AI In Telecommunication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

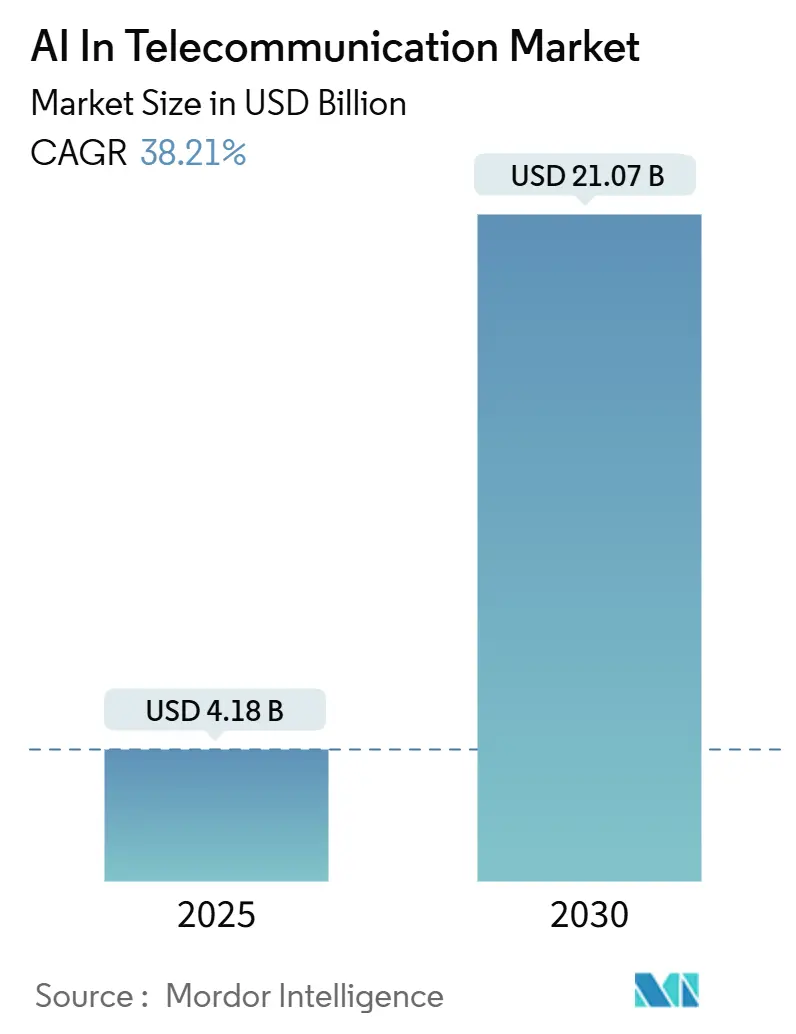

| Market Size (2025) | USD 4.18 Billion |

| Market Size (2030) | USD 21.07 Billion |

| Growth Rate (2025 - 2030) | 38.21% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

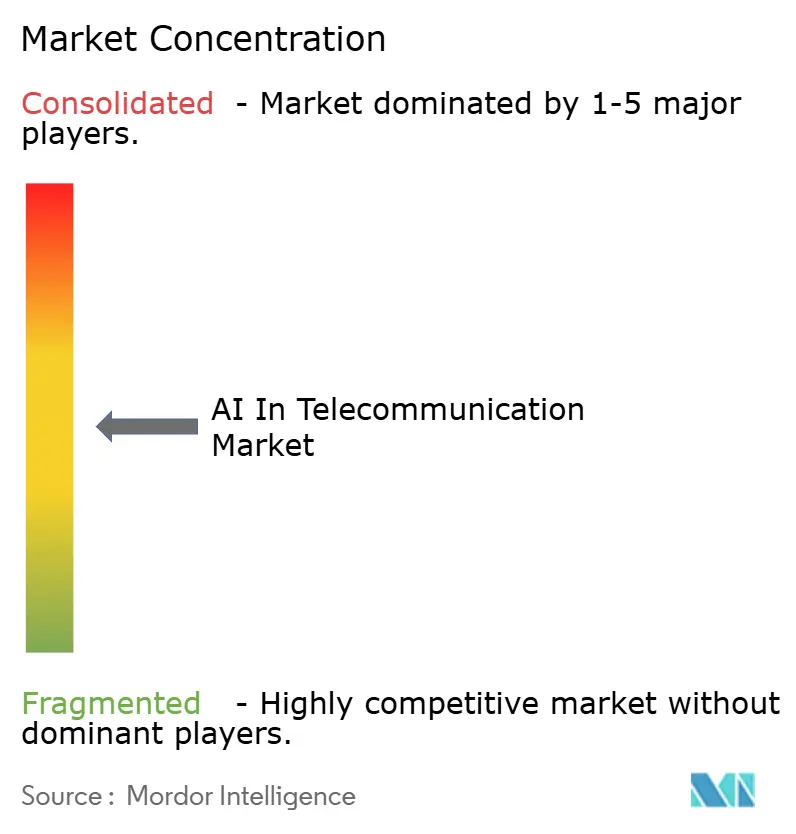

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Telecommunication Market Analysis by Mordor Intelligence

The AI In Telecommunication Market size is estimated at USD 4.18 billion in 2025, and is expected to reach USD 21.07 billion by 2030, at a CAGR of 38.21% during the forecast period (2025-2030).

This momentum signals a decisive shift from pilots toward scaled deployments that monetize network data, unlock automation savings, and create premium 5G service tiers. Hyperscalers are lowering entry barriers by offering pre-packaged MLOps stacks, while operators focus on spending on energy optimization, slice orchestration, and predictive maintenance. Regulatory clarity—most notably the EU AI Act—creates compliance costs but also establishes harmonized ground rules that encourage cross-border roll-outs. Intensifying competition from over-the-top (OTT) platforms forces carriers to match AI-driven quality-of-experience guarantees or risk revenue leakage to content providers. Venture funding continues to flow into niche startups that specialize in reinforcement learning and computer vision, accelerating the pace of product innovation and price pressure.

Key Report Takeaways

- By operator type, mobile network operators led with 53.88% AI in telecommunication market share in 2024, whereas OTT providers are projected to expand at a 48.86% CAGR through 2030.

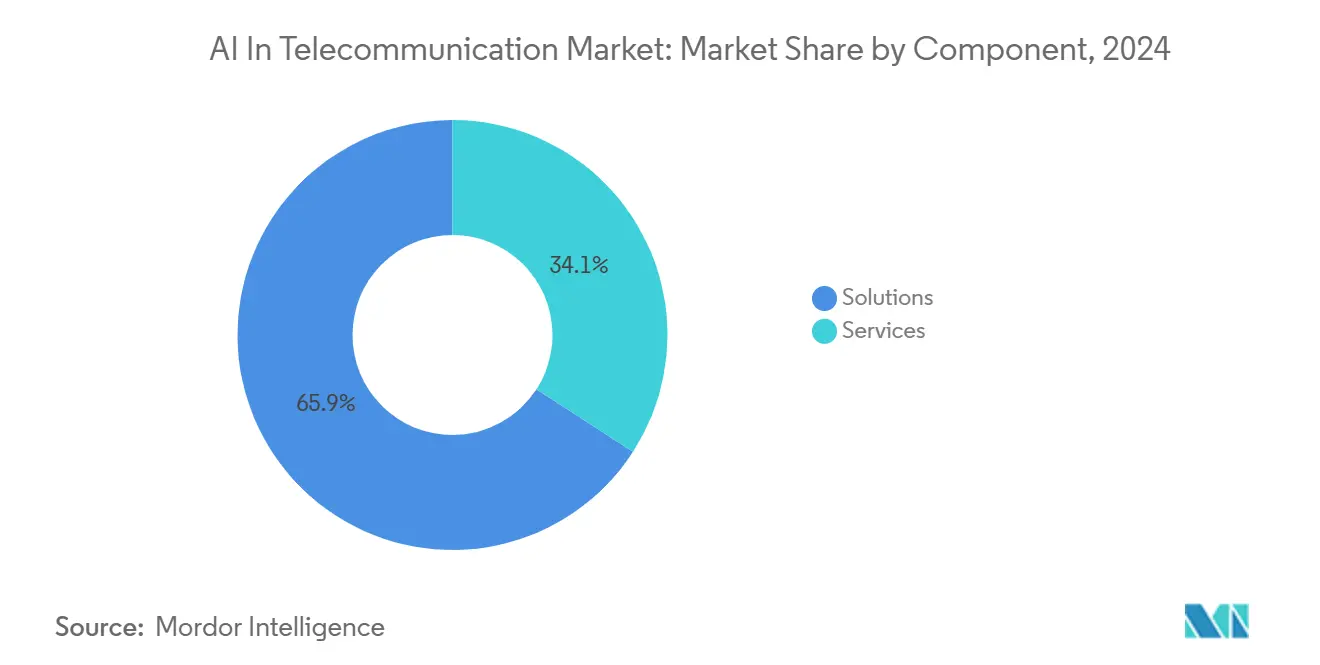

- By component, solutions captured 65.87% revenue in 2024, while services are forecast to grow at a 45.74% CAGR between 2025 and 2030.

- By deployment mode, cloud accounted for 58.48% of the AI in telecommunication market size in 2024 and is set to grow at 36.41% through 2030.

- By 2024, computer vision is expected to advance at a 46.59% CAGR, outpacing the 42.98% share held by machine-learning-centric spending.

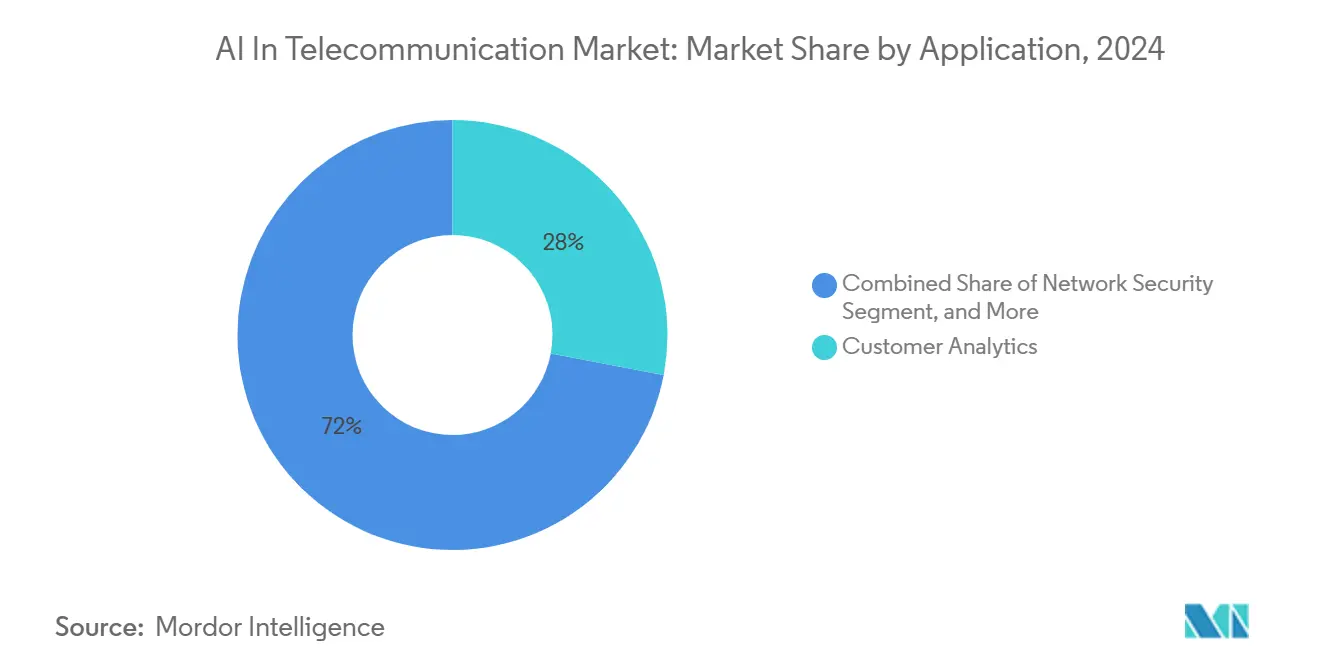

- By application, network security is projected to grow at 45.28% from 2025 to 2030, surpassing customer analytics, which accounted for 27.98% of the 2024 revenue.

- By geography, North America commanded 37.37% of 2024 revenue, while Asia-Pacific is on track for a 42.21% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Telecommunication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven O-RAN energy-efficiency mandates | +6.5% | Global, early uptake in Europe and North America | Medium term (2-4 years) |

| AI-native slice-SLA marketplaces for premium 5G services | +7.2% | APAC core, North America, spillover to Middle East | Short term (≤ 2 years) |

| Surge in AI-based anomaly detection after 5G SA roll-outs | +6.8% | Global, concentrated where 5G SA live | Short term (≤ 2 years) |

| Telco-specific foundation models accelerating 6G pilots | +5.5% | APAC, North America | Long term (≥ 4 years) |

| Real-time customer-data monetization platforms | +5.9% | North America, Europe, APAC Tier-1s | Medium term (2-4 years) |

| Edge-cloud convergence lowering AI TCO | +6.3% | Global, infrastructure dense in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Driven O-RAN Energy-Efficiency Mandates

Open radio access network initiatives now embed reinforcement-learning agents that predict traffic six hours ahead, power down radios during lulls, and still honor service-level agreements. Vodafone’s German trial achieved 15-20% energy savings and reduced diesel runtime at remote sites, translating sustainability targets into direct cost savings.[1]Vodafone Group, “AI-Driven Energy Trials in Germany,” vodafone.com The European Corporate Sustainability Reporting Directive and emerging FCC benchmarks heighten the urgency by linking emissions metrics to license obligations.

AI-Native Slice-SLA Marketplaces For Premium 5G Services

Deutsche Telekom’s live marketplace guarantees latency and throughput within 15-minute windows, mirroring cloud spot-instance economics and monetizing idle capacity.[2]Deutsche Telekom, “MagentaBusiness Network Slicing,” telekom.comSK Telecom cut slice-activation time from hours to minutes by automating policy validation and bearer configuration, enabling latency-critical use cases such as remote surgery. Gulf carriers are replicating the model for autonomous-vehicle fleets, signaling the global diffusion of this technology.

Surge in AI-Based Anomaly Detection After 5G SA Roll-Outs

Standalone cores replace monoliths with microservices, exposing fresh attack surfaces that rules-based firewalls miss. AT&T disclosed a 40% spike in anomalous session requests within weeks of SA activation, detected by machine-learning models that correlate control-plane telemetry in milliseconds. China Mobile now processes 10 TB of signaling data per day, blocking zero-day exploits through AI correlation with national threat feeds. Release 19 of 3GPP will standardize cross-operator security analytics, enabling the sharing of threat intelligence at scale.

Telco-Specific Foundation Models Accelerating 6G Pilots

NTT DOCOMO’s “Telco-GPT” compresses a decade of alarms and topology into a foundation model that speeds root-cause analysis by 60%.[3]NTT DOCOMO, “Telco-GPT Launch,” docomo.ne.jpSamsung’s U.S. research arm utilizes reinforcement learning to co-optimally balance beamforming and scheduling in terahertz bands, where coherence times are typically below 1 ms. South Korea’s ministry has earmarked KRW 50 billion to commercialize such models before 6G commercialization targets in 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithm-bias regulations raise compliance costs | -3.2% | Europe, North America | Short term (≤ 2 years) |

| Vendor lock-in fears around proprietary AI stacks | -2.8% | Global | Medium term (2-4 years) |

| Scarcity of telco-grade AI talent outside Tier-1s | -2.5% | Global | Long term (≥ 4 years) |

| CapEx squeeze amid delayed 5G ROI | -3.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Algorithm-Bias Regulations Raise Compliance Costs

The EU AI Act categorizes telecom AI as high-risk, requiring conformity assessments, risk-management files, and human oversight before it can be used in a live environment. Orange reported EUR 12 million in incremental compliance spend and a six-month delay to the dynamic spectrum-sharing rollout. California’s pending AI Accountability Act could bring similar measures to U.S. carriers, escalating legal diligence and slowing product cycles.

Vendor Lock-In Fears Around Proprietary AI Stacks

A TM Forum survey shows 68% of operators fear closed APIs will replicate past OSS silos, intensifying scrutiny of hyperscaler contracts. Telefónica now favors open-source frameworks like Kubeflow despite potential performance trade-offs. The Linux Foundation’s “Telco AI Toolkit” aims to standardize packaging and cut switching costs, encouraging multi-vendor ecosystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Platforms as Operators Outsource Complexity

Services are projected to climb at a 45.74% CAGR to 2030 as carriers outsource model training, drift detection, and governance, favoring outcome-based contracts. A five-year managed-AI deal with a European operator commits Infosys to uptime gains across 15,000 sites, illustrating carrier appetite for risk transfer. Solutions, while still larger in absolute terms, increasingly bundle pre-trained models and orchestration APIs, reflecting a pivot from licensing toward platform-as-a-service. IBM’s Watsonx.ai reduces cold-start time by shipping telecom-tuned foundation models, a draw for operators with sparse labeled data.

In the AI in telecommunication market, managed services resonate with Tier-2 carriers that lack data-science staff, while Tier-1s adopt hybrid models that pair internal centers of excellence with external specialty projects. Platform vendors differentiate through MLOps automation, native OSS/BSS connectors, and compliance toolkits that generate EU AI Act documentation on demand. This gap between desired outcomes and internal skills drives sustained services expansion.

By Deployment Mode: Hybrid Architectures Balance Latency and Economics

Cloud models secured 58.48% of 2024 revenue and are expected to expand at 36.41% through hyperscaler partnerships, such as Microsoft Azure for Operators, which offers GPU-rich templates that can be spun up in a day. Latency-critical inference—slice admission, fraud detection—still runs on edge servers co-located with user-plane functions. Hybrid architectures emerge as a compromise: training in central clouds and inference at distributed nodes to respect latency and data-sovereignty rules.

The AI in telecommunication market size for cloud workloads widens as public-cloud cost curves outpace on-premises depreciation. Yet TRAI’s data-localization consultations, along with similar rules in China, Russia, and the Gulf, ensure a baseline of domestic processing. Edge deployments gain from micro-data-center kits and inference accelerators that fit tower power envelopes, broadening use cases such as crowd-analytics at venues and predictive maintenance of rural sites.

By Technology: Computer Vision Surges on Maintenance and Assurance Use Cases

Computer vision, which is expected to expand at a 46.59% rate through 2030, underpins drone inspections that flag corroded antennas and vegetation encroachment, thereby reducing field visits by 40%. The AI in the telecommunication market share for machine learning remains highest, but growth moderates as penetration increases. Reinforcement learning targets spectrum allocation and energy control, while NLP powers generative chatbots that resolve billing in self-service portals.

DeepSig’s OmniPHY leverages deep reinforcement learning to adapt modulation schemes in high-mobility scenarios, resulting in 20-30% throughput improvement and demonstrating startup agility in niche algorithms. NEC’s visual-quality module streams client video frames to diagnose pixelation, mapping impairments to backhaul or RAN congestion, and prioritizing fixes. As 6G pilots test terahertz channels, vision and reinforcement learning become core technologies for ensuring beam alignment and ultra-low latency.

By Application: Network Security Accelerates Post-5G SA Migration

Network security grows at 45.28% as microservice-based cores widen attack surfaces. Cisco logged a 25% rise in service-provider security revenue on AI-aligned demand. Predictive maintenance, churn analytics, and slice assurance remain high-value applications; however, anomaly detection overtakes as operators race to comply with zero-trust guidelines.

The AI in telecommunication market size linked to customer analytics tapers as Tier-1 saturation nears, but SMB-focused analytics packages offer new volume. Fraud detection remains a pressing issue in emerging markets, where SIM-box fraud reportedly drains USD 4 billion annually. AI models analyzing call-detail patterns can now detect these schemes in seconds, replacing periodic audits.

By Operator Type: OTT Providers Bypass Carriers With Embedded Intelligence

OTT platforms integrate adaptive bitrate algorithms that predict congestion and pre-position content, eroding carrier differentiation. Netflix now routes streams to alternate peering points 30 minutes ahead, maintaining buffer-free playback. The AI in telecommunication market sees OTT growth at 48.86% CAGR as they internalize quality control, while carriers answer with AI-backed SLA guarantees in enterprise private 5G offers.

Mobile network operators still account for over half of the revenue but are shifting investment to AI-powered assurance to defend their value. Fixed-line ISPs deploy AI to anticipate fiber cuts associated with construction permits and weather, rerouting traffic preemptively. Satellite and MVNO operators are experimenting with AI for beam steering and wholesale rate optimization, signaling the broader diffusion of intelligent automation beyond traditional carriers.

Geography Analysis

North America, with 37.37% of 2024 revenue, benefits from deep cloud infrastructure, a robust talent pool, and regulatory nudges such as FCC incentives for AI-based interference mitigation. Canada’s CAD 50 million fund pairs carriers with universities on AI efficiency projects, while Mexico’s IFT consults on AI fraud-detection guidelines. Enterprise demand for AI-governed private 5G campuses accelerates carrier edge-cloud investments.

Asia-Pacific grows fastest at 42.21% CAGR, fueled by China’s 3.5 million 5G base stations, India’s INR 100 billion “Bharat 6G Vision,” and South Korea’s foundation-model collaborations. NTT DOCOMO’s January 2025 Telco-GPT launch and Australia’s fire-prediction pilots broaden regional adoption. Government funding, deep device penetration, and aggressive 6G timelines underpin sustained expansion.

Europe balances regulatory overhead with innovation. Deutsche Telekom, Orange, and Vodafone channel AI into energy optimization to meet Scope 3 disclosure rules. The EU AI Act introduces compliance cost yet yields a single market for AI telecom solutions. Ofcom’s transparency code aims to protect consumers without stifling experimentation. Russia subsidizes domestic AI stacks to reduce reliance on foreign vendors, signaling sovereignty themes.

Middle East and Africa present smaller bases but high growth. Dubai’s autonomous-fleet slice marketplace exemplifies smart-city adoption, while MTN’s continent-wide fraud-detection roll-out targets revenue leakage. Regulatory bodies from Nigeria to Brazil explore AI frameworks that balance innovation and consumer privacy, creating mixed compliance landscapes that vendors must navigate.

Competitive Landscape

The AI in telecommunication market features moderate fragmentation. Infrastructure majors embed AI into RAN and core, hyperscalers monetize GPU scale, startups tackle narrow use cases, and integrators offer outcome guarantees. Patent filings on AI-native orchestration rise, with Ericsson’s 2024 submission blending energy and QoS optimization. LF AI & Data’s toolkit pushes interoperability, lowering barriers for smaller players. White-space niches include rural energy optimization and satellite-terrestrial convergence.

Dominant vendors leverage installed-base intimacy, but open APIs erode lock-in. Startups partner with integrators to reach carriers wary of immature products. Pricing pressure intensifies as hyperscalers commoditize MLOps. Talent scarcity rewards vendors that bundle automation and compliance templates, helping carriers adopt AI without large data-science teams.

AI In Telecommunication Industry Leaders

International Business Machines Corporation

Microsoft Corporation

Google LLC

Intel Corporation

NVIDIA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: NTT DOCOMO launched “Telco-GPT,” cutting outage root-cause time by 60%.

- November 2024: Microsoft expanded Azure for Operators with USD 500 million in GPU capacity.

- October 2024: Ericsson and NVIDIA formed a joint venture for AI-accelerated RAN software.

- September 2024: SK Telecom deployed an AI slice orchestrator that activates slices in under 3 minutes.

Global AI In Telecommunication Market Report Scope

| Solutions | Software Tools |

| Platforms | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premises |

| Hybrid / Edge |

| Machine Learning |

| Deep Learning |

| Natural Language Processing |

| Computer Vision |

| Reinforcement Learning |

| Customer Analytics |

| Network Security |

| Network Optimization |

| Predictive Maintenance / Self-Diagnostics |

| Virtual Assistance / Chatbots |

| Fraud Management and Revenue Assurance |

| Others |

| Mobile Network Operators (MNOs) |

| Fixed / ISP |

| Virtual Network Operators (MVNO / Satellite) |

| Over-The-Top (OTT) Service Providers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Solutions | Software Tools | |

| Platforms | |||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Hybrid / Edge | |||

| By Technology | Machine Learning | ||

| Deep Learning | |||

| Natural Language Processing | |||

| Computer Vision | |||

| Reinforcement Learning | |||

| By Application | Customer Analytics | ||

| Network Security | |||

| Network Optimization | |||

| Predictive Maintenance / Self-Diagnostics | |||

| Virtual Assistance / Chatbots | |||

| Fraud Management and Revenue Assurance | |||

| Others | |||

| By Operator Type | Mobile Network Operators (MNOs) | ||

| Fixed / ISP | |||

| Virtual Network Operators (MVNO / Satellite) | |||

| Over-The-Top (OTT) Service Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the AI in telecommunication market in 2025?

It is valued at USD 4.18 billion and is projected to reach USD 21.07 billion by 2030, reflecting a 38.21% CAGR.

Which application is growing fastest within telecom AI?

Network security is expanding at a 45.28% CAGR as 5G standalone cores create new threat surfaces.

Why are OTT providers gaining ground?

Embedded AI lets OTT platforms predict congestion and pre-position content, delivering buffer-free experiences without relying on carrier optimizations.

What role does the EU AI Act play?

The Act classifies telecom AI as high-risk, requiring conformity assessments and documentation, which raises compliance costs but sets uniform rules across the bloc.

Which region shows the highest growth outlook?

Asia-Pacific is forecast to grow at a 42.21% CAGR through 2030, driven by aggressive 5G build-outs and government AI funding.

How are operators addressing energy efficiency?

AI-powered O-RAN agents that predict traffic and power down radios during low demand have demonstrated 15-20% energy savings in live trials.

Page last updated on: