AI-Driven Fiber Backbone Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

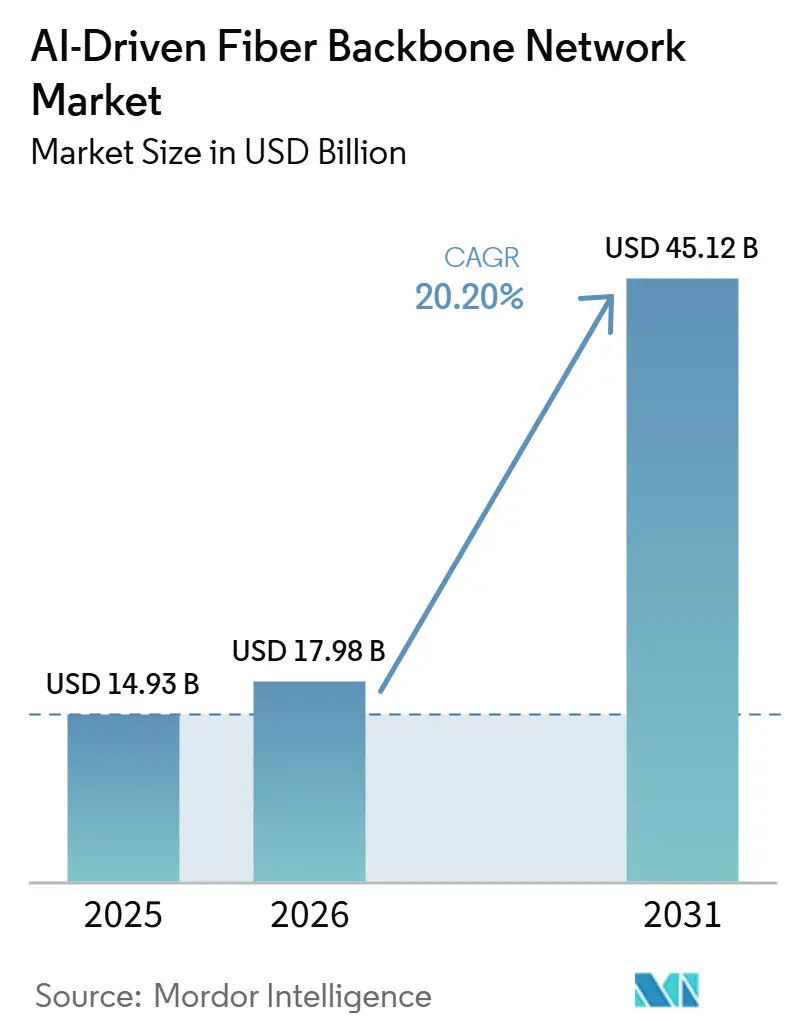

| Market Size (2026) | USD 17.98 Billion |

| Market Size (2031) | USD 45.12 Billion |

| Growth Rate (2026 - 2031) | 20.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

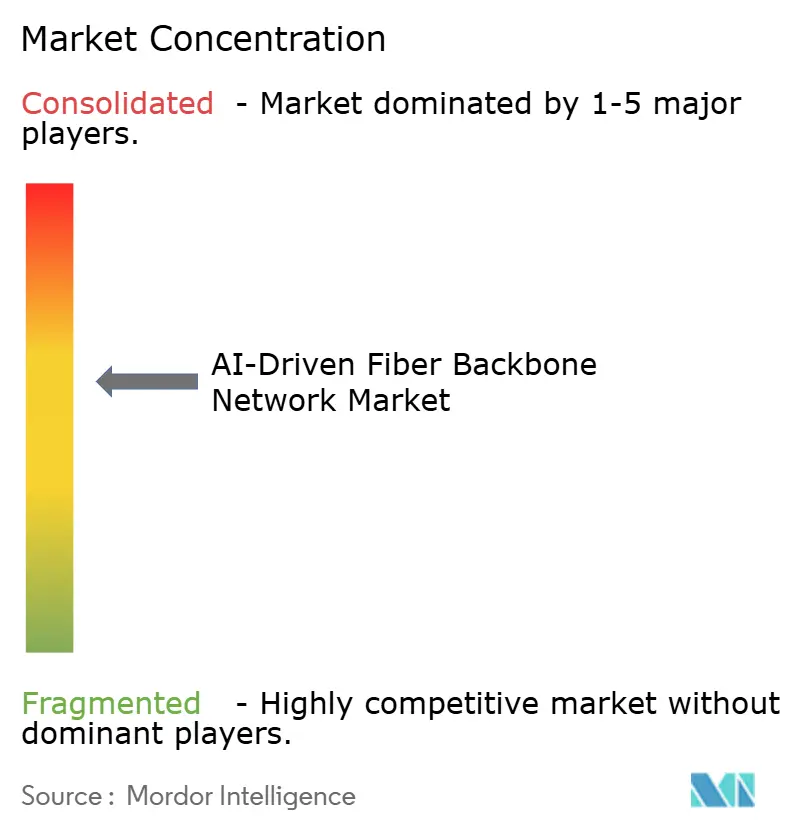

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Driven Fiber Backbone Network Market Analysis by Mordor Intelligence

The AI-driven fiber backbone network market size is expected to grow from USD 14.93 billion in 2025 to USD 17.98 billion in 2026 and is forecast to reach USD 45.12 billion by 2031 at 20.20% CAGR over 2026-2031. The AI-driven fiber backbone network market is expanding because AI training and inference workloads now depend on dense optical links across multiple campuses and data centers, which limits the physical network's capacity and directly constrains compute throughput. Demand is also shifting away from older telecom traffic patterns, as hyperscalers now buy fiber, transceivers, amplifiers, and routing capacity to keep GPU clusters synchronized over short- and medium-distance links. This is changing vendor strategy across the AI-driven fiber backbone network market, with greater emphasis on coherent optics, denser line systems, and software that automates optical path control and failure recovery. Capital is moving toward corridor builds, campus interconnects, and sovereign backbone projects, which are widening opportunities for fiber operators, optical equipment vendors, and infrastructure investors. At the same time, the AI-driven fiber backbone network market still faces pressure from high build costs, component lead times, and multivendor integration problems that can slow deployment even when demand remains strong.

Key Report Takeaways

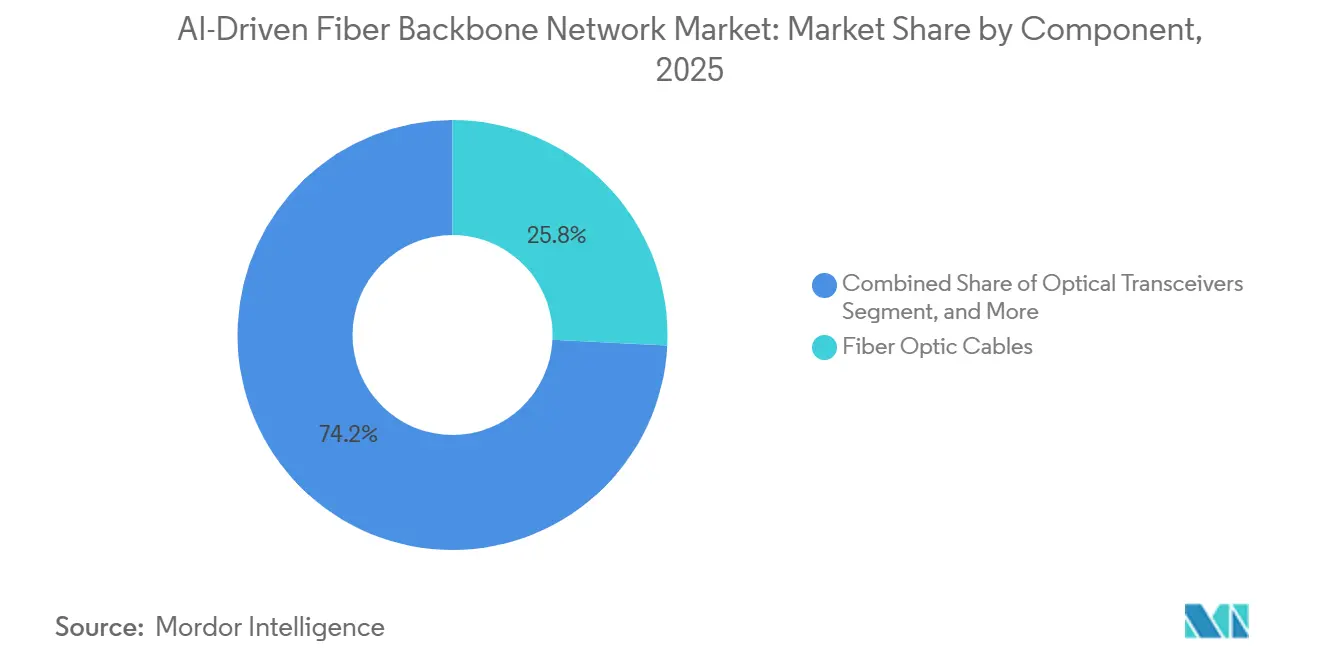

- By component, fiber optic cables led with 25.77% share of the AI-driven fiber backbone network market in 2025, while optical transceivers are projected to expand at a 21.33% CAGR through 2031.

- By network type, wired backbone networks held 78.88% share in 2025 and are projected to record the highest CAGR at 22.12% through 2031.

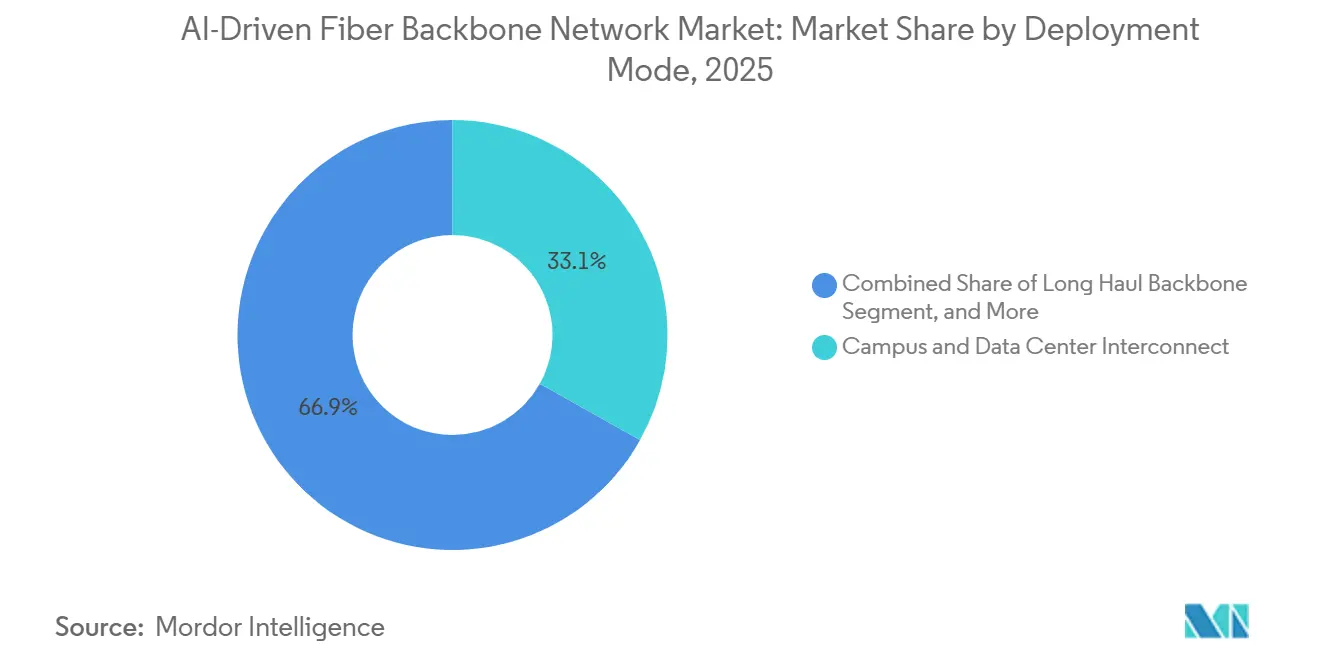

- By deployment mode, campus and data center interconnect accounted for 33.12% share of the AI-driven fiber backbone network market in 2025 and is projected to expand at a 23.10% CAGR through 2031.

- By application, cloud and hyperscale data center interconnect represented 32.11% share in 2025, while AI training cluster interconnect is projected to advance at a 22.67% CAGR through 2031.

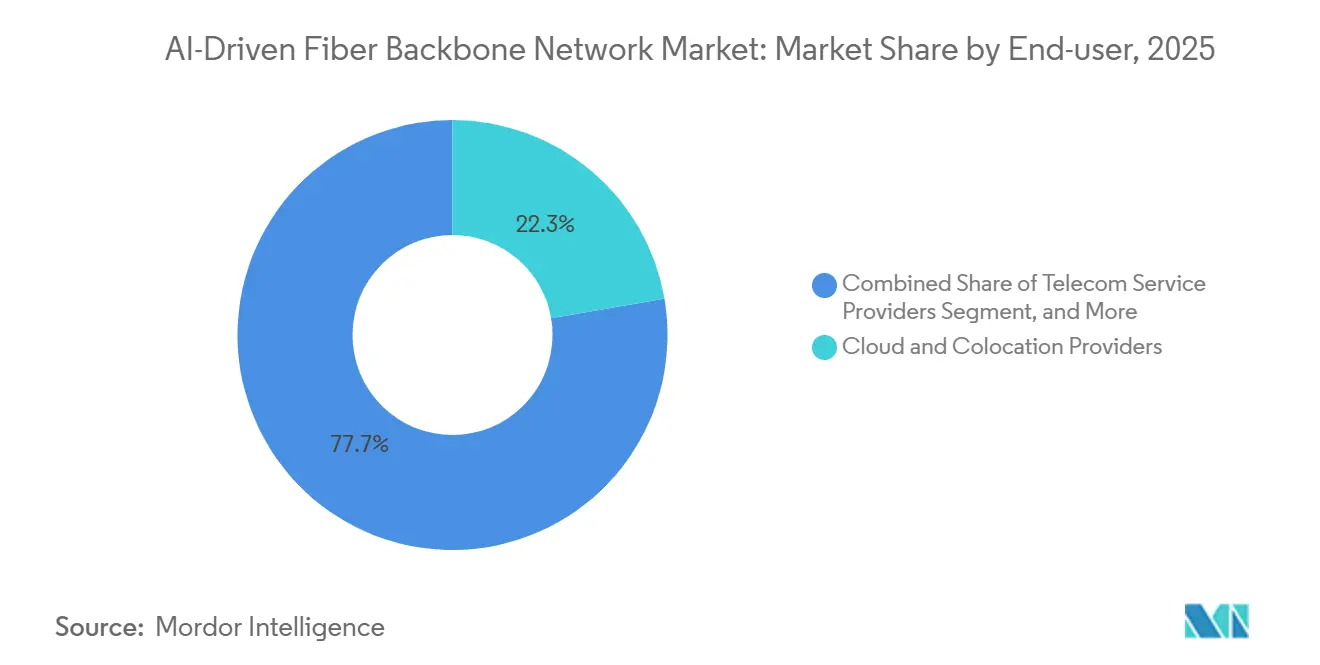

- By end user, cloud and colocation providers held 22.31% share in 2025 and are projected to post the fastest CAGR at 22.87% through 2031.

- By geography, North America led with 30.12% share in 2025, while Asia-Pacific is projected to expand at a 21.77% CAGR through 2031, reflecting the broad regional momentum of the AI-driven fiber backbone network market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Driven Fiber Backbone Network Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| AI-Driven Traffic Engineering for Latency-Critical AI Workloads | +4.8% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Hyperscale Campus-To-Campus Fiber Expansion | +4.2% | North America and Asia-Pacific core, with spillover to Europe | Medium term (2-4 years) |

| Shift Toward Coherent Optics and Higher Line Rates | +3.5% | Global | Medium term (2-4 years) |

| Automated Fault Prediction and Self-Healing Backbone Operations | +2.3% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Rising Need for Power-Efficient Cross-Site AI Interconnects | +1.6% | Global, highest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Fiber Buildouts for Sovereign AI And Data Residency Networks | +1.4% | Europe, Middle East, Canada, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Traffic Engineering for Latency-Critical AI Workloads

The AI-driven fiber backbone network market is being driven by traffic patterns that differ significantly from legacy telecom flows. AI training clusters generate bursty, all-to-all exchanges that can fill a 400G link in very little time, so operators need path selection that responds to latency, congestion, and queue depth with far more precision. That is moving network control away from static planning and toward software-defined traffic engineering, treating routing policy as a direct part of AI infrastructure performance. In June 2026, Nokia introduced an Autonomous Networks Agent Library with agentic AI capabilities for intent-based routing updates without human intervention, which showed how operators are preparing for AI-native optical control.[1]Nokia, “Nokia Advances Autonomous Networks Portfolio With Upgraded Agentic AI Capabilities, DTW26,” GlobeNewswire, globenewswire.comA 2026 field trial published in the Journal of Optical Communications and Networking demonstrated an LLM-powered AI agent that handled wavelength provisioning, failure management, and optical power optimization on a 440 km testbed in under 1 minute.[2]Optica Publishing Group, “Field Trial of an LLM-Powered AI Agent for Autonomous Optical Networks, A Full-Lifecycle Demonstration,” Journal of Optical Communications and Networking, optica.org As a result, the AI-driven fiber backbone network market is increasingly linking network engineering decisions to GPU utilization, service reliability, and the speed of cluster activation.

Hyperscale Campus-To-Campus Fiber Expansion

The AI-driven fiber backbone network market is also being lifted by campus-to-campus fiber expansion around new compute corridors. Build activity is moving beyond traditional urban hubs as AI facilities are following power availability, land availability, and expansion capacity into inland regions and secondary markets. This is turning dark fiber into a core input for AI infrastructure rather than a simple latency upgrade, raising the value of operators that control strategic routes. In January 2026, Corning and Meta signed a multiyear agreement worth up to USD 6 billion for optical fiber and connectivity solutions, and Corning expanded its Hickory, North Carolina, facility to support that demand.[3]Corning Incorporated, “Corning and Meta Announce Multiyear, up to USD 6 Billion Agreement to Accelerate US Data Center Buildout,” Corning News Releases, corning.com In February 2026, FiberLight committed USD 350 million to 1,400 route miles in West Texas, demonstrating how quickly AI corridor construction is moving into new backbone geographies.[4]FiberLight, “FiberLight's W. Texas AI Infrastructure Investment ~USD 500M,” FiberLight News, fiberlight.com This expansion pattern is widening the addressable market for cable makers, network builders, and route owners across the AI-driven fiber backbone network.

Shift Toward Coherent Optics and Higher Line Rates

The AI-driven fiber backbone network market is undergoing a much faster transition to higher optical speeds than earlier network cycles. The move from 400G to 800G and the early deployment of 1.6T are happening in a compressed window because AI cluster scaling requires both higher throughput and higher density. Vendors are now designing portfolios around coherent pluggables, dense multi-rail amplification, and optical front ends that can support faster upgrades with lower power per bit. Nokia presented an application-optimized coherent optical suite at OFC 2026, including a multi-rail in-line amplifier that can support 160 fiber pairs per rack, with general availability expected in 2026.[5]Nokia, “Nokia Launches Suite of Application-Optimized Optical Solutions for AI-Era Networks,” Nokia Newsroom, nokia.com Ciena introduced hyper-rail photonics that delivered 128 fiber pairs per rack at 75% lower power consumption, demonstrating that power and density are now central buying criteria in the AI-driven fiber backbone network market. Marvell also began customer sampling of its COLORZ 1600 1.6T ZR and ZR+ pluggable in 2026, which pushed the AI-driven fiber backbone network market further toward the next coherent generation.

Automated Fault Prediction and Self-Healing Backbone Operations

The AI-driven fiber backbone network market is gaining support from automated assurance and self-healing functions, as manual recovery windows are becoming too short at 800G and above. Operators can no longer rely on reactive ticketing when a service problem can interrupt a training run that spans thousands of GPUs and multiple sites. This is making telemetry quality, anomaly detection, and automated localization more important in backbone procurement and operations. In May 2026, NTT announced the first DSP chip with an embedded function that monitors the full optical network length during live operation and reduces computational load by a factor of 100 compared with prior methods. Research presented at OFC 2026 introduced UniOpt, a unified foundation-model framework for forecasting, anomaly detection, localization, and lifetime prediction across optical networks. Separate OFC 2026 testbed work also demonstrated self-healing recovery in under 30 seconds in wideband IPoWDM environments, supporting broader automation across the AI-driven fiber backbone network market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Capital Intensity of Fiber Backbone Upgrades | -3.2% | Global, most pronounced in emerging markets and smaller operators | Medium term (2-4 years) |

| Legacy Multivendor Integration Complexity | -2.1% | Global, highest in mature telecom markets with layered infrastructure | Medium term (2-4 years) |

| Fiber Supply Bottlenecks and Specialized Component Lead Times | -1.3% | Global, most acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Cybersecurity Exposure Across Core Routing and Optical Layers | -0.9% | Global, with heightened sensitivity in government and defense segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Fiber Backbone Upgrades

High capital intensity remains a major restraint on the AI-driven fiber backbone network market, as national and regional backbone upgrades require substantial commitments before revenue becomes fully visible. Projects often involve dense wavelength upgrades, coherent amplifier replacement, and router refresh cycles that stretch payback periods well past the near term. Smaller carriers are under added pressure because hyperscalers can secure capacity and priority for components through longer, larger purchase agreements. The January 2026 Corning and Meta agreement, worth up to USD 6 billion, showed the scale at which top buyers can lock in supply and shape manufacturing allocation. Mid-tier operators often need anchor contracts before they can move ahead with major backbone builds, which slows rollout in parts of the AI-driven fiber backbone network market that are not backed by hyperscaler demand. As line systems move toward 1.6T-era designs, the cost of redesigning optical infrastructure is also rising, which is widening the gap between well-capitalized builders and capacity lessors.

Legacy Multivendor Integration Complexity

Legacy multivendor integration is another brake on the AI-driven fiber backbone network market, as many carrier backbones were assembled over decades of hardware cycles. That leaves operators with optical, IP, and management layers that do not always expose the telemetry detail needed for AI-driven control and assurance. In many cases, translation middleware is needed between legacy management planes and new automation tools, which introduces delays and weakens reliability. Open architectures offer partial relief, but production deployment still requires years of engineering and changes to the operating model. KDDI's June 2026 commercial launch of cluster router operations, built on open routing hardware developed through the Telecom Infra Project since 2020, showed that disaggregated approaches can work at scale after a sustained integration effort. Because of this, the AI-driven fiber backbone network market is not constrained only by hardware supply; it is also constrained by how quickly operators can make mixed-vendor environments behave like unified AI-era systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Transceivers Gaining Share as Speed Migration Accelerates

Optical transceivers are the fastest-growing component segment in the AI-driven fiber backbone network market, with a 21.33% CAGR through 2031, while fiber optic cables held 25.77% share of the AI-driven fiber backbone network market size in 2025. This pairing matters because the market needs both more physical route capacity and faster active optics simultaneously, rather than one replacing the other. Transceivers are gaining momentum as hyperscalers move from 400G to 800G and begin early adoption of 1.6T modules for campus links and distributed data center routes. Marvell began customer sampling of its COLORZ 1600 1.6T ZR and ZR+ pluggable in 2026, targeting links from campus distances up to 12 miles and distributed routes up to 621 miles. That shortens upgrade cycles in the AI-driven fiber backbone network market, as operators can prepare for denser AI workloads without waiting for slower architectural refresh cycles.

Fiber optic cables still anchor the installed base because long-term dark fiber agreements and backbone route construction are sunk investments that shape future equipment demand. Corning's multiyear supply agreement with Meta showed that cable demand is now directly tied to AI data center buildouts rather than only telecom expansion or enterprise access needs. Optical switches, routers, and amplifiers are also being redesigned for denser multi-rail AI interconnects, as shown by Ciena's hyper-rail photonics platform and its strong emphasis on power reduction. The remaining component pool, including passive elements and co-packaged optical approaches, is becoming more relevant as the AI-driven fiber backbone network market pushes optics closer to compute platforms. That means component competition is no longer only about standalone hardware volume; it is also about how well each layer fits dense AI networking architectures.

By Network Type: Wired Backbone Maintains Structural Primacy for AI Workloads

Wired backbone networks held 78.88% of the AI-driven fiber backbone network market share in 2025 and are projected to grow at a 22.12% CAGR through 2031. That dual position reflects a structural reality: AI training traffic requires deterministic, low-latency performance, very low jitter, and throughput levels that wireless systems cannot match across large, synchronized clusters. Collective GPU operations depend on repeatable timing, which keeps fiber at the center of performance-sensitive transport design. In March 2026, NTT East Japan completed an IOWN All-Photonics Network trial for distributed AI inference between Tokyo and Fukuoka, achieving performance equivalent to a local data center environment over more than 1,000 km. The AI-driven fiber backbone network market, therefore, continues to treat wired transport not as one option among many, but as the default backbone for high-intensity AI workloads.

Wireless backbone networks still play a useful role in regions where fiber economics are weaker or deployment conditions are more challenging. Their main opportunities are in 5G backhaul densification, mobile edge AI inference, and last-mile aggregation, rather than in the core interconnect layer for training clusters. This keeps wireless growth relevant in rural, island, and lower-density markets without altering the basic structure of the AI-driven fiber backbone network. The practical split is clear: fiber carries the AI-critical synchronization layer, while wireless supports complementary access and aggregation functions. That separation supports stable demand for both network types, but it keeps the growth center of the AI-driven fiber backbone network market firmly on wired infrastructure.

By Deployment Mode: Campus And DCI Drive Market Momentum

Campus and data center interconnect accounted for 33.12% of the AI-driven fiber backbone network market in 2025, and the market size for campus and data center interconnect is projected to expand at a 23.10% CAGR through 2031. This segment leads because AI campuses need dense, short-to-medium-range optical links between co-located or closely distributed GPU clusters. Traffic in these environments is heavily east-west, which means the network is optimized for machine-to-machine synchronization rather than older client-server patterns. That changes the design logic for amplifiers, routing, and optical line systems inside the AI-driven fiber backbone network market. Marvell's 1.6T pluggable roadmap, built for campus and distributed data center links, reflects how quickly vendors are tuning products to this deployment model.

The long-haul backbone still matters because AI models, sovereign copies, and major cloud regions require inter-regional transport as their training and inference footprints spread across countries and continents. Ciena activated WaveLogic 6 Extreme on the Batam-Jakarta segment of the Matrix Cable System in June 2026, delivering 1 Tb/s per wavelength over 1,055 km, demonstrating that advanced coherent transport is moving well beyond metro use cases. The metro backbone remains the aggregation layer between campus DCI and long-haul infrastructure, and its value rises as operators build AI-capable capacity in secondary cities. The AI-driven fiber backbone network market is, therefore, seeing all 3 deployment modes remain relevant, but campus and DCI are setting the pace because they sit closest to the current center of AI compute spending. This is why the strongest procurement urgency is appearing in short- and medium-range optical deployments.

By Application: AI Training and Cloud Interconnect Define Market Priority

Cloud and hyperscale data center interconnect accounted for 32.11% of the AI-driven fiber backbone network market in 2025, while AI training cluster interconnect is projected to expand at a 22.67% CAGR through 2031. Cloud and hyperscale interconnects remain the largest because they already serve a large installed base of inter-facility capacity that is now being refreshed from older transmission speeds to 400G and 800G platforms. The AI training cluster interconnect is growing faster because every new model generation triggers fresh cluster buildout and new low-latency transport demand. The NTT distributed inference trial between Tokyo and Fukuoka reinforced the growing dependence of both training and inference environments on high-performance optical backbones across separate sites. Both installed cloud backbone refresh demand and new training-led expansion demand are therefore shaping the AI-driven fiber backbone network market.

Telecom core and transport remain major applications because carriers still need to absorb rising AI traffic across their national and regional networks. Government and sovereign networks are becoming more important as countries seek closed optical environments for sensitive workloads and domestic data control. In 2025, BT became the first UK provider to offer a full sovereign services portfolio, combining sovereign fiber connectivity, voice, cloud, and AI services. Enterprise-wide area backbones are also gaining attention as firms in regulated sectors weigh the cost of dedicated fiber against recurring shared-cloud bandwidth spend. That broadens the AI-driven fiber backbone network market's application base beyond hyperscaler campuses and reinforces the case for specialized backbone design.

By End User: Cloud And Colocation Providers Set the Demand Pace Across Segments

Cloud and colocation providers held 22.31% share in 2025 and are projected to grow at a 22.87% CAGR through 2031 in the AI-driven fiber backbone network market. Their influence is larger than the headline share suggests because they buy optical equipment directly and also anchor long-term route construction by signing large fiber commitments. This dual role shapes both vendor roadmaps and the financing logic behind new backbone corridors. Corning's multiyear agreement with Meta showed how hyperscaler-linked demand is now influencing upstream fiber manufacturing decisions. Zayo's 2026 anchor customer commitment for 8,000 route miles of new AI-corridor builds showed how infrastructure expansion is increasingly secured around large customer demand before full route deployment.

Telecom service providers remain the largest owners of installed assets across many national networks, but their share of new optical spending is under pressure from direct hyperscaler procurement and alternative infrastructure ownership models. Government and defense buyers are increasing interest in closed optical environments where sovereignty and security requirements limit shared commercial use. Research and education networks continue to matter because they often validate new coherent technologies in real operating conditions before wider commercial adoption. Enterprises are the fastest-growing non-cloud customer group because AI workloads are forcing a more direct comparison between dedicated backbone investment and recurring network service costs. This mix keeps the AI-driven fiber backbone network market broad-based, even though cloud and colocation providers still set the strongest demand signal for suppliers and route builders.

Geography Analysis

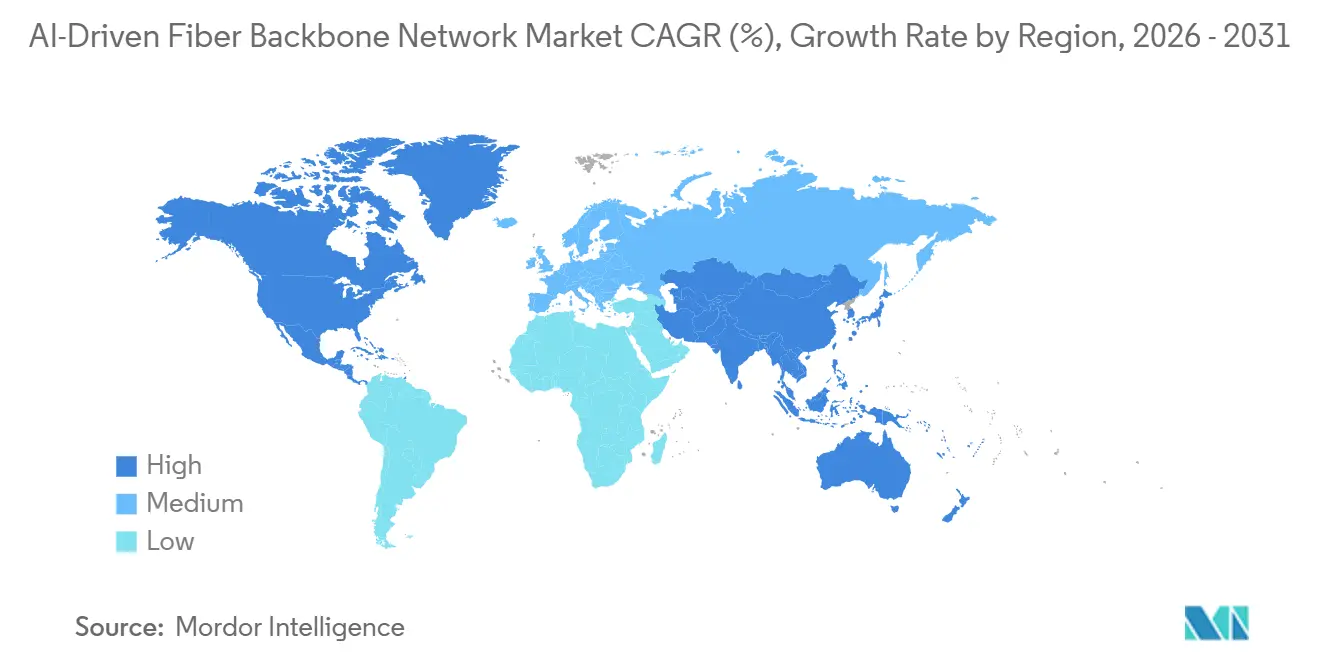

North America accounted for 30.12% of the AI-driven fiber backbone network market share in 2025, making it the largest regional market. The region benefits from the highest concentration of hyperscaler campuses and a visible shift in backbone investment toward AI corridors rather than legacy metro cores. In January 2026, Corning and Meta signed a multiyear agreement worth up to USD 6 billion, which expanded US manufacturing support for AI data center and fiber deployment needs. In February 2026, FiberLight committed USD 350 million to new West Texas infrastructure, underscoring how inland, power-rich locations are becoming backbone priorities. Zayo also completed the acquisition of Crown Castle's Fiber Solutions business in 2025 and later secured an anchor customer for 8,000 route miles of new AI-corridor builds, which showed how asset consolidation is supporting regional scale in the AI-driven fiber backbone network market.

Asia-Pacific is projected to grow at a 21.77% CAGR through 2031, which makes it the fastest-growing regional block in the AI-driven fiber backbone network market. Regional demand is being supported by state-backed backbone planning, new data center development, and stronger interest in low-latency intercity AI transport. In March 2026, NTT completed a field trial of its IOWN All-Photonics Network for distributed AI inference between Tokyo and Fukuoka, which demonstrated local-data-center-like performance over long-distance optical infrastructure. In June 2026, KDDI launched commercial cluster router operations as part of its Digital Belt vision, which linked data center assets, submarine cables, and edge nodes into a lower-latency national compute fabric.

Europe holds a significant share of the AI-driven fiber backbone network market, as cloud expansion and sovereign data requirements continue to drive backbone spending across major economies. BT strengthened that position in 2025, becoming the first UK provider to offer a full sovereign service portfolio for regulated workloads requiring domestic data residency. South America is emerging as a demand center as nearshoring and regional AI infrastructure plans raise the need for stronger cross-border and inland fiber routes. The Middle East and Africa remain earlier in their development curve, but sovereign AI programs in the Gulf and landing-station-linked terrestrial backbone demand in South Africa and Egypt are creating a clearer long-term role in the AI-driven fiber backbone network market.

Competitive Landscape

The AI-driven fiber backbone network market shows moderate-to-high concentration at the optical systems layer, while the fiber operations and dark fiber layers remain more fragmented across regional builders and infrastructure owners. Competition centers on coherent optics, power efficiency, control-plane automation, and the ability to align hardware roadmaps with hyperscaler deployment speeds. Nokia strengthened its position in March 2026 by launching an application-optimized coherent optical suite with 4 new DSPs and a target to reduce the total cost of ownership by up to 70%. Ciena responded with the Vesta 200 6.4T CPX pluggable optical engine and new hyper-rail photonics capabilities, which pushed the competition toward higher density and lower power operation. Marvell added pressure from the component side by sampling its 1.6T COLORZ 1600 pluggable in 2026, which showed that the AI-driven fiber backbone network market is attracting competition from both established systems vendors and advanced silicon-led suppliers.

A second layer of competition is forming around ownership of the physical corridor itself. Corning's agreement with Meta showed that upstream supply relationships are becoming strategic assets in the AI-driven fiber backbone network market rather than routine procurement contracts. Zayo's acquisition of Crown Castle's Fiber Solutions business and its later 8,000 route-mile anchor build commitment showed that scale in route ownership can be as important as equipment differentiation. Equinix, Nokia, and Arteria Networks also completed a proof of concept for a quantum-safe optical link between Paris and Bordeaux in May 2026, which signaled that security posture is becoming part of vendor differentiation in backbone procurement.

The AI-driven fiber backbone network market still has room for challengers, particularly among mid-tier operators that need affordable upgrades and sovereign network mandates that favor local or open architectures. KDDI's launch of a commercial cluster router, built on open routing hardware developed through the Telecom Infra Project, demonstrated that disaggregated models are gaining commercial credibility in demanding environments. Optica-published fieldwork on autonomous provisioning and self-healing optical control also suggests that software capability will matter more in future competitive rankings than raw hardware speed. This means the AI-driven fiber backbone network market is not converging on a single vendor order, because route ownership, coherent design, automation depth, and compliance readiness are all shaping competitive outcomes simultaneously.

AI-Driven Fiber Backbone Network Industry Leaders

Ciena Corporation

Nokia Corporation

Cisco Systems, Inc.

Coherent Corp.

NEC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: BIG Fiber secured USD 250 million in debt financing led by Stonepeak Credit and La Caisse, with an additional USD 100 million accordion feature, to accelerate dark fiber expansion across US markets, including Greater Atlanta. The financing targets greenfield construction and overbuilds of legacy telecom corridors requiring AI-scale capacity.

- May 2026: NTT announced the world's first DSP chip with an embedded function to monitor the full optical network length during live transmission, reducing computational load by a factor of 100 compared to prior approaches. The technology enables transceivers to self-identify faults along the entire link without external measurement equipment, materially advancing autonomous backbone operations.

- March 2026: Nokia launched a comprehensive suite of application-optimized coherent optical transport solutions at OFC 2026, built around 4 new DSPs and multiple InP and silicon-photonics optical front ends. The suite targets up to 70% total cost of ownership reduction, with Nokia's multi-rail in-line amplifier delivering 160 fiber pairs per rack, available in the second half of 2026.

- March 2026: Ciena unveiled 1600ZR pluggables based on 2nm silicon, hyper-rail photonics delivering 128 fiber pairs per rack at 75% lower power consumption, and agentic AI network automation tools at OFC 2026. The announcements followed Ciena's acquisition of Nubis Communications and positioned the company for the emerging co-packaged optics generation.

Global AI-Driven Fiber Backbone Network Market Report Scope

The AI-Driven Fiber Backbone Network Market Report is Segmented by Component (Cables, Transceivers, Switches, Amplifiers, and Other Components), Network Type (Wired and Wireless), Deployment Mode (Long Haul, Metro, and Campus/DCI), Application (AI Training, Cloud DCI, Telecom Core, Government, and Enterprise WAN), End User (Telecom Service Providers, Cloud and Colocation Providers, Enterprises, Government and Defense, and Research and Education Networks), and Geography (North America, South America, Europe, Asia-Pacific, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Fiber Optic Cables |

| Optical Transceivers |

| Optical Switches and Routers |

| Optical Amplifiers |

| Other Components |

| Wired Backbone Network |

| Wireless Backbone Network |

| Long Haul Backbone |

| Metro Backbone |

| Campus and Data Center Interconnect |

| AI Training Cluster Interconnect |

| Cloud and Hyperscale Data Center Interconnect |

| Telecom Core and Transport |

| Government and Sovereign Networks |

| Enterprise Wide Area Backbones |

| Telecom Service Providers |

| Cloud and Colocation Providers |

| Enterprises |

| Government and Defense |

| Research and Education Networks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Fiber Optic Cables | ||

| Optical Transceivers | |||

| Optical Switches and Routers | |||

| Optical Amplifiers | |||

| Other Components | |||

| By Network Type | Wired Backbone Network | ||

| Wireless Backbone Network | |||

| By Deployment Mode | Long Haul Backbone | ||

| Metro Backbone | |||

| Campus and Data Center Interconnect | |||

| By Application | AI Training Cluster Interconnect | ||

| Cloud and Hyperscale Data Center Interconnect | |||

| Telecom Core and Transport | |||

| Government and Sovereign Networks | |||

| Enterprise Wide Area Backbones | |||

| By End User | Telecom Service Providers | ||

| Cloud and Colocation Providers | |||

| Enterprises | |||

| Government and Defense | |||

| Research and Education Networks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the AI-driven fiber backbone network market size in 2026, and how large is it expected to become by 2031?

The AI-driven fiber backbone network market stood at USD 17.98 billion in 2026 and is forecast to reach USD 45.12 billion by 2031, growing at a 20.20% CAGR over 2026-2031.

What is driving demand for AI-driven fiber backbone networks right now?

The main drivers are multi-campus GPU clusters, higher demand for campus and data center interconnect, and the shift toward 800G and early 1.6T optical upgrades.

Which component area is growing the fastest in AI-driven fiber backbone deployments?

Optical transceivers are the fastest-growing component segment, with a projected 21.33% CAGR through 2031, while fiber optic cables remained the largest component group in 2025.

Why are wired backbone networks still dominant for AI workloads?

Wired backbone networks held an 78.88% share in 2025 because AI training requires deterministic, low-latency, very low jitter, and terabit-scale throughput that wireless backbones do not reliably provide.

Which regions are leading adoption and growth in this space?

North America led with 30.12% share in 2025, while Asia-Pacific is projected to be the fastest-growing region at a 21.77% CAGR through 2031.

How are vendors competing in AI-driven fiber backbone systems?

Vendors are competing through coherent optics, higher-density line systems, lower power consumption, open architectures, and stronger automation for routing, assurance, and fault recovery.

Page last updated on: