AI Enabled Care Delivery Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 54.27 Billion |

| Market Size (2031) | USD 193.42 Billion |

| Growth Rate (2026 - 2031) | 28.94% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Enabled Care Delivery Transformation Market Analysis by Mordor Intelligence

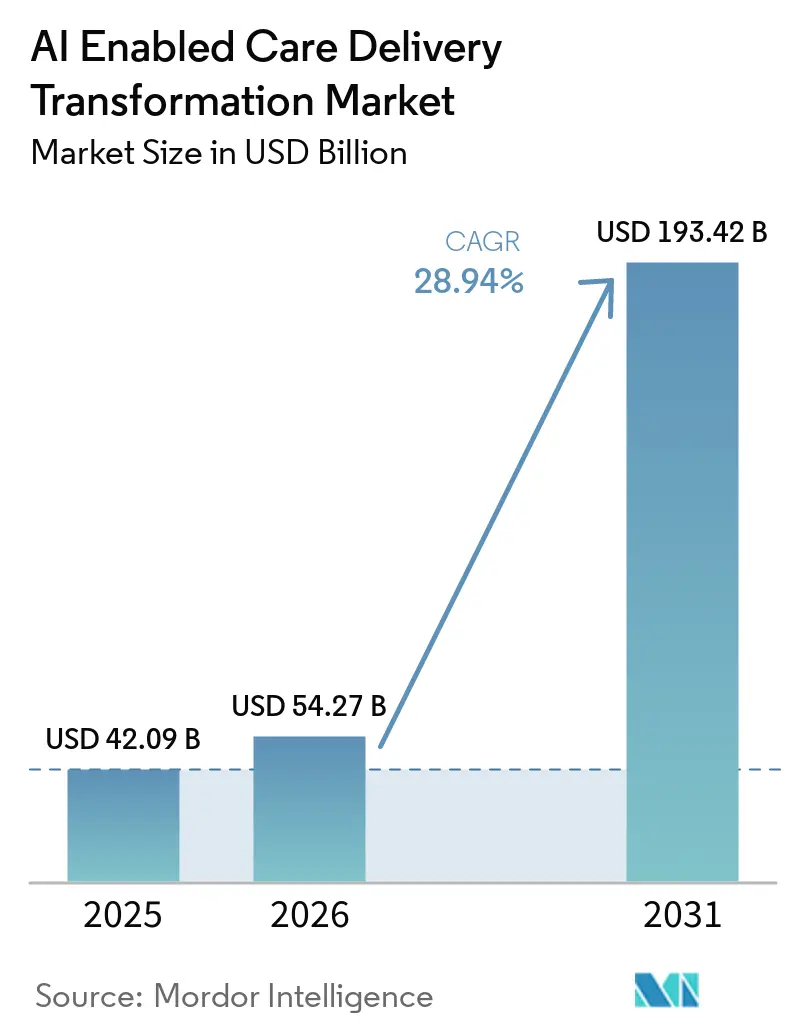

The AI-Enabled Care Delivery Transformation Market was valued at USD 42.09 billion in 2025 and is projected to grow to USD 54.27 billion in 2026, reaching USD 193.42 billion by 2031. The market is expected to register a robust CAGR of 28.94% during the forecast period from 2026 to 2031.

Health systems now treat algorithmic tools as core infrastructure, embedding them in revenue-cycle workflows, clinical documentation, and care-coordination platforms that protect operating margins and mitigate wage inflation. The U.S. Department of Health and Human Services reported 271 live AI deployments across its agencies in 2025 and anticipates a 70% rise by 2027, confirming that public-sector demand is scaling from pilots to production. On the regulatory front, the U.S. Food and Drug Administration’s January 2025 draft guidance for lifecycle management of AI enabled medical devices, followed by Good AI Practice principles in January 2026, created a predictable approval path that reduces time-to-market risk and spurs private-capital inflows. Providers that move quickly are capturing measurable value: Microsoft’s DAX Copilot, integrated with Epic’s electronic-health-record system, now processes more than 1 million patient encounters each month and frees roughly five minutes of documentation time per visit capacity that translates into two additional daily patient slots per clinician.

Key Report Takeaways

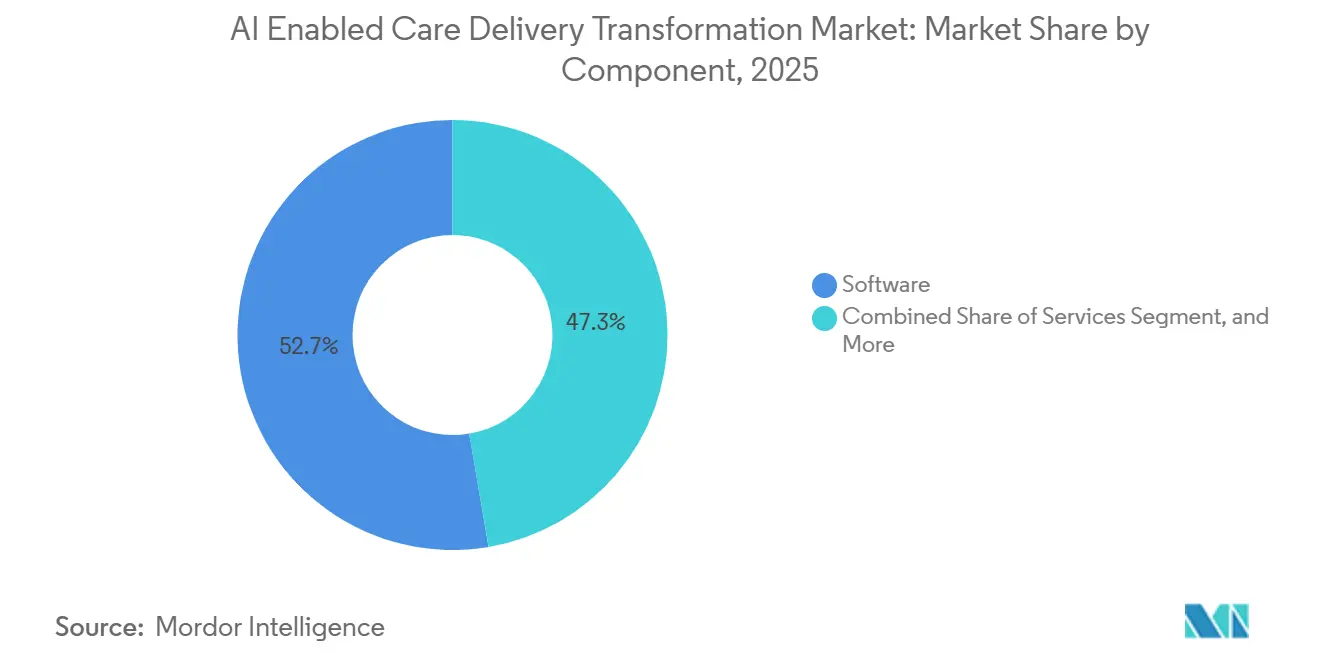

- By component, software solutions held 52.68% of the AI enabled care delivery transformation market share in 2025, while modular AI platforms are forecast to expand at a 29.71% CAGR to 2031.

- By application, administrative & workflow automation accounted for 34.61% CAGR growth, overtaking clinical decision support’s 32.46% revenue share in 2025 in the AI enabled care delivery transformation market.

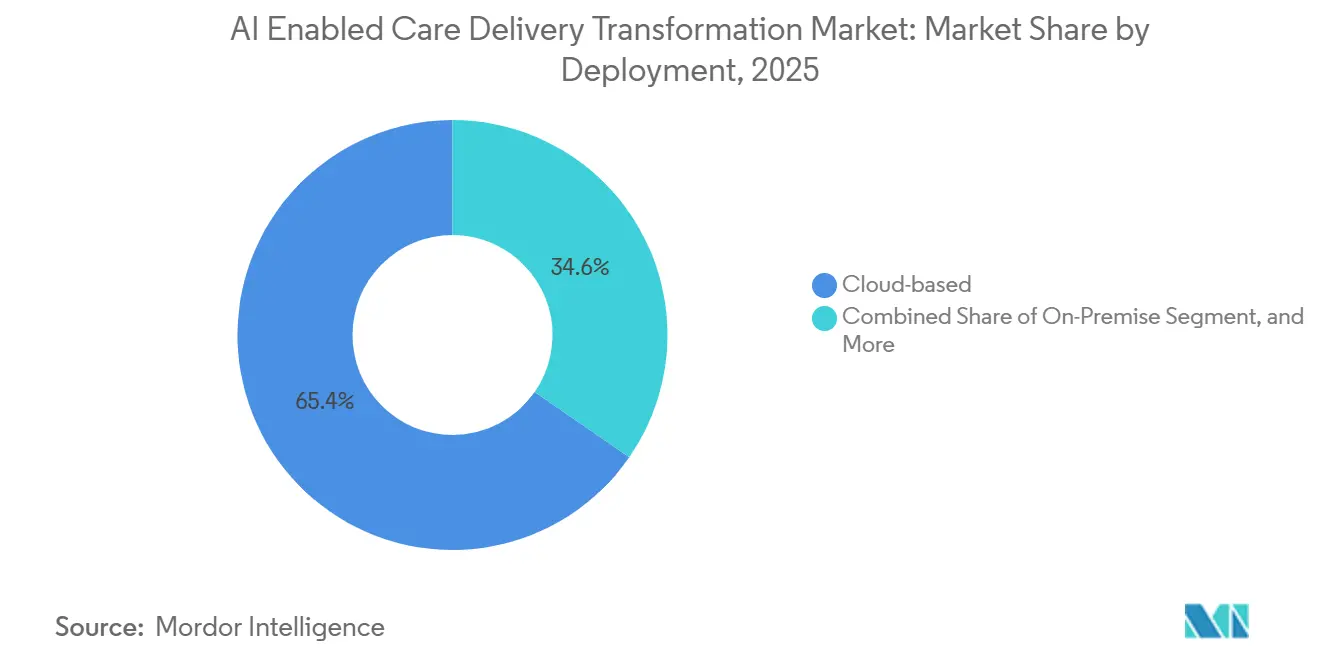

- By deployment, cloud models commanded 65.37% of the 2025 base, while hybrid approaches are on track for a 31.45% CAGR due to data-sovereignty rules in the AI enabled care delivery transformation market.

- By end user, hospitals and health systems led with 48.38% of the AI enabled care delivery transformation market size in 2025; digital health providers are rising fastest at a 30.24% CAGR through 2031.

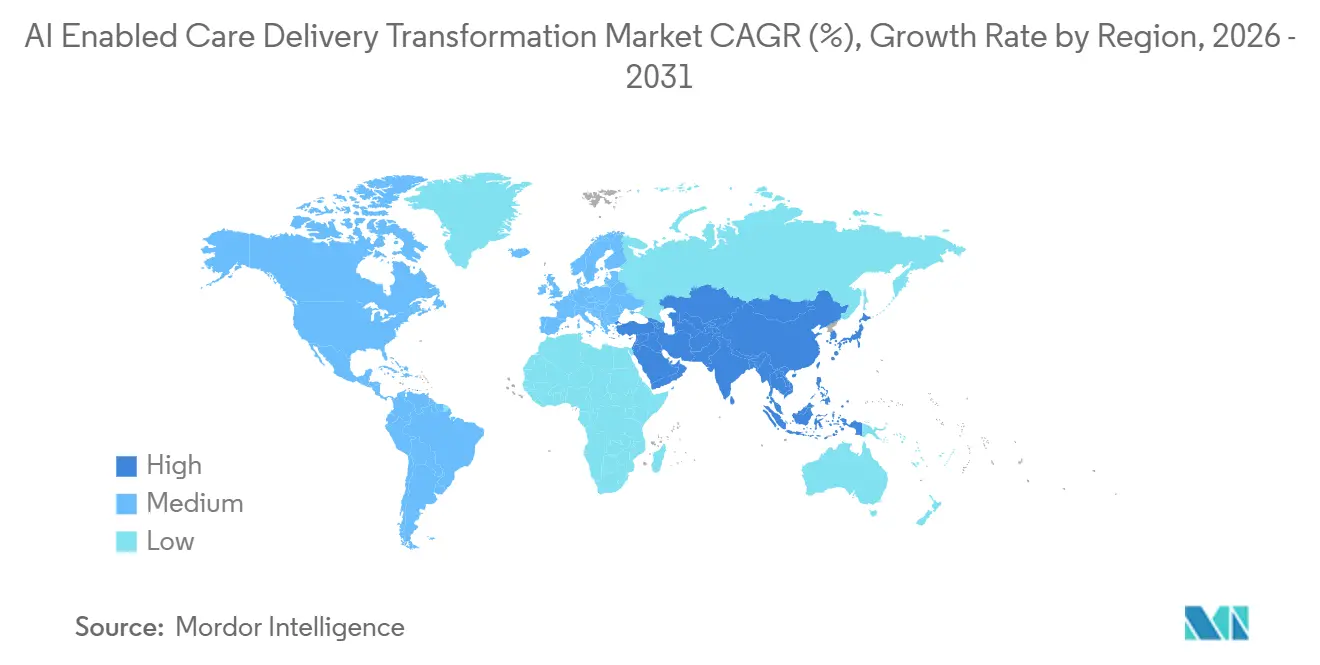

- By geography, North America held 36.46% share in 2025. Asia-Pacific is forecast to be the fastest growing at an 33.48% CAGR through 2031 in the AI enabled care delivery transformation market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Enabled Care Delivery Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Adoption in Clinical Workflows | +8.2% | Global, with North America and Europe leading deployment density | Medium term (2-4 years) |

| Growing Need to Reduce Healthcare Cost & Operational Burden | +7.5% | Global, particularly acute in North America due to labor shortages | Short term (≤ 2 years) |

| Explosion of Healthcare Data | +6.1% | Global, with Asia-Pacific experiencing fastest data-volume growth | Long term (≥ 4 years) |

| Shift Toward Value-Based & Personalized Care Models | +5.8% | North America and Europe, with CMS and NHS mandates driving adoption | Medium term (2-4 years) |

| Synthetic Data & Federated Learning | +3.4% | Global, with Europe leading due to GDPR requirements | Long term (≥ 4 years) |

| Modular AI Micro-Services for Plug-and-Play EHR Integration | +2.9% | Global, accelerated by the HHS HTI-5 interoperability rule | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AI Adoption in Clinical Workflows

Ambient documentation tools reached 68% U.S. hospital adoption in 2025, a 62% year-on-year increase that addresses physician burnout as much as efficiency.[1]Eliciting Insights, “Ambient Clinical Documentation Adoption in U.S. Health Systems,” Microsoft’s DAX Copilot, deployed across Epic sites, processes in excess of 1 million encounters per month and trims visit documentation by roughly five minutes, allowing each clinician to see two more patients daily. Hospitals that scale ambient AI report an 18% reduction in voluntary clinician turnover, recouping subscription costs within 14 months. Clinical-documentation-improvement platforms reached 43% penetration in 2025, propelled by Medicare Severity–Diagnosis-Related Group optimization, which lifts case-mix index scores and reimbursement. The FDA’s Good AI Practice principles, published in January 2026, outline ten lifecycle tenets that give vendors regulatory clarity as they branch into diagnostic and therapeutic domains.

Growing Need to Reduce Healthcare Cost & Operational Burden

Administrative automation delivered USD 258 billion in cost savings for U.S. providers in 2024, with revenue-cycle management and prior authorization representing 64% of that value.[2]CAQH, “2024 Index: Administrative Cost Savings Through Automation,” Persistent wage inflation averaging 5.3% annually from 2022 to 2025 widens the ROI gap between human labor and algorithmic tools. A 2025 National Bureau of Economic Research study projected full-scale AI deployment could unlock USD 200-360 billion in annual savings by automating 40-60% of billing, scheduling, and utilization-review tasks.[3]National Bureau of Economic Research, “Economic Impact of AI in Healthcare Administration,” CMS guidance released in August 2025 formally allowed automated approvals for low-complexity prior-authorization requests, accelerating natural-language-processing investment. Implementation paybacks materialize within six to nine months, half the horizon typical for clinical decision support, making administrative use cases the near-term growth engine.

Explosion of Healthcare Data

Electronic health record systems generated 2.5 exabytes of clinical data worldwide in 2025 and are doubling roughly every 18 months. Federated-learning architectures let algorithms train across distributed datasets while keeping protected health information local; an NIH-led sepsis consortium demonstrated parity with centralized methods across 47 hospitals in 2025.[4]National Institutes of Health, “Federated Learning for Sepsis Prediction,” Complementing federated learning, synthetic-data generators create statistically faithful records that eliminate re-identification risk. The FDA’s January 2026 guidance endorsed synthetic datasets for certain pre-market validations, provided sponsors prove distributional fidelity. Combined, these technologies resolve the historical trade-off between data liquidity and privacy, enabling multi-site collaborations without centralizing raw patient records.

Shift toward Value-Based & Personalized Care Models

CMS aims to place all traditional Medicare beneficiaries in value-based arrangements by 2030, driving provider demand for predictive risk stratification, care-gap closure, and readmission prevention tools. Participation in Innovation Center pilots climbed 25% between 2023 and 2024, now covering more than 50 million lives. AI enabled population-health platforms integrate claims, labs, social determinants, and wearable streams to individualize care plans that raise quality scores and curb the total cost of care. Personalized medicine is converging with payer incentives: in 2025, the FDA cleared three AI-guided companion diagnostics that match oncology patients to targeted therapies, limiting adverse events linked to trial-and-error prescribing. As reimbursement rewards precision over volume, scalable algorithms become indispensable for managing millions of covered lives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Security & Evolving Regulations | -4.3% | Global, with Europe experiencing highest compliance burden under GDPR and AI Act | Short term (≤ 2 years) |

| Integration & Workflow Adoption Challenges | -3.7% | Global, particularly acute in legacy health systems with on-premise EHR infrastructure | Medium term (2-4 years) |

| Model-Drift Risk Requiring Continuous Clinical Validation | -2.8% | Global, with FDA and EMA requiring ongoing performance monitoring | Long term (≥ 4 years) |

| Rising AI Compute Carbon Footprint Conflicting with ESG Goals | -1.9% | Global, particularly relevant for health systems with Scope 3 emission reduction targets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Security & Evolving Regulations

The European Union’s AI Act, effective August 2024 with phased enforcement in 2025, designates most clinical decision aids as high-risk, compelling conformity assessments, third-party audits, and post-market surveillance that extend commercialization by 9-12 months. GDPR further restricts automated outputs that create “legal or similarly significant effects” without human review, reducing efficiency gains by forcing manual checkpoints. Breach incidents involving protected health information rose 32% in 2025, heightening executive hesitation to move sensitive workloads to cloud platforms despite superior AI capacity. The FDA’s August 2025 Change-Control guidance lets sponsors pre-define algorithm updates, trimming supplemental filings, but it does not override international data-localization laws that fragment training corpora. Until harmonization emerges, compliance drag will temper near-term growth, particularly for vendors aiming at multinational rollouts.

Integration & Workflow Adoption Challenges

Hospitals racing to meet 2010-2015 Meaningful-Use incentives installed monolithic EHRs ill-suited to FHIR integration, making middleware expensive and platform migrations disruptive. A 2025 CHIME survey named interoperability gaps the top deployment barrier, cited by 58% of IT executives. Clinician skepticism compounds technical friction: algorithms that contradict ingrained pattern-recognition heuristics often see muted uptake unless accompanied by transparent logic. The HTI-5 mandate for surfacing decision-support rationale aims to build trust, yet early feedback suggests overly technical explanations suppress adoption if cognitive overhead rises. Lifecycle management remains another hurdle; model drift requires continuous retraining, a capability many hospitals outsource, increasing the total cost of ownership and vendor lock-in.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Eclipse Custom Builds

Software solutions commanded 52.68% of the AI enabled care delivery transformation market share in 2025, yet modular AI platforms are accelerating at a 29.71% CAGR through 2031 as providers favor configurable building blocks over bespoke code. The AI enabled care delivery transformation market size for platform offerings is projected to expand rapidly as Google’s Med-PaLM 2 and Microsoft’s Azure Health Data Services enable institution-level fine-tuning in days rather than quarters. Cloud vendors bundle pre-trained language and vision models that shorten validation cycles and lower capital intensity. Services revenue implementation, training, and managed analytics rise in tandem because many health systems lack in-house data-science capacity.

The December 2025 HTI-5 Rule codified FHIR interoperability, allowing vendors to “build once, deploy anywhere,” which amplifies component reuse and tilts momentum toward platform ecosystems. NVIDIA’s 2025 healthcare-optimized GPUs reduced inference latency for imaging models by 40%, making specialized hardware an infrastructure prerequisite for real-time use cases. The FDA’s Good AI Practice guidance endorses modular pipelines that isolate preprocessing from inference, letting sponsors update sub-components without re-validation a stance that inherently privileges platform architectures over monoliths.

By Application: Administrative Automation Overtakes Clinical Tools

Administrative and workflow automation experienced the fastest growth, achieving a 34.61% CAGR, driven by near-term return on investment and tangible cost savings. Revenue-cycle use cases alone represent USD 165 billion in annual spending, and AI-based prior-authorization engines cut approval time from 3.2 to 1.1 days in 2025. The CMS August 2025 memo permitting automated low-complexity approvals removed a regulatory choke point, unlocking payer/provider procurement cycles.

Clinical decision support still held a 32.46% revenue share because quality-metric improvement under value-based reimbursement preserves top-line revenue. Sepsis early-warning systems, for example, reduce mortality 15-20% when coupled with rapid-response workflows, avoiding costly ICU admissions. Patient engagement and virtual-care tools gained traction as 30 million remote monitoring devices streamed physiologic data into AI triage pipelines in 2025. Remote monitoring now consolidates around chronic-disease management, where near-real-time parameter feeds let algorithms titrate medications before decompensation.

By Deployment: Hybrid Models Bridge Governance and Agility

Cloud deployments owned 65.37% of 2025 revenue thanks to elastic compute, managed services, and pay-as-you-go pricing. AWS HealthLake and Google Cloud Healthcare API together processed more than 500 million clinical transactions in 2025 with HIPAA eligibility. Yet the hybrid model is growing at 31.45% CAGR as health systems keep identifiers on-premise for HIPAA compliance while shipping de-identified images to GPU clusters.

Microsoft Azure Arc and Google Anthos extend cloud services into private data centers, cutting hybrid-orchestration overhead by around 35% and opening the model to mid-size providers. On-premise persists where state privacy statutes or international data-localization laws bar cross-border transfers, or when perpetual EHR licenses make migration uneconomic until refresh cycles. HTI-5’s API mandates the removal of environment lock-in, letting organizations shift workloads without ripping out integrations, thus accelerating hybrid uptake

By End User: Digital Disruptors Gain Share

Hospitals and health systems retained 48.38% of the AI enabled care delivery transformation market size in 2025, but digital health providers are expanding at a 30.24% CAGR as they deploy cloud-native platforms without legacy capital constraints. Companies like Babylon Health logged over 10 million virtual consultations monthly in 2025, achieving 60-70% lower per-encounter cost through algorithmic triage. Hospitals still dominate high-acuity scenarios, such as surgical robotics, intraoperative imaging, and critical-care analytics that demand on-site infrastructure.

Ambulatory care centers occupy a middle ground; they adopt AI for scheduling, no-show prediction, and chronic-care management, yet lack the budget of academic medical centers. FDA draft guidance from January 2025 streamlined 510(k) filings for software-as-a-medical-device, lowering entry barriers for digital-only providers. Payers, pharma, and device firms increasingly embed AI in claims adjudication, drug discovery, and post-market surveillance, blurring traditional vertical boundaries.

Geography Analysis

North America generated 36.46% of 2025 revenue, underpinned by CMS reimbursement programs that reward AI-driven quality gains and offset labor shortages exacerbated by 5.3% annual wage inflation. The December 2025 HTI-5 Rule mandates decision-support transparency and FHIR APIs, lowering interoperability costs unique to the region. Canada’s single-payer systems deploy AI for wait-time optimization, while Mexico’s private-hospital chains bundle AI decision support into cloud EHR subscriptions for urban populations.

Asia-Pacific is the fastest-growing region at a 33.48% CAGR. China’s National Healthcare Security Administration processed over 200 million AI-assisted prior-authorization claims per month in 2025, slashing approval times 60%. India’s Ayushman Bharat Digital Mission is integrating smartphone-based AI screening for tuberculosis and diabetic retinopathy to reach rural districts. Japan’s aging society fuels remote monitoring demand, while Australia’s Therapeutic Goods Administration harmonized device review processes with the FDA in 2025, easing foreign market entry. South Korea earmarked USD 2 billion for precision-oncology AI through 2025 grants.

Europe grows more slowly because the AI Act adds 9-12 months to commercialization timelines, although the European Health Data Space promises to unlock federated learning once member states align governance. Germany pilots AI-supported diabetes programs that integrate wearable feeds with EHRs, and the U.K.’s NHS deployed AI radiology tools across 200 hospitals in 2025 to ease clinician shortages. Middle East & Africa benefit from Gulf sovereign-wealth investment: Saudi Arabia’s Vision 2030 allocated USD 1.5 billion to AI smart-hospital projects in 2025. South America’s ministries pilot epidemic-prediction algorithms, leveraging mobile-data telemetry to detect outbreaks faster than lab confirmations.

Competitive Landscape

Hyperscale clouds Microsoft, Google, AWS bundle AI services with IaaS and offer EHR integration toolkits. EHR incumbents such as Epic, Oracle Health, and athenahealth embed proprietary models to defend installed bases, while specialists like Tempus, Viz.ai, and Aidoc focus on oncology, stroke triage, and imaging, leveraging clinical validation moats. Epic’s late-2024 partnership with Microsoft to embed DAX Copilot illustrates a hybrid approach where incumbents license external foundation models rather than build from scratch.

Interoperability rules favor nimble entrants offering modular micro-services that plug into FHIR APIs, compressing sales cycles and lowering switching costs. NVIDIA monetizes its 40% latency advantage in healthcare GPUs by bundling inference software and professional services, creating both hardware and ecosystem lock-in. Continuous-learning capabilities that automate drift detection and retraining align with the FDA’s Predetermined Change-Control guidance, granting operational advantage to platforms with built-in lifecycle governance. NIH-led federated consortia suggest future differentiation may hinge on orchestrating multi-institutional research networks rather than owning a single algorithm.

AI Enabled Care Delivery Transformation Industry Leaders

Amazon Web Services (AWS)

Epic Systems

Google (Alphabet)

IBM

Microsoft

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Partnered with to launch the AI-powered “Health100” platform. The solution was developed to integrate healthcare data sources and provide real-time health management, personalized insights, and AI-driven care delivery support for consumers.

- January 2026: The FDA released Good AI Practice principles, outlining ten lifecycle tenets that reduce compliance uncertainty for pharmaceutical sponsors integrating machine-learning into research and post-market safety.

- December 2025: HHS finalized the HTI-5 Rule, mandating FHIR APIs and decision-support transparency to lower interoperability barriers.

Global AI Enabled Care Delivery Transformation Market Report Scope

As per the scope of the report, AI enabled care delivery transformation refers to the use of artificial intelligence technologies such as machine learning, natural language processing, and predictive analytics to optimize and automate healthcare delivery processes. It enhances clinical decision-making, patient monitoring, and care coordination by enabling real-time, data-driven insights across care settings. The goal is to improve treatment outcomes, operational efficiency, and patient experience while reducing healthcare costs.

The AI enabled care delivery transformation market is segmented by component, application, deployment, end user, and geography. By component, the market is segmented into software, services, and platforms / AI models. By application, the market is segmented into clinical decision support, patient engagement & virtual care, administrative & workflow automation, remote monitoring/telehealth, and others. By deployment, the market is segmented into cloud-based, on-premise, and hybrid. By end user, the market is segmented into hospitals & health systems, ambulatory care centers, digital health providers, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Software |

| Services |

| Platforms / AI Models |

| Clinical Decision Support |

| Patient Engagement & Virtual Care |

| Administrative & Workflow Automation |

| Remote Monitoring / Telehealth |

| Others |

| Cloud-based |

| On-premise |

| Hybrid |

| Hospitals & Health Systems |

| Ambulatory Care Centers |

| Digital Health Providers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Platforms / AI Models | ||

| By Application | Clinical Decision Support | |

| Patient Engagement & Virtual Care | ||

| Administrative & Workflow Automation | ||

| Remote Monitoring / Telehealth | ||

| Others | ||

| By Deployment | Cloud-based | |

| On-premise | ||

| Hybrid | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory Care Centers | ||

| Digital Health Providers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the AI Enabled Care Delivery Transformation market?

The AI enabled care delivery transformation market size stands at USD 54.27 billion in 2026, with a 28.94% CAGR projected through 2031.

Which segment is expanding fastest by revenue?

Administrative and workflow automation leads with a 34.61% CAGR because paybacks materialize within nine months.

Who are the dominant platform providers?

Hyperscale clouds Microsoft Azure, Google Cloud, and AWS bundle AI services with FHIR connectors that accelerate deployment.

Why is Asia-Pacific growing faster than other regions?

National digital-health programs in China and India prioritize AI enabled telemedicine to mitigate physician shortages, driving a 25.48% CAGR.

What regulatory actions in 2025-2026 most influenced adoption?

The FDA’s Good AI Practice principles and HHS’s HTI-5 Rule created a predictable device-approval path and mandated FHIR interoperability, lowering deployment risk.

Page last updated on: