming waste and highlights the notable carbon advantages of recycling over certain virgin outputs, given feasible logistics. In Hong Kong, public sector facilities are transforming sorted concrete and rock into graded recycled rockfill. This not only aids civil projects but also alleviates the pressure on primary aggregate supplies. To broaden the applications of recycled aggregates, it's crucial to establish clear specifications and acceptance criteria, with quality control integrated into demolition and recovery processes. With enhanced upstream sorting, metals and asphalt see heightened recovery rates, and their stable markets bolster facility economics. As product certification and procurement standards evolve, they pave the way for premium applications, enriching the revenue landscape of the Asia-Pacific Construction and Demolition Waste Management market.

The Others segment, encompassing plastics, wood composites, and glass, is set to lead with a robust 7.3% CAGR growth rate until 2031. This surge is attributed to advancements like optical sensors, AI-driven sorting, and wet washing systems, which elevate feedstock purity for engineered products. In China, digital platforms are streamlining site and transport oversight, enhancing material quality at municipal facilities, and bolstering the reuse of bricks, curbstones, and road bedding. Across the Asia-Pacific, company-driven recycling initiatives are channeling both post-industrial and post-consumer plastics into construction, reinforcing a commitment to circularity. As facilities refine their separation techniques for mixed materials, the resulting residual stream diminishes, yielding more uniform outputs suitable for biomass fuels or secondary raw materials. This technological evolution is vital for maximizing yields from mixed inputs and aligns with heightened utilization goals in public contracts. The synergy of digital oversight, sophisticated sorting, and market development amplifies the potential for the Others segment in the Asia-Pacific Construction and Demolition Waste Management arena.

By Service: Landfilling Leads Revenue, Recycling Captures Growth Momentum

Landfilling and disposal accounted for 41.7% of service revenue in 2025 because many cities remain in transition toward high recovery, and this mix continues to shape investment timing and logistics strategies across the Asia-Pacific Construction and Demolition Waste Management market. Chinese regulators now require classification at source, video surveillance at site exits, and electronic waybills for waste shipments. These measures reduce informal disposal and increase throughput at licensed facilities. The same guidance formalizes joint enforcement, heightens penalties for violations, and integrates project-level waste reduction costs into budgets, which tilts incentives toward recycling or engineered treatment where capacity is available. Municipal plants in select cities demonstrate how recycled aggregates can be directed into public works, which stabilizes demand for recovered products and improves landfill diversion rates. As methane controls tighten and landfill capacity constraints become more visible, fee structures and compliance requirements will keep shifting the service mix. These drivers collectively support long-run share gains for recovery-focused services within the Asia-Pacific Construction and Demolition Waste Management market.

Recycling and material recovery are projected to expand at a 6.9% CAGR through 2031 as utilization targets, circular procurement criteria, and corporate decarbonization plans converge. China’s national guidance sets resource utilization expectations for construction waste and codifies oversight tools that improve input quality at recovery plants. Industrial parks and joint ventures are rolling out digital platforms that track material flows and convert recycled aggregates into finished products that meet municipal specifications. In parallel, development-backed projects in underserved markets are adding resource recovery capacity designed to divert mixed waste and produce standardized outputs for local construction, agriculture, and manufacturing. These shifts are reinforced by city-scale evidence on emissions benefits from recycling and by public sector demonstrations of recycled rockfill, which together strengthen the case for recycled content in public tenders. As these practices scale, the Asia-Pacific Construction and Demolition Waste Management market captures more value from recovery while shrinking residual disposal needs.

Geography Analysis

China plays a central role in the Asia-Pacific Construction and Demolition Waste Management market, driven by national efforts to improve solid waste governance. These efforts include clear guidelines for classifying, supervising, and reusing construction waste. The State Council's action plan sets a goal to fully utilize bulk solid waste by 2030 and requires project budgets to account for waste reduction costs, encouraging more resource-efficient delivery models. Recent instructions from the General Office of the State Council provide practical steps for waste classification, digital tracking, and joint enforcement to tackle illegal dumping and improve municipal practices. In Shanghai, local rules now require video surveillance at construction-site exits and electronic waybills for transport, strengthening oversight and discouraging violations through fines. As these policies take effect, city-level resource utilization goals align with procurement needs, creating a more reliable demand for recycled aggregates and engineered products. Private companies are working with municipalities to implement digital twins and AI-driven solutions in facilities, helping them meet performance and quality targets. These measures not only support compliance-driven growth but also reinforce China's leading position in the Asia-Pacific Construction and Demolition Waste Management market. [3]Shanghai Municipal Bureau of Justice, “Provisions of Shanghai Municipality on the Disposal and Management of Construction Wastes,” Shanghai Government, shanghai.gov.cn

India is the fastest-growing market in the Asia-Pacific Construction and Demolition Waste Management sector, thanks to its urban infrastructure projects and sanitation initiatives focused on cleaner cities and better resource use. While many cities are expanding their C&D processing capacities, long-term growth depends on better planning, improved waste segregation, and a formal market for recycled products. New regulations, set to take effect in 2026, will strengthen extended producer responsibility for large projects and require digital compliance through national platforms. Development finance has already helped improve urban waste systems, and additional funding tied to climate goals could speed up the development of recovery infrastructure. Public procurement policies that prioritize recycled content are also increasing demand for secondary aggregates and engineered materials. As compliance improves, contractors are adopting better practices for sorting and documenting waste from construction sites to processing plants. These changes position India for sustained growth in the Asia-Pacific Construction and Demolition Waste Management market.

Japan's strong regulatory framework and advanced recovery technologies set an example for other countries in Asia. The country achieves high recycling rates for key materials due to laws requiring separation, documentation, and certified handling. Research at the city level shows the carbon benefits of recycling materials like concrete, metals, and wood, especially when transport and plant energy are optimized. This supports the adoption of similar practices in other urban areas. Both corporate and public projects are expanding the range of recycled-content products, including geopolymer alternatives and specialty aggregates that can reduce emissions. In Hong Kong, a public sector crushing plant demonstrates the scalability and reliability of recycled rockfill, highlighting the importance of proper sorting and quality control in demolition processes. Across the ASEAN region, circular economy initiatives and extended producer responsibility programs are gaining momentum. Vietnam's national action plan provides a clear roadmap for improving waste collection and recovery. Meanwhile, new resource recovery centers in underserved Pacific regions are helping divert mixed waste and produce standardized materials for local construction and manufacturing. Together, these developments reflect a regional shift toward performance-based waste management, supporting steady growth in the Asia-Pacific Construction and Demolition Waste Management market.

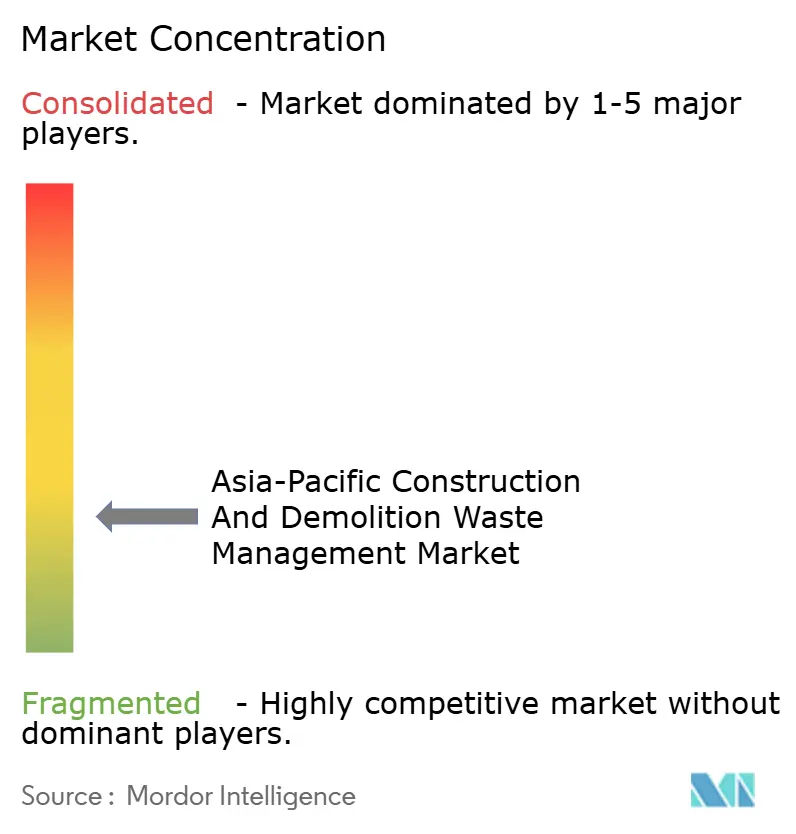

Competitive Landscape

The Asia-Pacific Construction and Demolition Waste Management market is shaped by integrated municipal programs, policy-backed procurement, and a mix of international and regional operators that combine collection, sorting, and recovery. In China, joint ventures are aligning digital supervision with plant operations to raise reuse rates and to convert recycled aggregates into standardized products for public works. These models rely on real-time data, AI-enabled analytics, and engineering know-how to improve quality and throughput. In Japan, companies participating in resource circulation demonstrations are scaling chemical and material recycling in coordination with government programs, which can expand feedstock outlets for plastics and composite materials from demolition workflows. Operators with multi-country footprints are investing in platforms and capacity expansions that position them for stronger offtake integration and for compliance-ready services in markets that are tightening enforcement. This progression supports network effects across sites and vehicles, which reduce unit costs and improve service reliability in the Asia-Pacific Construction and Demolition Waste Management market.

Technology providers are focusing on energy-efficient crushing, screening, and high-purity sortation to improve recycled aggregate quality and to meet contractor expectations. Public agencies that operate dedicated plants and publish specifications for recycled rockfill or aggregate help de-risk demand for secondary materials and establish market confidence. Digital twins and AI are being applied within waste-to-energy and recovery parks to balance loads, reduce downtime, and optimize maintenance, which raises asset productivity. Regulatory direction on classification and documentation at construction sites increases the value of licensed services that can ensure chain-of-custody integrity from jobsite to facility. These capabilities create competitive differentiation in bidding for long-term municipal contracts and enable operators to commit to higher diversion performance. Across priority markets, scale, compliance readiness, and technology adoption remain the principal levers of advantage in the Asia-Pacific Construction and Demolition Waste Management market.

Partnerships that connect municipal authorities, private operators, and development programs are expanding infrastructure where processing capacity has been limited. In the Pacific, new resource recovery centers are designed to divert mixed waste from landfills and to produce graded outputs that support local construction and agriculture. In Southeast Asia, national circular economy frameworks set direction for EPR and material recovery and provide a policy platform for project origination and finance. Across North Asia, corporate-led initiatives aligned with public goals are piloting advanced recovery for hard-to-recycle fractions, which diversifies revenue beyond core aggregates. As more jurisdictions codify reusable content in public tenders and reinforce monitoring, operators that combine logistics, advanced sorting, and certified products gain share. This evolution amplifies the importance of integrated platforms that can deliver credible data, consistent outputs, and reliable service levels across the Asia-Pacific Construction and Demolition Waste Management market.

Asia-Pacific Construction And Demolition Waste Management Industry Leaders

AESG

Wastech

Veolia

Metso

SUEZ Asia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SUS ENVIRONMENT completed its inaugural bilingual sustainability report, refreshed its visual identity, and outlined a ten-year growth strategy while winning multiple ESG recognitions.

- December 2025: China’s State Council issued the Solid Waste Comprehensive Management Action Plan with targets for the comprehensive utilization of bulk solid waste and integration of waste reduction costs into project budgets.

- November 2025: SUS Indonesia was named a qualified partner for a National Waste-to-Energy Initiative, with overseas projects progressing in parallel.

- November 2025: J&T Recycling and J Circular System joined Japan’s FY2025 Resource Circulation Systems Construction Demonstration Project for olefin and PET resin recycling in the Greater Tokyo Area

Asia-Pacific Construction And Demolition Waste Management Market Report Scope

The Asia-Pacific Construction and Demolition Waste Management Market is Segmented by Waste Type (Non-Hazardous Waste, and Hazardous Waste), by Material (Concrete & Bricks, Asphalt, Metal, Timber, Soil and Sand, Gypsum & Drywall, and Others), by Service (Collection & Transportation, Sorting & Segregation, Recycling & Material Recovery, and Landfilling & Disposal), and by Geography (China, Japan, India, South Korea, ASEAN, Australia, and Rest of Asia-Pacific). Forecasts are Provided in Terms of Value in USD.

| Non-Hazardous Waste |

| Hazardous Waste |

| Concrete & Bricks |

| Asphalt |

| Metal |

| Timber |

| Soil and Sand |

| Gypsum & Drywall |

| Others (Plastic, Wood, Glass) |

| Collection & Transportation |

| Sorting & Segregation |

| Recycling & Material Recovery |

| Landfilling & Disposal |

| China |

| Japan |

| India |

| South Korea |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) |

| Australia |

| Rest of Asia-Pacific |

| By Waste Type | Non-Hazardous Waste |

| Hazardous Waste | |

| By Material | Concrete & Bricks |

| Asphalt | |

| Metal | |

| Timber | |

| Soil and Sand | |

| Gypsum & Drywall | |

| Others (Plastic, Wood, Glass) | |

| By Service | Collection & Transportation |

| Sorting & Segregation | |

| Recycling & Material Recovery | |

| Landfilling & Disposal | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the Asia-Pacific Construction and Demolition Waste Management market size and growth outlook to 2031

The Asia-Pacific Construction and Demolition Waste Management market size is USD 35.2 billion in 2025, projected at USD 37.6 billion in 2026 and USD 52.4 billion by 2031, reflecting a 6.87% CAGR from 2026 to 2031.

Which service lines are gaining the fastest momentum across Asia-Pacific

Recycling and material recovery is projected to post a 6.9% CAGR through 2031, helped by utilization targets, circular procurement criteria, and stricter supervision that improves input quality and traceability.

Which materials dominate processed volumes in the region

Concrete and bricks led with 61.2% share in 2025, reflecting their prevalence in building stock and renovations, with asphalt and metals also recording strong recovery when sorting quality is high.

Which countries are setting the policy pace for construction waste management

China anchors policy momentum with comprehensive action plans and operating guidance on classification, tracking, and enforcement, while Japan and Hong Kong demonstrate high-performance recycling models and Vietnam advances a national circular economy plan.

What are the key barriers to faster adoption of recycled aggregates

Cultural preference for virgin materials, limited processing capacity in some markets, and uneven enforcement constrain adoption, though stronger standards, digital tracking, and circular procurement are improving acceptance.

How are hazardous fractions being handled within C&D flows

Jurisdictions that ban asbestos and require licensed contractors for removal, transport, and disposal are expanding specialized handling, and public health campaigns in Indonesia and elsewhere are building support for stricter asbestos controls.

Page last updated on: