AI In Procurement Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.99 Billion |

| Market Size (2031) | USD 19.74 Billion |

| Growth Rate (2026 - 2031) | 31.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Procurement Platforms Market Analysis by Mordor Intelligence

The AI In Procurement Platforms Market size is projected to expand from USD 3.79 billion in 2025 and USD 4.99 billion in 2026 to USD 19.74 billion by 2031, registering a CAGR of 31.67% between 2026 to 2031.

The AI in procurement platforms market is evolving as enterprises demand tools that act on approved workflows rather than just providing static reports or dashboards. Factors such as cloud connectivity, stricter compliance requirements, and increased supplier risk exposure are driving vendors to redesign source-to-pay platforms with real-time data access and auditable decision support. Recent updates from SAP, Coupa, and GEP highlight the rapid shift toward AI-native workflows. The market is attracting investments as the focus extends beyond efficiency to include control, resilience, and policy enforcement across large supplier networks. Rising competition is evident as established suite vendors accelerate AI releases, while specialized players target high-value workflows like negotiation, supplier intelligence, and contract intelligence, leaving limited opportunities for underprepared vendors.

Key Report Takeaways

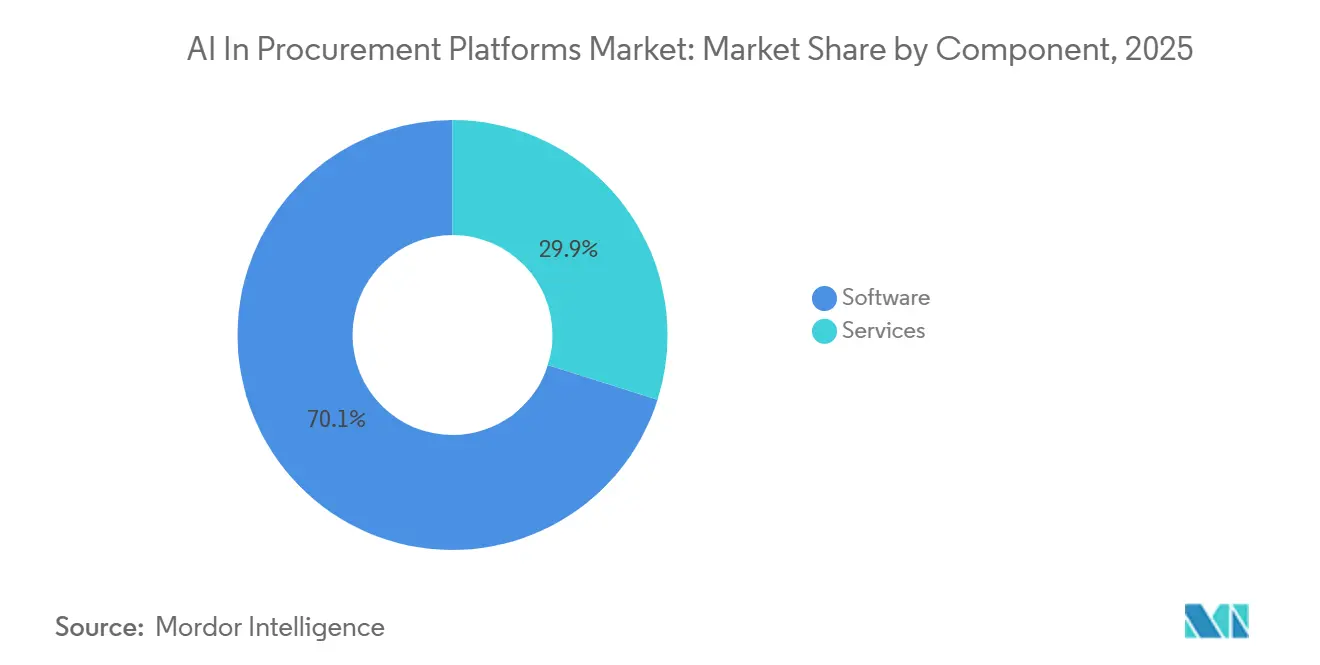

- By component, software held 70.14% revenue share in 2025, while services is projected to expand at a 32.88% CAGR through 2031.

- By deployment, cloud-based deployment held 72.3% share in 2025, while on-premise deployment is projected to grow at a 31.99% CAGR through 2031.

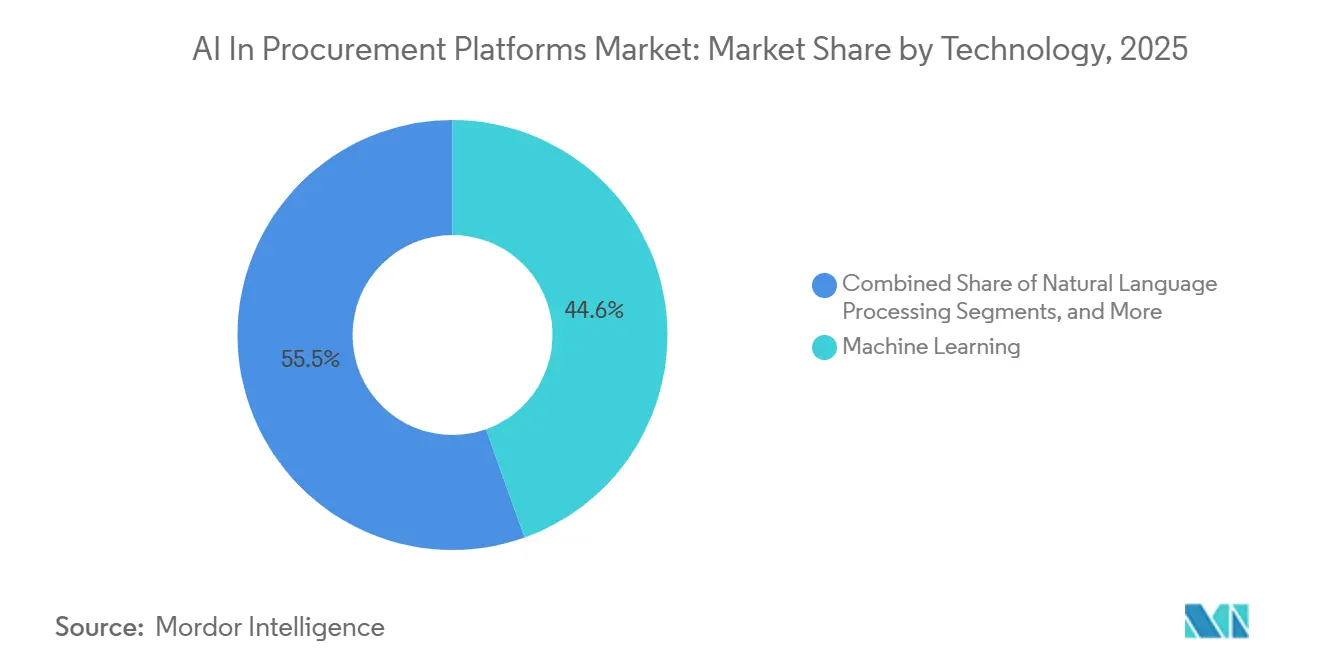

- By technology, machine learning held 44.55% share in 2025, while natural language processing is projected to grow at a 32.34% CAGR from 2026 to 2031.

- By application, Supplier Management & Discovery held 25.45% share in 2025, while Risk Management & Predictive Analytics is projected to grow at a 33.56% CAGR through 2031.

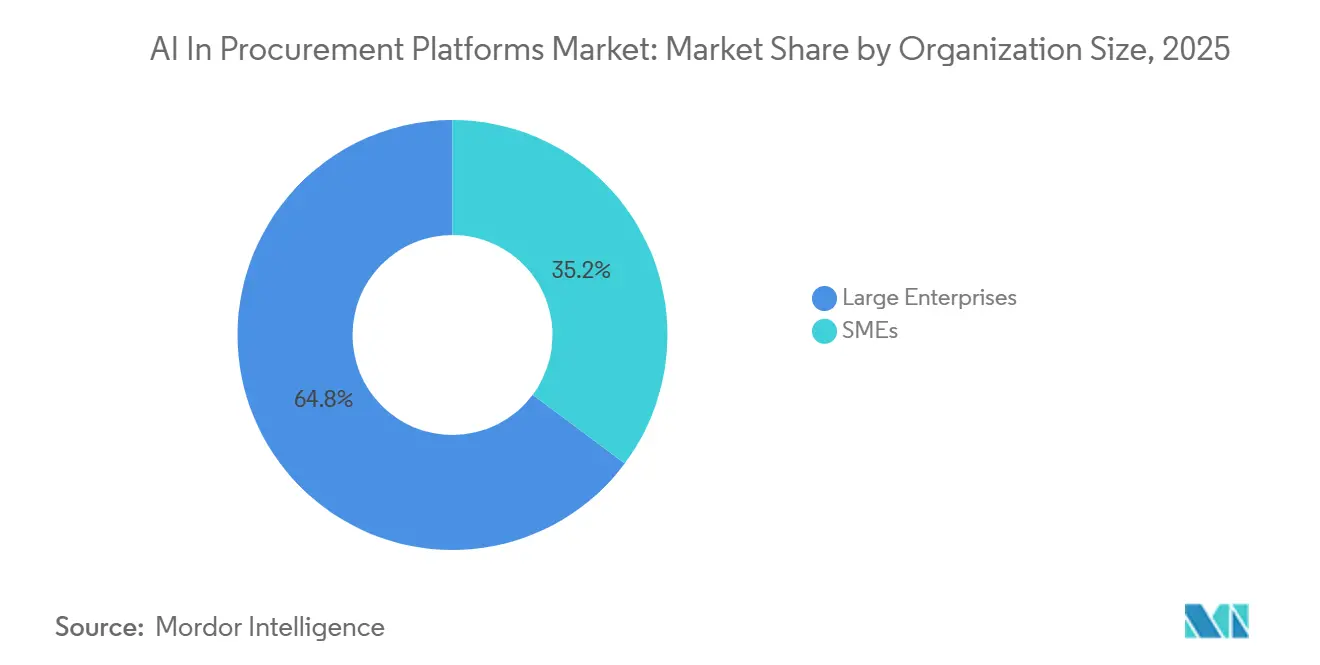

- By organization size, large enterprises held 64.80% share in 2025, while SMEs are projected to expand at a 33.67% CAGR through 2031.

- By end-use industry, manufacturing held 35.75% share in 2025, while healthcare and life sciences is projected to grow at a 33.98% CAGR through 2031.

- By geography, North America held 41.20% share in 2025, while Asia-Pacific is projected to expand at a 34.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Procurement Platforms Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cost-takeout and spend-visibility mandates | +5.2% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| Supplier risk and resilience management | +4.8% | Global, APAC core for supply chain density, MEA for raw-material sourcing | Medium term (2-4 years) |

| Cloud-native source-to-pay modernization | +4.5% | North America, Western Europe, with spillover to APAC and Latin America | Short term (≤ 2 years), Medium term (2-4 years) |

| Agentic ai for tail-spend automation | +6.1% | Global, with early-adopter clusters in North America, UK, and ANZ | Short term (≤ 2 years) |

| Integration of generative AI and predictive analytics | +5.8% | Global, highest in markets with mature ERP ecosystems such as the US, Germany, and Japan | Medium term (2-4 years) |

| Scope 3 and supplier compliance data burden | +3.2% | EU core, with spillover to North America and ANZ through multinational supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Agentic AI for Tail-Spend Automation Redefines Savings Baselines

Agentic AI is transforming the procurement platforms market by automating tail-spend tasks that were previously manual and fragmented. This shift is driving the focus from basic workflow support to systems capable of executing approved sourcing and negotiation actions across diverse supplier bases. In 2025, Pactum reported significant growth in spend managed by its AI agents and annual recurring revenue, reflecting the increasing adoption of autonomous procurement workflows.[1]Pactum, “Pactum Secures USD 54 Million in Series C Funding to Scale Agentic AI in Procurement,” Pactum, pactum.com Similarly, Coupa launched new solutions in 2026 to accelerate agentic AI value delivery, marking a shift from experimentation to scaled execution.[2]Coupa Software, “Coupa Launches Coupa Compose and Catalyst to Accelerate Agentic AI Value and Delivery at Inspire 2026,” PR Newswire, prnewswire.com Vendors enabling automated actions from approved policies are gaining traction, while suppliers lagging in digital readiness face mounting pressure.

Scope 3 and Supplier Compliance Data Burden Drives Platform Stickiness

Procurement platforms are becoming critical as they integrate supplier compliance data, audit records, and sustainability reporting workflows. Buyers now view these platforms as essential for managing compliance through continuous data capture, validation, and exception handling across supplier networks. Icertis expanded its partnership with SAP in 2026 to deliver AI-driven contract intelligence, highlighting the demand for embedded compliance logic in procurement. Consolidating emissions data, certifications, and contract obligations in one system increases switching costs for customers. Vendors building unified data pipelines early are gaining retention advantages as customers avoid recreating audit trails and reporting logic on new platforms.

Integration of Generative AI and Predictive Analytics Compresses Sourcing Cycles

Sourcing cycles are compressing as generative AI integrates into sourcing, intake, and contract workflows. SAP introduced its next-gen SAP Ariba in 2026, incorporating advanced bid analysis and intake management features to streamline procurement requests. JAGGAER launched JAI, a multilingual conversational interface, to address procurement-related queries, making such tools practical for daily operations. These advancements enable faster transitions from request intake to contract action, allowing teams with clean data and strong workflows to respond quickly to supply changes and pricing opportunities. Organizations with fragmented data systems risk falling behind as integrated capabilities become standard.

Cloud-Native Source-to-Pay Modernization Displaces On-Premise Legacy Systems

The procurement platforms market is increasingly favoring cloud-native architectures due to their ability to support live connections across ERP systems, supplier networks, and finance platforms. GEP’s Quantum Intelligence platform reduces deployment time for source-to-pay connections, showcasing the efficiency of modern cloud designs. SAP’s 2026 rebuild of Ariba further emphasizes the shift toward connected cloud foundations.[3]SAP News, “SAP Unveils the Autonomous Enterprise,” SAP News Center, news.sap.com Centralized cloud environments simplify updates and enhance scalability, widening the gap with legacy systems that require complex integrations. Cloud adoption is now seen as a strategic model for faster value realization and scalable automation in procurement.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data quality and interoperability challenges | -3.1% | Global, most acute in fragmented mid-market and APAC markets with legacy ERP diversity | Medium term (2-4 years) |

| Concern regarding cybersecurity | -2.4% | Global, heightened in BFSI and healthcare, particularly under GDPR and HIPAA frameworks | Short term (≤ 2 years), Medium term (2-4 years) |

| High implementation and integration cost | -2.8% | Most pronounced in SME and government segments, with spillover to mid-tier enterprise globally | Medium term (2-4 years) |

| Autonomous buying governance and liability limits | -1.9% | EU, US, and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Quality and Interoperability Challenges Constrain AI Agent Reliability

The AI in procurement platforms market faces challenges due to unclean and disconnected procurement data. Disparate systems housing supplier records, contracts, item masters, and spend categories reduce AI output reliability and delay deployments. A 2025 survey by MonotaRO of 407 procurement managers from Japanese firms with annual revenues above JPY 10 billion found that 70% had not implemented generative AI in procurement operations, citing data quality and availability as key barriers. The market's success depends on customers' ability to harmonize data across business units and regions, a task often underestimated, leading to extended payback periods.

Autonomous Buying Governance and Liability Limits Create Structural Adoption Ceilings

Governance constraints limit the adoption of AI in procurement platforms as buyers seek automation but remain cautious about removing human accountability in critical purchasing decisions. This creates a ceiling for fully autonomous buying in areas involving supplier risk, complex contracts, policy exceptions, or public accountability. Vendors are focusing on enhancing oversight features like contract intelligence, intake controls, and role-based workflows. While adoption is expected to grow in phases, fully autonomous decision-making will remain limited in many procurement scenarios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals a Platform-to-Partnership Shift

In 2025, software accounted for 70.14% of revenue, reflecting the AI in procurement platforms market's reliance on platform licensing and suite adoption among large enterprises. Vendors like SAP, Oracle, Coupa, and JAGGAER have built a strong software base through extensive source-to-pay deployments, shaping buyer entry into the market. The software segment highlights the demand for integrated systems managing sourcing, supplier management, spend visibility, contracts, and policy enforcement.

Services are projected to grow at a 32.88% CAGR from 2026 to 2031, making it the fastest-growing component. This growth reflects the need for process design, data preparation, system integration, and change management alongside software activation. Coupa's launch of Catalyst in May 2026, an AI transformation service, underscores the shift toward a platform-plus-delivery model, where delivery support becomes a strategic revenue stream.

By Deployment: Cloud Dominance Deepens as Security Certifications Raise the Bar

Cloud-based deployment held 72.3% of the market share in 2025, emphasizing the preference for scalable and connected operating models. Cloud solutions enable seamless data transfer across ERP systems, supplier portals, and finance tools without lengthy upgrade cycles. This architecture supports AI features reliant on real-time data and ensures faster access to new functionalities compared to on-premise systems.

On-premise deployment is forecast to grow at a 31.99% CAGR from 2026 to 2031, though its use cases remain limited. GEP highlights that its cloud infrastructure significantly reduces deployment time for source-to-pay connections, further solidifying the operational advantages of cloud solutions.

By Technology: Machine Learning Anchors the Stack, NLP Redefines the Interface

Machine learning held a 44.55% share of the technology segment in 2025, reflecting its critical role in classification, forecasting, scoring, and anomaly detection. These capabilities support core procurement tasks like spend categorization and supplier assessment, forming the foundation for advanced AI functions. The market continues to rely on proven analytical engines while integrating newer user interfaces.

Natural language processing is projected to grow at a 32.34% CAGR from 2026 to 2031, driven by its applications in conversational intake, contract intelligence, and multilingual query support. JAGGAER's launch of JAI in May 2026, with support for 28 languages, highlights the growing adoption of NLP as a practical procurement interface.

By Application: Risk Management Accelerates as Supplier Exposure Broadens

Supplier Management & Discovery accounted for 25.45% of the application segment in 2025, emphasizing its foundational role in supplier visibility and data quality. Accurate supplier records and performance data are essential for downstream processes like sourcing and contracts, making supplier data a key value driver in the market.

Risk Management & Predictive Analytics is forecast to grow at a 33.56% CAGR from 2026 to 2031, reflecting its increasing importance in resilience, compliance, and executive oversight. Supplier risk is now a central focus, driving demand for predictive analytics in procurement.

By Organization Size: SME Adoption Closes the Gap Through Modular Deployment

Large enterprises held 64,80% of the market share in 2025, driven by their ability to invest in multi-year source-to-pay programs and support data integration and governance. Their category volume justifies automation across sourcing, contracting, and supplier onboarding, shaping the early market landscape.

SMEs are projected to grow at a 33.67% CAGR from 2026 to 2031, supported by modular SaaS pricing, faster implementation models, and targeted AI features. SAP's GROW positioning and Coupa's modular approach lower entry barriers for mid-market buyers, expanding the addressable market.

By End-use Industry: Healthcare Outpaces All Verticals as Compliance Costs Intensify

Manufacturing held 35.75% of the market share in 2025, reflecting its reliance on structured sourcing and predictive support due to dense supplier networks and high direct-material spending. The sector's need to align supplier intelligence with demand and pricing makes it a key driver of procurement AI adoption.

Healthcare and life sciences are projected to grow at a 33.98% CAGR from 2026 to 2031, driven by traceability, drug supply risk management, and stronger control over regulated buying environments. Institutional support for standardized and technology-enabled procurement processes further accelerates growth in this sector.

Geography Analysis

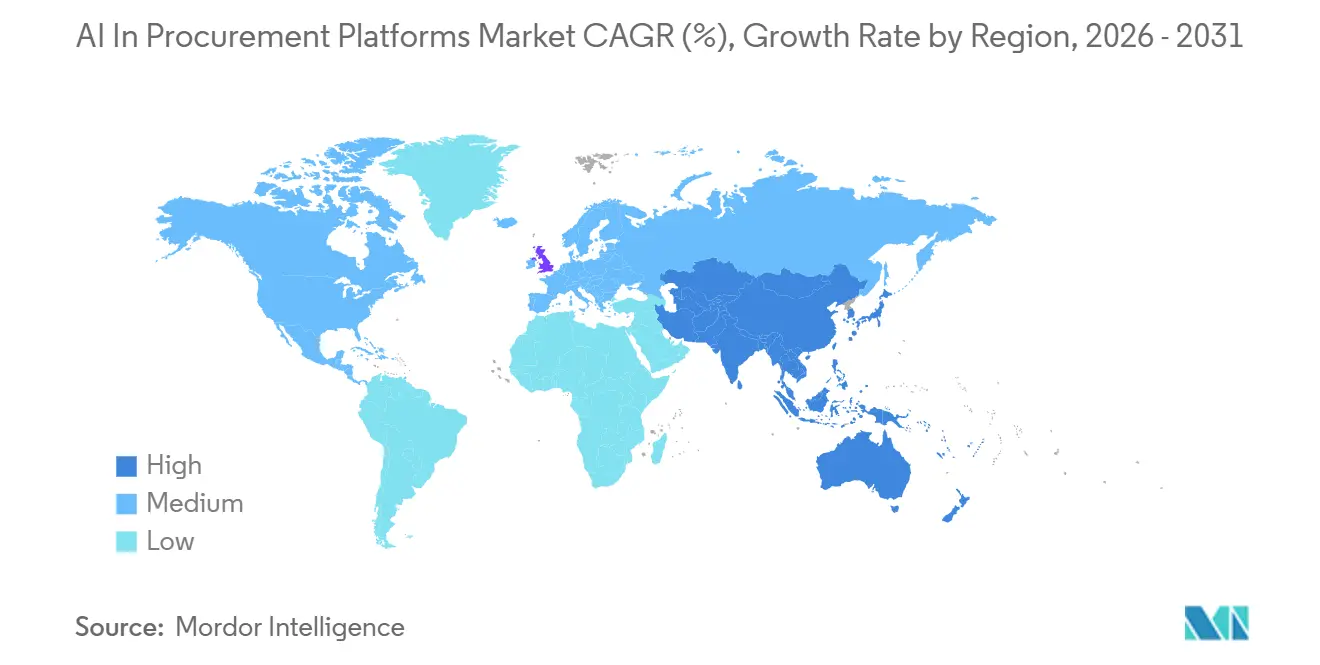

In 2025, North America accounted for 41.20% of the AI in procurement platforms market, making it the leading regional revenue contributor. The U.S. dominates due to significant enterprise IT budgets, a strong source-to-pay vendor base, and procurement organizations prioritizing digital transformation. Canada and Mexico benefit from supply chain proximity to the U.S. and nearshoring trends, driving demand for integrated supplier onboarding and risk management solutions.

Asia-Pacific is projected to grow at a 34.15% CAGR from 2026 to 2031, emerging as the fastest-growing region in the AI in procurement platforms market. High transaction volumes, varying procurement maturity, and digitalization pressures drive growth across public and private sectors. China leads with government-driven digitalization and enterprise procurement modernization, while Japan faces data quality challenges, indicating future adoption potential as readiness improves.

Europe remains a key market as procurement leaders focus on documenting, monitoring, and governing digital decision tools, increasing the demand for platforms offering auditability and contract-level control. In South America, Brazil and Argentina lead adoption, leveraging procurement platforms to address supplier fragmentation, cross-border trade complexities, and compliance variations. The market reflects diverse regional dynamics, with North America leading in scale, Asia-Pacific in growth, Europe in compliance, and South America in operational complexity, shaping varied vendor strategies.

Competitive Landscape

The AI in procurement platforms market balances between concentration and fragmentation. A few full-suite vendors, including SAP, Oracle, Workday, Coupa, GEP, Ivalua, JAGGAER, and Zycus, dominate enterprise attention, particularly in complex source-to-pay programs. Meanwhile, niche players gain traction in specialized areas like autonomous negotiation, supplier intelligence, and contract AI, maintaining market competitiveness despite the dominance of key vendors.

Established players are accelerating AI-native releases and ecosystem strategies. SAP introduced its Autonomous Enterprise framework in May 2026, featuring over 50 domain-specific Joule Assistants and a significant partner fund. Earlier, SAP revamped Ariba on its Business Technology Platform, integrating Joule’s Bid Analysis Agent and enhancing procurement workflows. Coupa launched Compose and Catalyst in May 2026, combining AI functionality with transformation services, emphasizing faster customer activation. These developments highlight the need for functional AI, robust deployment support, and adaptable architectures.

Specialist vendors continue to capture valuable niches in the market. Pactum’s USD 54 million Series C funding in June 2025 reflected strong investor confidence in agentic negotiation. JAGGAER’s launch of JAI in May 2026 showcased the value of conversational support in procurement when aligned with proprietary data. Icertis expanded its SAP partnership in April 2026 to deliver AI-driven contract intelligence for public sector and government contractors. These trends suggest full-suite vendors may increasingly integrate specialized agents to enhance specific workflows.

AI In Procurement Platforms Industry Leaders

Arkestro, Inc.

Basware Corporation

Coupa Software Inc.

Oracle Corporation

Pactum AI, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP SE introduced the Autonomous Enterprise framework at SAP Sapphire, deploying over 50 domain-specific Joule Assistants for finance, supply chain, and procurement. The initiative included a EUR 100 million (USD 116.0 million) partner fund and strategic AI partnerships with Anthropic, Google Cloud, and Microsoft, marking a significant advancement in AI procurement architecture.

- May 2026: JAGGAER launched JAI, an AI procurement assistant integrated into the JAGGAER One platform, capable of addressing queries in 28 languages. Early adopters reported a 50% reduction in support ticket volume, with JAI also identifying off-contract spending and supplier risks using company-specific data.

- April 2026: Icertis expanded its SAP partnership to deliver AI-driven contract intelligence for federal agencies and government contractors, ensuring FAR and DFARS compliance and driving over 80% year-on-year growth in its public sector business.

- March 2026: SAP released the next-generation SAP Ariba, rebuilt on the SAP Business Technology Platform. The update integrates Joule's Bid Analysis Agent into sourcing workflows and introduces Intake Management as a unified entry point for procurement requests, transitioning SAP to an AI-native source-to-pay suite.

Global AI In Procurement Platforms Market Report Scope

As per the scope of the report, AI in procurement platforms refers to the use of artificial intelligence and machine learning to automate and optimize the Source-to-Pay (S2P) process. These platforms function as "smart assistants", analyzing vast amounts of data to streamline supplier discovery, contract management, spend analysis, and risk assessment.

The AI in procurement platforms market is segmented by component, deployment, technology, application, organization size, end-use industry, and geography. By component, the market includes software and services. By deployment, the market is segmented into cloud-based and on-premise. By technology, the market is categorized into machine learning, natural language processing, predictive analytics, generative AI/LLMs, and computer vision/intelligent document processing. By application, the market includes supplier management & discovery, sourcing event management & RFx automation, spend analytics, contract lifecycle management, procure-to-pay/guided buying, risk management & predictive analytics, and invoice automation & accounts payable. By organization size, the market is segmented into large enterprises and SMEs. By end-use industry, the market is categorized into manufacturing, retail & e-commerce, healthcare & life sciences, BFSI, IT & telecom, government & public sector, energy & utilities, and transportation & logistics. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Services |

| Cloud-based |

| On-premise |

| Machine Learning |

| Natural Language Processing |

| Predictive Analytics |

| Generative AI / LLMs |

| Computer Vision / Intelligent Document Processing |

| Supplier Management & Discovery |

| Sourcing Event Management & RFx Automation |

| Spend Analytics |

| Contract Lifecycle Management |

| Procure-to-Pay / Guided Buying |

| Risk Management & Predictive Analytics |

| Invoice Automation & Accounts Payable |

| Large Enterprises |

| SMEs |

| Manufacturing |

| Retail & E-commerce |

| Healthcare & Life Sciences |

| BFSI |

| IT & Telecom |

| Government & Public Sector |

| Energy & Utilities |

| Transportation & Logistics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment | Cloud-based | |

| On-premise | ||

| By Technology | Machine Learning | |

| Natural Language Processing | ||

| Predictive Analytics | ||

| Generative AI / LLMs | ||

| Computer Vision / Intelligent Document Processing | ||

| By Application | Supplier Management & Discovery | |

| Sourcing Event Management & RFx Automation | ||

| Spend Analytics | ||

| Contract Lifecycle Management | ||

| Procure-to-Pay / Guided Buying | ||

| Risk Management & Predictive Analytics | ||

| Invoice Automation & Accounts Payable | ||

| By Organization Size | Large Enterprises | |

| SMEs | ||

| By End-use Industry | Manufacturing | |

| Retail & E-commerce | ||

| Healthcare & Life Sciences | ||

| BFSI | ||

| IT & Telecom | ||

| Government & Public Sector | ||

| Energy & Utilities | ||

| Transportation & Logistics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which deployment model leads adoption in procurement AI platforms?

Cloud-based deployment led with 72.3% share in 2025, mainly because buyers need faster integration, easier updates, and better support for connected workflows.

Which application area is growing the fastest in procurement AI?

Risk Management & Predictive Analytics is the fastest-growing application, with a projected 33.56% CAGR from 2026 to 2031.

Which end-use sector has the largest revenue base and which is growing fastest?

Manufacturing held the largest share at 35.75% in 2025, while healthcare and life sciences is projected to grow the fastest at a 33.98% CAGR through 2031.

Which region leads global demand and which region is expanding the fastest?

North America led with 41.20% share in 2025, while Asia-Pacific is projected to grow the fastest at a 34.15% CAGR through 2031.

Why are services growing faster than software in this space?

Services is projected to grow at 32.88% CAGR because enterprises need implementation support, workflow design, data preparation, and change management to scale agentic procurement use cases.

Page last updated on: