AI-powered Surgical Monitor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

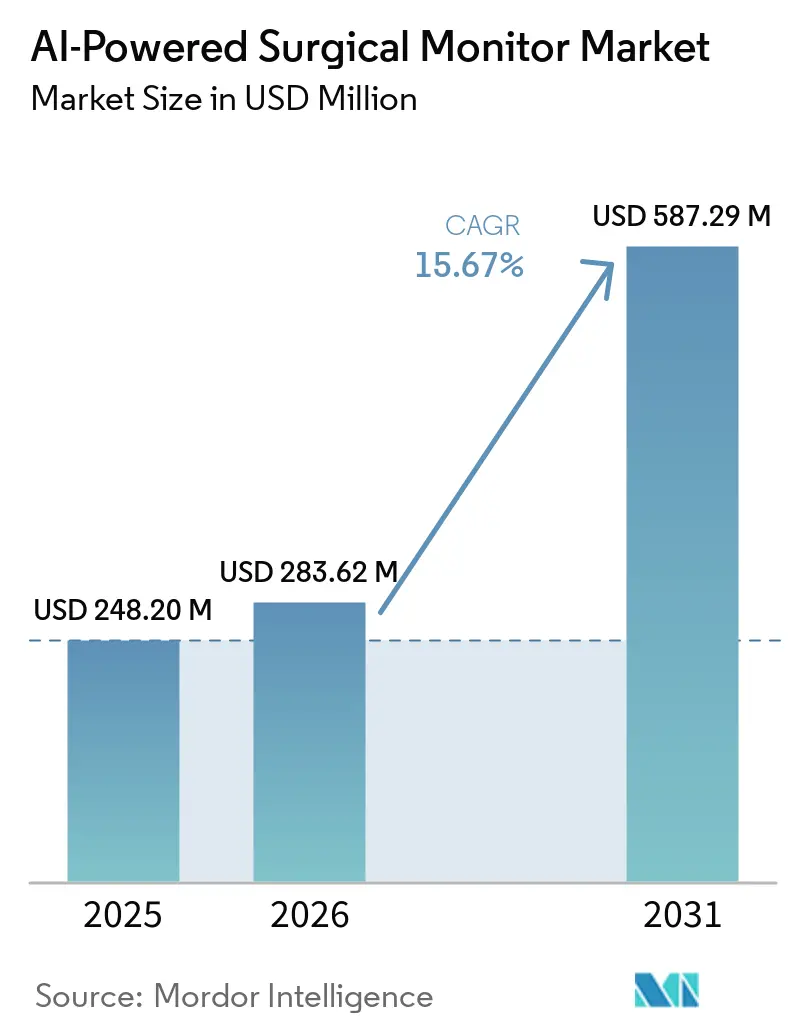

| Market Size (2026) | USD 283.62 Million |

| Market Size (2031) | USD 587.29 Million |

| Growth Rate (2026 - 2031) | 15.67% CAGR |

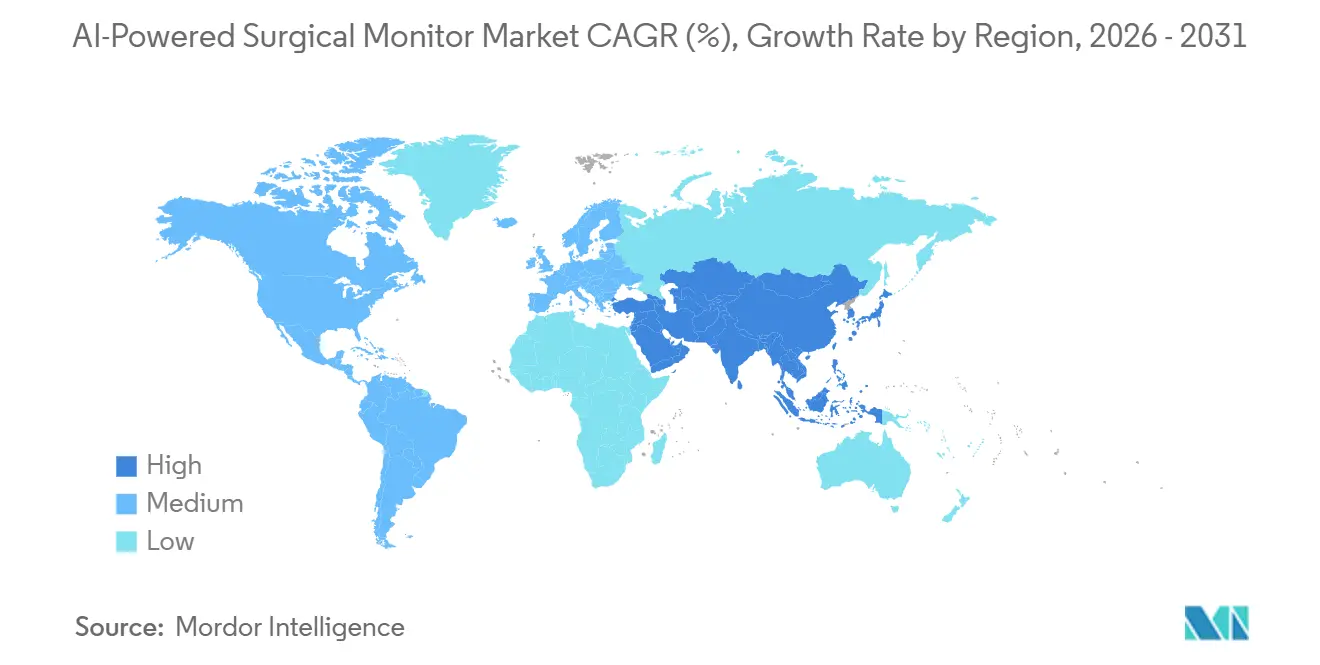

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

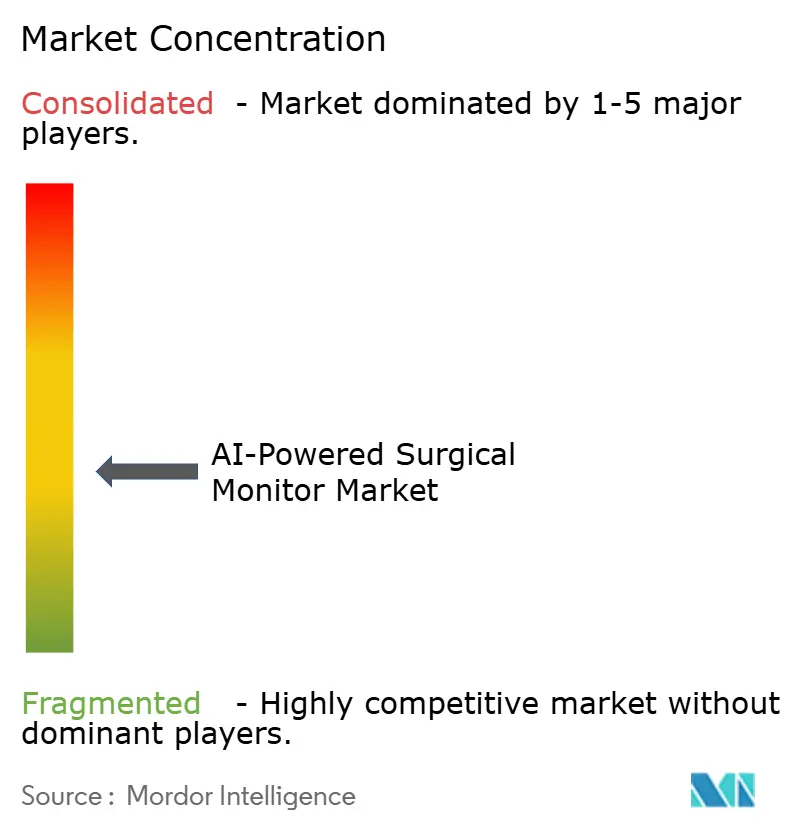

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-powered Surgical Monitor Market Analysis by Mordor Intelligence

The AI-powered Surgical Monitor Market size is projected to expand from USD 248.20 million in 2025 and USD 283.62 million in 2026 to USD 587.29 million by 2031, registering a CAGR of 15.67% between 2026 to 2031.

The market is advancing because minimally invasive and image-guided procedures place the surgeon’s working view on a monitor for the full duration of the operation, which makes display quality and screen-based guidance central to surgical workflow. The commercial rollout of embedded AI is also changing the monitor from a viewing device into a live support layer that can assist with recognition, overlay, and workflow prompts during surgery. Regulatory clearances in the United States, Europe, and Japan are reducing the distance between research validation and hospital deployment, which is widening the addressable base for premium visualization platforms and AI-ready compute modules. The display refresh cycle is reinforcing this adoption path because hospitals and outpatient facilities are upgrading toward brighter, higher-contrast, and higher-resolution systems that can support fluorescence imaging, robotic video output, and AI overlays with better fidelity. Competition remains active across hardware incumbents, display specialists, and AI-focused software players, while spending cycles, reimbursement uncertainty, interoperability gaps, and cybersecurity duties continue to shape adoption speed across health systems.

Key Report Takeaways

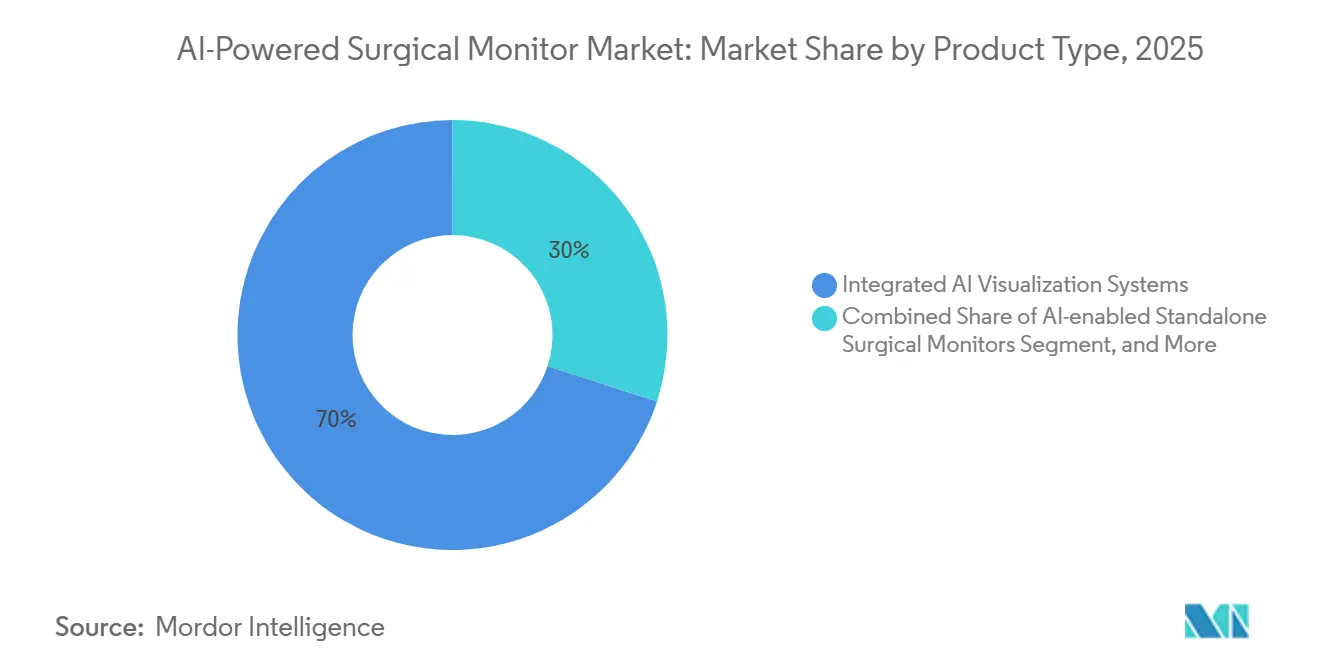

- By product type, integrated AI visualization Systems held 70.02% of the AI-powered Surgical Monitor Market share in 2025, while AI-enabled OR integration display platforms are projected to expand at 16.05% CAGR through 2031.

- By display technology, LED-backlit LCD panels accounted for 56.46% of revenue in 2025, while OLED is forecast to record the highest CAGR at 15.47% through 2031.

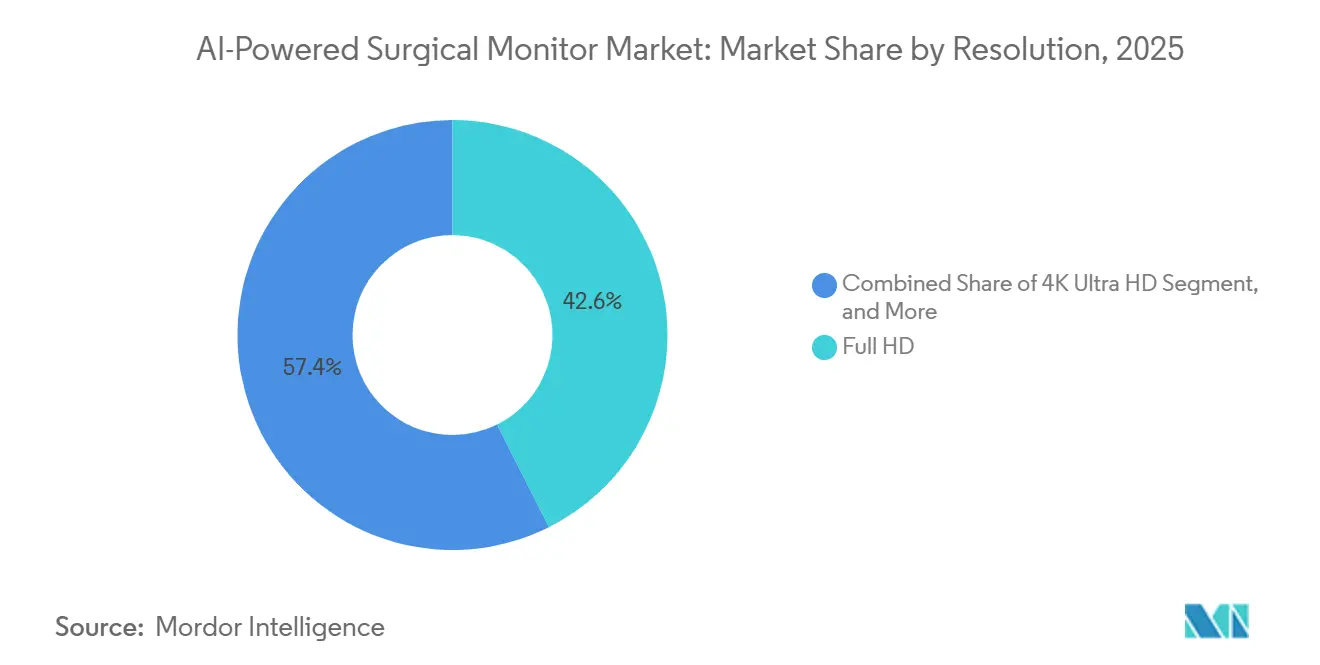

- By resolution, Full HD represented 42.57% of demand in 2025, while 4K Ultra HD is expected to grow fastest at 17.26% CAGR through 2031.

- By application, laparoscopy captured 33.03% share of the AI-powered Surgical Monitor Market size in 2025, while endoscopy is projected to advance at 19.54% CAGR through 2031.

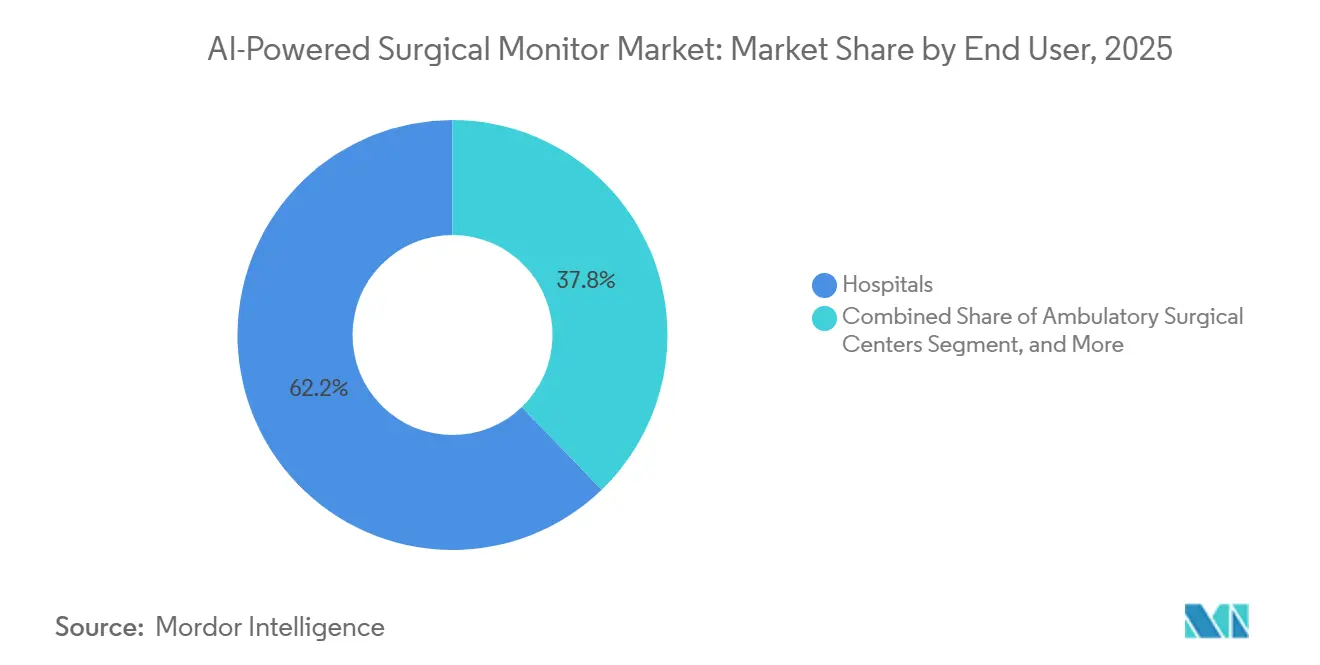

- By end user, hospitals held 62.18% of the AI-powered Surgical Monitor Market size in 2025, while ambulatory surgical centers are expected to post the fastest growth at 17.20% CAGR through 2031.

- By geography, North America led with 43.56% of global revenue in 2025, while Asia-Pacific is forecast to expand at the fastest regional CAGR of 17.89% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-powered Surgical Monitor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Minimally Invasive and Image-Guided Surgery Volumes | +3.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| 4K and 3D Upgrade Cycle in Hybrid Operating Rooms | +2.4% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| ASC Migration Lifts Demand for Compact Visualization Suites | +2.0% | North America, with early adoption in Europe and Australia | Medium term (2-4 years) |

| Embedded AI for Intraoperative Detection and Workflow Automation | +2.8% | Global, with early concentration in North America and Japan | Long term (≥ 4 years) |

| Regulatory Legitimization of Real-Time AI Video Augmentation | +1.6% | North America, Europe, and Japan | Medium term (2-4 years) |

| Need for Multi-Modal Overlays Across Robotics and Navigation | +1.9% | North America and Asia-Pacific, with spillover to Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Minimally Invasive and Image-Guided Surgery Volumes

The AI-powered Surgical Monitor Market is benefiting from the structural rise of minimally invasive and image-guided surgery because the surgeon’s operative field is viewed through a monitor from start to finish. This makes brightness, contrast, latency, and image stability part of clinical workflow rather than secondary hardware features. MedPAC reported that U.S. ambulatory surgical centers performed 6.4 million surgical procedures in 2024 across 6,436 facilities, while procedure volume per 1,000 Medicare beneficiaries increased 3.4% year over year, which shows the procedural base supporting the AI-powered Surgical Monitor Market is still broadening.[1]Dan Zabinski and Alexandra Harris, “Ambulatory Surgical Center Services, Status Report,” MedPAC, medpac.gov A January 2026 study in Frontiers in Surgery found that AI-assisted object detection increased the share of surgeons identifying critical lymph nodes within 2 seconds from 4.67% to 42.99%, which links screen-based AI support to measurable intraoperative performance. That type of outcome linkage is making procurement discussions more clinical and less equipment-centered, which supports faster replacement decisions in academic hospitals and advanced surgical centers. As a result, the AI-powered Surgical Monitor Market is gaining from both rising case volumes and growing belief that visualization quality can directly affect surgical consistency.

Embedded AI for Intraoperative Detection and Workflow Automation

The AI-powered Surgical Monitor Market is also moving forward because embedded AI has shifted from single-task experiments toward multi-task systems that can run at clinically usable speeds during live surgery. In October 2025, Frontiers in Oncology reported that the Intelligent Surgical Assistant for laparoscopic liver surgery reached 89% instrument and organ recognition accuracy at 19.2 fps and delivered an AP50 of 95.2% on an external validation cohort, which supports the move toward real-time on-screen assistance.[2]L. Li, Bin Xuan, Xin Song, Yu Tian, Xiangcai Meng, Jiexia Wen, Tao Zheng, Chenglin Liu, and Yimin Wang, “AI-Assisted Surgical Vision, Evaluating YOLOv8 and YOLOv12 for Real-Time Detection in Colon Cancer Surgery,” Frontiers in Surgery, frontiersin.org This matters for the AI-powered Surgical Monitor Market because edge-based compute reduces dependence on cloud bandwidth, which allows hospitals to adopt advanced display systems without waiting for a full IT overhaul. The monitor is therefore becoming a compute endpoint as well as a display surface, and that is changing how hospitals define technical specifications. Procurement teams are beginning to ask for support for overlay execution, data handling, and software extensibility, in addition to conventional display measures. That shift raises the long-term value of platforms that can host future algorithms, which strengthens the commercial position of vendors with scalable hardware and software architectures.

ASC Migration Lifts Demand for Compact Visualization Suites

The AI-powered Surgical Monitor Market is seeing new demand from outpatient care because ambulatory surgical centers are taking on more complex orthopedic, spinal, and urologic procedures. MedPAC’s January 2026 update showed that CMS applied a 2.6% base payment rate increase for 2026, which improves the funding backdrop for equipment investment in the ASC channel. This shift matters for the AI-powered Surgical Monitor Market because ASCs usually operate with tighter room footprints, lower power flexibility, and faster turnover expectations than hospitals. Vendors that can package professional visualization and AI functions into compact, software-defined systems are better aligned with this channel than those relying on large integrated tower configurations. Caresyntax and Pristine Surgical announced a partnership in March 2025 to connect surgical intelligence tools with Pristine’s Summit 4K single-use digital arthroscope and Pristine Connect cloud platform for orthopedic ASC workflows, which shows that suppliers are already building outpatient-focused data and imaging pathways.[3]Caresyntax, “Caresyntax and Pristine Surgical Announce Partnership to Advance Surgical Intelligence,” Caresyntax, caresyntax.com As procedure migration continues, the AI-powered Surgical Monitor Market is likely to see stronger unit demand from facilities that need compact systems, faster setup, and lower integration burden.

Regulatory Legitimization of Real-Time AI Video Augmentation

The AI-powered Surgical Monitor Market is gaining credibility because regulators are now defining clearer paths for real-time AI video augmentation products. Hypervision Surgical received FDA clearance for HYPERSNAP in July 2025 under a new product code for AI and machine learning-based real-time video augmentation in surgical imaging systems, which reduced regulatory ambiguity for later entrants in this product class. Proprio received its second FDA 510(k) clearance in April 2025 for an AI platform that provides real-time 3D intraoperative measurements without radiation-based imaging, which shows that regulators are accepting more advanced forms of intraoperative guidance. In Europe, KARL STORZ secured CE certification for Innersight3D in July 2025, while in Japan NEDO demonstrated a surgical vision-language model during live gastric cancer surgery at Keio University Hospital in February 2026, which shows that commercial and clinical validation is broadening across the major regulatory regions. Clearer regulatory precedent is lowering the perceived risk of future product launches, and this is improving confidence among manufacturers, hospitals, and investors. That environment supports the AI-powered Surgical Monitor Market because hospitals are more willing to buy AI-ready hardware when the software roadmap has a visible route to clearance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost and Complex OR Integration | -1.3% | Global, with acute pressure in cost-constrained systems in South and Southeast Asia and the Middle East and Africa | Medium term (2-4 years) |

| Legacy Interoperability Across Towers and Video Protocols | -0.8% | Global, most severe in North America and Europe because of the large legacy base | Medium term (2-4 years) |

| Liability and Reimbursement Ambiguity for AI-Guided Decisions | -0.6% | North America and Europe, with growing concern in Japan and South Korea | Long term (≥ 4 years) |

| OR Video Governance and Cybersecurity Burden | -0.5% | Global, with the highest compliance burden in the United States and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Complex OR Integration

The AI-powered Surgical Monitor Market still faces slower conversion in many health systems because a fully integrated visualization suite with AI compute and OR connectivity can carry a very high upfront cost. This challenge is amplified when hybrid operating rooms require support for multiple imaging modalities, robotics feeds, and routing systems inside one environment. A July 2025 paper in Frontiers in Digital Health found that 75% of surveyed medical device manufacturers cited inadequate human-machine interface requirements in current interoperability standards, while 87.5% would not share risk-management documentation with unknown network participants, which shows how governance and liability concerns add to technical complexity. The result is that the AI-powered Surgical Monitor Market does not operate like a simple replacement market, because large systems often come with long service obligations and lengthy committee review. Vendors need stronger proof on operating efficiency, complication reduction, or total episode economics to displace installed platforms. Until that proof becomes more consistent across procedures and health systems, capital discipline will continue to slow adoption in facilities with stretched budgets.

OR Video Governance and Cybersecurity Burden

The AI-powered Surgical Monitor Market is also constrained by the expanding compliance burden that follows intraoperative video capture, AI processing, and data movement across surgical networks. Once patient-linked video enters routine workflow, hospitals must manage retention, access control, pseudonymization, and incident response under frameworks such as HIPAA, GDPR, and device cybersecurity guidance. This burden is greater for the AI-powered Surgical Monitor Market than for conventional surgical displays because AI-enabled systems often introduce software layers, connected compute, and broader data exchange across the operating room. KARL STORZ stated in November 2024 that its IMAGE1 S surgical video system received the highest cybersecurity certification available to medical devices, which shows that security posture is becoming a visible competitive differentiator and not only a compliance obligation. Hospitals with limited IT security staffing may delay upgrades even when clinical interest is high, because the post-purchase governance work extends far beyond installation. This means the AI-powered Surgical Monitor Market must advance alongside hospital cybersecurity maturity, not only alongside clinical demand for better visualization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integrated Platforms Anchor Revenue, OR Integration Displays Accelerate

Integrated AI Visualization Systems held 70.02% of the AI-powered Surgical Monitor Market size in 2025, which shows that hospitals still prefer consolidated architectures that reduce vendor coordination and centralize service obligations. In the AI-powered Surgical Monitor Market, these systems are favored because imaging management, AI processing, and multi-source routing can be delivered through a single platform rather than separate hardware layers. Olympus launched VISERA ELITE III in the United States in March 2026, and the platform combined True 4K and 3D imaging, Narrow Band Imaging, fluorescence-guided surgery in Magenta Mode, continuous auto-focus, and integration with Olympus VaultStream and LiveStream portals, which reflects how integrated systems are broadening their software role. The AI-powered Surgical Monitor Market continues to reward this format because procurement teams often view a unified stack as lower risk when surgical uptime and service accountability matter. The installed base in larger hospitals also supports integrated platforms because these facilities are more likely to run multi-specialty ORs that need a common imaging backbone.

AI-enabled OR Integration Display Platforms are forecast to grow at 16.05% CAGR through 2031, making them the fastest-expanding product category in the AI-powered surgical monitor industry because hybrid OR builds increasingly need one display fabric to handle multiple live data sources. In the AI-powered Surgical Monitor Market, this category is gaining because robotic feeds, navigation inputs, and imaging overlays must coexist without forcing separate screens and duplicate routing hardware. Standalone AI-enabled monitors still serve smaller ASCs and specialty clinics where full integration is too costly, and AI-guidance display platforms remain the frontier category where real-time overlays and robotic interfaces are most tightly linked. Across the AI-powered surgical monitor industry, baseline requirements such as IEC 60601 electrical safety and ISO 13485 quality management continue to shape vendor qualification before feature differentiation becomes relevant.

By Display Technology: LED Holds Installed-Base Share as OLED Gains in Fluorescence Applications

LED-backlit LCD panels accounted for 56.46% of revenue in 2025, which reflects the large installed base, lower acquisition cost, and broad compatibility that still shape the AI-powered Surgical Monitor Market. Many hospitals continue to rely on LED-backlit LCD systems because they fit existing video chains and meet everyday surgical needs without the premium pricing attached to newer emissive technologies. The AI-powered Surgical Monitor Market still gives LED an advantage in replacement cycles where facilities prioritize reliability, service familiarity, and budget discipline over top-end contrast performance. Even so, the technology ceiling of conventional LCD becomes more visible when AI overlays, fluorescence signals, and dark-field imaging are used in the same procedure. This is why the AI-powered Surgical Monitor Market is steadily creating room for premium tiers rather than removing the volume base of LED systems all at once.

OLED is projected to grow at 15.47% CAGR through 2031 because per-pixel light control supports fluorescence-guided surgery and tissue-oxygenation overlays that depend on strong contrast separation. Hypervision Surgical’s FDA-cleared HYPERSNAP system uses hyperspectral imaging with AI-powered analytics and operates at more than 60 fps, which underlines the type of demanding image environment that benefits from higher display fidelity. EIZO launched the CuratOR EX3245H in April 2026 with a Mini-LED backlight, more than 2,000 local dimming zones, a 1,000,000:1 contrast ratio, and IP45 front-panel protection, while LG introduced a 31.5-inch 4K Mini-LED surgical monitor in November 2025 with automated failover input switching and workflow presets, which together show how Mini-LED is being positioned as a practical bridge between standard LED and premium OLED in the AI-powered Surgical Monitor Market. As a result, the AI-powered Surgical Monitor Market is developing a three-tier technology ladder where LED retains scale, Mini-LED broadens mid-premium demand, and OLED addresses the most image-sensitive procedures.

By Resolution: Full HD Installed Base Faces Structured Displacement by 4K

Full HD held 42.57% of global demand in 2025, which shows that legacy minimally invasive towers still influence the AI-powered Surgical Monitor Market across community hospitals and smaller outpatient settings. Many facilities continue to operate Full HD because camera systems, recorders, and workflow habits were built around that standard and do not require immediate replacement for every procedure type. The AI-powered Surgical Monitor Market therefore still carries a large installed base that moves according to budget timing rather than purely according to technical superiority. Full HD remains relevant in entry-level endoscopy towers and lower-complexity use cases where image detail requirements are less demanding. That installed base keeps the transition orderly, but it also means the long-term shift toward higher resolution is already embedded in replacement planning.

4K Ultra HD is forecast to expand at 17.26% CAGR in AI-powered Surgical Monitor Market size through 2031 because robotic platforms and AI overlays perform better when native output and rendered anatomy are displayed with greater detail. In March 2026, Olympus said that a 2025 clinical survey found 8 out of 10 surgeons agreed that Yellow Enhancement on a 4K CMOS sensor-based system helped them identify vessels, nerves, and other critical structures within adipose tissue, which supports the practical case for higher-resolution viewing. The AI-powered Surgical Monitor Market is therefore moving toward 4K not only for visual sharpness but also because sub-4K rendering can limit the perceived value of real-time anatomical guidance. HD systems still occupy the low end, and 8K remains early in deployment for neurosurgery and exoscope settings where magnification and working distance create different demands. The AI-powered Surgical Monitor Market is likely to keep 4K as the main upgrade destination because it aligns clinical usability, hardware availability, and AI rendering needs better than either legacy HD or still-emerging 8K options.

By Application: Laparoscopy Anchors Volume, Endoscopy Surges on AI Detection Protocols

Laparoscopy represented 33.03% of total revenue in 2025, which shows that the AI-powered Surgical Monitor Market is still anchored by the global volume of general surgery, colorectal procedures, and upper gastrointestinal oncology. The application leads because laparoscopic surgery depends on a screen-mediated operative view, which makes monitor quality central to the surgeon’s ability to interpret anatomy and instrument position. In January 2026, Frontiers in Surgery reported that YOLOv12 achieved an accuracy of 0.867 for real-time object detection in colon cancer surgery at 333 fps, which supports the use of AI-enabled visualization in laparoscopic workflows. A January 2025 article in npj Digital Medicine also showed AI-assisted intra-abdominal metastasis recognition during laparoscopic gastric cancer surgery with 0.99 specificity, which adds further clinical support for the AI-powered Surgical Monitor Market in this application. These findings matter because purchasers are more willing to invest when display upgrades can be tied to better recognition, faster response, and more standardized procedure quality.

Endoscopy is forecast to grow at 19.54% CAGR through 2031, the fastest among applications in the AI-powered Surgical Monitor Market, because lesion detection tools have moved into routine hospital use in major countries. The application is benefiting from repeated refresh cycles as imaging systems and AI modules are upgraded together rather than in isolation. Robotic-assisted surgery, arthroscopy, and neurosurgery remain smaller by share, but they are high-value parts of the AI-powered Surgical Monitor Market because they demand more advanced overlays, more integration, and tighter image performance. An October 2025 paper in Annals of Coloproctology described the first AI-assisted augmented reality instrument de-occlusion during robotic-assisted right hemicolectomy, which shows how advanced visualization needs are expanding into robotic procedures as well. The result is a market where laparoscopic volume supports scale while endoscopy and robotics raise the technological ceiling.

By End User: Hospitals Drive Revenue, ASCs Drive Unit Momentum

Hospitals accounted for 62.18% of the AI-powered Surgical Monitor Market size in 2025 because they continue to dominate hybrid OR investment, robotic program deployment, and enterprise-scale digital infrastructure. In the AI-powered Surgical Monitor Market, hospitals also remain the main buyers of multi-source visualization platforms because they run larger surgical portfolios and have stronger demand for integrated imaging, documentation, and analytics. Academic medical centers add to this advantage because they are often early adopters of AI-supported workflow tools and advanced visualization modes. This makes hospitals the most important revenue base for suppliers selling higher-value systems with wider software capabilities. It also means the AI-powered Surgical Monitor Market still depends heavily on capital budgeting cycles within large health systems, even as lower-cost channels become more relevant.

Ambulatory surgical centers are projected to grow at 17.20% CAGR through 2031, which gives the AI-powered surgical monitor industry its strongest unit-growth channel as more complex procedures move outside inpatient settings. MedPAC reported 6.4 million ASC procedures across 6,436 U.S. facilities in 2024 and noted the 2026 payment update from CMS, which confirms that the outpatient base remains supportive for incremental equipment spending. The AI-powered Surgical Monitor Market is responding with systems that fit tighter room layouts, faster turnover patterns, and lower integration complexity than hospital-first platforms. Specialty clinics remain smaller, but they offer targeted opportunities for single-application systems in fields such as ophthalmology and ENT where the AI-powered surgical monitor industry can deploy focused configurations without the full multi-modality burden of hospital procurement.

Geography Analysis

North America held 43.56% of the AI-powered Surgical Monitor Market share in 2025, which kept it as the largest regional contributor because it combines advanced robotic surgery infrastructure, a deep outpatient base, and early regulatory acceptance of intraoperative AI. The AI-powered Surgical Monitor Market in the region is supported by the FDA’s new product code for AI and machine learning based real-time video augmentation, first applied to Hypervision Surgical’s HYPERSNAP clearance in July 2025. MedPAC reported that the United States had 6,436 ASCs and 6.4 million ASC procedures in 2024, which reinforces the scale of the outpatient channel that can accelerate visualization upgrades. Canada adds demand through large hospital systems, although public procurement cycles can extend refresh timing. Mexico remains more concentrated in private hospital networks in major cities, which favors targeted premium deployments rather than broad national rollout.

Europe remains a major center for the AI-powered Surgical Monitor Market because robotic surgery volumes are high and regulatory compliance standards are strict enough to favor vendors with deeper quality and documentation infrastructure. Intuitive said in July 2025 that da Vinci 5 received CE Mark, and the company also reported that European da Vinci procedures grew 21% in 2025 and exceeded 1.1 million, which indicates strong regional procedure depth for high-end visualization demand. KARL STORZ stated in November 2025 that its OR1 platform was installed in more than 12,000 ORs globally and that the company was advancing SurgicalAIHubGermany with research partners, which shows how established European vendors are deepening software capabilities around a large installed base. The AI-powered Surgical Monitor Market in the region, therefore, combines strong clinical demand with a compliance environment that raises entry barriers and supports consolidation around experienced vendors.

Asia-Pacific is projected to expand at 17.89% CAGR in the AI-powered Surgical Monitor Market size through 2031, making it the fastest-growing regional arena as Japan, China, South Korea, and India move along different but complementary adoption paths. The AI-powered Surgical Monitor Market in Japan is benefiting from PMDA-backed momentum for intraoperative AI and from clinical demonstrations that show these tools can operate in live surgical settings. NEDO announced in March 2026 that it had developed a surgery-focused generative AI system and demonstrated clinical-grade intraoperative dialogue performance during live gastric cancer surgery at Keio University Hospital, which strengthens Japan’s role as a reference market for AI-supported surgical visualization. Medtronic launched the Touch Surgery ecosystem in Japan in April 2026 for use with the Hugo robotic platform and conventional laparoscopic setups, which signals that suppliers are treating Japan as an important commercialization base for AI-enabled surgical video workflows. China adds scale through hospital modernization and demand for 4K imaging in tier-1 networks, while India contributes through corporate hospital expansion and partnership-led technology adoption. South Korea adds another layer of growth because its domestic robotics ecosystem creates demand for compatible visualization and overlay systems across newer surgical platforms.

Competitive Landscape

The AI-powered Surgical Monitor Market is defined by three broad groups, integrated surgical platform vendors, specialist display manufacturers, and AI-focused software companies that sit on top of hardware ecosystems. This structure keeps the AI-powered Surgical Monitor Market competitive because no single player controls every layer of the workflow from optics to display to analytics. KARL STORZ and Olympus remain central in the installed base through proprietary imaging ecosystems and operating room relationships, while Intuitive influences the surrounding visualization stack through robotic platform adoption and software-linked workflow expectations. In March 2026, Olympus launched VISERA ELITE III in the United States with 4K and 3D imaging, NBI, fluorescence-guided surgery, and digital workflow connectivity, which shows how established hardware players are defending their position by expanding the software and integration value of their systems. The AI-powered Surgical Monitor Market, therefore, rewards vendors that can hold customers through workflow continuity as much as through panel performance alone.

Display-focused companies still play a meaningful role because the AI-powered Surgical Monitor Market requires specialized brightness, contrast, durability, failover behavior, and compliance support that consumer display makers do not usually address. EIZO’s April 2026 launch of the CuratOR EX3245H and LG’s November 2025 launch of a 31.5-inch 4K Mini-LED surgical monitor show how display specialists are pushing into higher-value image environments with stronger local dimming, ingress protection, and workflow features. These companies compete by improving the visual substrate that AI overlays and robotic video depend on, even when they do not own the full imaging chain. That keeps the AI-powered Surgical Monitor Market open to suppliers that can differentiate on display engineering without replicating an endoscopy or robotics portfolio.

AI-native vendors are adding pressure from another direction because the AI-powered Surgical Monitor Market increasingly values analytics, overlay accuracy, and workflow automation rather than only screen specifications. Hypervision Surgical’s July 2025 FDA clearance for HYPERSNAP and Proprio’s April 2025 FDA clearance for real-time 3D intraoperative measurements show that newer entrants can gain credibility when they solve a specific clinical problem with regulatory support. Caresyntax’s March 2025 partnership with Pristine Surgical also shows that software-led vendors are trying to build data pathways in outpatient environments where incumbents are less entrenched. The AI-powered Surgical Monitor Market is therefore competitive at both the platform level and the software layer, and that makes interoperability, regulatory execution, and clinical validation decisive competitive tools. Vendors that can combine installed-base access with proof of workflow value are likely to sustain the strongest positions as the market matures.

AI-powered Surgical Monitor Industry Leaders

CONMED Corporation

Getinge AB

Intuitive Surgical, Inc.

Olympus Corporation

Intuitive Surgical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hypervision Surgical raised GBP17 million in a Series A funding round co-led by IP Group plc to accelerate commercial deployment of its HYPERSNAP hyperspectral AI surgical system following FDA 510(k) clearance in July 2025 and UK CE certification. The funding will expand clinical adoption in the United States, the United Kingdom, and Europe, building on over 170 procedures completed across three NHS trusts, and will advance next-generation hyperspectral sensing technology integration across open, minimally invasive, robotic, and microscopic surgical platforms.

- March 2026: Olympus launched its VISERA ELITE III surgical imaging platform in the United States through the Sony-Olympus Medical joint venture. The platform integrates True 4K and 3D imaging, NBI technology, Yellow Enhancement, Fluorescence-Guided Surgery in full 4K, and software-scalable feature activation in a single system with EHR and IT integration via the Olympus VaultStream and LiveStream portals.

- December 2025: Medtronic received FDA 510(k) clearance for its Hugo robotic-assisted surgery system for urologic procedures in the United States, integrating the Touch Surgery digital ecosystem for AI-powered post-operative case insights and remote tele-proctoring. The system addresses approximately 230,000 annual U.S. urologic procedures, including prostatectomy, nephrectomy, and cystectomy.

- September 2025: Intuitive Surgical introduced real-time surgical insight capabilities for da Vinci 5, including Force Gauge (tissue force visualization at 0–6.5 Newton resolution), in-console video replay, and Network CCM for remote software updates, all receiving FDA 510(k) clearance. The da Vinci 5 platform records over 10,000 times the computing power of da Vinci Xi, supporting sequential software releases.

Global AI-powered Surgical Monitor Market Report Scope

The AI-powered Surgical Monitor Market refers to the medical technology sector encompassing high-resolution displays, software platforms, and video analytics equipped with machine learning and computer vision. These systems assist surgeons and operating room (OR) staff by analyzing surgical data, vital signs, and video feeds in real-time.

The AI-powered Surgical Monitor Market is Segmented by Product Type (Standalone, Integrated Visualization, OR Integration, AI-guidance), Display (LED LCD, OLED, Mini-LED/MicroLED), Resolution (HD, Full HD, 4K, 8K), Application (Laparoscopy, Endoscopy, Arthroscopy, ENT, Neurosurgery, Orthopedic, CV Surgery, Robotic), End User (Hospitals, ASCs, Clinics), and Geography (North America, Europe, APAC, MEA, South America). Value in USD.

| AI-enabled Standalone Surgical Monitors |

| Integrated AI Visualization Systems |

| AI-enabled OR Integration Display Platforms |

| AI-guidance Display Platforms |

| LED-backlit LCD |

| OLED |

| Mini-LED and MicroLED |

| HD |

| Full HD |

| 4K Ultra HD |

| 8K Ultra HD |

| Laparoscopy |

| Endoscopy |

| Arthroscopy |

| ENT Surgery |

| Neurosurgery |

| Orthopedic Surgery |

| Cardiovascular Surgery |

| Robotic-assisted Surgery |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | AI-enabled Standalone Surgical Monitors | |

| Integrated AI Visualization Systems | ||

| AI-enabled OR Integration Display Platforms | ||

| AI-guidance Display Platforms | ||

| By Display Technology | LED-backlit LCD | |

| OLED | ||

| Mini-LED and MicroLED | ||

| By Resolution | HD | |

| Full HD | ||

| 4K Ultra HD | ||

| 8K Ultra HD | ||

| By Application | Laparoscopy | |

| Endoscopy | ||

| Arthroscopy | ||

| ENT Surgery | ||

| Neurosurgery | ||

| Orthopedic Surgery | ||

| Cardiovascular Surgery | ||

| Robotic-assisted Surgery | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the AI-powered Surgical Monitor Market?

The AI-powered Surgical Monitor Market stands at USD 283.62 million in 2026 and is projected to reach USD 587.29 million by 2031, growing at a 15.7% CAGR over 2026-2031.

Which region leads demand for AI-powered surgical monitors?

North America led global revenue with a 43.56% share in 2025, supported by advanced robotic surgery infrastructure, FDA regulatory progress, and a large ASC base.

Which application is growing fastest in AI-powered surgical monitors?

Endoscopy is the fastest-growing application with a 19.54% CAGR through 2031, driven by the wider clinical use of AI-assisted lesion detection and image-guided workflows.

Why are hospitals still the main buyers of AI-powered surgical monitors?

Hospitals held 62.18% of demand in 2025 because they invest more heavily in hybrid ORs, robotic programs, enterprise imaging systems, and multi-source visualization platforms.

What technology shift is shaping display upgrades in surgical visualization?

The market is moving from legacy LED-backlit LCD systems toward Mini-LED and OLED options, while 4K Ultra HD is becoming the main upgrade path because it better supports robotic output and AI overlays.

Page last updated on: