Aircraft Paint Services Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

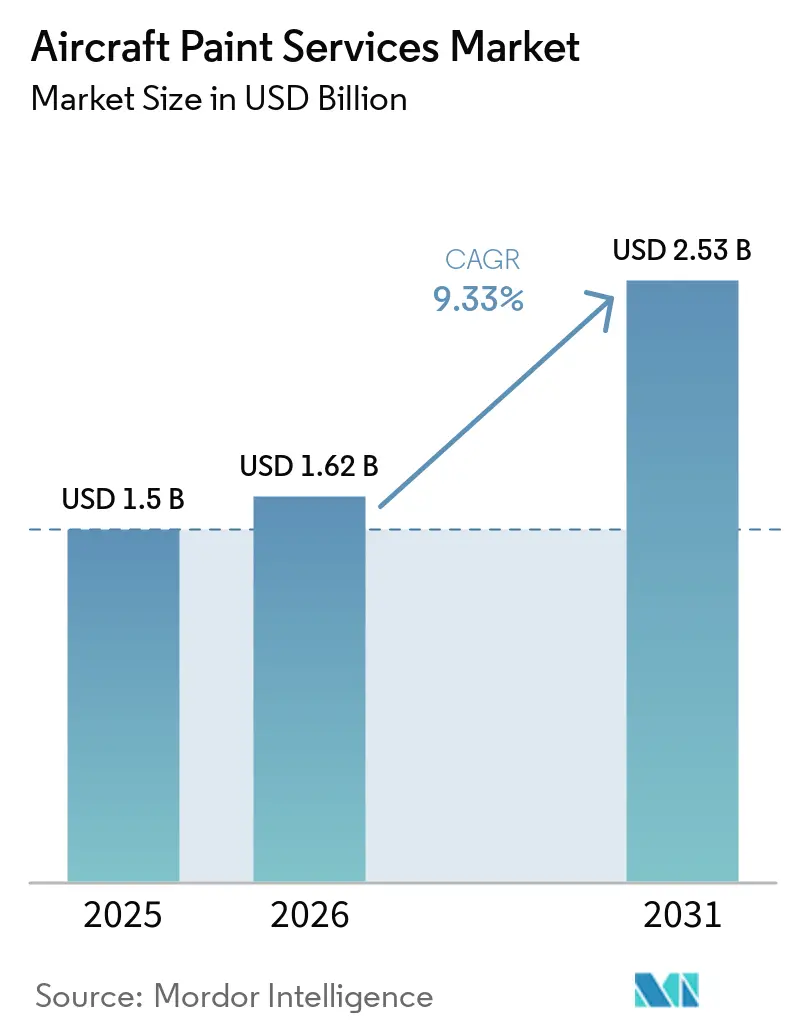

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 9.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Paint Services Market Analysis by Mordor Intelligence

The aircraft paint services market size is expected to grow from USD 1.50 billion in 2025 to USD 1.62 billion in 2026 and is projected to reach USD 2.53 billion by 2031, at a 9.33% CAGR over 2026-2031. First-paint volume is supported by new aircraft handovers, with Airbus reporting 793 deliveries in 2025, sustaining baseline demand even as supply chain constraints moderated build rates. The end-user composition remains dominated by airlines and lessors, highlighting the influence of lease transition cycles and fleet turnover on paint-shop activity during a given quarter. Advances in base-coat and clear-coat systems, chrome-free primers, and lightweight cabin coatings are reshaping turnaround times, warranty compliance, and lifecycle economics, thereby improving the value proposition for operators seeking to reduce ground time without compromising durability. North America remains the largest regional base by revenue share. At the same time, Asia-Pacific is set to expand the fastest on the back of significant fleet additions, especially in India, where official projections point to a sharp increase in active aircraft and in-country MRO capability. Regulatory and programmatic funding signals in Europe, including European Defence Fund allocations for propulsion and loyal-wingman capabilities, add a structural boost to unmanned demand that will flow into paint-service requirements through 2031.

Key Report Takeaways

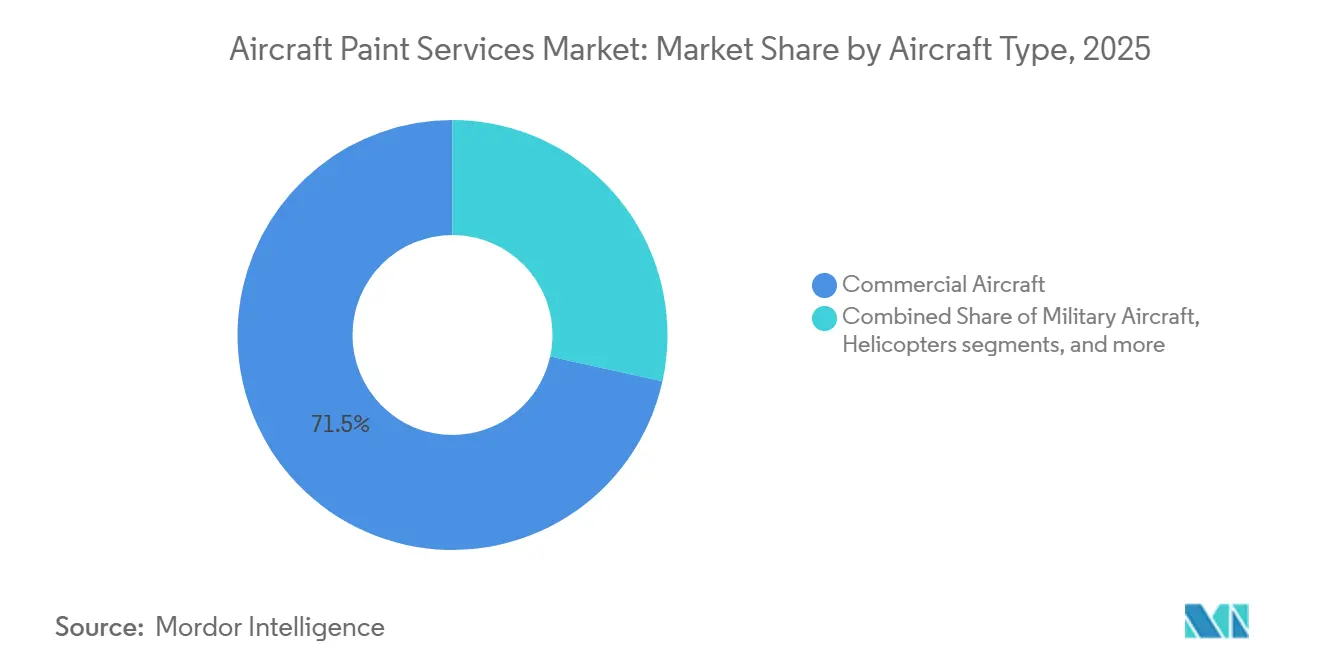

- By aircraft type, commercial aircraft accounted for a 71.54% share of the aircraft paint services market in 2025; unmanned aerial vehicles are projected to expand at a 14.53% CAGR through 2031.

- By service type, exterior painting accounted for 54.55% of the aircraft paint services market in 2025; custom livery is expected to grow at a 12.50% CAGR through 2031.

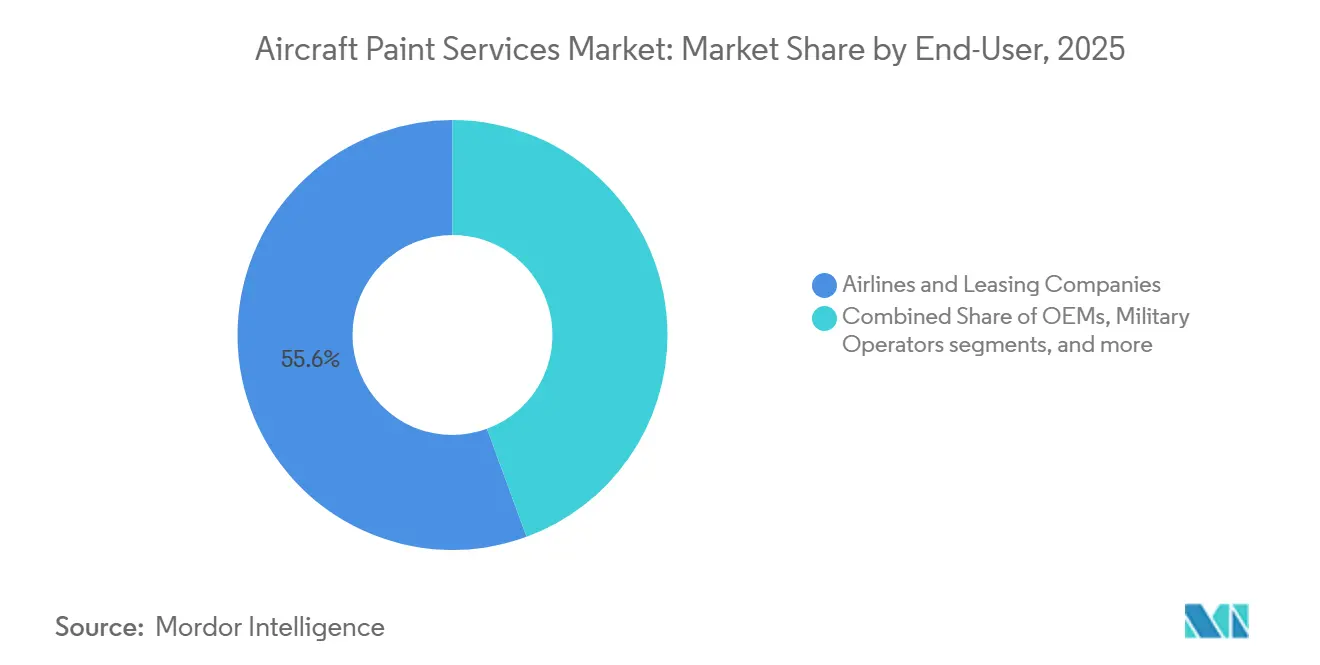

- By end user, airlines and leasing companies captured 55.60% of the aircraft paint services market in 2025; business jet operators are forecast to record an 11.65% CAGR through 2031.

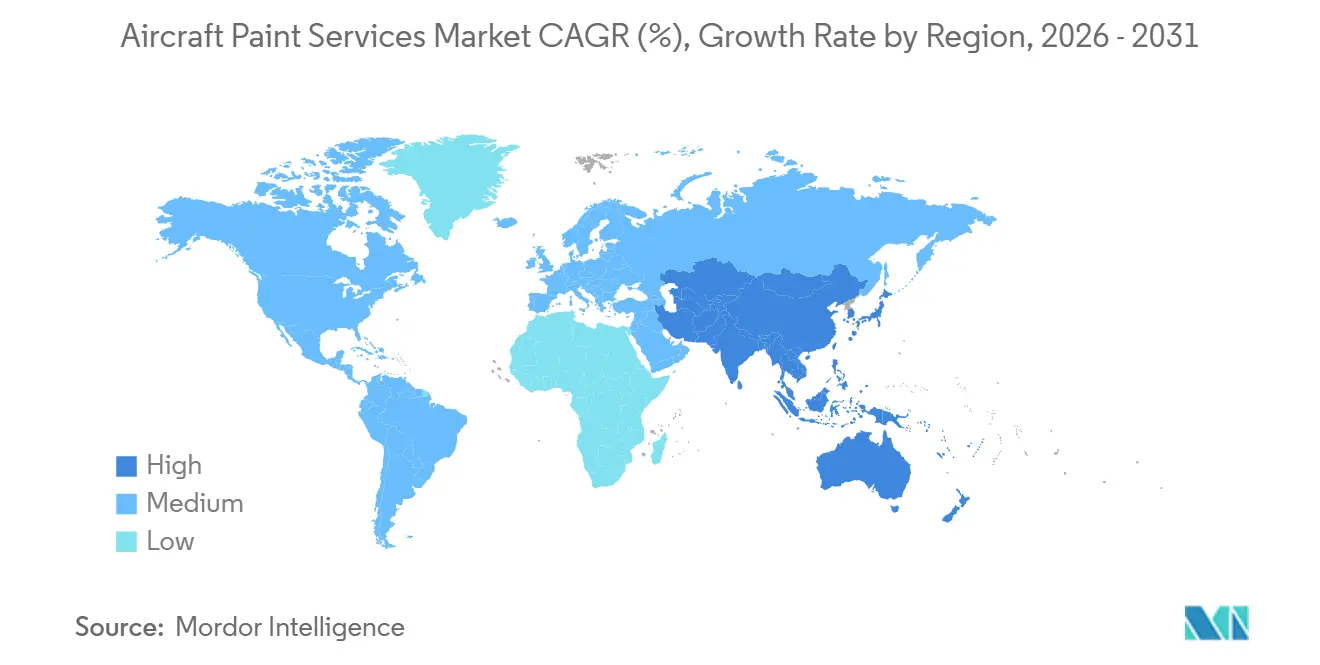

- By geography, North America held 34.05% share of the aircraft paint services market in 2025; Asia-Pacific is projected to post an 11.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aircraft Paint Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of base-coat/clear-coat systems to cut TAT | +3.5% | Global, particularly North America and Europe MRO hubs | Short term (≤ 2 years) |

| Fleet expansion of low-cost carriers | +3.2% | Global, with Asia-Pacific (India, Southeast Asia) and Middle East as epicenters | Medium term (2-4 years) |

| Up-gauging of widebody aircraft by major airlines | +2.8% | North America, Europe, Middle East legacy hubs | Medium term (2-4 years) |

| DER-approved chrome-free primers unlocking US DoD work | +2.4% | North America (US military installations), spill-over to NATO allies in Europe | Medium term (2-4 years) |

| Stringent OEM warranty requirements on paint longevity | +2.1% | Global, concentrated in OEM delivery centers (Airbus Hamburg/Mobile, Boeing Everett/Charleston) | Long term (≥ 4 years) |

| Green UV-cured cabin top-coat for reduced VOC emissions | +1.9% | Global, earliest adoption in Europe (REACH compliance zones) and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion of Low-Cost Carriers

Boeing projects delivery demand for 43,600 new commercial airplanes by 2044, with single-aisle types accounting for the vast majority, aligning well with low-cost carrier fleet profiles that intensify repaint cycles and first-paint volume in the aircraft paint services market.[1]Source: Boeing Market Analysis Team, “Commercial Market Outlook 2025–2044,” Boeing, boeing.com India exemplifies the expansion path, with official planning documents outlining a domestic fleet that could more than double by 2031 and a policy agenda designed to localize maintenance, repair, and paint capability within national borders. Airbus supported throughput with 793 commercial deliveries in 2025, and a meaningful portion of those aircraft moved through certified bays at delivery centers that standardize paint quality under warranty terms. Shorter repaint intervals are often a strategic decision for high-utilization carriers, aimed at maintaining brand and asset value. This approach supports a consistent workflow for paint shops, even during periods of reduced lease transitions, ensuring the market remains tied to recurring workscopes. Fiscal incentives and customs simplification in India are intended to reduce ferry costs and expand domestic supply, encouraging new hangar development near major hubs and supporting locally executed repaints that had previously been moved offshore.

Up-Gauging of Widebody Aircraft by Major Airlines

Network carriers are increasing long-haul capacity by up-gauging, which involves widebody aircraft repaint events. These events require more labor hours and materials per cycle, leading to higher average ticket sizes per slot for providers and enabling premium pricing in the market. Boeing’s long-term outlook indicates a large-scale replacement wave for in-service airplanes over the next two decades, a pattern that extends economic lives in the near term and sustains repaint and refinishing demand as fleets bridge to new types. Delivery centers and MRO capacity configured for wide bodies operate with higher utilization thresholds, which channel more work to certified sites such as the Airbus-linked paint complex in Mobile, which has expanded to manage recurring volume under multi-year contracts. Capacity scale and certification status remain strategic differentiators, and operators prize predictable turnaround in climate-controlled widebody bays that can integrate structural checks and refinishing during the same visit, reducing ground time. Warranty-compliant application and airworthiness oversight under European and US frameworks continue to set minimum performance standards for durability and adhesion, shaping repaint timing and supplier selection.

Stringent OEM Warranty Requirements on Paint Longevity

OEMs embed paint-performance clauses into delivery documentation that tie corrosion protection and cosmetic durability to warranty coverage. This practice pushes operators to plan refinishing on shorter intervals as warranties approach expiration. Lessors maintain this discipline during redelivery by inspecting gloss retention and verifying film thickness and adhesion against established thresholds, emphasizing the importance of certified systems and processes in the market. Coating vendors that meet accelerated-weathering and chemical-resistance criteria earn approved status at the OEM level, and these endorsements limit competitive entry and align paint choices with warranty eligibility. Material and process innovation has accelerated, with automated spray solutions and process control introduced to reduce variability, following earlier adhesion concerns on new-generation airframes that prompted closer scrutiny of primer and application windows. Vertically integrated solutions that combine cabin modification and exterior refinishing under a single program help airlines satisfy concurrent warranty and airworthiness requirements in fewer visits, which strengthens provider stickiness over the planning horizon.

Rapid Adoption of Base-coat/Clear-coat Systems to Cut TAT

Next-generation base-coat and clear-coat chemistries enable same-day color and protective layer application, reducing typical ground time by several days and boosting hangar throughput across the market. easyJet is rolling out a lightweight three-layer system across a subset of its fleet, reducing per-airframe mass by 27 kg, with plans to scale by 2030 to capture fuel and emissions savings at the fleet level.[2]Source: easyJet Media Team, “easyJet Trials New Paint That Lowers the Weight and Fuel Burn of the Aircraft in a World First,” easyJet, easyjet.com Operators recognize the combined benefit of faster curing and weight reduction, which together improve revenue days and operating cost while maintaining appearance standards. Airlines in capacity-constrained geographies have reported efficiency gains from rapid-cure and low-VOC exterior systems as well as simplified interior refinishing sequences that remove steps and reduce labor-hour requirements. OEM-approved materials and digital training programs further standardize application quality, which helps align warranty compliance with faster turn times at certified paint shops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising labor-hour costs in EU and US MRO hubs | -2.9% | Western Europe (Germany, France, UK) and US Sunbelt/Northeast wage zones | Long term (≥ 4 years) |

| Highly cyclical airline maintenance budgets | -2.7% | Global, acute in emerging markets (South America, Africa) during economic downturns | Short term (≤ 2 years) |

| Limited availability of large-bay paint hangars | -2.3% | North America and Europe mature MRO hubs, critical shortage in Asia-Pacific growth corridors | Medium term (2-4 years) |

| Volatility in titanium-dioxide prices | -1.6% | Global, with supply concentrated in China (60% global capacity) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Highly Cyclical Airline Maintenance Budgets

Lease transition cycles are expected to decline through late 2025 as operators extend leases while awaiting delayed deliveries, reducing demand for short-notice repaint projects and prompting paint providers to rely on long-term volume contracts to maintain stable utilization. Airlines prioritized flight operations during peak travel windows and deferred cosmetic work where corrosion limits allowed, which pulled discretionary spend into narrower seasonal windows and constrained shop schedules. Providers with multi-year agreements and OEM-linked volume, including those serving Airbus final-assembly lines, kept baseline throughput above break-even, which proved decisive during softer quarters. Smaller independents faced price pressure and lower slot certainty in this environment, and many pivoted to adjacent workscopes or sought alliances that could smooth demand across cycles. The net effect is a sharper divide between capacity guaranteed by multi-year commitments and opportunistic volume that fluctuates with macro conditions and lease schedules, which prolongs volatility for providers without anchor contracts.[3]Source: Vallair Editorial Team, “MRO Management Nov–Dec 2025 – 2026 Outlook,” Vallair, vallair.aero

Limited Availability of Large-Bay Paint Hangars

Climate-controlled large-bay infrastructure is tight in mature hubs, and permitting timelines plus environmental compliance requirements elongate project delivery, which caps near-term expansion potential in the market. Europe has seen targeted investments to alleviate congestion, with Magnetic Group’s three-hangar project in Tallinn designed to raise paint capacity while preserving EASA certifications in a cost-competitive location. The Middle East is adding specialized capacity as well, with a new Dubai South facility positioned to serve regional fleets that treat liveries as a core brand element and cycle through heavy checks on predictable intervals. Network planning and slot allocation remain complex at airports where runway availability and taxi-time constraints limit the sites where hangars can be built or expanded, which pushes providers to satellite locations with better land availability. Ferry requirements can erode some of the wage arbitrage benefits when aircraft must travel long distances to reach available bays, reinforcing the value of regional density and multi-bay campuses near final-assembly or maintenance clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: UAVs Outpacing Legacy Manned-Fleet Growth

Commercial aircraft accounted for 71.54% of the market share in 2025, driven by Airbus's 793 deliveries. These deliveries supported consistent first-paint flow and airline rebranding initiatives associated with new fleet introductions. This scale effect remains a key anchor for the market, underpinning utilization at delivery centers and certified sites that manage warranty-compliant applications and rapid turnarounds for single-aisle types.

UAVs will expand the fastest at a 14.53% CAGR through 2031, propelled by European Defence Fund support for loyal-wingman propulsion development of EUR 20 million (USD 21.6 million) and the proliferation of reconnaissance and patrol missions that require corrosion-resistant and mission-specific coatings. Military aircraft continue to provide steady repaint cycles through depot maintenance and the transition to chrome-free primers aligned to US and allied requirements, which directs a share of capacity to DER-qualified shops that can bundle airworthiness documentation with surface treatment and exterior finishing. General aviation aircraft and helicopters form stable niche streams driven by saltwater corrosion exposure and mission needs rather than branding cadence, which sustains smaller-bay operations and specialty coating workscopes.

The evolving procurement trends for unmanned platforms introduce specific workflow requirements for the industry. These include masking for sensors, low-observable topcoats when specified, and ensuring mission durability while maintaining a lower total paint mass per unit compared to larger commercial models. As defense budgets prioritize collaborative combat aircraft and surveillance fleets, qualified providers will see a higher mix of military specifications in their order books, which increases documentation intensity and certification oversight per slot. For commercial fleets, repaint timing remains closely linked to branding programs, warranty milestones, and corrosion-control windows, and this triangle of drivers continues to define line-flow predictability for high-throughput shops focused on narrowbody programs. The result is a bifurcated workload, with recurring single-aisle events setting the drumbeat and specialized unmanned or military projects layering on higher-margin but more variable schedules across the market.

By Service Type: Custom Livery Monetizing Brand Differentiation

Exterior painting accounted for 54.55% of the projected 2025 revenue, highlighting its critical role in providing corrosion protection and warranty-compliant finishes that ensure aircraft remain operational and meet market appearance standards. Custom livery is the fastest-growing segment, with a 12.50% CAGR through 2031, as airlines convert special events into brand amplification that justifies premium pricing for complex masking, multiple color transitions, and metallic or pearlescent effects. High-visibility cases, such as Cathay Pacific’s 80th-anniversary A350 livery, highlight how carefully staged campaigns generate earned media and push liveries to the forefront of brand strategy in a crowded marketplace. Interior painting supports cabin refresh programs and passenger-experience upgrades, and the category benefits from process consolidation that removes steps and reduces labor hours per widebody refresh when using new-generation fillers and primers. Specialized services, including stripping, partial repaints, and protective layups, round out the mix, and their cadence reflects lease schedules and residual-value protection for lessors that track appearance and film thickness throughout the term.

Airlines increasingly evaluate paint choices through the lens of operational efficiency, driving the adoption of lightweight, rapid-cure systems as part of broader fuel and emissions strategies within the aircraft paint services industry. easyJet’s program exemplifies this shift with tangible weight and emissions outcomes alongside the throughput benefits of shorter cure windows at hangar level, and similar approaches are surfacing in Asia and Europe through low-VOC and humidity-cure technologies. As multi-color and heritage schemes move from one-off events to rolling campaigns, providers are scaling design, approval, and execution workflows to standardize complex projects without extending ground time, helping stabilize margins on a product mix that has historically been labor-intensive. The outcome is a service landscape where basic exterior jobs remain the baseline activity, while custom liveries and interior streamlining account for a growing share of differentiation and margin in the market.

By End-User: Business Jet Operators Exploiting Backlog Growth

Airlines and leasing companies captured 55.60% of end-user revenue in 2025 as scale buyers leveraged multi-year agreements and proximity to delivery centers to secure predictable throughput across the market. Business jet operators are expected to grow at an 11.65% CAGR through 2031, driven by strong backlogs that feed completion-center activity, owner-driven liveries, and cabin finishes that demand bespoke execution. OEMs and completion houses have responded by adding specialized capacity to integrate paint with interior completions, reducing handoffs and compressing program timelines for high-net-worth (HNW) and corporate buyers. Military operators contribute consistent demand through depot cycles and chrome-free transitions, which funnel work to DER-approved providers that can sign airworthiness documentation and coordinate with defense customers on specification control. Deployable corrosion-control and protection capabilities are also emerging for forward locations, which expands the use cases for chrome-free primers and topcoats within defense networks.

Across end users, contract structure and certification define provider selection and pricing power in the market. Airlines and lessors tend to bundle repaints with heavy checks or delivery events to reduce ground time. At the same time, business jet customers value bespoke execution and are more likely to pay for premium slots and expedited delivery. Defense customers emphasize qualification and repeatability, which narrows the field to shops with the right materials approvals, test data, and documentation practices for government oversight. Regional capacity additions in the Middle East and Europe are supplementing North American and Asian networks, helping align supply with user needs and reducing ferry exposure for certain missions. As a result, the end-user mix supports a diversified stream of projects that balance high-volume, standardized narrowbody work with specialized and higher-margin jobs across business and defense categories in the market.

Geography Analysis

North America held 34.05% in 2025 and remained the largest regional base for the market, supported by OEM delivery centers and multi-bay campuses in the southeastern US that concentrate first-paint work and high-throughput narrowbody programs. The Airbus-linked Mobile, Alabama, complex expanded to five paint bays and increased annual service capacity to manage recurring line flow under extended contracts, helping stabilize utilization during a period of deferred lease-transition work. The regional supply chain is tightening cycle times as well, with a major coatings investment in North Carolina that centralizes aerospace production and reduces lead times for shops across the Southeast. Certification density and workforce experience continue to support North America’s leadership position, even as wage inflation and labor availability remain strategic considerations for paint providers and MRO networks.

Asia-Pacific is projected to deliver the fastest growth trajectory at an 11.60% CAGR in market size through 2031, led by India’s fleet expansion and a policy agenda focused on in-country MRO and paint capabilities that reduce the historic reliance on overseas shops. Government documentation outlines a pathway for domestic paint facilities near major hubs. It suggests sizable demand growth as the national fleet scales to 2031, which should lift regional throughput and shorten ferry distances for Indian operators. In China, incumbent coatings suppliers have long-standing partnerships with major carriers, and vendor programs around training and process standardization continue to support quality and compliance within local fleets. Capacity remains clustered in a handful of metro areas, so cross-border routing to regional hubs in Southeast and East Asia continues for complex projects, especially when widebody bays and custom-livery capabilities are required.

Europe maintains a substantial market share through certified providers and targeted expansions, including a three-hangar complex in Tallinn scheduled to increase paint capacity while maintaining compliance with EASA standards. The Middle East continues to add dedicated paint infrastructure, such as the Dubai South facility designed for regional fleets with strong livery and branding requirements, which helps absorb demand from carriers cycling through heavy checks at regular intervals. South America and Africa remain more episodic in paint demand due to smaller fleet bases and capital-intensive infrastructure hurdles, which keep complex work gravitating toward established hubs with larger certified networks. Across regions, certification frameworks and OEM warranty requirements standardize execution and narrow provider selection, which favors multi-bay campuses and delivery-center partners that can assure throughput and turn times across the market.

Competitive Landscape

The aircraft paint services market is moderately consolidated, with specialized paint providers operating alongside vertically integrated MRO networks and OEM delivery centers that capture a sizable portion of first-paint volume. Specialists and diversified networks compete on a combination of turnaround time, certification depth, and proximity to customers, which has encouraged multi-year capacity agreements to insulate utilization from lease-transition volatility. MAAS Aviation extended its Airbus-linked program in Mobile and expanded to five bays, supporting an annual throughput that underpins steady revenue amid cyclical pressure for opportunistic repaint work. Sustainability credentials have also been incorporated into bid criteria for certain operators and lessors, benefiting providers that disclose environmental performance and invest in process efficiency. On the material side, suppliers are consolidating aerospace production and training investments in key locations, thereby shortening lead times and standardizing application practices for certified paint shops across the US and Asian clusters.

Competitive tactics reflect a blend of technology adoption and capacity placement. easyJet’s decision to deploy a lightweight three-layer coating system captures fuel and emissions savings while reinforcing the carrier’s brand and procurement preferences, and this is the type of program that can influence selection criteria for paint providers across Europe. Sherwin-Williams added approvals for exterior systems aligned with chrome-free mandates, broadening the qualified material set for military and commercial users preparing for regulatory deadlines. Defense users, such as Saab, have introduced deployable corrosion-control and protection modules designed for rapid setup at forward bases, which create new requirements for shops that support airframes returning from forward deployment. These moves, combined with OEM-linked capacity and delivery-center integrations, are shaping a landscape where scale, certification, and technology together define competitive position in the market.

Certification and warranty frameworks heighten barriers to entry. OEMs and regulators define the approved materials and process envelopes, thereby elevating the importance of vendor endorsements, accelerated-weathering data, and documented outcomes within specified cure windows. Providers that integrate cabin work with exterior repaint can compress customer ground time and deepen relationships across airframe families, which improves stickiness as fleets transition between heavy checks and appearance maintenance. Geographic density around final-assembly sites and business-aviation completion centers confers advantages in scheduling, ferry reduction, and line-of-sight access to materials, helping larger campuses maintain high utilization across seasonal market cycles. Through 2031, competitive position will likely hinge on multi-year customer agreements, qualified material portfolios, and a demonstrated ability to turn aircraft faster without compromising durability or warranty compliance.

Aircraft Paint Services Industry Leaders

Air Livery Limited

International Aerospace Coatings Limited

Singapore Technologies Engineering Ltd.

Lufthansa Technik Intercoat GmbH (Lufthansa Technik AG)

Expressair Aviation Limited (MAAS Aviation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Aerofleet Coatings Management introduced the Iris CMX, its second drone-based inspection tool. This innovative tool directly gauges coating performance with a specialized three-in-one contact sensor. In collaboration with Donecle, the Iris CMX captures accurate quantitative metrics for dry-film thickness, color, and gloss. This advancement elevates the accuracy, consistency, and repeatability of coating inspections. The Iris GVI drone, Aerofleet's existing tool, traverses a predetermined grid over an aircraft, capturing up to 600 high-definition photos during a comprehensive visual analysis. The coatings management software scrutinizes these images, identifying any coating issues or wear. With the integration of this sophisticated two-drone system, Aerofleet enhances its ability to pinpoint the optimal repainting time for an aircraft, moving beyond mere time- or flight-hour-based assessments.

- October 2025: MAAS Aviation extended its five-year agreement with Airbus for A320 and A220 aircraft painting in Mobile, Alabama. The facility, expanded in 2024 to include five paint bays with an annual capacity of 200 aircraft, supports Airbus’ growing single-aisle production. This agreement highlights the strategic importance of robust partnerships in scaling production, improving supply chain efficiency, and maintaining competitive positioning in the aerospace industry amid increasing demand for single-aisle aircraft.

- July 2025: MAAS Aviation’s extended agreement with Ryanair until 2035 reinforces its role in Ryanair’s fleet expansion strategy. Covering 500 aircraft repaints, the partnership integrates painting services with maintenance operations, ensuring efficiency and reduced downtime. This supports Ryanair’s growth to 800 aircraft and 300 million passengers annually by 2034.

Global Aircraft Paint Services Market Report Scope

The aircraft paint services market encompasses specialized services such as surface preparation, protective coating application, and aesthetic finishing. These services ensure compliance with aviation safety standards, enhance corrosion resistance, improve fuel efficiency through advanced coatings, and support airline branding through customized designs. Providers offer maintenance, repainting, and refinishing solutions to airlines, OEMs, and MROs, making paint services an essential aspect of aircraft lifecycle management and operational efficiency.

The aircraft paint services market is segmented by aircraft type, service type, end-user, and geography. By component, the market is segmented into commercial aircraft, military aircraft, general aviation aircraft, helicopters, and unmanned aerial vehicles (UAVs). By service type, the market is segmented into exterior painting, interior painting, custom livery, and others. By end-user, the market is segmented into airlines and leasing companies, OEMs, military operators, and business jet operators. The report also covers the market sizes and forecasts for the aircraft paint services market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Commercial Aircraft |

| Military Aircraft |

| General Aviation Aircraft |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

| Exterior Painting |

| Interior Painting |

| Custom Livery |

| Others |

| Airlines and Leasing Companies |

| OEMs |

| Military Operators |

| Business Jet Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Commercial Aircraft | ||

| Military Aircraft | |||

| General Aviation Aircraft | |||

| Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Service Type | Exterior Painting | ||

| Interior Painting | |||

| Custom Livery | |||

| Others | |||

| By End-User | Airlines and Leasing Companies | ||

| OEMs | |||

| Military Operators | |||

| Business Jet Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the aircraft paint services market size and growth outlook to 2031?

The aircraft paint services market size was valued at USD 1.50 billion in 2025 and is projected to reach USD 2.53 billion by 2031, registering a 9.33% CAGR over 2026-2031.

Which aircraft type drives the largest share today and which segment grows fastest?

Commercial aircraft accounted for 71.54% in 2025, while unmanned aerial vehicles are projected to grow fastest at a 14.53% CAGR through 2031.

Which regions lead and which region is the near-term growth hotspot?

North America led with 34.05% in 2025, and Asia-Pacific is the near-term hotspot with a projected 11.60% CAGR through 2031 supported by India’s fleet ramp-up and domestic MRO capacity building.

What technology shifts are reducing aircraft paint turnaround times?

Base-coat and clear-coat systems enable same-day application of color and protective layers, cutting ground time by several days and aligning with lightweight systems that reduce fuel burn for operators.

How are warranty and regulatory requirements shaping provider selection?

OEM warranties and airworthiness frameworks elevate the need for approved materials, documented processes, and certified providers, which narrows selection to shops that can assure durability and compliance within set cure and film guidelines.

Which end-user categories underpin demand resilience?

Airlines and lessors provided scale volume at 65.20% of 2025 revenue, while business jet operators add higher-margin bespoke projects and are projected to grow at an 11.65% CAGR through 2031.

Page last updated on: