AI Search Advertising Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.25 Billion |

| Market Size (2031) | USD 32.89 Billion |

| Growth Rate (2026 - 2031) | 58.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Search Advertising Market Analysis by Mordor Intelligence

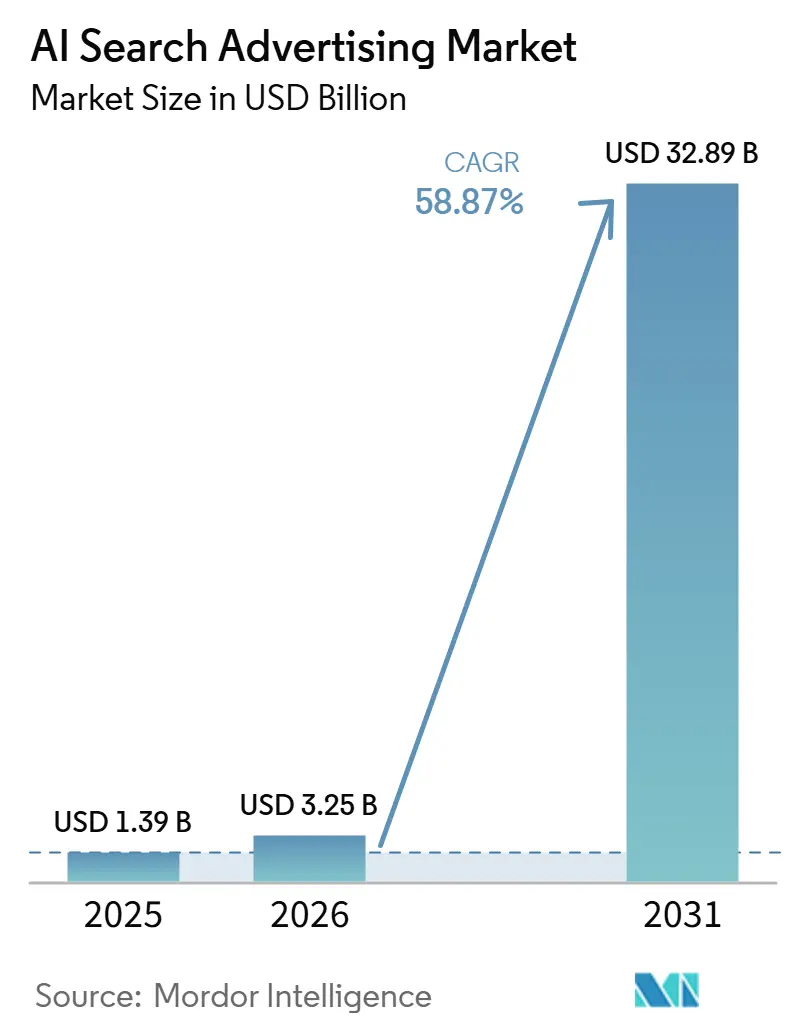

The AI Search Advertising Market size is expected to grow from USD 1.39 billion in 2025 to USD 3.25 billion in 2026 and is forecast to reach USD 32.89 billion by 2031 at 58.87% CAGR over 2026-2031. The AI search advertising market is entering a commercial-scale-up phase as Google, Microsoft, and OpenAI have all introduced monetization models for AI-led search and assistant experiences. Growth is being supported by the shift from keyword matching toward intent-aware delivery, which is changing how inventory is created, matched, and optimized inside search journeys. The studied market is also benefiting from stronger advertiser interest in automated campaign tools, cloud-based execution, and first-party data systems that can support closed-loop measurement in privacy-constrained environments. At the same time, adoption is still being shaped by measurement gaps, concentration of available inventory across a small number of platforms, and tighter brand safety review in regulated sectors. Competitive positioning will continue to depend on platform access, product depth, and the ability to help advertisers manage attribution, campaign migration, and AI-native creative execution.

Key Report Takeaways

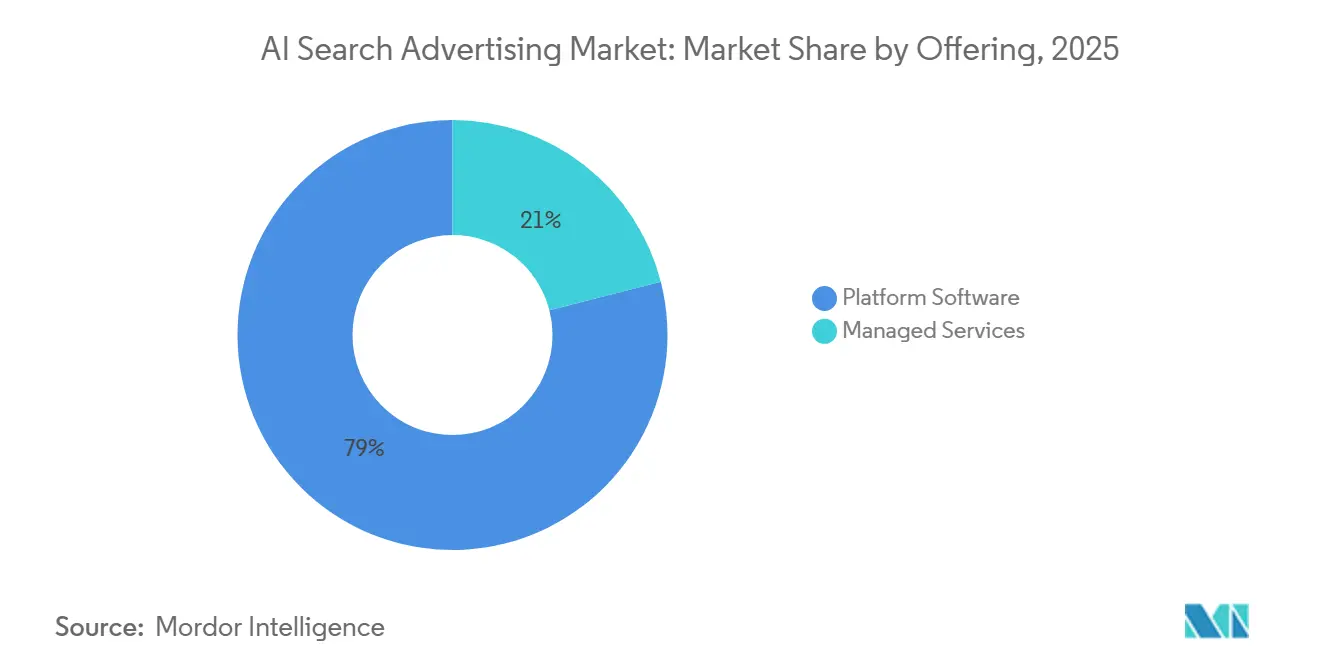

- By offering, platform software accounted for 78.98% of revenue share in the AI search advertising market in 2025, while managed services are projected to expand at a 60.72% CAGR through 2031.

- By ad format, sponsored links in search results held 47.79% of revenue share in the AI search advertising market in 2025, while conversational search ads are projected to expand at a 68.34% CAGR through 2031.

- By deployment, cloud accounted for 92.21% of revenue share in the AI search advertising market in 2025 and is also projected to record the fastest CAGR at 61.50% through 2031.

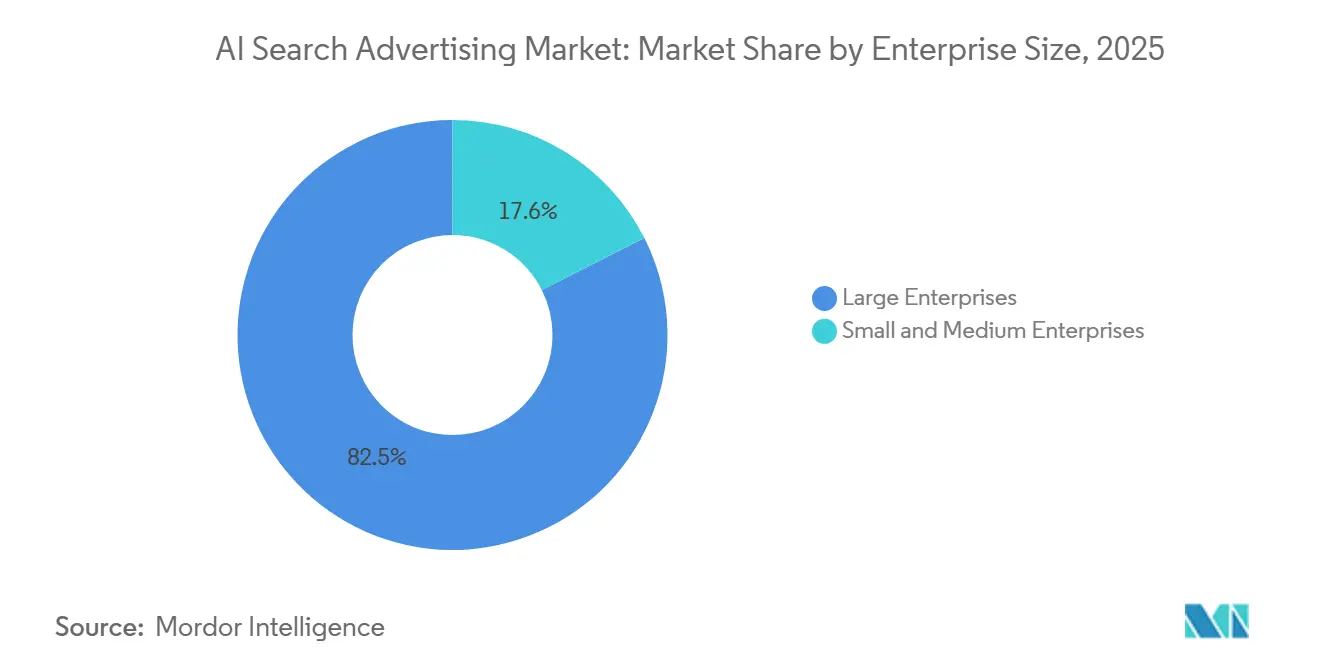

- By enterprise size, large enterprises held 82.45% of revenue share in the AI search advertising market in 2025, while small and medium enterprises are projected to expand at a 62.22% CAGR through 2031.

- By end user industry, retail and e-commerce accounted for 29.99% of revenue share in the AI search advertising market in 2025, while travel and hospitality are projected to expand at a 65.56% CAGR through 2031.

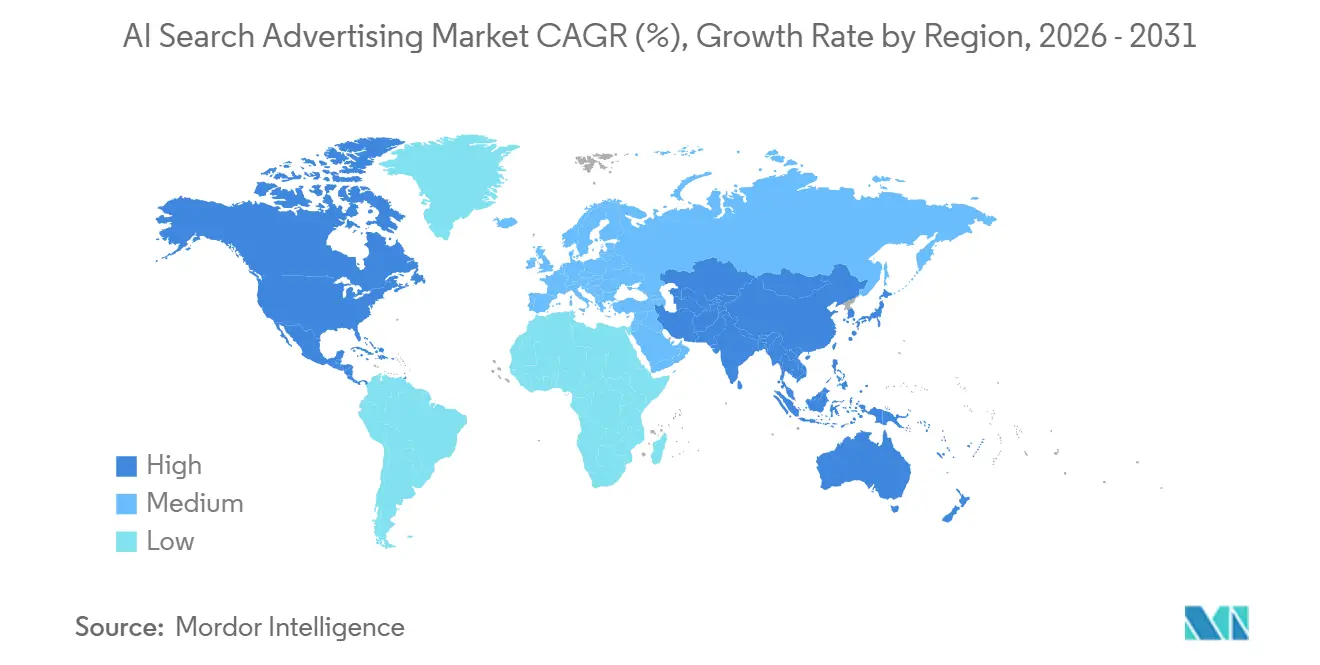

- By geography, North America held 37.78% of the revenue share in the AI search advertising market in 2025, while Asia-Pacific is projected to expand at a 63.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Search Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of AI-Powered Search Surfaces Across Search and Assistant Experiences | +15.2% | Global, with concentrated early gains in North America and Asia-Pacific | Short term (≤ 2 years) |

| Shift From Keyword-Only Targeting to Intent-Aware Ad Delivery | +12.4% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Higher Conversion Uplift From Search Campaign Automation and Broad Match Optimization | +9.8% | Global, enterprise-heavy markets leading | Medium term (2-4 years) |

| Growing Demand for First-Party Data and Closed-Loop Measurement in Privacy-Constrained Search | +7.6% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Rise of Conversational Commerce and Product Discovery Inside AI Search Journeys | +5.8% | Asia-Pacific core, with spillover to North America and Europe | Medium term (2-4 years) |

| Monetization Push By Platform Owners to Build New Search Ad Inventory | +4.2% | Global, led by a United States-headquartered platform owners | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of AI-Powered Search Surfaces Across Search and Assistant Experiences

The AI search advertising market entered a new phase when AI search surfaces shifted from product testing to commercial rollout across search and assistant experiences. Google expanded ad visibility within AI-led search journeys through AI Mode and newer Gemini-based formats that place sponsored content closer to answer-generation and discovery flows.[1]Google, “Ads in AI Mode,” Google Business, business.google.com Google also introduced Conversational Discovery Ads and Highlighted Answers, expanding the number of monetizable placements available within AI search experiences. Microsoft reported that AI-driven sessions nearly tripled in 2025 and that agentic browser traffic rose sharply, which shows how quickly advertiser-relevant search behavior is moving into AI interfaces. This matters because AI surfaces do not simply add more impressions; they also change where intent becomes visible and where sponsored results can appear. As more discovery, comparison, and answer-led journeys move into these environments, the AI search advertising market gains a larger and more commercially useful inventory base.

Shift From Keyword-Only Targeting to Intent-Aware Ad Delivery

The AI search advertising market is also being driven by the shift from keyword matching to intent-aware ad delivery. Google announced AI Max for Search campaigns left beta in April 2026 and confirmed that Dynamic Search Ads will be upgraded to AI Max from September 2026. That change makes intent modeling a practical requirement for advertisers seeking broad reach across AI-enabled search environments. Google stated that AI Max can deliver more conversions at similar efficiency by matching ads to more complex query behavior than keyword-only setups can capture. Microsoft also presented stronger engagement and conversion outcomes for Copilot ad placements, which supports the case for moving budgets toward AI-led query interpretation and away from narrower legacy targeting logic. The result is a structural change in campaign management, where advertisers increasingly compete on intent coverage, training data quality, and automation readiness rather than on keyword lists alone.

Higher Conversion Uplift From Search Campaign Automation and Broad Match Optimization

Stronger conversion outcomes from automation are becoming one of the clearest commercial supports for the AI search advertising market. Google’s Gemini-based ad formats were designed to generate contextual explanations and place ad content within more interactive search flows, thereby shortening the path between query and action. Microsoft stated that Brand Agents and broader AI search tools improved session quality and conversion performance in early deployments, especially where retailer and commerce integrations were already in place. This creates a practical incentive for advertisers to move more campaigns into systems that can automate creative matching, query interpretation, and real-time bid optimization. It also gives large advertisers a reason to migrate budget more quickly, as performance gains can be measured at the campaign level rather than only at the inventory level. Over time, that performance gap is likely to widen between advertisers that actively use AI-led automation and those that still rely on manual structures.

Growing Demand for First-Party Data and Closed-Loop Measurement in Privacy-Constrained Search

The AI search advertising market is also being shaped by a stronger need for first-party data and more direct measurement systems. As AI search journeys become less dependent on conventional click paths, advertisers need better ways to connect exposure, engagement, and conversion across channels. Microsoft introduced Clarity AI Visibility to help brands understand how AI systems discover and cite their content, which adds a new layer of signal to search performance management.[2]Microsoft Advertising, “Building a New AI Economy That Creates Value for Everyone,” Microsoft Advertising Blog, about.ads.microsoft.com This raises the value of advertisers that already have clean customer data, server-side tracking, and stronger internal analytics discipline. It also improves the position of managed service providers, enabling them to help clients implement attribution frameworks without relying on fading third-party identifiers. As privacy rules and AI disclosure requirements continue to expand, the advertisers best prepared for the AI search advertising market will be those that can combine first-party data depth with dependable closed-loop measurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CPC Pressure and Shrinking Visibility Due to AI Overviews and SERP Compression | -7.4% | Global, with sharper impact in North America and Europe | Short term (≤ 2 years) |

| Limited Inventory and Weak Performance Proof in Standalone AI Chatbot Ads | -6.8% | Global, most acute outside the United States, where AI Chat ad platforms are not yet live | Medium term (2-4 years) |

| Measurement Opacity From Hidden Queries and Zero-Click Search Behavior | -4.6% | North America and Europe, with less pronounced effects in Asia-Pacific | Medium term (2-4 years) |

| Brand Safety, Hallucination Risk, and Inconsistent Context Matching in Generative Search Placements | -3.2% | Global, especially regulated sectors in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising CPC Pressure and Shrinking Visibility Due to AI Overviews and SERP Compression

A near-term constraint on the AI search advertising market is the way AI-generated search layouts can compress visible space and change traffic patterns. As search journeys shift toward AI summaries, recommendation lists, and guided-answer formats, advertisers may face fewer obvious placement opportunities at the top of the page. Google’s rollout of ads in AI Mode confirms that monetization remains active inside these surfaces, but it also means visibility is increasingly tied to newer inventory rules and format eligibility requirements. Google’s required migration from Dynamic Search Ads to AI Max further suggests that advertisers will need updated campaign structures to compete effectively inside these environments.[3]Google, “Dynamic Search Ads Are Upgrading to AI Max,” Google Business, business.google.com This can increase operating pressure for smaller advertisers that lack automated bidding, data feedback loops, and in-house optimization resources. The restraint is likely to soften over time, but it remains a meaningful adoption barrier while pricing, placement behavior, and measurement standards are still settling.

Limited Inventory and Weak Performance Proof in Standalone AI Chatbot Ads

The AI search advertising market also faces a supply-side constraint, as the number of commercially meaningful standalone AI chatbot ad surfaces remains limited. Most live scale today still sits with established platform owners that already control search demand, advertiser relationships, and auction infrastructure. Google and Microsoft both expanded their AI-led ad products in 2026, which helped validate the opportunity, but it also underscored how concentrated the available inventory remains. For advertisers outside the earliest launch markets, access to conversational inventory remains uneven, slowing testing and keeping budget allocation cautious. This matters especially for brands that want evidence across multiple platforms before shifting large shares of spend into AI-led placements. Until more platforms demonstrate stable reach, broader geographic access, and repeatable performance proof, inventory concentration will continue to restrain the pace of expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Software Anchored Execution While Services Scaled Faster

Platform software accounted for 78.98% of the AI search advertising market in 2025, which shows how strongly advertisers still rely on native campaign systems controlled by platform owners. These environments sit closest to auction data, intent interpretation, and format eligibility, so they remain central to execution quality and scale. Google’s transition from Dynamic Search Ads to AI Max reinforces that the most important product shifts are happening inside core platform infrastructure rather than at the outer edge of the tool stack. Microsoft’s open pilot for AI Max for Search also reflected the same pattern, where access to AI-led ad delivery remains tied to the platform layer itself. In practical terms, the dominant role of platform software means advertisers often need to adapt their workflows to the rules, inventory logic, and measurement systems set by a small group of platform owners.

Managed services are projected to expand at a 60.72% CAGR through 2031, indicating a clear execution gap within the AI search advertising industry. Many brands can buy access to AI-led formats, but fewer can manage first-party data feeds, migrate to AI Max, interpret queries, vary creative, and redesign attribution without outside help. That gap is widening as AI search campaigns become less keyword-led and more dependent on automation, cloud delivery, and real-time signal management. Service providers that can translate platform complexity into repeatable operating models are therefore gaining a larger role in campaign setup, governance, and performance tuning. This is why managed services are not displacing platform software, but are scaling alongside it as advertisers try to keep pace with changing AI search workflows.

By Ad Format: Conversational Ads Gained Speed While Sponsored Links Kept Scale

Sponsored links in search results accounted for 47.79% of the market in 2025, indicating that traditional text-led formats still accounted for the largest share of revenue. That position reflected their familiarity, their broad reach across Google Search and Bing, and the fact that advertisers already had established planning and optimization processes around them. The AI search advertising market still depends on sponsored links for current volume because they remain embedded in mainstream search buying behavior. Even so, format leadership in scale is no longer the same as leadership in momentum. The newer format story is being written by ad units that sit closer to AI-generated answers, discovery prompts, and guided product evaluation.

Conversational search ads are projected to expand at a 68.34% CAGR through 2031, making them the fastest-growing ad format in the AI search advertising market. Google introduced Conversational Discovery Ads and Highlighted Answers in May 2026, which moved sponsored messaging directly into AI Mode recommendation and answer environments. Google also cited consumer research showing that AI Mode users made faster, more confident purchase decisions, which supports the case for in-answer placements that reduce friction along the decision path. Product listing ads and other commerce-led formats are also gaining traction as platforms use AI to explain products at the query level rather than just listing them. This keeps sponsored links relevant in the near term, but it shifts the long-term growth center toward more conversational, context-aware inventory.

By Deployment: Cloud Stayed Dominant Because AI Search Execution Depends On Scale

Cloud accounted for 92.21% of the AI search advertising market in 2025, and cloud is also projected to expand at a 61.50% CAGR through 2031. This pairing is important because it shows that the largest deployment model is still the one gaining speed, rather than ceding ground to alternatives. The AI search advertising market relies on real-time inference, fast creative rendering, and continuous bidding decisions across large query volumes, and those functions align more naturally with cloud infrastructure than with local deployment models. Google’s AI Max transition and Microsoft’s AI-led ad tools both reflect product paths that are delivered through platform-scale cloud environments. That makes cloud access less of an optional architectural choice and more of a practical requirement for participating in higher-performing AI search at scale.

On-premise deployment still has a place in tightly regulated settings, especially where institutions want closer control over sensitive data or must comply with localization requirements. Even there, adoption is limited because the newest generative ad products are launched and updated within cloud-native ecosystems. This limits the functional equivalence that on-premises setups can offer compared to current product generations. The AI search advertising market is therefore likely to remain heavily cloud-led, with on-premise serving only narrow use cases rather than broad campaign demand. Over the forecast period, deployment decisions will continue to be driven by performance, access, model availability, and security governance rather than by a preference for local infrastructure.

By Enterprise Size: Large Enterprises Led Early, but SMEs Started to Open Up

Large enterprises held 82.45% of the market in 2025, reflecting their stronger ability to invest early in data systems, integrations, and dedicated AI campaign teams. The AI search advertising market initially favored these buyers because they could absorb testing costs, meet spend thresholds, and build the technical connections needed for campaign learning and attribution. They were also better positioned to run multi-format strategies across search, shopping, and conversational placements simultaneously. This created an early structural advantage that smaller advertisers could not easily match.

Small and medium enterprises are projected to expand at a 62.22% CAGR through 2031, signaling that access barriers are easing. The removal of minimum spend requirements for ChatGPT Ads Manager and the broader opening of AI-led self-serve search tools widened the path for smaller advertisers to test these formats. Microsoft’s expansion of AI Max for Search in an open pilot also supported that shift by making AI-enabled campaign access available to a broader set of advertisers. Even so, the AI search advertising market still presents friction for SMEs because setup now depends more on measurement readiness, data hygiene, and automation literacy than on creative budget alone. That is why smaller advertisers are likely to grow faster in adoption while still depending more heavily on simplified tools and outside support.

By End User Industry: Retail Kept Revenue Leadership While Travel Accelerated Fastest

Retail and e-commerce accounted for 29.99% of the AI search advertising market in 2025, making it the largest end-user segment. This was a natural fit because retail demand already sits close to product discovery, comparison, and purchase intent, which are the exact moments AI-led search experiences are trying to improve. Retail advertisers also benefit from richer product feeds, faster testing cycles, and more direct conversion signals than many regulated or longer-consideration sectors. That gives them a clear advantage when platforms roll out AI-led shopping, recommendations, and answer-based product placements. The segment, therefore, remained the strongest current revenue base, even as other industries began to accelerate.

Travel and hospitality are projected to expand at a 65.56% CAGR through 2031, which makes them the fastest-growing end-user segment in the AI search advertising market. Google consolidated travel ad formats into a unified AI Max-powered search campaign structure, simplifying how hotels, flights, and car rental inventory can be bought and optimized within AI-led search experiences. Google, Alvarez, and Marsal also described a future in which AI-led personalization and more agentic discovery reshape how travel decisions are made and recorded, strengthening the case for early investment by travel brands. BFSI and healthcare still matter, but both remain more constrained because claim control, disclosure, and review processes are harder to manage in generative placements. Media and entertainment, IT and telecommunications, automotive, and education remain earlier in adoption, although automotive and education are showing stronger intent signals than several other emerging verticals.

Geography Analysis

North America held 37.78% of the AI search advertising market share in 2025, maintaining the region's lead in both commercial rollout and platform control. The United States remained the operating center for the category because Google, Microsoft, and OpenAI all advanced AI-led ad products from their home-market base. Google made ads available in AI Mode and added new Gemini-based ad formats in 2026, widening monetization pathways in the region. Microsoft also opened AI Max for Search more broadly and extended its availability across Copilot and Bing AI surfaces, strengthening the region’s lead in commercial availability. That early access gave North American advertisers a practical advantage in testing formats, building measurement systems, and shaping best practices before many international peers had comparable inventory.

Asia-Pacific is projected to expand at a 63.39% CAGR in the AI search advertising market size through 2031, making it the fastest-growing geography. China provided the strongest scale signal, with its generative AI user base reaching 602 million in December 2025, equal to 42.8% of the population. That user base provides a strong behavioral foundation for AI-led search monetization, even though platform structures differ from those in Western markets. India is becoming more relevant as an adtech engineering and platform support hub, giving the region a broader operational role than demand alone. Australia, South Korea, and Southeast Asia are also contributing to regional expansion as advertisers test AI-enabled formats in mobile-first digital environments.

Europe remains more constrained in the near term because advertiser access to some conversational AI inventory has been less complete than in the United States. The United Kingdom, France, and Germany are leading regional adoption, while Italy and Spain are still earlier in their rollouts and budget migrations. This leaves much of Europe dependent on search ecosystems that already have live scale, narrowing pricing flexibility and slowing multi-platform experimentation. South America remains smaller today, but mobile-led adoption creates room for faster future scaling from a lower base. The Middle East is developing more quickly, with government-backed AI programs supporting digital infrastructure, platform readiness, and enterprise adoption. Saudi Arabia and the UAE are the clearest examples of this acceleration, as national AI policies have made the region more attractive for commercial deployment. Africa remains the earliest-stage geography, with South Africa still the most developed regional market for digital advertising and future AI search monetization.

Competitive Landscape

The AI search advertising market is consolidating around a small set of platform owners that control search demand, model development, advertiser relationships, and inventory creation. Google remains the most structurally advantaged participant because it can connect AI Overviews, AI Mode, AI Max, shopping flows, and search auctions within a single operating stack. Its decision to move Dynamic Search Ads into AI Max showed that it is not treating AI search as an add-on, but as the new default path for automated search buying. Microsoft is the clearest large-scale challenger because it has expanded AI Max for Search and extended AI-led delivery across Copilot and Bing surfaces. OpenAI has also become an important competitive force because ChatGPT Ads Manager introduced a third meaningful monetized AI search surface, even though geographic access and operating maturity still lag the largest incumbents.

The next competitive layer sits below the major inventory owners and focuses on optimization, verification, and campaign management. These companies are not trying to replace core search platforms, but to make them easier to use, safer to buy, and easier to measure. DoubleVerify’s expansion into AI-generated placement verification reflects how brand safety is becoming a more central buying criterion as generative responses and sponsored content converge. Verve Group made one of the more visible strategic moves in 2026 by launching conversational intent targeting that combines zero-party data, search intent intelligence, and anonymized LLM activity signals in a single decision layer. That type of positioning matters because the AI search advertising market is no longer defined only by inventory ownership, but also by who can make AI-led buying more transparent and more actionable.

Competitive behavior is increasingly centered on product migration, workflow simplification, and control of advertiser data. Google’s release of Conversational Discovery Ads and Highlighted Answers showed how quickly the leading platform can introduce new inventory types inside AI-generated search flows. Microsoft’s rollout of Offer Highlights and broader AI Max access showed a parallel strategy focused on making Copilot and Bing commercially credible at a larger scale. OpenAI’s move to open ChatGPT Ads Manager more broadly also signaled that competitive pressure is rising around self-serve accessibility and lower spend barriers. At the same time, the AI search advertising market still leaves room for managed service firms and software specialists because many advertisers need help with migration, attribution, and governance, even after the major platforms simplify access.

AI Search Advertising Industry Leaders

Google LLC

Microsoft Corporation

Amazon.com, Inc.

Yandex N.V.

NAVER Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: OpenAI confirmed the rollout of conversion-optimized ChatGPT ad campaigns, with early access starting June 5, 2026, for advertisers who pre-configured the OpenAI Pixel or Conversions API by June 1. This introduced performance-bidding mechanics to AI conversational search advertising for the first time, directly competing with Google’s conversion-optimized campaign infrastructure.

- June 2026: Microsoft unveiled the expansion of Microsoft Web IQ at BUILD 2026, an AI-native search infrastructure connecting AI agents to real-time business intelligence via grounding APIs. Nasdaq deployed Web IQ for its Boardvantage AI applications, marking one of the first major financial sector implementations of AI-native search infrastructure for advertising-adjacent discovery workflows.

- May 2026: Google announced Conversational Discovery Ads and Highlighted Answers at Google Marketing Live on May 20, 2026. Both Gemini-powered formats placed ads directly inside AI Mode responses and recommendation lists with an independent AI-written explainer alongside each ad, eliminating the structural separation between sponsored and organic content in Google Search for the first time.

Global AI Search Advertising Market Report Scope

The AI Search Advertising Market comprises software platforms and managed services that enable businesses to create, manage, optimize, and deliver advertisements within AI-powered search experiences, including conversational search, generative AI assistants, and AI-driven search engines. The market revenue is generated through subscriptions and licensing of AI search advertising platforms, managed campaign services, usage-based platform fees, and advertising spend associated with sponsored search results, conversational search ads, product listing advertisements, and other AI-native ad formats deployed across cloud and on-premise environments for enterprises across multiple industries.

The AI Search Advertising Market Report is Segmented by Offering (Platform Software and Managed Services), Ad Format (Sponsored Links in Search Results, Conversational Search Ads, Product Listing Ads in AI Search Experiences, and Other Ad Formats (Shopping and Commerce Cards, etc.)), Deployment (Cloud and On-Premise), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End User Industry (Retail and E-Commerce, BFSI, Travel and Hospitality, Healthcare and Life Sciences, Media and Entertainment, IT and Telecommunications, Automotive, Education, and Other End User Industry), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform Software |

| Managed Services |

| Sponsored Links in Search Results |

| Conversational Search Ads |

| Product Listing Ads in AI Search Experiences |

| Other Ad Formats (Shopping and Commerce Cards, etc.) |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium Enterprises |

| Retail and E-Commerce |

| BFSI |

| Travel and Hospitality |

| Healthcare and Life Sciences |

| Media and Entertainment |

| IT and Telecommunications |

| Automotive |

| Education |

| Other End User Industry |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By offering | Platform Software | ||

| Managed Services | |||

| By Ad Format | Sponsored Links in Search Results | ||

| Conversational Search Ads | |||

| Product Listing Ads in AI Search Experiences | |||

| Other Ad Formats (Shopping and Commerce Cards, etc.) | |||

| By Deployment | Cloud | ||

| On-Premise | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End User Industry | Retail and E-Commerce | ||

| BFSI | |||

| Travel and Hospitality | |||

| Healthcare and Life Sciences | |||

| Media and Entertainment | |||

| IT and Telecommunications | |||

| Automotive | |||

| Education | |||

| Other End User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of AI search advertising?

The AI search advertising market size was USD 1.39 billion in 2025, reached USD 3.25 billion in 2026, and is forecast to reach USD 32.89 billion by 2031 at a 58.87% CAGR.

Which region leads AI search advertising today?

North America led with 37.78% share in 2025 because the region had the earliest commercial rollout and hosts the main platform owners.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to record the fastest growth at a 63.39% CAGR, supported by a large AI user base and strong platform activity across several countries.

Which ad format is gaining momentum the fastest?

Conversational search ads are expected to grow the fastest at a 68.34% CAGR as platforms place sponsored content closer to AI-generated answers and guided discovery.

Why are managed services growing so quickly in this space?

Managed services are projected to grow at a 60.72% CAGR because many advertisers still need help with AI Max migration, attribution setup, first-party data use, and campaign optimization.

Which end user segment is creating the strongest growth opportunity?

Travel and hospitality are expected to expand at a 65.56% CAGR as AI-led trip planning, unified campaign structures, and personalized discovery become more central to travel advertising.

Page last updated on: