Anaplastic Astrocytoma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

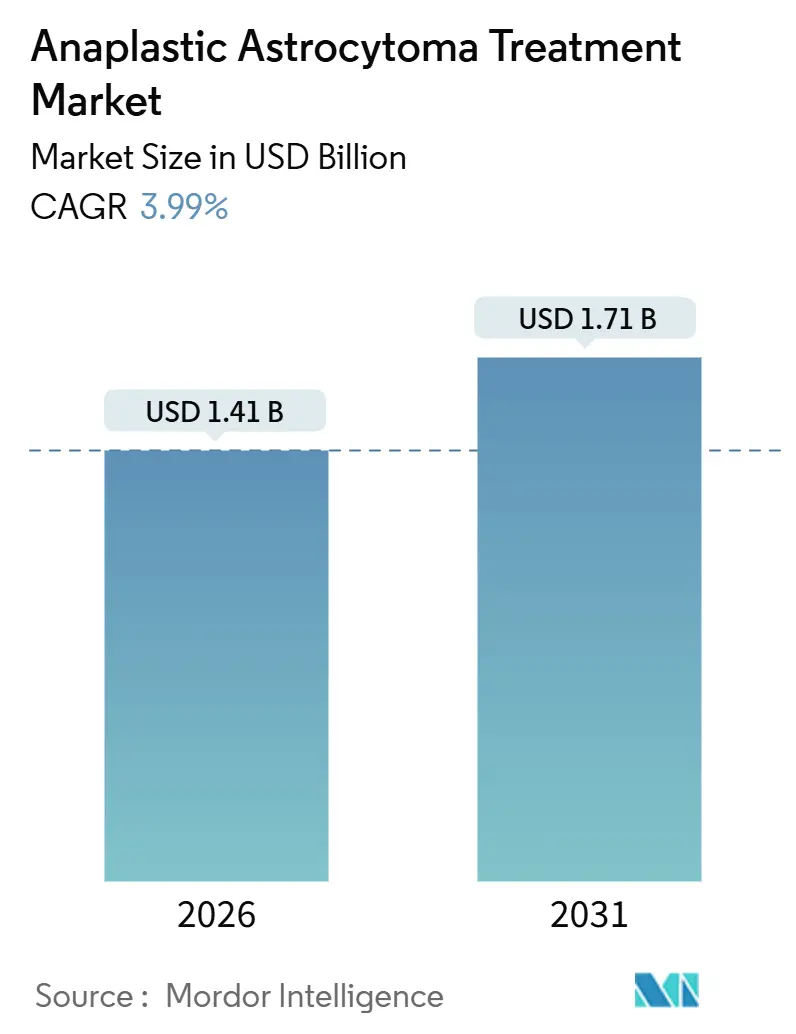

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

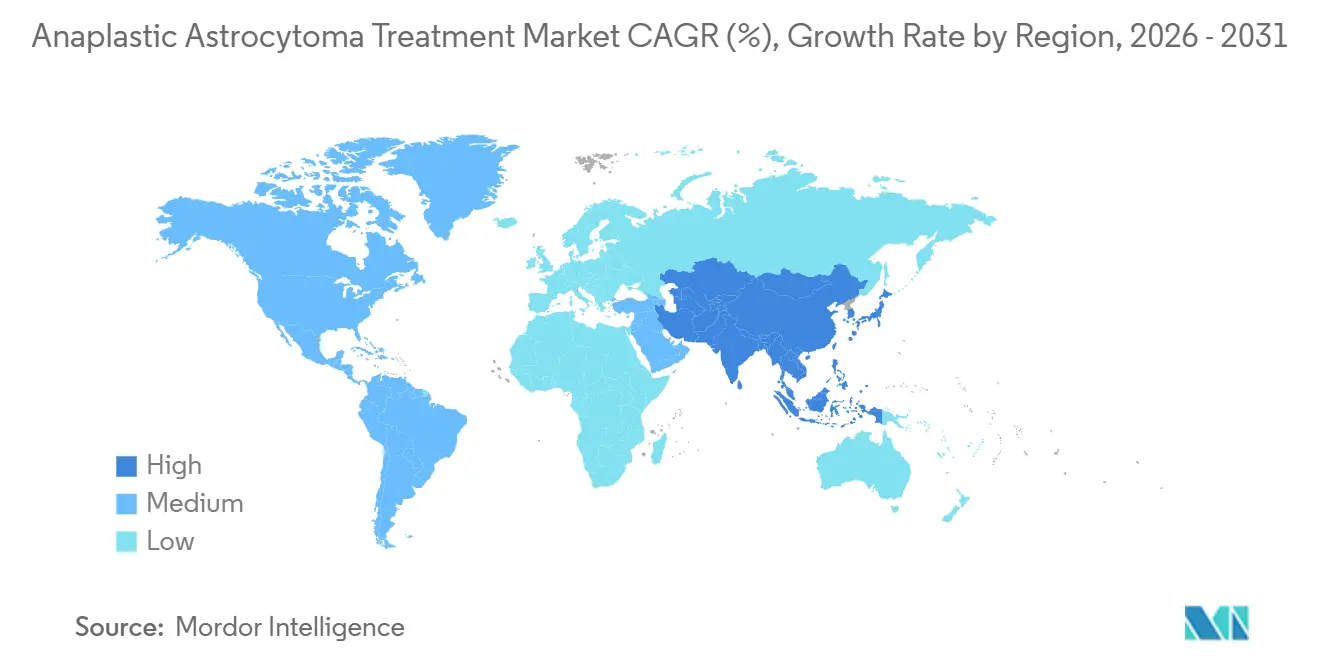

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anaplastic Astrocytoma Treatment Market Analysis by Mordor Intelligence

The Anaplastic Astrocytoma Treatment Market size is estimated at USD 1.41 billion in 2026, and is expected to reach USD 1.71 billion by 2031, at a CAGR of 3.99% during the forecast period (2026-2031).

Current growth rests on two contrasting realities: rapid uptake of IDH-targeted therapy by the IDH-mutant majority and the stubborn survival gap in the IDH-wildtype minority. Wider generic temozolomide access, proton-beam expansion, and guideline-driven molecular testing sustain steady first-line revenues, while emerging dual inhibitors, antibody-drug conjugates, and basket-trial immunotherapies define long-run upside. Competitive dynamics remain moderate, as only a handful of branded agents enjoy anaplastic-astrocytoma-specific labels, and most regimens still borrow glioblastoma precedents. The anaplastic astrocytoma treatment market must therefore balance orphan-drug pricing, payer scrutiny, and modest patient volumes against a pipeline poised to shift standards of care over the next decade.

Key Report Takeaways

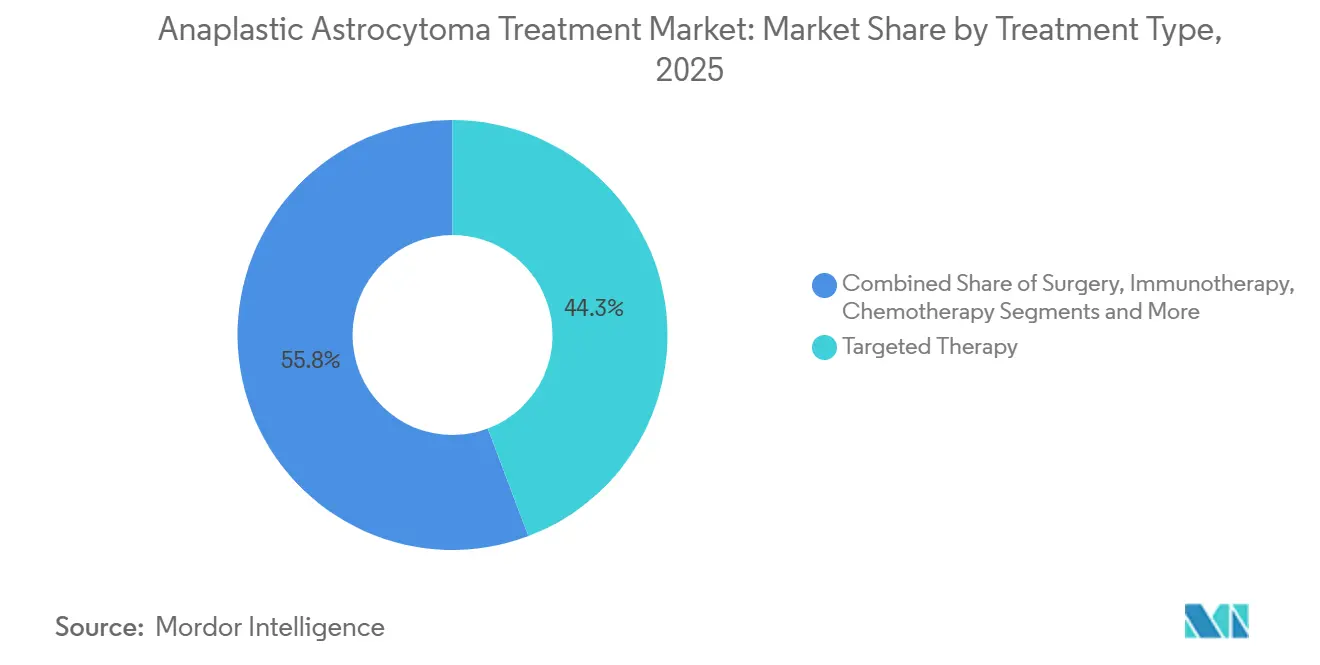

- Targeted therapy held 44.25% of the anaplastic astrocytoma treatment market share in 2025, while immunotherapy posted the fastest projected CAGR at 5.73% through 2031.

- First-line protocols accounted for 66.14% of 2025 revenue, whereas second-line options are forecast to expand at a 6.58% CAGR on the strength of lomustine rechallenge and IDH-inhibitor combinations.

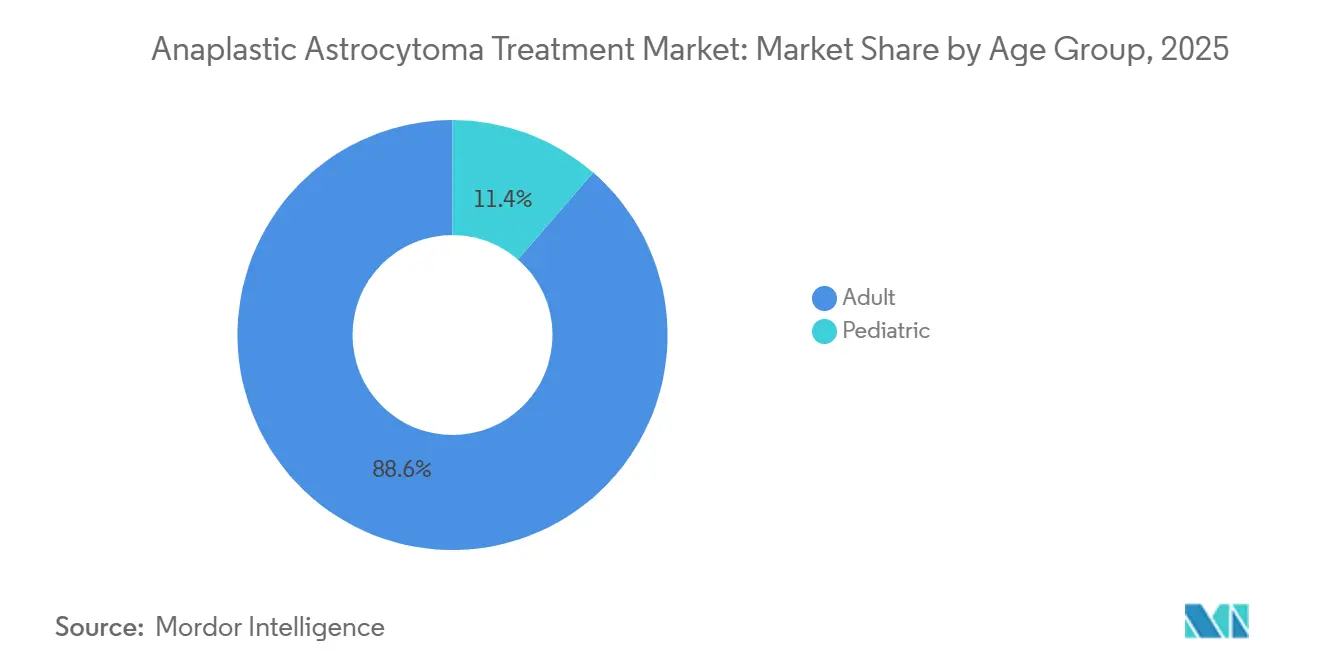

- Adult patients represented 88.63% of 2025 volume, yet the pediatric segment is expected to grow at a robust 7.02% CAGR, buoyed by age-specific genomic discoveries.

- Hospitals generated 53.38% of end-user revenue in 2025, but specialty clinics and neuro-oncology centers are growing at a 5.24% CAGR as multidisciplinary tumor boards and proton-beam units proliferate.

- North America dominated with a 42.46% revenue contribution in 2025; Asia-Pacific is projected to post the highest regional growth at 6.22% CAGR, led by generic alkylator affordability and expanding molecular-diagnostic capacity.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anaplastic Astrocytoma Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Guideline-backed radiotherapy plus temozolomide for IDH-mutant grade 3 tumors | +0.8% | North America, Western Europe | Medium term (2–4 years) |

| Molecular classification and biomarker testing expansion | +1.2% | Global, strongest in developed markets | Medium term (2–4 years) |

| Generic alkylator availability improving affordability | +0.9% | Asia-Pacific, Latin America | Short term (≤2 years) |

| MGMT promoter methylation testing optimizing chemotherapy use | +0.6% | North America, Western Europe, urban Asia-Pacific | Medium term (2–4 years) |

| Pipeline momentum in IDH inhibitors and novel combinations | +1.1% | Global | Long term (≥4 years) |

| Adoption of hypofractionated IMRT and proton-beam protocols | +0.7% | North America, Western Europe, Japan, South Korea | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Guideline-Backed Radiotherapy Plus Temozolomide Supports Long-Term Control

NCCN and EANO protocols recommend focal radiotherapy followed by adjuvant temozolomide for IDH-mutant anaplastic astrocytoma, sustaining first-line dominance through 2031.[1]National Comprehensive Cancer Network Editorial Board, “Central Nervous System Cancers, Version 2.2026,” National Comprehensive Cancer Network, nccn.org Generic temozolomide from Cipla and other Indian manufacturers has trimmed per-cycle costs by 60 % in many low- and middle-income countries, driving adherence in Asia-Pacific and Latin America. U.S. and German centers increasingly deploy hypofractionated schedules—54 Gy in 30 fractions—to shorten therapy without compromising control.[2]Jiří Kratochvil et al., “Hypofractionated Radiotherapy for Grade 3 Glioma: A Multicenter Experience,” International Journal of Radiation Oncology, redjournal.org Proton-beam operators in Japan and South Korea report hippocampal-sparing protocols that safeguard cognitive outcomes for younger, IDH-mutant adults. Vorasidenib’s 2024 approval for grade 2 glioma has sparked trials testing the agent as an adjuvant add-on after chemoradiation in grade 3 disease.

Molecular Classification Accelerates Targeted Therapy Uptake

Routine profiling for IDH mutations, MGMT methylation, 1p/19q codeletion, and ATRX loss now guides therapy selection, lifting targeted agents to 44.25% of 2025 revenue. Ivosidenib’s 2024 approval for IDH1-mutant relapsed glioma delivered the first glioma-specific small-molecule option, achieving a 35% objective response rate in real-world U.S. cohorts.[3] Kristen B. Peters et al., “Real-World Outcomes With Ivosidenib in Relapsed IDH1-Mutant Gliomas,” Memorial Sloan Kettering Cancer Center, mskcc.org Vorasidenib’s 27.7-month median progression-free survival in INDIGO further validates dual inhibition, and Servier filed for a grade 3 indication in late 2025. Medicare and several European payers now reimburse comprehensive next-generation sequencing, enabling detection of BRAF, FGFR, and NTRK lesions that collectively occur in 5–8% of anaplastic astrocytomas. Molecular tumor boards in China and India are broadening trial participation, though costs still dampen uptake outside metropolitan hubs.

Generic Alkylator Penetration Enhances Affordability

Temozolomide’s patent lapse unleashed a crowded generic field—Cipla, Dr. Reddy’s, Sun Pharma, Teva, Zydus, and Hetero Labs—supplying more than 80% of global volume by 2026. Course pricing in India and Brazil now sits under USD 50, widening access and underpinning Asia-Pacific’s 6.22% CAGR. Lomustine pricing shocks in the United Kingdom during 2023 highlighted single-supplier risk, but FDA approval of a U.S. generic in 2024 restored competition and stabilized costs at USD 800 per cycle. Emerging Chinese producers pursue bioequivalence for dacarbazine and procarbazine, eyeing second-line share in a segment forecast to expand at 6.58% CAGR.

MGMT Promoter Methylation Testing Refines Chemotherapy Decisions

MGMT methylation status predicts temozolomide benefit, and testing penetrance surpasses 70 % in the United States and Western Europe. Methylated tumors experience a 40 % lower progression risk under adjuvant temozolomide, cementing the assay’s guideline status. Medicare reimbursement under CPT 81287 eliminates U.S. cost barriers, whereas Eastern Europe and Latin America still face coverage gaps. UCSF researchers published 2025 data linking circulating-tumor-DNA methylation signatures to tissue MGMT status, laying groundwork for noninvasive monitoring. FDA review of a liquid-biopsy MGMT test could democratize access for community practices in the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-rare patient pool reducing addressable volumes | –0.9% | Global | Long term (≥4 years) |

| Limited survival benefit and few AA-specific approvals | –0.7% | Global, acute in IDH-wildtype disease | Medium term (2–4 years) |

| Single-supplier exposure and lomustine price volatility | –0.4% | Europe, select emerging markets | Short term (≤2 years) |

| Reimbursement variability for advanced molecular diagnostics | –0.5% | Latin America, Middle East & Africa, parts of Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Ultra-Rare Incidence Limits Trial Feasibility and Revenue

Anaplastic astrocytoma represents barely 4 % of adult gliomas, equating to fewer than 1,500 U.S. cases yearly, a scale that caps peak sales potential and hampers trial enrollment. INDIGO took five years to accrue 331 participants across 13 nations. Orphan incentives offset part of the commercial risk, yet forecasts seldom exceed USD 200 million per asset, deterring large-cap entrants. International registries seek to pool data, but IDH and MGMT stratification fragments the cohort further. Venture capital funding toward anaplastic-astrocytoma start-ups slipped 30 % between 2023 and 2025.

Limited Survival Gains Dampen Second-Line Enthusiasm

IDH-wildtype tumors mirror glioblastoma and deliver only 15–18 months of median survival despite aggressive therapy. Beyond ivosidenib and vorasidenib, all other agents rely on off-label precedent, challenging reimbursement. A 2025 Cochrane analysis showed no lomustine survival advantage, yet European oncologists still prescribe it for lack of better options. Bevacizumab improves imaging but not survival, and nivolumab failed to meet endpoints in CheckMate 143. Patients consequently navigate a trade-off between toxicity and modest life extension.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Dominance of Targeted Therapy Coupled with Immunotherapy Upswing

Targeted therapy generated 44.25% of 2025 revenue for the anaplastic astrocytoma treatment market, largely through ivosidenib and vorasidenib that address up to 80 % of IDH-mutant cases. The duo is projected to extend progression-free intervals by double those of placebo comparators, carving room to displace lomustine in second-line care. Immunotherapy is the fastest climber at 5.73% CAGR, buoyed by basket protocols focusing on hypermutated and mismatch-repair-deficient tumors, albeit representing only a small genetic subset.

Continued chemoradiation use keeps alkylators and radiotherapy foundational, while IMRT and proton-beam schedules limit neurocognitive fallout. Surgery enables cytoreduction and molecular sampling but is often restricted by tumor proximity to eloquent structures. Tumor Treating Fields remains a niche owing to device-wearing burdens, yet trials pairing it with temozolomide could broaden uptake if compliance hurdles diminish.

By Line of Therapy: First-Line Command with Second-Line Momentum

First-line regimens contributed 66.14 % of 2025 demand in the anaplastic astrocytoma treatment market, backed by near-universal adoption of radiotherapy plus temozolomide in IDH-mutant settings. MGMT-methylation-guided selection further optimizes benefit.

Second-line therapy is forecast to rise 6.58% annually as lomustine, IDH inhibitors, and basket-trial entrants gain traction. U.S. centers report a 35 % response to ivosidenib in temozolomide-relapsed disease, shifting standard practice. Bevacizumab keeps a foothold for edema management, and combinations such as vorasidenib plus lomustine are under European evaluation.

By Age Group: Adult Predominance and Pediatric Upside

Adult cases accounted for 88.63 % of treated volume in 2025 within the anaplastic astrocytoma treatment market. These patients enjoy five-year survivals exceeding 60 % when IDH-mutant and MGMT-methylated, warranting intensive multimodal strategies.

Pediatric incidence is lower yet expanding at 7.02 % CAGR, fueled by discoveries of H3 K27M, ALK, and BRAF alterations that tailor targeted therapy choices. Proton-beam centers prioritize children to minimize late neurotoxicity, and an ongoing COG phase 2 study is probing vorasidenib safety in youths.

By End User: Hospital Leadership Amid Outpatient Shift

Hospitals generated 53.38 % of 2025 revenue in the anaplastic astrocytoma treatment market, reflecting their integrated surgery, radiotherapy, and inpatient chemotherapy functions. Major academic complexes anchor guideline adherence and trial participation.

Specialty clinics and dedicated neuro-oncology centers are pacing a 5.24% growth curve as outpatient infusion suites, proton-beam vaults, and tele-tumor boards demonstrate efficiency gains. Ambulatory surgical centers compete on biopsies and port placements, while academic institutes focus on translational research and precision-oncology trials.

Geography Analysis

North America supplied 42.46 % of 2025 revenues for the anaplastic astrocytoma treatment market, powered by high MGMT testing rates, Medicare-funded genomic profiling, and timely FDA approvals of ivosidenib, vorasidenib, and generic lomustine. Clinical-trial participation surpasses 60 %, accelerating early access to next-generation agents. Proton-beam penetration rose from 10 % in 2023 to 18 % in 2026 after payers accepted quality-of-life advantages.

Europe contributed about 30 % of 2025 demand, led by Germany, France, and the United Kingdom, all mandating MGMT testing prior to temozolomidee. EMA orphan designations for three novel IDH inhibitors indicate regulatory advocacy, yet lomustine pricing volatility in 2023–2024 exposed supply fragility until Indian generics entered the channel. Eastern European uptake lags due to partial reimbursement for NGS panels, though pan-European EORTC trials help bridge access gaps.

Asia-Pacific is on track for a 6.22% CAGR through 2031, the fastest among regions, as generic temozolomide affordability, MGMT assay rollout in urban centers, and growing proton-beam capacity in Japan and South Korea converge. China’s early-2026 vorasidenib approval and India’s in-house MGMT testing breakthroughs underscore momentum. Australia’s reimbursement of ivosidenib enhances access for IDH1-mutant patients.

Competitive Landscape

Market concentration is moderate: Servier, Agios, and Novocure dominate branded segments, whereas multiple generics split chemotherapy volume. Servier’s vorasidenib and Agios’s ivosidenib possess the only IDH-mutant approvals, granting near-monopoly within that genotype until patent expirations in the early 2030s. Novocure’s Optune maintains exclusive device status, though daily-usage burdens limit broad uptake. Roche and Merck continue immunotherapy exploration, yet efficacy remains confined to mismatch-repair-deficient niches. Generic makers—Cipla, Dr. Reddy’s, Sun Pharma, Teva, Zydus, Hetero—compete mainly on reliability and price. Strategic themes revolve around orphan-drug exclusivity, label expansions into grade 3 disease, and combination regimens pairing IDH blockade with alkylators or checkpoint agents. White-space opportunities include therapies for IDH-wildtype tumors and blood-brain-barrier-penetrant delivery technologies.

Anaplastic Astrocytoma Treatment Industry Leaders

Accord Healthcare Ltd.

Merck & Co., Inc.

Sun Pharmaceutical Industries Ltd.

Teva Pharmaceutical Industries Ltd.

Zydus Lifesciences Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: FDA granted fast-track designation to zotiraciclib (TG02) for recurrent high-grade gliomas with IDH1/2 mutations.

- July 2025: Mustang Bio received orphan-drug status for IL13Ra2-targeted CAR-T candidate MB-101 in recurrent diffuse and anaplastic astrocytoma.

- August 2024: FDA approved vorasidenib for IDH-mutant grade 2 glioma; Servier filed for grade 3 extension in Dec 2025

Global Anaplastic Astrocytoma Treatment Market Report Scope

Anaplastic astrocytoma treatment refers to an aggressive, multi-modal approach for managing Grade III, fast-growing brain tumors, involving surgical resection, radiotherapy, and chemotherapy (often temozolomide), with plans often personalized based on IDH mutation status.

The Anaplastic Astrocytoma Treatment Market Report is segmented by Treatment Type, Line of Therapy, Age Group, End User, and Geography.

By Treatment Type, the market is segmented into Surgery, Radiation Therapy, Chemotherapy, Targeted Therapy, Immunotherapy, and Tumor Treating Fields. By Line of Therapy, the market is segmented into First Line and Second Line. By Age Group, the market is segmented into Adult and Pediatric. By End User, the market is segmented into Hospitals, Specialty Clinics & Neuro-oncology Centers, Ambulatory Surgical Centers, and Academic & Research Institutes. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Surgery |

| Radiation Therapy |

| Chemotherapy |

| Targeted Therapy |

| Immunotherapy |

| Tumor Treating Fields (TTFields) |

| First Line |

| Second Line |

| Adult |

| Pediatric |

| Hospitals |

| Specialty Clinics & Neuro-oncology Centers |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Surgery | |

| Radiation Therapy | ||

| Chemotherapy | ||

| Targeted Therapy | ||

| Immunotherapy | ||

| Tumor Treating Fields (TTFields) | ||

| By Line of Therapy | First Line | |

| Second Line | ||

| By Age Group | Adult | |

| Pediatric | ||

| By End User | Hospitals | |

| Specialty Clinics & Neuro-oncology Centers | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the anaplastic astrocytoma treatment market today?

The anaplastic astrocytoma treatment market size reached USD 1.41 billion in 2026 and is set to climb to USD 1.71 billion by 2031.

Which therapy class currently leads spending?

IDH-targeted therapy generated 44.25% of 2025 revenue, the highest among all treatment types.

What region grows the fastest through 2031?

Asia-Pacific is forecast to expand at a 6.22% CAGR, the quickest regional pace.

Why are MGMT tests important?

MGMT promoter methylation predicts temozolomide benefit, lowering progression risk by 40% in methylated tumors.

What limits market expansion most?

Ultra-rare incidence restricts patient numbers, trial sizes, and peak-sales potential.

Page last updated on: