Amino Acid Disorders Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

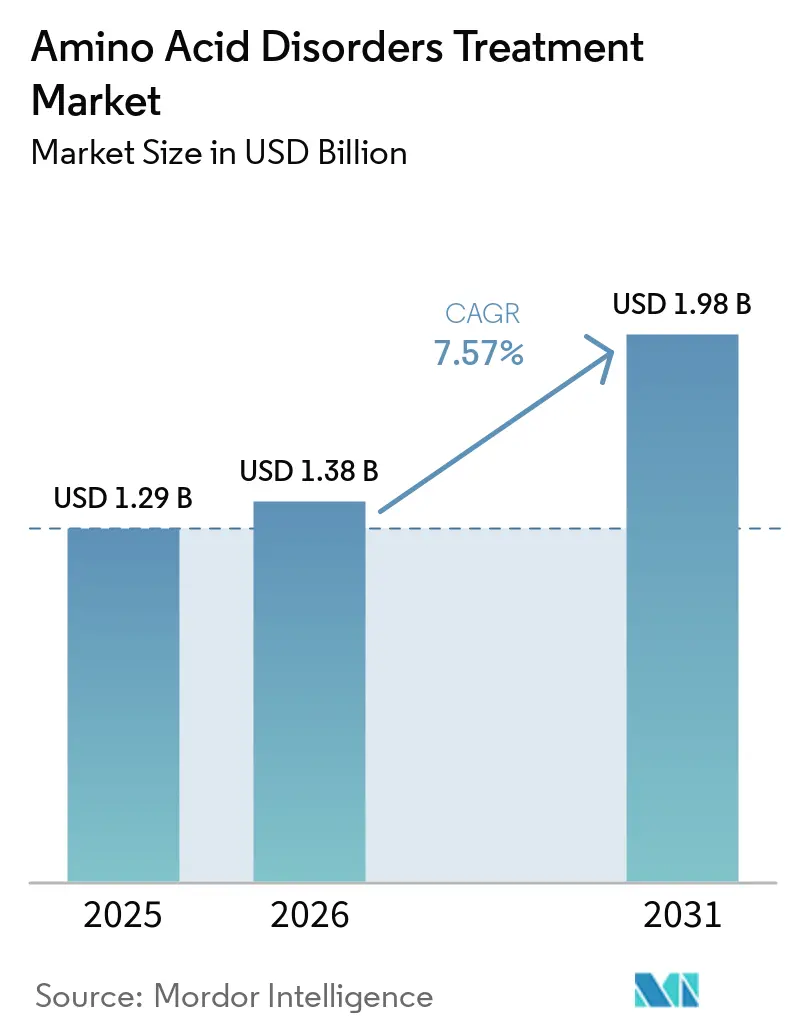

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 7.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Amino Acid Disorders Treatment Market Analysis by Mordor Intelligence

The Amino Acid Disorders Treatment Market size is expected to increase from USD 1.29 billion in 2025 to USD 1.38 billion in 2026 and reach USD 1.98 billion by 2031, growing at a CAGR of 7.57% over 2026-2031.

Broadening labels for approved therapies increases treated populations and sustains uptake, while real-world patient support and distribution models shorten time to therapy and improve adherence. Screening coverage is expanding across several countries in the Asia Pacific, where higher detection rates lift the diagnosed base and future therapy volumes. Advanced modalities are progressing, yet immunogenicity and manufacturing scale-up challenges continue to shape timelines and portfolio choices for next-generation platforms. Online specialty hubs and limited distribution networks add resilience and speed to patient access through tightly integrated benefit verification, prior authorization, and cold-chain fulfillment.

Key Report Takeaways

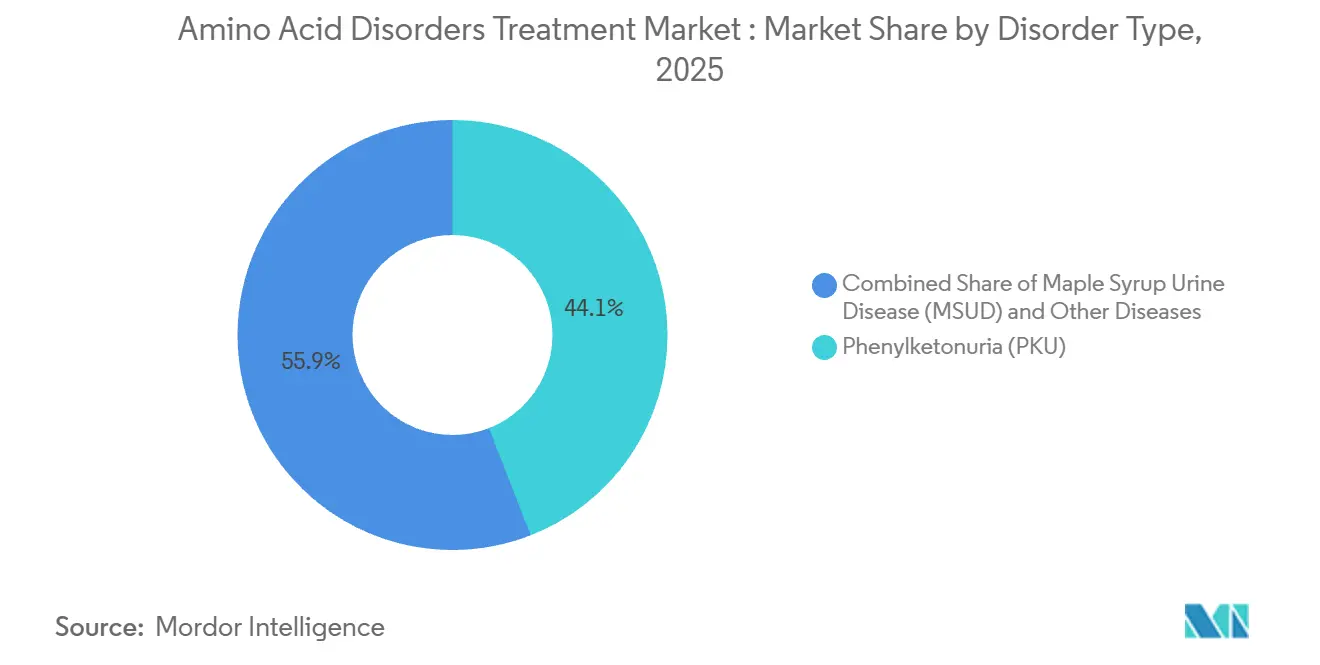

By disorder type, phenylketonuria led with 44.08% revenue share in 2025. It is also projected to post the fastest growth at 8.10% CAGR through 2031.

By treatment modality, medical nutrition commanded a 55.32% revenue share in 2025. Investigational and advanced therapies are set to grow at 8.22% CAGR over 2026–2031.

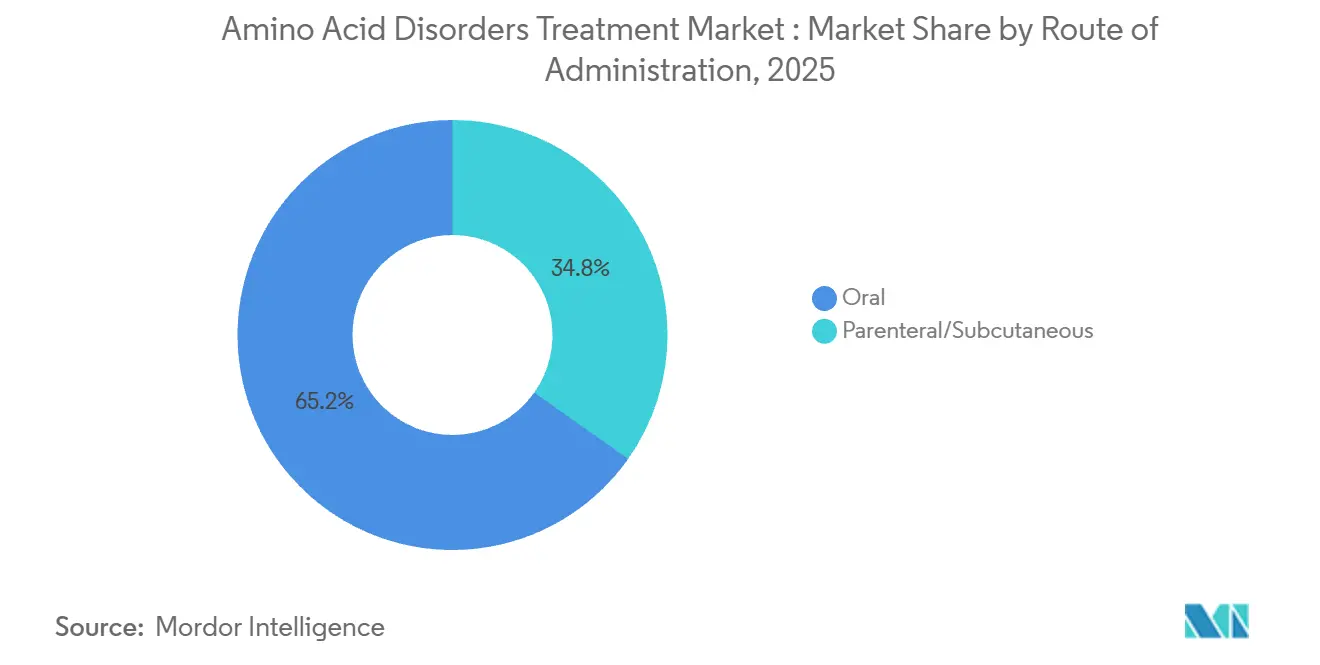

By route of administration, oral formulations held 65.23% revenue share in 2025. Parenteral and subcutaneous routes are forecast to expand at 8.30% CAGR through 2031.

By distribution channel, hospital pharmacies captured 48.22% revenue share in 2025. Online pharmacies are projected to grow at 8.12% CAGR during 2026–2031.

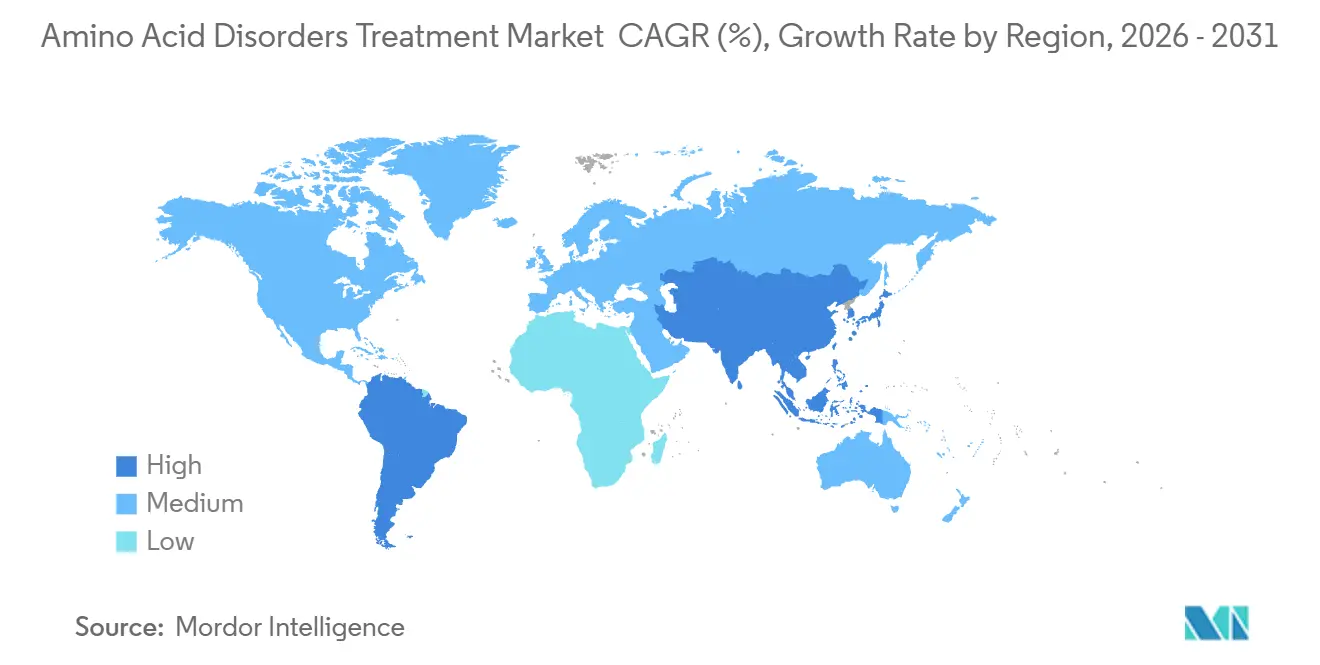

By geography, North America held 42.11% revenue share in 2025. Asia Pacific is projected to record a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Amino Acid Disorders Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Orphan-drug approvals expanding treatable patient pool | +1.8% | Global, with early gains in US, EU, Japan | Short term (≤ 2 years) |

| Global newborn screening expansion is increasing diagnosed base | +1.5% | APAC core, spill-over to MEA | Medium term (2–4 years) |

| Medical nutrition innovation (GMP-based, ready-to-drink) improving adherence | +1.2% | North America and the EU | Medium term (2–4 years) |

| Specialty pharmacy and patient-support hubs are improving access | +1.1% | North America and the EU | Short term (≤ 2 years) |

| Gut-targeted synthetic biotics enabling diet liberalization | +0.9% | Global | Long term (≥ 4 years) |

| Pipeline progress in BH4 precursors and multi-modal PKU therapies | +1.0% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Orphan-Drug Approvals Expanding Treatable Patient Pool

Broadened labels and new approvals are increasing the number of patients eligible for therapy, which lifts near-term initiations and sustains adherence support. In February 2026, the FDA cleared an enzyme therapy for adolescents aged 12–17, expanding access to a younger cohort following adult use and supporting ongoing revenue growth[1]BioMarin Pharmaceutical Inc., “United States Food and Drug Administration Approves BioMarin’s PALYNZIQ (pegvaliase-pqpz) for Adolescents 12 Years of Age and Older with Phenylketonuria (PKU)” . A tetrahydrobiopterin precursor received United States approval in July 2025 with a broad label that spans infants through adults, and the therapy also secured European Commission authorization, together setting up a synchronized launch trajectory across major markets. The European regulator granted an orphan designation to a hydroxocobalamin acetate candidate for homocystinuria, signaling pipeline breadth beyond phenylalanine hydroxylase deficiency. In June 2025, the FDA approved nitisinone tablets for alkaptonuria, the first approved therapy for this ultra-rare indication, and the manufacturer launched a companion support program to facilitate patient access. Post-approval risk management requirements remain in focus, since a mandated REMS for enzyme therapy includes anaphylaxis education and epinephrine auto-injector readiness for all patients and caregivers.

Global Newborn Screening Expansion Increasing Diagnosed Base

Policy updates and technology upgrades in newborn screening are increasing the detection of inherited metabolic diseases and aligning treatment pathways earlier in life. Australia’s national newborn bloodspot screening is expanding with new indications and is progressing additional lysosomal storage disorders through its ministerial pathway, which will translate into incremental annual diagnoses in the near term. In China, a regional registry covering 161,966 newborns from 2018 to 2024 documented an inherited metabolic disease incidence of 1 in 2,842 live births, a significantly higher detection rate than several prior cohorts, which underscores the impact of tandem mass spectrometry scale-up. New Zealand’s national funding expanded to include 14 phenylketonuria supplements in 2024, improving continuity of care for a small but growing cohort of users. Ontario updated its covered list in March 2025 to include 48 phenylketonuria-specific medical foods while changing how pharmacologic agents are approved, which shapes first-line therapy choice and budget impact. A 2025 multi-country analysis of genomic newborn screening programs showed strong convergence on a core set of genes, and it quantified the predictors that drive inclusion decisions, which can help harmonize and prioritize future expansions across geographies.

Medical Nutrition Innovation (GMP-Based, Ready-to-Drink) Improving Adherence

Glycomacropeptide-based formulas are improving palatability and helping patients meet protein-equivalent targets with lower phenylalanine content per gram, which supports adherence in children and adults. Suppliers have introduced ready-to-drink options with higher vitamin D content, resealable formats, and lower volume per gram of protein equivalent to reduce daily burden and improve fit with school and work schedules. Manufacturers have expanded recipe variants and launched products targeted to homocystinuria and maple syrup urine disease with added inulin and DHA, which address micronutrient gaps and support gut comfort and neurodevelopment goals. Ingredient platforms with reduced phenylalanine loads and improved immunological properties are gaining traction in patients with heightened sensitivity. Investments in European production lines for powder formats have modernized packaging, boosted shelf stability, and phased out sachets, which can reduce waste and improve inventory management for clinics and pharmacies. These changes together make adherence more achievable over long periods without introducing new complexity into daily routines.

Specialty Pharmacy and Patient-Support Hubs Improving Access

Patient access is improving as rare disease pharmacies expand capacity, add geographic redundancy, and integrate digital tools for benefit verification and prior authorization. A new 30,000 square-foot fulfillment facility with extensive cold-chain storage strengthens overnight coverage and throughput for temperature-sensitive shipments. Non-commercial dispensing arrangements and liaison models connect prescribers, payers, and patients, which compresses time to therapy and sustains high satisfaction scores. Manufacturer programs enroll the vast majority of insured patients, reduce out-of-pocket costs for eligible beneficiaries, and provide in-person injection training and diet integration guidance where required. Condition-specific case management and hub services help patients navigate coverage, copay foundation grants, and specialty pharmacy shipments across metabolic cohorts. Charitable assistance has consolidated under a unified program that issues grants for copays, coinsurance, premiums, and point-of-sale pharmacy needs across more than 130 funds, offering real-time eligibility and virtual pharmacy cards to streamline claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High therapy and medical food costs constraining access | -1.3% | Global, acute in APAC and MEA | Medium term (2–4 years) |

| Lifelong diet adherence challenges reducing real-world effectiveness | -0.9% | Global | Long term (≥ 4 years) |

| REMS/anaphylaxis risks limiting enzyme therapy uptake | -0.6% | North America and EU | Short term (≤ 2 years) |

| Pipeline uncertainty (gene therapy/editing durability, program terminations) | -0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy and Medical Food Costs Constraining Access

Total cost of care remains high and can exceed available assistance in certain payer segments, which delays starts and interrupts refills. Many patients rely on a combination of manufacturer copay support and foundation grants, yet annual grant caps do not always match full-year therapy costs, so layering of resources and hub navigation is often required. Access to programs from manufacturers can reduce out-of-pocket costs to very low levels for eligible commercially insured patients, but public program beneficiaries may experience shortfalls without supplemental aid. Public payers in some provinces and countries have expanded lists of covered medical foods for inherited metabolic diseases, which supports dietary management, though policy differences can still create uneven coverage. For ultra-rare indications, compassionate-use and free-goods initiatives have emerged to bridge affordability gaps across low- and middle-income countries. Even with these measures, benefit verification, prior authorization, and appeal cycles can extend timelines and heighten the risk of treatment gaps where pharmacy hub support is not integrated.

Lifelong Diet Adherence Challenges: Reducing Real-World Effectiveness

Dietary restriction over a lifetime is difficult to maintain, and non-adherence in adolescence and adulthood remains common, which can compromise metabolic control and quality-of-life outcomes. Evidence links lapses in dietary control to neurocognitive impacts, including attention and executive function challenges, which underscores the importance of sustained adherence support. Enzyme therapy and BH4-pathway agents can enable diet liberalization for certain patients, but careful monitoring and coaching are often required, especially where payer coverage for medical foods varies. Medical nutrition suppliers have improved palatability and micronutrient fortification to support long-term adherence, and programs led by clinical centers provide education and community engagement to help patients sustain habits through key life transitions. The gut microbiome profile in patients on restricted diets shows distinctive patterns and emerging biomarkers, which is prompting broader nutritional and clinical strategies to maintain metabolic control without unintended long-term effects. Continuous monitoring with real-world data, supported by patient-support hubs and registries, can improve visibility into adherence risks and inform timely interventions by care teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Phenylketonuria accounted for 44.08% in 2025 and is projected to grow at 8.10% CAGR from 2026 to 2031, reflecting broadened age access and the arrival of a BH4 precursor approved for patients one month and older. PKU’s share is supported by newborn screening penetration, which ensures early diagnosis and structured care across large health systems, while trial and registry evidence has demonstrated clinically meaningful reductions in phenylalanine with approved pharmacologic options. Outside PKU, maple syrup urine disease, homocystinuria, and tyrosinemia comprise a sizable minority of cases in treated populations in many regions and benefit from growing screening coverage . A new therapy for alkaptonuria, approved in 2025, has opened a first treatment path for a previously unmanaged ultra-rare condition, supported by a companion access program to extend availability in select countries [2]Cycle Pharmaceuticals, “HARLIKU Tablets Receive First FDA Approval as Treatment for Alkaptonuria,” . Policy updates and technology improvements are raising detection rates across certain Asia Pacific geographies, which will expand the patient funnel for both dietary and pharmacologic interventions through the forecast period.

PKU’s leadership reflects an ecosystem that covers dietary management, BH4-pathway agents, and enzyme substitution, which together anchor outcomes-focused care pathways under specialist oversight. The enzyme therapy’s United States and EU risk management frameworks include education and readiness measures for anaphylaxis management, which concentrate administration within trained centers and hubs. For homocystinuria, enzyme replacement and oral enzyme candidates have reported clinical progress and regulatory designations, with a Phase 3 program paused for manufacturing scale-up and pre-IND work continuing for an oral enzyme therapy. mRNA efforts targeting the same pathway have also received rare pediatric and orphan designations, indicating a broadening toolkit for long-term control. Taken together, these dynamics keep PKU at the forefront of the amino acid disorders treatment market while gradually addressing other indications in the disorder mix, and they support multi-year therapeutic innovation that balances safety, efficacy, and real-world adherence. PKU captured 44.08% of amino acid disorders treatment market share in 2025 as broader access and supportive care models reinforced uptake in newborn-screened cohorts.

By Treatment Modality: Medical Nutrition Holds Share, Investigational Therapies Race Ahead

Medical nutrition held 55.32% of revenue in 2025, with GMP-based and free amino acid formulations anchoring daily intake targets in pediatric and adult populations. Suppliers rolled out ready-to-drink formats with high vitamin D levels and lower volume per gram of protein equivalent, which reduced consumption burden and improved suitability for life and work routines. Innovation extended beyond PKU to include homocystinuria and maple syrup urine disease formulas with inulin and DHA, while ingredient platforms reduced phenylalanine content and improved gastrointestinal comfort for sensitive patients. European production investments modernized packaging and storage for powders, which supports hospital and retail workflows and reduces waste from sachet formats. Over the forecast period, the investigational and advanced category is projected to grow faster than the overall amino acid disorders treatment market as enzyme-replacement, oral enzyme, mRNA, and BH4-precursor approaches advance regulatory and manufacturing readiness.

Pharmacotherapy remains central to diet liberalization for many patients as a BH4 precursor with a broad United States and EU label expands options, and enzyme therapy continues to normalize phenylalanine for appropriate candidates within REMS frameworks. From 2025 to 2026, portfolio reassessments and program discontinuations in gene-editing underscore immune-barrier challenges in liver-directed delivery, which is encouraging a shift of investment toward modalities with nearer-term scalability . Medical nutrition will continue to anchor daily control in a wide patient base as advanced options expand, and improvements to palatability, density, and formats will keep medical foods essential to long-term management. The amino acid disorders treatment market size tied to investigational and advanced modalities is projected to expand alongside improved manufacturing and distribution readiness for parenteral and oral programs.

By Route of Administration: Parenteral Gains Share Through Enzyme Therapy Expansion

Oral formulations held 65.23% of 2025 revenue, covering powders, ready-to-drink formulas, and oral pharmacotherapies, while parenteral and subcutaneous routes are projected to grow faster than the overall market due to enzyme therapy use and administration under trained oversight. Adolescent label expansion in 2026 extends enzyme therapy’s use to an earlier age band, which adds to the base of subcutaneous users and positions centers for real-world safety and response monitoring. Parenteral delivery also includes intravenous amino acid solutions approved for acute decompensation in settings where oral or enteral regimens are not feasible, which expands use beyond chronic home management into critical care environments. Oral routes continue to dominate through broader BH4-precursor labeling and widespread medical nutrition use in both pediatric and adult care pathways.

The REMS framework and education programs for enzyme therapy encourage careful site-of-care selection and observation periods, which concentrate initiation in specialized clinics and integrated hubs that can support adverse event management and dose titration. Over the forecast horizon, parenteral growth benefits from expanding age eligibility and incremental patient additions, not a step-change in prevalence, which supports steady uptake at experienced centers with the capacity for training and monitoring. The amino acid disorders treatment market continues to reflect a dual-route reality where oral formats maximize reach and convenience and parenteral options unlock diet liberalization for specific patient profiles under specialist supervision. Oral formulations remain a first-line foundation, and parenteral therapies contribute to improved metabolic control where indicated and supported by patient preference and clinical judgment.

By Distribution Channel: Online Pharmacies Accelerate Through Digital Hub Integration

Hospital pharmacies captured 48.22% of 2025 revenue as the primary dispensing point for enzyme therapies, parenteral amino acid solutions used during acute decompensation, and medical nutrition starter kits for newborns. Online pharmacies are set to outpace the overall amino acid disorders treatment market through digital hub integration, e-portals, and adjacent access services such as benefit verification, copay navigation, and cold-chain management. Specialty hubs are expanding non-commercial dispensing relationships and manufacturer partnerships to compress time to therapy and maintain high program satisfaction as measured by partner recommendation and NPS metrics.

Manufacturer patient-support programs, including dedicated case management and training for self-injection, underpin adherence and smooth channel handoffs from clinic to home. Charitable assistance has consolidated under a single program that issues copay and pharmacy grants across more than 130 disease funds, guided by real-time eligibility checks and virtual cards to reduce point-of-sale friction. Retail pharmacies retain a role for oral agents and certain medical foods, but rare-disease limited distribution networks centralize dispensing with accredited rare hubs to ensure safety, monitoring, and temperature control. The channel mix will continue to reflect manufacturer preferences for limited networks that deliver REMS compliance and access services while leveraging hospital pharmacies for initiations and acute settings.

Geography Analysis

North America held 52.11% of revenue in 2025 and is expected to grow at a steady rate through 2031, supported by label expansions for enzyme therapy and approved BH4-precursor options that broaden community management pathways. The region benefits from strong specialist networks, integrated patient-support hubs, and manufacturer programs that enroll the vast majority of insured patients and reduce out-of-pocket costs for many commercially covered beneficiaries. Portfolio updates show that products facing generic competition have seen revenue pressure, while enzyme therapies and growth assets in rare-disease portfolios continue to climb. Provincial policy adjustments in Canada have refined coverage for medical foods and certain pharmacologic therapies, shaping first-line choices and referral patterns to exceptional access pathways. In the United States, education and monitoring requirements under REMS concentrate enzyme therapy use within trained centers, which aligns with limited distribution networks and integrated hubs for dispensing.

Europe maintains a large, treated base with universal newborn screening in key markets and region-wide approvals for both enzyme therapy and a BH4-precursor agent that covers infants through adults. Regulatory documents outline safety considerations, education requirements, and monitoring for hypophenylalaninemia, which are embedded into national risk management plans and patient education programs. European manufacturers have upgraded medical nutrition production capacity and packaging, which streamlines hospital and retail pharmacy logistics and supports consistent shelf availability. A therapy for alkaptonuria approved in 2025 demonstrates Europe’s role in global orphan portfolios and companion access strategies that include multi-country free-goods programs in lower-income settings.

Asia Pacific is projected to post a 5.24% CAGR through 2031, with the largest boost from newborn screening expansion and higher inherited metabolic disease detection rates in China and several other countries that have scaled tandem mass spectrometry. Australia’s national program is adding multiple conditions and has advanced additional lysosomal storage diseases through the ministerial decision pathway, which will produce incremental annual diagnoses and add to medical nutrition and pharmacotherapy demand. New Zealand extended funding for 14 phenylketonuria supplements in 2024, which supports adherence and continuity of care in a small patient population[3]Pharmac, “Decision to Fund Supplements for Phenylketonuria and Other Inherited Metabolic Diseases". In South America, access initiatives from manufacturers expand the availability of therapy in select countries, and similar programs in parts of the Middle East and Africa help patients where reimbursement remains limited. Across these regions, convergence on core gene lists in genomic newborn screening is likely to harmonize future protocols, which can standardize case finding and accelerate therapy uptake in the treatment of amino acid disorders.

Competitive Landscape

The amino acid disorders treatment market features a leader in enzyme therapies with a diversified rare-disease portfolio and expanding age access, while a BH4-precursor entrant with broad labeling is building share among responsive patients. Reported results in 2025 and 2026 show enzyme-focused revenue growth and portfolio prioritization that directs investment to high-potential assets and away from programs facing immunogenicity hurdles. In PKU, the enzyme therapy’s REMS and education programs are designed to manage anaphylaxis risks and ensure self-injection competence, which shapes site-of-care decisions and hub selection. For alkaptonuria, a 2025 approval created a first-in-class option, supported by a dedicated support program to reach eligible patients. In 2025, European authorization of a BH4 precursor and United States approval the following month established a global footprint, with patient-support resources facilitating onboarding and follow-up.

Medical nutrition leaders compete on palatability, protein-equivalent density, micronutrient fortification, and convenient formats, with notable activity in ready-to-drink formulations and ingredient innovation. Ready-to-drink GMP solutions with high vitamin D levels and compact serving volumes support daily adherence in busy settings. Innovations extend into indication-specific formulas that incorporate inulin and DHA and come with kosher certifications, offering better alignment to patient preferences and needs. Ingredient platforms with lower phenylalanine content help patients with sensitivity while improving immunological responses and blood-brain barrier amino acid competition profiles. Production investments in Europe have modernized powder packaging and supported sustainable manufacturing footprints. Adjacent nutrition portfolios from large manufacturers add to the ecosystem by serving patients who require amino acid-based or peptide-based alternatives when intact proteins are not tolerated.

Specialty pharmacy and hub technology are strategic differentiators as manufacturers and pharmacies co-develop programs that compress time to therapy and maintain adherence at scale. A new fulfillment center with expanded cold-chain storage enhances geographic redundancy and overnight coverage. AI-enabled hub platforms, therapy-specific care teams, and 24/7 pharmacist access are being deployed to improve benefit verification and refill continuity. Collaboration models that link providers, hubs, biopharma, and specialty pharmacies aim to reduce payer friction and accelerate onboarding. Portfolio moves in 2025 and 2026 show companies emphasizing high-potential enzyme therapy franchises and adding assets through M&A in adjacent rare disease categories, reflecting continued appetite for growth platforms in complex care. The amino acid disorders treatment market will continue to blend pharmacotherapy and medical nutrition advances with access infrastructure that supports safe initiation and sustained adherence.

Amino Acid Disorders Treatment Industry Leaders

BioMarin Pharmaceutical Inc.

Nestlé Health Science

Takeda Pharmaceutical

Merck & Co., Inc.

PTC Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: BioMarin Pharmaceutical received FDA approval for PALYNZIQ (pegvaliase-pqpz) in adolescents aged 12–17 with phenylketonuria, expanding access to a younger cohort and building on prior adult use.

- July 2025: PTC Therapeutics announced FDA approval of Sephience (sepiapterin) for hyperphenylalaninemia in children and adults one month and older, following European Commission authorization.

- July 2025: Cycle Pharmaceuticals received FDA approval for HARLIKU (nitisinone) Tablets for alkaptonuria and launched a patient support program

- June 2025: Ajinomoto Cambrooke marked its 25th anniversary and launched Homactin AA Plus and Vilactin AA Plus, ready-to-drink formulas tailored for homocystinuria and maple syrup urine disease

Global Amino Acid Disorders Treatment Market Report Scope

| Phenylketonuria (PKU) |

| Maple Syrup Urine Disease (MSUD) |

| Homocystinuria (HCU) |

| Tyrosinemia |

| Arginase 1 Deficiency (ARG1-D) |

| Medical Nutrition |

| Pharmacotherapy |

| Investigational/Advanced Modalities |

| Oral |

| Parenteral/Subcutaneous |

| Hospitals Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disorder Type | Phenylketonuria (PKU) | |

| Maple Syrup Urine Disease (MSUD) | ||

| Homocystinuria (HCU) | ||

| Tyrosinemia | ||

| Arginase 1 Deficiency (ARG1-D) | ||

| By Treatment Modality | Medical Nutrition | |

| Pharmacotherapy | ||

| Investigational/Advanced Modalities | ||

| By Route of Administration | Oral | |

| Parenteral/Subcutaneous | ||

| By Distribution Channel | Hospitals Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the amino acid disorders treatment market through 2031?

The amino acid disorders treatment market size reached USD 1.38 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at a 7.57% CAGR.

Which indication contributes the largest value within amino acid disorder treatments?

Phenylketonuria leads by value, supported by broad newborn screening coverage and expanded access to enzyme therapy and BH4-pathway options.

Which channels are growing fastest for therapy access and refills?

Online specialty pharmacies are expanding faster than the overall market due to integrated benefit verification, prior authorization support, and cold-chain fulfillment.

How are policy changes shaping diagnosed populations in Asia Pacific?

Expanded newborn screening and higher detection rates in parts of China and other countries are growing diagnosed cohorts and widening treatment pathways.

What role will medical nutrition play as new pharmacotherapies enter care pathways?

Medical nutrition remains foundational for daily control and is evolving with GMP-based ready-to-drink formats that improve palatability and convenience, complementing pharmacologic approaches for diet liberalization.

How are patient-support hubs affecting time to therapy?

Integrated hubs from specialty pharmacies and manufacturers compress time to therapy through coordinated benefits, training, and refill support, improving adherence for complex regimens.

Page last updated on: