AI Factory Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

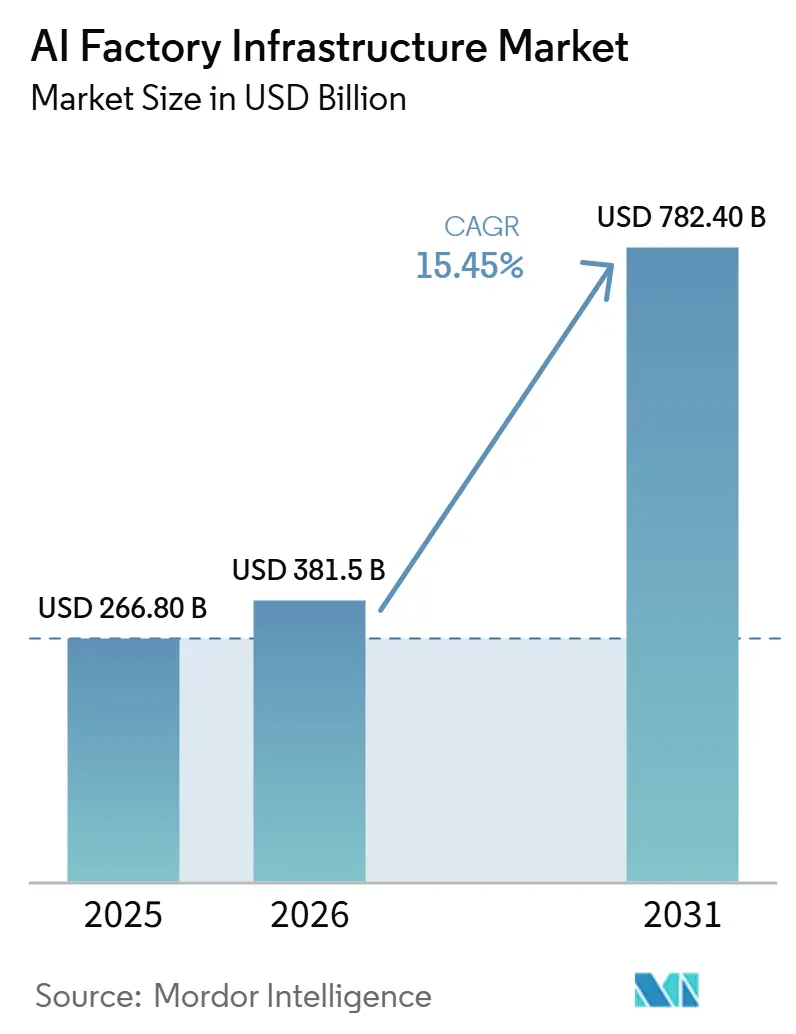

| Market Size (2026) | USD 381.5 Billion |

| Market Size (2031) | USD 782.40 Billion |

| Growth Rate (2026 - 2031) | 15.45% CAGR |

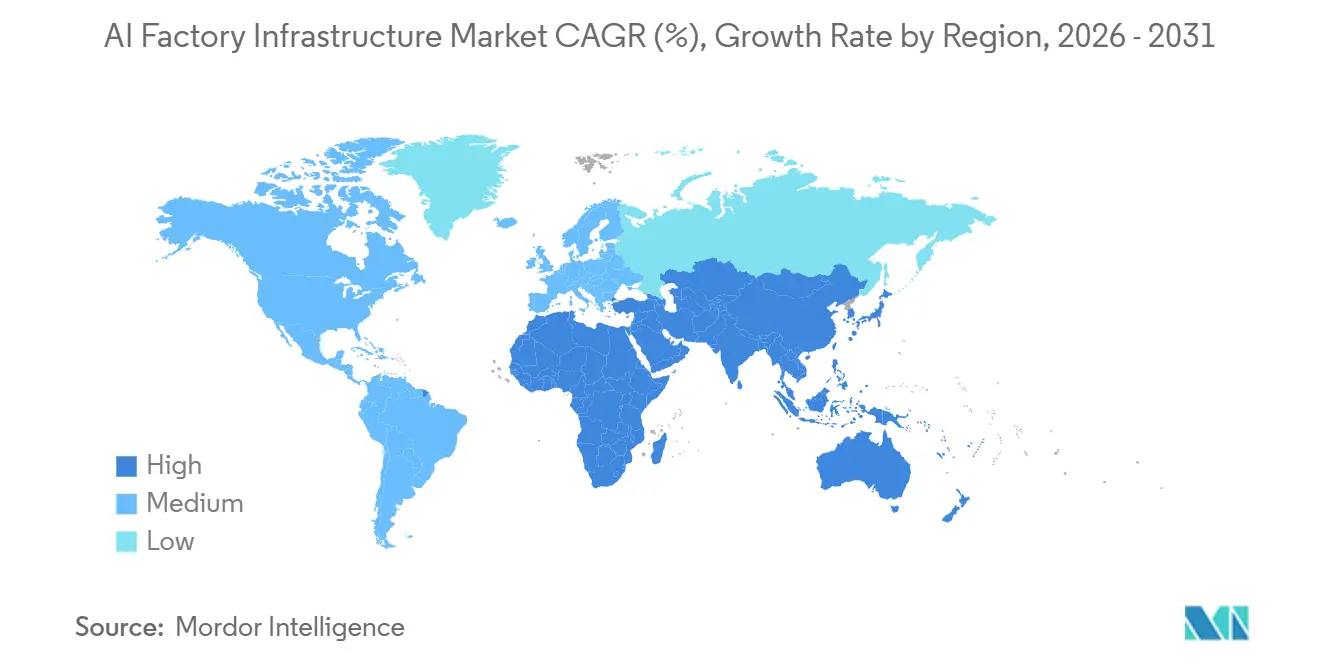

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

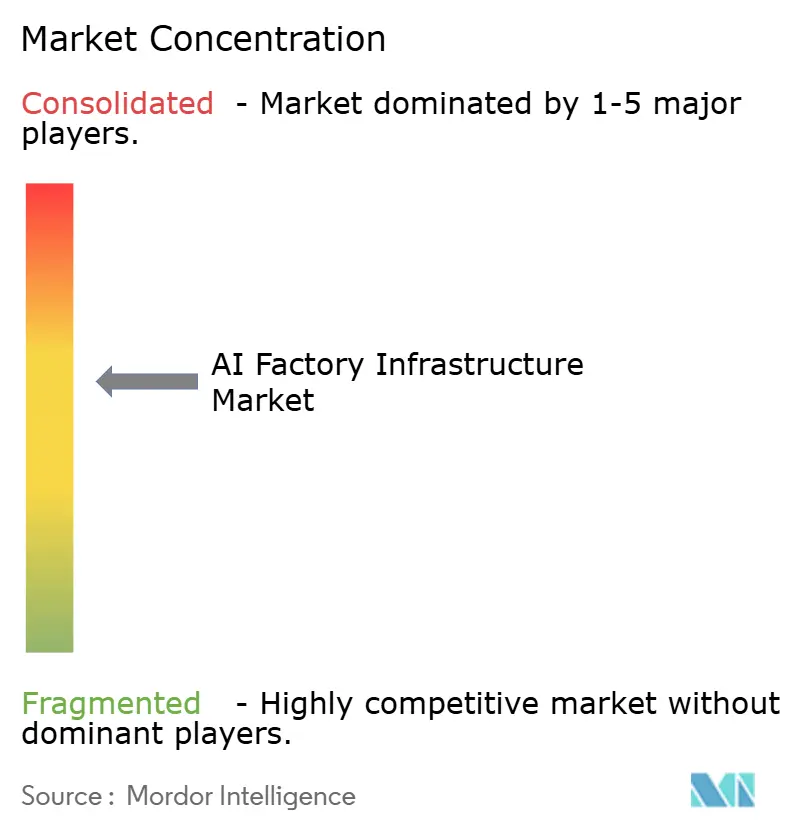

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Factory Infrastructure Market Analysis by Mordor Intelligence

The AI factory infrastructure market size is expected to grow from USD 266.8 billion in 2025 to USD 381.5 billion in 2026 and is forecast to reach USD 782.4 billion by 2031 at 15.45% CAGR over 2026-2031. Growth is being supported by a compressed capital spending cycle across large technology operators, with Amazon, Alphabet, and Meta raising infrastructure commitments in ways that have kept AI capacity expansion at the center of spending plans. The AI factory infrastructure market is also benefiting from the shift away from standard data center layouts toward AI-native facilities that require higher rack density, liquid cooling, and tighter power design. Demand is widening beyond pure cloud builds because sovereign compute rules, latency needs, and data residency requirements are making hybrid and localized deployments more relevant. The AI factory infrastructure market is seeing stronger competition in networking, cooling, and management software as buyers seek better utilization, faster deployment, and lower operational friction across large GPU estates. Power access limits, long interconnection timelines, and a shortage of specialized engineering capability are still slowing the pace at which new capacity can be brought online, even when capital is available.

Key Report Takeaways

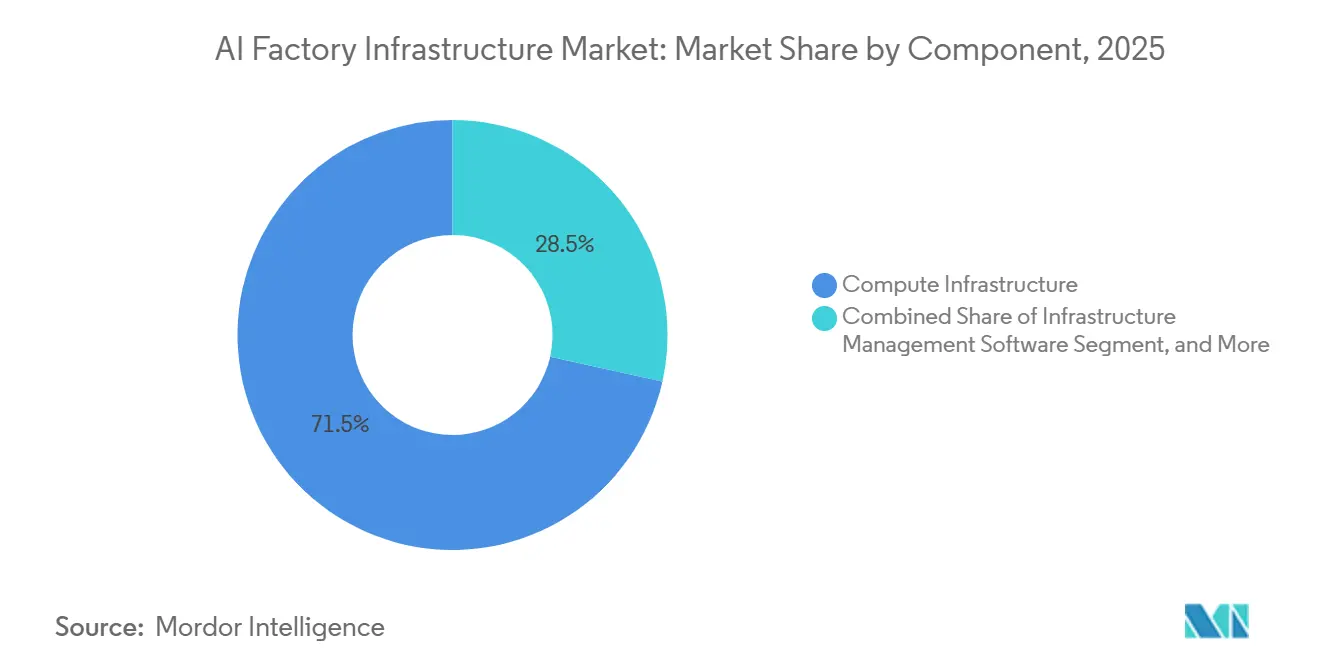

- By component, compute infrastructure held 71.53% of the AI factory infrastructure market share in 2025, while networking infrastructure is projected to expand at a 16.18% CAGR through 2031.

- By deployment model, cloud-based AI factories accounted for 65.36% share of the AI factory infrastructure market size in 2025, while hybrid AI factories are projected to grow at a 16.53% CAGR through 2031.

- By infrastructure type, large-scale AI superclusters held 40.27% share in 2025, while integrated AI pods and rack-scale systems are projected to advance at a 16.42% CAGR through 2031.

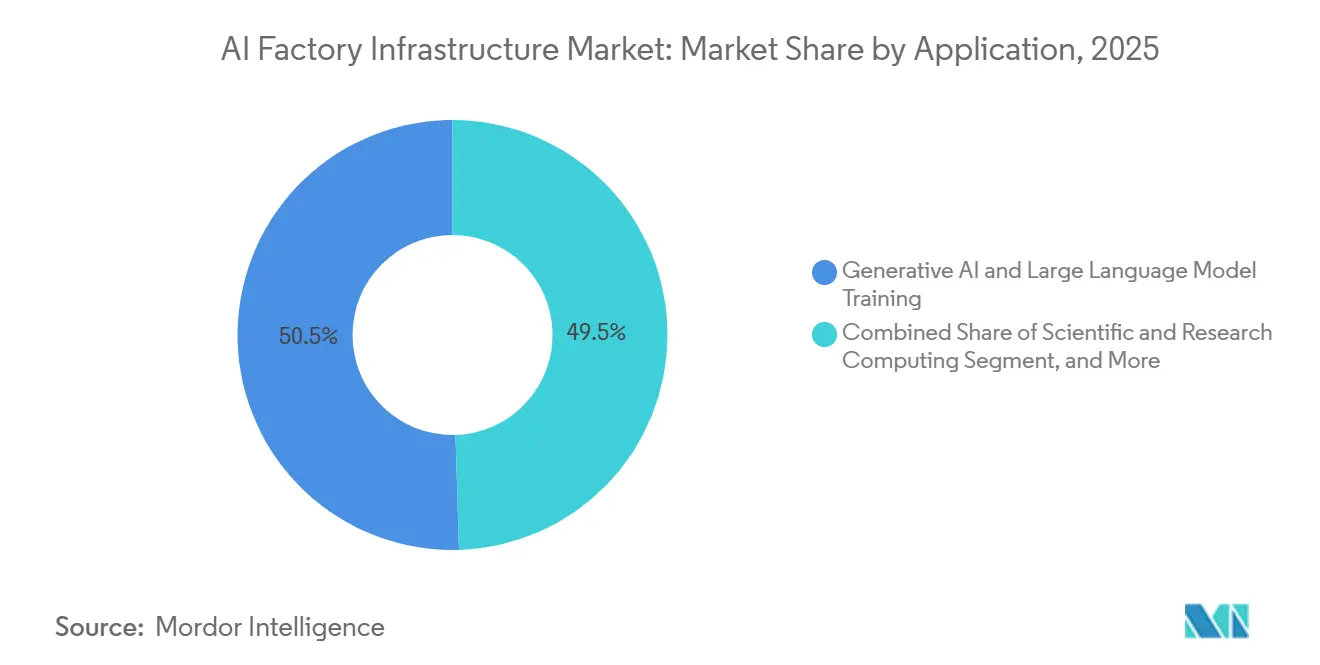

- By application, generative AI and LLM training accounted for 50.49% of the market in 2025, while AI inference and deployment are projected to expand at a 16.25% CAGR through 2031.

- By end user, hyperscalers and cloud providers held 67.16% share in 2025, while government and defense organizations are projected to grow at a 16.68% CAGR through 2031.

- By geography, North America held 62.35% share in 2025, while Asia-Pacific is projected to expand at a 16.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Factory Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Hyperscale AI Buildouts | +4.8% | Global, concentrated in North America with spillover to Asia-Pacific and Europe | Short term (≤ 2 years) |

| Rising Generative AI and Large Language Model Training Demand | +3.9% | Global, dominant in North America and China, accelerating across the Asia-Pacific | Short term (≤ 2 years) |

| Shift Toward AI-Native Data Center Architectures | +2.7% | North America and Europe core, and Asia-Pacific is accelerating | Medium term (2-4 years) |

| Enterprise Preference for Hybrid AI Deployment Models | +1.8% | Global, North America, and Europe are leading the adoption | Medium term (2-4 years) |

| Power-Density Engineering as a Competitive Differentiator | +1.1% | North America and Asia-Pacific core, spillover to the Middle East and Africa | Medium term (2-4 years) |

| Localized AI Sovereignty and Onshore Compute Mandates | +0.8% | European Union, United Kingdom, Canada, Japan, India, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Hyperscale AI Buildouts

Hyperscaler capital spending has moved to a level that is reshaping the AI factory infrastructure market across procurement, construction, and supply planning. Amazon reported USD 128.3 billion in capital expenditure for FY2025, while Alphabet reported USD 91.4 billion, pushing their combined 2025 spending above USD 219 billion and setting a high baseline for 2026 planning. Meta also committed USD 115 billion to USD 135 billion in 2026 infrastructure capex, which showed that large operators are treating AI capacity as a core investment line rather than a discretionary program. Microsoft’s Q1 FY2026 filing showed Azure revenue grew 40%, while Intelligent Cloud cost of revenue grew 43%, indicating how quickly AI infrastructure scale is pushing operating requirements higher. NVIDIA stated in its FY2026 10-K that data center availability, energy, and capital remain key factors for AI infrastructure buildout, which underlines how hyperscaler deployment pace is shaping the wider supply chain. This pattern is driving demand for system integration, networking fabrics, cooling systems, and power equipment across the AI factory infrastructure market, as each new build locks in spending far beyond the GPU layer.

Rising Generative AI And Large Language Model Training Demand

Generative AI and LLM training remain a major driver of the AI factory infrastructure market, as large-scale training still requires the highest-density compute environments. The AI factory infrastructure market is also expanding because inference capacity is being built alongside training capacity, rather than replacing it. Deployed AI services require low-latency inference systems that differ from frontier training clusters, widening the infrastructure surface area operators must provision. Google Cloud’s Virgo network design showed the scale of this requirement by linking 134,000 chips with up to 47 petabits per second of non-blocking bisectional bandwidth in a single fabric.[1]Google LLC, “Introducing Virgo Network Megascale Data Center Fabric,” Google Cloud Blog, cloud.google.com The application mix inside the AI factory infrastructure market reflects the same shift, with generative AI and LLM training leading in 2025 and AI inference and deployment posting the fastest forecast growth through 2031. This combination supports parallel demand for compute nodes, high-speed switching, storage throughput, and thermal control, rather than concentrating spending in a single layer of the stack.

Shift Toward AI-Native Data Center Architectures

The AI factory infrastructure market is moving away from standard colocation layouts because current AI racks require much higher power density and more advanced thermal control. Schneider Electric stated that AI-driven rack densities are moving past 100 kW, which requires direct-to-chip liquid cooling and changes to power distribution and facility design that legacy environments do not readily support. NVIDIA’s DSX AI factory reference design for the Vera Rubin generation calls for 100% liquid cooling across chips and networking components and uses a closed-loop system designed for 45°C inlet temperatures. Schneider Electric also noted in April 2026 that integrated power and liquid-cooling systems for AI data centers need to be engineered as a single system from the grid to the chip, which raises the project threshold for buyers and vendors alike. This shift is increasing the amount of non-compute spending tied to each deployment in the AI factory infrastructure market because power conversion, liquid loops, UPS systems, and control software now move together. It is also favoring vendors that can deliver integrated designs instead of isolated components, which is changing how contracts are awarded across the AI factory infrastructure market.

Enterprise Preference for Hybrid AI Deployment Models

Hybrid deployment is becoming increasingly important in the AI factory infrastructure market, as many enterprises need both cloud elasticity and direct control over sensitive workloads. The European Commission’s June 2026 sovereignty package, which included the proposed Cloud and AI Development Act, moved this issue further into formal policy by outlining an EU-wide framework for cloud sovereignty certification. The United Kingdom’s AI Hardware Plan also tied private investment in AI Growth Zones to sovereign and localized compute development, which supports the case for mixed deployment models rather than cloud-only architectures. HPE’s April 2026 expansion of its AI Factory portfolio included HPE AI Grid, which was designed to connect AI factories and distributed inference clusters across regional and edge locations. This is widening the software and networking opportunities in the AI factory infrastructure market, as orchestration, workload placement, and cross-site data handling become more important when compute is split across environments. It also makes the AI factory infrastructure market less dependent on a single deployment model, as buyers now plan around compliance, latency, and cost predictability simultaneously.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex for Compute, Power, and Cooling Systems | -2.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Grid Interconnection Delays and Power Availability Constraints | -1.9% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Semiconductor and High-Density Hardware Supply Bottlenecks | -1.1% | Global, with disproportionate impact in markets with export restrictions | Short term (≤ 2 years) |

| Scarcity of AI Infrastructure Engineering Talent | -0.8% | North America and Europe acutest, growing globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex for Compute, Power, and Cooling Systems

The AI factory infrastructure market remains constrained by the cost of building production-ready environments around modern GPU systems. Buyers are not only paying for compute, but also funding liquid-cooling loops, higher-capacity power systems, UPS upgrades, networking layers, and control software that scale with rack density. Schneider Electric’s engineering guidance made clear that an integrated power and cooling architecture is now a core requirement for high-density AI facilities, pushing project budgets upward even before full hardware deployment begins. Microsoft’s Q1 FY2026 filing showed a 300-basis-point decline in Intelligent Cloud gross margin, tied directly to AI infrastructure scaling costs, indicating that even large operators are under financial pressure as capacity expands. This cost profile is steering some organizations toward managed AI cloud capacity or smaller rack-scale deployments instead of greenfield builds across the AI factory infrastructure market. It is also increasing the value of vendors that can shorten deployment time or reduce integration complexity because time-to-production now has a direct budget effect.

Grid Interconnection Delays and Power Availability Constraints

Power access is one of the clearest limits on how fast the AI factory infrastructure market can add new capacity. Large deployments can move from planning to buildout faster than utilities can deliver reliable interconnection, creating a mismatch between demand and energization. This is forcing some operators to favor sites with pre-secured access, while others are studying behind-the-meter generation, direct utility partnerships, or other workarounds that add cost and complexity. The result is a stronger concentration of near-term supply in markets where permits and power readiness are already in place, which supports incumbents and slows some new entrants in the AI factory infrastructure market. These delays do not reduce the strategic need for AI capacity, but they can postpone revenue realization and shift customer demand toward existing cloud regions. Over time, this constraint can keep pricing firms in commissioned facilities while raising the entry threshold for operators that lack power certainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Networking Infrastructure Closes the Gap on Compute

Compute infrastructure held 71.53% of the AI factory infrastructure market share in 2025, which reflected the central role of GPU procurement in every large deployment cycle. That lead was tied to successive NVIDIA platform generations, including H100, Blackwell, and Vera Rubin, which kept compute at the front of capital allocation for both hyperscalers and specialist AI cloud operators. NVIDIA confirmed in April 2026 that Vera Rubin moved into full production, with Dell Technologies, HPE, Lenovo, and Super Micro Computer serving as system builders. Storage infrastructure and management software still matter because buyers need sustained throughput, workload scheduling, and tighter GPU utilization to make dense clusters economically viable.

Networking infrastructure is projected to grow at a 16.18% CAGR through 2031, making it the fastest-growing component of the AI factory infrastructure market. The rise of networking spend reflects the need to move data across larger GPU fabrics without creating bottlenecks at the switch layer. NVIDIA’s Vera Rubin platform includes Spectrum-X Ethernet options, which shows that open Ethernet architectures are becoming a more visible part of rack-scale AI system design. Co-packaged optics are also entering the discussion because lower latency and better power efficiency become more valuable as cluster sizes expand. This is creating a wider vendor field in the AI factory infrastructure market because performance is now being judged across compute, switching, fabric design, and system integration rather than at the accelerator layer alone.

By Deployment Model: Hybrid AI Factories Move Into The Mainstream

Cloud-based AI factories held a 65.36% share of the AI factory infrastructure market in 2025, reflecting the build pace and scale of AWS, Microsoft Azure, and Google Cloud. Public cloud remains central because hyperscalers control much of the commissioned capacity that can support large training and inference workloads at short notice. At the same time, on-premises AI factories remain relevant for organizations that need classified compute, national data control, or low-latency inference that the public cloud cannot fully provide. The European Commission, the United Kingdom, and Canada each moved policy attention toward sovereign compute in 2026, which supported the case for domestically controlled infrastructure in regulated environments.

Hybrid AI factories are projected to grow at a 16.53% CAGR through 2031, which makes them the fastest-growing deployment model in the AI factory infrastructure market. Organizations that began with cloud-only strategies are now balancing burst capacity against cost volatility, data movement limits, and latency requirements. That shift is widening demand for orchestration software that can place workloads across cloud, on-premise, regional, and edge environments without wasting GPU capacity. HPE AI Grid, launched in April 2026, directly addressed this requirement by linking AI factories and distributed inference clusters across multiple sites. Hybrid adoption also strengthens adjacent spending in the AI factory infrastructure market because network fabrics, storage coordination, and policy controls become more important when compute is distributed instead of centralized.

By Infrastructure Type: Rack-Scale Systems Gain Ground as Superclusters Mature

Large-scale AI superclusters accounted for 40.27% of the infrastructure type segment in 2025, making them the largest format in the AI factory infrastructure market. These environments are still the preferred choice for hyperscalers building training systems, where inter-GPU bandwidth, cooling, and power delivery must be engineered as a single architecture. AI server clusters and custom AI clusters serve a broader buyer base, ranging from enterprise users to specialist AI cloud operators. Custom clusters offer flexibility, but they also introduce greater design complexity and integration risk, which can slow deployment and increase procurement friction.

Integrated AI pods and rack-scale systems are projected to grow at a 16.42% CAGR through 2031, giving them the fastest expansion rate in the AI factory infrastructure market. NVIDIA’s GB200 NVL72 and Vera Rubin NVL72 systems are important here because they package compute, networking, and liquid cooling into a standard rack format that can shorten time-to-production.[2]NVIDIA Corporation, “NVIDIA Vera Rubin Ramps into Full Production to Power Agentic AI Factories Worldwide,” NVIDIA Investor Relations, investor.nvidia.com Dell delivered the first operational Vera Rubin NVL72 rack to CoreWeave in March 2026, demonstrating that integrated pod deployments can reach production faster than greenfield supercluster projects. Standards tied to power distribution and thermal design also matter more in this format because buyers in regulated sectors want pre-integrated systems that fit recognized engineering envelopes. As a result, the AI factory infrastructure market is seeing more value shift toward vendors that can sell validated rack-scale systems rather than only discrete hardware elements.

By Application: Inference Economics Broadens the Demand Base

Generative AI and LLM training accounted for 50.49% of the AI factory infrastructure market in 2025, making it the largest application in the market. This part of the AI factory infrastructure market still depends on the highest-bandwidth, lowest-latency environments because frontier model development requires sustained full-load operation across dense clusters. It also supports continued procurement of top-tier accelerators, as each new model generation continues to raise performance and cooling requirements. That is why supercluster spending remains relevant even as more downstream AI use cases move into production.

AI inference and deployment are projected to grow at a 16.25% CAGR through 2031, which makes it the fastest-growing application in the AI factory infrastructure market. Inference demand is rising because deployed AI services need large volumes of low-latency compute that must sit closer to users, enterprise systems, and operational workflows. Healthcare and drug discovery AI, digital twin and industrial AI, scientific computing, and autonomous systems all add demand, but each uses the infrastructure stack in a different way. Some need training-grade throughput, while others need secure, distributed, or latency-sensitive deployment conditions. This diversity matters because it keeps the AI factory infrastructure market from converging on only one architecture and supports spending across superclusters, rack-scale systems, cloud capacity, and hybrid environments at the same time.

By End User: Government And Defense Gain Strategic Weight

Hyperscalers and cloud providers held a 67.16% share in 2025, making them the largest end-user group in the AI factory infrastructure market. Their lead reflected the capital, operating scale, and supply chain leverage needed to commission large AI factories on compressed timelines. Enterprises formed the next major buyer group, and Dell stated in March 2026 that the Dell AI Factory with NVIDIA had passed 4,000 customer deployments globally. Research institutions, BFSI firms, manufacturers, and healthcare organizations each have distinct compliance requirements and workload needs, broadening the commercial base of the AI factory infrastructure market beyond large cloud operators.

Government and defense organizations are projected to grow at a 16.68% CAGR through 2031, which makes them the fastest-growing end-user segment in the AI factory infrastructure market. The White House issued NSPM-11 in June 2026, directing defense and intelligence agencies to develop a roadmap for advanced AI computing facilities with high-security requirements. Canada also committed up to CAD 1 billion (USD 730 million) to sovereign compute infrastructure, underscoring that secure national AI capacity has become a policy priority beyond the United States. These moves raise the strategic role of secure, domestically controlled compute and make government demand more consequential to vendor positioning. They also support a broader view of the AI factory infrastructure market, where defense, civilian public agencies, and sovereign compute programs now influence deployment patterns alongside commercial cloud spending.

Geography Analysis

North America held 62.35% of the AI factory infrastructure market share in 2025, which reflected the region’s lead in hyperscaler spending and commissioned data center capacity. Amazon and Alphabet together reported more than USD 219 billion in capital expenditure in 2025, keeping North America at the center of the AI factory infrastructure market and reinforcing their advantage in scaling new projects.[3]Alphabet Inc., “Annual Report on Form 10-K for the Fiscal Year Ended December 31, 2025,” Alphabet Investor Relations, abc.xyz The region also benefits from a dense ecosystem of OEMs, cloud operators, specialized builders, and power and cooling vendors that can quickly move large projects from design to deployment. Canada is becoming a supporting node because its sovereign compute program committed up to CAD 1 billion (USD 730 million) for domestic high-performance AI infrastructure. Power access remains the main near-term limit, meaning operators with pre-secured grid capacity are likely to retain an advantage in pricing, delivery timing, and expansion options.

Asia-Pacific is projected to grow at a 16.91% CAGR through 2031, which makes it the fastest-growing geography in the AI factory infrastructure market. Growth is being supported by sovereign compute priorities in Japan, India, Southeast Asia, and by China’s domestically funded expansion of AI infrastructure. The region is also seeing more interest in AI-grade data center design, where efficiency, thermal management, and localized control are becoming more important in procurement decisions. This keeps Asia-Pacific central to the next growth phase of the AI factory infrastructure market, even though North America still leads in current scale.

Europe, South America, and the Middle East and Africa remain smaller in current scale, but each has strategic importance in the AI factory infrastructure market. Europe is balancing stronger sovereign compute ambitions against grid and permitting delays, while the European Commission’s June 2026 technology sovereignty package is expected to support domestic deployment and cloud sovereignty certification. The United Kingdom has also elevated AI infrastructure in national planning through its AI Hardware Plan and its support for AI Growth Zones. The Middle East and Africa, especially the UAE and Saudi Arabia, are attracting interest because of available power and favorable data center economics, while South America remains earlier in development and more concentrated in Brazil’s primary urban markets.

Competitive Landscape

The AI factory infrastructure market is moderately concentrated at the compute and platform layers because NVIDIA’s GPU architecture and reference designs set the technical baseline for many new deployments. Dell Technologies, HPE, Lenovo, and Super Micro Computer are competing less on core accelerator design and more on integration speed, delivery execution, and supply chain certainty. NVIDIA’s April 2026 production announcement for Vera Rubin showed that more than 25 ecosystem partners were moving across the platform simultaneously, underscoring the scale of its ecosystem influence. CoreWeave also expanded its strategic role in the AI factory infrastructure market through a June 2026 agreement with NVIDIA to support more than 5 GW of AI factory buildout by 2030, underscoring the growing importance of pure-play AI infrastructure operators between traditional hosting and hyperscale cloud.[4]CoreWeave, Inc. and NVIDIA Corporation, “NVIDIA And CoreWeave Strengthen Collaboration to Accelerate Buildout of AI Factories,” CoreWeave Investor Relations, coreweave.com Dell strengthened its position in June 2026 with the PowerEdge XE8812, which scaled to 144 GPUs per rack and extended the density available in its AI Factory portfolio.

Competition is also rising in power, cooling, and systems engineering because high-density AI facilities cannot scale solely on compute. Schneider Electric has strengthened its position by publishing engineering guidance for AI data center design and by promoting integrated power and liquid cooling as a unified requirement for dense AI deployments. HPE’s April 2026 expansion of its AI Factory offering also showed that vendors are pushing into distributed inference orchestration and hybrid deployment tools, not only server integration. This matters because buyers increasingly want validated architecture, lower deployment risk, and better utilization rather than only access to hardware.

The networking layer remains one of the most open areas of competition in the AI factory infrastructure market because Ethernet-based fabrics are gaining visibility beside proprietary approaches. That shift can help vendors that compete through open systems design, fabric management, or energy efficiency rather than through accelerator ownership. China adds a separate competitive track, where domestic operators such as Alibaba Cloud and Tencent are building AI infrastructure at scale under different policy and ecosystem conditions. Europe may also create a distinct lane for sovereign AI factory providers if cloud sovereignty rules become more formal and procurement begins to favor operational independence. Across the broader AI factory infrastructure market, this keeps the landscape active and only moderately concentrated because leadership in compute does not fully determine outcomes in networking, cooling, software, or sovereign deployment models.

AI Factory Infrastructure Industry Leaders

NVIDIA Corporation

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dell Technologies introduced the PowerEdge XE8812 server featuring NVIDIA Vera Rubin NVL4 architecture, scaling to 144 GPUs per rack, the highest density in Dell's AI Factory portfolio, and advancing sovereign AI initiatives globally, the announcement came alongside accelerating international deployments spanning genomic research, engineering design, and government compute programs.

- June 2026: NVIDIA and CoreWeave announced an expanded collaboration to accelerate the buildout of more than 5 GW of AI factories by 2030, covering multiple NVIDIA infrastructure generations, including Rubin platform systems, Vera CPUs, and BlueField storage architectures, making it among the largest public AI factory capacity commitments by any non-hyperscale operator.

- June 2026: The European Commission proposed the European Technological Sovereignty Package, including the Cloud and AI Development Act and Chips Act 2.0, explicitly designed to streamline data center deployment across the EU, establish a harmonized sovereignty certification framework for cloud and AI services, and catalyze domestic AI factory investment.

- May 2026: The US DOD's FY2027 budget request included USD 29.5 billion for the AI Arsenal initiative to consolidate scattered GPU clusters into integrated, SCIF-accredited AI data centers across the joint force, the Pentagon's largest single AI infrastructure investment proposal.

Global AI Factory Infrastructure Market Report Scope

AI Factory Infrastructure refers to the integrated physical and digital systems that support the large-scale development, training, deployment, and operation of artificial intelligence workloads. The scope includes high-performance computing hardware, GPUs and accelerators, data storage, networking, power and cooling systems, data center facilities, orchestration software, and related services that enable enterprises, cloud providers, and research organizations to build and operate AI models efficiently.

The AI Factory Infrastructure Market Report is Segmented by Component (Compute Infrastructure, Networking Infrastructure, Storage Infrastructure, Infrastructure Management Software, and Other Components), Deployment (Cloud-Based AI Factories, On-Premise AI Factories, and Hybrid AI Factories), Infrastructure Type (AI Server Clusters, Integrated AI Pod / Rack-Scale Systems, Large-Scale AI Superclusters, and Custom AI Clusters), Application (Generative AI and Large Language Model Training, AI Inference and Deployment, Autonomous Systems Development, Scientific and Research Computing, Digital Twin and Industrial AI, and Healthcare and Drug Discovery AI), End User (Hyperscalers and Cloud Providers, Enterprises, Research and Academic Institutions, Healthcare and Life Sciences Organizations, BFSI Companies, Industrial and Manufacturing Companies, and Government and Defense Organizations), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Compute Infrastructure |

| Networking Infrastructure |

| Storage Infrastructure |

| Infrastructure Management Software |

| Other Components |

| Cloud-Based AI Factories |

| On-Premise AI Factories |

| Hybrid AI Factories |

| AI Server Clusters |

| Integrated AI Pod / Rack-Scale Systems |

| Large-Scale AI Superclusters |

| Custom AI Clusters |

| Generative AI and Large Language Model Training |

| AI Inference and Deployment |

| Autonomous Systems Development |

| Scientific and Research Computing |

| Digital Twin and Industrial AI |

| Healthcare and Drug Discovery AI |

| Hyperscalers and Cloud Providers |

| Enterprises |

| Research and Academic Institutions |

| Healthcare and Life Sciences Organizations |

| BFSI Companies |

| Industrial and Manufacturing Companies |

| Government and Defense Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Component | Compute Infrastructure | |

| Networking Infrastructure | ||

| Storage Infrastructure | ||

| Infrastructure Management Software | ||

| Other Components | ||

| By Deployment Model | Cloud-Based AI Factories | |

| On-Premise AI Factories | ||

| Hybrid AI Factories | ||

| By Infrastructure Type | AI Server Clusters | |

| Integrated AI Pod / Rack-Scale Systems | ||

| Large-Scale AI Superclusters | ||

| Custom AI Clusters | ||

| By Application | Generative AI and Large Language Model Training | |

| AI Inference and Deployment | ||

| Autonomous Systems Development | ||

| Scientific and Research Computing | ||

| Digital Twin and Industrial AI | ||

| Healthcare and Drug Discovery AI | ||

| By End User | Hyperscalers and Cloud Providers | |

| Enterprises | ||

| Research and Academic Institutions | ||

| Healthcare and Life Sciences Organizations | ||

| BFSI Companies | ||

| Industrial and Manufacturing Companies | ||

| Government and Defense Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the AI factory infrastructure space?

The AI factory infrastructure market size was USD 266.8 billion in 2025, is expected to reach USD 381.5 billion in 2026, and is forecast to reach USD 782.4 billion by 2031 at a 15.45% CAGR.

Which component leads to spending in AI factory infrastructure?

Compute infrastructure led in 2025 with a 71.53% share, driven by GPU procurement, dense training systems, and platform refresh cycles.

Why is networking becoming more important in AI factory deployments?

Networking infrastructure is the fastest-growing component at a 16.18% CAGR because larger GPU clusters need stronger data movement, lower latency, and better fabric efficiency as deployments scale.

Why are hybrid AI factories gaining traction with enterprises?

Hybrid models are growing at a 16.53% CAGR because many organizations need a mix of cloud burst capacity, on-premise control, data residency compliance, and lower inference latency.

Which application is expanding the fastest through 2031?

AI inference and deployment is the fastest-growing application at a 16.25% CAGR as more AI services move into production and require low-latency, production-grade infrastructure.

Which regions are shaping near-term expansion the most?

North America remained the largest region with 62.35% share in 2025, while Asia-Pacific is projected to grow the fastest at a 16.91% CAGR through 2031 as sovereign compute programs and domestic capacity expansion accelerate.

Page last updated on: