AI Code Generation and Developer Assistant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

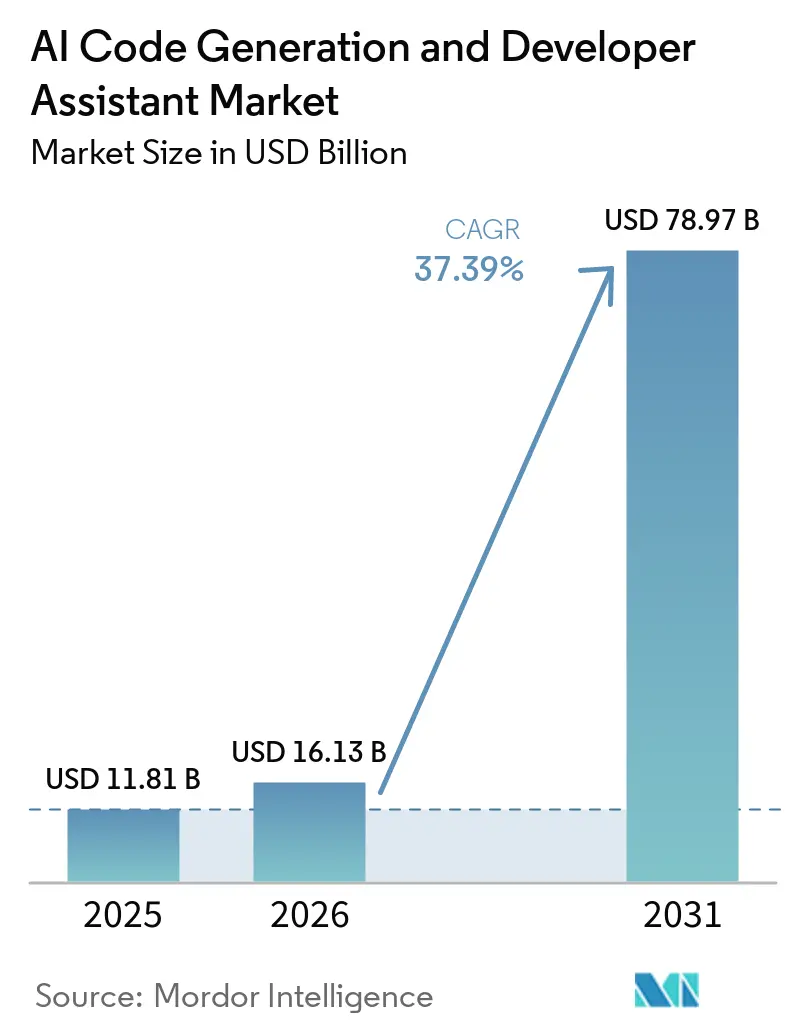

| Market Size (2026) | USD 16.13 Billion |

| Market Size (2031) | USD 78.97 Billion |

| Growth Rate (2026 - 2031) | 37.39% CAGR |

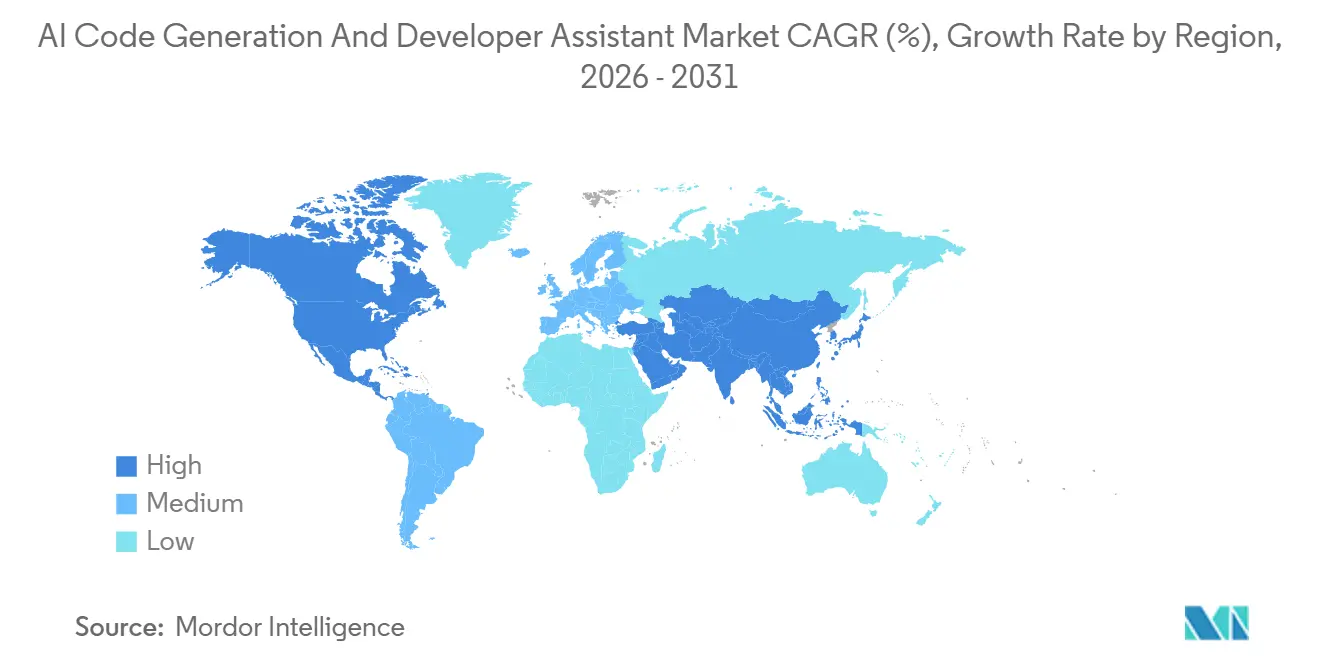

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Code Generation and Developer Assistant Market Analysis by Mordor Intelligence

The AI code generation market size is expected to grow from USD 11.8 billion in 2025 to USD 16.13 billion in 2026 and is forecast to reach USD 78.97 billion by 2031 at 37.39% CAGR over 2026-2031. Developer shortages, projected to deepen by 40% in 2026, are pushing enterprises toward automated tooling that boosts productivity without requiring proportional hiring. Large language models are now capable of context-aware synthesis, letting organizations embed assistants directly into integrated development environments and DevOps flows. Early movers report productivity gains ranging from 20% to 45%, even though nearly half of AI-generated code fails its first security review. Competitive urgency is intensifying as hyperscalers, independent software vendors, and venture-backed start-ups all race to lock in distribution before switching costs harden.

Key Report Takeaways

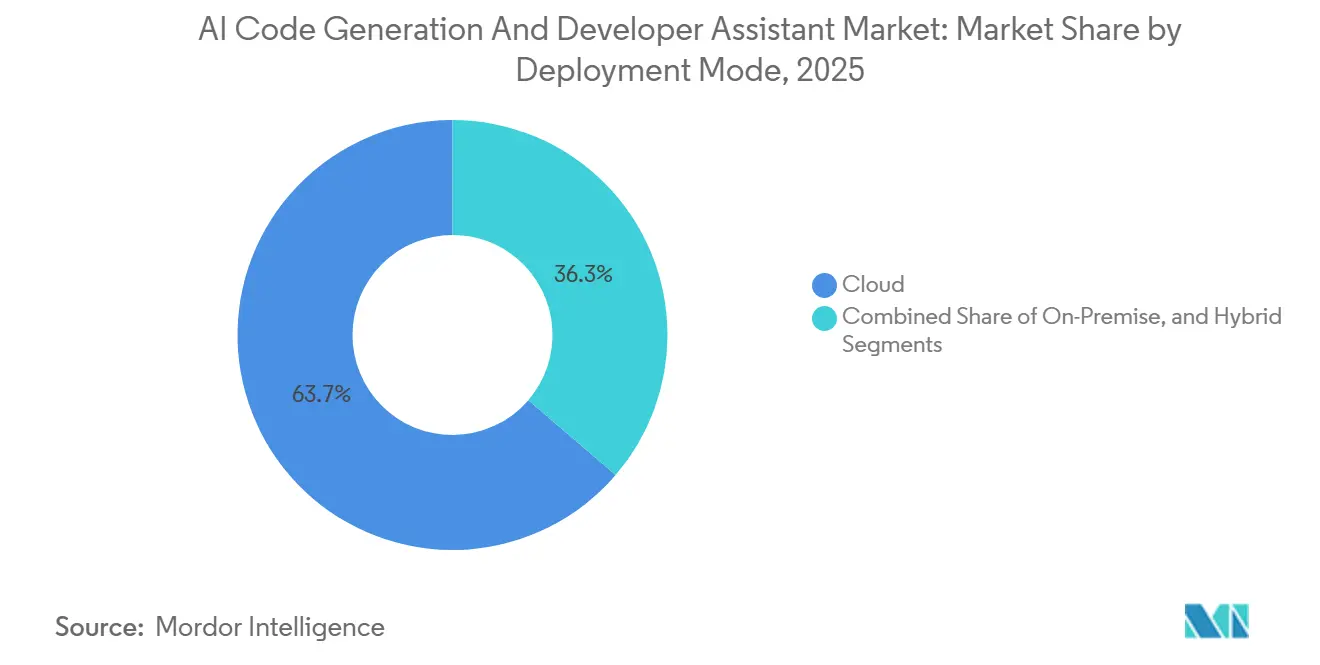

- By deployment mode, cloud deployment accounted for 63.71% of 2025 revenue, while hybrid deployment is the fastest-growing mode, with a 37.99% CAGR to 2031.

- By function, code generation and autocompletion led with 46.33% share in 2025, whereas agentic workflow orchestration is expanding at a 38.59% CAGR over the forecast period.

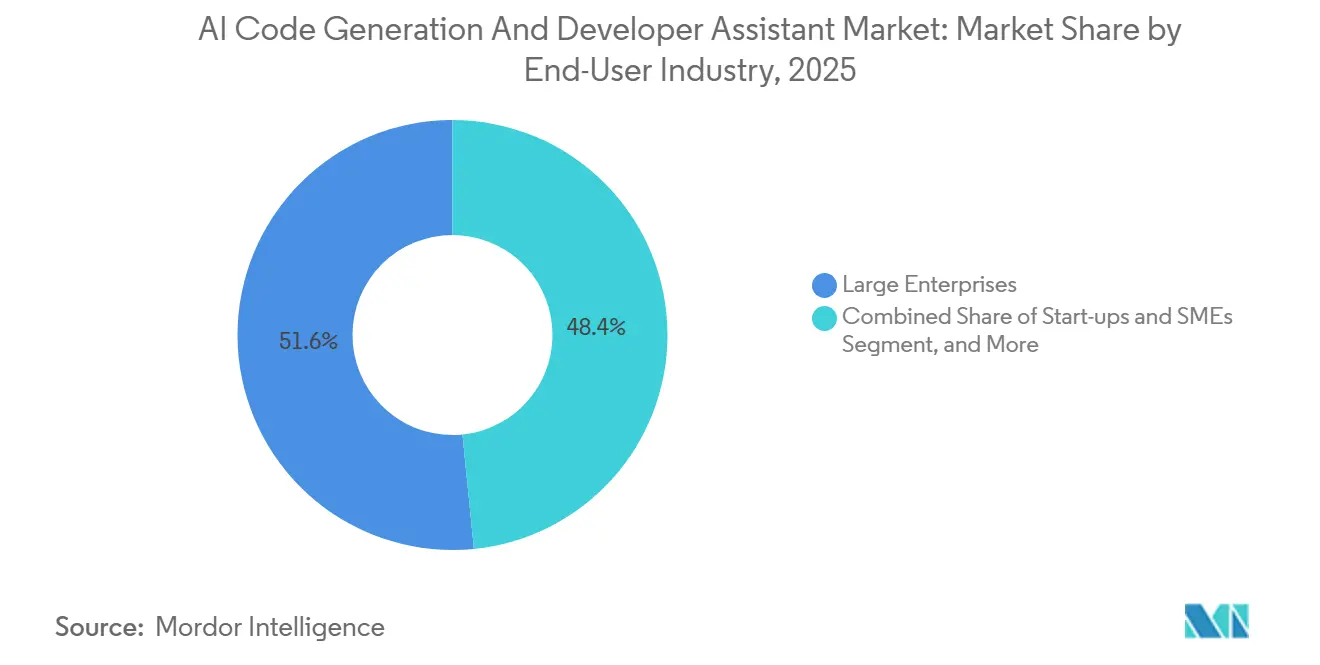

- By end-user industry, large enterprises accounted for 51.59% of the 2025 total, yet small and medium enterprises are advancing at 38.67% CAGR.

- By application, software development accounted for 49.42% of 2025 spend, while DevOps and CI/CD are projected to grow at a 37.73% CAGR through 2031.

- By geography, North America accounted for 39.37% of 2025 demand, but Asia-Pacific is poised for the fastest growth, with a 37.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Code Generation and Developer Assistant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Enterprise Adoption of AI-Assisted Development Tools | +6.5% | Global with concentration in North America and Europe | Short term (≤ 2 years) |

| Rapid Advances in Large Language Models Enabling Context-Aware Code Generation | +5.5% | Global | Medium term (2-4 years) |

| Growing Shortage of Skilled Software Developers Worldwide | +4.8% | Global, acute in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Integration of AI Assistants into Popular IDEs and DevOps Pipelines | +4.2% | Global | Short term (≤ 2 years) |

| Emergence of Agentic Workflows Automating Multi-Step Coding Tasks | +3.8% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| On-Device or Edge Code-Generation Models Reducing Data-Sovereignty Barriers | +2.5% | Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Enterprise Adoption Of AI-Assisted Development Tools

Enterprise procurement surged in 2025 and 2026 as businesses sought faster release cycles to counter limited headcount. Microsoft disclosed 15 million Microsoft 365 Copilot seats and 4.7 million GitHub Copilot paid subscribers by the second quarter of 2026, demonstrating board-level endorsement of automated coding platforms.[1]Microsoft Corporation, “Investor Relations – FY26 Q2 Earnings,” microsoft.com Replit reported that 85% of Fortune 500 firms now use its workspace, proving that adoption has moved beyond pilot programs. Companies that embed assistants into day-to-day workflows record 55% faster code completion on average, but legal and compliance reviews are lengthening procurement cycles. Vendors responding with explicit IP indemnities and usage analytics are gaining favor, especially in regulated sectors. The net effect is a short-term surge in revenue concentration among players offering enterprise-grade governance features.

Rapid Advances In Large Language Models Enabling Context-Aware Code Generation

The release of GPT-5.4 in early 2026 lifted reasoning accuracy and expanded context windows, allowing assistants to span entire repositories in a single prompt. GitHub integrated the upgrade within hours, which immediately translated into higher solution rates for multi-file edits and automatic test generation. Anthropic’s Claude 3.5 Sonnet, already woven into Replit’s Agent, triggered a tenfold revenue jump for the platform in the months after launch. Frontier-model vendors are pivoting from pure inference services toward differentiated reasoning APIs, opening a premium tier that cost-sensitive firms may find prohibitive. Smaller open-source models lag, leaving the market divided between elite paid offerings and value-oriented alternatives.

Growing Shortage Of Skilled Software Developers Worldwide

Stack Overflow data show an estimated shortfall of 1.4 million to 4 million developers in 2025, worsening by 40% in 2026. The median time-to-hire for senior engineers in North America has stretched past 90 days, forcing companies to supplement rather than replace talent. AI code assistants enable adjacent roles to contribute to codebases, broadening the talent pool. Enterprises are launching internal AI literacy programs so product managers and designers can author prototypes, easing pressure on overstretched engineering teams. Yet reliance on machine-generated code introduces technical debt, so firms retain senior reviewers to refactor outputs before production.

Integration Of AI Assistants Into Popular IDEs And DevOps Pipelines

Developer enthusiasm rises when suggestions appear inline without context switching. GitHub Copilot now supports Visual Studio Code, JetBrains, Neovim, Xcode, and Eclipse, providing a consistent experience across teams' preferred editors. Sourcegraph’s Cody allows hot-swapping between multiple models in JetBrains, letting engineers trial different outputs instantaneously. Tabnine extended agentic capabilities to the command line in January 2026, automating repository analysis and test execution.[2]Tabnine, “Trusted AI Now Generally Available,” tabnine.com Deep integration lowers friction and drives daily active usage, which in turn cements vendor lock-in through stored prompts, preference files, and project-level settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intellectual-Property and Licensing Uncertainty Around AI-Generated Code | -4.5% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Data-Privacy and Security Concerns in Regulated Industries | -3.2% | Global, particularly Europe, North America, Asia-Pacific | Medium term (2-4 years) |

| Model Hallucination Leading to Hidden Security Vulnerabilities | -2.0% | Global | Medium term (2-4 years) |

| Integration Complexity with Legacy Build Systems and Toolchains | -1.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Intellectual-Property And Licensing Uncertainty Around AI-Generated Code

The class-action suit alleging Copilot training infringed copyrighted repositories remains unresolved, producing board-level hesitancy in sectors with strict IP stewardship. Tabnine counters by training solely on permissive licenses and offering broad indemnity clauses. Legal clarity is unlikely before 2027, so many companies insist on human review of every AI contribution and audit trails linking code snippets to prompts. Vendors with transparent dataset provenance and contractual indemnity are capturing finance and healthcare accounts, while opaque models face elongated sales cycles.

Data-Privacy And Security Concerns In Regulated Industries

IEEE research found that AI-generated code embeds 1.88 times more hardcoded passwords and 2.74 times more cross-site-scripting vectors than human-generated code. Healthcare, finance, and defense organizations cannot risk pushing proprietary logic through multi-tenant clouds, so on-premises or air-gapped options have grown in appeal. Tabnine’s Trusted AI platform supports Dell PowerEdge servers and zero data retention, satisfying GDPR, HIPAA, and ISO 9001 frameworks. Anthropic’s Claude Marketplace adds centralized procurement controls, giving compliance teams unified spend visibility. Vendors that certify to FedRAMP or CMMC standards unlock budget pools otherwise unavailable to cloud-only competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Leadership, Hybrid Momentum

The cloud slice accounted for 63.71% of the 2025 value, reflecting the ease with which frontier models can be integrated into existing pipelines. This integration has become a cornerstone of the AI code-generation market-share narrative, as businesses increasingly prioritize the seamless adoption of advanced technologies. Hybrid configurations are advancing at a 37.99% CAGR, driven by enterprises seeking to balance data sovereignty with the benefits of continuous model upgrades. This trend is adding a significant wedge to the AI code generation market size calculation, as organizations aim to optimize their operational frameworks.

Cloud-first vendors are gaining traction by offering weekly model refreshes, pay-per-token billing, and instantaneous onboarding, making them the preferred choice for green-field projects. However, industries such as financial services, defense, and healthcare are increasingly opting for solutions like Tabnine or Rosetic, which provide single-tenant or air-gapped installations. These options are particularly appealing due to their compliance with stringent regulations such as GDPR and HIPAA. Multi-vendor strategies are also emerging, where low-risk internal tools remain in the cloud, while production code for critical workloads is compiled on-premises. Providers capable of unifying telemetry, policy, and billing across both cloud and on-premises environments are well positioned to gain market share in the broader AI code generation market by effectively addressing their clients' diverse needs.

By Function: Agentic Orchestration Takes Center Stage

Code generation and autocompletion accounted for 46.33% of 2025 spending, establishing themselves as the foundational components of the AI code generation market size for functional segments. These features remain critical for developers, offering significant efficiency gains and reducing manual coding efforts. However, agentic orchestration, while representing a smaller share of the market, is growing at an impressive 38.59% CAGR. This growth trajectory highlights its potential to redefine how teams derive value from AI-driven coding tools. Traditional functionalities, such as debugging, test generation, and documentation, are increasingly integrated into broader platforms rather than being offered as stand-alone solutions. This shift is diminishing the competitive edge of single-function tools, pushing vendors to innovate and expand their offerings to remain relevant in the evolving market landscape.

Advanced tools like Reflection AI and GitHub’s coding agents are transforming workflows by automating processes across the entire development lifecycle, from planning and coding to testing and pull-request stages. These capabilities enable enterprises to achieve significant headcount savings, which were previously considered unattainable. Organizations are now prioritizing platforms that combine orchestration capabilities with robust governance features, ensuring compliance and operational efficiency. This trend is creating pressure on single-function vendors to diversify their capabilities or risk being commoditized. As a result, the AI code generation industry is increasingly consolidating around comprehensive suites that integrate basic code-completion capabilities with advanced autonomous workflows, catering to the growing demand for end-to-end solutions.

By End-User Industry: Democratization Extends Reach

Large enterprises accounted for 51.59% of revenue in 2025, underscoring their dominance in early adoption of the AI code-generation market. These organizations have been quick to integrate AI-driven tools into their workflows, leveraging their resources to adopt advanced solutions that enhance productivity and efficiency. On the other hand, small and medium businesses (SMEs) are emerging as a rapidly growing segment, with a compound annual growth rate (CAGR) of 38.67%. This growth is supported by affordable subscription models, often priced around USD 10 per seat, which lower the barriers to entry for smaller organizations. SMEs are increasingly adopting browser-native platforms like Replit, which simplify the setup process and enable non-technical users, such as designers and marketers, to create prototypes using conversational prompts.

Enterprise buyers, however, have distinct priorities, focusing on features such as single sign-on, usage analytics, and custom model fine-tuning to safeguard their intellectual property and ensure seamless integration into existing systems. Educational institutions are also playing a significant role by incorporating AI assistants into their curricula, preparing students to enter the workforce with proficiency in AI-augmented workflows. While government and non-profit sectors have been slower to adopt these technologies due to stringent procurement processes, they represent a stable and reliable revenue stream once contracts are secured. This broad adoption across various verticals is contributing to the overall expansion of the AI code generation market, with each segment playing a unique role in shaping its growth trajectory.

By Application: DevOps Integration Unlocks New Efficiencies

Software development accounted for 49.42% of 2025 spend, highlighting its critical role in driving value within the AI code generation market. This segment remains a cornerstone as organizations increasingly adopt AI-powered tools to streamline coding processes and enhance efficiency. DevOps and CI/CD workflows are expected to grow at a robust 37.73% CAGR, indicating that the benefits of AI code generation extend beyond basic coding tasks to include automation of complex pipelines. Tools like Tabnine’s command-line interface enable seamless dependency updates and repository audits directly within the terminal, while GitHub Actions integrate Copilot suggestions into build scripts, further optimizing development workflows[3]Tabnine, “February Recap – Trusted AI,” tabnine.com. These advancements demonstrate the growing reliance on AI to simplify and accelerate software development processes.

Low-code and no-code platforms are also expanding the reach of AI code generation by empowering non-developers to create internal tools and prototypes with minimal technical expertise. This strategic shift aims to democratize access to AI-driven development, allowing a broader range of workers to contribute to innovation. Additionally, data science notebooks and embedded firmware projects are leveraging AI assistants for tasks such as boilerplate scaffolding, reducing manual effort, and accelerating project timelines. These developments underscore the increasing versatility of AI code-generation tools, which cater to a diverse range of use cases and user profiles, further solidifying their position within the broader software development ecosystem.

Geography Analysis

North America accounted for 39.37% of projected demand in 2025, establishing itself as the commercial anchor of the AI code-generation market. The region benefits from several structural advantages, including a high density of venture capital investments, the presence of hyperscalers, and an enterprise culture that prioritizes innovation. In the United States, federal programs actively promote AI adoption across both defense and civilian agencies, driving significant growth. Meanwhile, Canada and Mexico are experiencing a more gradual uptake of AI code generation technologies, primarily due to smaller talent pools and limited resources compared to the United States.

Asia-Pacific is emerging as the fastest-growing region, with a remarkable compound annual growth rate (CAGR) of 37.94%. This growth is fueled by India’s extensive developer workforce, which numbers approximately 5 million, and China’s robust sovereign AI programs. Companies like DeepSeek are introducing cost-efficient AI models that align with Chinese data-localization policies, ensuring compliance with local regulations. In India, major outsourcing firms are integrating AI-powered coding assistants to significantly reduce turnaround times for their Western clients, enhancing operational efficiency. Additionally, Japan and South Korea, both facing challenges related to shrinking workforces, are increasingly adopting AI coding tools as a means to boost productivity and address labor shortages.

Europe demonstrates a balance between moderate growth and regulatory leadership in the AI code generation market. The General Data Protection Regulation (GDPR) and the forthcoming EU AI Act are setting global benchmarks for compliance, creating opportunities for vendors that achieve early certification. These regulations not only shape the market but also encourage innovation among compliant vendors. In the Middle East and Africa, the market is still nascent but is showing signs of growth as governments invest in initiatives such as digital skills academies to build a future-ready workforce. Collectively, these regional dynamics contribute to a multi-polar growth trajectory, diversifying revenue streams and creating opportunities for vendors operating in the AI code generation market.

Competitive Landscape

OpenAI raised USD 122 billion in March 2026, pushing its valuation to USD 852 billion and funding the rapid expansion of Codex, which serves more than 2 million weekly users.[4]OpenAI, “OpenAI Raises USD 122 Billion,” openai.com Microsoft exploits its control of GitHub and Visual Studio to bundle Copilot into existing contracts, securing 4.7 million paid seats alongside 15 million Microsoft 365 Copilot licenses. Anthropic’s Claude Marketplace aggregates spend across partner applications, simplifying procurement for enterprises that favor consolidated billing.

Replit secured USD 400 million at a USD 9 billion valuation, ballooning annualized revenue from USD 2.8 million to USD 150 million within a year. Tabnine targets compliance-driven markets with zero data retention and air-gapped deployment, while Rosetic’s hybrid deterministic architecture aims to slash token costs by up to 80%. Cursor, valued at USD 29.3 billion in late 2025, reimagines the integrated development environment around AI-native workflows, challenging incumbents anchored to legacy editors.

Competition revolves around three levers such as model quality, deployment flexibility, and ecosystem integration. Frontier-model owners wield scale advantages but face scrutiny over the provenance of their training data. Start-ups leverage agility to ship niche features, such as deterministic reasoning engines or low-latency on-device models. Strategic partnerships, Replit with Google Cloud, GitLab with Claude, illustrate a land-grab for distribution before enterprise toolchains ossify, shaping the long-run structure of the AI code generation market.

AI Code Generation and Developer Assistant Industry Leaders

GitHub, Inc.

OpenAI L.L.C.

Anthropic P.B.C.

Replit, Inc.

Tabnine Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: OpenAI raised USD 122 billion in committed capital at a post-money valuation of USD 852 billion to scale Codex and expand compute infrastructure.

- March 2026: Replit closed a USD 400 million round at a USD 9 billion valuation, reporting 40 million users and USD 150 million annualized revenue.

- March 2026: Anthropic launched Claude Marketplace, allowing enterprises to allocate existing spend commitments to partner tools.

- March 2026: SolveAI secured USD 50 million across seed and Series A rounds to accelerate its conversational app-development platform.

Global AI Code Generation and Developer Assistant Market Report Scope

The AI Code Generation and Developer Assistant Market refers to the ecosystem of software tools and platforms that leverage artificial intelligence, particularly large language models and machine learning to assist in the software development lifecycle. These solutions enable automated or semi-automated code creation, enhancement, testing, debugging, and documentation, thereby improving developer productivity, reducing time-to-market, and minimizing human error.

The AI Code Generation and Developer Assistant Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Function (Code Generation and Autocompletion, Debugging and Error Detection, Code Review and Optimization, Test Generation, Documentation Generation, and Agentic Workflow Orchestration), End-User Industry (Individual Developers and Freelancers, Start-ups and SMEs, Large Enterprises, Educational Institutions, and Government and Non-Profit Organizations), Application (Software Development, DevOps and CI/CD, Data Science and Analytics, Embedded and IoT Development, and Low-Code/No-Code Development), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Code Generation and Autocompletion |

| Debugging and Error Detection |

| Code Review and Optimization |

| Test Generation |

| Documentation Generation |

| Agentic Workflow Orchestration |

| Individual Developers and Freelancers |

| Start-ups and SMEs |

| Large Enterprises |

| Educational Institutions |

| Government and Non-Profit Organizations |

| Software Development |

| DevOps and CI/CD |

| Data Science and Analytics |

| Embedded and IoT Development |

| Low-Code / No-Code Development |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Function | Code Generation and Autocompletion | ||

| Debugging and Error Detection | |||

| Code Review and Optimization | |||

| Test Generation | |||

| Documentation Generation | |||

| Agentic Workflow Orchestration | |||

| By End-User Industry | Individual Developers and Freelancers | ||

| Start-ups and SMEs | |||

| Large Enterprises | |||

| Educational Institutions | |||

| Government and Non-Profit Organizations | |||

| By Application | Software Development | ||

| DevOps and CI/CD | |||

| Data Science and Analytics | |||

| Embedded and IoT Development | |||

| Low-Code / No-Code Development | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the AI code generation market in 2026?

It is valued at USD 16.13 billion in 2026, on its way to USD 78.97 billion by 2031.

What is the forecast CAGR for AI-driven coding tools?

The market is projected to expand at a 37.39% CAGR between 2026 and 2031.

Which deployment model is growing fastest?

Hybrid architectures are advancing at 37.99% CAGR as organizations balance cloud agility with data sovereignty.

Where is regional growth most pronounced?

Asia-Pacific leads with a 37.94% CAGR, driven by developer scale in India and sovereign AI initiatives in China.

What functional capability shows the highest growth?

Agentic workflow orchestration tops growth at 38.59% CAGR as enterprises seek autonomous task execution.

Why are regulated industries cautious about AI code generation?

Concerns over IP ownership, data privacy, and increased security vulnerabilities slow adoption until vendors provide indemnification and on-premises options.

Page last updated on: