Anhydrous Dibasic Calcium Phosphate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

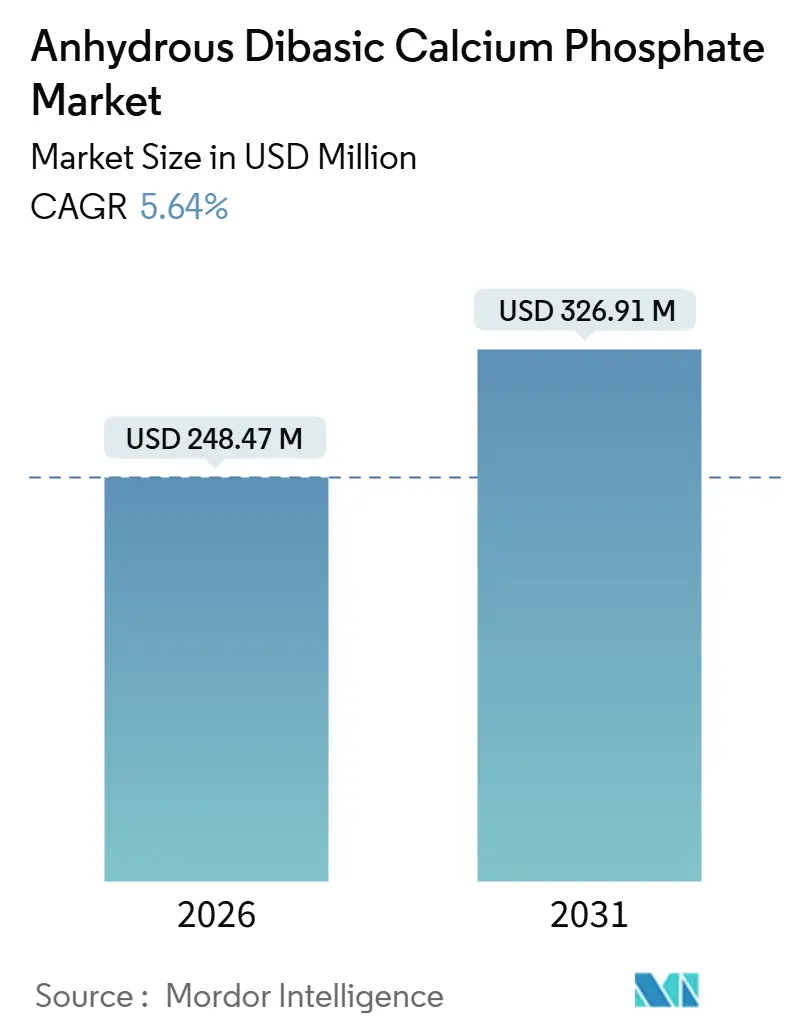

| Market Size (2026) | USD 248.47 Million |

| Market Size (2031) | USD 326.91 Million |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

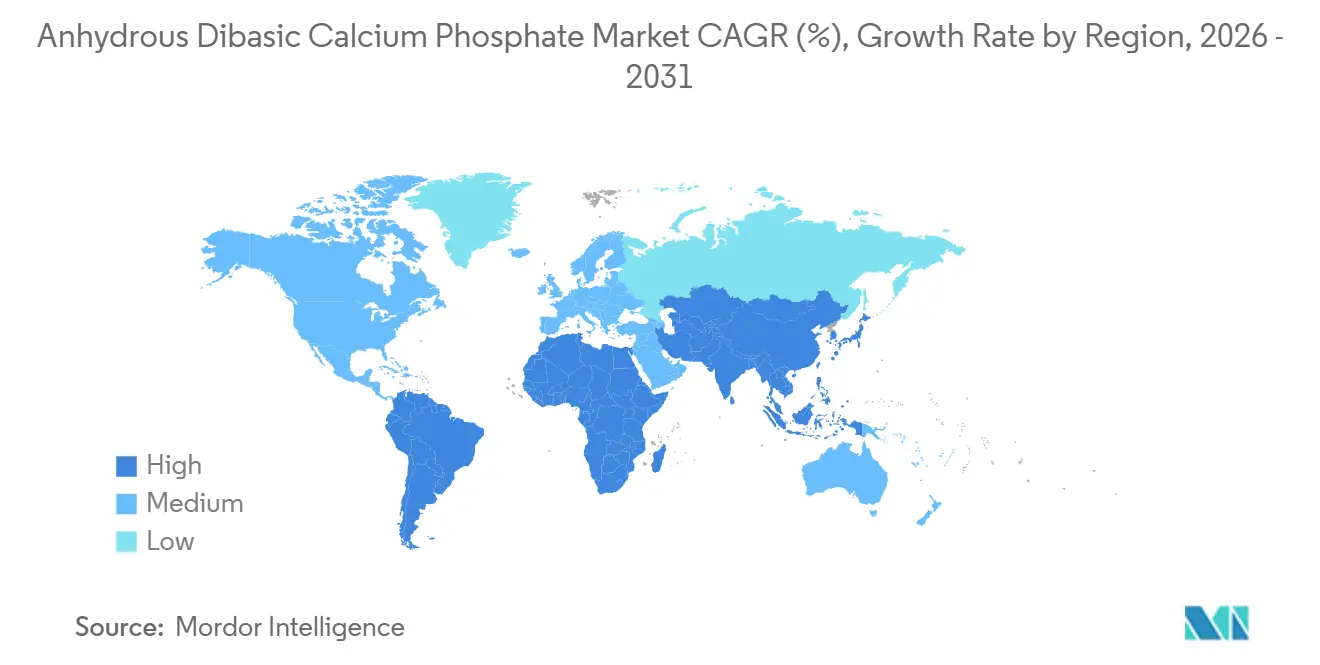

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

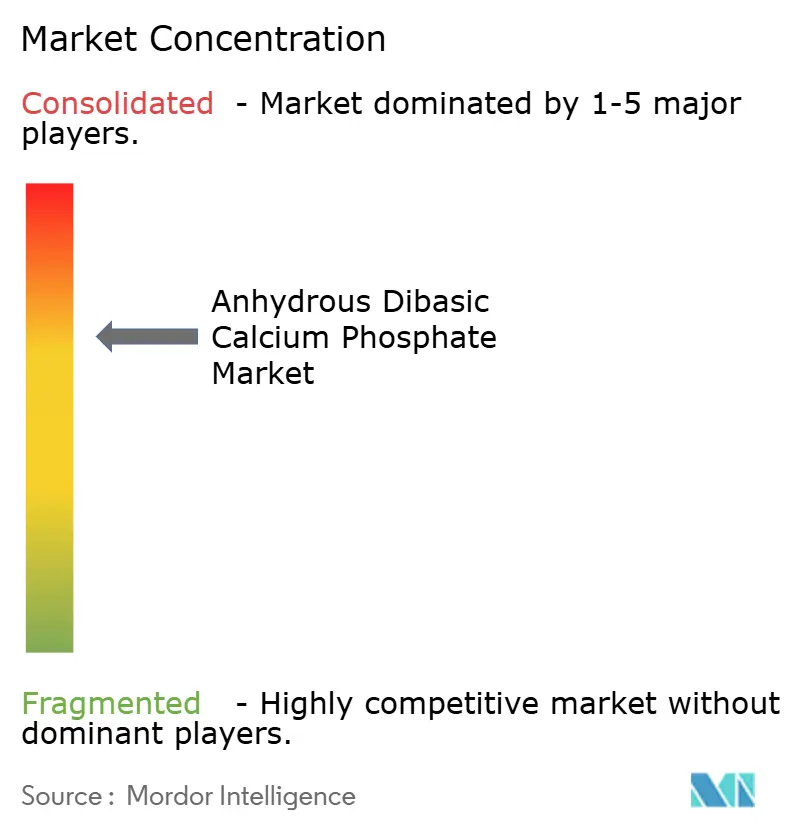

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anhydrous Dibasic Calcium Phosphate Market Analysis by Mordor Intelligence

The Anhydrous Dibasic Calcium Phosphate Market size is estimated at USD 248.47 million in 2026, and is expected to reach USD 326.91 million by 2031, at a CAGR of 5.64% during the forecast period (2026-2031).

Rising demand for moisture-stable excipients in solid-dose pharmaceuticals, growing consumer affinity for bone-health nutraceuticals, and capacity additions in Asia-Pacific underpin this expansion of the anhydrous dibasic calcium phosphate market. Suppliers that invested early in advanced milling technology are benefiting from the United States Pharmacopeia’s 2024 monograph revision, which tightened heavy-metal limits and mandated narrower particle-size distributions.[1]United States Pharmacopeia, “Dibasic Calcium Phosphate Anhydrous Monograph,” USP, usp.org Elevate phosphate-rock prices have encouraged vertically integrated producers to secure captive ore supplies, while mid-tier firms are differentiating through surface-modified grades that improve calcium release kinetics. Regulatory convergence around ICH Q3D impurity guidelines is amplifying demand for high-purity variants, especially among contract development and manufacturing organizations that run continuous tableting lines. At the same time, dairy-alternative brands are incorporating anhydrous calcium phosphate to match the nutritional profile of cow’s milk, broadening the addressable base for the anhydrous dibasic calcium phosphate market.

Key Report Takeaways

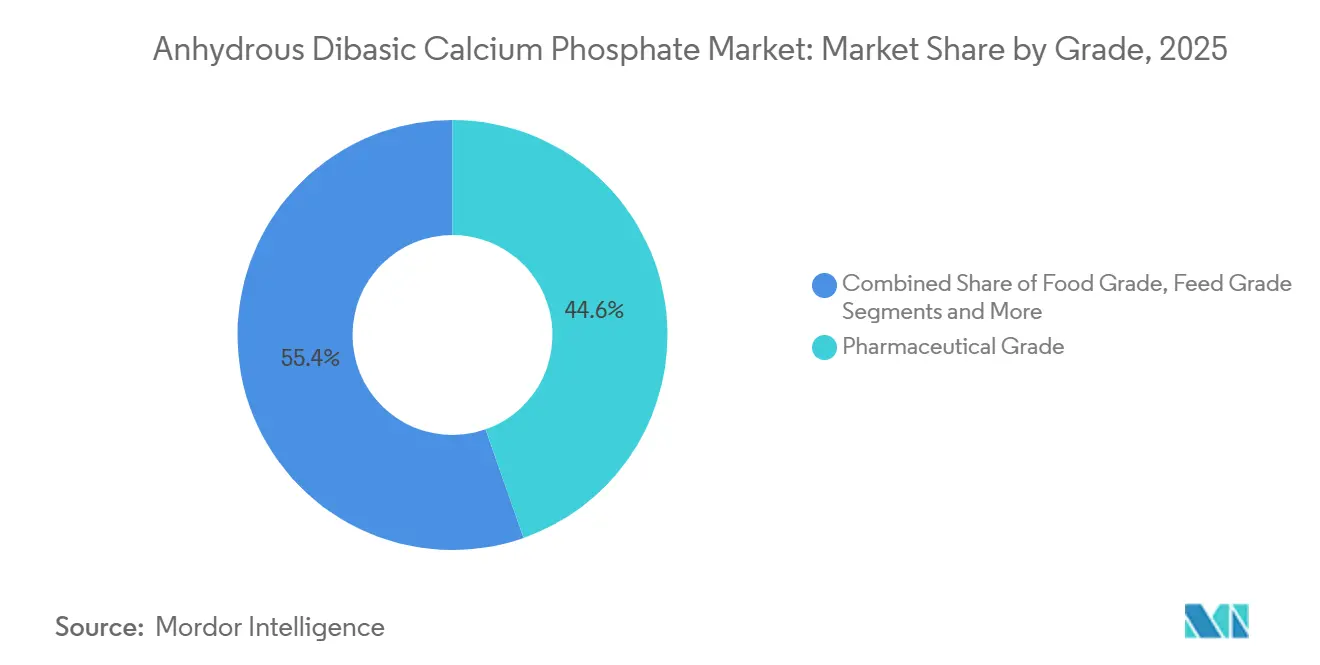

- By grade, pharmaceutical-grade material led with 44.63% revenue share in 2025, and it is projected to expand at a 9.24% CAGR through 2031 as compendial limits tighten.

- By application, nutraceutical supplements advanced at the fastest 9.79% CAGR, while pharmaceuticals retained 37.46% of 2025 demand.

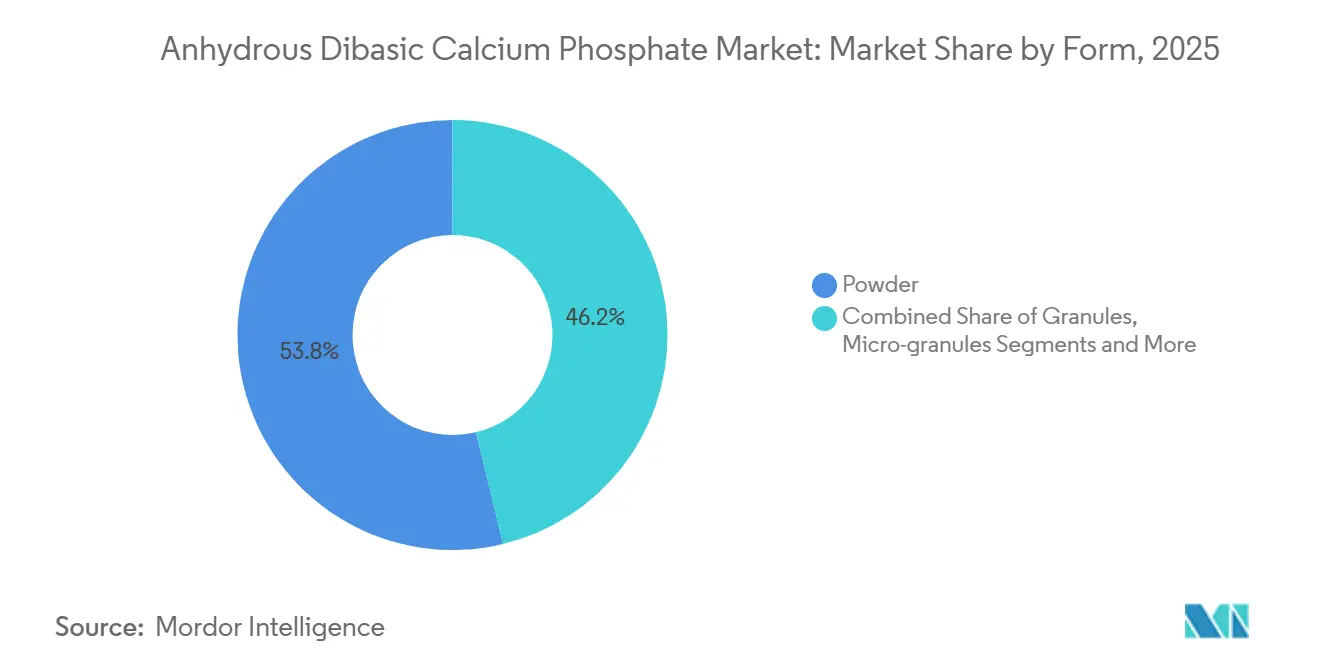

- By form, powder held 53.77% of 2025 volume; micro-granules are set to post an 8.41% CAGR to 2031 as high-speed tablet presses proliferate.

- By end-user industry, pharmaceutical manufacturers commanded 39.14% share in 2025, whereas nutraceutical producers are forecast to accelerate at an 8.92% CAGR through 2031.

- By geography, North America captured 32.65% of 2025 demand, while Asia-Pacific is poised to register the strongest 7.28% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anhydrous Dibasic Calcium Phosphate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Calcium-Fortified Food & Beverages | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Surge in Solid-Dose Pharmaceutical Production | +1.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of the Global Animal Feed Industry | +0.9% | Asia-Pacific, spill-over to South America | Medium term (2-4 years) |

| Growth in Nutraceutical Calcium Supplements | +1.3% | North America, Europe, Asia-Pacific emerging markets | Short term (≤ 2 years) |

| Shift From Dihydrate to Anhydrous Grade for Moisture-Sensitive APIs | +0.8% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Phosphate Recovery Technologies Lowering Input Costs | +0.6% | Europe, North America pilot projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Calcium-Fortified Food & Beverages

Food formulators are weaving calcium fortification into product reformulations to meet consumer expectations for functional nutrition. Anhydrous grades are preferred because they offer a neutral taste profile and high elemental calcium that does not precipitate during ultra-high-temperature processing. The Organisation for Economic Co-operation and Development urged member states in 2024 to harmonize calcium-fortification labeling, a step that standardizes ingredient requirements and rewards ISO 22000-certified producers.[2]Organisation for Economic Co-operation and Development, “Guidelines on Calcium Fortification Labeling,” OECD, oecd.org Dairy-alternative makers are using the material to replicate milk’s calcium content, while bakers adopt it as a leavening acid that avoids metallic off-notes. Together, these developments expand reach for the anhydrous dibasic calcium phosphate market.

Surge in Solid-Dose Pharmaceutical Production

Contract manufacturers are scaling solid-dose capacity to meet biosimilar launches and a swelling generic pipeline. The U.S. FDA cleared 47 new solid-dose formulations in 2024, up 12% from 2023, highlighting the sector’s momentum.[3]United States Food and Drug Administration, “New Drug Approvals and Regulatory Guidance,” FDA, fda.gov Anhydrous dibasic calcium phosphate functions both as a diluent and a disintegrant, enabling strong yet fast-dissolving tablets and simplifying scale-up to commercial lines. Southeast Asian plants attract investment as labor costs remain competitive and local regulators embrace ICH Q3D, which in turn drives local excipient sourcing. This dynamic fuels additional growth for the anhydrous dibasic calcium phosphate market.

Expansion of the Global Animal Feed Industry

Poultry and swine growers are boosting feed-conversion ratios, increasing phosphorus requirements and pushing demand for bioavailable calcium sources. The International Energy Agency observed that lithium-iron-phosphate battery growth is pulling material away from agriculture, tightening feed-grade supply. Producers choose anhydrous calcium phosphate because its low moisture reduces mycotoxin risks in humid storage. The shift from antibiotic growth promoters toward mineral premixes further elevates its role as both nutrient and carrier, reinforcing demand in the anhydrous dibasic calcium phosphate market.

Growth in Nutraceutical Calcium Supplements

Aging populations in North America, Europe, and Japan are consuming more bone-health tablets. The World Health Organization raised daily calcium intake targets for seniors to 1,200 mg in 2024, expanding multi-dose regimens. E-commerce is opening new channels for niche brands that stress clean-label formulations, forcing contract manufacturers to source non-GMO, allergen-free calcium phosphate. Sports-nutrition lines are also integrating the compound into powders and bars, adding another layer of growth for the anhydrous dibasic calcium phosphate market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Phosphate-Rock Prices & Supply | -0.9% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Stricter Environmental Rules on Phosphate Mining | -0.7% | China, Europe, North America | Medium term (2-4 years) |

| Product Substitution by Tricalcium Phosphate in Chewables | -0.4% | North America, Europe | Medium term (2-4 years) |

| Concerns over Nano-Contaminant Thresholds | -0.3% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Phosphate-Rock Prices & Supply

Phosphate-rock prices jumped 18% over 2024 due to export curbs in China and weather-related hits to Moroccan mines. Freight costs rose in parallel, squeezing margins for processors lacking captive ore. Vertically integrated majors can buffer swings, but specialty players that buy merchant acid remain exposed, which can slow capacity expansion in the anhydrous dibasic calcium phosphate market.

Stricter Environmental Rules on Phosphate Mining

China and the European Union tightened sulfur-dioxide and particulate limits for phosphoric-acid plants in 2024, mandating scrubber retrofits that cost USD 15-25 million per site. The U.S. EPA now requires baseline water-quality studies before mine openings, extending permitting by up to 18 months. Compliance raises conversion costs and could trim future supply to the anhydrous dibasic calcium phosphate market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Stricter Pharma Standards Unlock Premiums

Pharmaceutical-grade material held a 44.63% slice of 2025 revenue, and this segment is projected to expand at a brisk 9.24% CAGR through 2031. The anhydrous dibasic calcium phosphate market size for pharmaceutical-grade excipients rises because direct-compression systems demand tighter particle-size control and ultra-low heavy-metal content. USP’s 2024 monograph revision tightened arsenic and lead limits, prompting suppliers to install in-line spectroscopy and source ore from certified mines. As a result, many small producers cannot fund the necessary upgrades, consolidating supply. Premiums of 30-40% over food grades have become commonplace, and vertically integrated players are using these margins to bankroll R&D on surface-modified particles.

Beyond direct-compression tablets, high-purity grades are gaining ground in biologics, where they act as buffering agents in lyophilized vials. Food-grade material addresses fortification, yet buyers remain price-sensitive, capping upgrades. Feed-grade products compete with monocalcium phosphate on bioavailability and cost. Industrial-grade usage in ceramics and flame retardants is stagnant, limited by synthetic substitutes. Overall, regulatory harmonization is boosting the pharmaceutical slice of the anhydrous dibasic calcium phosphate market and elevating entry barriers.

By Application: Nutraceuticals Race Ahead

Nutraceutical supplements posted the fastest 9.79% CAGR to 2031, reflecting consumers’ shift from treatment to prevention. Personalized nutrition platforms that rely on genetic or microbiome testing are proliferating, and contract manufacturers must handle smaller batches and frequent SKU rotations. As a result, the anhydrous dibasic calcium phosphate market share tied to nutraceuticals is widening. Pharmaceutical applications, while mature, still represent 37.46% of 2025 value and benefit from biosimilar launches that demand ICH-compliant excipients. Food-and-beverage fortification is growing in emerging economies that legislate micronutrient enrichment to combat deficiencies. Feed additives expand in Asia-Pacific, where livestock output is rising to meet protein demand.

Pharmaceutical brands value excipient traceability, driving multi-year supply contracts. Nutraceutical newcomers use e-commerce to reach global buyers, placing speed-to-market over long validation cycles. Clean-label activism poses moderate resistance to intentional additives, but calcium phosphate’s natural origin and GRAS status shelter it. Overall, applications beyond pharma now set the growth pace for the anhydrous dibasic calcium phosphate market.

By Form: Micro-Granules Enable High-Speed Lines

Powder remained the default, claiming 53.77% of 2025 tonnage, yet micro-granules are expected to post an 8.41% CAGR through 2031. Continuous tablet-presses require flowable, dust-free excipients to keep die cavities filled at rotation speeds above 200,000 tablets per hour. Micro-granules deliver uniform bulk density that loss-in-weight feeders crave, elevating their pull within the anhydrous dibasic calcium phosphate market. The premium sits near 15-20%, but pharmaceutical producers are willing to pay to curb weight variation and slash rejects.

Food processors rely on powders for dairy drinks or bakery mixes because dispersion is straightforward. However, airborne dust raises occupational-health alarms, prompting gradual exploration of granulated alternatives. Granules provide intermediate flow but their irregular shape can segregate during blending, making micro-granules the preferred upgrade path in high-throughput pharma lines. These technical advantages underpin the micro-granule trajectory in the anhydrous dibasic calcium phosphate market.

By End-User Industry: Nutraceutical Firms Steal the Spotlight

Nutraceutical manufacturers are slated for an 8.92% CAGR through 2031, beating pharmaceutical firms that held 39.14% of 2025 demand. Direct-to-consumer supplement brands can launch products in months, not years, shaping a nimble segment of the anhydrous dibasic calcium phosphate market. Food-and-beverage processors are fortifying plant milk and bakery staples to differentiate commoditized SKUs, though margin pressure restrains ingredient premiums. Animal nutrition companies consolidate via M&A, with global majors buying regional premix specialists to secure distribution. Agricultural input suppliers stay niche because calcium phosphate’s solubility limits agronomic efficacy.

Pharmaceutical giants split into innovators prioritizing traceability and generics focused on cost. This bifurcation lets mid-tier suppliers carve a lane by offering pharma-grade material below multinational prices while maintaining compliance. Nutraceutical players are also testing gummies and effervescents, formats where calcium phosphate’s role is shifting from direct compression to structure or mouthfeel enhancement. Each trend reshapes demand dynamics across the anhydrous dibasic calcium phosphate market.

Geography Analysis

North America controlled 32.65% of the anhydrous dibasic calcium phosphate market in 2025, anchored by a mature pharmaceutical sector and strict fortification rules. The FDA sharpened impurity limits for supplements in 2024, compelling suppliers to document robust traceability. Canada’s aging population fuels bone-health tablets, while Mexico’s contract-manufacturing expansion lures multinational pharma players seeking cost-effective plants. Yet new phosphate-processing projects face permitting cycles of up to five years, limiting capacity growth and keeping the regional market concentrated.

Asia-Pacific is forecast to chart a 7.28% CAGR to 2031, the highest globally, as rising incomes and urbanization lift supplement consumption. China houses integrated phosphate complexes run by Hubei Xingfa and Wengfu, which supply both domestic and export customers. India’s Drug Controller General issued 120 new manufacturing licenses in 2024, fostering local demand for excipients. Japan and South Korea remain premium markets where clinically validated supplements command high price points. Emerging hubs such as Vietnam and Thailand capitalize on low labor costs and nearby ore deposits, solidifying Asia-Pacific’s role in the anhydrous dibasic calcium phosphate market.

Europe recorded strong but steadier growth. EFSA’s 2024 nano-guidance forces producers to invest in particle-size analytics, favoring large incumbents. Germany, France, and the United Kingdom dominate regional consumption through established pharma and nutraceutical channels. Southern Europe broadens fortification schemes to tackle deficiencies, and Middle East & Africa plus South America remain smaller markets. Still, Brazil’s livestock boom and GCC food-security drives open pockets of opportunity. Together, these geographies round out global demand for the anhydrous dibasic calcium phosphate market.

Competitive Landscape

The anhydrous dibasic calcium phosphate market is moderately fragmented. ICL Group, OCP Group, and Yara leverage vertical integration from mining to finished ingredients, shielding margins from phosphate-rock volatility. Regional specialists such as Prayon, BK Giulini, and Budenheim compete on technical service, offering customized particle distributions for direct-compression lines. Chinese producers, including Hubei Xingfa and Guizhou Zerophos, have increased export volumes while securing ISO 9001 and FSSC 22000 credentials to penetrate regulated markets.

White-space niches center on biologics-grade and surface-modified variants. Innophos upgraded its electron-capture-grade facility in 2024, targeting analytical applications that command premiums north of 50%. Patent activity shows emphasis on spray-drying to yield spherical particles with tight distribution, improving blend uniformity. Phosphate-recovery startups seek to extract calcium phosphate from wastewater, promising 20-30% raw-material savings once regulatory hurdles are cleared. The combination of integration advantages and innovation pipelines shapes competitive stakes in the anhydrous dibasic calcium phosphate market.

Anhydrous Dibasic Calcium Phosphate Industry Leaders

ICL Group Ltd.

Prayon S.A.

OCP Group

Innophos Holdings, Inc.

EuroChem Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Canberra Chemicals partnered with Invetek Advanced Solutions to roll out InveCal, a premium calcium phosphate excipient range manufactured in India’s state-of-the-art plants.

- January 2025: Fuji Chemical Industries spotlighted Fujicalin, a low-nitrite anhydrous dicalcium phosphate that supports drug makers in mitigating nitrosamine risks.

- October 2024: dsm-firmenich inaugurated a USD 60 million calcium-phosphate premix factory in São Paulo to serve South American poultry and swine producers.

Global Anhydrous Dibasic Calcium Phosphate Market Report Scope

Anhydrous Dibasic Calcium Phosphate is a water-insoluble, white, odorless, and tasteless powder used as a pharmaceutical filler, dietary calcium supplement, and anticaking agent, characterized by high porosity and thermal stability.

The Anhydrous Dibasic Calcium Phosphate Market Report is Segmented by Grade, Application, Form, End User, and Geography. By Grade, the market is segmented into Pharmaceutical, Food, Feed, and Industrial. By Application, the market is segmented into Pharmaceuticals, Food & Beverage, Animal Feed, Fertilizers, and Others. By Form, the market is segmented into Powder, Granules, and Micro-granules. By End User, the market is segmented into Pharmaceutical, Nutraceutical, Food & Beverage, Animal Nutrition, and Agricultural. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Pharmaceutical Grade |

| Food Grade |

| Feed Grade |

| Industrial Grade |

| Pharmaceuticals |

| Food & Beverage Fortification |

| Animal Feed Additives |

| Fertilizers |

| Others |

| Powder |

| Granules |

| Micro-granules |

| Pharmaceutical Manufacturers |

| Nutraceutical Producers |

| Food & Beverage Processors |

| Animal Nutrition Companies |

| Agricultural Input Suppliers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Grade | Pharmaceutical Grade | |

| Food Grade | ||

| Feed Grade | ||

| Industrial Grade | ||

| By Application | Pharmaceuticals | |

| Food & Beverage Fortification | ||

| Animal Feed Additives | ||

| Fertilizers | ||

| Others | ||

| By Form | Powder | |

| Granules | ||

| Micro-granules | ||

| By End-User Industry | Pharmaceutical Manufacturers | |

| Nutraceutical Producers | ||

| Food & Beverage Processors | ||

| Animal Nutrition Companies | ||

| Agricultural Input Suppliers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What drives recent growth in the anhydrous dibasic calcium phosphate market?

Higher demand for moisture-stable pharmaceutical excipients, rising nutraceutical consumption, and Asia-Pacific capacity additions are key growth catalysts.

How large is the anhydrous dibasic calcium phosphate market size today?

The market stood at USD 248.47 million in 2026 and is projected to reach USD 326.91 million by 2031.

Which application segment is expanding the fastest?

Nutraceutical supplements are expected to post a 9.79% CAGR through 2031, outpacing pharmaceuticals and food fortification.

Which geography is registering the highest CAGR?

Asia-Pacific is forecast to grow at 7.28% CAGR, driven by expanding pharmaceutical manufacturing in China and India.

Why are micro-granules gaining favor in pharmaceuticals?

Micro-granules offer superior flowability and consistent bulk density, maximizing uptime on high-speed tablet presses and reducing weight variation.

How are environmental regulations affecting supply?

Stricter emission and wastewater rules in China, the EU, and the U.S. raise production costs, potentially constraining future capacity expansions.

Page last updated on: