AI-integrated Blood Analyzers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

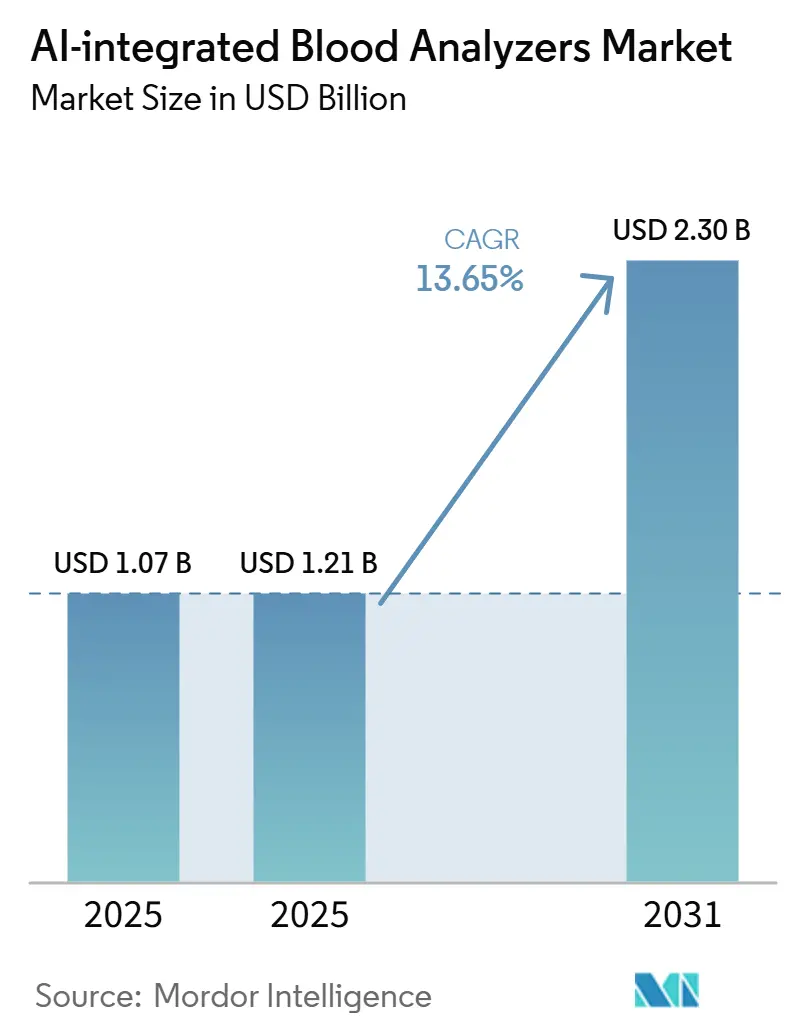

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 2.30 Billion |

| Growth Rate (2025 - 2031) | 13.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

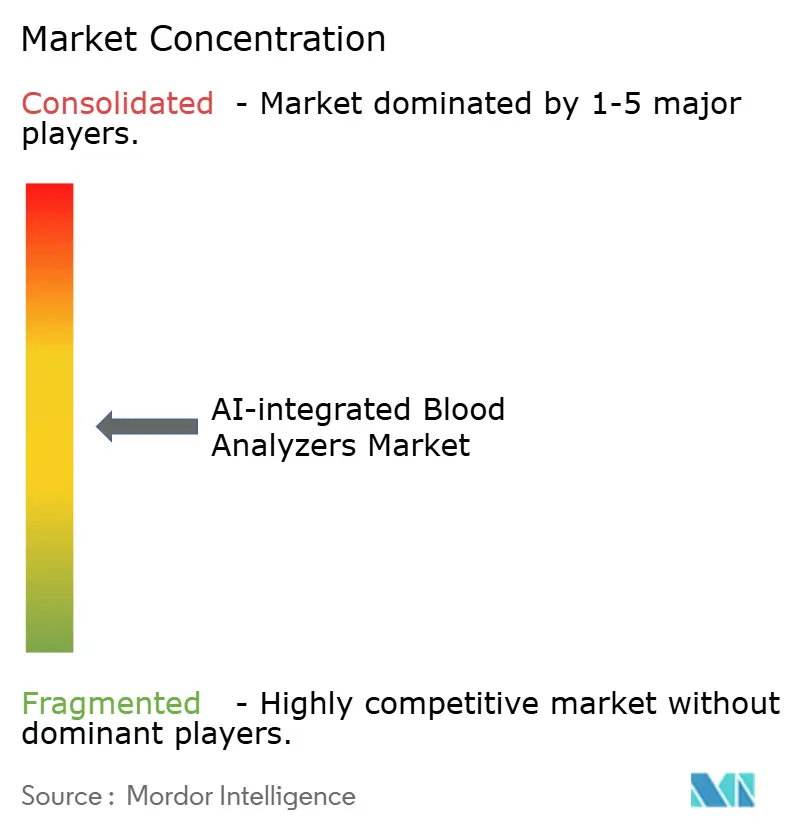

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-integrated Blood Analyzers Market Analysis by Mordor Intelligence

The AI-integrated Blood Analyzers Market size is expected to increase from USD 1.07 billion in 2025 to USD 1.21 billion in 2026 and reach USD 2.30 billion by 2031, growing at a CAGR of 13.65% over 2026-2031.

Persistent screening demand continues to support the AI-integrated blood analyzers market because the World Health Organization reported in 2025 that anemia among women of reproductive age remained at 30.7%, which keeps routine blood testing volumes high across many care settings.[1]World Health Organization, “WHO Global Anaemia Estimates: Key Findings, 2025,” World Health Organization, who.int The AI-integrated blood analyzers market is also expanding because laboratories are under pressure to process more complete blood count and morphology workloads with fewer trained reviewers, which makes automation and decision support more useful in day-to-day operations. Vendors in the AI-integrated blood analyzers market are responding by pairing analyzers with digital morphology review, workflow connectivity, and software upgrades, which helps them defend existing accounts and deepen recurring revenue streams. The strongest openings in the AI-integrated blood analyzers market are appearing in decentralized testing, remote review across multi-site laboratory networks, and software overlays that can be added to installed systems without replacing the full instrument base. Adoption in the AI-integrated blood analyzers market still moves unevenly because high capital cost, limited reimbursement for AI-specific functions, and strict validation expectations continue to slow purchasing in price-sensitive settings.

Key Report Takeaways

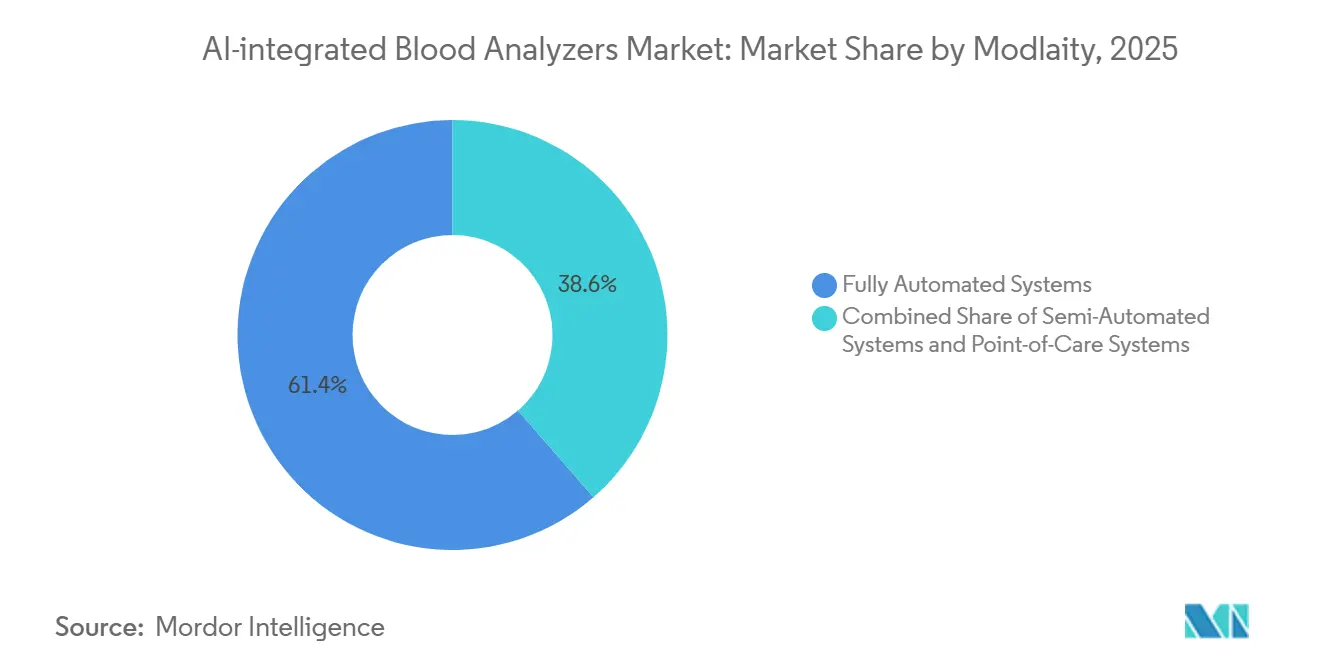

- By modality, Fully Automated Systems held 61.38% of revenue in 2025, while Point-of-Care Systems are projected to expand at a 16.63% CAGR through 2031.

- By product type, AI-integrated blood Analyzers accounted for 47.14% of revenue in 2025, while AI Blood Analysis Software is forecast to grow at a 17.16% CAGR through 2031.

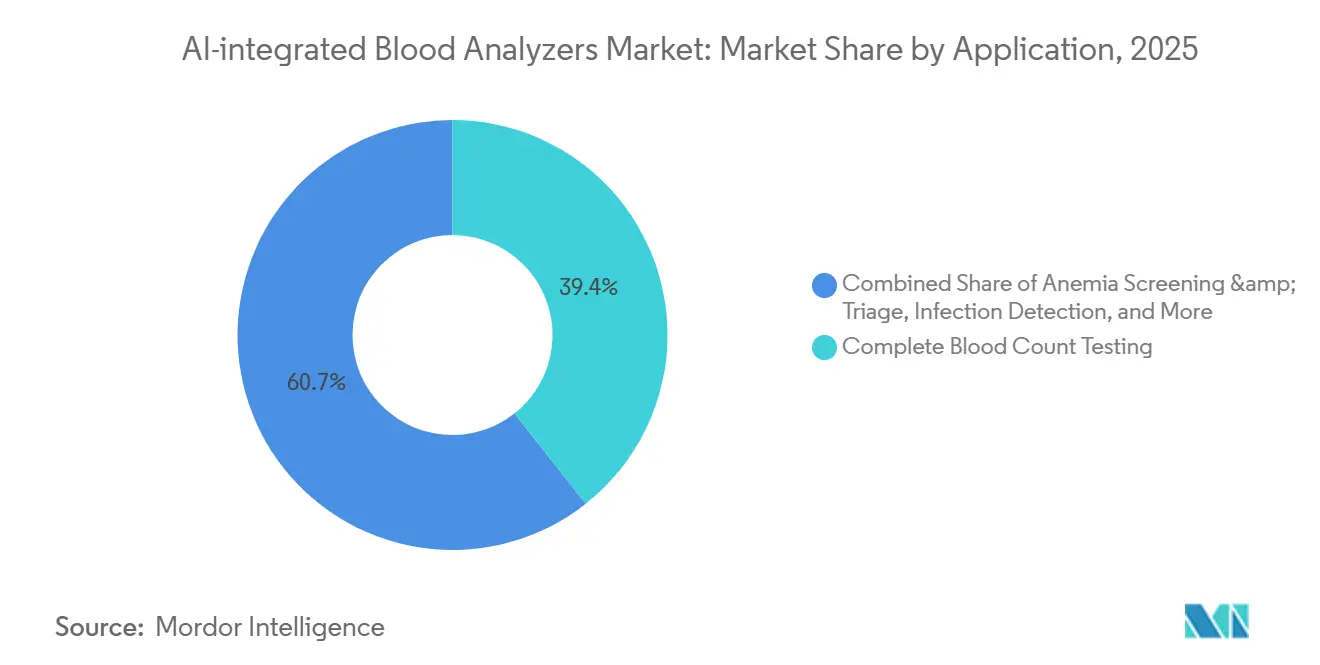

- By application, Complete Blood Count Testing represented 39.35% of revenue in 2025, while Blood Cancer Diagnostics is expected to record the fastest CAGR at 16.48% through 2031.

- By end user, Hospitals captured 46.43% of revenue in 2025, while Diagnostic Laboratories are projected to advance at a 14.88% CAGR through 2031.

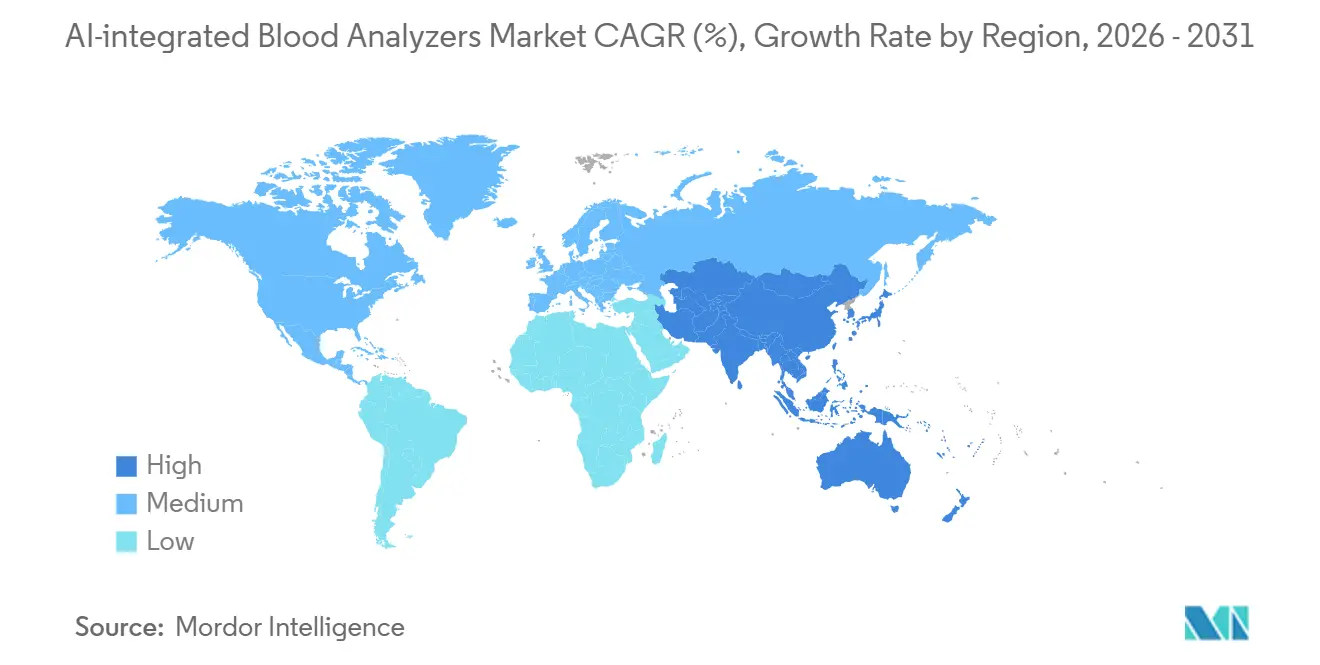

- By geography, North America held 42.36% of revenue in 2025, while Asia-Pacific is forecast to grow at a 15.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-integrated Blood Analyzers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for AI-Assisted Morphology Review | +3.2% | Global, concentrated in North America, Europe, and East Asia | Medium term (2-4 years) |

| Expansion of Fully Automated High-Throughput Labs | +2.5% | North America, Western Europe, APAC core including China, Japan, and South Korea | Short term (≤ 2 years) |

| Rising Blood Disorder Screening Volumes | +2.3% | Global, with highest pull in South Asia, Sub-Saharan Africa, and APAC | Long term (≥ 4 years) |

| Decentralized Testing Needs in Acute and Urgent Care | +2.1% | North America and APAC, with spillover to MEA and South America | Medium term (2-4 years) |

| Increasing LIS and Digital Workflow Integration | +1.8% | North America and Europe, with early adoption in APAC tier-1 cities | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for AI-Assisted Morphology Review

Manual peripheral blood smear review remains one of the slowest steps in laboratory hematology because it still depends heavily on trained staff and careful visual judgment. The user-supplied material notes that this step can take 10-20 minutes per slide under manual review, while AI-assisted morphology platforms can cut that to under 5 minutes in suitable workflows. The same source reported that the CellaVision DM series delivered a 50% reduction in total smear analysis time with 92% preclassification accuracy, and the Sysmex DI-60 reduced hands-on time by more than 144 seconds per slide in prospective studies.[2]J. Yao et al., “Application of Artificial Intelligence in Laboratory Hematology: Advances, Challenges, and Prospects,” Acta Pharmaceutica Sinica B, sciencedirect.com In the AI-integrated blood analyzers market, that time gain matters because it improves throughput without asking labs to add scarce morphology specialists. It also allows a pathologist or senior reviewer to oversee several sites from one location, which supports hub-and-spoke laboratory models that are becoming more common in large health systems. This is why the AI-integrated blood analyzers market is finding demand not only in major hospitals, but also in laboratory networks that need consistent review quality across urban and rural locations.

Expansion of Fully Automated High-Throughput Labs

The shift toward fully automated laboratory workcells continues to support the AI-integrated blood analyzers market because central laboratories need more throughput, better consistency, and fewer manual steps. Sysmex America introduced the next-generation XR-Series in May 2026 for high-complexity and high-volume laboratories, and the platform builds on the established XN-Series with higher throughput, enhanced AI analytics, and easier automation integration. The same direction is visible in mid-market automation, where Mindray and Inpeco signed a strategic cooperation agreement in June 2024 to connect hematology solutions with total laboratory automation systems and a broader in vitro diagnostics data architecture. The AI-integrated blood analyzers market benefits from this pattern because hospital systems are consolidating satellite laboratories into larger reference sites, and those sites need analyzer fleets that can handle more daily samples with fewer interruptions. Laboratory information system connectivity becomes more important under this model because high-volume sites want one workflow that links sample handling, analyzer output, digital morphology, and result release. As more laboratories standardize around integrated automation stacks, the AI-integrated blood analyzers market gains from replacement demand, software add-ons, and longer service relationships.

Rising Blood Disorder Screening Volumes

The AI-integrated blood analyzers market is supported by persistent screening demand for anemia and other blood disorders that require repeated testing over time. In parallel, the user-supplied material describes how blood cancer diagnostics is becoming a major growth pocket because patients with hematologic malignancies need repeated complete blood count and morphology monitoring across treatment cycles. The clinical role of AI is also moving upstream, since validated models cited in the input can identify chronic myeloid leukemia risk from historical blood count data up to 5 years before clinical diagnosis. That changes the role of routine blood testing from simple measurement toward earlier pattern recognition in selected use cases. As this pattern spreads, the AI-integrated blood analyzers market benefits both from higher test volume and from the rising value of software that can flag clinically meaningful changes before a full specialist review.

Decentralized Testing Needs in Acute and Urgent Care

The AI-integrated blood analyzers market is also moving into acute and urgent care settings where speed matters as much as analytical accuracy. The user material shows that compact and AI-supported systems are expanding the practical role of point-of-care blood testing beyond simple convenience, especially when facilities need results quickly and cannot depend on a central lab for every case. Clinical validation work on the Hilab Lens AI-supported point-of-care complete blood count platform showed sensitivity above 89%, specificity above 88.5%, and kappa coefficients above 0.81, which narrowed the performance gap with central laboratory standards.[3]Hilab / Springer Nature, “Clinical Validation of the Hilab Lens for AI-Supported Point-of-Care CBC Testing in Pediatric Oncology,” Communications Medicine, springer.com In July 2026, ASUS Blade received Health Sciences Authority approval in Singapore for AI-powered peripheral blood film analysis software, with reported agreement of 99%-100% against expert reviewers, which highlights how regulatory acceptance is widening for AI-based blood review tools outside core laboratories. The AI-integrated blood analyzers market gains from this because urgent care centers, ambulatory sites, and smaller facilities can add blood testing closer to the patient instead of sending every sample to a distant hub. This creates incremental demand in the AI-integrated blood analyzer market rather than simply shifting volume away from large laboratories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Instrument and Per-Test Cost Burden | -1.6% | Global, most acute in South Asia, MEA, and South America | Long term (≥ 4 years) |

| Validation Gaps Versus Central Laboratory Standards | -1.2% | Global, particularly North America and Europe where FDA and IVDR compliance is mandatory | Medium term (2-4 years) |

| Data Privacy and Cybersecurity Compliance Complexity | -0.9% | North America and the EU, with spillover to India and APAC | Medium term (2-4 years) |

| Shortage of Skilled Hematology Review Personnel | -0.7% | Global, concentrated in rural and emerging-market settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Instrument and Per-Test Cost Burden

The AI-integrated blood analyzers market still faces a clear affordability barrier because full digital morphology capability, imaging hardware, software, and integration often require a level of spending that many smaller facilities cannot justify. The input notes that validated AI morphology platforms with high-resolution digital imaging and decision support software often carry list prices above USD 100,000. At the same time, reagent and per-test costs add recurring pressure on already tight laboratory budgets. This matters most in public systems and lower-tier facilities where reimbursement structures were built around conventional hematology testing rather than premium AI-enabled workflows. The AI-integrated blood analyzers market, therefore, risks splitting into two adoption tracks, with large reference laboratories moving faster while smaller and price-sensitive providers remain on older systems for longer. That split can slow total addressable demand even when the clinical case for automation is strong. It also increases pressure on vendors in the AI-integrated blood analyzer market to offer leasing, modular upgrades, or software overlays that lower the upfront hurdle.

Validation Gaps Versus Central Laboratory Standards

Validation remains a major restraint for the AI-integrated blood analyzers market because AI-enabled analyzers and digital review tools must prove that they perform consistently across sites, populations, and laboratory practices. The user-supplied material notes that the FDA now classifies relevant AI and machine learning automated blood analyzers under 21 CFR 864.5220, and that the Sysmex XR-Series received 510(k) clearance through this pathway, which shows that regulatory review is active and specific rather than informal. The same material also states that European IVDR requirements have raised the level of clinical evidence needed for market access, which lengthens development and validation cycles for many suppliers. Multi-site performance is especially important because an AI model trained under one staining protocol or patient mix may not perform the same way in another institution without additional study and tuning. Data privacy and cybersecurity controls add another layer of work because networked analyzers and image-sharing systems must meet local compliance expectations before wide deployment. The AI-integrated blood analyzers market also depends on skilled human oversight during abnormal case review, so staff shortages can still slow adoption even when the technology itself is ready.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Full Automation Holds the Revenue Base While Point-of-Care Expands the Addressable Need

Fully Automated Systems held 61.38% of revenue in 2025, which gave them the largest position in the AI-integrated blood analyzers market. Fully Automated Systems held 61.38% of the AI-integrated hematology blood market share in 2025 because large hospital laboratories and reference centers already depend on these platforms for high daily sample volumes. Their position is reinforced by laboratory consolidation, because larger centralized sites prefer workcells that can process thousands of samples with fewer manual steps and fewer interruptions. These systems also benefit from sunk capital and established operating routines, which makes replacement cycles more gradual and raises switching costs once automation tracks are in place. In the AI-integrated blood analyzers market, the installed foundation gives leading suppliers a stable revenue base from analyzers, reagents, maintenance, and software upgrades.

Semi-Automated Systems continue to serve mid-volume laboratories that need dependable 5-part differential capability but cannot justify a full workcell buildout. The user input shows that this segment is gradually losing ground from both sides because affordable compact devices pressure it at the lower end, while leasing and scaling programs pull higher-volume sites toward full automation. Point-of-Care Systems are the fastest-growing modality with a 16.63% CAGR through 2031, and that pace reflects more than instrument miniaturization. The AI-integrated blood analyzers market is therefore widening not only across large laboratories, but also across urgent care, ambulatory, and remote settings where near-patient testing can shorten clinical decision time. This dynamic broadens the addressable need of the AI-integrated blood analyzers market without removing the operational importance of high-throughput central sites.

By Product Type: Software Is Growing Faster Than Hardware Across the Portfolio

AI-integrated Blood Analyzers controlled 47.14% of product-type revenue in 2025, which kept core analyzer hardware at the center of the AI-integrated blood analyzers market. That leading share came from the global installed base built by large manufacturers such as Sysmex, Beckman Coulter, and Siemens Healthineers, whose high-throughput analyzer lines remain the base layer for routine complete blood count testing. Hardware still matters because analyzer contracts often anchor reagent pull-through, service agreements, and workflow standardization inside large laboratory accounts. AI Digital Morphology Analyzers remain the most differentiated hardware category because they address one of the most labor-intensive parts of blood review and allow subtle abnormalities to be reviewed in a more structured way. AI-Integrated Point-of-Care Blood Analyzers are also gaining visibility because compact formats can extend testing access into settings that do not have full laboratory infrastructure.

AI Blood Analysis Software is the fastest-growing product type, and the AI-integrated blood analyzers market size for this segment is projected to expand at a 17.16% CAGR through 2031. That growth is important because software can be deployed as a service layer, updated more often than hardware, and added to existing instrument fleets without forcing a full replacement cycle. The user-supplied material also describes software monetization as the main value creation shift in the market, which means the revenue center is moving from one-time equipment purchase toward recurring analytics, decision support, and workflow modules. Within the AI-integrated blood analyzers industry, this makes installed-base access more valuable than pure instrument shipment volume. It also explains why suppliers are investing in digital morphology, connectivity, and remote review functions that can sit on top of existing analyzer footprints. As this pattern deepens, the AI-integrated blood analyzers market is likely to see stronger competition around image interpretation, flagging algorithms, and service contracts than around analyzer mechanics alone.

By Application: CBC Testing Anchors Demand While Blood Cancer Diagnostics Adds the Fastest Lift

Complete Blood Count Testing retained 39.35% of application revenue in 2025, which made it the largest use case in the AI-integrated blood analyzers market. Complete Blood Count Testing accounted for 39.35% share of the AI-integrated blood analyzers market size in 2025 because it remains one of the most widely ordered diagnostic tests across routine screening, acute care, chronic disease monitoring, and treatment follow-up. This scale gives CBC testing a stable base that supports analyzer placement and reagent demand across hospitals, laboratories, and decentralized settings. The application also benefits from the fact that even small improvements in turnaround time or abnormal flagging can create visible workflow gains when the test volume is very high. In the AI-integrated blood analyzers market, this is why suppliers still treat routine CBC capability as the entry point for larger software and morphology offerings.

Blood Cancer Diagnostics is the fastest-growing application at a 16.48% CAGR through 2031, which gives it a larger strategic role in the AI-integrated blood analyzers market than its current revenue size suggests. The user input cites validated model performance of 99.5% for acute lymphoblastic leukemia, 98.8% for acute myeloid leukemia, and 99.7% for acute promyelocytic leukemia, which shows that AI-based blood review is already approaching specialist-level performance in selected subtyping tasks. The same source notes that machine learning models applied to routine blood count data can identify chronic myeloid leukemia risk as early as 5 years before clinical diagnosis, which strengthens the medical case for advanced pattern detection in routine testing. Infection Detection is also gaining traction because AI flagging at the blood count level can support faster distinction between bacterial and viral patterns in the clinical workflow described in the user draft. Digital Morphology and Peripheral Smear Review remain directly shaped by AI because autonomous platforms can analyze many more cells than conventional smear standards, which changes both review depth and staffing needs. Prenatal, neonatal, wellness, and preventive use cases are still early, but their presence suggests that the AI-integrated blood analyzers market is expanding beyond acute and specialist pathways into broader screening and longitudinal monitoring.

By End User: Hospitals Keep the Revenue Lead While Diagnostic Laboratories Add the Strongest Growth

Hospitals held 46.43% of end-user revenue in 2025, which made them the largest buying group in the AI-integrated blood analyzers market. Their lead reflects the concentration of complex hematology testing inside hospital settings, including blood cancer workup, presurgical screening, intensive care monitoring, and inpatient acute care. Hospitals also have the broadest need for integrated analyzer capability because they must support both routine blood count testing and higher-acuity morphology review within one infrastructure. In the AI-integrated blood analyzers market, hospital laboratories often set the benchmark for validation, procurement review, and multispecialty workflow integration. That is why hospitals remain the main revenue anchor even as other end-user groups adopt AI-enabled systems more quickly on a percentage growth basis.

Diagnostic Laboratories are the fastest-growing end user with a 14.88% CAGR through 2031, and this reflects the operating model of the AI-integrated blood analyzers industry as much as it reflects test volume. Independent and reference laboratories run under tighter per-test economics, so reducing manual slide review time and improving release speed can directly affect margins and customer retention. The same benefit supports remote review across multi-site networks, where one specialist team can supervise a broader catchment area through digital morphology and centralized workflow controls. Blood Banks and Transfusion Centers also matter because AI-enabled blood analysis can support donor screening and compatibility-related workflows at a scale that is hard to manage manually. Ambulatory and Urgent Care Centers are becoming more relevant as compact AI-supported systems move blood testing closer to patients who previously would have been referred to a hospital or a large diagnostic chain. Research and Academic Institutes remain an important early channel because clinical validation work in these centers often shapes the commercial confidence that later drives broader uptake in the AI-integrated blood analyzers market.

Geography Analysis

North America accounted for 42.36% of the AI-integrated blood analyzers market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense base of high-throughput reference laboratories, established reimbursement structures for in vitro diagnostics, and a regulatory pathway that is increasingly familiar with AI-enabled hematology devices. In the United States, laboratory consolidation and staff shortages continue to support demand for automation because larger networks want more throughput and more consistent review quality from fewer specialized personnel. The FDA clearance pathway is also shaping supplier behavior, as shown by the Sysmex XR-Series clearance under the relevant automated blood analyzer classification and the steady push toward next-generation systems with more integrated analytics. Canada and Mexico remain smaller but important contributors, with Canada favoring networked digital review models and Mexico offering room for mid-tier analyzer uptake through its growing private diagnostic laboratory base.

Asia-Pacific is the fastest-growing region, and the AI-integrated blood analyzers market size in the region is forecast to expand at a 15.32% CAGR through 2031. The region is diverse because China combines large import demand with stronger domestic manufacturing, while Japan and South Korea maintain deeper capability in advanced laboratory instrumentation and premium clinical workflows. Mindray’s hematology push and its total laboratory automation cooperation with Inpeco show how local and regional suppliers are trying to deepen their position not only through analyzers, but also through connected laboratory ecosystems. India’s demand profile in the user draft is tied closely to diagnostic laboratory expansion and higher screening needs for blood disorders, which makes scalable analyzer deployment especially relevant outside major hospital systems. In July 2026, ASUS Blade received Health Sciences Authority approval in Singapore for AI-powered peripheral blood film analysis software, which signals that Southeast Asia is becoming a useful early-adoption and validation point for AI morphology tools.

Europe remains an important revenue base for the AI-integrated blood analyzers market because accreditation expectations and digital laboratory practices support the adoption of AI-assisted review, especially in Germany, France, the United Kingdom, and the Nordic countries. The region’s stricter regulatory and compliance environment creates more work for vendors, but it also favors suppliers that can document performance, oversight, and quality control in a structured way.

Competitive Landscape

The AI-integrated blood analyzers market is moderately consolidated at the top, with Sysmex Corporation, Beckman Coulter, and Siemens Healthineers holding the strongest global reach in analyzer placements and distribution. Their position comes from large installed bases, established service networks, long-standing laboratory relationships, and the ability to bundle analyzers with reagents, digital review, and workflow connectivity. Sysmex remains a central force in the AI-integrated blood analyzers market because its next-generation XR-Series keeps the company active in high-complexity and high-volume laboratories that want better throughput and tighter automation integration. Beckman Coulter and Siemens Healthineers remain important because large hospital and laboratory customers still value broad menu coverage, operational reliability, and enterprise-level support. At the same time, AI-focused challengers are putting pressure on the software and morphology layer of the AI-integrated blood analyzers market by targeting specific review bottlenecks rather than trying to replace the whole analyzer stack at once.

A clear strategic move came from Mindray, which completed the acquisition of a 75% controlling stake in DiaSys Diagnostic Systems GmbH in December 2024 to strengthen its European presence and add clinical chemistry reagent capability to its broader diagnostics portfolio. Another move came from Mindray’s June 2024 strategic cooperation with Inpeco, which tied hematology systems more closely to total laboratory automation and data management, and that supports a stronger ecosystem position rather than a stand-alone instrument strategy. Sysmex responded on the throughput and automation side with the XR-Series introduction in 2026, which shows that incumbent competition is centered on refresh cycles that deepen analyzer performance and workflow integration rather than on simple unit placement alone. Scopio Labs also continued to expand the competitive boundary through regulatory progress in digital morphology and bone marrow analysis, including earlier FDA clearance for its digital bone marrow aspirate application and later feature expansion on the X100 and X100HT platforms. These moves show that the AI-integrated blood analyzers market is being shaped by both broad portfolio vendors and specialist firms that focus on digital interpretation.

Competition in the AI-integrated blood analyzers market is therefore no longer defined only by analyzer throughput, because software, image quality, interoperability, and regulatory readiness now influence purchasing decisions more directly. The user draft also points to openings in AI-native point-of-care systems, subscription software overlays for non-AI installed bases, and AI-enabled bone marrow analysis, all of which remain less settled than routine analyzer hardware. Smaller entrants still face real barriers because commercial success now depends on validation depth, cybersecurity readiness, and the ability to support laboratories through formal compliance review. Even so, the AI-integrated blood analyzers market remains open enough for specialists to win share in selected workflows, especially where they can shorten review time or add clinically useful decision support without forcing customers to replace the entire analyzer fleet.

AI-integrated Blood Analyzers Industry Leaders

Abbott Laboratories

Beckman Coulter, Inc.

F. Hoffmann-La Roche Ltd

Siemens Healthineers AG

Sysmex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: ASUS Blade received Health Sciences Authority (HSA) approval in Singapore for its AI-powered peripheral blood film analysis software, achieving 99%-100% agreement with expert reviewers.

- May 2026: Sysmex America introduced the next-generation XR-Series hematology solution, including the XR-10 and XR-9000 configurations for high-complexity and high-volume laboratories, building on the established XN-Series platform with higher throughput, enhanced AI analytics, and streamlined automation integration.

- April 2026: Scopio Labs received EU IVDR certification for its Full-Field Digital Bone Marrow Application, expanding its regulatory footprint in Europe following earlier CE marking for its full-field digital morphology platforms in February 2026.

- July 2025: Scopio Labs received its fourth FDA clearance (K243144) for enhanced AI decision support system features on the X100 and X100HT platforms, adding automated analysis for 23 RBC morphology parameters and platelet clump detection in peripheral blood smears.

Global AI-integrated Blood Analyzers Market Report Scope

The AI-Integrated Blood Analyzers Market comprises diagnostic instruments that combine artificial intelligence, machine learning, and advanced data analytics with blood analysis technologies to automate sample processing, enhance cell identification, and support clinical decision-making. These systems improve the accuracy, speed, and consistency of hematology and blood diagnostics by enabling intelligent flagging of abnormalities, automated morphology analysis, and predictive workflow optimization. The market is driven by increasing demand for high-throughput laboratory automation, early disease detection, and AI-enabled precision diagnostics across hospitals, diagnostic laboratories, and research institutions.

As per the scope of the report, AI in healthcare information systems refers to the integration of artificial intelligence technologies into hospital information systems, EHRs, and clinical decision support platforms to improve patient care and operational efficiency. It leverages tools such as machine learning, natural language processing, and predictive analytics to analyze complex medical data, automate workflows, and support clinicians in diagnosis and treatment planning. By embedding AI into healthcare IT infrastructure, these systems enable personalized care, reduce errors, and optimize resource utilization, ultimately enhancing patient outcomes and population health.

The AI-integrated blood analyzers market is segmented by modality, product type, application, end user, and geography. By modality, it is further divided into fully automated systems, semi-automated systems, and point-of-care systems. By product type, it is segmented into AI-integrated hematology analyzers, AI-integrated point-of-care blood analyzers, AI-based digital morphology analyzers, and AI-blood analysis software. By application, the market is segmented into complete blood count testing, anemia screening and triage, blood cancer diagnostics, infection detection, hemorrhagic condition monitoring, digital morphology and peripheral smear review, and others. By end user, the market is segmented into hospitals, diagnostic laboratories, blood banks and transfusion centers, ambulatory and urgent care centers, research and academic institutes, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Fully Automated Systems |

| Semi-Automated Systems |

| Point-of-Care Systems |

| AI-Integrated Hematology Analyzers |

| AI-Integrated Point-of-Care Blood Analyzers |

| AI-Based Digital Morphology Analyzers |

| AI Blood Analysis Software |

| Complete Blood Count Testing |

| Anemia Screening and Triage |

| Blood Cancer Diagnostics |

| Infection Detection |

| Hemorrhagic Condition Monitoring |

| Digital Morphology and Peripheral Smear Review |

| Others (Prenatal and Neonatal Testing, Wellness & Preventive Health, etc.) |

| Hospitals |

| Diagnostic Laboratories |

| Blood Banks and Transfusion Centers |

| Ambulatory and Urgent Care Centers |

| Research and Academic Institutes |

| Others (Mobile Diagnostic Units, Dialysis Centers, etc.) |

| United States |

| Canada |

| Mexico |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| GCC |

| South Africa |

| Rest of Middle East and Africa |

| Brazil |

| Argentina |

| Rest of South America |

| By Modality | Fully Automated Systems |

| Semi-Automated Systems | |

| Point-of-Care Systems | |

| By Product Type | AI-Integrated Hematology Analyzers |

| AI-Integrated Point-of-Care Blood Analyzers | |

| AI-Based Digital Morphology Analyzers | |

| AI Blood Analysis Software | |

| By Application | Complete Blood Count Testing |

| Anemia Screening and Triage | |

| Blood Cancer Diagnostics | |

| Infection Detection | |

| Hemorrhagic Condition Monitoring | |

| Digital Morphology and Peripheral Smear Review | |

| Others (Prenatal and Neonatal Testing, Wellness & Preventive Health, etc.) | |

| By End User | Hospitals |

| Diagnostic Laboratories | |

| Blood Banks and Transfusion Centers | |

| Ambulatory and Urgent Care Centers | |

| Research and Academic Institutes | |

| Others (Mobile Diagnostic Units, Dialysis Centers, etc.) | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the AI-integrated hematology analyzers space?

The AI-integrated hematology analyzers market size was USD 1.07 billion in 2025 and is forecast to reach USD 2.30 billion by 2031 at a 13.65% CAGR.

Which region leads global revenue?

North America led with 42.36% of revenue in 2025 because of its large high-throughput lab base, reimbursement support, and active regulatory pathway for AI-enabled devices.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region with a 15.32% CAGR through 2031, supported by domestic manufacturing, laboratory expansion, and wider regulatory acceptance.

Which product category is expanding the fastest?

AI Blood Analysis Software is the fastest-growing product type with a 17.16% CAGR, reflecting the shift toward recurring software, workflow, and decision-support revenue.

Why are hospitals still the largest end users?

Hospitals held 46.43% of revenue in 2025 because they manage high-acuity cases, large CBC volumes, cancer workups, and intensive care monitoring that require more capable analyzer setups.

Which application area offers the strongest growth potential?

Blood Cancer Diagnostics is projected to grow at a 16.48% CAGR through 2031 because AI is improving morphology review and helping detect clinically meaningful blood count patterns earlier.

Page last updated on: