AI-Driven Retinal Screening Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.57 Billion |

| Market Size (2031) | USD 1.30 Billion |

| Growth Rate (2026 - 2031) | 17.85% CAGR |

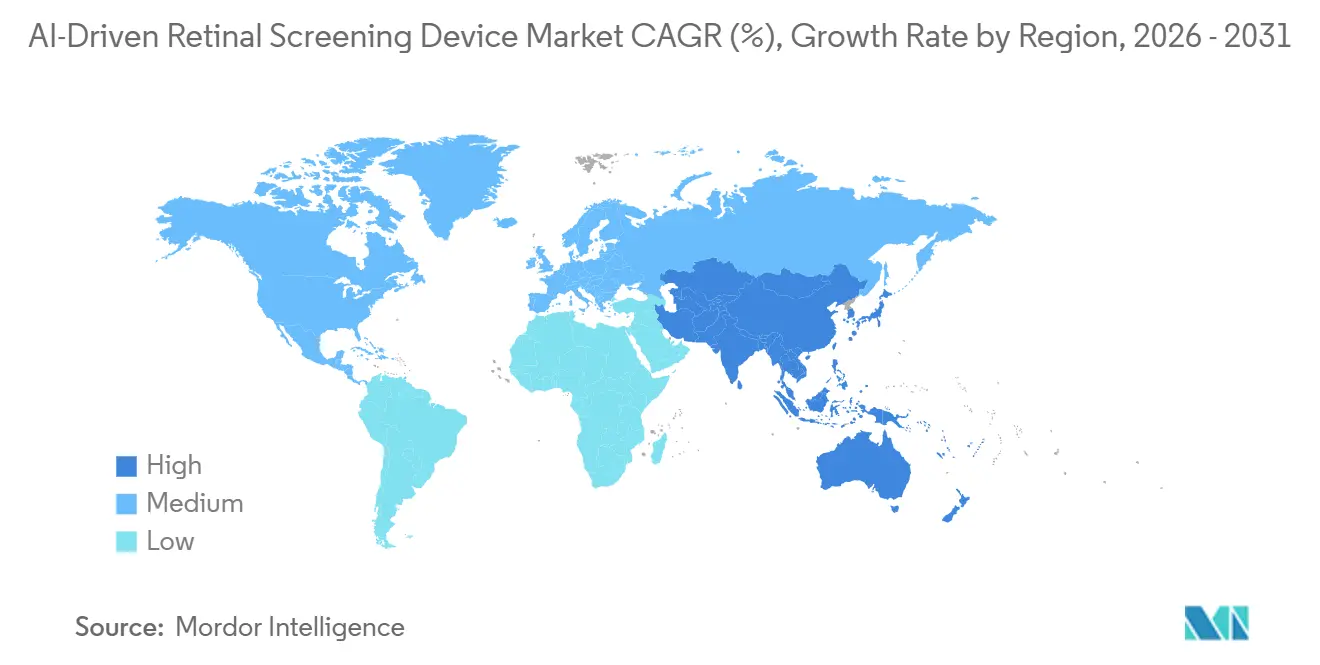

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Driven Retinal Screening Device Market Analysis by Mordor Intelligence

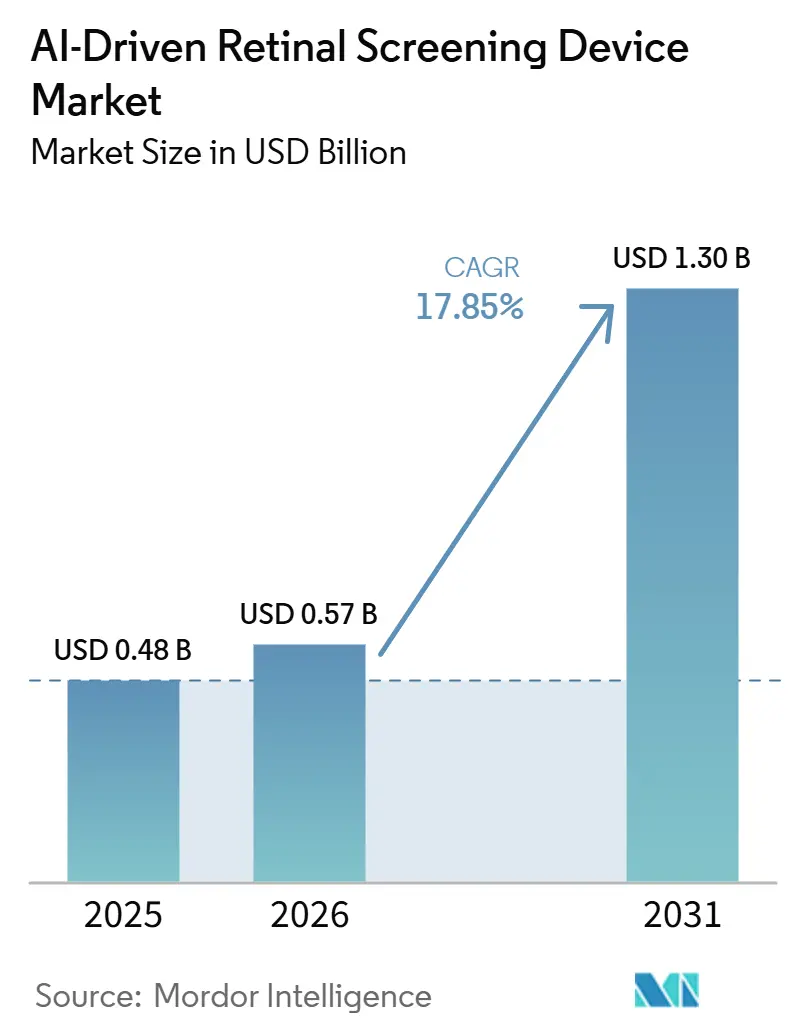

The AI-driven retinal screening device market size is expected to grow from USD 484.53 million in 2025 to USD 570.52 million in 2026 and is forecast to reach USD 1,298.60 million by 2031 at 17.85% CAGR over 2026-2031.

The AI-driven retinal screening device market is moving into a stronger adoption phase because autonomous AI clearances, specialist shortages, and the shift of diabetic eye care into primary care are now working together instead of developing separately. The AI-driven retinal screening device market is also benefiting from a software-led revenue model, since recurring subscriptions, integration work, and cloud services are carrying more value than one-time hardware sales. Demand conditions remain durable because diabetes prevalence continues to rise, a large share of cases remain undiagnosed, and diabetic retinopathy screening demand is far larger than what specialist-only care models can absorb at scale. The AI-driven retinal screening device market is also shaped by a split competitive structure, where imaging incumbents use installed device bases and workflow access, while pure-play AI firms compete through autonomous screening performance and cloud flexibility. Reimbursement inconsistency and stricter data governance still limit rollout speed in some care settings, but those same pressures favor larger vendors that can sustain compliance, integration, and post-market monitoring across multiple jurisdictions

Key Report Takeaways

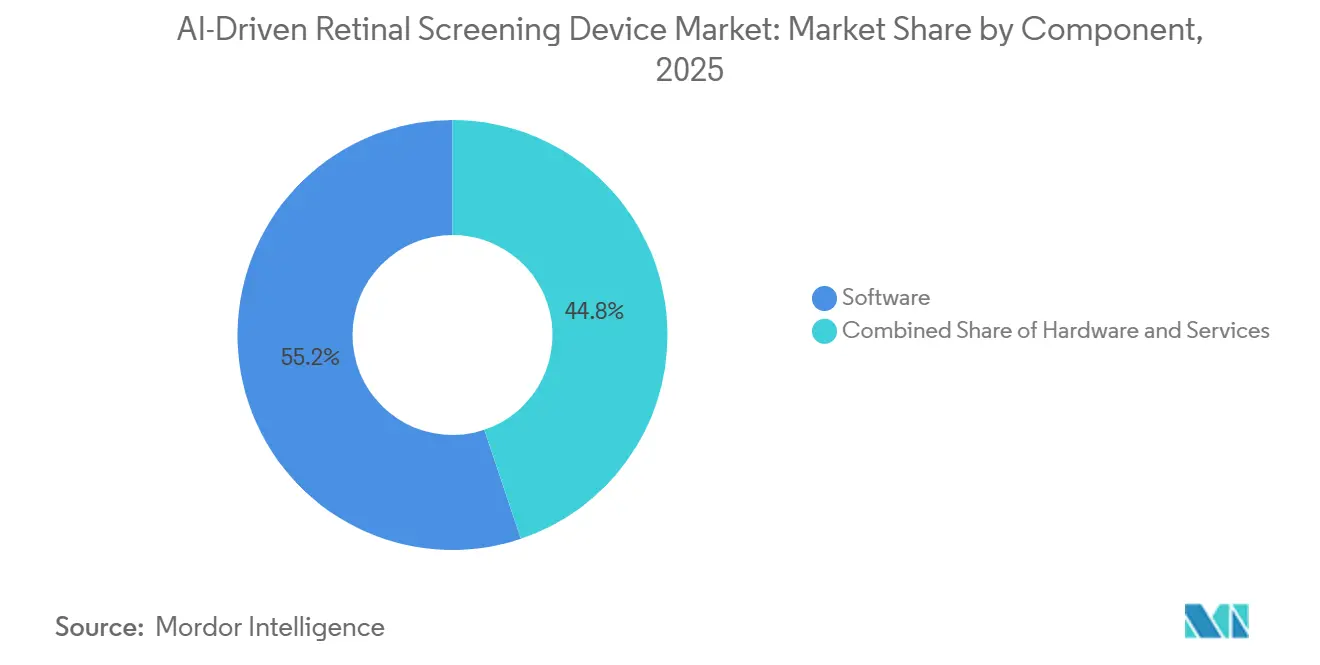

- By component, software held 55.16% share in 2025, while services is forecast to grow at 21.98% CAGR through 2031.

- By technology, fundus image-based AI held 56.18% share in 2025, while multi-modal AI is forecast to grow at 24.15% CAGR through 2031.

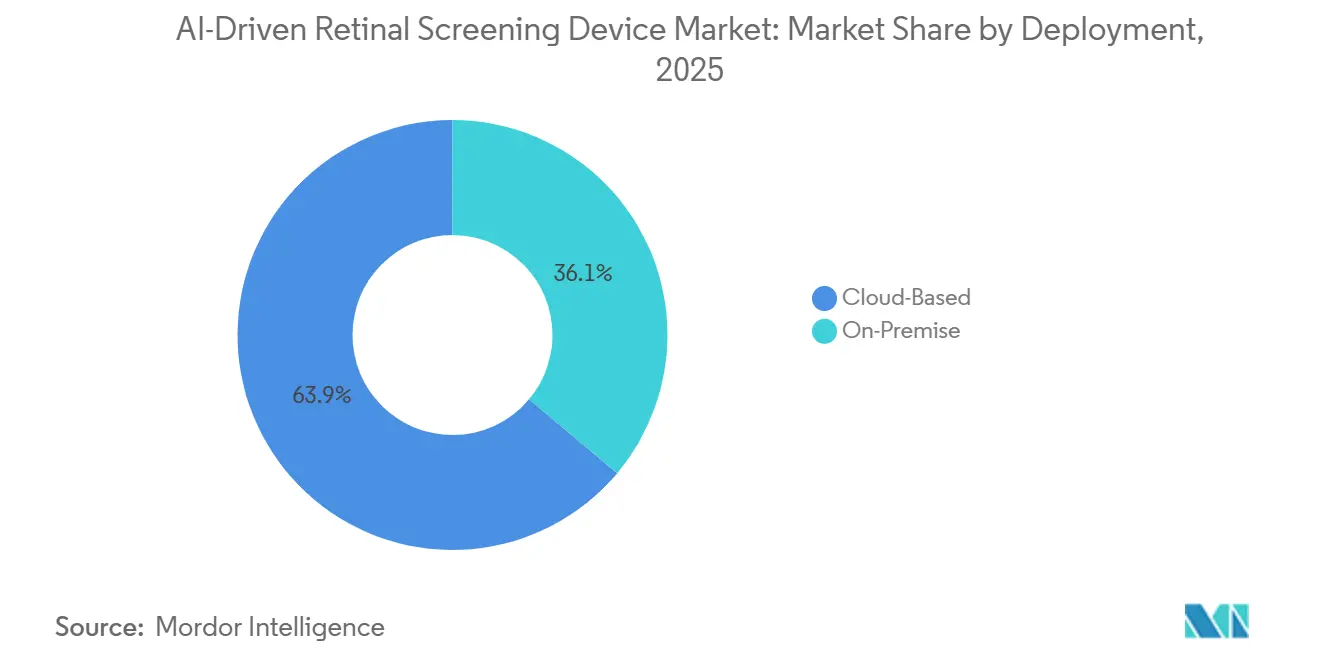

- By deployment, cloud-based solutions held 63.89% share in 2025, and the segment is also the fastest-growing deployment mode through 2031.

- By application, diabetic retinopathy accounted for 43.18% of the AI-driven retinal screening device market size in 2025, while age-related macular degeneration is forecast to grow at 22.39% CAGR through 2031.

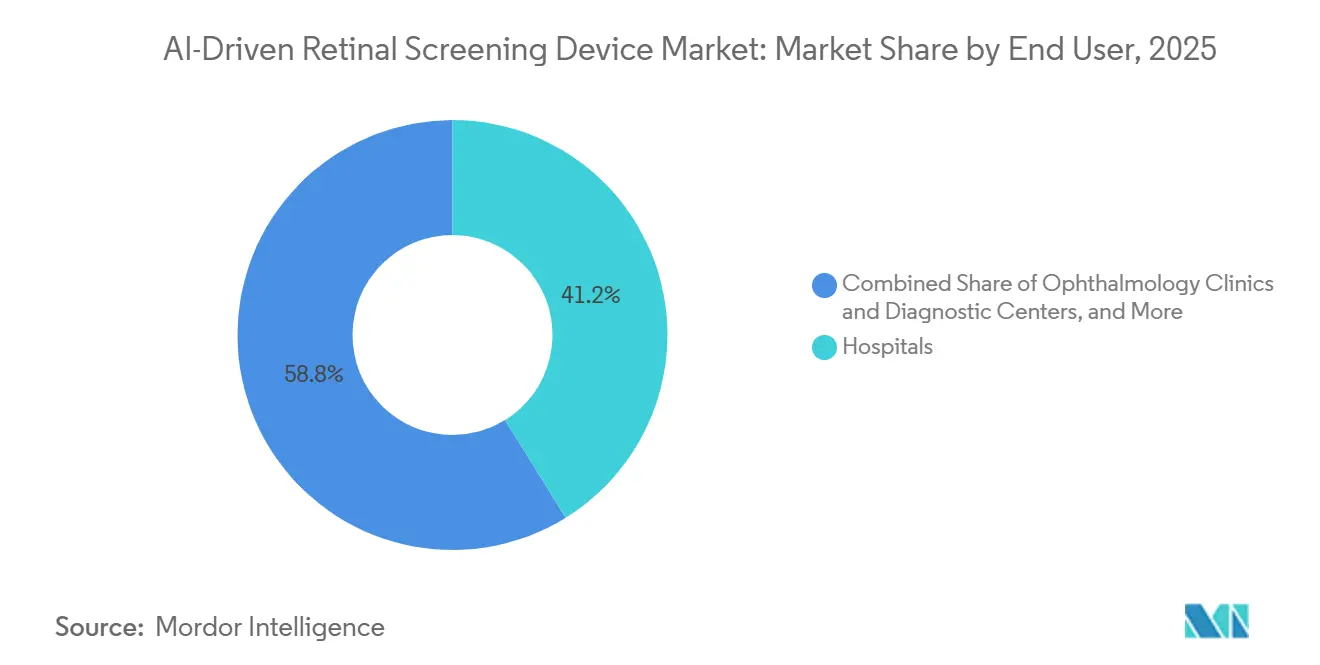

- By end user, hospitals held 41.18% share in 2025, while ophthalmology clinics are forecast to grow at 23.44% CAGR through 2031.

- By geography, North America held 43.18% of the AI-driven retinal screening device market share in 2025, while Asia-Pacific is forecast to grow at 25.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Driven Retinal Screening Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Burden and Undiagnosed Retinopathy Risk | +4.20% | Global, highest magnitude in South-East Asia, MENA, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Shortage of Ophthalmologists and Specialist Bottlenecks | +3.80% | Global, most acute in South Asia, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Shift Toward Point-of-Care and Primary Care Screening | +3.40% | North America and Europe, with spillover into urban Asia-Pacific | Short term (≤ 2 years) |

| Cloud Integration and Teleophthalmology Workflow Adoption | +2.80% | North America, Europe, urban Asia-Pacific, and emerging GCC markets | Medium term (2-4 years) |

| Regulatory Clearance Momentum for Autonomous Screening | +2.30% | North America and Europe, with early adoption in Japan and South Korea | Short term (≤ 2 years) |

| Under-Served Rural and Non-Acute Screening Channels | +1.80% | Asia-Pacific core, with spillover into MEA and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Burden and Undiagnosed Retinopathy Risk

The AI-driven retinal screening device market is being supported by a large and persistent pool of people who need regular eye screening but are still outside formal care pathways. In 2024, 589 million adults worldwide lived with diabetes, and 42.80% of them were undiagnosed, which left a very large population exposed to delayed retinal disease detection. A 2025 review covering 21 countries reported pooled diabetic retinopathy prevalence of 28.40% among people with diabetes, which supports the view that the screening burden is structurally large and long-lasting.[1]IDF diabetes Atlas: A worldwide review of studies utilizing retinal photography to screen for diabetic retinopathy from 2017 to 2024 inclusive Because 81% of people with diabetes live in low- and middle-income countries, the AI-driven retinal screening device market is not tightly tied to premium device affordability and is instead pushed by the need for scale and lower cost delivery. This pattern supports software-led platforms and portable screening workflows, since they can reach primary care sites and underserved populations faster than specialist-centered service models.

Shortage of Ophthalmologists and Specialist Bottlenecks

The AI-driven retinal screening device market is also advancing because the eye care workforce remains too limited and too unevenly distributed to support specialist-led screening at the needed scale. A 2026 workforce estimate placed the global supply at 275,551 ophthalmologists, or 34 per million people, with only 6 countries accounting for half of the total supply.[2]The global eye care workforce: 2023 estimates across ophthalmologists, optometrists, and allied personnel India was reported to have only 1 ophthalmologist for every 65,000 people, which shows why demand is moving toward triage and screening models that do not depend on large specialist teams. The same supply gap appears in other regions, and published research has shown that even high-income countries face large future workforce requirements to maintain access standards. This makes AI screening less of an optional tool and more of a capacity substitute that helps referral networks absorb rising diabetes-related eye disease volumes.

Shift Toward Point-of-Care and Primary Care Screening

The AI-driven retinal screening device market is gaining speed as retinal screening moves closer to the patient and away from specialist-only settings. In April 2024, the FDA cleared AEYE-DS for use with the Optomed Aurora handheld camera, which marked the first autonomous AI retinal screening clearance for a handheld device and widened the range of care settings where screening can take place. A 2026 study in the Johns Hopkins primary care system found that autonomous AI diabetic retinopathy screening increased subsequent presentation to eye care among at-risk patients. That result matters because it shows that the value of screening AI is not limited to image interpretation; it also improves follow-through into treatment pathways. As the AI-driven retinal screening device market expands in primary and preventive care, vendors with portable form factors and simple workflows are likely to benefit most.

Cloud Integration and Teleophthalmology Workflow Adoption

The AI-driven retinal screening device market is also being shaped by the growing role of cloud delivery, since remote workflows depend on fast image transfer, structured reporting, and system interoperability. Remidio Connect links handheld retinal imaging with EMR systems through HL7 messaging and returns graded results into clinical workflows, which shows how cloud delivery can support distributed screening programs. The 2025 HERMES trial reported that teleophthalmology reduced unnecessary urgent hospital referrals when compared with standard community optometry pathways. A 2026 AAAI publication also described a cloud-hosted framework for multi-disease retinal screening that fits teleophthalmology and EMR workflows. This supports the position of vendors that can embed retinal AI inside referral systems, reading networks, and hospital information flows instead of selling stand-alone diagnostic tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Model Governance, and Cross-Border Data Restrictions | -0.90% | European Union, China, and India | Long term (≥ 4 years) |

| Reimbursement Fragmentation across Care Settings | -0.70% | North America and Europe | Medium term (2-4 years) |

| Clinical Validation Burden Across Multiple Pathologies | -0.40% | Global, concentrated in markets requiring independent re-validation | Long term (≥ 4 years) |

| High Integration Friction with Legacy Imaging and EHR Systems | -0.30% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Model Governance, and Cross-Border Data Restrictions

The AI-driven retinal screening device market faces a meaningful restraint from tightening data governance rules across major healthcare systems. The European Health Data Space Regulation, published in March 2025, added new secondary-use governance obligations that interact with existing GDPR standards and complicate cross-border handling of health imaging data. China also introduced YY/T 1949-2024, its first industry-specific dataset standard for diabetic retinopathy fundus images, which signaled a more formal approach to training data quality and validation. German guidance issued in 2025 further reinforced the view that retinal imaging data often require stronger protection than simple pseudonymization workflows can provide. These overlapping rules raise compliance costs and slow model transfer across regions, which gives larger vendors a clearer advantage in the AI-driven retinal screening device market.

Reimbursement Fragmentation Across Care Settings

The AI-driven retinal screening device market is also constrained by uneven reimbursement, especially when screening expands beyond well-funded health systems. Coverage for remote diabetic retinopathy screening codes declined significantly, and the decline was linked to unequal access across patient groups. A 2025 policy review found that AI reimbursement in the United States healthcare remained concentrated in affluent urban settings and academic medical centers. Regional reimbursement variation also makes it harder for large providers to deploy a uniform enterprise model across multiple sites. This keeps rollout slower in rural clinics, safety-net settings, and smaller practices, even where the clinical need for automated screening is strongest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Economics Anchor Platform Margins

Software held 55.16% of the AI-driven retinal screening device market share in 2025, while services are forecast to grow at 21.98% CAGR through 2031. That pattern shows where commercial value is concentrating, since recurring algorithm access, workflow integration, cloud hosting, and support contracts carry more durable revenue than device shipments alone. The AI-driven retinal screening device market is therefore moving toward platform economics where software becomes the main value layer, and hardware becomes the access point for image capture. Hardware still matters because image quality remains the base input for any screening system, but its pricing power is under pressure as more vendors seek compatibility across multi-brand camera fleets.

This balance also explains why workflow depth now matters more than stand-alone diagnostic performance. Vendors that can connect retinal screening outputs into EMR, referral, and teleophthalmology systems are in a stronger position to hold renewals and expand accounts over time. The AI-driven retinal screening device industry is, therefore, rewarding platforms that can manage operational tasks around the algorithm, not just the algorithm itself. Services should continue to rise because hospitals and health systems increasingly require onboarding, validation support, training, and post-market monitoring as part of procurement. That trend favors vendors that can package clinical, technical, and regulatory support together under longer-term contracts.

By Technology: Fundus AI Leads, Multi-Modal Accelerates

Fundus image-based AI held 56.18% share in 2025, while multi-modal AI is forecast to grow at 24.15% CAGR through 2031. Fundus-based systems led early adoption because they aligned with lower-cost non-mydriatic cameras, simpler primary care workflows, and the first wave of autonomous regulatory clearances. The AI-driven retinal screening device market has therefore built its initial scale on technologies that can be deployed without the cost and workflow demands of OCT-heavy pathways. Multi-modal AI is now expanding faster because providers want broader single-encounter screening that can assess diabetic retinopathy, age-related macular degeneration, and glaucoma from paired inputs.

Peer-reviewed research from 2025 showed that models combining fundus photography and OCT improved performance across multiple retinal conditions when compared with single-modality systems. Another 2025 study reported 93.52% sensitivity and 95.00% specificity for a hybrid glaucoma screening model based on fundus images, which supports continued progress toward broader clinical use.[3]A hybrid multi model artificial intelligence approach for glaucoma screening using fundus images OCT-based AI, machine learning, deep learning, and natural language processing still serve narrower workflow roles, but their relevance rises as the AI-driven retinal screening device market moves from single-disease screening to more integrated retinal assessment. The AI-driven retinal screening device industry is likely to see more value shift toward technology stacks that support multi-disease decision support rather than narrow single-indication tools.

By Deployment: Cloud-Based Dominance Reflects Platform Lock-In Economics

Cloud-based deployment held 63.89% share in 2025 and was also the fastest-growing deployment mode in the AI-driven retinal screening device market. This indicates that market expansion is not waiting for a future cloud transition, because that shift is already well advanced in commercial practice. Cloud delivery helps vendors push software updates, new pathology modules, and compliance changes across connected systems without relying on manual site-by-site updates. It also supports teleophthalmology, distributed screening, and enterprise contracting models that depend on centralized management and reporting.

On-premise deployment remains relevant where data localization, hospital IT rules, or cross-border transfer concerns limit external cloud use. Those conditions are especially important in some public hospital settings in China and in parts of Europe where data protection reviews can slow cloud approvals. Even so, published evidence from 2026 showed that cloud-hosted multi-disease retinal AI can be deployed in community and primary care settings with strong clinician and patient acceptance. The AI-driven retinal screening device market continues to favor vendors that can deliver secure cloud orchestration at scale while still supporting restricted environments when needed. This deployment structure also stretches vendor relationships beyond the life of any single imaging device, since value becomes linked to throughput, reporting, and referral management.

By Application: Diabetic Retinopathy Sets the Standard, AMD Gains Momentum

Diabetic retinopathy captured 43.18% of the AI-driven retinal screening device market size in 2025, while age-related macular degeneration is forecast to grow at 22.39% CAGR through 2031. Diabetic retinopathy led the way because it was the first major indication to gain autonomous AI commercial traction, and it aligns with large diabetes populations, regular screening needs, and clearer reimbursement pathways. The AI-driven retinal screening device market has therefore built its first strong revenue base around diabetic eye disease, where clinical burden, payer interest, and workflow standardization already overlap. AMD is growing faster because aging populations in North America, Europe, and East Asia are increasing demand for earlier retinal disease detection and follow-up support.

Glaucoma is also becoming more relevant as model performance improves and multi-modal datasets become more available. Research published in 2025 also showed that multi-disease frameworks can classify many distinct fundus conditions in a single encounter, which supports expansion into cataract-related screening, hypertensive retinopathy, pathological myopia, and retinal vein occlusion. The pace of expansion outside diabetic retinopathy will still depend on how quickly additional applications achieve regulatory acceptance and fit into reimbursable care pathways. That means the AI-driven retinal screening device market should keep its largest revenue pool in diabetic retinopathy for now, even as growth broadens into other retinal conditions.

By End User: Hospitals Anchor Volume, Clinics Drive Growth

Hospitals held 41.18% share in 2025, while ophthalmology clinics are forecast to grow at 23.44% CAGR through 2031. Hospitals led early deployment because they had stronger procurement capacity, larger diabetes and endocrinology patient flows, and higher tolerance for introducing first-generation AI systems into formal clinical pathways. This gave hospitals a central role in validating the AI-driven retinal screening device market and proving workflow reliability for wider adoption. Ophthalmology clinics are now growing faster because they are absorbing AI-positive referrals from primary care settings and using AI tools to handle more patients without matching increases in specialist staffing.

Mobile clinics and rural camps are also becoming more important, where specialist access and clinic density remain limited. Portable systems such as Remidio's handheld retinal imaging platform support that expansion by bringing image capture and referral triage closer to underserved populations. Diagnostic centers and academic institutions play supporting roles, since one group delivers throughput and the other generates the evidence base for extended clinical use. Telemedicine providers have also become more visible buyers in the AI-driven retinal screening device market because asynchronous retinal reading and cloud-based review create scalable service models. This broadening end-user mix shows that market growth is no longer tied only to hospital purchasing cycles.

Geography Analysis

North America held 43.18% of the AI-driven retinal screening device market share in 2025, which kept it as the leading regional revenue base. The region benefits from the presence of multiple commercially available autonomous AI screening systems, a more established reimbursement pathway for autonomous retinal screening, and stronger provider familiarity with primary care-based diabetic eye screening workflows. The United States remained the center of regional demand because the rollout is extending beyond large academic centers into community and federally qualified health settings. A Utah deployment reported in November 2025 found that around 1 in 4 screened diabetes patients required urgent ophthalmology referral within 3 months, which supports the practical screening value of scaled primary care use. Europe ranked as the second-largest regional market, with 13 CE-certified AI diabetic retinopathy systems in commercial deployment as of 2026.[4]Artificial Intelligence-Based Medical Devices for Diabetic Retinopathy Screening in the European Union

Germany, the United Kingdom, and France have remained the leading European adoption centers. The United Kingdom also contributed early teleophthalmology evidence through the HERMES trial, which helped support broader confidence in remote retinal triage. Europe still faces a slower operating environment than North America because cross-border data governance and retraining requirements are becoming more demanding under newer regulatory rules. That means Europe remains important in the AI-driven retinal screening device market, but growth can be more dependent on regulatory navigation and local deployment design.

Asia-Pacific is forecast to grow at 25.67% CAGR through 2031, which makes it the fastest-growing region in the AI-driven retinal screening device market. The region combines very large diabetes populations, specialist shortages, and active healthcare digitization programs. China remains central because regulators are formalizing dataset expectations for diabetic retinopathy AI, while providers are using AI to scale screening beyond specialist-heavy hospital models. India is also important because it combines a very high diabetes burden with a visible local vendor base and persistent ophthalmologist shortages.

Competitive Landscape

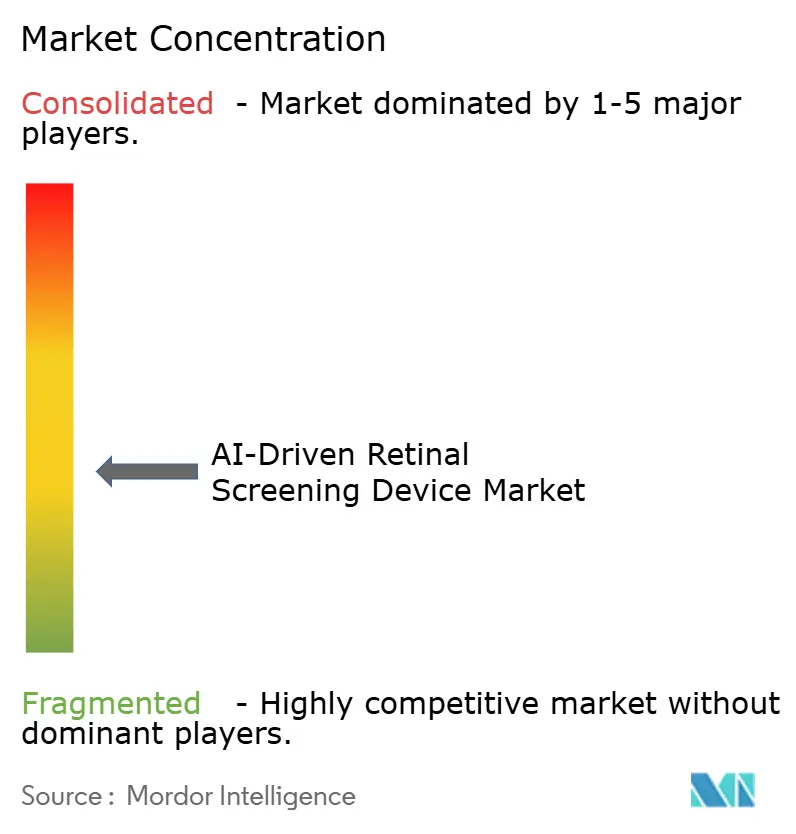

The AI-driven retinal screening device market is moderately fragmented, and the strongest competitive advantage comes from workflow integration depth rather than image classification alone. Large ophthalmic imaging companies such as Carl Zeiss Meditec, Topcon Corporation, and Heidelberg Engineering bring installed device bases, provider relationships, and easier access to clinical workflows. Pure-play firms such as Digital Diagnostics, Eyenuk, and AEYE Health compete through autonomous screening capability, regulatory progress, and deployment flexibility across third-party cameras. This keeps the AI-driven retinal screening device market open to both hardware-linked platforms and software-first challengers.

A clear strategic pattern is the move from narrow retinal screening toward broader data platforms and multi-condition analytics. Topcon Healthcare signed a definitive agreement in October 2025 to acquire Toku, which brought retinal-photo-based tools for cardiovascular risk, biological age, and kidney disease into Topcon's connected care platform. Carl Zeiss Meditec has also been strengthening its digital ecosystem through its ZEISS Research Data Platform and through a June 2026 strategic agreement with Aier Eye Hospital Group that included deeper collaboration in AI-assisted diagnostics and integrated digital workflows. Heidelberg Engineering expanded its app-centered AI ecosystem through collaborations with deepeye Medical and NetraMind Innovations, which shows how imaging incumbents are widening their software layer without rebuilding core hardware franchises. These moves show that competitive positioning in the AI-driven retinal screening device market is shifting toward data access, workflow ownership, and adjacent clinical use cases.

White space remains in portable rural screening, autonomous multi-pathology detection at the point of care, and retinal-image-based systemic disease assessment inside primary care systems. Smaller companies such as Remidio, Forus Health, Thirona B.V., and Mediwhale are relevant because they target gaps that enterprise imaging platforms do not always serve well. Open research is also pushing competitive pressure higher, since a 2026 publication described a fundus-based framework for 15-disease screening, which reduces the long-term defensibility of single-indication premium models. At the same time, regulatory compliance under medical device quality and post-market requirements still favors companies with established clinical, software, and regulatory operating capacity. The AI-driven retinal screening device market is therefore likely to stay moderately fragmented, but scale advantages should become clearer around vendors that control integration, evidence generation, and longitudinal data flows.

AI-Driven Retinal Screening Device Industry Leaders

Bosch Healthcare Solutions GmbH

Carl Zeiss Meditec AG

Eyenuk, Inc.

Optomed Plc

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Carl Zeiss Meditec signed a strategic agreement with Aier Eye Hospital Group for the purchase and installation of 25 VISUMAX 800 femtosecond laser systems across multiple Aier locations, with both parties committing to deeper collaborative development in AI-assisted diagnostics and integrated digital workflows.

- October 2025: Topcon Healthcare signed a definitive agreement to acquire Toku Inc., integrating Toku's CLAiR, BioAge, and MyKidneyAI platforms, trained on 4.3 million de-identified retinal images, into Topcon's Harmony connected care ecosystem.

- October 2025: Heidelberg Engineering and NetraMind Innovations launched the NMI-ChoroidAI application on the Heidelberg AppWay marketplace, providing automated quantitative choroidal health analysis from routine OCT scans, expanding the AppWay AI ecosystem.

- May 2025: Carl Zeiss Meditec received CE mark approval for CIRRUS PathFinder, an AI-integrated clinical support tool using deep learning to automatically identify abnormal macular OCT B-scans and provide AI-enhanced OCTA image quality and multi-layer segmentation.

Global AI-Driven Retinal Screening Device Market Report Scope

The AI-driven retinal screening device market comprises medical devices and software solutions that utilize artificial intelligence (AI), including machine learning and deep learning algorithms, to analyze retinal images for the automated detection, classification, and assessment of retinal and optic nerve diseases. These systems assist healthcare professionals by providing rapid, accurate, and standardized screening results, enabling early diagnosis, timely referral, and improved clinical decision-making.

The AI-driven retinal screening device market is segmented by component, technology, deployment, application, end user, and geography. By component, it is further divided into hardware, Software, and services. By technology, it is segmented into fundus image-based AI, optical coherence tomography-based AI, multi-model AI, and others. By deployment, it is segmented into cloud-based and on-premise. By application, the market is segmented into diabetic retinopathy, age-related macular degeneration, glaucoma, cataract, and others. By end user, the market is segmented into hospitals, ophthalmology clinics, diagnostic centers, academic and research institutions, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Hardware |

| Software |

| Services |

| Fundus Image-Based AI |

| Optical Coherence Tomography-Based AI |

| Multi-Modal AI |

| Others (OCTA-Based AI, Ultra-Widefield (UWF) Imaging AI, etc.) |

| Cloud-Based |

| On-Premise |

| Diabetic Retinopathy |

| Age-Related Macular Degeneration |

| Glaucoma |

| Cataract |

| (Diabetic Macular Edema, Retinal Vein Occlusion, etc.) |

| Hospitals |

| Ophthalmology Clinics |

| Diagnostic Centers |

| Academic and Research Institutions |

| Others (Telemedicine Providers, Mobile Clinics, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Technology | Fundus Image-Based AI | |

| Optical Coherence Tomography-Based AI | ||

| Multi-Modal AI | ||

| Others (OCTA-Based AI, Ultra-Widefield (UWF) Imaging AI, etc.) | ||

| By Deployment | Cloud-Based | |

| On-Premise | ||

| By Application | Diabetic Retinopathy | |

| Age-Related Macular Degeneration | ||

| Glaucoma | ||

| Cataract | ||

| (Diabetic Macular Edema, Retinal Vein Occlusion, etc.) | ||

| By End User | Hospitals | |

| Ophthalmology Clinics | ||

| Diagnostic Centers | ||

| Academic and Research Institutions | ||

| Others (Telemedicine Providers, Mobile Clinics, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for AI-driven retinal screening devices?

The AI-driven retinal screening device market is forecast to reach USD 1,298.60 million by 2031 from USD 570.52 million in 2026, with a 17.85% CAGR over 2026-2031

Which application area currently leads revenue generation?

Diabetic retinopathy led with a 43.18% application share in 2025 because it aligns with the largest validated screening need and the strongest autonomous AI commercialization path.

Which technology segment is expanding the fastest?

Multi-modal AI is the fastest-growing technology segment, with a forecast CAGR of 24.15% through 2031, as providers look for broader multi-disease retinal assessment in one workflow.

Why are cloud-based deployments dominant in retinal AI?

Cloud-based deployment held 63.89% share in 2025 because it supports model updates, teleophthalmology workflows, EMR integration, and enterprise scale management more effectively than isolated on-premises systems.

Which end-user group offers the strongest growth potential?

Ophthalmology clinics are projected to grow at 23.44% CAGR through 2031 as they absorb referrals from primary care screening and use AI to manage throughput with limited staffing growth.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing regional cluster at 25.67% CAGR through 2031, supported by large diabetes populations, specialist shortages, and active healthcare AI integration programs.

Page last updated on: