AI Infrastructure-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 70.91 Billion |

| Market Size (2031) | USD 279.94 Billion |

| Growth Rate (2026 - 2031) | 31.60% CAGR |

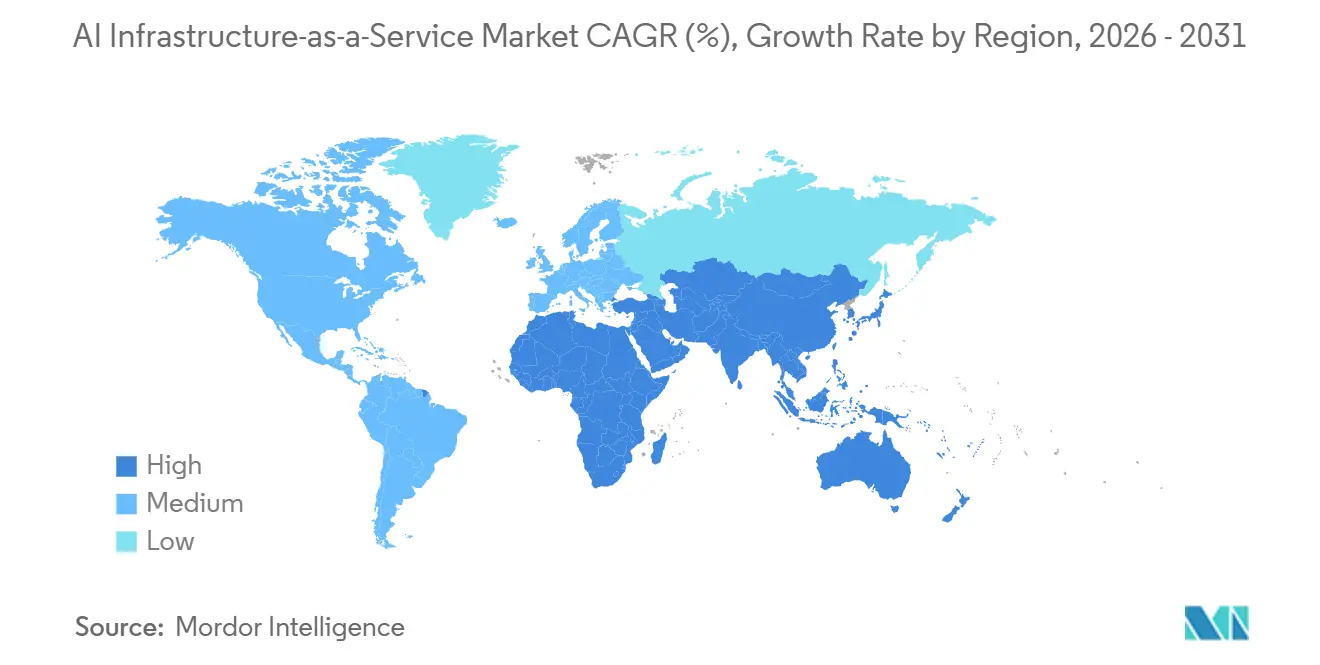

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

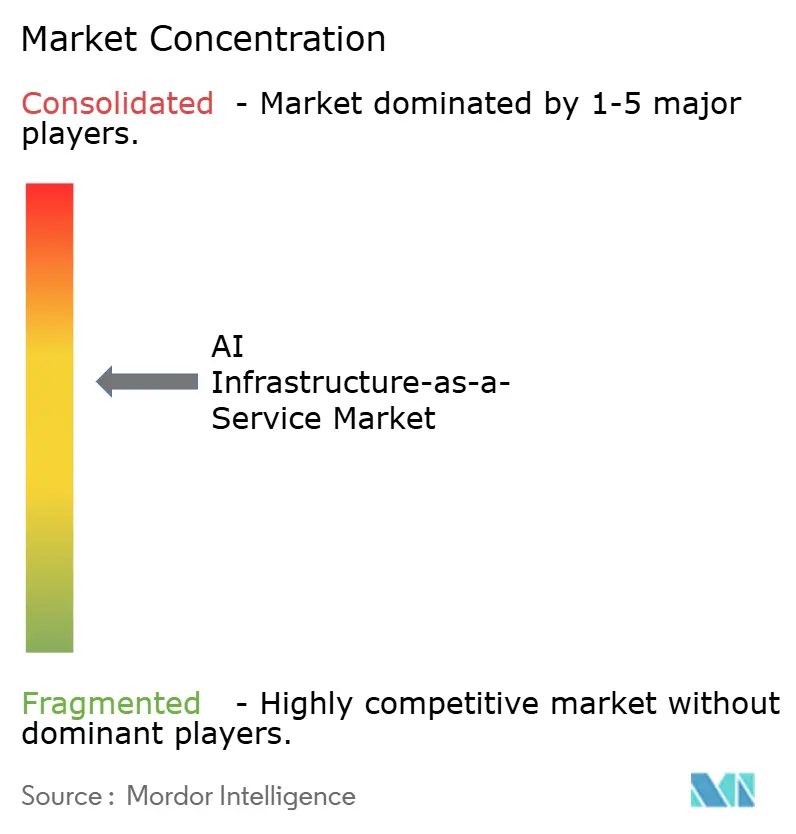

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Infrastructure-as-a-Service Market Analysis by Mordor Intelligence

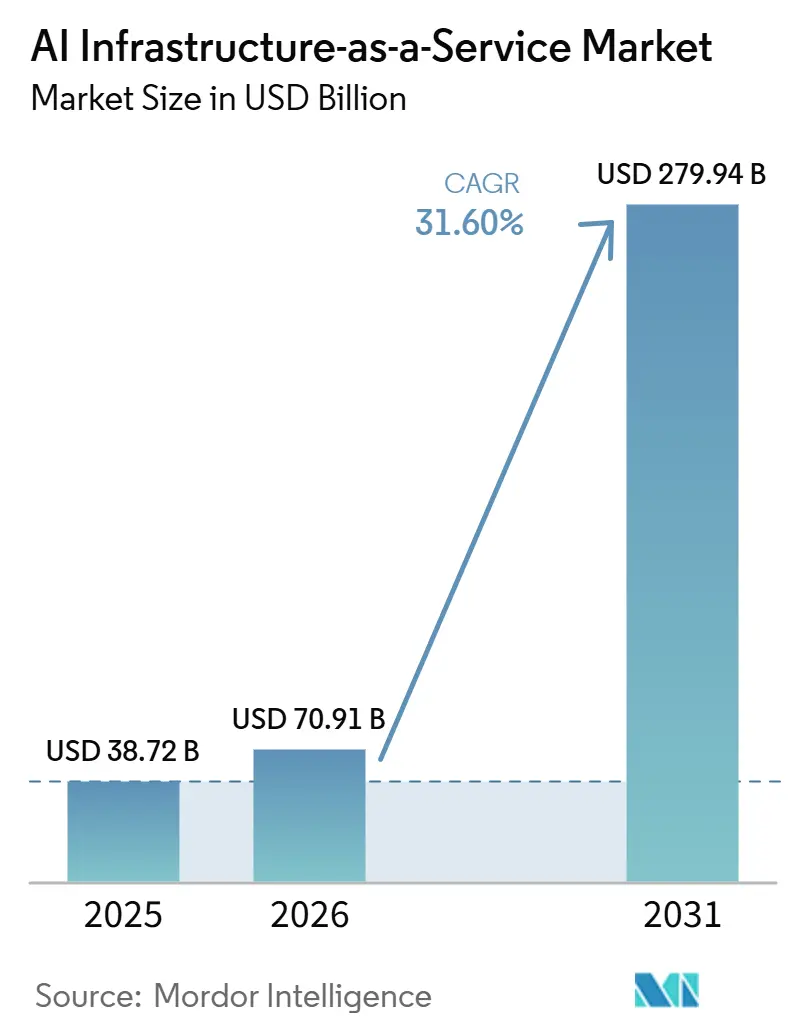

The AI Infrastructure-as-a-Service market size is expected to grow from USD 38.72 billion in 2025 to USD 70.91 billion in 2026 and is forecast to reach USD 279.94 billion by 2031 at 31.60% CAGR over 2026-2031. The AI Infrastructure-as-a-Service market is moving from an early phase focused on large training clusters to a broader utility model in which enterprises buy AI compute as an on-demand service rather than owning the hardware. Demand is also shifting toward inference-heavy production use, raising the value of orchestration, latency control, and distributed capacity over raw compute alone. The competitive structure reflects this change, with hyperscalers retaining scale advantages while GPU-focused cloud providers win business through configuration depth, faster provisioning, and specialized performance. Sovereign cloud requirements across Europe, the Middle East, and Asia-Pacific are opening new room for region-specific capacity and regulated deployments. At the same time, memory shortages, long GPU lead times, and power-related commissioning delays are keeping supply tight and preserving favorable pricing conditions for well-capitalized providers in the AI Infrastructure-as-a-Service market.

Key Report Takeaways

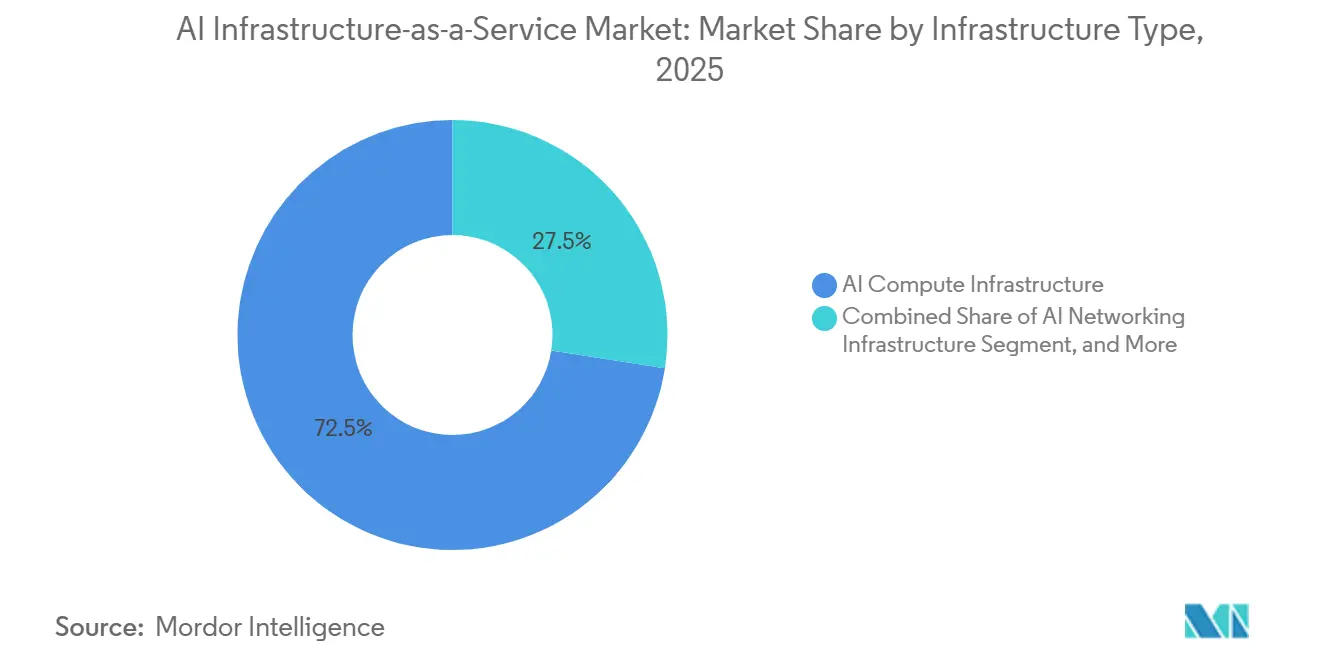

- By infrastructure type, AI Compute Infrastructure led with 72.53% of the AI Infrastructure-as-a-Service market share in 2025, while AI Infrastructure Management and Orchestration is projected to expand at 32.78% CAGR through 2031.

- By workload type, Model Training and Fine-Tuning accounted for 49.34% of revenue in 2025, while Model Inference and Serving are projected to grow at a CAGR of 32.45% through 2031.

- By deployment mode, Public Cloud accounted for 68.07% of revenue in 2025, while Hybrid Cloud is expected to expand at 31.93% CAGR through 2031.

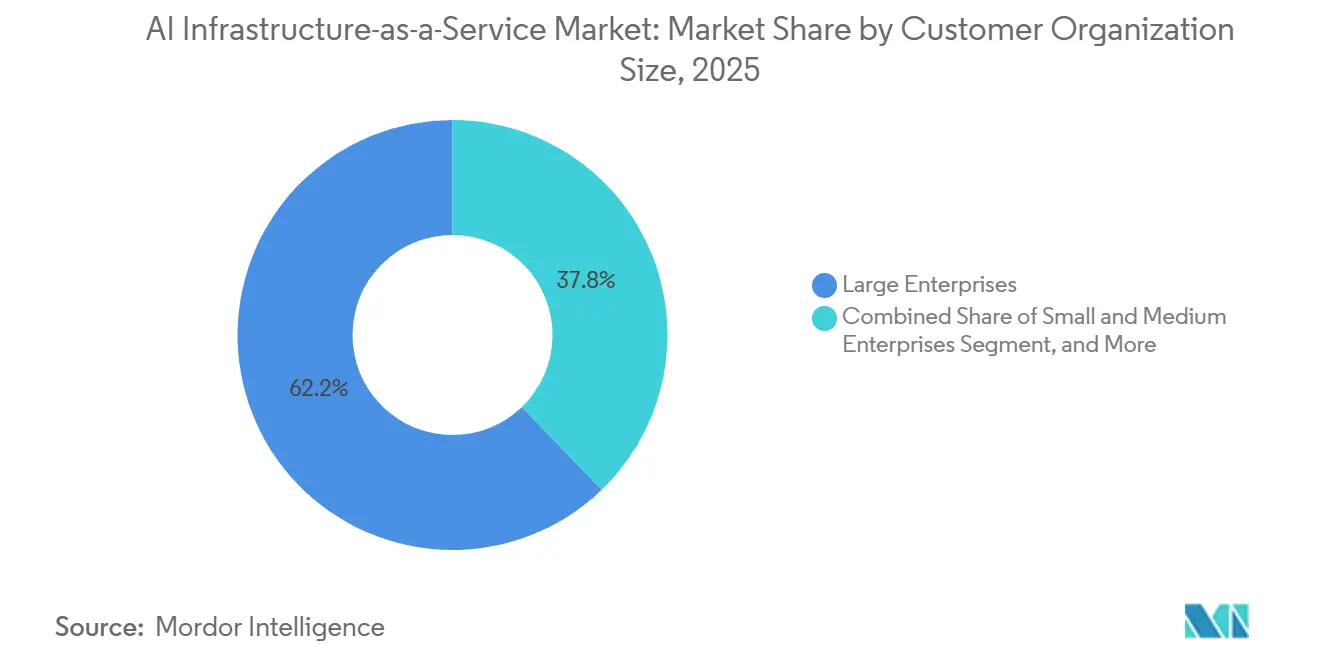

- By customer organization size, Large Enterprises accounted for 62.21% of revenue in 2025, while Small and Medium Enterprises are projected to grow at a 32.51% CAGR through 2031.

- By end-use industry, IT, Cloud, SaaS, and Digital Services accounted for 37.58% of revenue in 2025, while Automotive and Mobility are expected to grow at a 32.46% CAGR through 2031.

- By geography, North America held 56.12% of the AI Infrastructure-as-a-Service market share in 2025, while Asia-Pacific is projected to expand at 32.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Infrastructure-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elastic GPU Capacity Demand for Training and Inference | +7.2% | Global, led by North America and the Asia-Pacific | Short term (≤ 2 years) |

| Shift to Usage-Based AI Infrastructure Consumption | +6.5% | Global | Short term (≤ 2 years) |

| Managed AI Workload Stack Adoption | +5.8% | North America and Europe | Medium term (2-4 years) |

| Need For Edge-Ready Low-Latency AI Infrastructure | +4.1% | Asia-Pacific and North America, with spillover to the Middle East and Africa | Medium term (2-4 years) |

| Expansion of Sovereign and Residency-Compliant AI Clouds | +3.0% | Europe, the Middle East and Africa, and Asia-Pacific | Medium term (2-4 years) |

| Demand for Multi-Model and Multi-Tenant AI Platforms | +2.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand For Elastic GPU Capacity Fuels AI IaaS Expansion

The strongest draw of the AI Infrastructure-as-a-Service market is the ability to scale GPU access up or down as workload volumes change. Many enterprises cannot accurately predict training runs, fine-tuning cycles, or inference peaks to justify fixed hardware ownership. That uncertainty makes burst access more valuable than static reservations, especially when model releases, application launches, or customer traffic can shift sharply within days. Akamai reported in 2026 that 64% of organizations required end-to-end AI response times below 250 milliseconds for critical use cases, while 50% of current deployments failed to meet that standard at peak load, which reinforces the value of elastic infrastructure tuned for scale and responsiveness.[1]Akamai, “AI Survey, 50% Of Organizations Struggle To Maintain Latency At Scale,” Akamai Blog, akamai.com The AI Infrastructure-as-a-Service market is also seeing a shift in utilization, as inference now consumes a larger share of GPU hours than it did during the earlier training-led phase. This pattern favors providers that can quickly release capacity, move workloads across clusters, and support low-latency serving in production.

Shift From Capex-Heavy AI Buildouts to Usage-Based Consumption Models

The AI Infrastructure-as-a-Service market is benefiting from a clear shift away from capital-intensive GPU ownership toward operating-cost models. Enterprise AI programs are scaling quickly, but the hardware needed to support them can take many months to procure, install, and optimize. That timing mismatch creates stranded capital risk, especially as newer GPU generations deliver higher performance and shorten the useful life of earlier systems. Usage-based procurement reduces that risk by letting firms align compute spending with active models, business units, and deployment schedules. It also makes AI budgets easier to trace, because teams can map costs to specific applications rather than amortize them across broad infrastructure pools. As the AI Infrastructure-as-a-Service market matures, this spending model is likely to remain one of the main reasons enterprises choose shared or dedicated cloud capacity over owned GPU estates.

Rapid Enterprise Adoption of Managed AI Workload Stacks

Managed workload stacks are becoming a larger part of the AI Infrastructure-as-a-Service market because they shorten the path from model selection to live deployment. Many buyers now want pre-integrated compute, storage, networking, orchestration, and serving tools rather than assembling each layer themselves. This is especially relevant for firms that have application and data teams but lack deep infrastructure engineering resources. Lambda's August 2025 move to exit its on-premises hardware business and focus on cloud-based AI services and AI factory operations reflects this change in demand. Providers that combine model libraries, fine-tuning workflows, observability tools, and serving APIs are capturing more value than those that offer only bare compute. That trend is widening the addressable customer base of the AI Infrastructure-as-a-Service market by lowering the skill threshold for adoption and making repeat consumption easier for smaller organizations.

Growing Need for Edge-Ready Low-Latency AI Infrastructure

The AI Infrastructure-as-a-Service market is no longer defined only by centralized hyperscale training clusters. A growing set of use cases, including autonomous control, industrial automation, fraud detection, and real-time digital agents, requires inference close to where data is generated. These workloads are sensitive to latency, network jitter, and service continuity, which makes distributed deployment a practical requirement rather than a design preference. That is raising demand for providers that can extend orchestration, monitoring, and lifecycle management from core regions to edge locations. Smaller task-specific models are also helping this shift by making it more practical to run useful inference outside the largest data center clusters. The AI Infrastructure-as-a-Service market is therefore expanding into a broader delivery model in which central training capacity and edge-aware serving capacity must work together within a single operating framework.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GPU And High-Bandwidth Memory Supply Constraints | -3.8% | Global | Short term (≤ 2 years) |

| High Power Density and Cooling Requirements | -2.7% | Global, acute in North America and the Asia-Pacific | Medium term (2-4 years) |

| Interoperability And Vendor Lock-In Across AI Stack Layers | -1.9% | Global | Medium term (2-4 years) |

| Cross-Border Data and AI Governance Compliance Burden | -1.4% | Europe, Asia-Pacific, the Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic GPU And HBM Scarcity Limits Capacity Expansion

The largest near-term constraint on the AI Infrastructure-as-a-Service market is not demand, but the limited supply of advanced GPUs and the memory packages required to build them. High-bandwidth memory remains the critical upstream bottleneck because GPU assembly cannot scale without it. Industry reporting in 2026 showed that SK Hynix had pre-sold its HBM3e output through 2026 and substantially into 2027, while Micron projected that the HBM market would rise from USD 35 billion in 2025 to USD 100 billion by 2028. The same report noted that SK Hynix, Samsung, and Micron accounted for close to 95% of global HBM output, leaving little room for rapid supply diversification. Long lead times for advanced NVIDIA systems mean providers often have customer demand in hand before the required hardware is available. As a result, the AI Infrastructure-as-a-Service market faces a short-term revenue ceiling driven by supply availability rather than weak customer interest.

High Power Density and Cooling Challenges Slow Data Center Build-Out

Power and cooling are the second major brake on the AI Infrastructure-as-a-Service market. Modern AI clusters draw far more power per rack than conventional enterprise infrastructure, which pushes providers toward liquid cooling, stronger grid access, and more complex commissioning plans. These requirements raise project cost and lengthen the time needed to bring new capacity online in established data center corridors. They also complicate site selection, because not every location can support dense AI infrastructure without electrical upgrades or additional thermal engineering. The International Energy Agency noted that cooling systems account for 7-30% of total data center electricity consumption, and that share rises as computing density increases.[2]International Energy Agency, “Energy Demand From AI,” IEA, iea.org This means the AI Infrastructure-as-a-Service market must address not only compute demand but also the practical limits of power delivery, heat removal, and deployment timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure Type: Compute Leads Revenue While Orchestration Gains Strategic Weight

AI Compute Infrastructure held 72.53% of the AI Infrastructure-as-a-Service market share in 2025, which reflects the very high value of GPU cluster rentals and AI accelerator provisioning at scale. This part of the AI Infrastructure-as-a-Service market remains the economic core of the stack because nearly every training and inference workload depends on access to expensive accelerated compute. The dollar intensity of NVIDIA H100 and Blackwell systems keeps compute at the center of customer spending, even when software and orchestration become more important for buying decisions. Storage and networking remain essential supporting layers, because training performance depends on fast dataset retrieval and low-latency communication across multiple nodes. AI Storage Infrastructure supports sustained throughput for large datasets, while AI Networking Infrastructure enables distributed jobs that would otherwise suffer from bottlenecks between servers.

AI Infrastructure Management and Orchestration is projected to grow at a 32.78% CAGR through 2031, making it the fastest-rising subsegment of the AI Infrastructure-as-a-Service market. This growth reflects the move from single-cluster experimentation to multi-cloud, multi-model, and multi-region production environments. As inference takes a larger share of GPU utilization, enterprises need tools that can route jobs to the right hardware tier while meeting latency and cost targets. That makes orchestration software more central to customer value, because it connects scheduling, utilization monitoring, workload placement, and policy control. The AI Infrastructure-as-a-Service industry is therefore shifting from a hardware-centered purchase decision to a platform-centered one, where the ability to manage heterogeneous fleets becomes a key source of differentiation. Providers that combine compute access with strong management tooling are likely to retain accounts longer, because migration becomes harder once customers depend on those operating layers. This also gives smaller specialists room to compete, because they can add value in software even when they cannot match hyperscaler infrastructure breadth. Over time, orchestration is likely to capture a larger share of revenue as buyers prioritize workload efficiency and operating control alongside raw capacity. The result is a more balanced segment structure within the AI Infrastructure-as-a-Service market, even though compute remains the largest revenue pool today.

By Workload Type: Inference Growth Changes Revenue Mix Across the Stack

Model Training and Fine-Tuning accounted for 49.34% of revenue in 2025, making it the largest workload category in the AI Infrastructure-as-a-Service market. This leadership came from the high cost of dense GPU clusters, advanced interconnects, and long-duration jobs required for large-scale model development. Training workloads still matter because many enterprises and model developers continue to fine-tune frontier or domain-specific systems for production use. They also create demand for managed data preparation, storage throughput, and performance monitoring across large distributed environments. Even as the workload mix broadens, training remains a large revenue anchor because it consumes the most premium hardware and often runs on reserved or highly specialized cluster setups.

Model Inference and Serving is projected to grow at 32.45% CAGR through 2031, making it the fastest-growing workload in the AI Infrastructure-as-a-Service market. Vast.ai stated in 2026 that inference workloads accounted for roughly two-thirds of AI compute, supporting the view that production usage now outweighs experimentation in many environments. This shift changes infrastructure economics because inference is continuous, latency-sensitive, and closely tied to customer-facing demand. It also increases interest in model routing, autoscaling, caching, and co-located services such as vector databases for retrieval-augmented generation pipelines. AI Data Processing and Analytics remains important because enterprises need managed pipelines to prepare training data, ground responses, and support retrieval workflows after deployment. Other AI workloads, including synthetic data generation, reinforcement learning from human feedback, and simulation for drug discovery or autonomous systems, add burst demand that broadens utilization patterns.

By Deployment Mode: Public Cloud Stays Largest While Hybrid Architectures Gain Ground

Public Cloud accounted for 68.07% share of the AI Infrastructure-as-a-Service market size in 2025, making it the dominant deployment model. Its lead comes from fast provisioning, access to the newest GPU generations, broad geographic reach, and built-in AI services that reduce setup time for enterprise teams. For many buyers, public infrastructure remains the easiest way to launch pilots, expand capacity quickly, and avoid long hardware procurement cycles. It also gives customers access to a wide range of services, including managed training, model hosting, data pipelines, and observability tools, all within a single environment. This combination keeps Public Cloud central to the AI Infrastructure-as-a-Service market, especially for organizations that prioritize speed and global availability.

Hybrid Cloud is projected to grow at a 31.93% CAGR through 2031, making it the fastest-growing deployment mode in the AI Infrastructure-as-a-Service market. The main reason is workload separation: sensitive or regulated tasks stay on dedicated infrastructure, while burst training or seasonal demand moves to shared public capacity. This approach gives enterprises greater control over data placement and cost allocation without sacrificing access to large, elastic GPU pools. Managed Private Cloud also has a growing role, particularly for government bodies and regulated enterprises that need single-tenant environments, tailored networking, or stronger isolation controls. Across these deployment paths, customers increasingly want portability between sites, regions, and providers so they can avoid lock-in and keep procurement options open. That need is turning deployment strategy into a longer-term design choice rather than a simple hosting decision. The AI Infrastructure-as-a-Service market is therefore expanding across mixed environments where orchestration and policy control matter as much as raw capacity. Providers that support smooth workload movement across deployment modes are likely to be better positioned as enterprise architectures become more complex.

By Customer Organization Size: Large Enterprises Lead Today While SME Adoption Accelerates

Large Enterprises accounted for 62.21% of revenue in 2025, making them the largest customer segment in the AI Infrastructure-as-a-Service market. Their lead reflects larger IT budgets, deeper data resources, and AI programs mature enough to justify reserved cluster agreements or dedicated service arrangements. These organizations often run multiple model initiatives simultaneously, which supports high utilization and makes enterprise pricing models more attractive. They also place strong value on global support, integrated billing, and broad security controls, which favors providers with large platform footprints. This keeps enterprise demand concentrated with hyperscalers and major specialists that can deliver capacity, service continuity, and long-term account management at scale.

Small and Medium Enterprises are projected to grow at 32.51% CAGR through 2031, making them the fastest-rising customer segment in the AI Infrastructure-as-a-Service market. Their growth is being supported by per-second billing, managed workload stacks, and pre-built serving APIs that lower the technical barrier to adoption. Many smaller firms want to deploy AI in products or operations, but they do not want to build internal infrastructure teams first. That creates strong demand for providers that package compute, orchestration, and deployment tools into simpler service layers. Government, research, and educational organizations form the third customer group and bring different requirements, including sovereign cloud alignment, research-grade performance, and predictable access windows. The AI Infrastructure-as-a-Service industry is responding by developing more vertical and institution-specific bundles instead of one generic cloud offer for every buyer. This broadens the customer base without changing the fact that large enterprises still anchor most current revenue. Over time, recurring consumption from smaller organizations could become a meaningful stabilizer for the AI Infrastructure-as-a-Service market as adoption spreads beyond the earliest heavy users.

By End-Use Industry: Digital Services Dominate Current Spending While Automotive Expands Fastest

IT, Cloud, SaaS, and Digital Services accounted for 37.58% of revenue in 2025, making this the largest end-use group in the AI Infrastructure-as-a-Service market. The segment benefits from a self-reinforcing demand pattern, as many cloud-native companies build AI products on the same infrastructure services they also consume. These firms typically have the technical readiness to quickly integrate model training, inference, and deployment pipelines. Their customer-facing software products also generate recurring inference demand, which supports sustained infrastructure spend after the initial build phase. This keeps digital services at the center of the AI Infrastructure-as-a-Service market and makes them an important early adopter base for new service features.

Automotive and Mobility is projected to grow at 32.46% CAGR through 2031, making it the fastest-growing end-use segment in the AI Infrastructure-as-a-Service market. The main drivers are autonomous driving simulation, model retraining on real-world fleet data, and AI-enabled operational systems that require both central training and distributed inference. Telecommunications, BFSI, and Healthcare and Life Sciences remain large demand pools for their own reasons, including customer service automation, fraud detection, trading models, imaging analysis, and drug discovery workloads. Other end-use groups, including manufacturing, retail, energy, and agriculture, widen the addressable base and reduce the current concentration around technology-led customers. As these sectors mature, providers will need more verticalized service packages instead of broad compute catalogs. The AI Infrastructure-as-a-Service industry is likely to see stronger adoption where providers combine infrastructure with workflow support tailored to each use case.

Geography Analysis

North America held 56.12% of the AI Infrastructure-as-a-Service market in 2025, which kept it as the largest regional contributor. The region’s lead rests on hyperscaler scale, early enterprise AI adoption, and deep access to capital for data center and GPU expansion. The United States remains the core market because most of the largest cloud platforms, AI software ecosystems, and high-value enterprise contracts are concentrated there. Canada adds strategic weight through renewable-energy-linked data center development and its proximity to major United States cloud corridors. Mexico supports the regional picture through a growing nearshore digital services base that can benefit from lower-latency access to North American AI infrastructure.

Europe held a meaningful share of the AI Infrastructure-as-a-Service market in 2025, with Germany, the United Kingdom, and France serving as the main national demand centers. Regional demand is being shaped by sovereign cloud priorities, procurement rules, and the need for clearer control over training data, infrastructure location, and operational governance. These conditions are giving local and sovereignty-aligned providers more room to compete in regulated workloads than they had before 2024. The AI Infrastructure-as-a-Service market in Europe is therefore evolving with a stronger policy layer than in North America, especially in finance, healthcare, and government use cases. That makes compliance features, audit trails, and regional operating models more important for winning enterprise contracts.

Asia-Pacific is projected to expand at 32.84% CAGR through 2031, making it the fastest-growing regional segment in the AI Infrastructure-as-a-Service market. China remains the largest single market in the region, while Japan, South Korea, and India each support different demand patterns tied to industrial policy, semiconductors, software services, and regulated enterprise adoption. Southeast Asia, led by Malaysia, Singapore, and Thailand, is gaining importance as a regional deployment hub because of its land, tax, and power advantages. South America and the Middle East and Africa are smaller today, but both are becoming more relevant as sovereign AI programs, telecom demand, and greenfield data center projects expand the future footprint of the AI Infrastructure-as-a-Service market.

Competitive Landscape

The AI Infrastructure-as-a-Service market in 2026 remains split between hyperscalers and specialist GPU cloud providers, but the gap between scale and specialization is narrowing. CoreWeave, Inc., Nebius Group N.V., Lambda, Inc., Crusoe Energy Systems LLC, and Vultr Holdings Corporation still hold the broadest platform reach, the deepest enterprise relationships, and the strongest ability to bundle compute with storage, security, and software services. That gives them a structural advantage with large accounts that want a single provider across multiple layers of the stack. At the same time, the AI Infrastructure-as-a-Service market has created space for neoclouds that compete by offering faster access to accelerators, more tailored cluster configurations, and sharper performance for training or serving. This two-tier structure means competition is no longer only about who owns the most global infrastructure, but also about who can deliver the best fit for specific AI workloads.

CoreWeave is the clearest example of how fast a specialist can scale in the AI Infrastructure-as-a-Service market. It's April 2026, and a USD 8.5 billion financing facility, backed by investment-grade ratings, gives it a stronger path to capacity expansion at a time when many competitors still depend on smaller funding channels. The company also secured a USD 6 billion AI cloud agreement with Jane Street in April 2026, alongside a USD 1 billion equity investment, underscoring how financial services buyers are committing to dedicated AI infrastructure at scale.[3]CoreWeave, “Jane Street Signs USD 6 Billion AI Cloud Agreement With CoreWeave,” CoreWeave, wf.coreweave.com NVIDIA’s January 2026 USD 2.0 billion private placement investment in CoreWeave extended that strategic tie and pushed vertical alignment further into cloud delivery. Oracle is also gaining traction by emphasizing low-latency cluster design, which shows that architecture choices can still win accounts even in a market led by larger brands. These moves indicate that the AI Infrastructure-as-a-Service market rewards both capital access and technical differentiation.

Competitive white space remains strongest in sovereign AI cloud services, orchestration software, and greenfield regional build-outs. Providers that can deliver true technical sovereignty, rather than simple regional hosting, are better placed in government and regulated enterprise tenders. The orchestration layer is also still open, because customers increasingly want multi-model serving, fleet optimization, and better workload portability across hardware types. Smaller providers such as TensorWave, Genesis Cloud, and FluidStack are carving out positions through AMD access, European footprints, or marketplace-style capacity models. This keeps the AI Infrastructure-as-a-Service market moderately concentrated rather than closed, because platform scale matters, but specialized providers are still shaping how enterprise demand gets served.

AI Infrastructure-as-a-Service Industry Leaders

CoreWeave, Inc.

Nebius Group N.V.

Lambda, Inc.

Crusoe Energy Systems LLC

Vultr Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Lenovo reported an AI server backlog of USD 21 billion, with HBM shortages cited as the primary constraint on fulfillment timelines, underscoring the structural supply limitations facing AI IaaS capacity expansion industry wide.

- May 2026: Core Scientific announced the acquisition of 265 acres in Hunt County, Texas, near Dallas, supporting up to 285 MW of leasable AI data center capacity, as part of its ongoing expansion program for CoreWeave infrastructure.

- May 2026: Akamai published survey data showing 50% of enterprise AI deployments fail to meet latency SLAs at peak load, reinforcing urgency for edge-distributed AI IaaS architectures that complement centralized cloud GPU clusters.

- April 2026: CoreWeave closed a USD 8.5 billion delayed draw term loan facility, DDTL 4.0, receiving investment-grade ratings of A3 from Moody's and A low from DBRS, the first GPU-backed financing structure to achieve investment-grade status globally. The facility enabled CoreWeave to borrow up to USD 7.5 billion initially, accelerating infrastructure expansion to meet growing enterprise backlog.

Global AI Infrastructure-as-a-Service Market Report Scope

AI Infrastructure-as-a-Service refers to cloud-based infrastructure solutions that provide the computing power, storage, networking, and software environments required to develop, train, deploy, and manage artificial intelligence workloads. The scope of the report covers the AI Infrastructure-as-a-Service market, including key infrastructure components, deployment models, end-user industries, and geographic regions. The report analyzes market trends, growth drivers, challenges, competitive landscape, and opportunities during the study period.

The AI Infrastructure-as-a-Service Market Report is Segmented by Infrastructure Type (AI Compute Infrastructure, AI Storage Infrastructure, AI Networking Infrastructure, and AI Infrastructure Management and Orchestration), Workload Type (Model Training and Fine-Tuning, Model Inference and Serving, AI Data Processing and Analytics, and Other AI Workloads), Deployment Mode (Public Cloud, Managed Private Cloud, and Hybrid Cloud), Customer Organization Size (Large Enterprises, Small and Medium Enterprises, and Government, Research, and Educational Organizations), End-Use (IT, Cloud, SaaS, and Digital Services, Telecommunications, BFSI, Healthcare and Life Sciences, Automotive and Mobility, and Other End-Use Industries), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| AI Compute Infrastructure |

| AI Storage Infrastructure |

| AI Networking Infrastructure |

| AI Infrastructure Management and Orchestration |

| Model Training and Fine-Tuning |

| Model Inference and Serving |

| AI Data Processing and Analytics |

| Other AI Workloads |

| Public Cloud |

| Managed Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Government, Research, and Educational Organizations |

| IT, Cloud, SaaS, and Digital Services |

| Telecommunications |

| BFSI |

| Healthcare and Life Sciences |

| Automotive and Mobility |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Infrastructure Type | AI Compute Infrastructure | |

| AI Storage Infrastructure | ||

| AI Networking Infrastructure | ||

| AI Infrastructure Management and Orchestration | ||

| By Workload Type | Model Training and Fine-Tuning | |

| Model Inference and Serving | ||

| AI Data Processing and Analytics | ||

| Other AI Workloads | ||

| By Deployment Mode | Public Cloud | |

| Managed Private Cloud | ||

| Hybrid Cloud | ||

| By Customer Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| Government, Research, and Educational Organizations | ||

| By End-Use Industry | IT, Cloud, SaaS, and Digital Services | |

| Telecommunications | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Automotive and Mobility | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the AI Infrastructure-as-a-Service space?

The AI Infrastructure-as-a-Service market size was USD 38.72 billion in 2025, stood at USD 70.91 billion in 2026, and is forecast to reach USD 279.94 billion by 2031 at a 31.60% CAGR.

Which infrastructure segment leads revenue in AI Infrastructure-as-a-Service?

AI Compute Infrastructure led with 72.53% of revenue in 2025 because GPU cluster rentals and accelerator access still account for the largest portion of customer spending.

Why is inference becoming more important than training for cloud AI platforms?

Production AI use is expanding faster than experimentation, and Model Inference and Serving is projected to grow at 32.45% CAGR through 2031 as more applications run continuously at scale.

Which deployment model is growing fastest for AI Infrastructure-as-a-Service?

Hybrid Cloud is the fastest-growing deployment mode, with a projected 31.93% CAGR through 2031, as enterprises balance regulated workloads with burst compute needs.

Which region is growing fastest for AI Infrastructure-as-a-Service?

Asia-Pacific is projected to grow at 32.84% CAGR through 2031, supported by rising regional capacity build-outs and expanding enterprise AI adoption.

Which end users are creating the next wave of demand?

Automotive and Mobility is the fastest-growing end-use segment at 32.46% CAGR, while broader adoption is also spreading across telecom, BFSI, healthcare, manufacturing, retail, energy, and agriculture.

Page last updated on: