AI Skin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 19.28% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

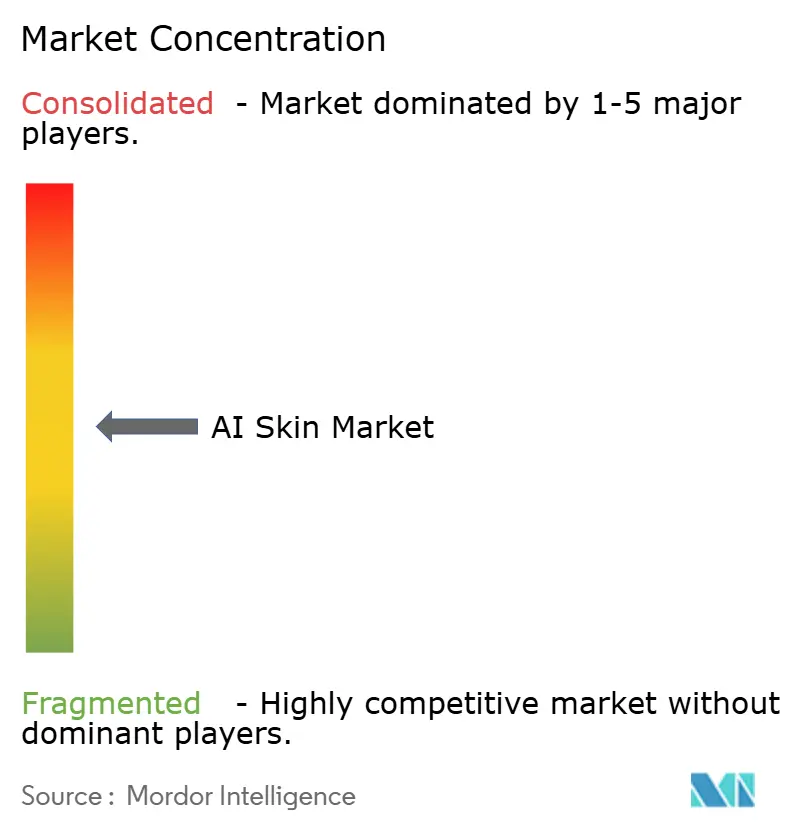

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Skin Market Analysis by Mordor Intelligence

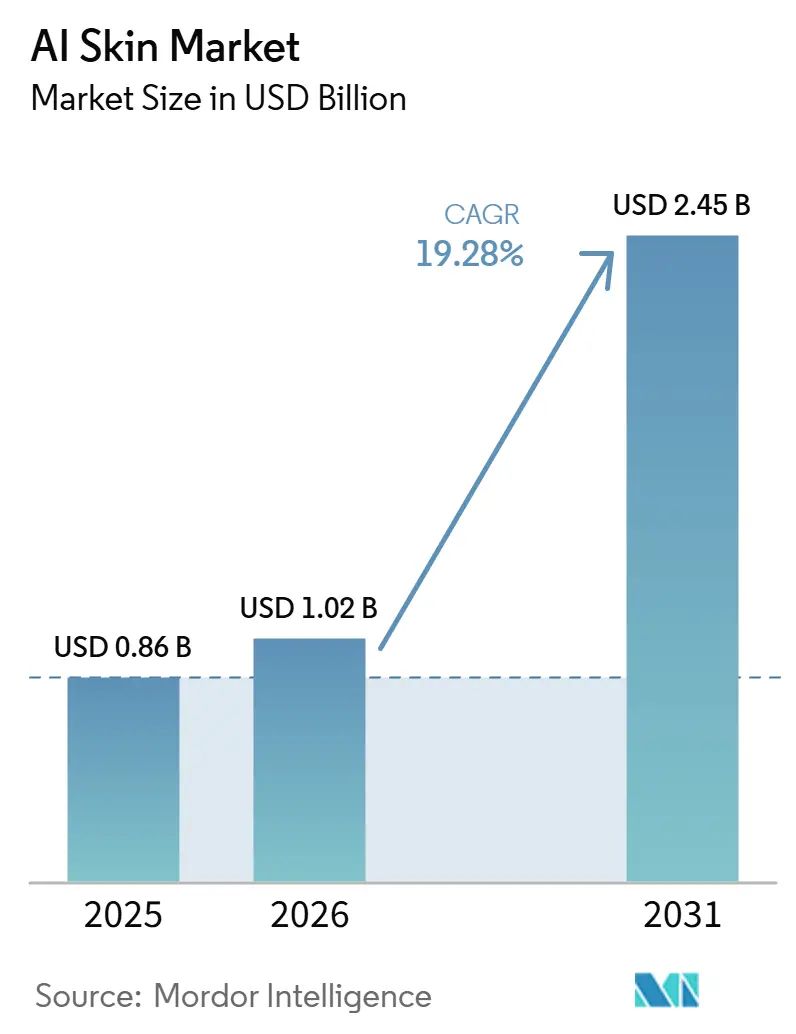

The AI Skin Market size is expected to increase from USD 0.86 billion in 2025 to USD 1.02 billion in 2026 and reach USD 2.45 billion by 2031, growing at a CAGR of 19.28% over 2026-2031.

The AI skin market is expanding because dermatology care is moving toward faster diagnosis, wider screening access, and more data-led consumer skin assessment across clinical and retail settings. The AI skin market is also benefiting from the combined use of computer vision, natural language processing, and wearable photonics, which is moving skin analysis beyond hospitals into primary care, aesthetics, and direct-to-consumer use. These shifts are reinforcing each other, which is shortening adoption timelines that would usually take much longer. Competitive activity in the AI skin market is rising across clinical device makers and beauty technology platforms, while regulatory complexity and dataset bias still limit how quickly new entrants can scale across regions. The strongest opportunity in the AI skin market remains the expansion of edge-based and consumer-facing tools that can ease referral backlogs, widen access, and generate larger pools of real-world skin data for future model improvement.

Key Report Takeaways

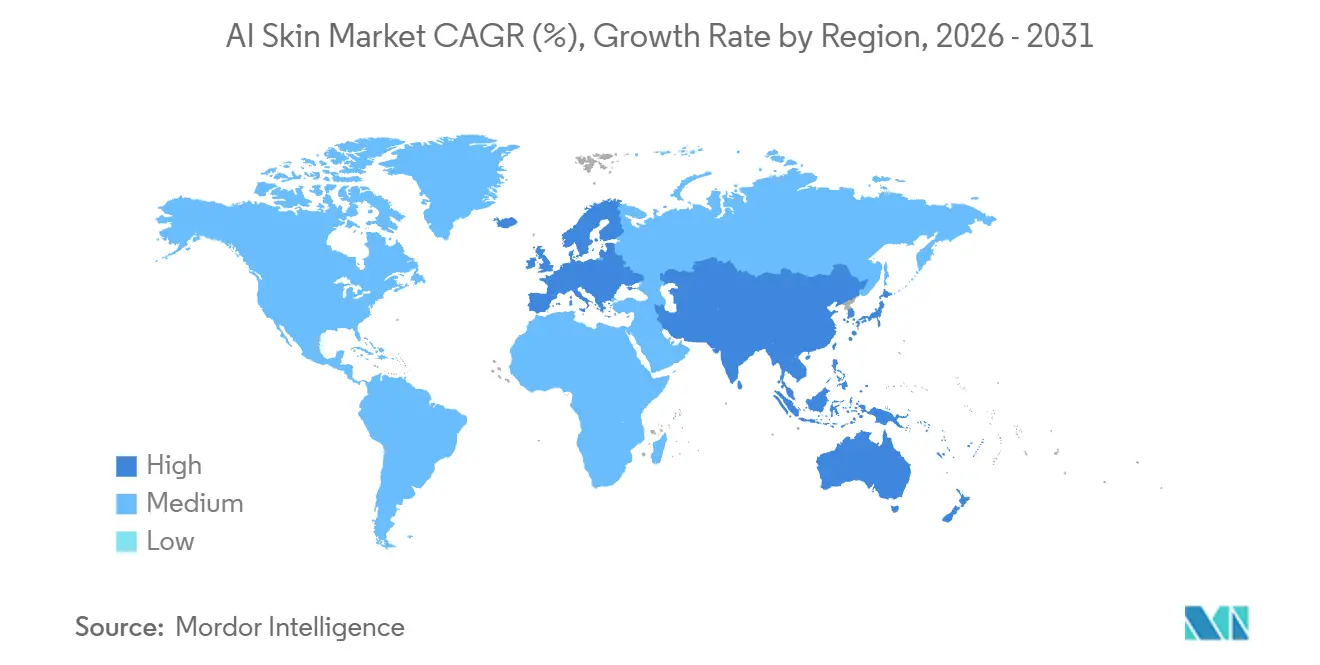

By region, North America held 38.1% share in 2025, while Asia Pacific is projected to grow at a 21.7% CAGR through 2031.

By application, Dermatology and Clinical Diagnostics accounted for 51.8% share in 2025, while Cosmetics and Personal Care is forecast to expand at a 20.5% CAGR through 2031.

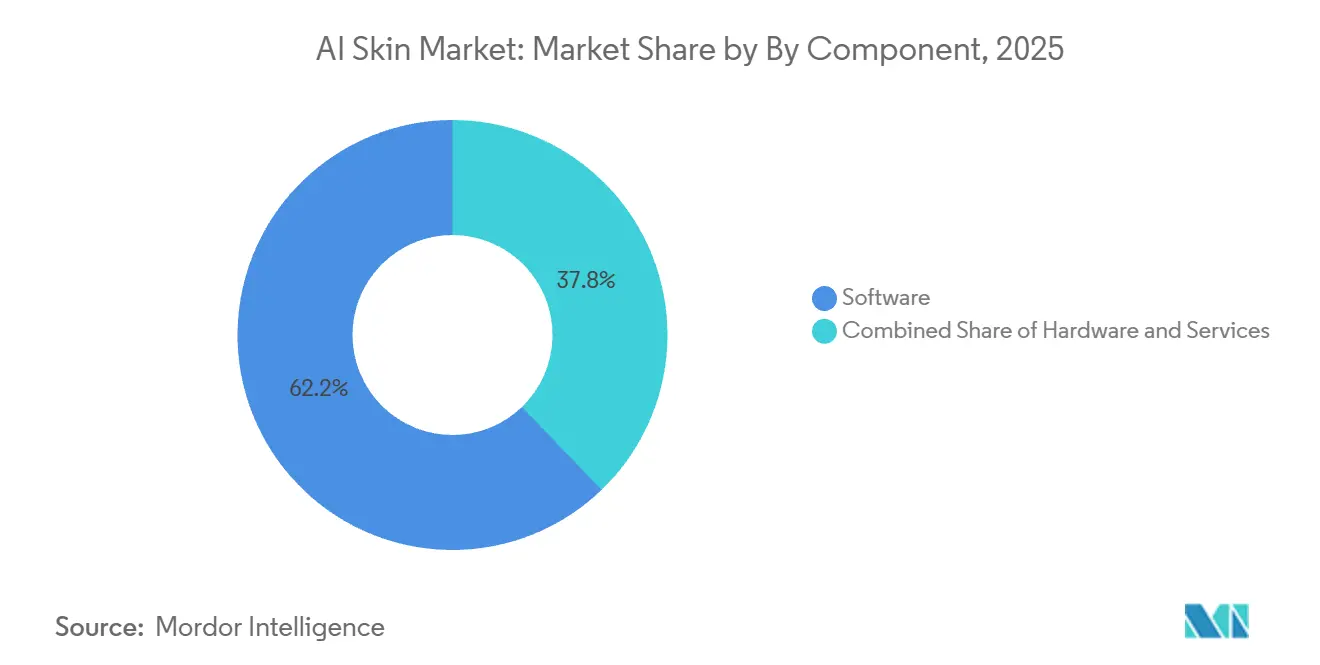

By component, Software held 62.2% share in 2025, while Services is projected to grow at a 19.8% CAGR through 2031.

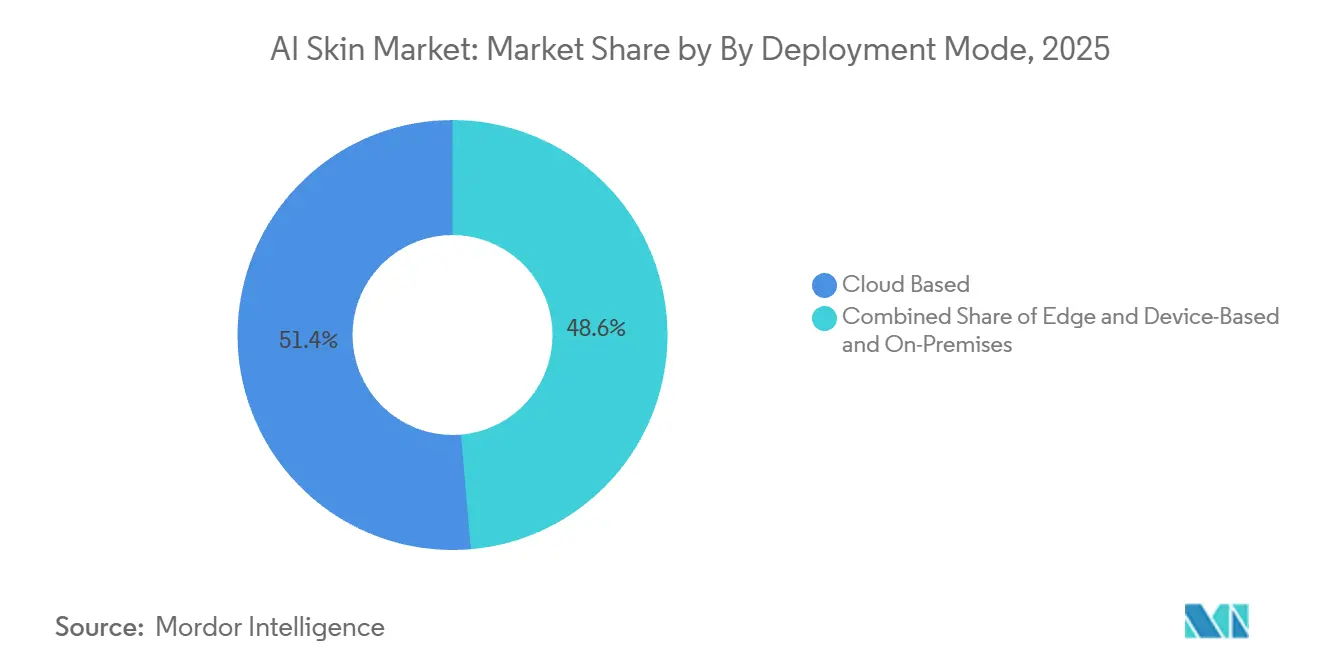

By deployment mode, Cloud-Based held 51.4% share in 2025, while Edge and Device-Based is forecast to grow at a 21.3% CAGR through 2031.

By end user, Dermatology Clinics and Hospitals held 40.2% share in 2025, while Consumers and Direct-to-App Users are projected to expand at a 19.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Skin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Personalized Skincare Recommendations | +4.3% | Global, with early gains in North America, South Korea, Japan | Medium term (2-4 years) |

| Expansion of Teledermatology and Remote Skin Screening | +3.6% | North America, Europe, APAC, including India and Australia | Short term (≤ 2 years) |

| Accuracy Gains From Deep Learning-Based Skin Lesion Analysis | +4.0% | Global, concentrated in U.S., U.K., and EU clinical settings | Medium term (2-4 years) |

| Beauty Retail and D2C Adoption of AI Skin Diagnostics | +3.2% | North America, South Korea, China, DACH region | Short term (≤ 2 years) |

| Multimodal Skin Intelligence Using Imaging, Genomics, and Related Modalities | +1.6% | North America, France, Japan | Long term (≥ 4 years) |

| Payer and Provider Pilots for AI-Assisted Dermatology Triage | +0.8% | North America, U.K. NHS, GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Personalized Skincare Recommendations

Personalization is changing the commercial logic of the AI skin market because skin analysis is becoming a direct revenue tool instead of a simple digital feature. The strongest effect comes from how real-time skin assessments shorten the buying journey and turn a skin scan into an immediate product recommendation. This is pushing brands to treat AI skin tools as part of conversion infrastructure across online, mobile, and retail channels. The AI skin market is also gaining from the way these tools create large volumes of first-party skin data that can support formulation work, user retargeting, and stronger brand retention over time. At the same time, scaling these data models across countries depends on compliance with privacy and health data rules such as GDPR and HIPAA.

Expansion of Teledermatology and Remote Skin Screening

The AI skin market is gaining from teledermatology because remote screening is becoming part of frontline triage rather than a secondary convenience. This model reduces pressure on specialist capacity by handling patient intake, image review, and prioritization earlier in the care pathway. In May 2026, Teladoc Health[1]Teladoc Health, “Dermatology Services Available Through Walmart Better Care Services,” Teladoc Health expanded dermatology access through Walmart’s Better Care Services platform, allowing consumers to upload skin images and receive board-certified dermatologist review within 24 hours for USD 89 per visit. This retail-linked model widens access beyond conventional care settings and brings the AI skin market into a much larger consumer flow. It also increases demand for triage systems trained on diverse patient groups, which makes dataset quality and skin tone coverage more important for future adoption.

Accuracy Gains From Deep Learning-Based Skin Lesion Analysis

The AI skin market is moving forward because clinical accuracy claims are now supported by larger and stronger validation results. PanDerm, published in Nature Medicine[2]Nature Medicine, “PanDerm Multimodal Vision Foundation Model For Dermatology,” Nature Medicine in June 2025, was trained on more than 2 million real-world skin images from 11 clinical institutions across 4 imaging modalities and delivered state-of-the-art results across 28 dermatology benchmarks. The same study reported that the model outperformed clinicians by 10.2% in early-stage melanoma detection and improved clinician diagnostic accuracy by 11% when used as a decision-support tool. A separate algorithm validated on a Korean national dataset of 51,038 images achieved an AUC of 0.946 for binary malignancy classification, which was reported as comparable with expert dermatologist performance. These results are giving the AI skin market stronger support for physician trust, regulatory filings, and payer discussions, even though weaker performance on darker skin tones still limits commercial confidence in several populations.

Beauty Retail and D2C Adoption of AI Skin Diagnostics

Beauty brands are creating one of the fastest commercial routes for the AI skin market because the point of sale is becoming a point of diagnosis. L’Oréal’s Longevity AI Cloud analyzes more than 260 skin longevity biomarkers and is being used across brands to shift skincare toward predictive and preventive use. This model matters because retail environments can generate skin data continuously and at a scale that most clinical settings cannot match. That gives brand-linked platforms a stronger position in consumer skin applications, where repeated use and large data volumes matter as much as pure diagnostic precision. The AI skin market is therefore seeing retail and direct-to-consumer channels become a major training and monetization surface alongside hospitals and telehealth networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dataset Bias Across Skin Tones and Under-Representation | -1.2% | Global, acute in Sub-Saharan Africa, South Asia, Latin America | Short term (≤ 2 years) |

| Fragmented Regulatory Pathways for Adaptive AI and Software | -1.4% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Limited Clinical Trust in Black-Box Recommendations | -0.9% | Global, concentrated in established clinical markets | Medium term (2-4 years) |

| Shortage of High-Quality Labeled Dermatology Image Data | -0.8% | Global, acute in low-income and rural markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dataset Bias Across Skin Tones and Under-Representation

Dataset bias remains one of the most serious limits on the AI skin market because training data still does not reflect global skin diversity. A 2025 study in the Journal of the European Academy of Dermatology and Venereology found that only 10.2% of 4,000 AI-generated dermatological images depicted dark skin tones, and only 15% accurately represented the intended clinical condition. The same issue appears in benchmark datasets used across the AI skin market, where image collections have historically come from Europe, North America, and Oceania. This creates measurable performance gaps for populations in India, Southeast Asia, Latin America, and Sub-Saharan Africa, where real-world deployment may not match the training mix. Correcting this issue will require more coordinated dataset development and stronger incentives for inclusive evidence generation across both regulators and industry participants.

Fragmented Regulatory Pathways for Adaptive AI and Software

Regulation is slowing parts of the AI skin market because developers must navigate different requirements across the United States and Europe. The FDA published AI and machine learning device lifecycle guidance in January 2025 and updated its Predetermined Change Control Plan guidance in August 2025, increasing the documentation expected for adaptive models. In Europe, AI-enabled medical devices fall under the EU Medical Device Regulation and the EU AI Act, which raises the compliance load for companies that want to sell in both regions. This makes market entry more difficult for smaller developers that do not have broad regulatory affairs resources. The effect on the AI skin market is not only higher cost, but also slower model iteration in a field where new training data and performance updates are still arriving quickly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Holds the Core, Services Power the Network Effect

Software held 62.2% of the AI skin market share in 2025, reflecting the scale advantages of software-led delivery across clinical and consumer use cases. The AI skin market has favored software because cloud-accessible tools can be deployed widely across clinics, aesthetic centers, and brand platforms without the same hardware burden. Perfect Corp.’s AI Skin Analysis was trained on more than 70,000 medical-grade images and reported intraclass correlation scores above 0.90 in a study published in the Journal of Dermatological Treatment[3]Perfect Corp., “AI Skin Analysis Validation And Product Overview,” Perfect Corp., which helped establish a visible software performance benchmark. Hardware remained smaller, but it kept a specialized role because high-resolution and multimodal skin imaging still relies on purpose-built optics in certain workflows. Devices such as Kiehl’s Derma-Reader 2.0 and FotoFinder’s mobile dermatoscopy systems show that the AI skin industry still needs dedicated hardware where imaging quality and workflow control are critical.

Services is projected to expand at a 19.8% CAGR through 2031, making it the fastest-growing component area in the AI skin market. This growth is tied to API-based delivery, where providers embed skin intelligence into beauty, pharmacy, telehealth, and digital health platforms rather than selling only standalone tools. The AI skin market size for services is being widened by this white-labeled model because many operators can adopt AI assessment without building their own models from the ground up. Autoderm launched Germany’s first API-based AI skin analysis service with CE certification in December 2025, and the platform had already carried out more than 2 million API-based skin image analyses globally. This architecture expands the AI skin market beyond direct device procurement and gives services a faster scaling profile than the broader category baseline.

By Application: Clinical Diagnostics Anchors Revenue, Cosmetics Drives Volume Growth

Dermatology and Clinical Diagnostics accounted for 51.8% share of the AI skin market size in 2025, which kept this segment at the center of current revenue generation. The AI skin market remains anchored here because clinical contracts are larger, reimbursement discussions matter more, and once integrated, clinical systems are harder to displace than consumer tools. This segment also benefits from the way physicians and hospitals value evidence depth, workflow continuity, and compliance over pure speed of adoption. In March 2026, the FDA finalized the reclassification of optical melanoma detection devices and related electrical impedance spectrometers from Class III to Class II, lowering the entry barrier for software-aided adjunctive diagnostic devices for skin lesions . That step supports more product entry and should help sustain the clinical role of the AI skin market over the next few years.

Cosmetics and Personal Care is forecast to grow at a 20.5% CAGR through 2031, making it the fastest-expanding application in the AI skin market. The core driver is that a selfie-based scan can turn directly into a tailored product path, which shortens purchase consideration and lifts conversion in consumer channels. Haut.AI announced a June 2026 collaboration with OLAY[4]Haut.AI And OLAY, “Virtual Companion Technology Launch Announcement,” PR Newswire to introduce Virtual Companion technology that uses clinical data modeling to simulate how a recommended routine may perform over time on a user’s skin profile. This shows how the line between diagnosis and beauty recommendation is narrowing in the AI skin market. When beauty platforms bring clinical-style simulation into the purchase moment, the commercial boundary between cosmetic guidance and diagnostic support becomes harder to separate even if regulation still treats them differently.

By Deployment Mode: Cloud Dominates Today, Edge Architecture Defines Tomorrow

Cloud-Based deployment held 51.4% share in 2025, which kept it as the leading operating model in the AI skin market. Cloud architecture remains important because it supports centralized model training, broad access, continuous retraining, and the API-first structure used by many current platforms. These features suit beauty brands, telehealth operators, and consumer platforms where inference speed is less critical than scalability and easy integration. Cloud systems also fit the current economics of the AI skin market because one platform can serve several brands or channels from the same software layer. This is why cloud remains the largest deployment mode even as alternative architectures gain speed.

Edge and Device-Based deployment is projected to grow at a 21.3% CAGR through 2031, making it the fastest-growing deployment option in the AI skin market. Growth is coming from point-of-care use, portable diagnostics, and consumer devices where local inference matters for latency, workflow reliability, and reduced cloud dependence. Research published in the Journal of Supercomputing showed that edge GPU boards delivered the lowest energy use in hyperspectral skin analysis tasks, which strengthens the case for portable and power-efficient tools SPRINGER.COM. Skin Analytics launched DERM Zero in June 2026 as a regulated AI medical device that delivers autonomous Class III-level skin cancer assessments from a standard smartphone, showing how edge logic can be used at scale in real clinical pathways SKINANALYTICS.COM. The AI skin market is therefore moving toward a mixed deployment model where cloud keeps scale advantages while edge systems capture settings that need speed, privacy, and greater workflow independence.

By End User: Clinical Anchor Holds, Direct-to-Consumer Accelerates

Dermatology Clinics and Hospitals held 40.2% of the AI skin market share in 2025, which kept them as the largest end-user group. This leadership reflects the fact that the AI skin market still draws significant value from specialist workflows, imaging systems, and established documentation practices inside clinical settings. Providers such as MetaOptima and FotoFinder are strengthening this position by embedding AI into existing imaging and reporting processes rather than asking clinicians to adopt separate tools. PathAI received FDA Breakthrough Device Designation in March 2026 for PathAssist Derm, an AI-powered whole slide image analysis system for skin lesions that supports dermatopathology triage workflows. Aesthetic and cosmetic centers, diagnostic laboratories, and medspa operators are also expanding their use of AI assessment because these tools support consultations, documentation, and higher-value treatment pathways.

Consumers and Direct-to-App Users are projected to grow at a 19.8% CAGR through 2031, making them the fastest-growing end-user cohort in the AI skin market. Demand is being driven by simple access, since a selfie, a messaging app, or an in-store tablet can generate immediate guidance without the wait associated with specialist appointments. This makes the AI skin market relevant to people who want quicker answers even when they still value physician oversight for serious concerns. The same pattern supports long-term demand in countries where specialist access remains uneven, because consumer tools can absorb early assessment demand that would otherwise go untreated or be delayed. As a result, the AI skin market is expanding both through convenience-led adoption in developed settings and access-led adoption in healthcare systems with limited specialist reach.

Geography Analysis

North America held 38.1% of the AI skin market share in 2025, which made it the largest regional contributor. The region leads because it has a high density of cleared dermatology AI products, active payer experimentation, and a large population that still faces access delays in specialist care. In March 2026, the FDA reclassified optical diagnostic devices for melanoma detection and related technologies from Class III to Class II, which reduced the burden for future product entry in this part of the AI skin market. Teladoc Health’s Walmart-linked dermatology service, launched in May 2026, also showed how retail infrastructure can widen skin access through a fast digital channel. Canada and Mexico add secondary growth potential because digital health investment and private care expansion can support further regional uptake.

Europe remains important in the AI skin market because regulation shapes both the speed and the quality threshold of adoption. The dual effect is that entry is more demanding, but products that clear these hurdles may benefit from stronger clinical trust. The United Kingdom has become a visible example, where Skin Analytics reported that DERM had assessed more than 230,000 patients and detected more than 20,000 cancers across 24 hospitals since 2020. Germany is also building traction through API-linked services for pharmacies, telemedicine platforms, and health insurers, which broadens use beyond hospital-only channels. France, Italy, and Spain are progressing more gradually, with activity centered more in private aesthetic clinics and direct-to-consumer beauty platforms.

Asia Pacific is the fastest-growing region in the AI skin market at a 21.7% CAGR through 2031. Growth is being supported by 3 different engines, consumer AI skin diagnostics linked to K-Beauty in South Korea, public digital health infrastructure in India, and hospital-linked AI deployment in China. This mix matters because it gives the AI skin market both consumer volume and clinical depth across the same region. India is especially relevant because national telemedicine infrastructure can improve distribution of digital dermatology tools beyond large cities. China adds momentum through physician-assistant models in urban hospitals, while South Korea continues to support data-rich consumer skincare ecosystems. Outside Asia Pacific, the Middle East and Africa and South America remain earlier-stage markets, but they are still strategically relevant because smartphone-led beauty personalization and community-level skin tools can support future scale in the AI skin market.

Competitive Landscape

The AI skin market is moderately fragmented and competition is forming across 2 broad tiers. One tier is made up of large beauty and consumer goods companies such as L’Oréal, Procter & Gamble, Shiseido, Unilever, and Beiersdorf, which are integrating AI into product development, retail, and direct-to-consumer engagement. The second tier includes specialized platform providers such as Perfect Corp., Revieve, Haut.AI, SkinVision, and MetaOptima, which mainly operate as infrastructure partners for brands, clinics, and telehealth providers. This structure means the AI skin market is not defined by one uniform rivalry, since consumer beauty platforms and regulated clinical tools often compete on different terms. It also means the AI skin market is seeing both partnership-led expansion and regulatory moat building at the same time.

L’Oréal’s June 2026 collaboration with OpenAI showed how large incumbents are extending the AI skin market into microbiome mapping, longevity science, and internal generative AI workflows. L’Oréal also agreed in June 2026 to acquire a majority stake in Innovist, which strengthened its digital-first skincare reach in India. Perfect Corp. is pursuing a different route in the AI skin market by scaling integrations and platform reach rather than relying on a narrow set of exclusive client relationships. Haut.AI’s work with OLAY added another example of how specialist vendors are using simulation and embedded personalization to deepen their role inside brand ecosystems.

A separate clinical device layer of the AI skin market includes DermaSensor, Skin Analytics, FotoFinder, PathAI, and SciBase, where competitive strength depends more on evidence quality and regulatory progress than on partner count. Skin Analytics used DERM Zero to push autonomous smartphone-based assessment into a regulated medical device format in June 2026. PathAI gained FDA Breakthrough Device Designation in March 2026 for PathAssist Derm, which supports its position in digital pathology and triage. SciBase submitted a 510(k) notification to expand Nevisense into non-melanoma skin cancers in July 2026, showing how regulatory milestones remain a key way to build defensible space in the AI skin market. Over the medium term, compliance demands under FDA guidance and the EU AI framework are likely to favor better-capitalized participants, which may gradually tighten the structure of the clinical side of the AI skin market.

AI Skin Industry Leaders

The Procter and Gamble Company

Johnson and Johnson Services, Inc.

The Estée Lauder Companies Inc.

DermaSensor, Inc.

L'Oréal SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SciBase submitted a 510(k) premarket notification to the FDA seeking to expand the US indication for Nevisense to include non-melanoma skin cancers, keratinocyte carcinomas, which would add the largest addressable skin cancer category to the only FDA-approved AI melanoma detection device currently on the US mark

- June 2026: SciBase submitted a 510(k) premarket notification to the FDA seeking to expand the US indication for Nevisense to include non-melanoma skin cancers, keratinocyte carcinomas, which would add the largest addressable skin cancer category to the only FDA-approved AI melanoma detection device currently on the US mark

- May 2026: Teladoc Health made its dermatology services available through Walmart's Better Care Services platform, enabling consumers to upload skin images and receive board-certified dermatologist review within 24 hours at USD 89 per cash-pay visit

- March 2026: SkinVision announced a research collaboration with Mayo Clinic to conduct an FDA-required pivotal trial evaluating the SkinVision app's AI-based skin spot assessment, representing a key milestone on its US regulatory clearance pathway

Global AI Skin Market Report Scope

| Software |

| Hardware |

| Services |

| In Vivo Diagnostics |

| In Vitro Diagnostics |

| Cloud Based |

| Hybrid |

| On Premises |

| Hospitals |

| Diagnostic Imaging Centers |

| Diagnostic Laboratories |

| Clinics and Other Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| United States | |

| Canada | |

| Mexico | |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Application | In Vivo Diagnostics | |

| In Vitro Diagnostics | ||

| By Deployment Mode | Cloud Based | |

| Hybrid | ||

| On Premises | ||

| By Tend User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Diagnostic Laboratories | ||

| Clinics and Other Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| United States | ||

| Canada | ||

| Mexico | ||

| Germany | ||

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the AI skin market by 2031

The AI skin market is forecast to reach USD 2.45 billion by 2031, up from USD 1.02 billion in 2026, with a 19.3% CAGR over 2026-2031.

Which region leads current demand for AI skin solutions?

North America led in 2025 with 38.1% share, supported by regulatory activity, payer pilots, and persistent dermatology access gaps.

Which region is growing the fastest in AI skin adoption?

Asia Pacific is projected to grow at a 21.7% CAGR through 2031 because it combines consumer beauty diagnostics, public digital health infrastructure, and hospital AI deployment.

Which application generates the most revenue today?

Dermatology and Clinical Diagnostics led with 51.8% share in 2025, driven by larger contract values and stronger clinical procurement pathways.

Which deployment model is expanding the fastest?

Edge and Device-Based deployment is growing at a 21.3% CAGR through 2031 as point-of-care use cases need faster inference and less reliance on cloud connectivity.

What is the main barrier to wider AI skin adoption?

Dataset bias across skin tones remains a major barrier because under-representation in training data can reduce clinical reliability and slow adoption across diverse populations.

Page last updated on: