Anesthesia CO2 Absorbents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

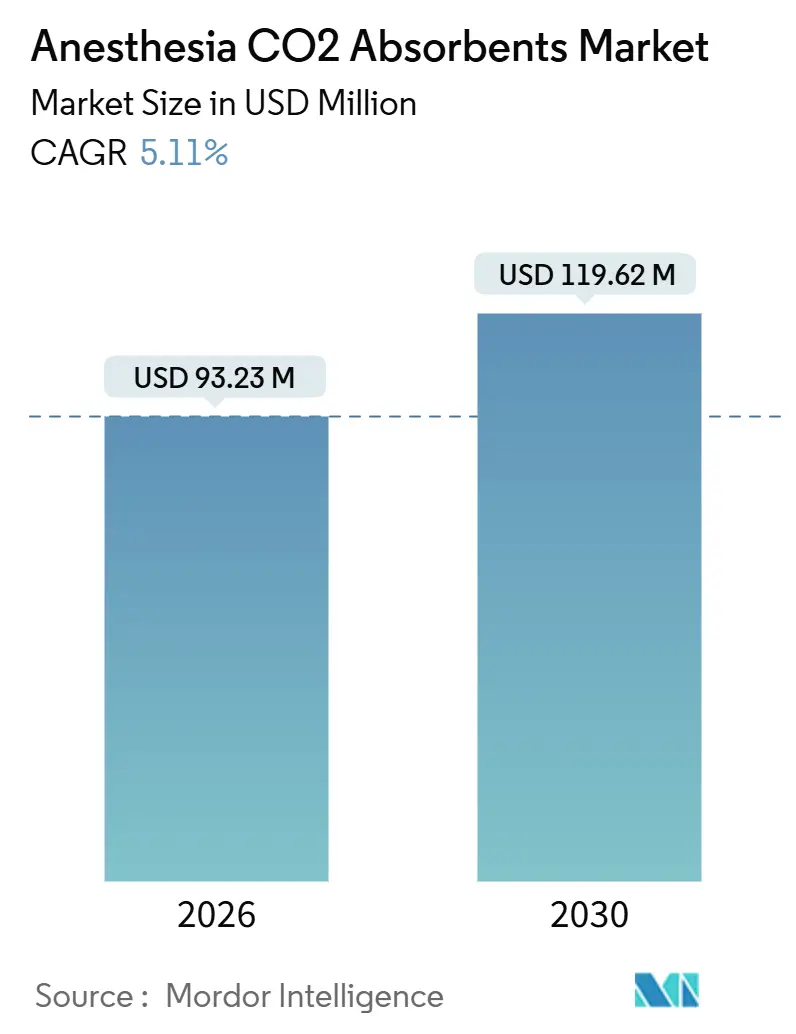

| Market Size (2026) | USD 93.23 Million |

| Market Size (2031) | USD 119.62 Million |

| Growth Rate (2026 - 2030) | 5.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anesthesia CO2 Absorbents Market Analysis by Mordor Intelligence

The Anesthesia CO2 Absorbents Market size is estimated at USD 93.23 million in 2026, and is expected to reach USD 119.62 million by 2031, at a CAGR of 5.11% during the forecast period (2026-2031).

Increasing ambulatory surgery volumes and adopting low-flow anesthesia are reducing per-case absorbent use. However, this decline is offset by premium product pricing and the expansion of operating rooms across Asia-Pacific. Hospitals remain the primary drivers of spending, but ambulatory centers and outpatient suites are scaling rapidly as payers incentivize same-day surgeries. Product demand is diverging between traditional soda lime and the safety-focused Amsorb, while environmental regulations are driving preference for premium options with landfill-safe pH profiles. Additionally, equipment vendors are incorporating absorbent sensors and software to extend canister life, influencing procurement decisions toward higher-performance formulations. As a result, the anesthesia CO₂ absorbents market is transitioning from a volume-driven model to a value-per-procedure approach.

Key Report Takeaways

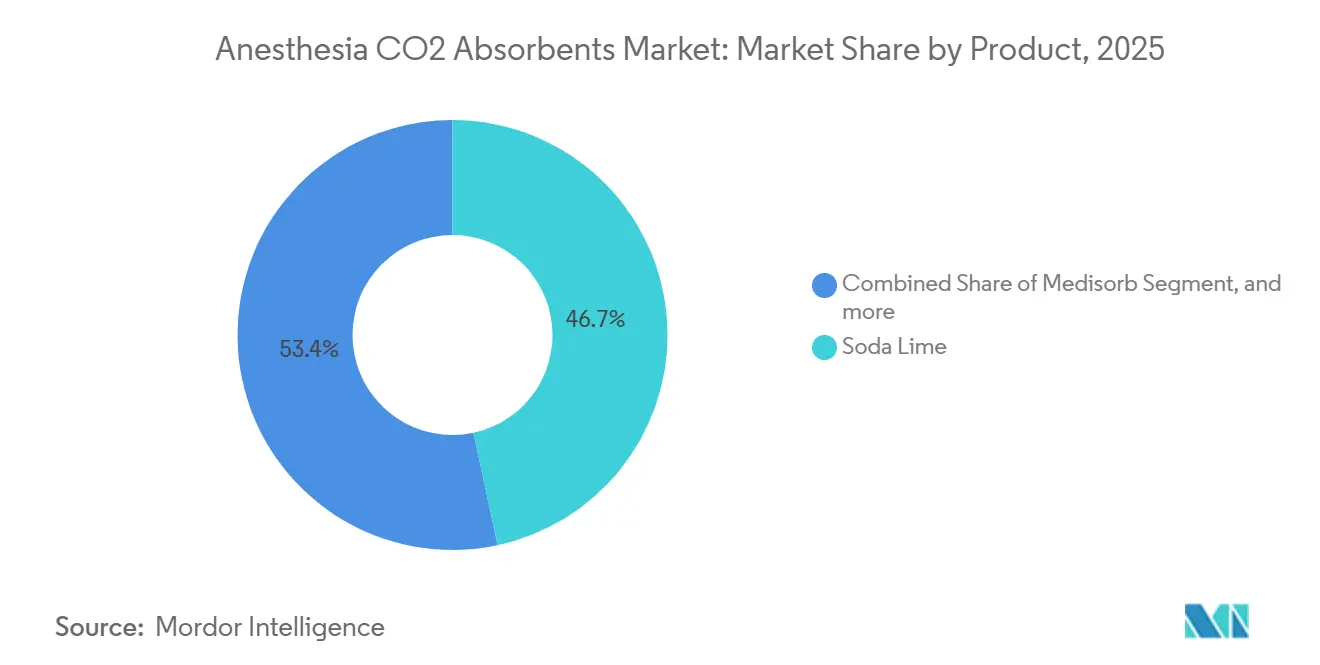

- By product, soda lime led with 46.65% of 2025 revenue, whereas Amsorb is forecast to grow at a 7.76% CAGR from 2026-2031.

- By absorbent type, premium formulations accounted for 57.54% of 2025 sales and are projected to expand at a 7.89% CAGR over the same horizon.

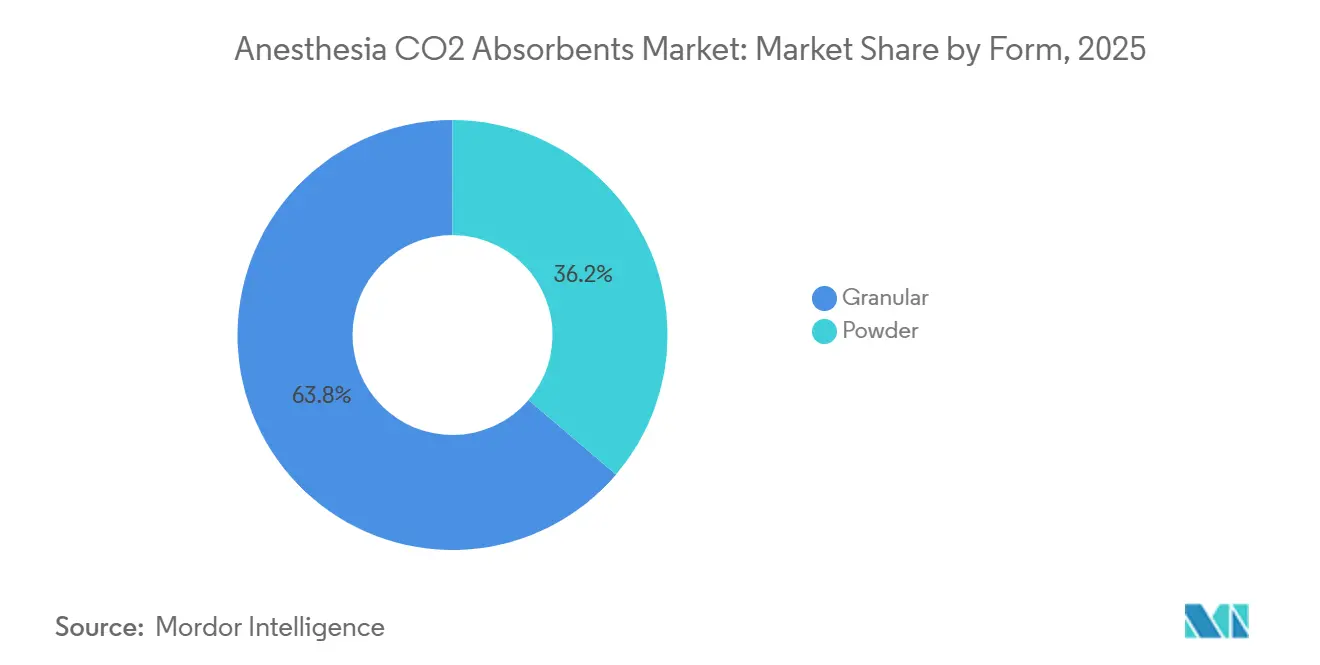

- By form factor, granular media accounted for 63.76% of 2025 turnover, while powder variants are advancing at an 8.11% CAGR to 2031.

- By end user, hospitals accounted for 58.65% of 2025 revenue, and ambulatory surgical centers had the fastest trajectory, with an 8.32% CAGR through 2031.

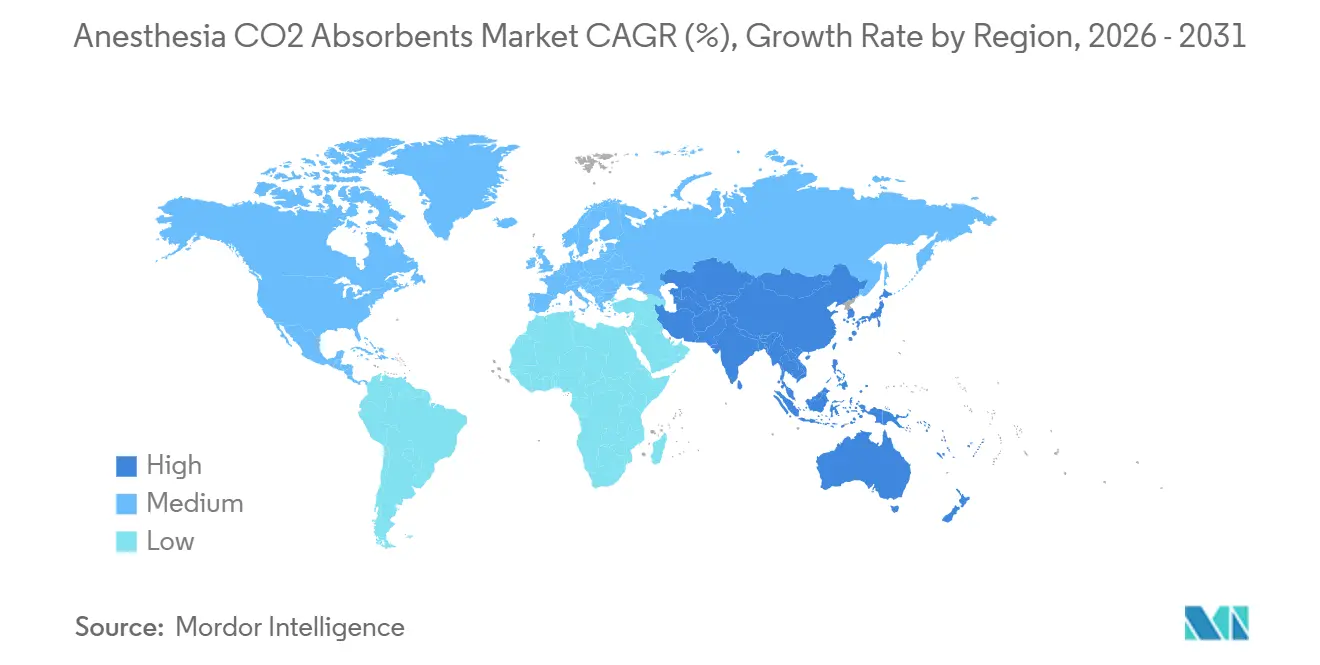

- By geography, North America controlled 42.65% of 2025 revenue, but Asia-Pacific is poised for a 6.43% CAGR through 2031 as operating-room capacity rises across China and India.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anesthesia CO2 Absorbents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume of Outpatient and Ambulatory Surgeries | +1.2% | Global, strongest in North America | Medium term (2-4 years) |

| Growing Adoption of Low-Flow Anesthesia Practices | +0.8% | North America, Europe, Australia | Long term (≥ 4 years) |

| Expansion of Healthcare Infrastructure in Emerging Economies | +1.5% | Asia-Pacific core, Middle East spillover | Long term (≥ 4 years) |

| Integration of Smart Operating Rooms with Sensor-Driven Absorbent Monitoring | +0.6% | North America, Western Europe | Medium term (2-4 years) |

| Hospital Sustainability Mandates for Green Anesthesia Consumables | +0.9% | North America, U.K., Nordics, Australia | Short–medium term (≤ 4 years) |

| Increasing Use of RFID-Tagged Absorbent Cartridges for Supply-Chain Transparency | +0.5% | Western Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Outpatient and Ambulatory Surgeries

Ambulatory surgical centers (ASCs) experienced a 5.7% growth in case counts between 2022 and 2023. In 2023, Medicare disbursed USD 6.8 billion to 6,308 certified ASCs. These facilities are increasingly adopting single-use, pre-filled absorbent canisters, which enhance operational efficiency by reducing turnover time by approximately three minutes per case. Accreditation bodies, such as the Joint Commission, now mandate irreversible dye indicators to prevent canister reuse, driving the transition toward premium SKUs[1]Joint Commission, “Ambulatory Accreditation Standards,” jointcommission.org. While price sensitivity remains high, the operational advantages enable branded disposables to sustain gross margins of nearly 40%. Consequently, the anesthesia CO₂ absorbents market continues to gain incremental value, even as per-procedure consumption declines.

Growing Adoption of Low-Flow Anesthesia Practices

A 2024 survey by GE HealthCare highlighted that while 83% of anesthesiologists acknowledge the cost-saving potential of low-flow techniques, only 14% utilize them in over 90% of cases. The FDA-cleared End-tidal Control software, which automates gas delivery, has demonstrated a reduction in volatile-anesthetic use of more than 25% during clinical trials. Real-world data from Nîmes University Hospital reported a sevoflurane consumption rate of 0.16 mL/min, effectively doubling the lifespan of each absorbent canister[2]Nîmes University Hospital, “Low-Flow Sevoflurane Study,” chu-nimes.fr. Consequently, fewer canisters are sold, yet providers are willing to pay a premium for advanced formulations that resist channeling and mitigate the formation of Compound A at ultra-low flows. These developments are driving the anesthesia CO₂ absorbents market toward high-margin, specialty chemistries.

Expansion of Healthcare Infrastructure in Emerging Economies

China has experienced a substantial increase in the number of public hospitals offering outpatient anesthesia, rising to over 2,800 in 2024 from fewer than 1,500 in 2020. In India, the National Health Mission funds 3,108 First Referral Units and more than 12,000 round-the-clock primary centers, many of which now feature advanced operating theaters. Similarly, Hong Kong has allocated HKD 3.2 billion to add 800 new hospital beds by 2025, integrating anesthesia workstations into turnkey packages[3]Hospital Authority Hong Kong, “Capacity Enhancement Programme 2025,” ha.org.hk. These initiatives prioritize ISO 13485-certified vendors, favoring global brands that can seamlessly integrate devices with proprietary absorbents. With the expansion of healthcare infrastructure, the anesthesia CO₂ absorbents market is positioned for significant growth, despite the challenges posed by regional price caps.

Integration of Smart Operating Rooms with Sensor-Driven Absorbent Monitoring

Multimodal monitoring platforms now integrate brain function, capnography, and absorbent conditions into a single display, streamlining operational efficiency. When paired with Philips IntelliVue, Medtronic's BIS Advance consolidates critical metrics to mitigate alarm fatigue. Dräger’s RFID-enabled ProAir canisters track service life with time stamps and automate replacement prompts. Early pilot programs reported zero stock-outs and a 58% reduction in supervisory workload, demonstrating the operational advantages of sensorized consumables. However, cross-vendor interoperability remains a key challenge. As hospitals increasingly adopt smart ORs, they are standardizing absorbents that interface seamlessly with machines, driving growth in the premium segment of the anesthesia CO₂ absorbents market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Premium CO₂ Absorbents | -0.7% | Global, acute in Asia-Pacific and MEA | Short term (≤ 2 years) |

| Environmental Disposal Challenges of Spent Absorbents | -0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Intermittent Supply Constraints for Pharmaceutical-Grade Calcium Hydroxide | -0.5% | Global, episodic spikes in Asia-Pacific | Short–medium term (≤ 4 years) |

| Safety Concerns over Compound A Formation during Sevoflurane Anesthesia | -0.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium CO₂ Absorbents

In North America, top-shelf products are priced at USD 18-25 per kilogram, compared to USD 12-15 for commodity soda lime. While lifecycle analyses suggest that disposal savings can offset the price difference, budget constraints in public hospitals often limit the adoption of premium products. Operating rooms in Asia and the Middle East spend only USD 3,000-5,000 annually on anesthesia consumables, which is just one-third of the expenditure in the United States. Currency fluctuations add further challenges; for example, a 3.2% depreciation of the rupee against the USD in 2024 increased landing costs, driving Hangzhou Tianshi Medical to boost local production. Although tiered portfolios provide some flexibility, high prices remain a significant barrier in the anesthesia CO₂ absorbents market.

Safety Concerns over Compound A Formation during Sevoflurane Anesthesia

Soda lime produces 18-23 ppm of Compound A under sevoflurane, compared to just 2 ppm for Amsorb. The ASA approved low-flow sevoflurane in 2023; however, updated FDA and Baxter labels in 2025 recommended against the use of potassium-hydroxide absorbents. A Class I recall of sevoflurane vaporizers in March 2025, triggered by hydrogen fluoride risks, further intensified regulatory scrutiny. Pediatric centers have predominantly shifted to low-alkali media, while cost-sensitive hospitals in the Asia-Pacific region continue to use soda lime, accepting its potential nephrotoxicity. These heightened safety concerns are expected to constrain market growth until perceptions improve.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Safety-Focused Amsorb Gains Momentum

In 2025, soda lime contributed 46.65% of the market's revenue, highlighting its established presence and compatibility with traditional workstations. However, the Anesthesia CO₂ absorbents market is transitioning toward Amsorb, which is projected to grow at a 7.76% CAGR through 2031. This growth is driven by its negligible Compound A output, pH level below 12.5, and irreversible dye indicators. Mid-tier products such as Medisorb and Drägersorb Free offer cost-effective safety improvements, while Litholyme addresses specialized extended-mission requirements. In North America and Europe, sustainability committees and pediatric units are driving Amsorb adoption. Conversely, the Asia-Pacific region remains focused on cost efficiency, enabling soda lime to retain its bulk-volume leadership. Over the forecast period, price convergence and regulatory changes are expected to reshape the product landscape, while soda lime will remain a key component of the anesthesia CO₂ absorbents market.

Equipment integration i influencing purchasing decisions. The Dräger Perseus A500 integrates with Drägersorb 800+ using optical sensors that provide real-time capacity monitoring, effectively locking hospitals into specific consumables. These closed ecosystems create high switching barriers. Additionally, formulary committees are increasingly considering lifetime disposal costs. For example, in North America, the hazardous classification of pH 14 soda lime adds USD 5-12 per canister. As landfill fees increase, Amsorb's non-hazardous classification is expected to drive greater adoption of low-alkali chemistries, boosting its value share in the Anesthesia CO₂ absorbents market.

By Type: Premium Formulations Extend Their Lead

By 2025, premium absorbents are expected to account for 57.54% of total revenue, driven by a strong CAGR of 7.89%. These products offer three distinct value propositions: alkali-free chemistry, landfill-safe pH, and sensor-ready packaging. In comparison, traditional soda lime, while more cost-effective, holds a smaller market share of 42.46% and experiences slower growth due to its Compound A liability, which dampens demand. A significant USD 1 billion agreement in 2024 between GE and Sutter Health highlights the industry's transition. This partnership demonstrates how bundling equipment accelerates the adoption of premium products by standardizing anesthetic workstations and their compatible consumables. Additionally, FDA and Baxter labeling that discourages the use of KOH absorbents effectively pushes the market toward premium options for sevoflurane cases, which are critical for a large portion of pediatric and outpatient procedures. These factors position the premium segment to dominate incremental revenue growth within the Anesthesia CO₂ absorbents market.

On the cost front, hospitals are realizing value through reduced hazardous-waste management requirements and minimized staff exposure to caustic dust. Suppliers are reinvesting their margins into R&D, focusing on advancements such as RFID tags and low-resistance geometries. As regulatory frameworks align with environmental objectives, the premium segment's market share is projected to exceed 65% by 2031, consolidating its pricing power within the anesthesia CO₂ absorbents market.

By Form: Granular Still Rules, Powder Climbs on Handling Advances

In 2025, granular media led the market, contributing 63.76% of the total turnover due to their low airflow resistance and ease of manual refills. Powder formats, previously challenged by dust-related issues, are projected to grow at a CAGR of 8.11% through 2031, driven by advancements such as agglomeration and anti-static coatings that minimize particulate release. With 15-20% higher absorption per kilogram, powders are particularly suited for low-flow anesthesia applications where capacity is a critical factor. Intersurgical’s AbCan™, a 1.1-liter disposable designed for Getinge Flow-i stations, leverages powder to provide extended runtime in a compact design, emphasizing the importance of efficient form factors. Workflow requirements influence product selection: high-volume centers tend to prefer pre-filled disposables, favoring powder, while resource-constrained settings often rely on bulk granular refills. Both formats remain integral to the Anesthesia CO₂ absorbents market.

By End User: Hospitals Dominate, ASCs Surge

In 2025, hospitals dominated the market with 58.65% of sales, driven by longer case durations and higher absorbent turnover per procedure. Ambulatory surgical centers (ASCs), however, are projected to grow at a robust CAGR of 8.32%, as payers increasingly shift orthopedic and cardiovascular procedures to these cost-efficient facilities. ASCs are adopting sealed, single-use canisters that streamline changeover processes and reduce contamination risks. These canisters deliver labor savings of USD 8-12 per case, effectively offsetting their higher upfront costs. Specialty clinics, including dental, pain management, and endoscopy, represent the smallest segment but require compact cartridges compatible with portable equipment. Additionally, hospitals are increasingly integrating absorbents into multiyear equipment lease agreements, ensuring a consistent supply while intensifying vendor lock-in within the Anesthesia CO₂ absorbents market.

Geography Analysis

In 2025, North America captured 42.65% of the revenue, driven by 6,308 Medicare-certified ASCs, stringent environmental regulations, and the early adoption of low-flow technologies. Although growth is expected to moderate to a 4.8% CAGR due to market maturity and declining per-room consumption, federal agencies' net-zero commitments continue to drive premium upgrades. In Canada, group purchasing contracts are compressing prices while ensuring consistent demand. Additionally, New Zealand's 2025 GE listing has introduced another centralized buyer to the vendor network.

The Asia-Pacific region is projected to grow at a 6.43% CAGR, gradually closing the gap with North America. China's public hospital reforms have significantly reduced wait times and increased surgical throughput, expanding the market for absorbents. In India, the PM-ABHIM initiative is injecting funds into district operating rooms, fueling demand for portable machines and small canisters in rural areas. Hong Kong's HKD 3.2 billion investment in capacity expansion underscores the region's focus on operating theater infrastructure. While soda lime remains the dominant choice due to price sensitivity, premium product adoption is gaining traction in tertiary hubs. These developments collectively strengthen the long-term growth prospects of the Anesthesia CO₂ absorbents market.

Europe presents a varied outlook. The U.K.'s National Health Service is mandating greener anesthesia practices, accelerating the transition to Amsorb, while Germany's DRG framework prioritizes cost efficiency, favoring soda lime. The 2025 partnership between Philips and Getinge integrates Flow-family workstations with IntelliVue monitors, shifting procurement strategies from standalone consumables to bundled contracts. In Latin America and the Middle East, growth is emerging from a smaller base. Saudi Arabia's Vision 2030 and the UAE's medical tourism initiatives are driving selective premium adoption. However, currency volatility and tariffs are creating opportunities for local producers in Brazil and Argentina.

Competitive Landscape

The anesthesia CO₂ absorbents market is moderately concentrated, with leading players 3M, Drägerwerk, Armstrong Medical, Intersurgical, and Baxter collectively accounting for approximately 60% of the market share. Advancements in safety chemistry, seamless device integration, and supply chain efficiency drive competition. In December 2025, Intersurgical acquired Teleflex’s Acute Care and Interventional Urology units, aiming to bundle airway consumables with CO₂ absorbents to enhance cross-selling opportunities across Europe and Asia-Pacific. In October 2025, GE HealthCare launched the Carestation 850, which integrates widescreen analytics with proprietary canisters, strengthening its consumables ecosystem and driving customer retention.

Drägerwerk is investing in RFID-enabled canisters that provide real-time capacity data to Perseus workstations, increasing switching costs for existing customers. Emerging players are focusing on niche innovations, such as compact powder absorbents for military and disaster applications, open-protocol sensors, and circular models for regenerating spent media. Chinese manufacturers, including Hangzhou Tianshi Medical, are gaining market share in Asia and the Middle East by offering ISO 13485-certified products at 30-40% lower prices. Teleflex’s 2024 anesthesia revenue of USD 101.1 million highlights the sector's resilience, although its divestiture reflects a strategic pivot toward higher-margin devices. Overall, suppliers in the Anesthesia CO₂ absorbents market are prioritizing differentiation strategies, reshaping value capture dynamics within the industry.

Anesthesia CO2 Absorbents Industry Leaders

3M

Drägerwerk AG & Co. KGaA

Armstrong Medical Ltd.

Intersurgical Ltd.

Baxter International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Intersurgical agreed to acquire Teleflex’s Acute Care and Interventional Urology lines, extending its anesthesia portfolio.

- October 2025: GE HealthCare debuted the Carestation 850 with refill-in-use vaporizers and widescreen data views

- October 2025: Philips and Getinge formed a commercial alliance marrying Flow-family workstations with IntelliVue monitoring.

- November 2024: Cardinal Health bought GI Alliance for USD 2.8 billion, adding anesthesia services to its distribution footprint.

Global Anesthesia CO2 Absorbents Market Report Scope

As per scope of the report, anesthesia CO₂ absorbents are materials used in breathing circuits to remove carbon dioxide from exhaled gases during anesthesia. They typically contain chemicals like soda lime or baralyme that chemically react with CO₂. These absorbents help ensure safe rebreathing of gases and maintain proper respiratory function during surgery.

The Anesthesia CO2 Absorbents Market is Segmented by Product (Soda Lime, Medisorb, Drägersorb, Amsorb, Litholyme, and Other Products), Type (Premium and Traditional), Form (Powder and Granular), End-User (Hospitals, Ambulatory Surgical Centers, and Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Soda Lime |

| Medisorb |

| Drägersorb |

| Amsorb |

| Litholyme |

| Other Products |

| Premium |

| Traditional |

| Powder |

| Granular |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Soda Lime | |

| Medisorb | ||

| Drägersorb | ||

| Amsorb | ||

| Litholyme | ||

| Other Products | ||

| By Type | Premium | |

| Traditional | ||

| By Form | Powder | |

| Granular | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Anesthesia CO? Absorbents market?

The market is valued at USD 93.23 million in 2026 and is projected to reach USD 119.62 million by 2031.

Which product type is growing fastest?

Amsorb leads growth with a 7.76% CAGR due to low Compound A production and landfill-safe pH.

Why are ambulatory surgical centers important for demand?

ASCs are expanding procedure volumes and favor disposable canisters, driving an 8.32% CAGR in absorbent purchases.

How does low-flow anesthesia influence absorbent consumption?

Automated low-flow protocols cut volatile-agent use and double canister life, shifting purchasing toward high-capacity premium media.

Which region will add the most new operating rooms?

Asia-Pacific, especially China and India, is investing heavily in surgical infrastructure, underpinning a 6.43% regional CAGR.

Are premium absorbents cost-effective despite higher prices?

When hazardous-waste fees and labor savings are included, total ownership costs often favor premium, alkali-free formulations.

Page last updated on: