AI In Elderly Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 44.61 Billion |

| Market Size (2031) | USD 90.35 Billion |

| Growth Rate (2026 - 2031) | 15.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Elderly Care Market Analysis by Mordor Intelligence

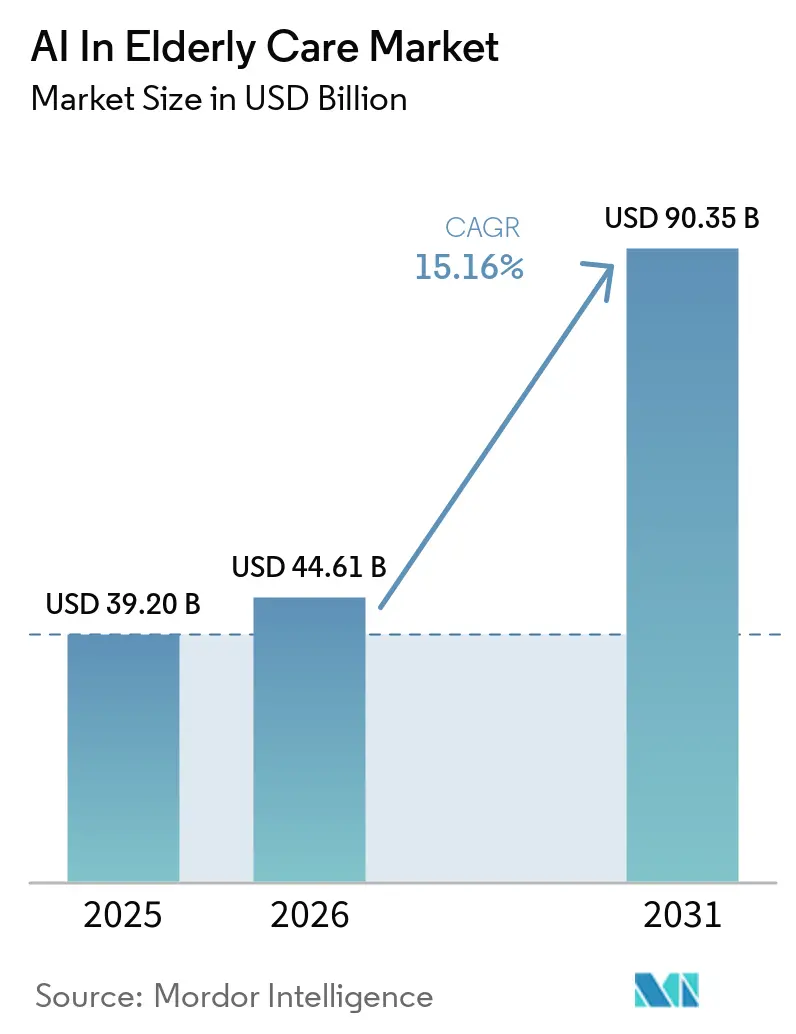

The AI In Elderly Care Market size is projected to be USD 39.20 billion in 2025, USD 44.61 billion in 2026, and reach USD 90.35 billion by 2031, growing at a CAGR of 15.16% from 2026 to 2031.

The AI in elderly care market is moving past small pilots because senior living operators, integrated health systems, and public payers are now signing longer contracts that support day-to-day care delivery across home, community, and facility settings. This shift is being supported by broad demand that comes from a larger elderly population, rising clinical complexity, and growing pressure on providers to do more with limited staff. Global population aging remains a durable base for demand, with people aged 60 and above reaching 1.22 billion in 2025 and the 80 and above group reaching 104 million, which keeps the AI in elderly care market tied to a long-duration care need rather than a short-cycle technology trend. Policy action is also reinforcing adoption, as staffing pressure in the United States and care digitization support in Japan are pushing operators toward workflow tools, monitoring systems, and automation that can deliver measurable labor relief. Competition in the AI in elderly care market is still spread across hardware, software, and services, but vendors that can combine privacy-aware monitoring, clinical workflow support, and integration capability are building a stronger position as buyers look for fewer vendors and clearer operational returns.

Key Report Takeaways

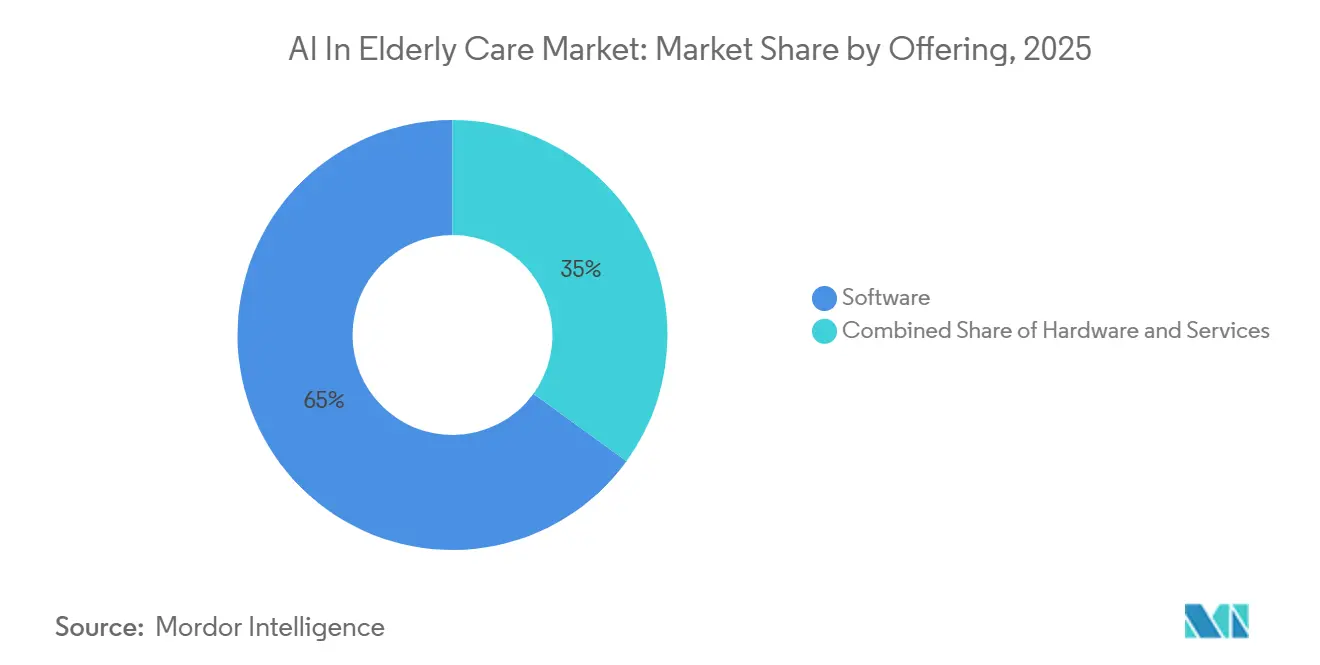

- By offering, software led with 65.02% revenue share in 2025, while services are forecast to expand at 16.17% CAGR through 2031.

- By deployment mode, cloud held 58.46% share in 2026 and is also the fastest-growing deployment type at 15.59% CAGR through 2031.

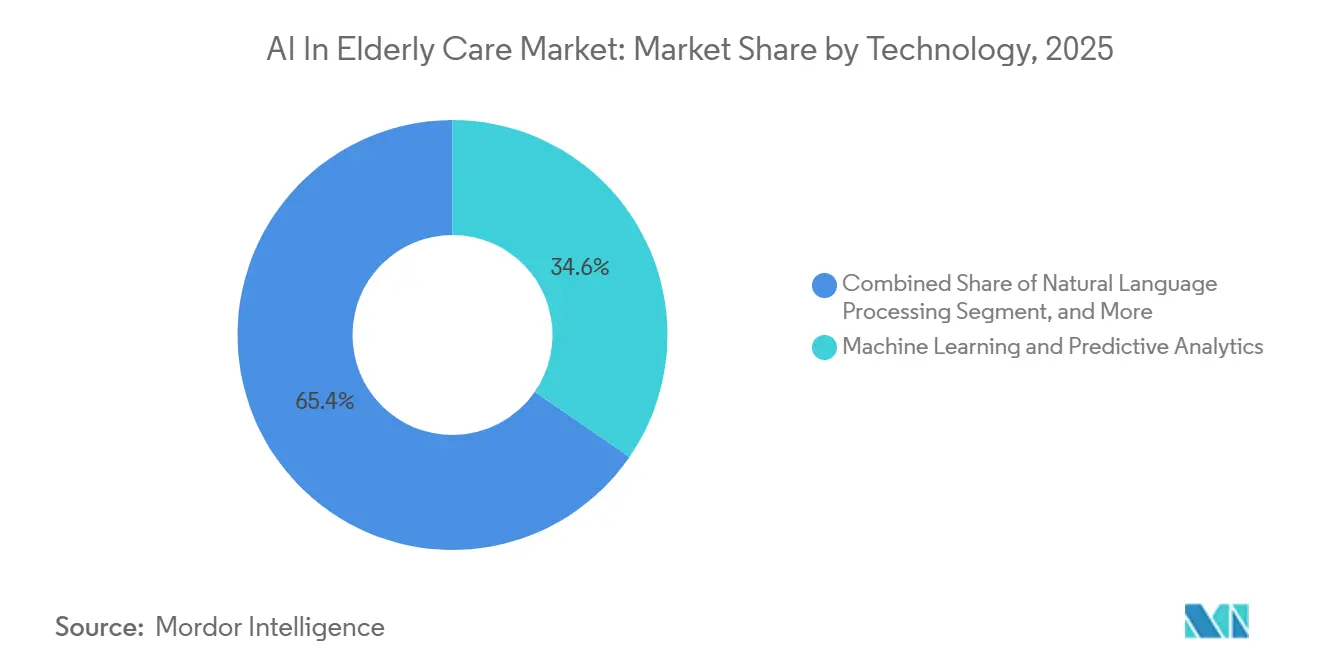

- By technology, machine learning and predictive analytics accounted for 34.57% of revenue in 2025, while robotics and robotic assistance are projected to grow at 17.39% CAGR through 2031.

- By application, remote monitoring and predictive alerts represented 41.03% share in 2025, while social interaction and companionship are projected to advance at 19.69% CAGR through 2031.

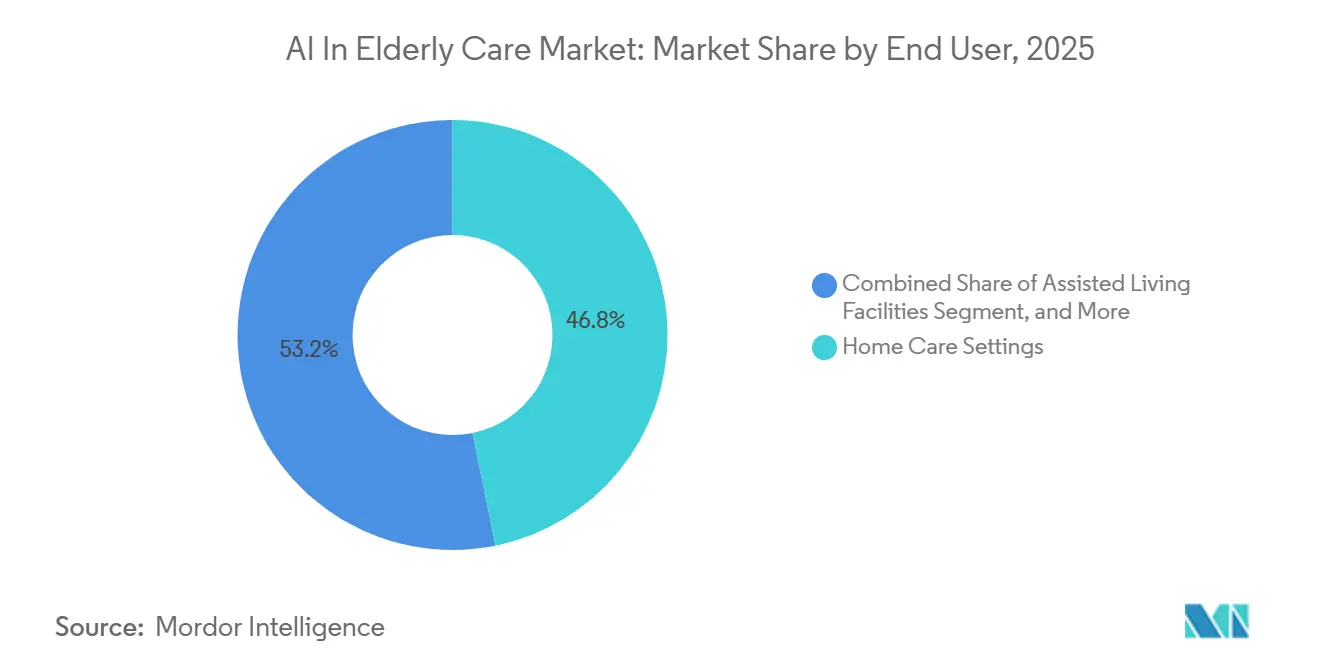

- By end user, home care captured 46.83% share in 2025, while assisted living facilities are forecast to expand at 17.33% CAGR through 2031.

- By geography, North America led with 37.83% of revenue in 2025, while Asia-Pacific is expected to record the fastest regional CAGR at 18.03% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Elderly Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Longer Life Expectancy Driving Structural Care Demand | +3.2% | Global | Long term (≥ 4 years) |

| Caregiver Shortages Across Senior Care Settings Compelling Technology Substitution | +2.8% | Global, acute in North America, Japan, and EU | Medium term (2-4 years) |

| Aging-in-Place Preference and Proactive Remote Monitoring Adoption | +2.3% | North America and Western Europe | Medium term (2-4 years) |

| Better AI Accuracy Across NLP, Vision, and Robotics Unlocking New Use Cases | +1.9% | Global, early gains in North America and APAC | Short term (≤ 2 years) |

| Privacy-Preserving Ambient Sensing Replacing Cameras and Wearables | +1.5% | Global, with early commercial scale in EU and Japan | Short term (≤ 2 years) |

| Staffing-Rule and Documentation ROI Driving Workflow AI Uptake, CMS Compliance Requirements | +1.2% | North America with spillover to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Longer Life Expectancy

The demographic foundation of the AI in elderly care market is expanding most quickly in the age groups that consume the highest amount of care. Global life expectancy at birth reached 73.3 years in 2024, and the added years are increasingly associated with chronic disease, functional decline, and recurring support needs rather than long periods of full health.[1]World Health Organization, “Ageing and Health,” World Health Organization, who.int The global population aged 60 and above reached 1.22 billion in 2025, and that group is projected to rise toward 1.4 billion by 2030, which keeps the AI in elderly care market tied to an expanding care base for the full forecast period. The population aged 80 and above already stood at 104 million and is projected to reach 263 million by 2050, which matters because this group has the highest intensity of supervision, medication support, and mobility assistance needs. In the United States, the population aged 80 and above stood at 14.75 million in 2025 and is projected to reach 18.79 million by 2030, which points to rising pressure on staffing models and facility operations.[2]American Health Care Association, “Nursing Home Workforce Report,” American Health Care Association, ahcancal.org China and India together are expected to hold a very large share of the global older population by 2050, which means product design in AI in elderly care market is increasingly being adapted for lower cost and resource-constrained care settings in Asia.

Caregiver Shortages Across Senior Care Settings

The AI in elderly care market is also being shaped by a labor shortage that is deeper than open vacancy numbers alone suggest. PHI projects that the United States direct care workforce must fill 9.7 million openings between 2024 and 2034, with 772,000 of those representing net new job growth rather than simple replacement demand. This means providers are not only struggling to hire, but they are also trying to maintain service quality while training large numbers of new workers into physically and emotionally demanding roles. In Japan, the required caregiver count reached 2.40 million by FY2026, while aging is projected to keep rising toward 2040, which widens the gap between labor supply and required care capacity. In this setting, the AI in elderly care market is benefiting from demand for tools that reduce charting time, simplify staff coordination, and identify resident risk earlier so fewer workers can manage more residents safely. The operational appeal is straightforward, because technologies that reduce documentation load and improve alert quality can support both productivity and worker retention in settings where every avoided hour of manual work matters.

Aging-In-Place and Proactive Remote Monitoring Adoption

The AI in elderly care market is also expanding because more care is shifting toward homes and community settings rather than large institutions. Home care already represented 46.8% of end-user demand in 2025, which shows that aging in place has moved from a preference trend into the leading delivery model for current spending. This shift is encouraging providers to favor ambient and low-friction systems that can monitor safety and basic health status without requiring constant human supervision or daily device management. Cairns Health commercially launched Luna in May 2025 as a radar-based AI care companion that combines contactless vital sign monitoring with real-time two-way voice interaction, which shows how sensing and conversational tools are now being packaged together for home use.[3]Cairns Health, “Cairns Health Commercially Releases Luna, an AI-Powered Digital Care Companion,” Cairns Health, cairns.ai Intuition Robotics also expanded ElliQ to Washington State Medicaid recipients in March 2026, and pilot users averaged 60 interactions per day while 95% reported reduced loneliness, which shows that companionship functions are becoming more closely linked with measurable care outcomes. In the AI in elderly care market, this home-based shift favors vendors that can support remote coordination across multiple caregivers, payers, and care pathways instead of relying only on feature depth inside a single facility.

Better AI Accuracy Across NLP, Vision, and Robotics

Improving model performance is broadening the range of tasks that can be trusted inside the AI in elderly care market. The HARMONY system presented at IJCAI 2025 achieved 95.9% activity recognition accuracy on depth camera data and 98.8% on WiFi CSI signals while also using homomorphic encryption, which brought privacy and reliability together in one design. Tokyo Metropolitan University research also showed that privacy-preserving thermal infrared and time of flight sensor fusion can track people with a mean absolute error of 0.172 meters, which narrows the performance gap with camera-based monitoring while avoiding many privacy objections. In robotics, mecwacare deployed 22 Abi companion robots across residential aged care homes in April 2026 for more than 1,500 residents, which shows that conversational robotics in elderly care is moving beyond controlled pilots and into wider facility use. RIKEN and Keio University School of Medicine also developed dialogue robots that use AI-curved voice prompts to detect cognitive difficulties in residents aged 65 to 85, which extends robotics from companionship into earlier cognitive support. As these gains come together, the AI in elderly care market is shifting from single-use tools toward platforms that can monitor, communicate, and assist within the same deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy, Cybersecurity, and Compliance Burden | -1.8% | Global, most acute in EU and North America | Long term (≥ 4 years) |

| Integration Cost and Legacy-System Complexity | -1.5% | Global, particularly emerging markets and fragmented SME operators | Medium term (2-4 years) |

| Surveillance Trust Gap Among Oldest-Old Users | -0.9% | Global, with higher resistance in Japan and Germany | Long term (≥ 4 years) |

| Tariff and Component Volatility in Sensors and Robotics | -0.7% | North America and Asia-Pacific supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Privacy, Cybersecurity, and Compliance Burden

The compliance barrier in the AI in elderly care market is rising at the same time that clinical and operational demand is accelerating. The EU AI Act entered into force in August 2024, and many healthcare related monitoring systems will face high risk obligations from August 2026, which increases the need for risk management, data governance, documentation, and human oversight before deployment. In the United States, protected health information rules under HIPAA add a separate layer of security and process requirements for any vendor working with resident level health data. Tokyo Metropolitan University research found that 82% of elderly subjects preferred privacy-protected monitoring systems over camera-based alternatives, which shows that privacy is not only a legal issue but also a user acceptance issue inside the AI in elderly care market. The challenge is that privacy preserving systems often require more advanced sensing, encryption, and data handling architecture, which raises development cost and slows smaller vendors. This gives larger and better funded suppliers a structural advantage because they can absorb compliance work more easily and spread those costs across a wider installed base.

Integration Cost and Legacy-System Complexity

The AI in elderly care market also faces a practical constraint in the form of fragmented and outdated care technology stacks. Many nursing homes and assisted living operators still rely on record systems that were built for charting and scheduling rather than continuous data exchange with AI tools, which makes clean interoperability difficult. When monitoring systems, workflow software, and alerts do not connect smoothly with daily records, the promised productivity gain becomes harder to capture and harder to prove. Japan has already reported interoperability barriers between care record systems and monitoring devices in the Care DX initiative, even with subsidies that reached JPY 300,000 per device, or USD 2,000, which shows that funding alone does not resolve technical friction. This challenge is even harder for smaller operators that do not have internal technical teams or large implementation budgets. At the same time, this same friction is gradually favoring cloud native and API first vendors in the AI in elderly care market because they are designing around interoperability as a core product feature rather than a later add-on.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Revenue Catching Up to Software Dominance

Software captured 65.02% of the AI in elderly care market share in 2025, which shows that platform subscriptions still form the spending core of the current adoption cycle. This lead reflects the strong role of software in resident monitoring, clinical workflow support, analytics, and alert management across both home and facility environments. Hardware remains necessary for sensing and robotics, but it does not capture the same margin profile because device competition is broader and pricing pressure is more visible. Services are projected to expand at 16.17% CAGR from 2026 to 2031, which means the AI in the elderly care industry is moving from simple product purchase toward full deployment support. That pattern usually appears when buyers no longer ask whether to adopt a tool and instead focus on how to make it work across staff, workflows, and reporting structures.

The services expansion matters because implementation, training, workflow redesign, and managed support now influence contract value more directly than they did in the early phase of adoption. Facilities that deploy AI tools across multiple buildings or care programs often need help mapping alerts, staff roles, and escalation protocols into existing care processes. This makes professional services more central to retention because poor onboarding can weaken outcomes even when the software itself is strong. Sage raised USD 65 million in March 2026, bringing its total capital raised to USD 124 million, which points to investor confidence in integrated models that combine predictive software with operational support for senior living and skilled nursing providers. As the AI in elderly care market matures, vendors that pair software with recurring service capacity are likely to defend pricing more effectively than companies that rely on standalone products.

By Deployment Mode: Cloud Leads and Sustains Its Advantage

Cloud deployment accounted for 58.46% share of the AI in elderly care market size in 2026, and it is also projected to grow at 15.59% CAGR through 2031. This combination of current scale and future growth shows that cloud has become the preferred operating model for multi-site providers that need centralized visibility and rapid software updates. In the AI in elderly care market, cloud architectures are especially attractive when operators manage distributed home care, assisted living, and nursing services under one administrative structure. Shared access to alerts, documentation tools, and model improvements is easier when platforms are centrally managed rather than installed separately inside each building. This advantage becomes more important as AI tools expand from simple monitoring into workflow support, reporting, and predictive decision assistance.

On-premises systems still hold a place in settings with strict data residency demands or highly controlled public sector procurement rules. Some European and Asia-Pacific operators also prefer on-premises or private cloud structures when they handle sensitive neurological or long-term clinical data. Even so, local systems usually update more slowly, and slower model updates can weaken performance when vendors are improving detection or language features quickly. Enzo Health raised USD 26 million in May 2026 to scale cloud-based AI across home health, linking intake automation, clinical documentation, and quality assurance in one workflow, which reflects where capital is moving inside the AI in elderly care market. The broader direction remains clear, because buyers increasingly want platforms that can be rolled out quickly, managed centrally, and extended across care settings without major local infrastructure work.

By Technology: Robotics Advances as Physical AI Enters Mainstream Deployment

Machine learning and predictive analytics held 34.57% of revenue in 2025, which confirms that analytical tools remain the backbone of the AI in elderly care market. These systems support fall risk scoring, medication adherence monitoring, staffing decisions, and early warning functions that providers can link to operational and clinical outcomes. Natural language processing is also becoming deeply embedded because it supports companion dialogue, voice prompts, documentation capture, and multilingual communication across elderly care settings. Robotics and robotic assistance is projected to grow at 17.39% CAGR from 2026 to 2031, showing that physical AI is becoming a more important spending category rather than a peripheral experiment. This shift reflects growing interest in transfer assistance, companionship, autonomous delivery, and activity support inside both residential and institutional care.

Computer vision is also changing, because the focus has moved from visible camera surveillance toward multimodal sensing that can identify motion patterns, posture changes, and distress without relying on facial capture. Research from Tokyo Metropolitan University showed that privacy-preserving passive thermal infrared and time of flight sensing can deliver strong tracking performance, which strengthens the case for non-camera monitoring in elderly care environments. The HARMONY system added further support by showing that sensor-agnostic telemonitoring can maintain high recognition accuracy while addressing privacy through encrypted processing. mecwacare’s April 2026 rollout of Abi robots and RIKEN’s work on dialogue-based cognitive screening both show that robotics is widening beyond companionship into more functional care support roles. As a result, the AI in elderly care industry is increasingly favoring technology stacks that can combine predictive analysis, sensing, and interaction rather than offering only one technical capability.

By Application: Remote Monitoring Anchors the Market While Companionship Accelerates

Remote monitoring and predictive alerts represented 41.03% share of the AI in elderly care market size in 2025, which keeps it as the largest application category in current spending. This leadership comes from the clear operational value of automated alert triage, reduced avoidable escalation, and wider supervision coverage without matching increases in staffing. Providers also view remote monitoring as a practical bridge between home care and facility care because similar sensing and alert logic can be adapted across both settings. Social interaction and companionship are expected to grow at 19.69% CAGR through 2031, which makes it the fastest-growing application in the AI in elderly care market. The speed of this segment reflects a stronger connection between loneliness, care quality, and measurable service outcomes than was recognized a few years ago.

Intuition Robotics reported that ElliQ users in Washington State’s Medicaid pilot averaged 60 interactions per day, while 95% reported reduced loneliness and 43% felt safer, which shows that companionship tools are now being evaluated against concrete wellbeing measures. Fall detection and prevention, medication management, and cognitive support still remain critical because they connect directly to liability, adherence, and early intervention goals. Cognitive support is gaining traction as dialogue systems improve and become more adaptive to older users with different comfort levels and health conditions. RIKEN and Keio University School of Medicine are using dialogue robots with AI personalized voice prompts to identify early cognitive difficulties, which points to a wider role for conversational tools in screening and support. Vendors that can combine monitoring, companionship, and cognitive functions on one platform are likely to secure larger contracts than suppliers limited to a single application.

By End User: Home Care Dominates but Assisted Living Closes the Gap Fastest

Home care held 46.83% of AI in elderly care market share in 2025, which reflects the strong pull of aging in place and the cost advantage of supporting people in residential settings. The AI in elderly care market has therefore developed with a large home-based demand base even before broader facility standardization has been completed. Home deployments are often chosen because they extend oversight without requiring continuous physical presence, which is valuable for families, agencies, and public payers managing labor shortages. Assisted living facilities are projected to grow at 17.33% CAGR through 2031, which shows that operators are expanding beyond simple emergency alert systems toward broader AI-enabled resident management. In practical terms, this means assisted living providers are using AI as part of occupancy strategy, labor management, and family communication rather than only for safety alerts.

Nursing homes remain important because their residents usually have higher acuity and stricter documentation requirements, which makes adoption more complex even when the need is strong. These providers often want AI tools that can support clinical workflow and compliance at the same time, not just resident monitoring in isolation. Other end users, including hospitals and specialist clinics, are still smaller in revenue terms, but they are gradually using AI tools to support post-acute transitions and cognitive assessment. Diligent Robotics was selected for AARP’s AgeTech Collaborative accelerator in October 2025, which signaled its move from hospital robotic assistance into senior living and long-term care settings. This overlap between hospital and elderly care use cases suggests that end-user boundaries inside the AI in elderly care market will continue to blur as care pathways become more distributed.

Geography Analysis

North America accounted for 37.83% share of the AI in elderly care market size in 2025, which kept it as the largest regional contributor. The region benefits from high care costs, strong digital infrastructure, and a provider base that is actively seeking labor saving tools across home, community, and institutional care. In the United States, the population aged 80 and above stood at 14.75 million in 2025 and is projected to reach 18.79 million by 2030, which continues to strengthen the long term need for AI supported elderly care delivery. CMS finalized a minimum staffing standard of 3.48 nursing hours per resident day in April 2024, and that policy has increased pressure on facilities to use documentation and workflow tools that support compliance where hiring remains difficult. Capital also remains available for deployment in the region, as shown by Sage’s March 2026 funding round and Enzo Health’s May 2026 raise, which both focused on scaling AI tools across senior care and home health settings. South America remains earlier in adoption, with smartphone led monitoring and voice companion use appearing before broader institutional deployments in many areas.

Europe is a large but uneven regional opportunity inside the AI in elderly care market. The population aged 65 and above in the European Union reached 21% in 2023 and is projected to reach 29% by 2050, which keeps demand anchored in long duration demographic change rather than short term technology cycles. The EU AI Act is reshaping product requirements because healthcare-related monitoring systems will face stricter obligations from August 2026, which raises entry barriers and favors vendors with stronger compliance resources. The United Kingdom is moving on a separate path, but AI documentation trials in community care settings still show that workflow support remains one of the most immediate use cases for elderly care providers in the region.

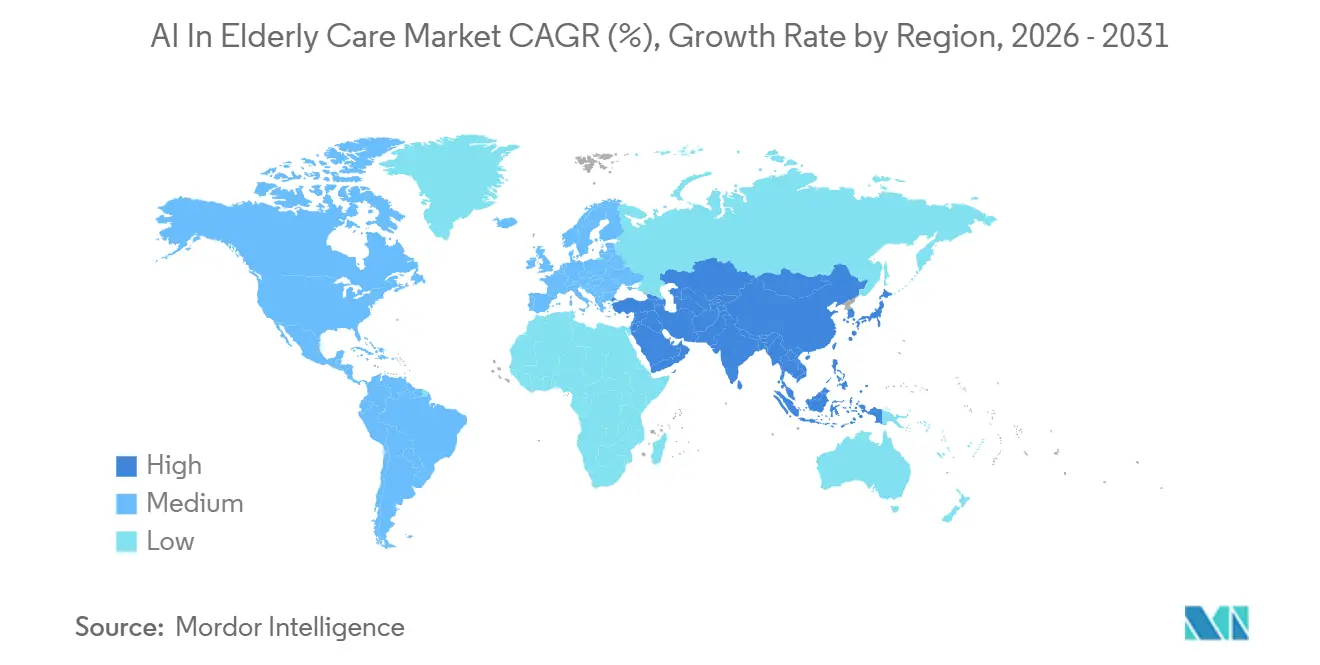

Asia-Pacific is the fastest-growing region in the AI in elderly care market, with an expected CAGR of 18.03% from 2026 to 2031. Japan remains a key driver because its aging rate reached 28.6% in 2020 and is projected to move toward 35% by 2040, while caregiver demand reached 2.40 million by FY2026. Japan’s government also committed JPY 1.9 billion, or USD 12.6 million, in its FY2024 supplementary budget for Care DX adoption packages, and a model project in Kitakyushu City reported a 35% reduction in overall care work time from coordinated technology use. China is also increasing its focus on AI robotics and elderly care infrastructure, while South Korea and Australia add support through digital readiness and aged care reform. The Middle East and Africa remain a smaller regional base, but premium facility deployments in GCC countries and community-oriented monitoring initiatives in parts of Africa suggest that adoption is beginning to widen beyond the most mature elderly care systems.

Competitive Landscape

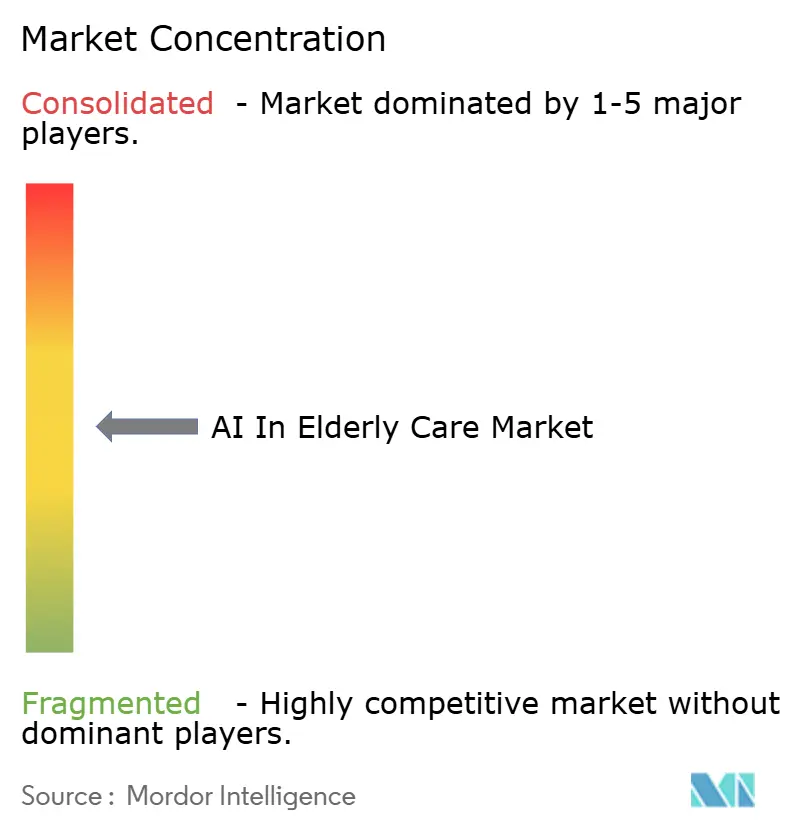

The AI in elderly care market remains moderately fragmented, with more than 200 active vendors spanning software, sensing hardware, robotics, and services. No single company holds a dominant position, and competition is spread across different parts of the value chain rather than concentrated around one product category. A two tier structure is gradually becoming clearer, with integrated platform vendors on one side and point solution suppliers on the other. Integrated vendors are better placed when buyers want monitoring, analytics, workflow support, and deployment services inside one contract. Point solution vendors can still win in narrow applications, but they face more pricing pressure when providers want fewer systems and a lower integration burden.

Technology choices now shape competitive advantage more directly than broad branding claims. Vendors using privacy-preserving radar, millimeter wave, infrared, and sensor fusion approaches are gaining traction because providers want safety monitoring without the burden of camera consent and higher breach sensitivity. The Applied Sciences research from Tokyo Metropolitan University reinforced this direction by showing that privacy-oriented sensing can still deliver strong tracking performance for assisted living use cases. Procurement standards also matter, and ISO 13482 is becoming more relevant for personal care robot selection in Europe and Japan, which raises the bar for newer entrants that have not completed certification work. This means the AI in elderly care market is not only a race to improve algorithms, but it is also a race to prove safety, compliance, and operational readiness.

Several company moves show how vendors are trying to build broader positions. Cairns Health acquired Together by Renee in October 2025 to add medication management and engagement features to its Luna ambient sensing platform, which shows a clear move toward platform expansion around the home care user. Sage raised USD 65 million in March 2026 to scale its predictive platform for senior care communities, which points to continued investor support for software-led models that claim measurable operational outcomes. Enzo Health then raised USD 26 million in May 2026 to extend cloud-based AI across home health workflows, which shows that the competitive field is also widening along the post-acute and home-based care continuum. The most attractive white space still appears in multilingual companionship, cognitive support, and workflow tools that can reduce labor pressure without adding user friction.

AI In Elderly Care Industry Leaders

CarePredict

IBM

Oracle Corporation

Samsung Electronics

Sensi.AI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Enzo Health raised USD 26 million to deploy AI across home health at scale, targeting intake automation, AI-assisted clinical documentation, and quality assurance workflows across home health and skilled nursing. The raise addresses a market where clinician turnover runs approximately 80% within 100 days of employment, with administrative burden cited as the primary driver.

- April 2026: mecwacare completed Australia's largest rollout of humanoid companion robots, deploying 22 Abi robots by Andromeda Robotics across its Victorian residential aged care homes to support over 1,500 residents, including those living with dementia and from culturally and linguistically diverse backgrounds. The robots support up to 90 languages and use machine learning to remember individual residents over time.

- March 2026: Sage raised USD 65 million in a Series C led by Goldman Sachs Alternatives, bringing total capital to USD 124 million, to scale its predictive AI senior care platform. Communities using the platform reported a 50% reduction in falls, 50% faster caregiver response times, and a USD 275 increase in net operating income per resident per month.

- March 2026: Intuition Robotics expanded ElliQ availability to Washington State Medicaid recipients under Community First Choice and Roads to Community Living programmes, marking the first statewide Medicaid offering of an AI smart care device. Pilot data showed participants engaged with ElliQ an average of 60 times per day, with 95% reporting reduced loneliness.

Global AI In Elderly Care Market Report Scope

The AI in Elderly Care Market encompasses software, devices, and digital platforms driven by Artificial Intelligence (AI) designed to assist, monitor, and improve the quality of life for aging populations. It shifts care from a reactive, labor-intensive model to a predictive, data-driven, and independent ecosystem.

The AI in Elderly Care Market Report provides a holistic segmentation framework covering all major dimensions of the industry. By offering, the market is divided into hardware, software, and services. In terms of deployment mode, solutions are offered as cloud-based and on-premise. The technology landscape spans machine learning & analytics, natural language processing (NLP), vision, robotics, and other AI-driven innovations. By application, the market is segmented into fall detection, remote monitoring, medication management, cognitive support, social interaction, and rehabilitation. The end-user base encompasses home care, assisted living, nursing homes, and other elderly care facilities. Geographically, the market is segmented into North America, Europe, Asia-Pacific (APAC), Middle East and Africa (MEA), and South America. Forecasts are provided in terms of market value (USD), offering insights into growth potential, investment opportunities, and competitive positioning across all these segments.

| Hardware |

| Software |

| Services |

| Cloud |

| On-Premise |

| Machine Learning and Predictive Analytics |

| Natural Language Processing |

| Computer Vision |

| Robotics and Robotic Assistance |

| Other Technology (Smart Home Devices and IoT Solutions, Generative AI Care Assistants, etc.) |

| Fall Detection and Prevention |

| Remote Monitoring and Predictive Alerts |

| Medication Management |

| Cognitive Support and Dementia Care |

| Social Interaction and Companionship |

| Rehabilitation and Daily Living Assistance |

| Home Care Settings |

| Assisted Living Facilities |

| Nursing Homes |

| Other End Users (Hospitals and Clinics, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Hardware | |

| Software | ||

| Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By Technology | Machine Learning and Predictive Analytics | |

| Natural Language Processing | ||

| Computer Vision | ||

| Robotics and Robotic Assistance | ||

| Other Technology (Smart Home Devices and IoT Solutions, Generative AI Care Assistants, etc.) | ||

| By Application | Fall Detection and Prevention | |

| Remote Monitoring and Predictive Alerts | ||

| Medication Management | ||

| Cognitive Support and Dementia Care | ||

| Social Interaction and Companionship | ||

| Rehabilitation and Daily Living Assistance | ||

| By End User | Home Care Settings | |

| Assisted Living Facilities | ||

| Nursing Homes | ||

| Other End Users (Hospitals and Clinics, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of AI in elderly care by 2031?

The AI in elderly care market is forecast to reach USD 90.35 billion by 2031 from USD 44.61 billion in 2026, which reflects sustained expansion across home care, assisted living, and nursing settings.

How fast is AI in elderly care expected to grow through 2031?

The AI in elderly care market is expected to grow at a 15.16% CAGR from 2026 to 2031, supported by aging populations, labor shortages, and broader deployment across monitoring and workflow tools.

Which offering category currently leads spending in elderly care AI?

Software led the market with 65.02% of revenue in 2025, while services are expected to grow faster as providers need implementation, training, and workflow support during larger rollouts.

Which application is growing the fastest in elderly care AI solutions?

Social interaction and companionship is the fastest-growing application with a projected 19.69% CAGR through 2031, while remote monitoring and predictive alerts remain the largest application by current share.

Which region leads adoption, and which one is growing the fastest?

North America led with 37.83% share in 2025, while Asia-Pacific is projected to expand the fastest at 18.03% CAGR through 2031 because of sharper demographic pressure and care workforce shortages.

Page last updated on: