AI In Revenue Cycle Management (RCM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.49 Billion |

| Market Size (2031) | USD 71.27 Billion |

| Growth Rate (2026 - 2031) | 27.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Revenue Cycle Management (RCM) Market Analysis by Mordor Intelligence

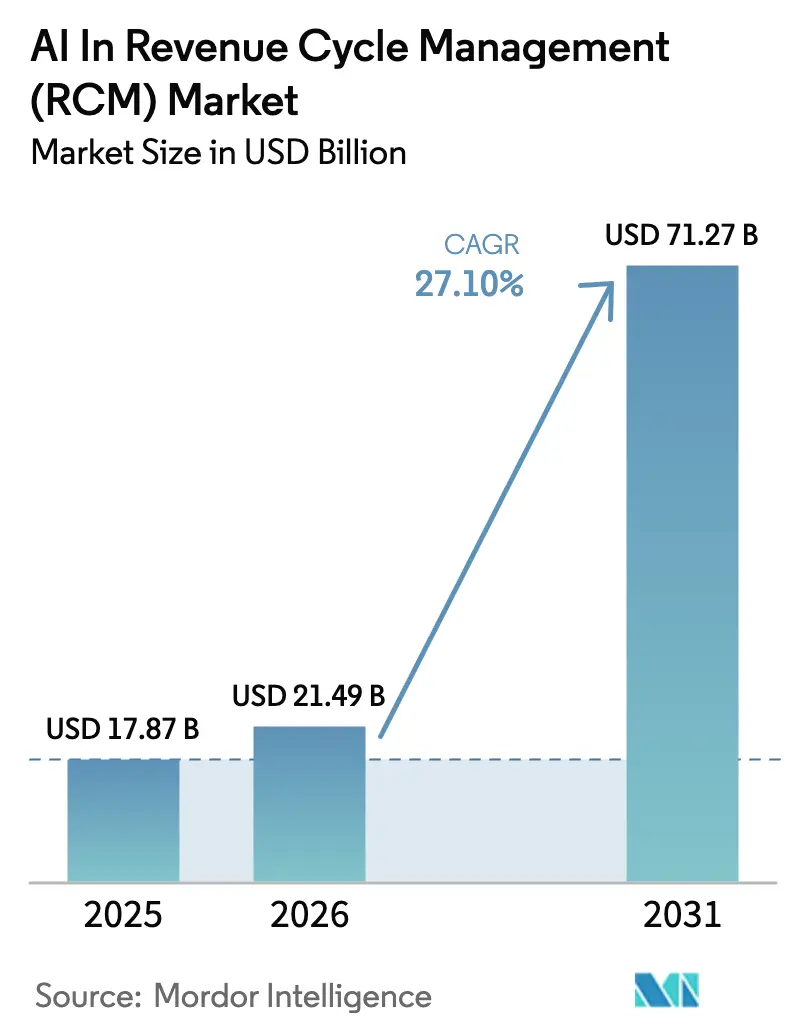

The AI in revenue cycle management market size is projected to expand from USD 17.87 billion in 2025 and USD 21.49 billion in 2026 to USD 71.27 billion by 2031, registering a CAGR of 27.10% between 2026 and 2031. Rapid digitization of payer–provider transactions, a wave of U.S. interoperability mandates, and rising denial volumes are accelerating platform deployments across hospitals and health plans. Mature electronic health record (EHR) vendors are embedding large-language-model (LLM) toolkits directly into clinical workflows, which intensifies pricing pressure on pure-play specialists but also widens the total addressable AI in revenue cycle management market by bringing first-time adopters into the ecosystem. Cloud hyperscalers are capturing infrastructure spend because elastic compute is required to parse unstructured clinical notes at scale, while zero-trust security architectures have become default bid requirements after the 2024 Change Healthcare ransomware incident. Investors remain confident, as shown by Waystar’s USD 968 million initial public offering in 2024 and a steady pipeline of Series C funding rounds across coding-automation start-ups. At the same time, compliance costs are rising: Colorado, California, and the European Union now require annual bias audits and impact assessments for AI-driven payment tools, a trend that favors vendors with strong governance programs.

Key Report Takeaways

- By component, software led with 68.34% revenue share in 2025; services are expanding at a 28.36% CAGR through 2031

- By deployment model, cloud-based solutions accounted for 73.46% of AI in the revenue cycle management market share in 2025 and are advancing at a 28.74% CAGR to 2031

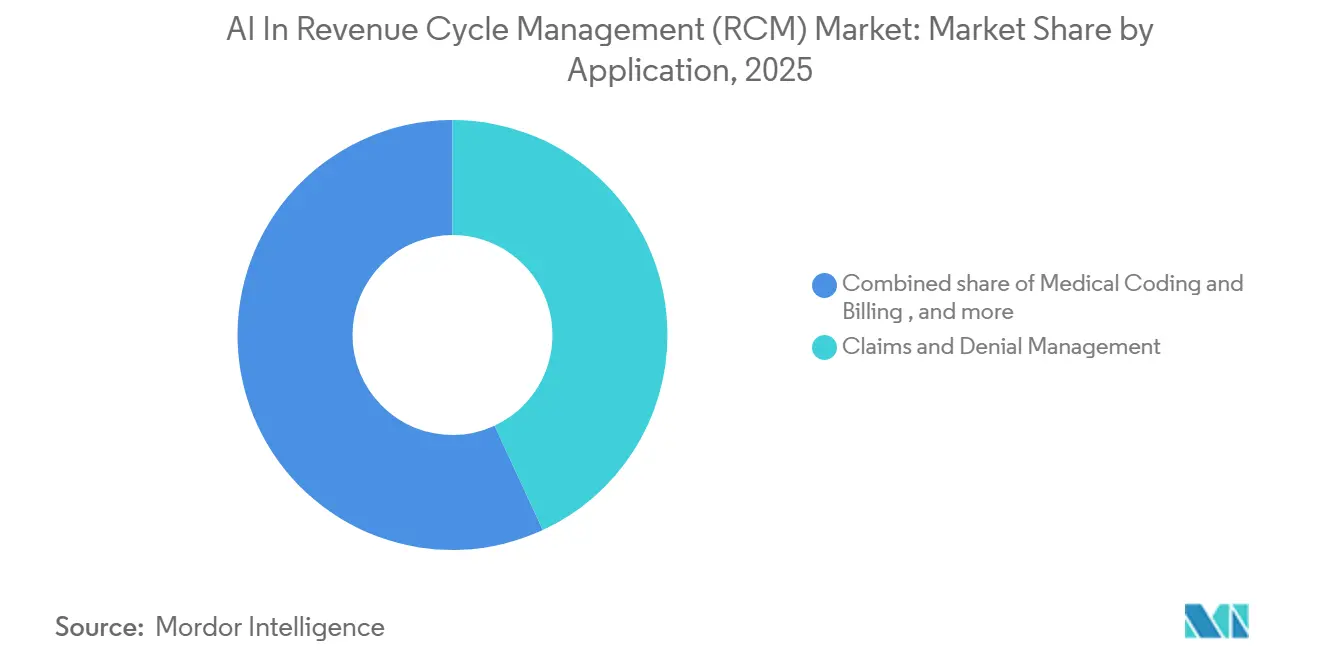

- By application, claims and denial management captured 43.13% spending in 2025, while patient access and eligibility verification is growing at a 27.53% CAGR through 2031

- By end user, hospitals and health systems generated 45.25% of 2025 revenue; payers represent the fastest-growing user group at a 27.68% CAGR

- By geography, North America held 42.33% share in 2025, yet Asia-Pacific is forecast to expand at a 29.84% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Revenue Cycle Management (RCM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising claim-volume and complexity accelerating AI adoption | +6.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Consumerization of healthcare increasing patient billing complexity | +4.2% | North America, Western Europe | Short term (≤ 2 years) |

| Shift toward value-based reimbursement models | +5.1% | North America, Australia, United Kingdom | Long term (≥ 4 years) |

| Regulatory push for price-transparency and clean-claim mandates | +3.9% | United States, European Union | Short term (≤ 2 years) |

| Generative-AI for autonomous prior-authorization approvals | +5.6% | North America, Asia-Pacific | Medium term (2-4 years) |

| Real-time payer API integration enabling instant benefits verification | +4.7% | United States, Canada, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Claim-Volume and Complexity Accelerating AI Adoption

U.S. healthcare providers process approximately 9 billion claims annually, with commercial payers rejecting 15-20% on first submission due to coding errors, missing documentation, or eligibility mismatches [1]Healthcare Financial Management Association, “2024 Revenue Cycle Survey,” hfma.org. The diagnosis code library grew to 72,000 entries under ICD-10, while procedure codes exceeded 10,000, so manual coders face a search space that few teams can master quickly. Proprietary payer edits now refresh quarterly, compelling providers to update rule sets that AI engines can ingest and deploy overnight. Early adopters report 30-40% drops in denial rates when machine-learning scrubbers flag errors before submission. These efficiencies translate into faster days-sales-outstanding and position AI as a must-have capability rather than a discretionary upgrade.

Consumerization of Healthcare Increasing Patient Billing Complexity

High-deductible health plans cover 29.3% of insured U.S. workers, shifting 30-35% of hospital revenue to patients, yet collection rates on those balances remain roughly 50-60% [2]Kaiser Family Foundation, “Employer Health Benefits Survey 2024,” kff.org. Providers therefore need accurate, real-time out-of-pocket estimates at registration in order to collect funds up front. AI platforms ingest machine-readable price files mandated by the Hospital Price Transparency Rule and return estimates in under three minutes, cutting front-desk time by two-thirds [3]Centers for Medicare & Medicaid Services, “Hospital Price Transparency Enforcement Update 2025,” cms.gov . Digital wallets and installment options embedded in patient portals have lifted upfront payments by as much as 60 percentage points. These gains make patient-access automation one of the fastest-growing application areas for AI in revenue cycle management.

Shift Toward Value-Based Reimbursement Models

The ACO REACH program expanded to 132 organizations caring for 13.7 million Medicare beneficiaries in 2025, requiring participants to manage total cost of care while meeting more than 40 quality metrics [4]CMS Innovation Center, “ACO REACH Model Participant List 2025,” innovation.cms.gov. Bundled payment models already cover 30% of Medicare surgical volume, so providers must predict episode costs within 2-3% accuracy to avoid losses. AI tools analyze historical claims, comorbidities, and regional pricing to forecast spend and surface high-risk patients for early intervention. Health systems that embedded these models have reported 15-25% reductions in episode costs while maintaining quality thresholds. As value-based contracts spread, predictive revenue-cycle modules become integral to financial sustainability.

Generative-AI for Autonomous Prior-Authorization Approvals

Physicians submit an average of 39 prior-authorizations each week, costing 13 staff hours and facing denial rates near 20%. Generative models now parse clinical notes, align diagnoses with payer rules, and auto-populate forms in under a minute, slashing manual workload. Pilot programs cut turnaround times from days to hours without raising denial percentages. Some clinicians worry that higher processing speed lets payers apply stricter criteria, yet early data show balanced gains for both sides. The prospect of same-day treatment starts makes autonomous prior-authorization one of the most compelling AI use cases for both providers and insurers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cybersecurity concerns for cloud AI | −3.2% | Global, heightened in United States and European Union | Short term (≤ 2 years) |

| High legacy-system integration costs | −2.8% | North America, Europe | Medium term (2-4 years) |

| Algorithmic bias triggering payer audit risks | −1.9% | United States, European Union | Medium term (2-4 years) |

| Emerging state-level AI governance limiting automated billing | −1.6% | United States (Colorado, California, Utah, Illinois) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cybersecurity Concerns for Cloud AI

A February 2024 ransomware attack on Change Healthcare shut down claims processing for more than 90 days and exposed protected data for 100 million individuals, saddling UnitedHealth Group with USD 872 million in remediation costs. The incident highlighted the systemic risk of centralized clearinghouses and made zero-trust architectures a contractual requirement for many providers. Procurement cycles now include detailed penetration testing and liability clauses, extending deal timelines by as much as a year. Cloud vendors respond with confidential-computing hardware and region-locked data stores, but these features raise infrastructure bills. Heightened security scrutiny therefore slows near-term adoption even as long-term demand remains intact.

Emerging State-Level AI Governance Limiting Automated Billing

Colorado’s SB 24-205, effective February 2026, requires annual impact assessments and consumer notices when AI influences billing decisions, while California’s AB 2013 carries fines of USD 2 500 per violation for undisclosed automation. Utah demands explicit patient consent before AI handles payment tasks, and Illinois has similar draft legislation. Vendors must now build jurisdiction-specific consent flows, versioned audit logs, and policy engines, fragmenting product roadmaps. The resulting complexity raises development costs by 20-30% and discourages nationwide launches. Providers operating in multiple states face a compliance mosaic that can delay AI rollouts despite clear financial benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Narrowing the Gap With Software

Services captured a 28.36% CAGR from 2026 to 2031, while software retained a 68.34% slice of 2025 revenue. This divergence reveals a structural shift in the AI in revenue cycle management market size for advisory and managed offerings, because hospitals lack in-house data scientists and interface engineers. Service vendors orchestrate model training, change management, and bias audits, roles that internal IT teams rarely staff at scale.

Software retains primacy because recurring subscriptions and per-claim pricing anchor revenue visibility. Embedded AI modules inside Epic, Oracle Health, and athenahealth automate claim scrubbing and denial prediction. Consumption-based contracts blur lines between software and services as vendors bundle continuous tuning and performance guarantees. Over time, hybrid deals in which vendors charge per dollar collected could reshape the AI in revenue cycle management market share metrics that investors track.

By Deployment Model: Cloud Growth Outpaces On-Premise

Cloud deployments held 73.46% share in 2025 and are expanding at a 28.74% CAGR. Elastic compute is indispensable for LLM inference on unstructured notes, and cloud marketplaces simplify procurement. Waystar’s Google Cloud partnership cut infrastructure costs by 40% and showcases how multitenant models fuel the AI in revenue cycle management market size for hyperscalers.

On-premise and hybrid strategies persist among security-sensitive integrated delivery networks. These operators route anonymized training data to cloud accelerators but keep protected health information in local clusters, a pattern that adds 15-20% to total cost of ownership. Confidential-computing chipsets are maturing and may accelerate cloud uptake after 2027. Until then, compliance anxieties slow wholesale migrations and create a two-tier market.

By Application: Patient Access Emerges as a Strategic Priority

Claims and denial management dominated spending with 43.13% share in 2025, yet patient-access tools are growing at a 27.53% CAGR as deductibles climb. Accurate estimates eliminate surprise bills and lift Hospital Consumer Assessment of Healthcare Providers and Systems scores, outcomes that carry reimbursement stakes. Upfront collections rose at health systems that embedded FHIR-based eligibility checks inside patient portals.

Medical-coding engines reach 90%+ precision and reduce certified coder workloads by half, freeing specialists for complex audits. Ambient documentation tools cut physician clerical time from two hours to 30 minutes daily and raise risk-adjusted revenue. Revenue-integrity analytics compare remittances against contract terms and reclaim underpayments. These extensions widen the functional footprint and sustain the AI in revenue cycle management market.

By End User: Payers Pursue Administrative Lift

Hospitals and health systems delivered 45.25% of 2025 revenue, but payers are accelerating adoption at a 27.68% CAGR. Generative AI shrinks prior-authorization turnaround to 14 hours at scale, and autonomous adjudication chips away at medical loss ratios. Physician groups, especially practices with under 10 clinicians, subscribe to turnkey RCM stacks priced at USD 3–8 per encounter, achieving enterprise-grade collection rates without expanding headcount.

Ambulatory surgical centers seek AI modules that reconcile bundled case-rates, while long-term care and home-health agencies trail due to slim margins. Nevertheless, payer investments will keep reshaping competitive dynamics and redirect product roadmaps in the AI in revenue cycle management industry.

Geography Analysis

North America commanded 42.33% of 2025 revenue. U.S. interoperability mandates and a USD 4.5 trillion spend base create fertile soil for AI pilots, and Canada is piloting automated adjudication to trim administrative overhead in single-payer settings. Mexican social insurance networks plan Spanish-language claim scrubbers that extend the AI in revenue cycle management market to Latin America.

Asia-Pacific is advancing at 29.84% CAGR, buoyed by India’s National Digital Health Mission, Japan’s long-term care automation grants, and Australia’s My Health Record. Many Asian hospitals skip legacy mainframes altogether, so they deploy cloud-native RCM stacks from day one, which accelerates booking cycles for vendors and enlarges the AI in revenue cycle management market size in the region.

Europe adopts steadily despite tight budgets. The EU AI Act raises compliance thresholds that advantage well-capitalized players, while Germany, the UK, and France seek to offset nurse shortages with coding robotics. The Middle East, particularly the GCC states, is investing in AI-enabled smart hospitals as part of economic diversification strategies, with Saudi Arabia's Vision 2030 allocating USD 65 billion for healthcare infrastructure that includes RCM automation. GCC states allocate oil surplus toward smart hospitals that include revenue-cycle AI, and South Africa’s private hospital chains pilot coding assistants to mitigate certified coder shortages.

Competitive Landscape

The sector is moderately fragmented. The top five providers account for a significant portion of global revenue, which places the AI in the revenue cycle management market at a mid-level concentration. Epic, Oracle Health, and athenahealth exploit installed bases to upsell embedded RCM AI. Waystar, R1 RCM, and AKASA focus on denial prediction and autonomous coding.

Hybrid offerings that bundle software, services, and revenue-sharing align incentives with clients and create sticky, multi-year contracts. Compliance readiness, such as SOC 2 and HITRUST accreditation plus bias-audit toolkits, has become a competitive wedge.

Exit events signal maturation. Waystar listed publicly in 2024, raising USD 968 million, and R1 RCM acquired Acclara for USD 95 million to ingest physician-coding expertise. Conversely, Olive AI’s 2023 wind-down highlighted execution risks of scaling across heterogeneous IT estates. Winners will pair model accuracy with bulletproof governance, preserving gross-margin headroom even as open-source LLMs compress price points.

AI In Revenue Cycle Management (RCM) Industry Leaders

AKASA

athenahealth

Epic Systems

Oracle Health

Waystar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Veradigm launched an AI-enabled analytics module for its Revenue Cycle Services platform, giving independent practices real-time financial insights.

- June 2025: FinThrive introduced Agentic AI within the revenue cycle management platform, which deploys digital agents to optimize workflows and accelerate revenue recovery.

- May 2025: Smarter Technologies unveiled an AI-powered revenue automation suite that blends advanced analytics with operational services for hospitals.

Global AI In Revenue Cycle Management (RCM) Market Report Scope

As per the scope of the report, AI in revenue cycle management (RCM) refers to the use of artificial intelligence technologies, such as machine learning, natural language processing, predictive analytics, and automation, to optimize and streamline financial processes in healthcare. It enhances tasks such as patient eligibility verification, medical coding, claims submission, denial management, payment posting, and revenue forecasting by reducing manual effort, minimizing errors, accelerating reimbursements, and improving overall financial performance for healthcare providers.

The AI revenue cycle management (RCM) market is segmented into component, deployment model, application, end user, and geography. By component, the market is segmented into software and services. By deployment model, the market is segmented into cloud-based and on-premise. By application, the market is segmented into claims & denial management, medical coding & billing, patient access & eligibility verification, clinical documentation improvement (CDI), and others. By end user, the market is segmented into hospitals & health systems, physician practices, ambulatory surgical centers, payers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Cloud-based |

| On-premise |

| Claims & Denial Management |

| Medical Coding & Billing |

| Patient Access & Eligibility Verification |

| Clinical Documentation Improvement (CDI) |

| Others |

| Hospitals & Health Systems |

| Physician Practices |

| Ambulatory Surgical Centers |

| Payers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-based | |

| On-premise | ||

| By Application | Claims & Denial Management | |

| Medical Coding & Billing | ||

| Patient Access & Eligibility Verification | ||

| Clinical Documentation Improvement (CDI) | ||

| Others | ||

| By End User | Hospitals & Health Systems | |

| Physician Practices | ||

| Ambulatory Surgical Centers | ||

| Payers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the AI in revenue cycle management market expected to grow through 2031?

It is forecast to climb from USD 21.49 billion in 2026 to USD 71.27 billion by 2031 at a 27.10% CAGR.

Which segment is expanding quickest within the AI in revenue cycle management market?

Cloud-based solutions are scaling at a 28.74% CAGR driven by the demand for cost efficiency, scalability, and streamlined revenue cycle operations.

Why are payers investing heavily in AI revenue cycle platforms?

Autonomous adjudication and faster prior-authorization decisions lower medical loss ratios, driving a 27.68% CAGR for payer spend.

Which region offers the most untapped growth potential?

Asia-Pacific leads with a 29.84% CAGR because many hospitals adopt cloud-native RCM stacks without legacy constraints.

Page last updated on: