AI Osteoporosis Screening Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

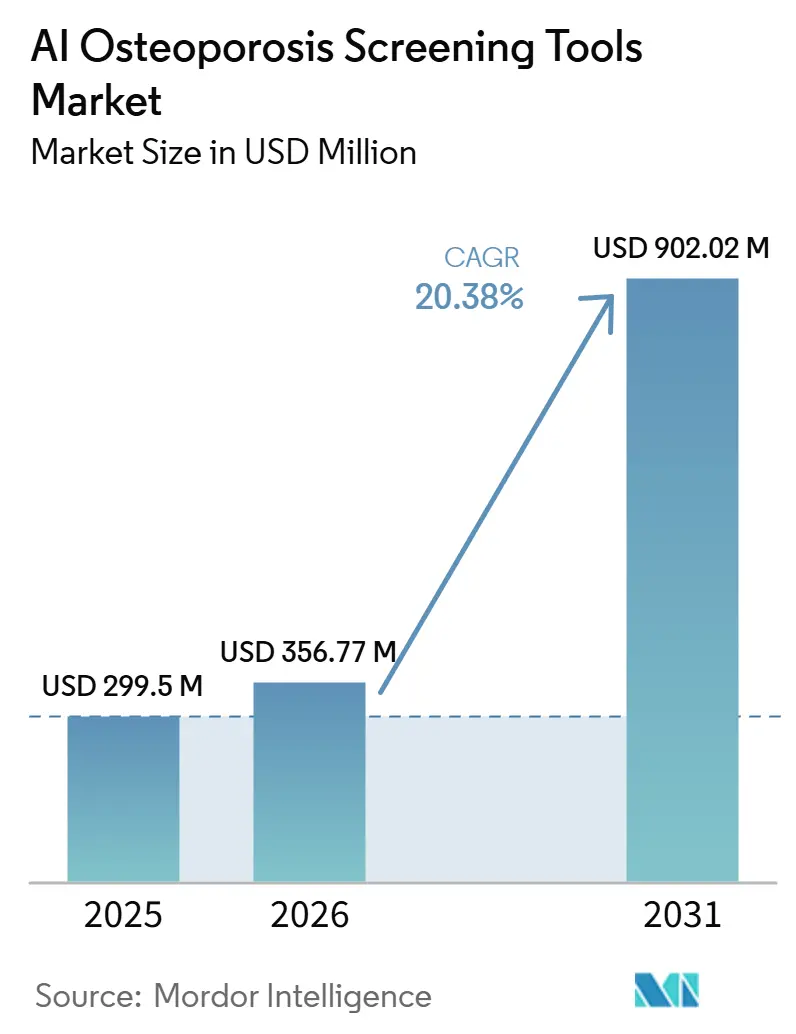

| Market Size (2026) | USD 356.77 Million |

| Market Size (2031) | USD 902.02 Million |

| Growth Rate (2026 - 2031) | 20.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Osteoporosis Screening Tools Market Analysis by Mordor Intelligence

The AI Osteoporosis Screening Tools Market size was valued at USD 299.5 million in 2025 and is estimated to grow from USD 356.77 million in 2026 to reach USD 902.02 million by 2031, at a CAGR of 20.38% during the forecast period (2026-2031).

More than 500 million people globally live with osteoporosis, and up to 80% of people who sustain fragility fractures still remain undiagnosed and untreated for the underlying condition, which keeps the AI osteoporosis screening tools market tied to a persistent care gap rather than a short demand cycle. Fragility fractures in adults older than 55 exceed 37 million each year worldwide, and hip fracture incidence is expected to rise sharply by 2050 as populations age, which supports long-duration demand for earlier screening and prevention in the AI osteoporosis screening tools market. Vendors in the AI osteoporosis screening tools market are gaining traction because their software can pull bone health signals from scans that health systems already perform, which helps facilities expand case finding without adding new imaging sessions or extra patient burden. Policy and data infrastructure are also improving the case for adoption, because the CMS TEAM model now links bone health optimization to episode-level accountability in U.S. hospitals, while the ONC HTI-5 proposed rule supports wider FHIR-based interoperability for clinical software. The main limits on the AI osteoporosis screening tools market remain reimbursement uncertainty, added regulatory documentation for adaptive software, and clinician caution around explainability and liability, so adoption will keep depending on how well vendors fit into real care pathways rather than on technical performance alone.

Key Report Takeaways

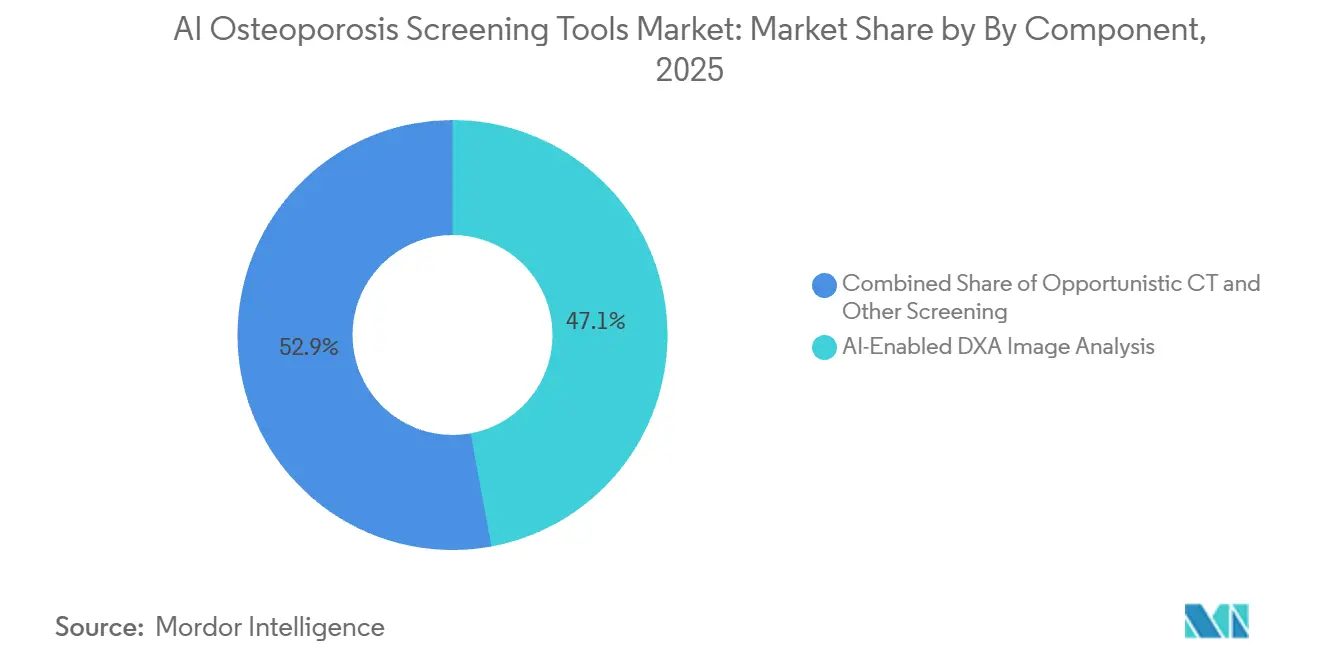

By technology, AI-Enabled DXA Image Analysis led with 47.1% revenue share in 2025, while Opportunistic CT and X-Ray AI Screening is forecast to expand at a 21.4% CAGR through 2031.

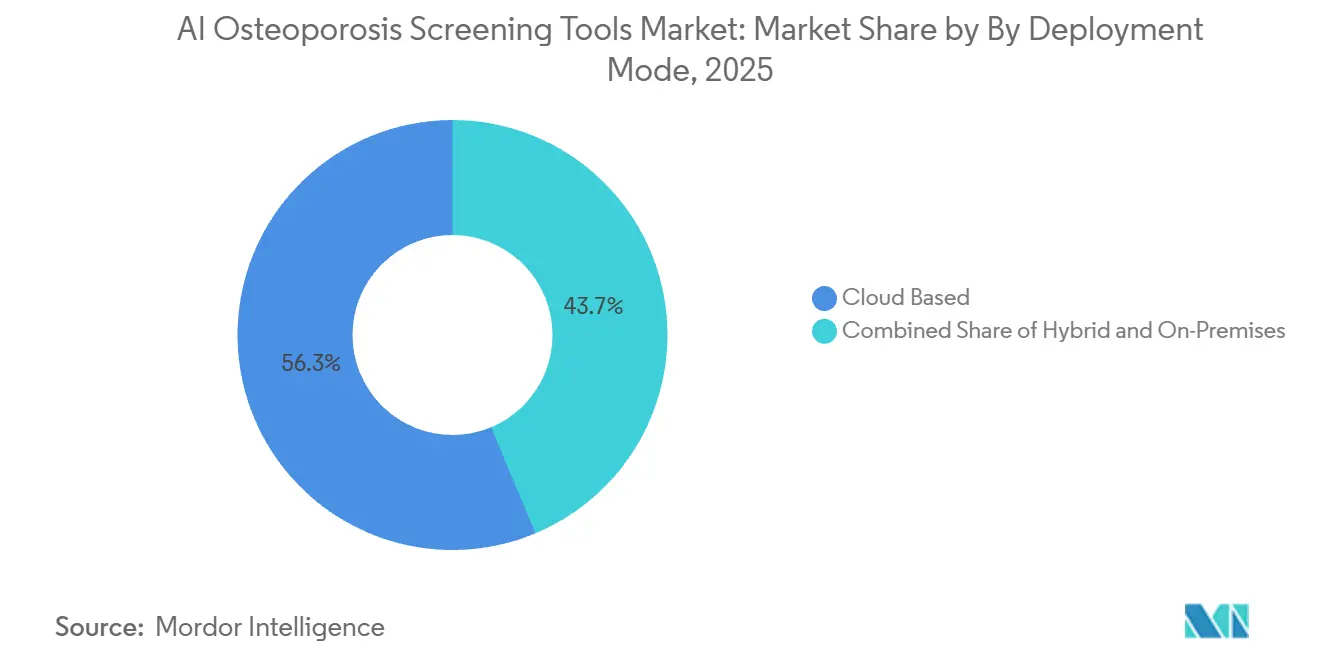

By deployment mode, Cloud-based deployment held 56.3% of revenue in 2025 and also recorded the highest projected CAGR at 22.3% through 2031.

By end user, Hospitals and diagnostic centers accounted for 43.2% of revenue in 2025, while Primary care networks recorded the highest projected CAGR at 20.9% through 2031.

By monetization model, Subscription-based pricing represented 52.1% of revenue in 2025, while Per-scan and usage-based pricing is projected to grow the fastest at a 20.9% CAGR through 2031.

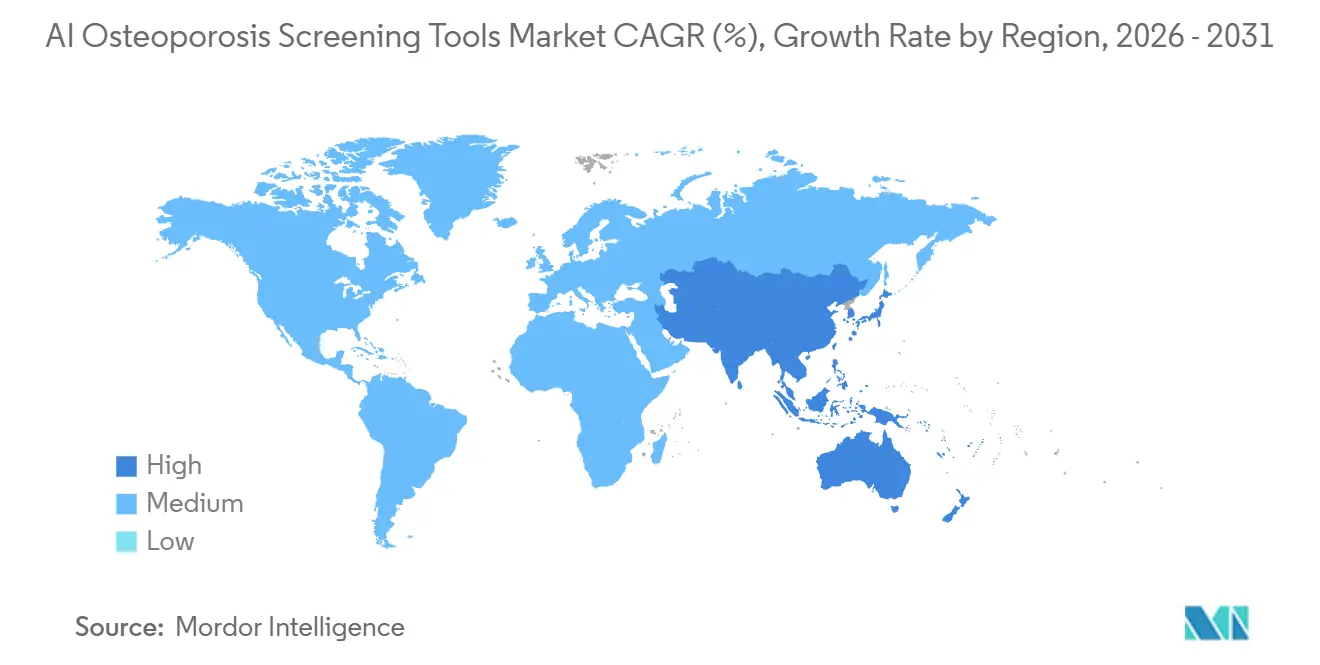

By geography, North America held 45.1% of revenue in 2025, while Asia Pacific is forecast to register the fastest CAGR at 22.1% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Osteoporosis Screening Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Osteoporosis Prevalence And Undiagnosed Burden | +5.2% | Global, highest urgency in Asia Pacific, Europe, and North America | Long term (≥ 4 years) |

| Expansion Of Opportunistic Screening From Existing Imaging Data | +5.8% | North America and Europe, with early gains in East Asia and Germany | Medium term (2-4 years) |

| AI Automation Reduces Radiologist And Technologist Workload | +3.5% | Global, with earliest concentration in North America and Western Europe | Short term (≤ 2 years) |

| Value-Based Care Incentives For Earlier Risk Stratification | +2.9% | North America, with spillover potential into Asia Pacific public systems | Medium term (2-4 years) |

| Cloud And EHR Integrated Deployment Improves Workflow Adoption | +2.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Under-Screened Primary Care Populations Offer Expansion | +2.5% | Asia Pacific core, with spillover into South America, MEA, and rural North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Osteoporosis Prevalence and Undiagnosed Burden

The AI osteoporosis screening tools market draws steady support from the scale of untreated bone disease across both developed and emerging care systems. The International Osteoporosis Foundation[1]International Osteoporosis Foundation, “On World Osteoporosis Day, Experts Warn of Growing Burden of Fragility Fractures,” IOF stated in 2025 that more than 500 million people live with osteoporosis worldwide, and only 1 in 5 fracture patients receives a diagnosis or appropriate therapy in many high-income settings. The shortfall is not limited to women, because real-world evidence from Rho showed that AI-prompted DXA referrals identified higher rates of true low bone mineral density in older men than conventional referral practice did, which points to a hidden pool of missed cases in the AI osteoporosis screening tools market. This matters because software that works without a clinician first ordering a dedicated bone exam can convert long-standing referral blind spots into routine screening opportunities inside ordinary imaging pathways. Long-range burden projections also remain severe, with Osteoporosis International projecting 397,537 deaths and 14,350,582 disability-adjusted life years among post-menopausal women from low bone mineral density-related fractures by 2050, which supports a long tail of need for prevention-oriented tools.

Expansion of Opportunistic Screening from Existing Imaging Data

The AI osteoporosis screening tools market is also benefiting from a clear shift toward opportunistic screening, where existing scans are reused to detect bone loss without adding new appointments. A 2025 multicenter cohort study reported that deep learning models applied to chest low-dose CT and lumbar CT delivered high diagnostic accuracy for osteoporosis across scanners from multiple manufacturers, which helps buyers trust wider deployment across mixed imaging fleets. Health systems also gain a practical advantage because opportunistic screening uses imaging that is already part of routine care, which lowers patient friction, avoids added radiation from separate exams, and cuts the need for dedicated screening slots. Economic findings strengthen the case, because studies in Germany, the United States, and Japan each concluded that AI-assisted opportunistic screening can be cost-effective in their respective settings. As a result, the AI osteoporosis screening tools market is moving beyond a narrow radiology software category and toward a broader role in population health detection and fracture prevention workflows.

AI Automation Reduces Radiologist and Technologist Workload

The AI osteoporosis screening tools market is gaining support because automation improves throughput without asking radiologists to give up clinical control. Canadian deployments of Rho processed more than 50,000 patients in routine care and nearly doubled initial bone health assessments, while radiologists still retained the option to include AI findings in their reports. That workflow change matters because it shifts case finding from a specialist referral step to background processing inside imaging systems, which reduces the chance that osteoporosis risk will be missed simply because no one initiated a formal bone workup. In lower-capacity settings, this kind of automation is not only an efficiency gain, but it is also often the only realistic way to expand screening at scale. Equipment-linked offerings such as syngo Osteo CT and Bone Health powered by enCORE also show how the AI osteoporosis screening tools market is embedding itself into installed imaging workflows rather than asking hospitals to build a separate operating model from scratch.

Value-Based Care Incentives for Earlier Risk Stratification

The AI osteoporosis screening tools market is also being pushed forward by payment models that reward earlier detection instead of later fracture treatment. The CMS TEAM model is in force from January 2026 and covers around 700 acute care U.S. hospitals across episode-based payment bundles, including spinal fusion and surgical hip and femur fracture treatment, where unrecognized osteopenia or osteoporosis can materially affect outcomes and costs. The Bone Health and Osteoporosis Foundation has also urged CMS to incorporate bone health assessment into joint replacement payment design, citing evidence that more than half of hip replacement patients have underlying osteoporosis or low bone mass. This changes the buyer logic in the AI osteoporosis screening tools market because hospital finance teams and care management leaders now have a reason to view screening software as a way to control episode risk, not just as a diagnostic add-on for radiology. Once bone health enters quality and payment accountability, procurement decisions are more likely to move from isolated department budgets toward broader institutional approval.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Clearance Burden For Clinical AI | -1.8% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Interoperability And Data Governance Constraints | -1.3% | Global, especially fragmented EHR environments in Asia Pacific and South America | Medium term (2-4 years) |

| Limited Reimbursement Visibility For AI-Assisted Screening | -2.2% | North America and Europe, with greater severity in MEA and South America | Long term (≥ 4 years) |

| Clinician Trust, Explainability, And Liability Concerns | -1.4% | Global, strongest in primary care settings and lower-resource systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement Visibility for AI-Assisted Screening

Reimbursement remains the most persistent commercial barrier in the AI osteoporosis screening tools market because many facilities still cannot match clinical value with a predictable payment path. Most vendors still rely on facility billing arrangements or per-read economics that are not standardized across payers, which makes revenue planning difficult for providers that want to deploy these tools at scale. The Bone Health and Osteoporosis Foundation stated in its 2024 CMS submission that existing code sets, including changes introduced through the 2025 Physician Fee Schedule, do not capture the coordination costs of fracture prevention and collaborative care programs. Europe faces a similar challenge, because the International Osteoporosis Foundation and Medimaps noted in 2025 that only 1 in 5 fracture patients across the European Union receives diagnosis or therapy, which shows how weak reimbursement and care coordination can limit screening uptake even when clinical need is high. Until payers treat preventive screening and follow-up as a recognized care pathway, the AI osteoporosis screening tools market will continue to face slower rollouts than its technical capabilities might suggest.

Clinician Trust, Explainability, and Liability Concerns

Clinician caution still slows the AI osteoporosis screening tools market, especially when software is expected to influence diagnosis, referral, or treatment decisions in routine care. A 2026 Asia Pacific consensus statement warned that unvalidated AI tools can misclassify patients and recommended that AI support clinical risk assessment rather than act as a standalone diagnostic decision maker. The same document also noted that models trained mostly on Western imaging datasets may underperform in Asia Pacific populations, which makes local validation important before broad use. Liability is another brake because radiologists or clinicians may still feel responsible for acknowledging or rejecting AI findings, even after a tool has regulatory clearance. That dynamic can reduce actual report inclusion and weaken the measurable clinical impact that vendors in the AI osteoporosis screening tools market need to show procurement teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: DXA Integration Anchors Revenue, CT Screening Accelerates Share Capture

AI-Enabled DXA Image Analysis held 47.1% of AI osteoporosis screening tools market share in 2025, which kept it as the largest technology segment because DXA remains the established reference workflow for bone mineral density measurement in clinical practice. Medimaps[2]Medimaps Group S.A., “Medimaps Breaks New Ground in Fracture Risk Assessment with FDA Clearance and MDR Certification for TBS Osteo Next Generation Software,” Medimaps stated in January 2025 that TBS Osteo Advanced is the only approved medical device software for bone microarchitecture evaluation in clinical settings, is used in more than 4 million procedures each year, and is referenced by more than 30 international clinical guidelines, which shows why DXA-linked software still anchors commercial revenue in the AI osteoporosis screening tools market. This segment benefits from an existing reimbursement structure around DXA, especially in North America, which makes buyer justification more straightforward than it is for newer opportunistic tools. It also fits cleanly into familiar radiology and metabolic bone disease workflows, so hospitals can add value without redesigning how core bone testing is already performed.

Opportunistic CT and X-Ray AI Screening is projected to be the fastest-expanding part of the AI osteoporosis screening tools market size at a 21.4% CAGR through 2031, because it can monetize imaging capacity that health systems already own. The April 2024 FDA De Novo authorization for Rho created a clear regulatory precedent for opportunistic low bone mineral density assessment from standard X-rays, which reduced one of the biggest adoption barriers for this branch of the AI osteoporosis screening tools industry FDA. A 2026 study [3]Chen S.-H. et al., “Advancing Diagnostic Equity Through Artificial Intelligence Chest Radiograph Screening for Osteoporosis in Asian Populations,” npj Digital Medicine in a Taiwanese screening population reported an AUC of 0.95 for an AI model reading chest X-rays for abnormal bone mineral density, which supports the clinical case for wider population deployment when local validation is in place. Ultrasound-based AI screening remains relevant in portable and resource-limited settings, while other tools such as combined bone-muscle frailty approaches and AI-assisted fracture risk calculators are still earlier-stage contributors. In rural China, portable DXA programs are already being used to widen screening access, and AI interpretation layers are being added to help scale analysis where specialist infrastructure is limited.

By Deployment Mode: Cloud Leads on Both Share and Growth as Workflow Integration Deepens

Cloud-based deployment held 56.3% revenue share in 2025 and is also expected to post the fastest growth at 22.3% CAGR through 2031, which makes it the most commercially favored deployment model in the AI osteoporosis screening tools market. This lead reflects the practical needs of AI software, because vendors must manage updates, support multiple sites, and connect outputs back into clinical systems without asking each hospital to maintain a separate software stack. Rho uses FHIR-standard integration to pull relevant data from electronic health records and return findings into workflow, which illustrates why cloud delivery is becoming central for facilities that want the AI osteoporosis screening tools market to operate as part of routine care rather than as a stand-alone application. Medimaps also expanded the case for cloud-style central management in 2025 when it launched TBS Osteo Advanced with multi-site fleet management capabilities, showing how network-level standardization matters in larger health systems.

The cloud segment is also benefiting because it fits the way enterprise buyers now assess software, where ongoing model refinement and shared governance matter as much as the first installation. For multi-location imaging groups, centralized administration reduces the burden of local version control and keeps quality more consistent across sites. That matters in the AI osteoporosis screening tools market because detection accuracy, workflow timing, and clinician acceptance all depend on dependable deployment rather than on algorithm performance alone. Cloud delivery therefore supports the shift from pilot projects toward system-wide contracts.

By End User: Hospitals Anchor Volume While Primary Care Unlocks the Next Market Layer

Hospitals and diagnostic centers accounted for 43.2% of revenue in 2025, which kept them as the leading end-user group in the AI osteoporosis screening tools market because they concentrate DXA scanners, PACS environments, and specialist radiology workflows. These sites are the natural first buyers because current products often enter through imaging departments that already interpret bone density or fracture-related findings. Specialty orthopedic, endocrine, and imaging clinics remain relevant secondary users, especially for DXA augmentation software that fits existing specialist pathways. Research and academic institutions contribute a smaller direct revenue base, but they remain important because they generate validation studies and guideline support that later shape commercial acceptance.

This end-user pattern matters because it shows that the AI osteoporosis screening tools market still rests on settings where clinical governance, imaging expertise, and software review capacity are already established. Large hospitals also have the best ability to connect screening outputs with follow-up care, which helps them demonstrate value beyond a single image result. That gives hospital-led deployments a strong role in early revenue formation for the AI osteoporosis screening tools market. It also explains why many vendors first prove utility in tertiary or networked care settings before moving further into community channels.

Primary care networks are expected to grow the fastest at a 20.9% CAGR through 2031, reflecting a steady shift in the AI osteoporosis screening tools market toward earlier detection before a fracture occurs. Real-world Rho data showed that AI-prompted DXA referrals surfaced higher-risk male cohorts than standard referral practice, which shows how community-facing workflows can reach patients who are often missed in specialist-led pathways. The CMS TEAM model also encourages hospital systems to pull bone health surveillance further upstream, because fracture-related episode accountability makes earlier identification financially relevant to broader care teams. As that happens, software in the AI osteoporosis screening tools industry is likely to move from a narrow radiology aid toward a care coordination input that supports referral, prevention, and follow-up across the continuum. The next layer of growth therefore depends less on adding specialist capacity and more on bringing routine risk detection into settings where patients first enter the system.

By Monetization Model: Subscription Captures Incumbent Share While Per-Scan Pricing Opens High-Growth Market Tiers

Subscription-based pricing represented 52.1% of revenue in 2025, which made it the leading commercial model in the AI osteoporosis screening tools market because vendors want recurring income, ongoing update coverage, and closer institutional ties. Medimaps shifted TBS Osteo Advanced to a subscription model in 2025, bundling software updates, analytical improvements, and support into a recurring arrangement that suits high-volume DXA facilities and larger health systems. Subscription pricing works well where scan volume is stable, and procurement teams prefer a predictable operating model rather than repeated purchasing decisions. It also supports the economics of the AI osteoporosis screening tools market because model performance, integration quality, and regulatory documentation all require continuous maintenance rather than one-time delivery.

This model remains especially strong among established vendors that already serve enterprise or network customers with large installed imaging bases. Buyers in those settings often value long-term service continuity and centralized software governance more than short-term flexibility on unit pricing. That keeps subscription revenue as the main incumbent base in the AI osteoporosis screening tools market. It also aligns with the broader move toward cloud delivery, where ongoing software management is part of the value proposition.

Geography Analysis

North America held 45.1% of AI osteoporosis screening tools market share in 2025, which made it the largest regional contributor because it combines dense DXA infrastructure, a mature FDA software pathway, and stronger reimbursement foundations than most other regions. The U.S. now adds a sharper demand trigger through TEAM, because hospitals covered under episode-based accountability have a clearer reason to improve bone health detection before costly complications occur. The region also benefits from an active regulatory pipeline, with several vendors already using FDA clearance as a credibility signal when approaching broader provider networks. Canada adds meaningful real-world validation, because routine-care Rho deployments there processed more than 50,000 patients and showed that AI-supported referral pathways can surface under-screened high-risk groups.

Europe remains important for the AI osteoporosis screening tools market because disease burden is large, but commercialization still moves through structural limits in reimbursement and care coordination. The International Osteoporosis Foundation estimated that 32 million Europeans aged 50 and over have osteoporosis, and annual osteoporotic fractures across the European Union, Switzerland, and the UK are projected to reach 5.34 million by 2034. Germany stands out because local research found AI chest radiograph screening to be cost-effective, which gives the region a more practical economic case for broader opportunistic deployment. At the same time, the European route still depends heavily on MDR compliance, and Medimaps' dual U.S. and EU clearance path has become an important reference point for suppliers that want to sell across both regions.

Asia Pacific is set to post the fastest growth in the AI osteoporosis screening tools market size at 22.1% CAGR through 2031, driven by a large aging population, limited DXA access in many countries, and growing acceptance of AI as a practical screening extension. The 2025 APCO-IOF[4]Asia Pacific Consortium on Osteoporosis and International Osteoporosis Foundation, “APCO-IOF Asia Pacific Regional Audit,” IOFregional audit found that osteoporosis is a national health priority in only 6 audited Asia Pacific countries, which underscores how much unmet need remains across the region. Japan stands out because local research found AI-assisted opportunistic chest radiograph screening to be cost-effective for fracture prevention in older women, even though screening rates remain low. China also represents a strong access-driven opportunity, because portable DXA programs in rural areas are widening screening coverage and creating demand for AI interpretation layers that can compensate for limited specialist capacity. The Middle East and Africa and South America remain early-stage markets, where infrastructure gaps and limited reimbursement still slow adoption, even though later-period digital health investment should create selective openings for the AI osteoporosis screening tools market.

Competitive Landscape

The AI osteoporosis screening tools market is split between imaging and densitometry incumbents that add software layers to existing hardware relationships, and AI-first vendors that build opportunistic screening on top of scans already performed in routine care. Hologic remains one of the strongest incumbents in bone densitometry through its Horizon DXA platform, and its strategy of linking bone assessment to existing mammography patient pathways shows how established OEMs are using installed clinical touchpoints to expand screening reach. Medimaps occupies an important position in the DXA-linked software layer, where its TBS Osteo platform adds bone microarchitecture insight without asking providers to replace established DXA workflows. Its 2025 partnership with OsteoSys is a useful example of how the AI osteoporosis screening tools market is expanding through hardware-software alliances that open new geographies through a single installed base agreement. That type of partnership matters because it lets software vendors scale through established channel access while OEMs raise the value of their equipment footprint.

AI-first suppliers compete more on regulatory reach, workflow integration, and dataset breadth across populations and scanner types. Nanox.AI has built a differentiated position through HealthVCF and HealthOST, and the company received a NICE Early Value Assessment recommendation in 2025, which signaled growing institutional interest in AI-based vertebral fracture and bone loss detection from routine CT scans. Gleamer's BoneView represents another focused strategy, using broad X-ray deployment and published workflow performance to strengthen its role in bone trauma and vertebral fracture detection. These vendors are important because they are trying to widen the AI osteoporosis screening tools market beyond DXA and into the much larger volume of non-dedicated imaging. Their commercial advantage is strongest when hospitals want immediate case finding gains without buying new scanners.

A separate competitive cluster is emerging around Asian software providers with strong local deployment and multi-jurisdiction ambition. INFERVISION states that InferRead CT Fracture has gained authorizations across multiple regulatory systems and has been deployed in more than 1,000 hospitals in over 30 countries, which gives it scale credibility in cross-border imaging AI. Shukun Technology reports deep penetration across top Chinese hospitals and positions bone density assessment as one output within broader chest and musculoskeletal AI packages, which can strengthen procurement appeal where buyers prefer multi-function platforms. Overall, the AI osteoporosis screening tools market remains fragmented because no single company controls the full chain of hardware, clinical workflow, reimbursement fit, and opportunistic screening breadth. Competitive advantage therefore comes less from a single feature and more from how well a vendor combines regulatory clearance, installed access, clinician trust, and enterprise integration.

AI Osteoporosis Screening Tools Industry Leaders

Hologic, Inc.

GE HealthCare

Siemens Healthineers AG

Koninklijke Philips N.V.

Qure.ai Technologies Pvt. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Medimaps Group launched TBS Osteo Advanced in Europe with MDR clearance, confirming it as the only approved medical device software for bone microarchitecture evaluation in clinical practice in Europe. The product introduces centralized multi-site DXA fleet management, soft tissue correction across broader BMI ranges, and a BMD-plus-TBS composite report delivered within seconds of DXA scan completion.

- June 2025: Medimaps launched TBS Osteo Advanced in the United States, transitioning to a subscription pricing model. The next-generation software expands patient eligibility beyond standard BMI limits through direct tissue thickness assessment, and is available across the company's 90 global markets

- December 2024: FDA 510(k) cleared TBS iNsight V4 from Medimaps, enabling trabecular bone score computation from DXA anterior-posterior lumbar spine images as an adjunct to standard BMD measurement in osteoporosis and fragility fracture risk assessment

- April 2024: FDA granted De Novo marketing authorization for Rho, the first FDA-authorized radiology software for opportunistic evaluation of low bone mineral density from standard X-rays. Canadian clinical deployments subsequently processed over 50,000 patients with results showing AI-prompted DXA referrals outperforming conventional standard-of-care protocols in high-risk male cohorts.

Global AI Osteoporosis Screening Tools Market Report Scope

| AI-Enabled DXA Image Analysis |

| Opportunistic CT and X-Ray AI Screening |

| Ultrasound-Based AI Screening |

| Other AI Screening Tools |

| Cloud Based |

| Hybrid |

| On Premises |

| Hospitals and Diagnostic Centers |

| Specialty Orthopedic and Endocrine Clinics |

| Imaging Centers |

| Primary Care Networks |

| Research and Academic Institutions |

| By Monetization Model (Value) |

| Subscription |

| Perpetual License |

| Per-Scan and Usage Based |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| United States | |

| Canada | |

| Mexico | |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | AI-Enabled DXA Image Analysis | |

| Opportunistic CT and X-Ray AI Screening | ||

| Ultrasound-Based AI Screening | ||

| Other AI Screening Tools | ||

| By Deployment Mode | Cloud Based | |

| Hybrid | ||

| On Premises | ||

| By End User | Hospitals and Diagnostic Centers | |

| Specialty Orthopedic and Endocrine Clinics | ||

| Imaging Centers | ||

| Primary Care Networks | ||

| Research and Academic Institutions | ||

| By Monetization Model (Value) | ||

| Subscription | ||

| Perpetual License | ||

| Per-Scan and Usage Based | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| United States | ||

| Canada | ||

| Mexico | ||

| Germany | ||

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving adoption of AI tools for osteoporosis screening?

Adoption is being driven by a large undiagnosed patient pool, rising fracture burden, and the ability to extract bone health signals from scans that are already being performed. The market stands at USD 356.8 million in 2026 and is forecast to reach USD 902 million by 2031 at a 20.4% CAGR.

Why is opportunistic screening gaining so much attention?

Opportunistic screening uses routine CT or X-ray images instead of requiring a separate bone exam, which lowers patient burden and can improve case finding. This is why CT and X-ray AI screening is projected to grow at a 21.4% CAGR through 2031.

Which technology segment currently leads revenue?

AI-enabled DXA image analysis leads revenue with a 47.1% share in 2025, supported by established clinical use, existing reimbursement pathways, and strong fit with current bone density workflows.

Which deployment model is expanding the fastest?

Cloud-based deployment leads with a 56.3% share in 2025 and is also the fastest-growing model at a 22.3% CAGR, mainly because it supports easier updates, multisite management, and deeper EHR integration.

Which region offers the strongest growth outlook?

Asia Pacific offers the strongest growth outlook with a 22.1% CAGR through 2031, supported by large aging populations, limited DXA access in many countries, and rising acceptance of AI as a scalable screening tool.

What is the biggest commercial barrier for vendors?

Reimbursement remains the biggest barrier because many providers still lack a clear and standardized payment path for AI-assisted screening. That slows procurement even when the clinical need and technical value are clear.

Page last updated on: