AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.25 Billion |

| Market Size (2031) | USD 96.05 Billion |

| Growth Rate (2026 - 2031) | 28.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Copilot Market Analysis by Mordor Intelligence

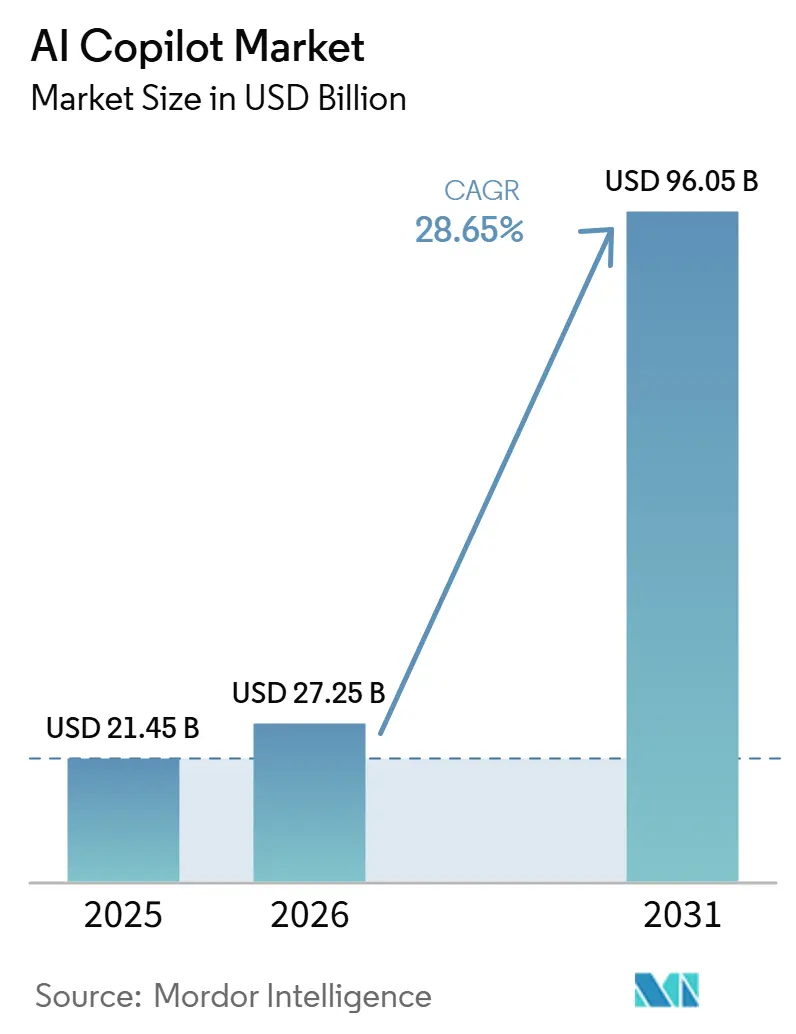

The AI Copilot Market size was valued at USD 21.45 billion in 2025, USD 27.25 billion in 2026, and is forecast to reach USD 96.05 billion by 2031 at a CAGR of 28.65% over 2026-2031. Growth is being supported by a clear shift in enterprise spending, where copilot tools are moving out of pilot budgets and into recurring IT and transformation budgets alongside cloud and cybersecurity. The market is also being shaped by strong vendor scale, as leading providers are expanding seat volumes, broadening integrations, and turning copilots into workflow layers that sit inside daily business software. Competition is rising rapidly as platform vendors, hyperscalers, and specialist providers vie to control the same user workflows and enterprise data environments. Demand is moving beyond simple text generation toward task execution, governance, and domain-specific use cases, raising the value of products that support regulated and high-volume work. At the same time, verification burdens, data control requirements, and overlapping software purchases are pushing buyers to favor vendors that can combine broad functionality with stronger governance and deployment flexibility.

Key Report Takeaways

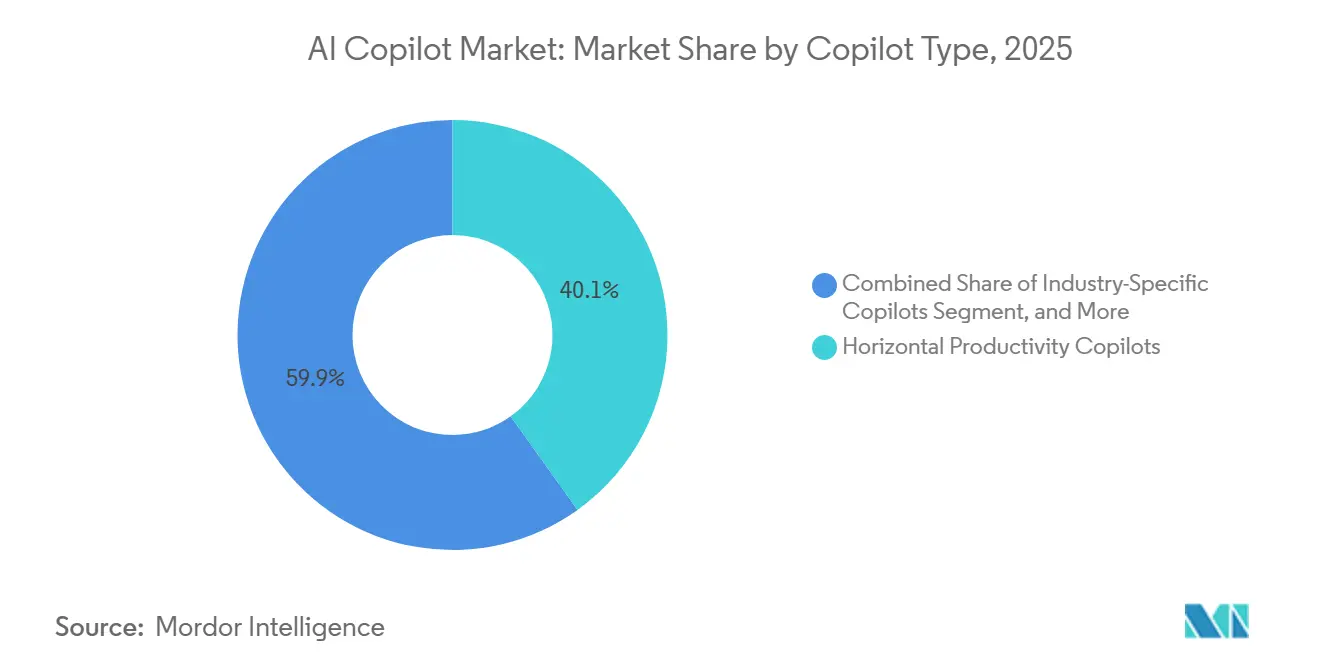

- By copilot type, Horizontal Productivity Copilots held 40.12% revenue share in the AI Copilot Market in 2025, while Industry-Specific Copilots are projected to expand at a 30.84% CAGR through 2031.

- By deployment mode, Cloud-Based deployment accounted for 71.24% of revenue in 2025, while Hybrid deployment is expected to record the highest CAGR of 31.16% through 2031.

- By organization size, Large Enterprises held 68.43% of revenue in 2025, while Small and Medium Enterprises are projected to grow at a 30.41% CAGR through 2031.

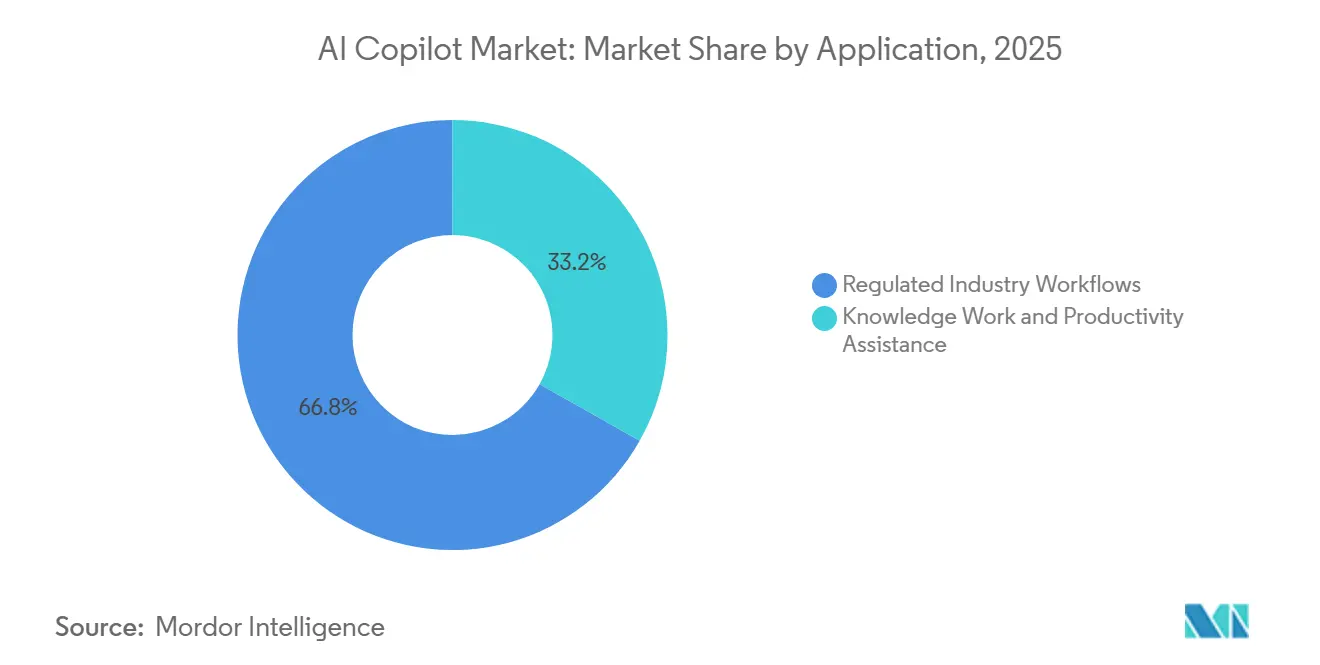

- By application, Knowledge Work and Productivity Assistance accounted for 33.18% of revenue in 2025, while Regulated Industry Workflows are projected to advance at a 31.73% CAGR through 2031.

- By end-user industry, IT and Telecommunications accounted for 22.47% of the AI Copilot Market revenue in 2025, while Government and Administration is expected to expand at a 30.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Native Productivity Benchmarks Reset Enterprise Seat Economics | +5.8% | Global, concentrated in North America and Northern Europe | Short term (≤ 2 years) |

| Embedded Copilot Workflows Reduce Switching Costs Across SaaS Suites | +5.2% | North America and Europe, with spillover into Asia-Pacific | Short term (≤ 2 years) |

| Agentic Task Execution Expands Copilot Use Beyond Text Generation | +4.6% | Global | Medium term (2-4 years) |

| Private Model Hosting Accelerates Regulated Enterprise Adoption | +4.1% | North America, Europe, and Asia-Pacific regulated sectors | Medium term (2-4 years) |

| Multimodal Copilots Unlock Higher-Value Knowledge Work Use Cases | +3.4% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Copilot Procurement Shifts From Pilot Budgets To Core IT Spending | +2.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ai Native Productivity Benchmarks Reset Enterprise Seat Economics

Enterprise buyers are now evaluating Copilot software against measurable productivity benchmarks rather than treating it as an open-ended experiment. Microsoft disclosed that more than 20 million paid Microsoft 365 Copilot seats were in use by April 2026, and the company also reported very large enterprise deployments from Accenture, Bayer, Johnson and Johnson, Mercedes-Benz, and Roche.[1]Microsoft Corporation, “Microsoft Q3 Fiscal Year 2026 Earnings Disclosure,” Microsoft, microsoft.com These deployments matter because they show that the AI Copilot Market is now being measured in enterprise-wide seat rollouts, not in narrow pilot groups. Once large employers make these commitments public, peer organizations face stronger internal pressure to justify slower adoption or smaller scope. GitHub Copilot also reached nearly 140,000 enterprise organizations by Q3 FY2026, which shows that the same benchmark logic is shaping technical teams as well as general productivity users. This is making seat economics more visible across the AI Copilot Market and supporting wider rollout decisions in which labor savings can be discussed in operational terms.

Embedded Copilot Workflows Reduce Switching Costs Across Saas Suites

Copilot tools gain traction faster when they are added to software that employees already use for much of the workday. ServiceNow announced in April 2026 that all customers would receive a complete AI package without an additional purchase and introduced Otto, a unified AI experience combining conversational AI, workflows, and enterprise search.[2]ServiceNow, Inc., “ServiceNow Moves Beyond the Sidecar AI Era, Giving Customers a Complete AI-Native Experience Across All Products and Packages,” ServiceNow, servicenow.com This reduces the need for a separate purchase case, thereby shortening sales cycles and lowering adoption friction. The result is that the AI Copilot Market is increasingly rewarding vendors that can embed copilots deeply into productivity, service, and workflow platforms rather than selling a standalone assistant. Buyers also face lower switching costs when the copilot is tied to data, permissions, and workflows already in place within the main software stack. That dynamic increases platform stickiness and puts more pressure on point solutions that cannot match the integration depth of large-suite providers.

Agentic Task Execution Expands Copilot Use Beyond Text Generation

The value of copilots is expanding because buyers now expect them to complete multistep work, not just generate responses. OpenAI introduced ChatGPT Work in July 2026 with integrations for Slack, Microsoft Teams, Google Drive, and SharePoint, positioning the product around autonomous execution inside existing workflow environments.[3]OpenAI, “ChatGPT Is Now a Partner for Your Most Ambitious Work,” OpenAI, openai.com Salesforce also launched Agentforce IT Service in February 2026, adding an agentic CMDB and autonomous IT resolution for enterprise service workflows. These launches show that the AI Copilot Market is moving from writing assistance toward execution, orchestration, and system interaction. As this shift continues, product value increasingly depends on identity controls, workflow access, and system integration rather than on model novelty alone. That keeps the AI Copilot Market closely tied to enterprise software architecture, because autonomous work still needs governance, approval paths, and clear operational boundaries.

Private Model Hosting Accelerates Regulated Enterprise Adoption

Regulated organizations have adopted copilots more carefully because they need stronger control over data, infrastructure, and oversight. The EU AI Act made Annex III high-risk system obligations effective from August 2, 2026, increasing the importance of technical documentation, conformity assessment, and human oversight for regulated use cases.[4]European Union, “Regulation (EU) 2024/1689 of the European Parliament and of the Council,” EUR-Lex, eur-lex.europa.eu Google stated that its Distributed Cloud platform can run Gemini model inference on customer-controlled hardware, while Teradata introduced AI Factory for private AI environments that require full data custody. These developments are expanding the AI Copilot Market by enabling deployment in sectors that could not rely solely on open cloud architecture. They also support hybrid and on-premises adoption patterns, since many buyers want cloud speed for low-risk tasks and tighter control for sensitive work. This is creating space for infrastructure-focused providers and application vendors, giving the AI Copilot Market a broader supply chain than it had before 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hallucination Risk and Output Verification Costs Slow High-Stakes Adoption | -2.8% | Global, strongest in regulated sectors such as healthcare, legal, and financial services | Short term (≤ 2 years) |

| Data Residency and Prompt Leakage Concerns Restrict Cloud-First Rollouts | -2.3% | Europe, Asia-Pacific, and Middle East regulated environments | Short term (≤ 2 years) |

| Copilot Sprawl Creates Seat Overlap And Governance Friction | -1.6% | North America and Europe, especially in large enterprises | Medium term (2-4 years) |

| Model Refresh Cycles Compress Differentiation And Pressure Pricing | -1.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hallucination Risk and Output Verification Costs Slow High-Stakes Adoption

Output reliability remains a core issue when copilots are used in legal, financial, healthcare, and public administration work. The EU AI Act places particular emphasis on human oversight and controlled use in higher-risk contexts, reflecting the need for traceable, reviewable outputs in sensitive workflows. This means the AI Copilot Market is not held back by curiosity or access, but by the cost of validating output before it can be used in high-consequence settings. Verification work reduces the time savings that buyers expect from deployment, especially where every response must be checked against policy, legal rules, or approved records. The issue is especially important for the fastest-growing regulated workflow use cases, because those applications depend on source attribution, defensible reasoning, and documented control. Until more vendors can combine speed with dependable governance, the AI Copilot Market will continue to face slower adoption in work where a single mistake can outweigh a large productivity gain.

Data Residency and Prompt Leakage Concerns Restrict Cloud-First Rollouts

Many enterprise buyers need assurance that prompts, internal documents, and workflow data remain inside approved geographic and technical boundaries. The EU AI Act has strengthened compliance expectations in regulated domains, while Google and Teradata have both positioned customer-controlled, private AI environments as solutions for organizations seeking greater infrastructure control. This has made hybrid deployment more attractive, as it allows firms to separate low-, and high-risk workloads without abandoning cloud-based productivity features. It also changes vendor selection criteria, since regulated buyers increasingly expect deployment flexibility as a baseline capability. The AI Copilot Market is therefore expanding fastest where providers can offer cloud convenience together with stronger controls for data handling and prompt privacy. Vendors that cannot support these requirements may still win small pilots, but they face a narrower path to large enterprise rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Incumbents Consolidate While Industry-Specific Entrants Accelerate

Horizontal Productivity Copilots held 40.12% of the AI Copilot Market share in 2025, which made them the largest copilot category by revenue. Their lead reflects the strength of tools that sit directly inside Microsoft 365, Google Workspace, and similar work environments, where users already spend a large part of the day. This placement shortens adoption cycles because organizations do not need to introduce a completely separate work surface or procurement category. It also helps large vendors bundle Copilot access into existing commercial agreements, making expansion easier once the first teams begin using the product. In the AI Copilot Market, this creates a self-reinforcing pattern where attention, integration, and procurement convenience all favor horizontal platforms.

Functional Workflow Copilots remained an important second tier because they support specific business processes in HR, finance, legal, and supply chain functions. Their value comes from task libraries and workflow alignment that connect more tightly with enterprise systems from providers such as SAP SE and Oracle. Technical and Engineering Copilots also advanced quickly, supported by GitHub Copilot momentum across nearly 140,000 enterprise organizations by Q3 FY2026. That trend suggests that engineering teams are becoming a second-scale engine for the AI Copilot Market, especially when coding, testing, and documentation tasks can be automated in controlled environments. Industry-Specific Copilots are projected to expand at a 30.84% CAGR through 2031 because healthcare, financial services, manufacturing, and legal buyers need domain-trained tools that can meet narrower accuracy and compliance expectations than a general assistant can support.

By Deployment Mode: Cloud Leads While Hybrid Scales Fast

Cloud-Based deployment accounted for 71.24% of the AI Copilot Market size in 2025, making it the largest deployment mode by a wide margin. The lead came from ease of activation, faster access to updated models, and the fact that many enterprises already had working relationships with major cloud providers. Cloud delivery also lowers the technical barrier by having the vendor manage the inference infrastructure, updates, and service availability. In practical terms, this allowed the AI Copilot Market to scale rapidly across organizations that wanted speed and limited implementation friction. It also aligned well with broad productivity use cases where sensitivity levels were lower, and the goal was quick activation across office workflows.

On-Premises deployment remained relevant in defense, intelligence, and central banking environments where data egress limits were much stricter. Hybrid deployment is projected to grow at a 31.16% CAGR through 2031 because it enables organizations to balance convenience and control. Google positioned Distributed Cloud around customer-controlled inference, and Teradata introduced AI Factory for private AI deployment with full data custody needs. These offerings show that hybrid design is no longer a temporary compromise, but a practical architecture for enterprises that need cloud-based interfaces and tighter governance for regulated tasks. As a result, the AI Copilot Market is broadening beyond pure SaaS delivery and giving infrastructure control a stronger role in buying decisions.

By Organization Size: Large Enterprise Leadership Masks An Sme Inflection

Large Enterprises accounted for 68.43% of revenue in 2025, indicating that organizations still led the AI Copilot Market with the scale to absorb change management, licensing, and integration costs. The strongest examples came from enterprise-wide rollouts where seat counts were large enough to justify direct governance and training programs. Microsoft reported that Accenture committed 740,000 Microsoft 365 Copilot seats, which remained the largest disclosed deployment in the market by April 2026. JBS also announced in March 2026 that Denso had reached 30,000 office workers with a 99% utilization rate and planned to extend deployment across its global group. These cases show why large enterprises continue to anchor the AI Copilot Market, since they can spread implementation costs across a bigger workforce and integrate copilots into complex process environments.

Small and Medium Enterprises are projected to grow at a 30.41% CAGR through 2031, indicating a clear widening of demand beyond the largest buyers. Intuit reported in its 2026 AI Impact Report that 77% of surveyed U.S. small and midsize businesses were using AI regularly in January 2026, up from 48% 18 months earlier, and 78% reported improved productivity. OECD data also showed a wide adoption gap between large and small firms in the EU in 2025, which indicates substantial room for SME catch-up. This gives the AI Copilot Market a strong medium-term expansion path through self-serve onboarding, pay-as-you-go pricing, and ready-made workflow templates. SMEs may not match enterprise seat counts, but their volume can become a major recurring revenue base if vendors keep deployment simple and pricing predictable.

By Application: Knowledge Work Anchors Today, Regulated Workflows Define Tomorrow

Knowledge Work and Productivity Assistance accounted for 33.18% of the AI Copilot Market in 2025, making it the largest application group. That position reflects the broad need for meeting summaries, drafting support, internal search, and day-to-day content creation across almost every industry. The category has scale because it maps to common office work instead of requiring a specialized data model or a dedicated process environment. In the AI Copilot Market, these use cases often become the first deployment wave because they can be introduced quickly and measured through time savings and user adoption. Software Engineering and Technical Operations also remained a major application area because code generation, testing support, and DevSecOps assistance fit naturally into structured digital workflows.

Customer and Employee Service Operations continued to gain relevance, as organizations sought measurable gains in response time and operational efficiency. Sales, Marketing, and Revenue Enablement tools also advanced as firms sought more consistent personalization and recommendation support within CRM-heavy environments. The market is shifting most quickly toward Regulated Industry Workflows, which are projected to grow at a 31.73% CAGR through 2031. This includes healthcare documentation, financial compliance drafting, legal discovery, and government case management, where outputs must be attributable, reviewable, and fit for formal decision processes. That shift matters because it pushes the AI Copilot Market beyond convenience tasks and into work with higher commercial value, but it also raises the importance of auditability, approval design, and deployment controls. The fastest growth is therefore coming from the application areas where product quality is judged less by fluency and more by whether the output can stand up to scrutiny.

By End-User Industry: It Leads, Government Drives Next Demand

IT and Telecommunications accounted for 22.47% of the AI Copilot Market revenue in 2025, making it the largest end-user industry. The segment moved early because AI-assisted development, network operations support, and automated service interactions fit well with digital workflows that were already software-centric. Firms in this segment also had stronger internal technical capacity, which reduced the friction of testing, securing, and scaling new tools. BFSI remained one of the next largest end-user groups because document processing, compliance monitoring, and personalized service use cases were commercially important, even if adoption was more deliberate. Healthcare and Life Sciences also continued to move forward, with copilots used for documentation, report drafting, and research-related workflows, though deployment design remained closely tied to data protection requirements.

Retail and E-Commerce companies continued to apply copilots to pricing, inventory support, and customer interaction generation. Industrial Manufacturing also expanded its use in maintenance support, process documentation, and supplier-facing work, where technical and engineering co-pilots can improve consistency. Government and Administration is projected to grow at a 30.92% CAGR through 2031, making it the fastest-growing end-user segment in the AI Copilot Market. California's Department of Technology announced in July 2026 that state departments and local governments would gain access to Claude at a 50% discount through a statewide agreement with Anthropic. This kind of centralized procurement can scale access much faster than department-by-department buying, which is why the AI Copilot Market is now seeing public administration move from a cautious buyer group to a large-volume demand center.

Geography Analysis

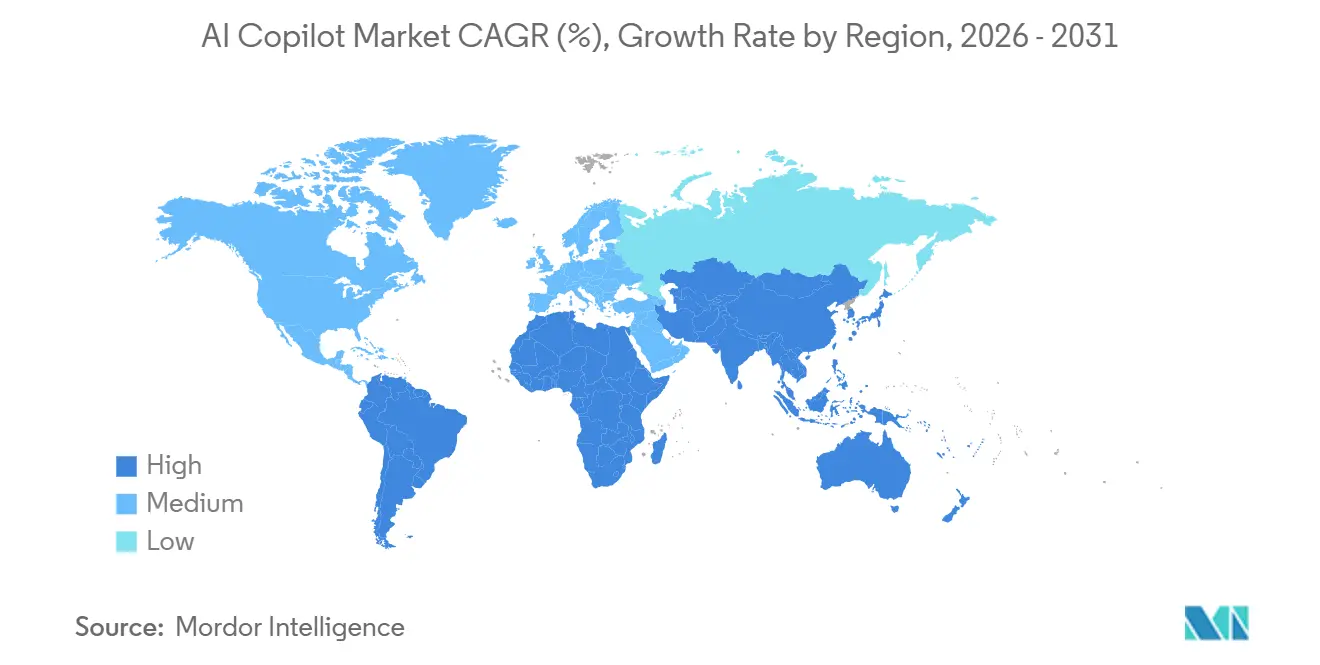

Asia-Pacific held 23.64% of the AI Copilot Market share in 2025, making it the largest regional market. The region benefited from public support for digital infrastructure, a large technology services workforce, and strong domestic competition in language model development. Country patterns within Asia-Pacific were not uniform, but large enterprise adoption in Japan showed that productivity pilots could move from the pilot stage to broad use when the deployment fit existing work habits. Microsoft customer stories showed that Nippon Steel expanded from an initial pilot to 11,000 enterprise licenses, while Mitsui and Co. maintained a very high monthly active utilization rate across nearly 5,000 users. These examples indicate that the AI Copilot Market in Asia-Pacific is supported by both workforce scale and a growing willingness to integrate copilots into core office and industrial workflows.

North America is projected to expand at a 31.38% CAGR through 2031, making it the fastest-growing regional market. The main reason is that procurement is shifting from departmental trials to multi-year commercial commitments that connect AI software with broader IT spending. Microsoft stated that new commercial bookings rose sharply in Q3 FY2026, suggesting a deeper pipeline of committed future AI and cloud expenditure. The AI Copilot Market in North America is also gaining support from state-level public-sector buying, as evidenced by California's statewide Anthropic agreement.

Europe, the Middle East, and Africa followed different demand paths in the AI Copilot Market. In Europe, the EU AI Act is reshaping supplier qualification by increasing the importance of compliance, human oversight, and infrastructure choices that fit regulated use cases. This favors vendors that already have data-residency-ready infrastructure and documented governance processes. In the Middle East and Africa, demand is building through public digital transformation programs and sovereign AI priorities, attracting greater vendor attention. South America remained earlier in the maturity cycle, with adoption still more concentrated in technology and financial services users who can access global platform offerings.

Competitive Landscape

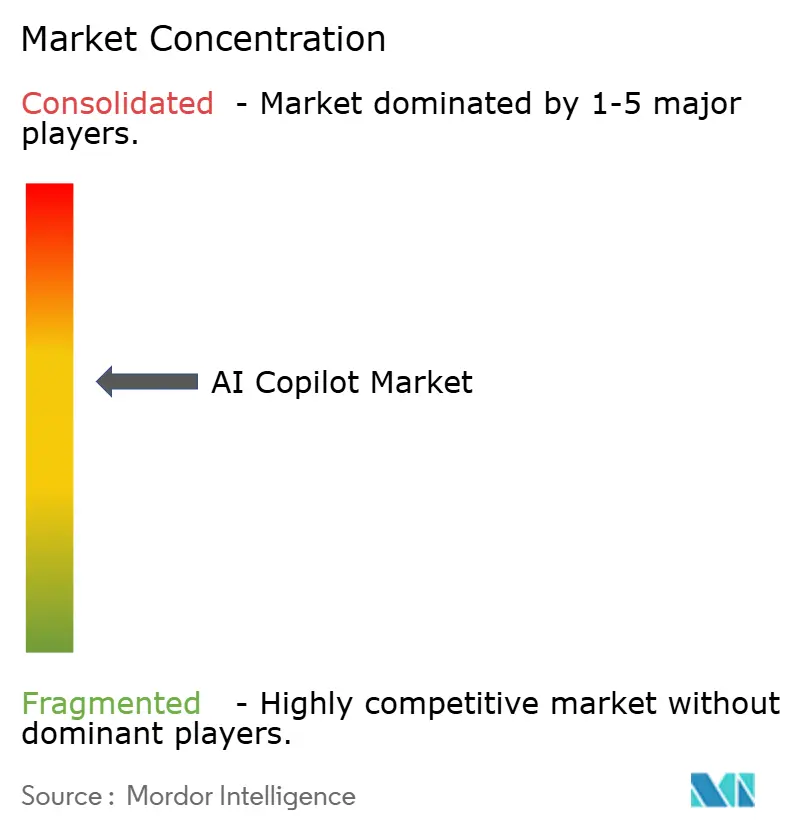

The AI Copilot Market showed moderate concentration at the platform layer, where Microsoft, Alphabet Inc., Salesforce, ServiceNow, and SAP had strong positions through existing enterprise relationships and software footprints. At the same time, the specialist layer remained fragmented because many vendors were competing in narrow workflow, vertical, and infrastructure categories. This created a market where scale mattered, but control over every use case was still far from settled. Microsoft continued to set the pace in enterprise seat volume through Microsoft 365 Copilot and GitHub Copilot, while ServiceNow, Salesforce, and OpenAI were all pushing toward more agentic product positioning. The competitive center of gravity in the AI Copilot Market is therefore shifting toward vendors that can combine scale, workflow access, and governance with broad enterprise distribution.

Several strategic moves during 2026 showed how competition is evolving. Salesforce launched Agentforce IT Service to target enterprise service management, featuring autonomous resolution and an agentic CMDB. OpenAI launched ChatGPT Work with integrations for collaboration and document systems, positioning the product as an execution layer within common enterprise tools. ServiceNow introduced Otto and expanded Build Agent integrations with major coding tools without additional licensing costs, strengthening its position in embedded enterprise workflow automation. These moves suggest that the AI Copilot Market is rewarding product breadth and integration reach more than stand-alone assistance features.

There is still meaningful white space in governance, observability, and model flexibility. Anthropic launched the Claude Partner Network in 2026 with an initial USD 100 million commitment, which signaled a push to build a more structured enterprise implementation ecosystem around its models. Glean also launched AI Gateway in July 2026 to help enterprises manage model access, governance, and costs across multiple LLM providers through a single interface. These actions point to a market where buyers want less lock-in and more control over how models are selected and governed. As the AI Copilot Market matures, competitive advantage is likely to come from orchestration, deployment choice, and operational trust as much as from model capability itself.

AI Copilot Industry Leaders

Microsoft Corporation

Alphabet Inc.

Salesforce, Inc.

ServiceNow, Inc.

Adobe Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: OpenAI launched ChatGPT Work, an agentic platform pairing GPT-5.6 models with enterprise integrations for Slack, Microsoft Teams, Google Drive, and SharePoint, enabling autonomous multi-step task execution within existing workflow environments. The launch directly targets enterprise productivity copilot incumbents by consolidating ChatGPT Enterprise's historical suite into a unified agentic interface with spend controls for enterprise administrators.

- July 2026: California's Department of Technology signed a statewide agreement with Anthropic, granting all California state departments and local governments access to Claude at a 50% discount through the SITeS procurement portal, alongside free workforce training and technical assistance.

- July 2026: Glean launched AI Gateway, an enterprise AI control plane enabling organizations to manage model access, governance, and cost optimization across multiple LLM providers through a single interface, addressing the multi-vendor complexity emerging in large enterprise AI stacks.

- May 2026: Anthropic raised USD 65 billion in Series H funding at a USD 965 billion post-money valuation, led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia Capital. The company's run-rate revenue had crossed USD 47 billion at the time of the raise, making it one of the largest private technology fundraises on record and valuing Anthropic ahead of many Fortune 100 enterprises.

Global AI Copilot Market Report Scope

The AI copilot market refers to the ecosystem of artificial intelligence-driven intelligent assistants integrated into enterprise and consumer software applications to enhance human capabilities and automate complex tasks. These copilots leverage advanced foundation models, including large language models (LLMs) and generative AI, to provide real-time contextual suggestions, generate content, analyze data, and execute workflows seamlessly within existing digital tools. The market encompasses various copilot types, ranging from general horizontal productivity tools and technical engineering assistants to specialized, functional, and industry-specific solutions. Deployed across cloud, hybrid, and on-premises environments, these AI systems serve organizations of all sizes worldwide. They are used across diverse applications, including knowledge work assistance, software development, customer and employee service operations, and sales enablement, across industries such as IT, BFSI, healthcare, and manufacturing. By acting as interactive embedded partners rather than standalone tools, AI copilots help organizations drive operational efficiency, reduce manual cognitive load, improve decision-making accuracy, and accelerate digital transformation.

The AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Copilot Type | Horizontal Productivity Copilots | ||

| Functional Workflow Copilots | |||

| Technical and Engineering Copilots | |||

| Industry-Specific Copilots | |||

| By Deployment | Cloud-Based | ||

| Hybrid | |||

| On-Premises | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Application | Knowledge Work and Productivity Assistance | ||

| Software Engineering and Technical Operations | |||

| Customer and Employee Service Operations | |||

| Sales, Marketing and Revenue Enablement | |||

| Business Process and Enterprise Operations | |||

| Regulated Industry Workflows | |||

| By End-User Industry | IT and Telecommunication | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Industrial Manufacturing | |||

| Education and Research Institutions | |||

| Media and Entertainment | |||

| Government and administration | |||

| Energy and Utilities | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the AI Copilot sector?

The AI Copilot Market size was valued at USD 21.45 billion in 2025, USD 27.25 billion in 2026, and is forecast to reach USD 96.05 billion by 2031 at a CAGR of 28.65% over 2026-2031.

Which copilot category leads revenue today?

Horizontal Productivity Copilots led revenue with a 40.12% share in 2025 because they are embedded in widely used workplace platforms and are easier to roll out at scale.

Which deployment model is growing fastest for enterprise adoption?

Hybrid deployment is projected to grow at a 31.16% CAGR through 2031 because it balances cloud convenience with tighter control over sensitive data and regulated workflows.

Why are large enterprises still ahead in adoption?

Large enterprises held 68.43% of revenue in 2025 because they can absorb licensing, governance, and integration costs more easily and can spread gains across a larger workforce.

Which application area is expanding the fastest?

Regulated Industry Workflows are projected to grow at a 31.73% CAGR through 2031 as buyers push copilots into healthcare, finance, legal, and government processes that need stronger oversight.

Which region is expected to grow the fastest through 2031?

North America is projected to expand at a 31.38% CAGR through 2031, supported by large enterprise contracts and rising public-sector procurement activity.

Page last updated on: