AI Studio Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

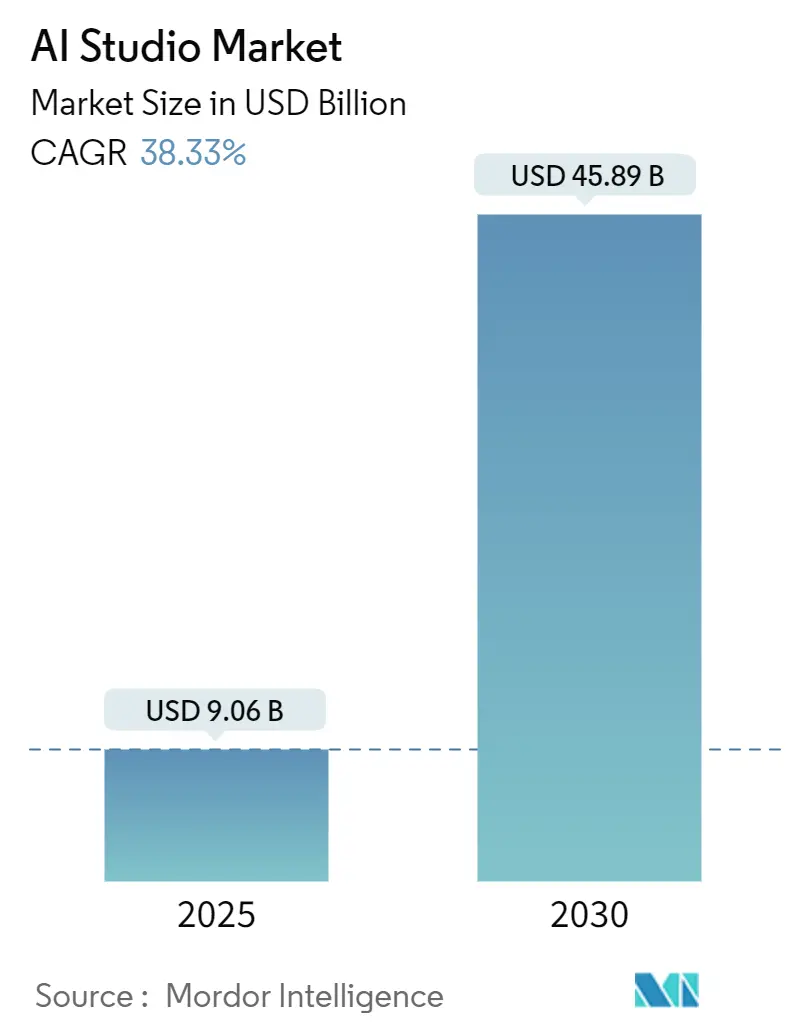

| Market Size (2025) | USD 9.06 Billion |

| Market Size (2030) | USD 45.89 Billion |

| Growth Rate (2025 - 2030) | 38.33% CAGR |

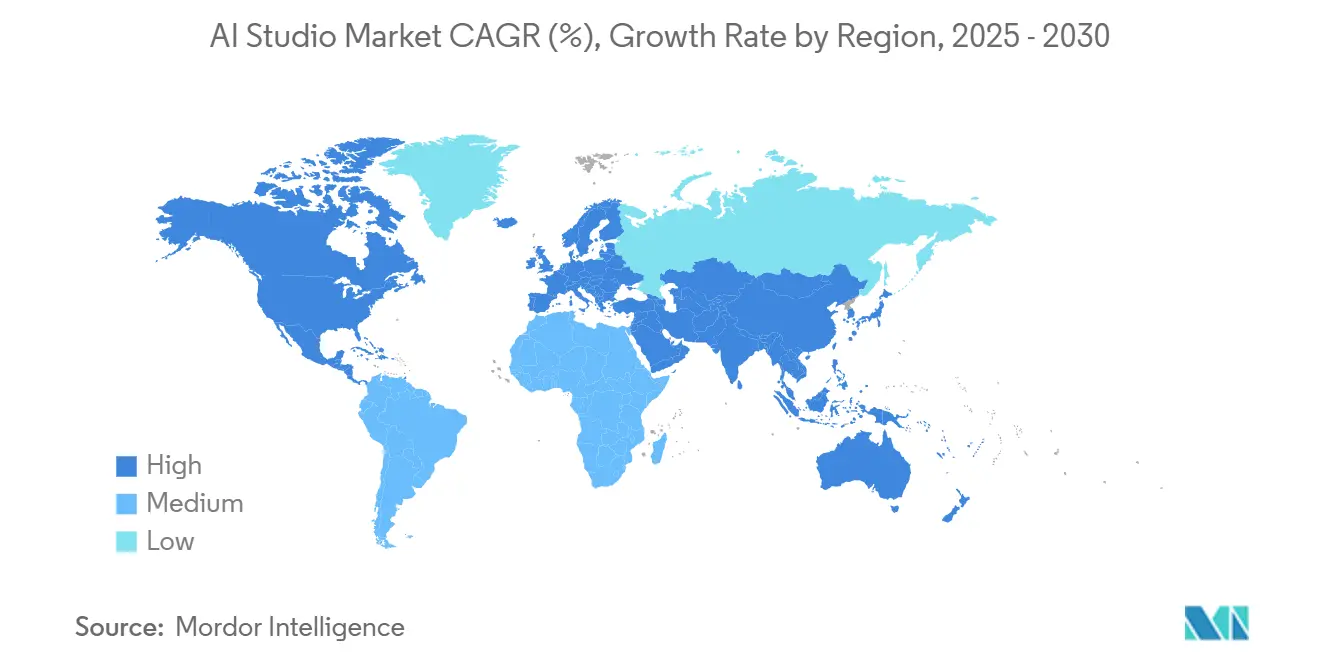

| Fastest Growing Market | Middle East |

| Largest Market | North America |

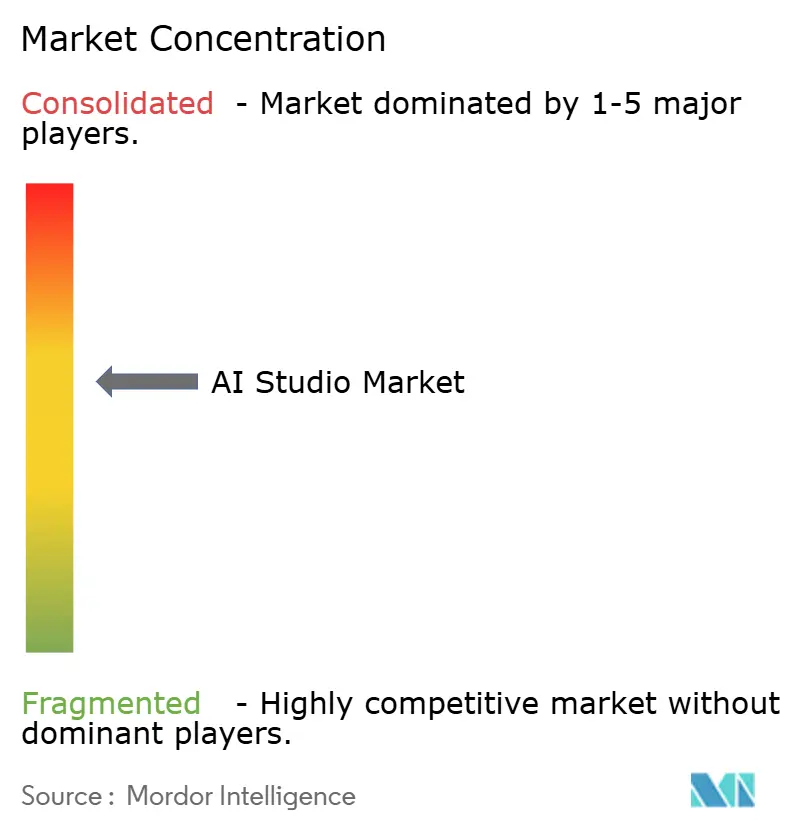

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Studio Market Analysis by Mordor Intelligence

The AI studio market size is projected to reach USD 9.06 billion in 2025 and is forecast to expand at a 38.33% CAGR to USD 45.89 billion by 2030, underscoring the urgency among enterprises to productionize generative AI while managing governance at scale. Rapid growth reflects three converging forces: the widespread release of foundation models that reduce development time, rising demand for low-code environments that enable non-experts to build models, and intensifying regulatory pressure for transparent and responsible AI workflows. Cloud deployment leads because organizations avoid the capital expense and operational burden of on-premise GPU clusters, yet hybrid architectures are scaling the fastest as companies reconcile latency, cost, and data-sovereignty needs. Model lifecycle management remains the primary use case, but computer vision workloads are accelerating as manufacturers and retailers seek real-time image analytics at the network edge. The competitive field is moderately concentrated, with hyperscale cloud vendors competing against specialist platform providers, while niche players fill gaps in verticals or at the edge.

Key Report Takeaways

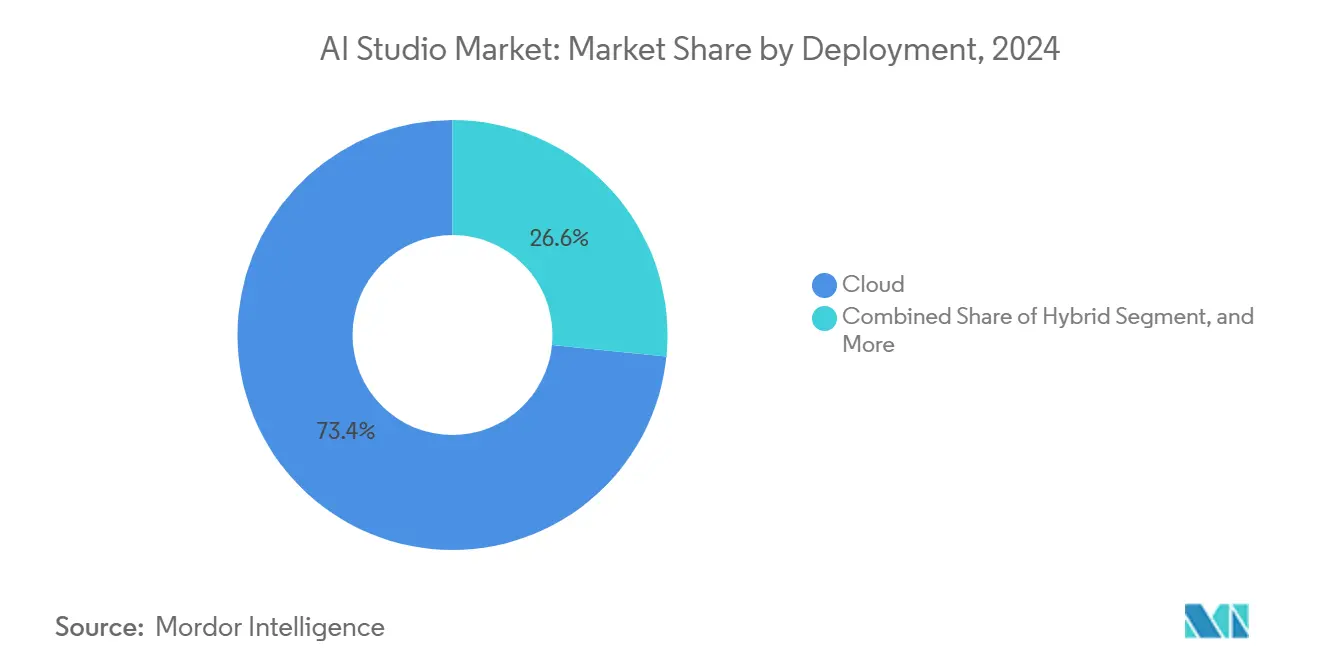

- By deployment, cloud captured 73.41% revenue share in 2024, while hybrid architectures are projected to grow at a 38.87% CAGR through 2030.

- By application, machine learning and MLOps held 39.67% of the AI studio market share in 2024, whereas computer vision is expected to advance at a 39.19% CAGR to 2030.

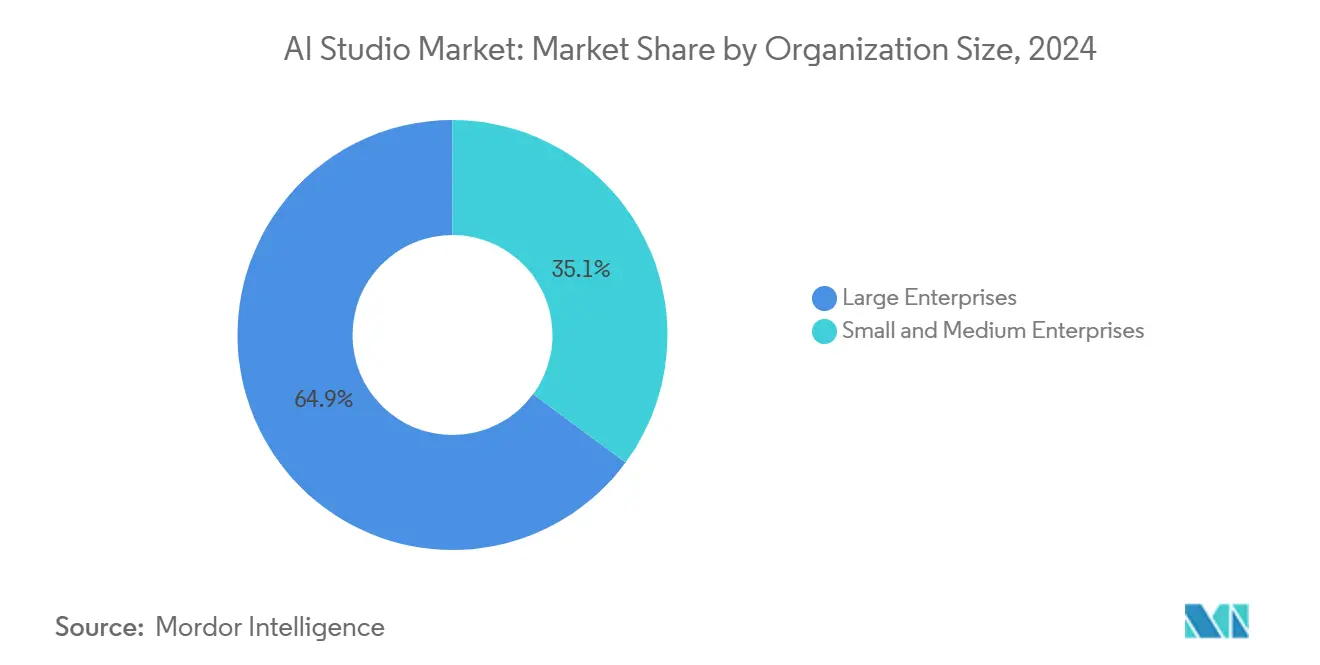

- By organization size, large enterprises commanded a 64.89% share of the AI studio market size in 2024; however, small and medium enterprises are expanding at a 38.91% CAGR over the same horizon.

- By end-user industry, banking, financial services, and insurance accounted for a 28.19% slice of the AI studio market in 2024, while retail and ecommerce are forecast to grow at a 39.34% CAGR to 2030.

- By geography, North America led with a 42.38% share in 2024, and the Middle East is projected to achieve a 39.26% CAGR through 2030.

Global AI Studio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Enterprise Adoption of Generative AI Platforms | +8.2% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Proliferation of Low-Code or No-Code Development Tools | +6.8% | Global, stronger uptake in Asia-Pacific SMEs | Medium term (2-4 years) |

| Surge in Venture Capital Funding for AI Startups | +5.4% | North America and Europe core, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Growing Availability of Pre-Trained Foundation Models | +7.1% | Global, regulatory variations in China and EU | Medium term (2-4 years) |

| Increasing Emphasis on Responsible AI Governance Frameworks | +4.3% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Vertical-Specific AI Studio Offerings for Domain Specialists | +5.9% | Global, sector-specific regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Enterprise Adoption of Generative AI Platforms

Enterprise spending on generative AI platforms reached USD 16.9 billion in 2024, and 72% of Fortune 500 companies now run at least one production model.[1]J. Lacy, “State of AI in the Enterprise, 4th Edition,” Deloitte, deloitte.com Proof-of-concept projects are giving way to fleet-scale deployments, which require integrated tooling for version control, monitoring, and rollback. Firms now judge vendors by their ability to simplify governance and automate compliance workflows rather than by raw model accuracy alone. Because generative AI impacts customer-facing workflows, business units are pushing for self-service portals, driving the purchase of full-stack AI studios rather than stitched-together point solutions. Vendors that embed templated pipelines and pre-approved guardrails reduce risk and shorten time-to-value, reinforcing demand for consolidated platforms in the AI studio market.

Proliferation of Low-Code or No-Code Development Tools

Low-code AI suites experienced a 127% year-over-year increase in adoption during 2024, led by Microsoft Power Platform and Google Vertex AI.[2]N. Patel, “New Models Added to Azure OpenAI Service,” Microsoft, microsoft.com Visual drag-and-drop workflows enable business analysts to set up document classifiers or chatbots without requiring Python expertise, thereby reducing project cycles from months to weeks. As non-technical staff build models, oversight gaps widen, so enterprises request unified audit logs, automated performance alerts, and built-in bias checks. Vendors respond by integrating citizen-developer interfaces with enterprise governance frameworks, establishing a new revenue stream for the AI studio market. The trend is particularly pronounced among Asia-Pacific SMEs that lack large data science teams but must digitize rapidly to stay competitive.

Surge in Venture Capital Funding for AI Startups

Venture investment in AI startups hit USD 29.1 billion in 2024, with infrastructure and platform plays capturing 34% of the haul.[3]S. Singh, “Global Analysis of Venture Funding Q2 2024,” KPMG, kpmg.com Floods of capital accelerate roadmap delivery, forcing incumbents to roll out new modules faster and drop prices. Big rounds for Databricks and H2O.ai bankroll larger field sales armies and deeper partner programs, widening global reach. Startups differentiate themselves through vertical accelerators, which bring pre-tuned models and data connectors tailored to sectors such as healthcare or manufacturing. Meanwhile, investors demand aggressive revenue targets, so platforms bundle more features into entry tiers, boosting buyer power and overall adoption across the AI studio market.

Growing Availability of Pre-Trained Foundation Models

Commercially available foundation models increased by 340% in 2024, and cloud vendors now expose more than 200 variants through model marketplaces. Ready-made models slash compute bills and time-to-deployment, especially in tightly regulated fields where custom training on sensitive data is discouraged. Domain-specific versions demonstrate 40-60% higher task accuracy than their generic counterparts, driving rapid adoption in finance, healthcare, and manufacturing. The explosion of choice introduces complexity around model selection and benchmarking, so platforms that automate side-by-side comparisons gain traction. Smaller, resource-efficient architectures optimized for edge devices further open up white space at the network perimeter, expanding the AI studio market into logistics hubs, retail stores, and factory floors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High TCO for On-Premise AI Infrastructure | -4.7% | Global, stronger impact in emerging markets | Medium term (2-4 years) |

| Limited Availability of Skilled MLOps Engineers | -6.2% | Global, acute shortages in Asia-Pacific and emerging markets | Long term (≥ 4 years) |

| Data Residency and Sovereignty Compliance Challenges | -3.8% | Europe and Asia-Pacific, China-specific rules | Medium term (2-4 years) |

| Fragmented Open-Source Licensing and IP Conflicts | -2.9% | Global, jurisdictional legal variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High TCO for On-Premise AI Infrastructure

Enterprise-grade AI clusters cost USD 2.8 million to USD 12.4 million to install, with annual operating expenses adding another 35-45%. Licensing, power, cooling, and specialist staff all contribute to the total cost of ownership, deterring mid-market buyers despite compliance-driven mandates for local processing. Vendors counter with managed private-cloud racks and GPU leasing plans that smooth capex into opex, yet those options still demand skilled teams for patching and monitoring. Accordingly, organizations outside heavily regulated verticals prefer cloud or hybrid approaches, tempering growth in the on-premise slice of the AI studio market.

Limited Availability of Skilled MLOps Engineers

In 2024, the global labor gap for MLOps talent reached 4.2 open roles per qualified data scientist or engineer. Salary inflation hit 40% in some Asia-Pacific cities as firms poach experts to maintain pipelines and uptime. Bottlenecks slow deployments and elevate project risk, pushing enterprises to prioritize platforms that automate drift detection, rollback, and compliance reporting. Vendors integrate one-click retraining and no-code monitoring dashboards, yet the automation itself requires deep platform engineering, perpetuating the skills crunch. Until education pipelines and tooling mature, talent scarcity will moderate the long-run expansion of the AI studio market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Drives Hybrid Innovation

Cloud deployments commanded 73.41% of the AI studio market share in 2024, reflecting the appeal of off-the-shelf GPU capacity, managed security, and frictionless scaling. That dominance secures a predictable revenue base for hyperscalers, while providing enterprises with immediate access to the latest foundation models. Yet regulatory and latency constraints spur interest in mixed environments. Hybrid architectures boast a 38.87% CAGR, blending on-premise data residency with cloud-side experimentation to optimize both compliance and cost. Edge nodes added to hybrid stacks process vision in factories and stores, cutting inference latency below 30 milliseconds. Over the forecast window, seamless workload mobility across on-premise, cloud, and edge fabric will shape product roadmaps and sustain momentum across the AI studio market.

Organizations that retain sensitive workloads on local clusters maintain a modest but strategic on-premises footprint. Financial institutions and governments use air-gapped GPU pods for confidential data while mirroring masked datasets to the cloud for model training. Platform vendors now ship consumption-based appliance bundles that shrink procurement cycles from quarters to weeks, easing entry for risk-averse sectors. As a result, the AI studio market size tied to hybrid and on-premise patterns is expected to grow steadily, even though cloud remains the largest value pool.

By Application: Computer Vision Accelerates Beyond MLOps Foundation

Machine learning and MLOps still account for 39.67% of the revenue share, as every production model requires deployment, monitoring, and rollback, regardless of the domain. Enterprises pay premiums for unified notebooks, pipeline orchestration, lineage tracking, and policy-based access control. However, computer vision revenues are climbing at a 39.19% CAGR as smart-factory rollouts and in-store analytics scale. Manufacturers utilize defect-detection models embedded in Jetson devices, while retailers tag shelf images to reduce stockouts by double digits. Edge-ready vision pipelines integrate with centralized AI studios, ensuring consistent governance.

Natural language processing remains the public face of enterprise AI as chat assistants proliferate, but vision modules now integrate with text and tabular data, enabling multimodal decision engines. Over the forecast period, turnkey templates for safety monitoring, fraud detection, and medical imaging will broaden appeal among organizations with limited data-science headcount, extending the AI studio market size deeper into operational workflows.

By Organization Size: SME Growth Challenges, Enterprise Dominance

Large enterprises controlled 64.89% of 2024 spending after years of building specialist data teams and committing to multi-year licenses that span data ingestion to model serving. These firms value role-based access, custom SLAs, and white-glove support, which favor full-suite platforms from cloud incumbents and silver-tier partners. Yet small and medium enterprises are scaling fastest, posting a 38.91% CAGR through 2030. Pay-per-use pricing, hosted notebooks, and wizard-driven pipelines remove upfront hurdles. Pre-built retail recommendations or finance risk scoring templates enable SMEs to activate models in just days. As democratization continues, SME demand will force vendors to simplify tiers and compress price lists, adding new revenue streams even as per-seat realizations dip.

Regional policy also fuels SME uptake. Tax credits in the European Union and Middle Eastern grant programs earmark funds for digital modernization among mid-market firms. Those incentives funnel budgets toward subscription packages that bundle compute, models, and governance in a single invoice, thereby enlarging the AI studio market.

By End-User Industry: Retail Innovation Outpaces Banking Leadership

Banking, financial services, and insurance retained a 28.19% share in 2024, thanks to the early adoption of model risk management frameworks and strong returns from fraud analytics. Institutions refresh platforms every two to three years to meet evolving supervisory guidance on explainability. They demand immutable audit trails and adversarial testing, steering spend toward providers with hardened governance modules.

Retail and ecommerce, by contrast, tops the growth charts with a 39.34% CAGR. Personalized search, dynamic pricing, and visual shelf monitoring use multimodal AI to lift basket sizes and reduce shrinkage. Stores deploy edge boxes running image models to flag out-of-stock items and trigger replenishment. Cloud studios synchronize those models nightly for retraining, ensuring version consistency across thousands of locations. Healthcare and life sciences experiment with clinical decision aids and prognosis models, while manufacturing pilots predictive maintenance suites that connect sensor feeds to anomaly detectors. Each advance continues to expand the total AI studio market size across various verticals.

Geography Analysis

North America accounted for 42.38% of 2024 revenues, driven by deep venture capital pools, a robust talent pipeline, and early regulatory signals that clarify liability and privacy obligations. United States enterprises dominate spending, focusing on cross-domain model reuse to maximize return on data assets. Canada punches above its weight in responsible AI research, nurturing startups that embed fairness metrics directly into their platform scaffolding.

Europe follows with steady adoption, guided by the GDPR and the upcoming AI Act. Germany leads industrial deployments, while the United Kingdom centers on fintech and pharma use cases. Vendors highlight compliance dashboards that map to EU risk tiers, making governance a key selling point. The Asia-Pacific region posts robust growth, driven by national AI policies and manufacturing upgrades. China’s 2025 guidance pushes local-language foundation models, and Japan automates automotive supply chains with hybrid cloud platforms.

The Middle East is the fastest riser with a 39.26% CAGR. Sovereign investment vehicles finance smart-city pilots, banking modernization, and industrial diversification. The UAE’s federal AI strategy earmarks funding for cloud credits and training, directly subsidizing AI studio subscriptions. Saudi Arabia deploys oil-field predictive models on private GPU clusters paired with cloud orchestration for retraining. South America records moderate momentum with Brazil’s fintech ecosystem expanding edge-friendly AI workloads, while Africa’s early adopters in telecom and mining lay the groundwork for broader regional uptake.

Competitive Landscape

The AI studio market shows moderate concentration. Top cloud providers bundle compute, data warehousing, and foundation models to lock in customers, but specialized vendors differentiate on vertical IP and user experience. Databricks combines lakehouse data management with collaborative notebooks, targeting regulated industries that require unified governance. H2O.ai stakes its claim in low-code automation for small and medium enterprises, while DataRobot relaunches under new ownership with a focus on rapid pilot-to-production transitions.

Vendors cluster around three playbooks. Horizontal suite providers pursue scale by covering every lifecycle phase from ingestion to monitoring. Vertical specialists craft domain-tuned models and compliance blueprints, shortening adoption cycles in sectors with strict standards. Edge disruptors miniaturize models and package federated learning to overcome data-sovereignty roadblocks and bandwidth limits, appealing to factories and retail chains. Differentiation increasingly hinges on automation, with auto-generated pipelines, code suggestions, and self-healing inference endpoints setting the pace in the AI studio market.

Strategic moves over the past year have intensified a rivalry. Microsoft has added GPT-4 Turbo to Azure Machine Learning Studio, enhancing its language model capabilities. Google introduced multimodal workflows within Vertex AI, unifying text, vision, and video in a single pane. IBM rolled out watsonx. Governance, signaling that responsible AI is now table stakes. As feature parity tightens, pricing creativity and ecosystem breadth will decide share gains through 2030.

AI Studio Industry Leaders

DataRobot Inc.

H2O.ai Inc.

Dataiku Inc.

RapidMiner Inc.

KNIME AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft added automated prompt-optimization and multimodal debugging tools to Azure Machine Learning Studio, expanding one-click deployment support for GPT-4 Turbo workloads.

- September 2025: Google Cloud introduced Vertex AI Edge Suite, a packaged hardware-software bundle that places low-power vision and language models on factory floors and retail sites for sub-20-millisecond inference.

- July 2025: Amazon Web Services opened its first European AI Accelerator Region in Spain, enabling SageMaker customers to train and serve large language models within EU data-sovereignty boundaries.

- March 2025: IBM launched watsonx Studio Lite, a pay-per-project tier that gives small and medium enterprises access to governance automation and model monitoring without long-term contracts.

Global AI Studio Market Report Scope

The AI Studio Market Report is Segmented by Deployment (Cloud, On-Premise, Hybrid), Application (Data Science and Analytics, Machine Learning and MLOps, Natural Language Processing, Computer Vision, Other Application), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Healthcare and Life Sciences, Banking Financial Services and Insurance, Retail and eCommerce, Manufacturing and Industrial, Information Technology and Telecom, Other End-User Industry), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Data Science and Analytics |

| Machine Learning and MLOps |

| Natural Language Processing |

| Computer Vision |

| Other Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance |

| Retail and eCommerce |

| Manufacturing and Industrial |

| Information Technology and Telecom |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Deployment | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Application | Data Science and Analytics | ||

| Machine Learning and MLOps | |||

| Natural Language Processing | |||

| Computer Vision | |||

| Other Applications | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Industry | Healthcare and Life Sciences | ||

| Banking, Financial Services and Insurance | |||

| Retail and eCommerce | |||

| Manufacturing and Industrial | |||

| Information Technology and Telecom | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What revenue growth is expected for the AI studio market by 2030?

The AI studio market size is projected to increase from USD 9.06 billion in 2025 to USD 45.89 billion by 2030, reflecting a 38.33% CAGR.

Which deployment mode is expanding the fastest?

Hybrid architectures are on track for a 38.87% CAGR between 2025 and 2030 as firms pair on-premise data control with cloud training flexibility.

Which end-user sector shows the highest future growth?

Retail and ecommerce lead with a projected 39.34% CAGR, driven by personalization, supply-chain optimization, and in-store computer vision analytics.

What is the main restraint hampering wider adoption?

A global shortage of skilled MLOps engineers, with demand outstripping supply by more than four to one, raises deployment risk and slows rollouts.

How concentrated is vendor competition?

The market scores a six on a 10-point scale because the top five players capture about 60% of spending, leaving room for niche and regional challengers.

Which region is growing the fastest?

The Middle East is forecast to advance at a 39.26% CAGR, propelled by national AI strategies and sovereign investment in smart-city and industrial projects.

Page last updated on: