AI-enabled Wound Analysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

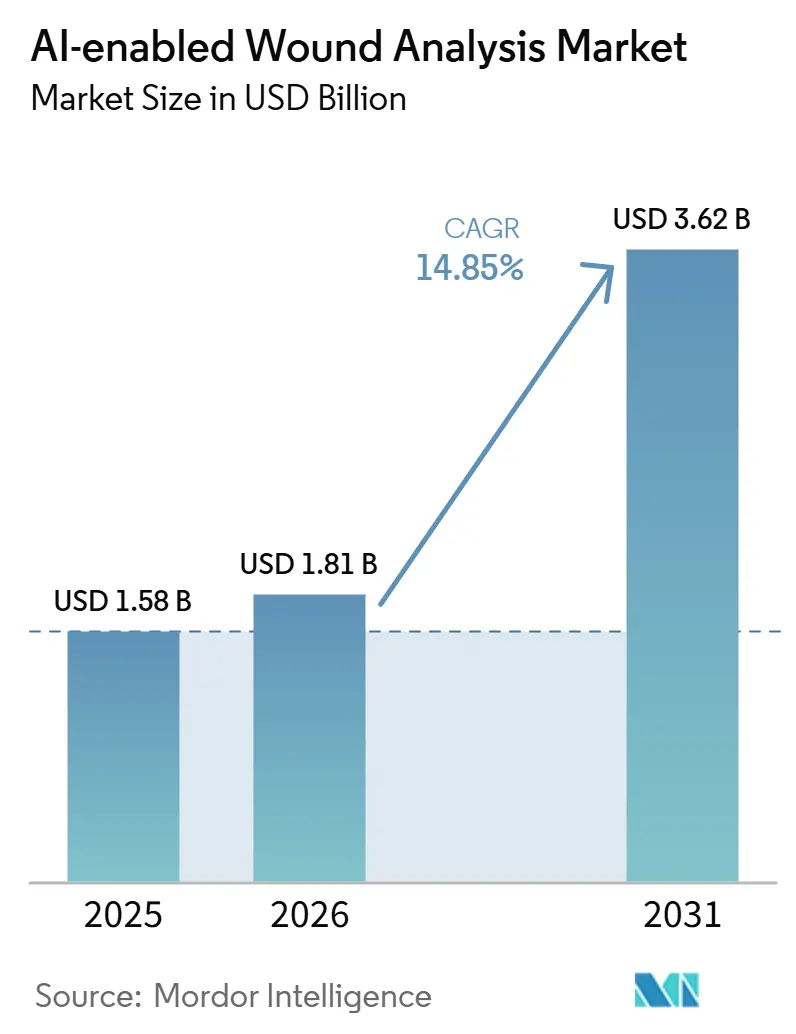

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 3.62 Billion |

| Growth Rate (2026 - 2031) | 14.85% CAGR |

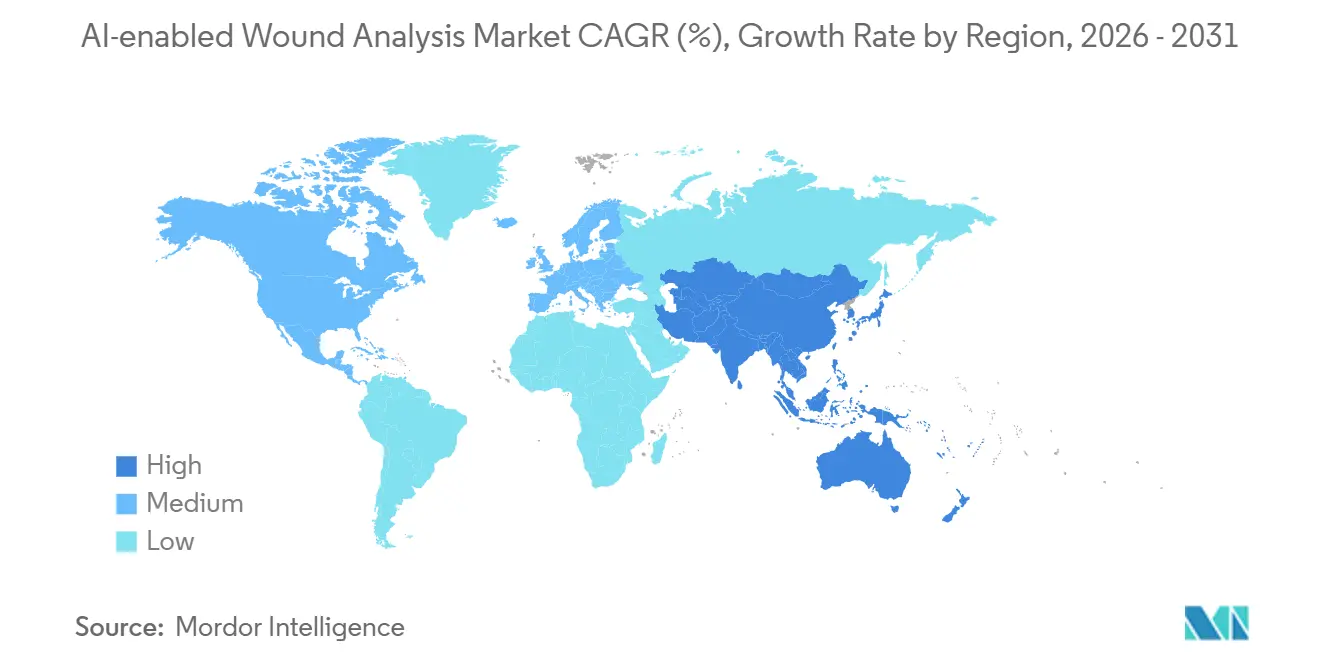

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-enabled Wound Analysis Market Analysis by Mordor Intelligence

The AI-enabled Wound Analysis Market size was valued at USD 1.58 billion in 2025 and is estimated to grow from USD 1.81 billion in 2026 to reach USD 3.62 billion by 2031, at a CAGR of 14.85% during the forecast period (2026-2031).

The market is moving away from subjective visual checks and paper records toward image-based workflows that can be used at the bedside, in the home, and through telemedicine platforms. An estimated 53.1 million Americans had diabetes in 2025, and diabetic foot ulcers affect 15% to 34% of people with diabetes over their lifetime, which keeps the need for frequent and standardized wound surveillance high.[1]Human Wound and Its Burden: Updated 2025 Compendium of Estimates Documentation-linked reimbursement pressure, shortages in wound specialty staff, and the push to connect imaging outputs with electronic records are moving adoption beyond early pilot users into broader health system buying cycles. Regional growth is being shaped by North America's stronger reimbursement and regulatory environment and by Asia-Pacific's faster digital health buildout, especially where governments are supporting AI deployment in care delivery. The competitive field includes focused imaging specialists and larger wound care companies, while skin-tone validation gaps and integration friction continue to shape the next stage of platform adoption.

Key Report Takeaways

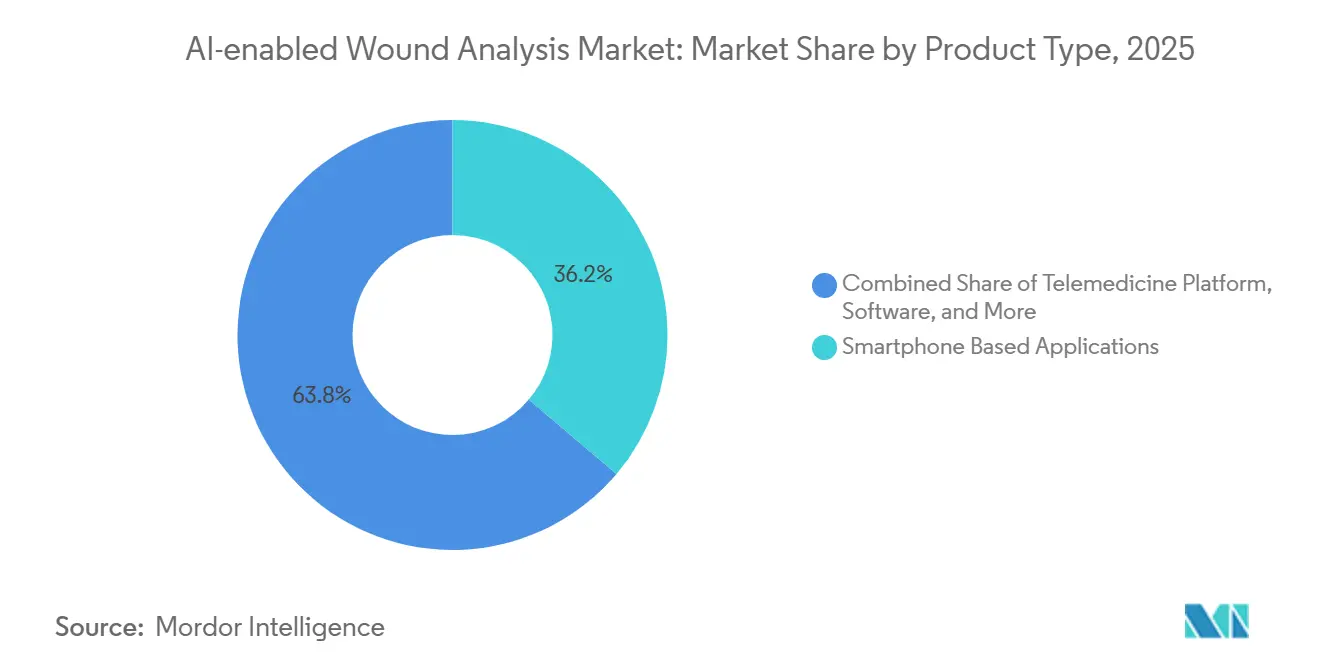

- By product type, smartphone applications held 36.18% revenue share in 2025, while telemedicine platforms are projected to expand at an 18.81% CAGR through 2031.

- By application, wound assessment and monitoring accounted for 41.68% of revenue in 2025, while healing prediction and decision support segment is forecast to grow at a 17.86% CAGR through 2031.

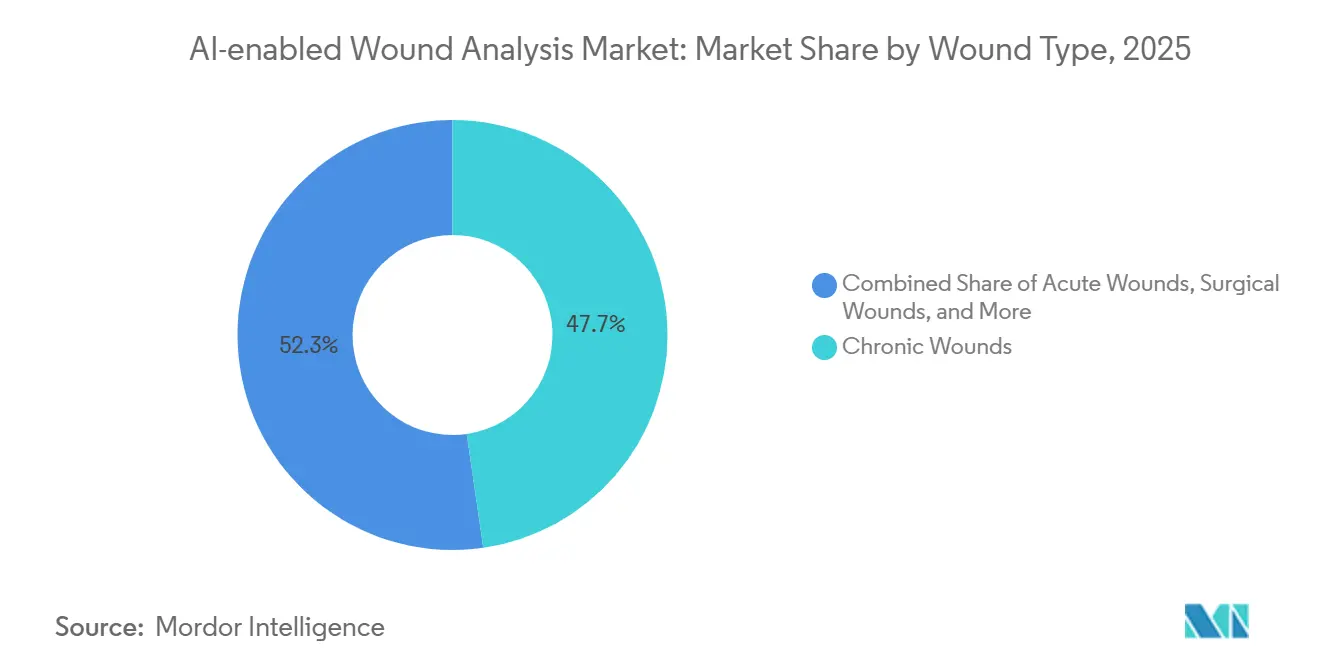

- By wound type, chronic wounds held 38.17% share in 2025, while surgical wounds are expected to advance at a 16.67% CAGR through 2031.

- By end user, hospitals held 47.55% share in 2025, while home healthcare agencies are projected to grow at a 17.34% CAGR through 2031.

- By geography, North America held 41.87% share in 2025, while Asia-Pacific is forecast to expand at a 19.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-enabled Wound Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Wound Burden and Diabetic Ulcer Surveillance Needs | +2.80% | Global, concentrated in North America, Europe, and South & East Asia | Long term (≥ 4 years) |

| Hospital Workflow Pressure and Demand for Faster Bedside Assessment | +2.20% | North America and Europe, with expanding relevance in Australia | Medium term (2-4 years) |

| Standardized Documentation and Reimbursement Traceability Requirements | +1.80% | North America, the EU, and Australia | Short term (≤ 2 years) |

| Expansion of Remote Wound Monitoring and Telewound Programs | +2.50% | North America, the UK, and APAC | Medium term (2-4 years) |

| AI-Assisted Infection Detection from Multimodal Imaging at Point of Care | +2.60% | Global, with the strongest adoption in North America, Europe, Japan, South Korea, and Australia | Medium term (2–4 years) |

| Cross-Device Interoperability with EHR and Care Coordination Platforms | +2.10% | North America and Europe, with growing adoption in APAC healthcare systems | Medium (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Wound Burden and Diabetic Ulcer Surveillance Needs

Chronic wound prevalence is creating a surveillance need that manual assessment cannot meet at scale. Globally, approximately 18.6 million people worldwide develop diabetic foot ulcers each year, and these ulcers precede 80% of lower-limb amputations among people diagnosed with diabetes.[2]Global Trends in Diabetic Foot Research (2004–2023): A Bibliometric Study Based on the Scopus DatabaseSoutheast Asia alone had more than 107 million people with diabetes in 2025, a figure projected to reach 185 million by 2050. Diabetic foot ulcer recurrence can reach 65% within 3 to 5 years after initial healing, which shifts the value of AI wound analysis from one-time support to ongoing surveillance infrastructure. In Europe, chronic wounds had a prevalence of 2.2 per 1,000 people, and diabetic foot disease is estimated to affect 16 million people over their lifetime across the WHO European Region, which supports the case for image-based monitoring at scale.

Hospital Workflow Pressure and Demand for Faster Bedside Assessment

Wound care takes a heavy share of nursing time in inpatient settings, and burnout is making the capacity problem more severe. A Net Health Q1 2025 survey found that 77.00% of wound care professionals reported significant burnout, while 47% identified smart documentation tools as a critical relief mechanism. AI-enabled bedside imaging reduces measurement variability, removes ruler-based errors, and lets non-specialist staff capture clinically valid documentation during routine care. A 2025 study published in PMC found that a digitally enabled wound care system used across 14 home health branches reduced skilled nursing visits per episode and created potential annual savings of up to USD 958,201 across a single home health organization.[3]Clinical, Operational, and Economic Benefits of a Digitally Enabled Wound Care Program in Home Health: Quasi-Experimental, Pre-Post Comparative Study This cost-avoidance logic helps explain why hospitals in the AI-enabled wound analysis market are adopting documentation and surveillance tools even when formal evidence development is still catching up with operational demand.

Standardized Documentation and Reimbursement Traceability Requirements

Reimbursement is increasingly tied to structured wound documentation rather than free-form clinical notes, and this is strengthening demand for image-led assessment platforms. Providers now place more value on timestamped wound images and objective measurements because they can support utilization review, internal quality checks, and payer-facing records. AI-generated wound images also fit more easily into audit-ready documentation standards than handwritten or inconsistent bedside notes. At the same time, HIPAA image-storage requirements and the broader regulatory focus on AI-enabled medical tools are raising the technical bar for wound documentation software. This is pushing procurement toward enterprise-grade platforms in the AI-enabled wound analysis market that can manage capture, storage, and record integration in one system.

Expansion of Remote Wound Monitoring and Telewound Programs

Remote wound monitoring is moving from an emergency workaround into a more permanent care model across chronic and post-acute settings. A 2025 systematic review and meta-analysis in JMIR mHealth and uHealth found that telemedicine improved healing scores, healing time, amputation rate, pain, and quality of life in chronic wound care. A 2025 French study in PMC reported that remote monitoring of chronic wounds reduced in-hospital consultations and lowered care costs versus conventional monitoring. In Japan, publicly funded KAKENHI research programs are developing AI wound management systems for home care deployment in response to aging demographics and bed constraints. In the United Kingdom, the NHS Transforming Wound Care Programme documented a 50% reduction in documentation time and the avoidance of 2,000 face-to-face visits in one trust, which is helping move these tools into standard district nursing workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Validation Gaps Across Diverse Skin Tones And Wound Presentations | -1.50% | Global, most acute in diverse urban markets across North America, the UK, and MEA | Long term (≥ 4 years) |

| Integration Friction With Legacy EHR And Nonstandard Imaging Workflows | -1.30% | Global, most pronounced in APAC emerging markets and non-FHIR-compliant U.S. facilities | Medium term (2-4 years) |

| Restraint: Reimbursement Uncertainty for AI-Enabled Wound Assessment in Some Care Settings | −1.90% | United States (non-standardized payer coverage), Latin America, Middle East & Africa, and parts of Asia-Pacific | Short to Medium term (1–3 years) |

| Restraint: Data Governance Constraints for Image Storage, Consent, and Cross-Site Analytics | −2.30% | Europe (GDPR), North America (HIPAA), Australia, and countries implementing stricter health data regulations | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Clinical Validation Gaps Across Diverse Skin Tones and Wound Presentations

AI wound analysis tools still face a measurable equity gap that creates clinical and procurement risk for health systems. A 2025 PLOS One study evaluating a surgical wound AI system reported 89% overall sensitivity, but it also found lower detection accuracy for some wound features in darker skin tones.[4]Wound imaging software and digital platform to assist review of surgical wounds using patient smartphones: The development and evaluation of artificial intelligence (WISDOM AI study) An IEEE BHI study in 2025 described datasets designed for diabetic foot ulcer recognition in communities of color because many existing models have been trained mainly on lighter-skinned populations. Published work in npj Digital Medicine has also reinforced the wider issue of skin-tone assessment and performance reporting in medical AI, which increases pressure on vendors to show more inclusive validation. A 2025 review in the Chinese Journal of Injury Repair and Wound Care likewise identified data diversity as a central unresolved challenge for AI use in chronic wound management.

Integration Friction with Legacy EHR and Nonstandard Imaging Workflows

EHR interoperability remains one of the main barriers to wider deployment in the AI-enabled wound analysis market. Hospitals and post-acute providers still operate across mixed digital environments that include proprietary records, older messaging standards, and uneven API access, which creates integration work for every deployment. Smaller community hospitals and long-term care facilities are especially exposed because many of them do not have the infrastructure needed for real-time image exchange and workflow automation. HIPAA-compliant image storage and consent management add another layer of implementation work before wound photos can move reliably across systems. The result is that device-level clearance alone does not guarantee scaled clinical adoption, which gives larger vendors with stronger integration teams an advantage over smaller specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartphone Applications Anchor Adoption; Telemedicine Platforms Define the Next Growth Tier

Smartphone applications held 36.18% of the AI-enabled wound analysis market size in 2025, which made them the largest product segment because the imaging hardware was already in the hands of bedside and community clinicians. Telemedicine platforms are projected to expand at an 18.81% CAGR through 2031 as health systems continue to invest in asynchronous wound review models that shift specialist time away from routine documentation. This product split reflects a practical buying pattern in which providers first choose the lowest-friction capture tool and then add review workflows around it. EMR integration software remains less visible in revenue terms, but it has a structurally important role because it determines whether wound images and measurements change the clinical workflow or stay trapped in a standalone app. AI-enabled imaging hardware occupies the high-precision tier, especially in spectral, fluorescence, and near-infrared formats, where buyers are looking for deeper tissue and infection-related signals.

The imaging hardware tier is moving forward through regulatory validation and tighter pairing with software platforms. Swift Medical's FDA 510(k)-cleared Swift Ray 1, announced in March 2026, showed this direction by linking handheld spectral imaging with a broader AI wound platform intended for hospital, home health, and remote care use. Product competition in the AI-enabled wound analysis market is therefore separating into mobile-first tools built for scale and device-led platforms built for depth. Smartphone-based applications remain easiest to deploy where budgets and training time are limited. Hardware-led platforms hold stronger positions in settings that want regulatory credentials and richer wound data at the point of care.

By Application: Assessment Anchors Revenue; Healing Prediction Reshapes Long-Term Value

Wound assessment and monitoring held 41.68% share in 2025 because standardized measurement remains the first and most common use case across the AI-enabled wound analysis market. Healing prediction and decision support is projected to grow at a 17.86% CAGR through 2031 as providers start to use AI not only to describe the wound but also to guide treatment and follow-up. This changes the commercial discussion from documentation quality alone to expected healing outcomes and better use of staff time. Infection detection and tissue characterization remain clinically important, but adoption is slower because these workflows often rely on more advanced devices and extra training. Remote wound documentation and care coordination are also expanding because image capture has become more central to how providers manage wounds across care settings.

The application mix shows that buyers usually start with measurement and then move toward prediction. MolecuLightDX received FDA qualification as a Medical Device Development Tool in January 2026, which strengthened the clinical standing of fluorescence-based wound measurement in research and product evaluation. As telemedicine investment continues, remote documentation is becoming harder to separate from broader care coordination. This means the AI-enabled wound analysis industry is moving toward applications that combine measurement, review, and longitudinal planning rather than isolated imaging functions alone.

By Wound Type: Chronic Wounds Drive Volume; Surgical Wounds Accelerate on Digital Documentation Momentum

Chronic wounds held 38.17% share in 2025, giving them the largest role in the AI-enabled wound analysis market share because diabetes, venous insufficiency, and pressure injuries create persistent monitoring demand. Surgical wounds are projected to grow at a 16.67% CAGR through 2031 as digital postoperative monitoring becomes more common through patient-facing and clinician-facing tools. Burn wounds are also gaining commercial traction after Spectral AI received FDA De Novo Classification for the DeepView System in May 2026. Acute wounds remain a smaller segment, with AI use concentrated in emergency and rapid reassessment workflows where speed and consistency matter most.

Chronic wound demand remains durable because recurrence, comorbidity, and repeated imaging needs create long follow-up cycles. Surgical and burn applications are widening the role of the AI-enabled wound analysis market beyond chronic care and into higher-acuity pathways. This mix gives vendors room to balance volume-driven chronic wound workflows with predictive and specialty applications that can command stronger clinical attention.

By End User: Hospitals Anchor Market Share; Home Healthcare Drives the Next Expansion Wave

Hospitals held 47.55% share in 2025 because they manage the most complex wounds, the highest documentation burden, and the greatest reimbursement exposure. Home healthcare agencies are projected to grow at a 17.34% CAGR through 2031 as care shifts outside institutions and staffing shortages make standardized remote documentation more valuable. Specialty clinics are adopting AI wound tools more selectively, usually where imaging precision can change treatment choices and follow-up intervals. Long-term care facilities remain underpenetrated even though patient need is strong.

End-user demand in the AI-enabled wound analysis market is tracking reimbursement risk and workforce strain more closely than simple wound volume alone. Hospitals still anchor spending because procurement teams value audit-ready records and consistent bedside capture. Home healthcare is becoming the clearest expansion channel because mobile AI tools let generalist staff document wounds with more specialist-level consistency. Long-term care can accelerate later as lower-cost mobile platforms reduce training and integration barriers.

Geography Analysis

North America held 41.87% of AI-enabled wound analysis market share in 2025, which made it the largest regional segment. The region benefits from stronger regulatory infrastructure, deeper specialist presence, and greater payer focus on documentation standards. Canada also acts as an active development hub, reflected in Swift Medical's 2026 FDA 510(k) clearance and federal co-investment through the DIGITAL Supercluster program. Mexico remains earlier in adoption because healthcare IT gaps still limit near-term rollout. This makes North America the reference region for product design, validation expectations, and procurement timing across the broader AI-enabled wound analysis market.

Europe is advancing through a more evidence-first adoption path, and the United Kingdom stands out as the most mature deployment setting in the region. Germany and France are progressing within the EU MDR framework, which favors vendors that can support stronger post-market evidence and compliance discipline. eKare's April 2025 partnership with Oxford Health NHS Foundation Trust reflects the European preference for proving clinical and economic value before scaling procurement.

Asia-Pacific is projected to expand at a 19.34% CAGR from 2026 to 2031, which makes it the fastest-growing region in the AI-enabled wound analysis market size by geography. India's digital health buildout, China's AI device review momentum, and Japan's publicly funded wound AI work are supporting that pace. A 2025 Chinese review identified wound assessment, remote monitoring, and decision support as the main clinical deployment areas for AI in chronic wound management.

Competitive Landscape

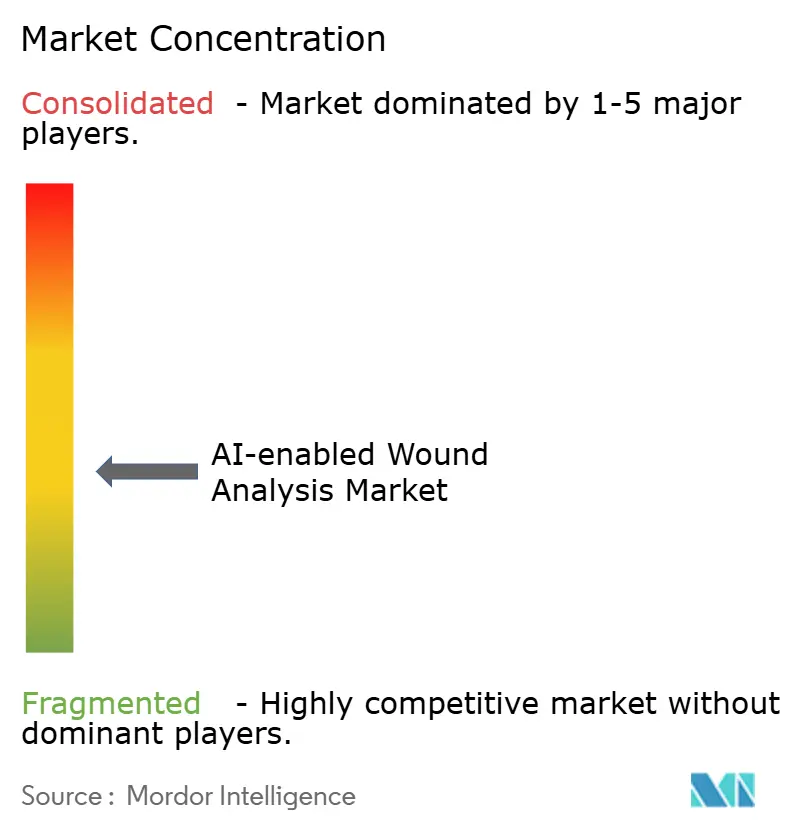

The competitive landscape in the AI-enabled wound analysis market remains moderately fragmented, with specialists and diversified wound care companies competing from different starting points. MolecuLight, Swift Medical, eKare, ARANZ Medical, and Net Health compete on imaging modality, clinical evidence depth, and integration breadth. Smith+Nephew, Solventum, and ConvaTec approach the space from broader wound management portfolios and established customer relationships. Data scale is becoming a durable advantage, illustrated by Swift Medical's platform being trained on more than 34.00 million clinically validated wound images. Regulatory validation also carries weight, and MolecuLightDX's FDA MDDT qualification in January 2026 strengthens the procurement position of vendors with clinically validated measurement tools.

Strategic moves are increasingly focused on workflow control rather than stand-alone imaging. In December 2025, Net Health integrated MolecuLight with Tissue Analytics, enabling fluorescence and thermal wound images to flow into Net Health WoundExpert and third-party Tissue Analytics-enabled EHR environments through a standards-based API. In April 2025, eKare partnered with Oxford Health NHS Foundation Trust to demonstrate the clinical and economic impact of its inSight 3D imaging and AI analytics platform in community nursing. In May 2026, Spectral AI secured FDA De Novo clearance for DeepView, which gave the company a differentiated position in predictive burn wound imaging.

The main white space now sits where wound images, care plans, and follow-up actions can be linked across care settings in real time. Privacy rules, interoperability standards, and post-market evidence demands are raising the engineering threshold for smaller vendors. This supports gradual consolidation at the data and integration layer, even while product-level competition stays broad. The AI-enabled wound analysis market, therefore, favors companies that can combine trusted measurement, compliant data handling, and workable integration in one platform.

AI-enabled Wound Analysis Industry Leaders

eKare, Inc.

Healthy.io Ltd.

MolecuLight Inc.

Net Health Systems, Inc.

Swift Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Spectral AI received FDA De Novo Classification for its DeepView System, authorizing commercial distribution in the United States for burn care across burn centers, trauma centers, and emergency departments.

- March 2026: Swift Medical received FDA 510(k) clearance for Swift Ray 1, a next-generation handheld spectral imaging device that integrates with its AI-powered Skin & Wound platform, trained on over 34 million clinically validated wound images.

- January 2026: MolecuLight's MolecuLightDX wound measurement function was qualified by the U.S. FDA as a Medical Device Development Tool, only the 20th qualification since the program's 2017 inception.

- December 2025: Net Health announced the platform integration of MolecuLight with Tissue Analytics, providing HIPAA-compliant automated documentation of fluorescence and thermal wound images directly into Net Health WoundExpert and any third-party Tissue Analytics-enabled EHR via a single standards-based connectivity API, creating end-to-end wound intelligence from bacterial imaging to clinical documentation.

Global AI-enabled Wound Analysis Market Report Scope

The AI-enabled wound analysis market comprises artificial intelligence-powered software platforms and imaging solutions designed to automatically assess, measure, classify, and monitor acute and chronic wounds using digital images and clinical data. These technologies leverage machine learning, deep learning, and computer vision algorithms to support healthcare professionals in wound evaluation, healing progression analysis, infection detection, and treatment decision-making.

The AI-enabled wound analysis market is segmented by product type, application, wound type, end user, and geography. By product type, it is further divided into smartphone-based applications, telemedicine platforms, software, and AI-enabled imaging hardware. By application, it is segmented into wound assessment and monitoring, healing prediction and decision support, infection detection and tissue characterization, and remote wound documentation and care coordination. By wound type, the market is segmented into chronic wounds, acute wounds, surgical wounds, and burn wounds. By end user, the market is segmented into hospitals, home healthcare agencies, specialty clinics, and long term care facilities. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Smartphone Based Applications |

| Telemedicine Platforms |

| Electronic Medical Record Integration Software |

| AI Enabled Imaging Hardware |

| Wound Assessment and Monitoring |

| Healing Prediction and Decision Support |

| Infection Detection and Tissue Characterization |

| Remote Wound Documentation and Care Coordination |

| Chronic Wounds |

| Acute Wounds |

| Surgical Wounds |

| Burn Wounds |

| Hospitals |

| Home Healthcare Agencies |

| Specialty Clinics |

| Long Term Care Facilities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Smartphone Based Applications | |

| Telemedicine Platforms | ||

| Electronic Medical Record Integration Software | ||

| AI Enabled Imaging Hardware | ||

| By Application | Wound Assessment and Monitoring | |

| Healing Prediction and Decision Support | ||

| Infection Detection and Tissue Characterization | ||

| Remote Wound Documentation and Care Coordination | ||

| By Wound Type | Chronic Wounds | |

| Acute Wounds | ||

| Surgical Wounds | ||

| Burn Wounds | ||

| By End User | Hospitals | |

| Home Healthcare Agencies | ||

| Specialty Clinics | ||

| Long Term Care Facilities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the AI-enabled wound analysis space by 2031?

It is forecast to reach USD 3.62 billion by 2031, rising from USD 1.81 billion in 2026 at a 14.85% CAGR.

Which region currently leads adoption?

North America led with 41.87% share in 2025 because of stronger reimbursement pressure, regulatory maturity, and specialist presence.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is projected to grow at 19.34% CAGR through 2031, supported by digital health expansion and policy-backed AI deployment.

Which product category holds the largest share today?

Which product category holds the largest share today? Smartphone applications led with 36.18% share in 2025 because they use existing clinician devices and carry lower deployment friction.

Why are home healthcare agencies becoming important buyers?

Home healthcare is projected to grow at 17.34% CAGR because staffing shortages and decentralized care models increase the value of remote, standardized wound documentation.

What is the main barrier to wider deployment?

The biggest barriers are skin-tone validation gaps and EHR integration friction, which raise clinical risk and slow enterprise rollout.

Page last updated on: