AI-powered Workforce Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

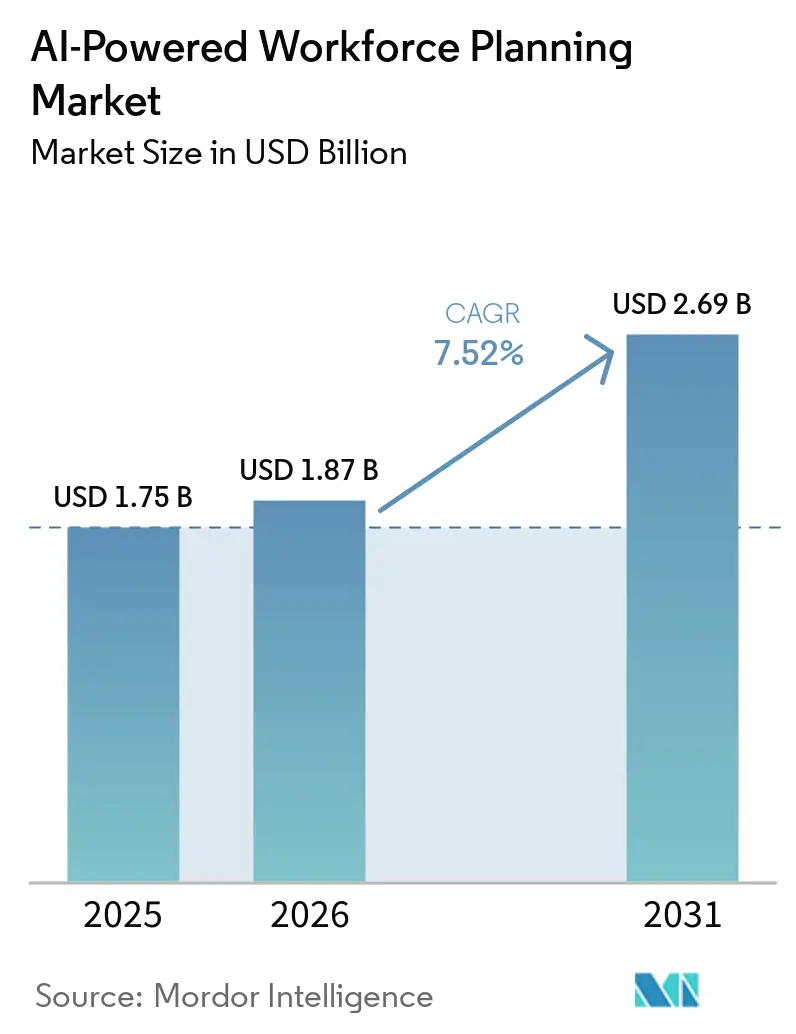

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 7.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-powered Workforce Planning Market Analysis by Mordor Intelligence

The AI-powered Workforce Planning Market size is expected to grow from USD 1.75 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.69 billion by 2031 at 7.52% CAGR over 2026-2031. Growth in the AI-powered Workforce Planning Market is being driven less by broad digitization budgets and more by a clear shift from annual headcount planning to continuous, AI-enabled workforce intelligence that updates more frequently. Organizations that once handled workforce planning mainly within HR are now tying it directly to finance, operations, and corporate strategy, shortening decision cycles from quarters to weeks and, in some cases, to near-real-time review windows. Demand is also rising because enterprise automation programs are forcing employers to decide which roles will change, which employees can be redeployed, and where reskilling budgets will create the fastest operational return. Competition in the AI-powered Workforce Planning Market is moving away from broad feature lists and toward model accuracy, explainability, integration depth, and the ability to fit into existing HCM and ERP environments. At the same time, regulatory compliance costs, data unification challenges, and resistance in regulated or union-sensitive settings are shaping buying behavior and keeping the AI-powered Workforce Planning Market moderately fragmented.

Key Report Takeaways

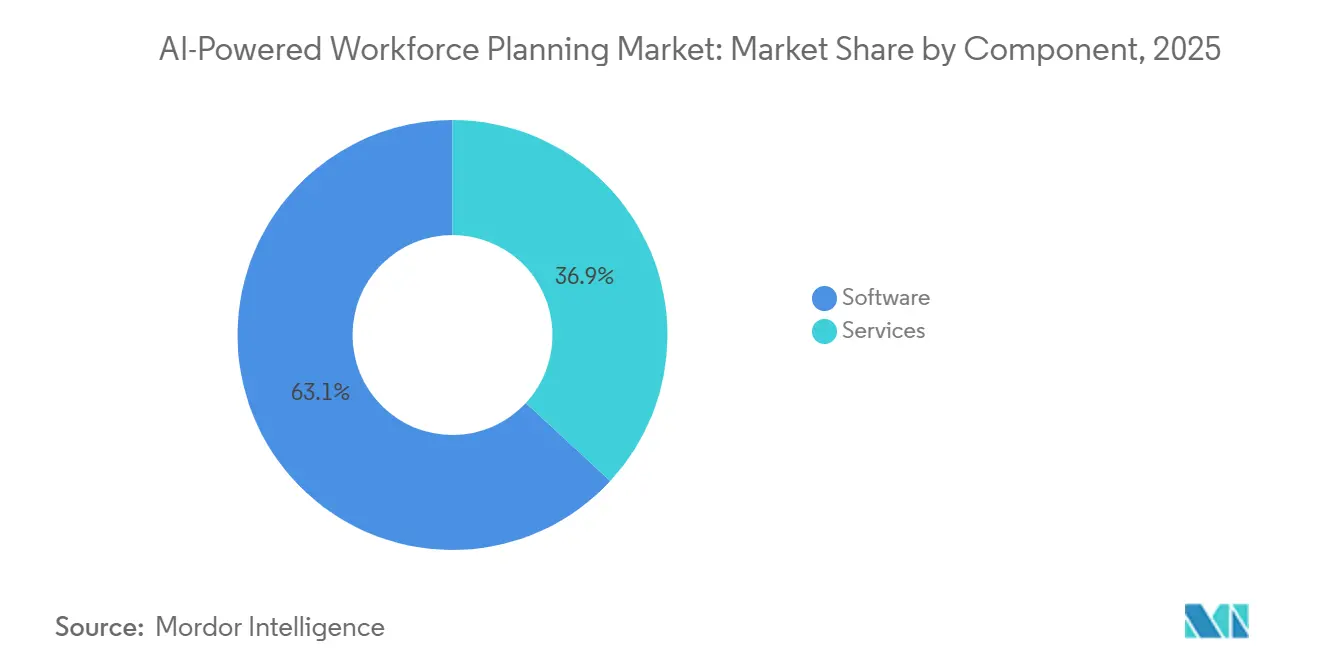

- By component, software held 63.12% of the AI-powered Workforce Planning Market share in 2025, while services is forecast to expand at a 10.41% CAGR through 2031.

- By software type, time and attendance management led with 37.14% share in 2025, while workforce analytics is projected to grow at a 9.33% CAGR through 2031.

- By deployment mode, on-premises accounted for 67.88% of the AI-powered Workforce Planning Market share in 2025, while cloud is forecast to advance at a 10.72% CAGR through 2031.

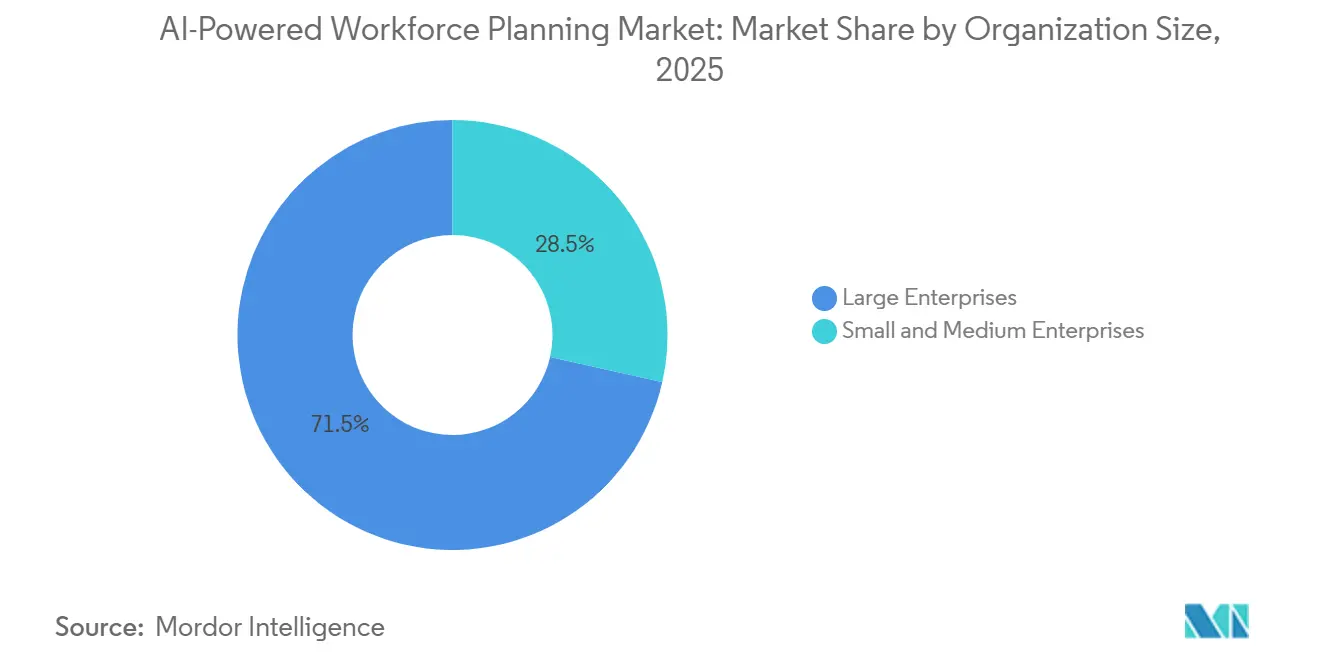

- By organization size, large enterprises held 71.49% share in 2025, while SMEs are expected to record the fastest growth at a 10.05% CAGR through 2031.

- By end-user industry, IT and telecommunications accounted for 32.41% of the AI-powered Workforce Planning Market share in 2025, while healthcare and life sciences is projected to expand at an 8.91% CAGR through 2031.

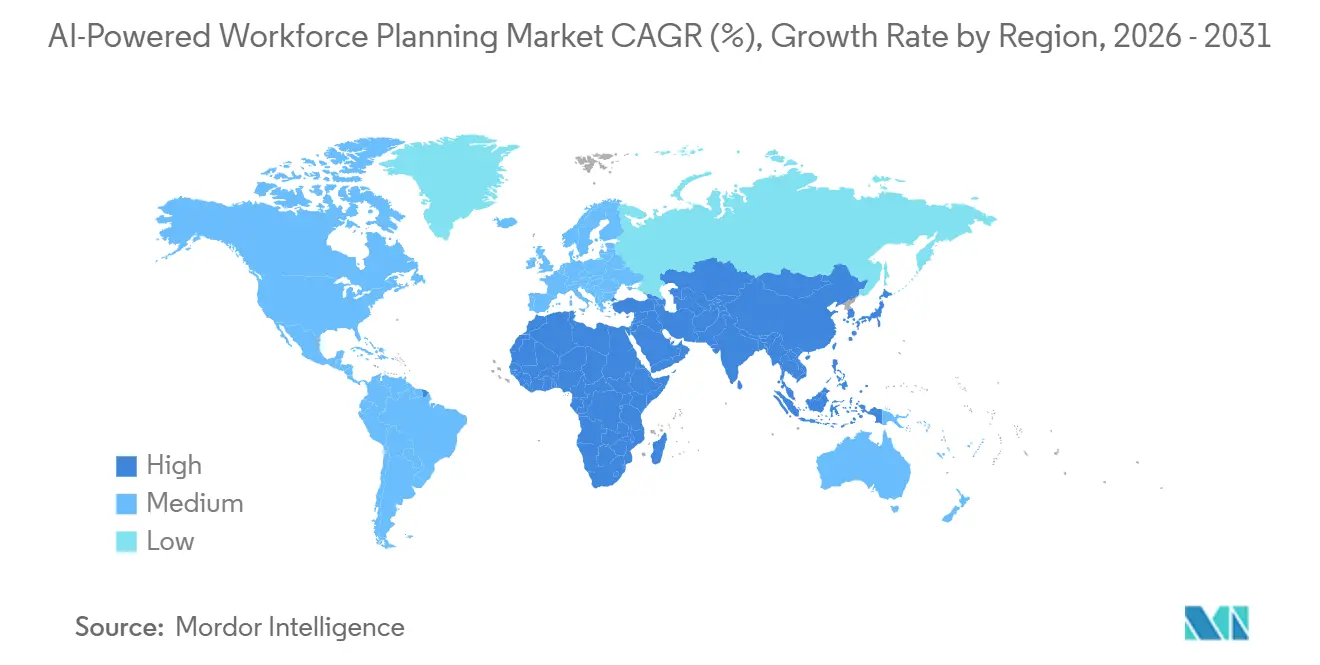

- By geography, North America held 38.56% share in 2025, while Asia-Pacific is forecast to grow at a 9.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-powered Workforce Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Agentic AI Copilots Compressing Workforce Planning Cycle Times | +2.1% | Global, with early gains in North America and Northern Europe | Short term (≤ 2 years) |

| Need for Data-Driven Talent Allocation in Hybrid and Distributed Workforces | +1.8% | Global, strongest in North America, Europe, and Australia and New Zealand | Medium term (2-4 years) |

| Rising Adoption of Skills-Based Workforce Planning and Internal Mobility | +1.5% | Global, with concentrated adoption in Europe and APAC | Medium term (2-4 years) |

| Cloud HCM and ERP Integration Enabling Continuous Workforce Forecasting | +1.2% | North America and EU core, with spillover to APAC and the Middle East | Medium term (2-4 years) |

| Labor Cost Pressure and Need for Productivity Optimization | +0.9% | Global, most acute in North America healthcare, retail, and manufacturing | Short term (≤ 2 years) to Medium term (2-4 years) |

| AI-Led Workforce Redeployment for Enterprise Automation Programs | +0.7% | North America and Europe, with early adoption in APAC technology sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Agentic AI Copilots Compress Enterprise Planning Cycles

The AI-powered Workforce Planning Market is moving beyond assistive AI tools and toward agentic systems that can connect data, run scenarios, and recommend actions with less human intervention. Product launches in 2025 and 2026 show that autonomous planning workflows are moving into mainstream workforce software roadmaps rather than remaining in experimental pilots.[1]Legion Technologies, “Legion Launches 90+ AI Workforce Innovations,” Legion Technologies, legion.co Legion introduced more than 90 AI workforce innovations in January 2026, and Eightfold introduced TalentForge in May 2026 to enable enterprises to build custom HR applications on its talent intelligence layer. That shift reduces the distance between a planning question and an operating response, especially when labor forecasts, schedules, and skills data need to be updated together. It also puts pressure on vendors that still rely on slower, human-reviewed batch workflows, as buyers increasingly expect continuous planning rather than periodic reporting. Enterprises still need strong override rules and auditable workflows because faster automation only supports the AI-powered Workforce Planning Market when governance is embedded into day-to-day planning processes.

Need for Data-Driven Talent Allocation in Hybrid and Distributed Workforces

Hybrid and distributed work models are making static workforce snapshots much less useful in the AI-powered Workforce Planning Market. Buyers increasingly need live visibility into staffing levels, schedules, internal mobility, labor demand, and budget limits across locations, teams, and worker types. SD Worx reported that 48.2% of European organizations identified scheduling efficiency and adequate staffing as primary reasons for making workforce planning a 2026 priority. That pattern shows that many employers are buying these tools to protect day-to-day operating continuity and service levels, not simply to pursue digital experimentation. Oracle’s prebuilt AI agents in Fusion Cloud HCM also demonstrate how vendors are integrating internal mobility, career development, succession planning, and payroll anomaly detection into a single, connected workflow. As hybrid work structures remain in place, platforms that connect talent availability with business demand are improving their position in the AI-powered Workforce Planning Market.

Rising Adoption of Skills-Based Workforce Planning and Internal Mobility

The AI-powered Workforce Planning Market is also benefiting from a clear move away from job-title planning and toward skills-based planning. SD Worx found that 55.3% of European organizations are shifting from job-role-based to skills-based planning, indicating that this change is already becoming routine in workforce processes. That change increases demand for platforms that can infer skills from work history, project activity, learning records, and performance signals, rather than relying solely on static employee profiles. Oracle’s September 2025 launch of internal mobility and succession planning agents shows how vendors are embedding skills logic directly into established HCM workflows. Orgvue’s Henshaw AI suite also reduced role-grouping work from months to minutes, which supports faster role clustering and redeployment planning at scale. As this shift deepens, the AI-powered Workforce Planning Market is moving closer to internal mobility, redeployment, and reskilling use cases that older planning systems handled only in a limited way.

Cloud HCM and ERP Integration Enable Continuous Workforce Forecasting

Cloud HCM and ERP integration is becoming a practical requirement in the AI-powered Workforce Planning Market because continuous forecasting depends on shared data across HR, finance, and operations. On-premises deployment still held 67.9% of the market in 2025, but cloud is projected to grow at a 10.7% CAGR through 2031, indicating that migration has already moved from pilot programs to a structural transition. Oracle embedded prebuilt AI agents directly into Fusion Cloud HCM, highlighting how vendors are using native cloud environments to deliver faster updates and tighter workflow integration. Legion’s SAP Endorsed App certification in January 2025 also showed how real-time synchronization with SuccessFactors, time tracking, and payroll data is becoming a stronger selling point in enterprise accounts. ATOSS reported that cloud and subscription revenue rose 28% year over year to EUR 92.7 million (USD 100.1 million) in FY2025, confirming that vendor revenue models are already shifting toward continuously updated delivery models. The vendors best positioned in the AI-powered Workforce Planning Market are therefore those with strong connectors, stable APIs, and the ability to fit cleanly into existing enterprise system stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Explainability, and Bias Risks in HR AI Models | -1.2% | EU, United States, and global | Short term (≤ 2 years) to Medium term (2-4 years) |

| Legacy Data Silos and Difficult Integration Across HR, Finance, and Operations | -0.9% | Global, most acute in manufacturing, government, and large diversified enterprises | Medium term (2-4 years) |

| Low Confidence in AI-Generated Skill Inference for Regulated and Unionized Roles | -0.5% | North America and Europe, especially healthcare, public sector, and unionized manufacturing | Medium term (2-4 years) |

| Diffuse Ownership Across HR, Finance, and Operations Slowing Enterprise Rollouts | -0.4% | Global, most acute in large enterprises with siloed planning functions | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Explainability, and Bias Risks in HR AI Models

Compliance pressure remains a real brake on the AI-powered Workforce Planning Market when AI models influence task allocation, performance review, workforce monitoring, or skill inference. The EU AI Act classifies several workplace AI uses as high-risk, requiring buyers to implement stronger documentation, oversight controls, and accountability before full deployment. In the United States, rules such as California's FEHA obligations and New York City’s annual bias audit requirements are pushing enterprises to require bias testing, record retention, and auditable decision logs before approving purchases. These obligations raise implementation costs and often lengthen sales cycles, especially for smaller vendors without dedicated governance teams. They also affect product design, because explainability is becoming a core buying criterion rather than an optional compliance feature. The result is a slower rollout path in regulated settings, even as larger vendors use governance readiness to differentiate themselves inside the AI-powered Workforce Planning Market.

Legacy Data Silos and Difficult Integration across HR, Finance, and Operations

Legacy data architecture continues to slow the AI-powered Workforce Planning Market because model quality depends on consistent and connected data across HR, finance, and operations. Many enterprises still store critical labor data across separate payroll systems, ERP instances, departmental tools, and spreadsheets, making it difficult to build and maintain unified planning models. Integration work, therefore, becomes the longest part of many implementations, especially when older systems still contain the most reliable operating records. This issue is strongest in manufacturing, government, and diversified enterprises, where system fragmentation is tied to long procurement cycles, business-unit autonomy, and older operating environments. It also reduces trust in AI outputs, because forecasting models are judged by the weakest source system connected to them. Until enterprises improve governance standards and integration layers, model sophistication in the AI-powered Workforce Planning Market will continue to outpace the quality of the input data supporting it.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Professional Services Demand Accelerates Alongside AI Platform Adoption

Software accounted for 63.12% of the AI-powered Workforce Planning Market share in 2025, indicating that scheduling, analytics, and planning platforms remain the foundational technology layer for enterprise deployment. This weight reflects the product-led structure used by many vendors, where software subscriptions establish the account footprint before service work expands it across teams and geographies. Even so, services are forecast to grow at a 10.41% CAGR through 2031, the fastest pace among component segments, indicating where implementation complexity is rising. The gap between software scale and services growth suggests that buyers are no longer purchasing only a tool; they are also purchasing configuration, governance support, and operating assistance. That pattern is becoming more visible as the AI-powered Workforce Planning Market moves from rule-based automation toward model-driven planning and continuous workforce intelligence.

Service demand rises further when vendors expand into verticals and countries where labor rules, union terms, and sector taxonomies need local configuration before the platform can be used effectively. ATOSS reported consulting revenue of EUR 35.9 million (USD 38.8 million) in FY2024, up 8% year over year, and linked part of that increase to more complex deployments in healthcare and logistics.[2]ATOSS Software SE, “ATOSS Annual Report 2024,” ATOSS Software SE, atoss.com For the AI-powered workforce planning industry, the result shows that product-led onboarding is still insufficient for many advanced planning and scheduling use cases. It also means the services layer can remain a meaningful revenue stream rather than a short implementation bridge that fades after go-live. Vendors that can combine scalable software with strong configuration, integration, and change support are likely to capture more durable revenue within the AI-powered Workforce Planning Market.

By Software Type: Analytics Platforms Accelerate the Shift from Descriptive to Prescriptive Planning

Time and attendance management accounted for 37.14% of the software type segment in 2025, while workforce analytics will grow at a 9.33% CAGR through 2031, reflecting a shift from control functions toward decision support. Time and attendance remained central because compliance, labor rules, payroll linkage, and schedule execution still anchor platform selection in many enterprise accounts. Workforce analytics is expanding faster because buyers increasingly want systems that connect workforce data to cost, risk, skill availability, and capacity decisions. This changes the way software budgets are framed, since planning tools are being evaluated not only as HR applications but also as operating intelligence layers. In the AI-powered Workforce Planning Market, that upgrade cycle is moving more value toward predictive and prescriptive capabilities than toward basic record-keeping functions.

Transactional modules such as scheduling, leave and absence management, and performance management remain sticky because they sit close to daily operations and are difficult to replace quickly. The next layer of spending is moving into analytics tools that sit above those modules and interpret attendance, performance, and staffing signals in a combined planning view. Orgvue introduced the Henshaw AI suite in December 2025, including automated role grouping and a natural language assistant for organizational data, which reduced manual work from months to minutes. That type of functionality supports faster role clustering, better skill mapping, and earlier detection of capacity gaps before those gaps affect business continuity. As a result, the AI-powered Workforce Planning Market is rewarding vendors that can turn operational data into forward-looking planning actions rather than static reports.

By Deployment Mode: Cloud Migration Accelerates Despite On-Premises Dominance

On-premises deployment held 67.88% of the market in 2025, but cloud is forecast to grow at a 10.72% CAGR through 2031, making deployment strategy one of the clearest transition points in the AI-powered Workforce Planning Market. The large on-premises base reflects older enterprise systems deeply integrated with payroll, ERP, compliance, and time-tracking workflows built over the last decade. That installed base has slowed migration, especially in healthcare, financial services, and the public sector, where data residency and operational continuity concerns remain prominent. Even so, new deployments are increasingly cloud-native because buyers want continuous updates, standard APIs, and faster access to new AI functionality. The result is not an abrupt replacement cycle, but a staged transition to hybrid and then to fuller cloud architectures.

Oracle’s September 2025 release of prebuilt AI agents inside Fusion Cloud HCM showed how cloud delivery lets vendors add mobility, succession, and payroll intelligence directly inside existing workflows. ATOSS reported that cloud and subscription revenue rose 28% year over year to EUR 92.7 million (USD 100.1 million) in FY2025, while cloud ARR reached EUR 101.3 million (USD 109.4 million). Those results show that vendor revenue models are already aligning with the cloud shift, even as many legacy customers still operate in mixed environments. For buyers, cloud adoption reduces the need for separate IT project cycles each time models, workflows, or integrations are updated. For vendors, that transition creates more cross-sell room, deeper stickiness, and a stronger long-term position in the AI-powered Workforce Planning Market.

By Organization Size: Enterprise Deployments Anchor Revenue While SME Adoption Broadens

Large enterprises held 71.49% of the AI-powered Workforce Planning Market in 2025, which reflects their higher seat volumes, broader service needs, and larger multi-country deployments. Complex workforce structures across retail, manufacturing, healthcare, and business services create planning requirements that grow faster than employee counts, especially when roles, locations, and labor models differ widely. That scale makes AI-based scenario modeling, skills mapping, labor forecasting, and capacity planning more valuable for enterprise buyers than for smaller organizations. Large organizations also tend to have the budgets and internal support teams needed to connect workforce planning with finance, operations, and enterprise change programs. This keeps enterprise accounts at the center of current revenue even as adoption spreads more widely across the customer base.

SMEs are forecast to expand at a 10.05% CAGR through 2031, making them the fastest-growing segment in the AI-powered Workforce Planning Market. Cloud delivery and modular pricing are the main reasons, since smaller businesses can adopt selected tools without committing to a full-suite enterprise rollout. TeamOhana said in April 2025 that its platform managed USD 6 billion in workforce spend for more than 30,000 employees, which shows that sophisticated headcount planning is moving into smaller and mid-market accounts. This lower entry barrier is widening the addressable customer base without changing the fact that large enterprises still account for most current revenue. Over time, SME adoption should broaden the AI-powered Workforce Planning Market, while enterprise deployments continue to anchor absolute spending and vendor account priorities.

By End-User Industry: Healthcare Labor Deficits Raise the Value of AI Planning

IT and telecommunications accounted for 32.41% of the end-user industry segment in 2025, while healthcare and life sciences are projected to grow at a 8.91% CAGR through 2031, indicating a split between current software maturity and rising labor pressure. IT and telecom led because cloud adoption, digital operating models, and rapidly changing skill needs made this vertical an early adopter of AI planning tools. Role redesign is especially important there, since employers are managing both growing AI skill demand and changes in how work is distributed between people and automation. In healthcare and life sciences, the purchase case is more immediate because staffing shortages affect service delivery, overtime costs, temporary labor use, and compliance exposure. That difference gives the AI-powered Workforce Planning Market two clear demand paths, one driven by digital maturity and one driven by labor scarcity.

The American Hospital Association’s 2026 workforce scan described persistent workforce shortages and placed annual nurse turnover costs at USD 3.9 million to USD 5.7 million per hospital. GE HealthCare reported that its census-forecasting deployment at Duke Health reduced temporary labor use by 50% and achieved 95% accuracy in staffing needs up to 14 days in advance. Those results explain why healthcare providers are treating scheduling and staffing forecasting as financial controls rather than convenience tools. Banking, manufacturing, retail, government, and other end-user groups still drive meaningful demand, with manufacturing showing increased interest in multi-skills shift planning that needs greater precision and fewer scheduling errors. This broad mix keeps the AI-powered Workforce Planning Market exposed to both knowledge-work planning needs and frontline labor optimization needs.

Geography Analysis

North America held 38.56% of the AI-powered Workforce Planning Market share in 2025, which made it the largest regional contributor and reflected earlier enterprise AI spending, mature cloud HCM adoption, and stronger software procurement cycles. The United States remains the core of that position because large health systems, technology firms, and retailers have sizable planning needs across distributed workforces and complex labor models. Health system labor pressure remains especially important, since hospitals are still absorbing high turnover costs and need better staffing forecasts and scheduling control to contain labor leakage. California FEHA rules and New York City’s annual bias audit requirements are also pushing buyers toward platforms with clearer controls, stronger auditability, and documented decision logic. Canada and Mexico add smaller but expanding demand as cross-border talent visibility and regional labor coordination become more relevant to enterprise workforce strategies.

Asia-Pacific is forecast to grow at 9.67% CAGR through 2031, which makes it the fastest-growing geography in the AI-powered Workforce Planning Market size. Growth in the region is being shaped by China’s enterprise AI programs, India’s large technology services base, and Japan’s need to manage labor scarcity more tightly across aging workforce structures. Demand also benefits from the need to coordinate permanent staff, contractors, and gig workers across large operating footprints, especially in technology and business services. Australia and New Zealand, Japan, South Korea, and the rest of Asia-Pacific broaden the regional base, while South Korea is showing early traction in electronics and semiconductor scheduling use cases.

Europe holds a material position in the AI-powered Workforce Planning Market, but procurement there is shaped by stronger compliance demands and more careful governance review than in several other regions. Workday reported in March 2026 that 41% of German companies said more than 60% of their workforce used AI tools in 2025, which shows high workplace AI exposure across the DACH region.[3]Anja Fordon, “KI im Personalmanagement 2026,” Workday DE, workday.com That same environment also requires employers to work through co-determination and monitoring concerns before deploying workforce AI at scale. South America remains earlier in adoption, with Brazil’s financial services and technology sectors supporting incremental demand, while the Middle East is using AI workforce planning inside broader digital transformation agendas. Africa is still nascent, but financial services and telecommunications in markets such as South Africa and Nigeria are creating early openings for the AI-powered Workforce Planning Market.

Competitive Landscape

The AI-powered Workforce Planning Market is moderately fragmented, with competition spread across workforce management suites, talent intelligence specialists, and headcount planning tools serving different enterprise needs. ATOSS Software SE, Quinyx, Legion Technologies, and WorkForce Software compete from the scheduling and workforce management side, while Eightfold AI, Gloat, Visier, and Orgvue focus more on skills, analytics, and organizational design. TeamOhana and Vemo represent a separate layer that connects finance and HR around headcount planning, especially for mid-market and growth-stage organizations. This mix means few vendors cover every functional category at the same depth, which keeps replacement decisions selective and preserves room for specialists. It also leaves white space for vendors to connect operational scheduling with longer-range skills forecasting within the AI-powered Workforce Planning Market.

Vendor strategies are increasingly shaped by architecture choices, especially whether the platform sits above existing HCM systems or tries to replace them. Oracle embedded prebuilt AI agents into Fusion Cloud HCM in September 2025, strengthening the case for extending an existing suite rather than adding a separate point solution.[4]Oracle, “Oracle AI Agents Help HR Leaders Boost Workforce Productivity and Enhance Performance Management,” Oracle, oracle.com Eightfold launched TalentForge in May 2026 so enterprises could build custom HR applications on top of its talent intelligence layer, reinforcing the orchestration model rather than a full system replacement. Legion expanded its ecosystem in January 2026 through its Rebus warehouse labor management partnership, demonstrating how AI-native scheduling vendors are leveraging integrations to deepen operational use cases.

ATOSS reported its 20th consecutive record year in FY2025, with cloud and subscription revenue rising 28% year over year to EUR 92.7 million (USD 100.1 million), and total ARR reaching EUR 140 million (USD 151.2 million). Eightfold’s ISO/IEC 42001:2023 certification for AI management systems also shows how governance credentials are becoming a clearer procurement differentiator in large enterprise accounts. The competitive gap is now shifting away from broad feature counts and toward model quality, explainability, workflow integration, and trust in AI outputs. Vendors are also investing in knowledge graphs, agentic workflows, and proprietary data assets that are harder for rivals to reproduce quickly. That combination of specialist strength, suite extensions, and limited dominance by any single provider keeps the AI-powered Workforce Planning Market competitive but not consolidated.

AI-powered Workforce Planning Industry Leaders

ATOSS Software SE

WorkForce Software, LLC

Quinyx AB

Legion Technologies, Inc.

Deputechnologies Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Eightfold AI launched TalentForge, a platform enabling enterprises to build custom-fit HR applications integrated with Eightfold's Talent Intelligence, featuring enterprise security architecture and auditable workflows pre-built from day one, enabling organizations to build bespoke workforce planning solutions without starting from scratch.

- April 2026: Visier unveiled the next generation of its Workforce AI platform at Outsmart 2026, introducing guided workforce planning capabilities that integrate demand, skills, and action planning with organizational design into a single connected intelligence layer, alongside a Glean Model Context Protocol integration enabling workforce data access within enterprise AI assistant workflows, general availability is scheduled for May 2026.

- March 2026: Novaworks.ai launched an agentic operating system for total workforce management built on the ServiceNow AI platform and raised USD 8 million in seed funding led by Stalwart Ventures with participation from ServiceNow Ventures and Bell Ventures, targeting replacement of legacy HCM systems with AI-native foundations.

- February 2026: Ando Technologies secured USD 4 million in seed financing led by Slow Ventures to expand its AI forecasting and scheduling platform for the global hourly workforce, having achieved 100% customer retention and over 90% daily demand accuracy in early deployments.

Global AI-powered Workforce Planning Market Report Scope

AI-powered workforce planning tools harness artificial intelligence and machine learning to forecast workforce demands and refine talent strategies. These platforms allow organizations to simulate future workforce scenarios, pinpoint skill gaps, and synchronize talent deployment with business goals. By integrating data from HR, operations, and external sources, they bolster predictive decision-making. The market's emphasis is on evolving traditional workforce planning into a nimble, data-centric, and strategic endeavor.

The AI-powered Workforce Planning Market Report is Segmented by Component (Software, and Services), Software Type (Workforce Scheduling and Planning, Time and Attendance Management, Leave and Absence Management, Workforce Analytics, Employee Performance Management, and Other Software Types), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Banking, Financial Services, and Insurance, Healthcare and Life Sciences, IT and Telecommunications, Manufacturing, Retail and E-commerce, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Workforce Scheduling and Planning |

| Time and Attendance Management |

| Leave and Absence Management |

| Workforce Analytics |

| Employee Performance Management |

| Other Software Types |

| Cloud |

| On-premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Banking, Financial Services, and Insurance |

| Healthcare and Life Sciences |

| IT and Telecommunications |

| Manufacturing |

| Retail and E-commerce |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia and New Zealand | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Software Type | Workforce Scheduling and Planning | |

| Time and Attendance Management | ||

| Leave and Absence Management | ||

| Workforce Analytics | ||

| Employee Performance Management | ||

| Other Software Types | ||

| By Deployment Mode | Cloud | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By End-user Industry | Banking, Financial Services, and Insurance | |

| Healthcare and Life Sciences | ||

| IT and Telecommunications | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia and New Zealand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the AI-powered Workforce Planning Market?

The AI-powered Workforce Planning Market was valued at USD 1.75 billion in 2025, stands at USD 1.87 billion in 2026, and is forecast to reach USD 2.69 billion by 2031 at a 7.52% CAGR.

Which region is growing fastest in AI-powered workforce planning?

Asia-Pacific is the fastest-growing region, with a projected 9.67% CAGR through 2031, driven by enterprise AI adoption, labor-market change, and large distributed workforce structures.

Which segment leads by component in AI-powered workforce planning?

Software leads the component mix with 63.12% share in 2025, while services is growing faster at a 10.41% CAGR as implementation, governance, and analytics support become more important.

Why is healthcare becoming a key demand area for workforce planning software?

Healthcare and life sciences is the fastest-growing end-user segment at 8.91% CAGR because labor shortages, turnover costs, and temporary staffing expenses are pushing providers toward better forecasting and scheduling.

Why is cloud deployment gaining ground over on-premises systems?

Cloud is projected to grow at 10.72% CAGR because it supports continuous model updates, standard APIs, and faster integration with HCM and ERP workflows, even though on-premises still held 67.88% share in 2025.

What is shaping competition among vendors in this space?

Competition is shifting from broad feature breadth to model accuracy, explainability, and integration depth, with vendors such as Oracle, ATOSS, Eightfold, Legion, and Orgvue using AI workflows and ecosystem links to differentiate.

Page last updated on: