AI-Based Prior Authorization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 4.21 Billion |

| Growth Rate (2026 - 2031) | 19.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

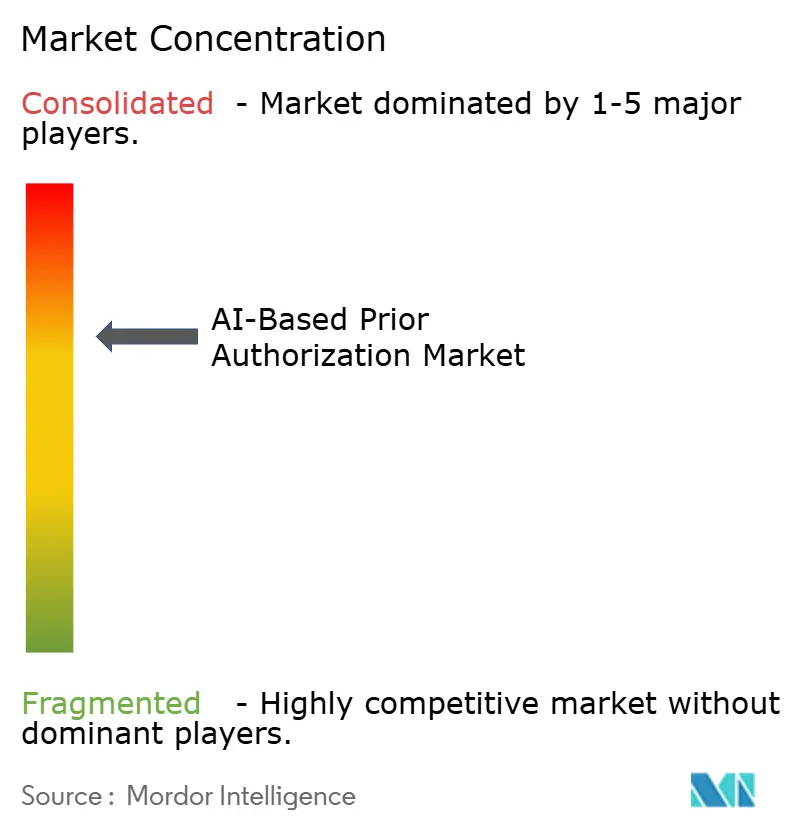

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Prior Authorization Market Analysis by Mordor Intelligence

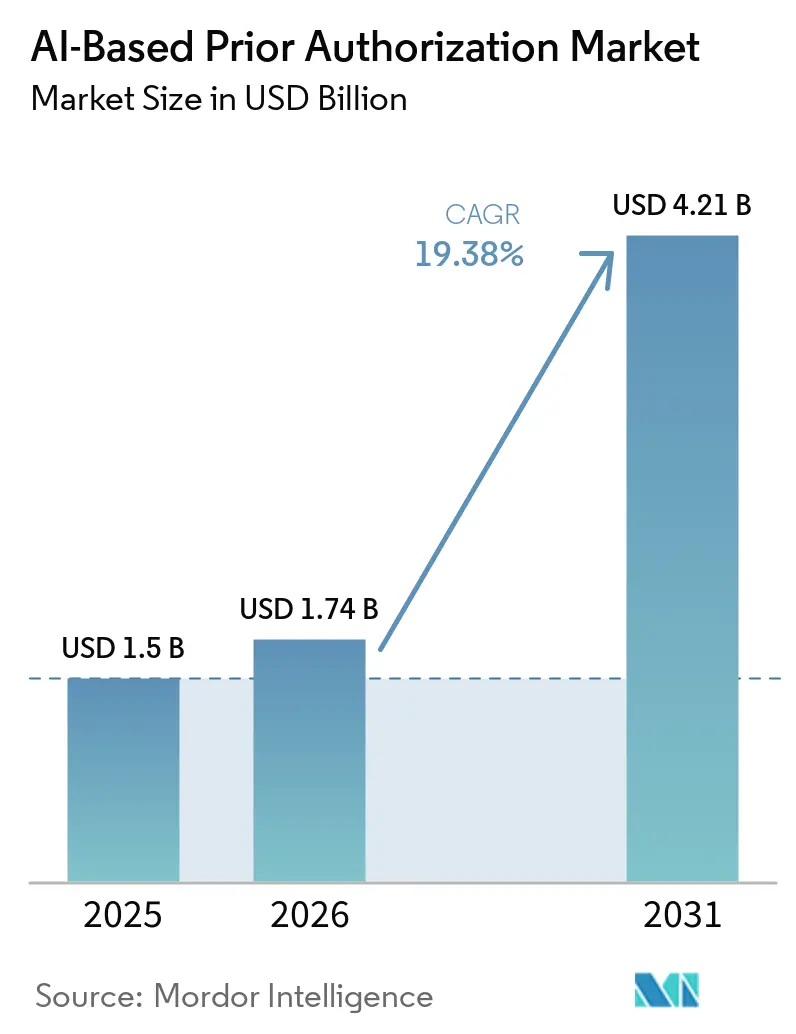

The AI-based prior authorization market size is expected to grow from USD 1.50 billion in 2025 to USD 1.74 billion in 2026 and is forecasted to reach USD 4.21 billion by 2031 at 19.38% CAGR over 2026-2031. Growth in the AI-based prior authorization market is being pushed by federal rules that now force faster decisions, stronger denial transparency, and API-based data exchange between payers and providers, which is shifting automation from a back-office option into a compliance requirement for many buyers. The AI-based prior authorization market is also being shaped by broader cost pressure across commercial plans, Medicare Advantage, and Medicaid managed care, where administrative savings and faster treatment approvals now carry direct financial value for both health plans and risk-bearing health systems. Buyers are no longer looking only for rules engines, because the AI-based prior authorization market is moving toward tools that can organize documentation, match evidence to payer criteria, and fit directly into clinical and revenue cycle workflows. Vendor positioning is also changing, because the AI-based prior authorization market now rewards platforms that can support FHIR-based interoperability, explainability controls, audit readiness, and cloud delivery without forcing clients into long implementation cycles. The result is a market where growth reflects a structural redesign of evidence exchange and utilization management, while state oversight of opaque AI decisions continues to shape how fast vendors can scale standardized models across jurisdictions.

Key Report Takeaways

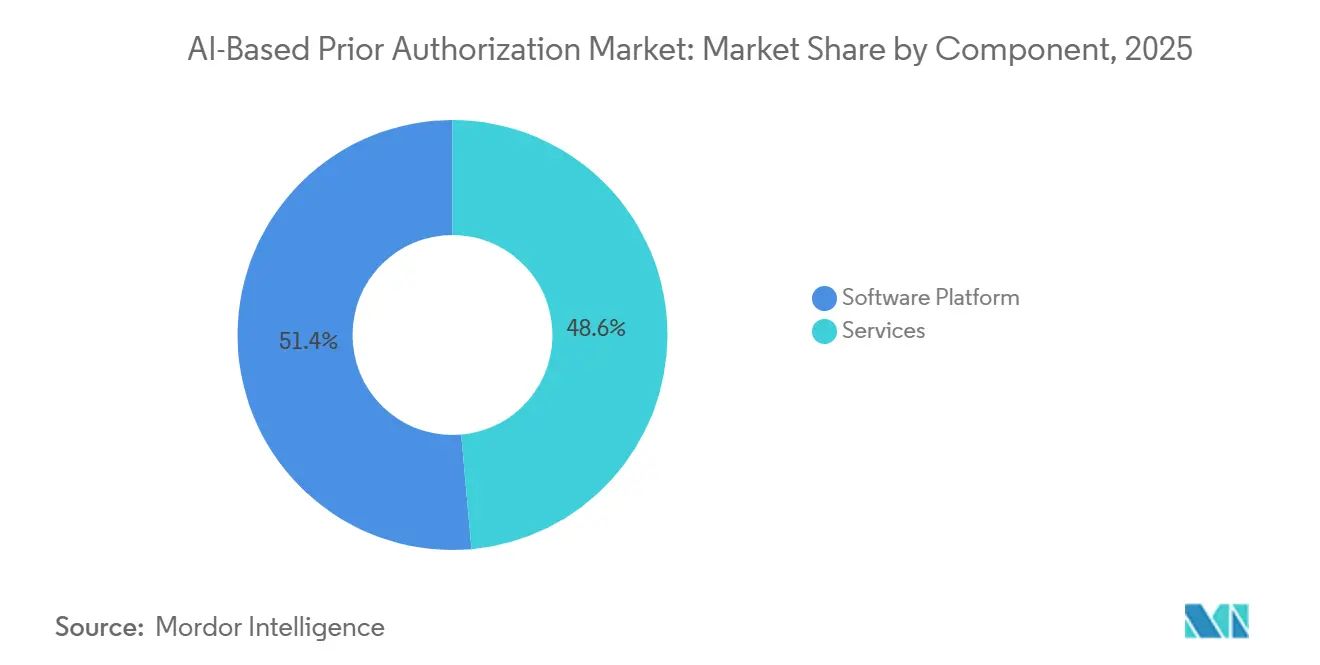

- By component, the software platform led with 51.44% of revenue in 2025, while services are forecasted to expand at a 19.67% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 55.76% of revenue in 2025 and also posted the highest projected CAGR at 20.17% through 2031.

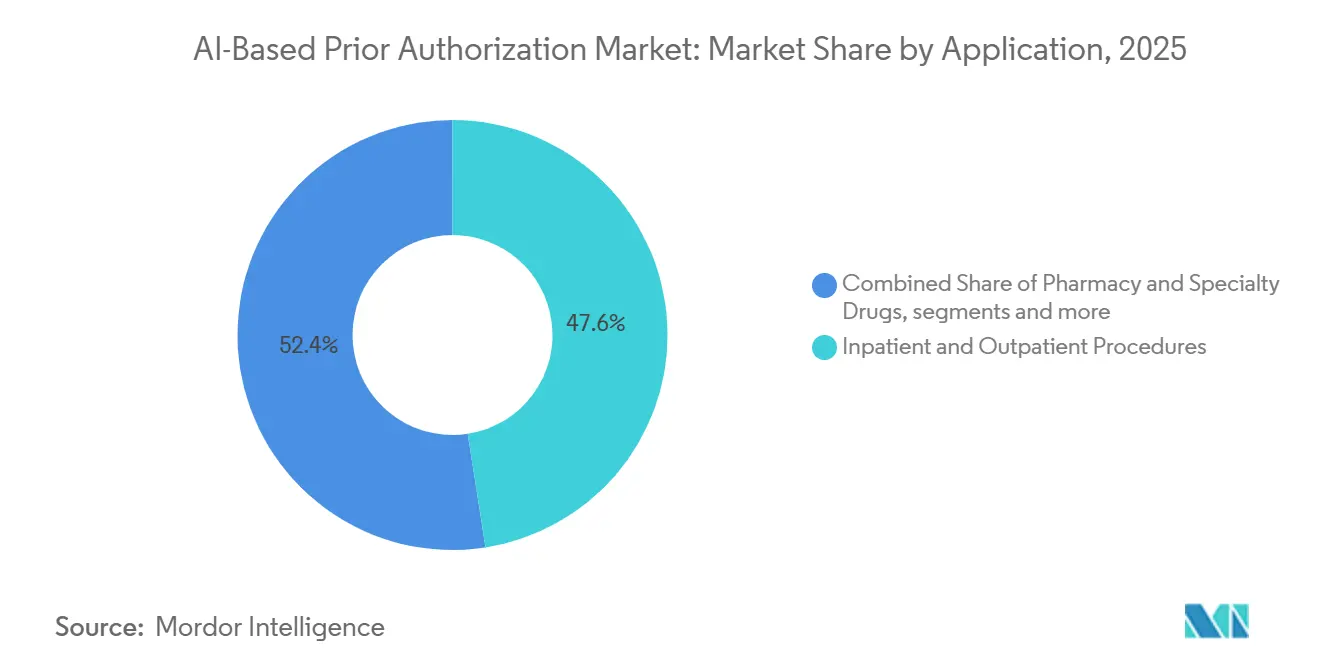

- By application, inpatient and outpatient procedures captured 47.55% of revenue in 2025, while pharmacy and specialty drugs are projected to grow at a 19.64% CAGR through 2031.

- By end-user, healthcare payers held 49.64% of revenue in 2025, while healthcare providers recorded the fastest projected CAGR at 20.36% through 2031.

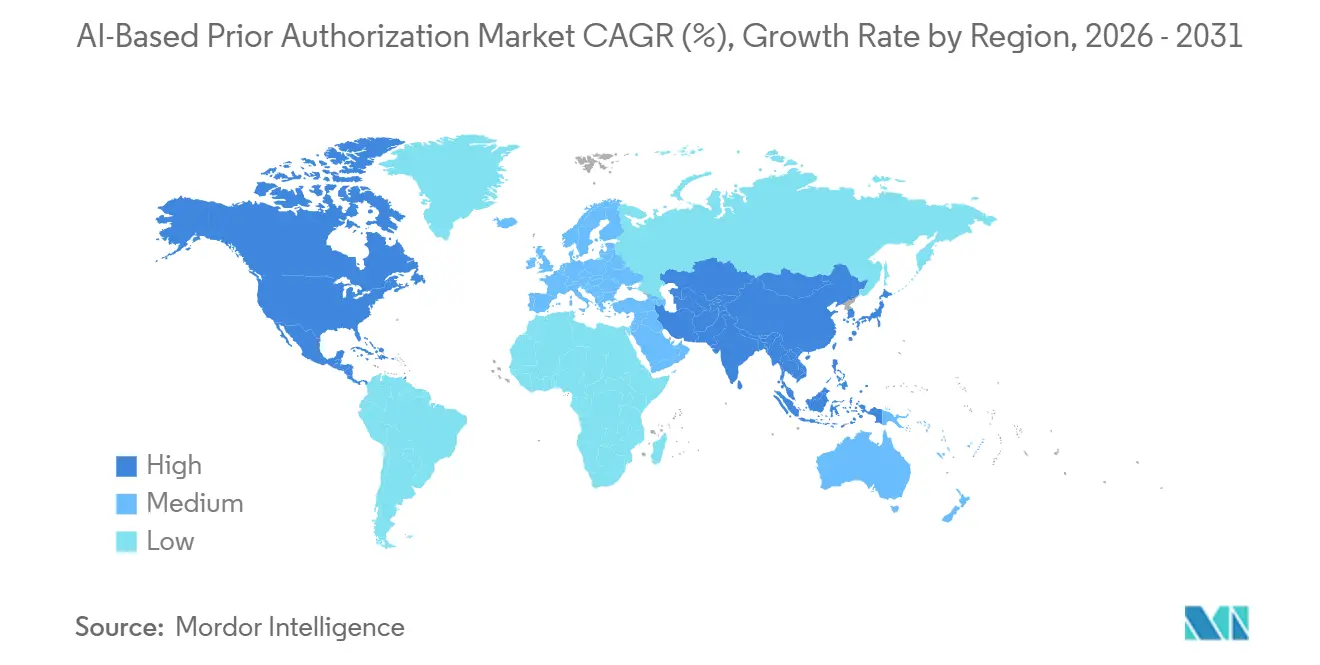

- By geography, North America held 52.23% of revenue in 2025, while Asia-Pacific recorded the highest projected CAGR at 21.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Prior Authorization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Payer Demand for Friction-Free Approvals | +3.2% | Global, with concentration in North America & EU | Short term (≤ 2 years) |

| CMS Interoperability Mandates (2026-2028) | +4.1% | North America (US core), spill-over to Canada | Short term (≤ 2 years) |

| Rapid EHR-Payer API Standardization (HL7 FHIR-Based) | +2.8% | North America & EU, with early gains in APAC | Medium term (2-4 years) |

| Cost-Containment Pressure Amid Value-Based Care Shift | +2.5% | Global | Medium term (2-4 years) |

| Emergence of GenAI Copilots for Prior-Auth Coding | +3.4% | North America, APAC core, spill-over to MEA | Medium term (2-4 years) |

| Specialty-Drug Benefit Design Complexity | +2.1% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In Payer Demand for Friction-Free Approvals

The AI-based prior authorization market is being lifted by the scale of waste tied to manual review, because CMS placed the administrative burden of prior authorization at USD 35 billion a year across the U.S. healthcare system and linked it to delays in 92% of reported care episodes.[1]Centers for Medicare & Medicaid Services, “Moving Prior Authorization into the 21st Century,” CMS Blog, cms.govCMS also noted that physicians spent an average of 13 hours a week on prior authorization work, which translated into 700 hours and USD 34,000 per provider each year that could otherwise support patient care. That burden is not disappearing, even when payers reduce low-value requirements, because the remaining requests are becoming more clinically dense and harder to process without automation. UnitedHealthcare stated in May 2026 that it would remove prior authorization requirements for 30% of remaining services by the end of 2026, which supports the view that simpler requests are being taken out while harder cases stay in the workflow. In the AI-based prior authorization market, that pattern shifts demand toward tools that can handle specialty drugs, oncology pathways, and rare disease documentation with fewer touches and better evidence matching rather than just higher transaction volume.

CMS Interoperability Mandates (2026-2028)

The AI-based prior authorization market is seeing its strongest near-term push from CMS-0057-F, which requires Medicare Advantage organizations, Medicaid and CHIP fee-for-service programs, Medicaid managed care plans, CHIP managed care entities, and Qualified Health Plan issuers on the Federally Facilitated Exchanges to meet faster decision timelines and build FHIR-based prior authorization APIs. The January 1, 2026 effective date for the new turnaround requirements has already changed procurement behavior, because delayed implementation now carries direct operational and reputational risk for covered entities. CMS then extended the pressure in April 2026 through proposed rule CMS-0062-P, which would bring drugs billed under both medical and pharmacy benefits into the electronic prior authorization framework and would make HL7 FHIR the HIPAA administrative standard for these transactions once finalized. The annual public reporting requirement for approval rates, denial rates, and average turnaround times adds another layer, because performance is no longer only an internal operations issue and becomes visible to regulators, providers, and competing plans. Within the AI-based prior authorization market, this combination of deadlines, standards, and transparency is pushing vendors and buyers toward faster deployment cycles and a stronger focus on automation that can hold up under audit.

Rapid EHR-Payer API Standardization (HL7 FHIR-Based)

The AI-based prior authorization market is also benefiting from steady HL7 FHIR standardization, because machine-readable documentation rules reduce the time spent gathering clinical records, checking payer criteria, and resubmitting incomplete requests. CMS has made this shift more concrete through the Prior Authorization Requirements, Documentation, and Decision API, which requires payers to expose documentation requirements and decision logic through a standardized interface rather than through portal-specific or fax-driven workflows. That changes the economics of automation, because once criteria libraries and endpoints become structured and reusable, the cost of adding the next automated pathway drops for both payers and technology vendors. It also changes product design inside the AI-based prior authorization market, where value now depends less on isolated workflow automation and more on how well a platform can sit between the EHR, the payer, and the clinician without losing context.

Cost-Containment Pressure Amid Value-Based Care Shift

The AI-based prior authorization market is gaining another layer of demand from value-based care, because providers that accept downside risk now need both faster authorizations for high-value care and tighter review logic for services that can raise avoidable costs. This creates a buyer group that was less active in earlier prior authorization software cycles, especially among integrated delivery networks, Medicare Advantage partners, and health systems managing capitated or shared-savings contracts. Healthcare providers are therefore moving up the demand curve inside the AI-based prior authorization market, because delays and denials now affect reimbursement timing, care progression, and total cost of care at the same time. CMS estimated that electronic prior authorization could generate USD 15 billion in administrative savings over 10 years, which keeps the economic case visible even when compliance spending rises in the short term. As a result, the AI-based prior authorization market is increasingly being framed not as an isolated IT purchase but as an operating model tool that can support margin protection, lower friction, and cleaner evidence exchange across risk-bearing workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Sharing Liability Concerns | -0.8% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Limited AI Training Datasets for Rare Specialties | -0.6% | Global | Long term (≥ 4 years) |

| Payer-Provider Trust Gap in Black-Box Models | -0.9% | Global | Medium term (2-4 years) |

| Fragmented State-Level Rule Variations | -0.7% | North America (US specifically) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sharing Liability Concerns

The AI-based prior authorization market faces a real brake from data-sharing risk, because broader API-based exchange increases the number of systems and vendors that touch protected health information during prior authorization workflows. KFF highlighted a core policy gap in 2025, noting that HIPAA applies to plans, providers, and clearinghouses, but not to every AI technology vendor that may gain access to health data through interoperable systems. KFF also found that 77% of the public was concerned about the privacy of personal health information shared with AI tools, which means adoption decisions are now shaped by trust as much as by productivity. The proposed federal framework is moving toward tighter inventory, logging, and contractual controls for AI systems that access electronic protected health information, but those requirements also raise deployment cost and slow procurement. In the AI-based prior authorization market, this restraint matters because buyers want faster automation, yet they also need stronger governance, clearer business associate structures, and a cleaner legal boundary for data use before scaling across large populations.[2]KFF, “Regulation of AI in Prior Authorization and Claims Review: A Look at Federal and State Consumer Protections,” KFF, kff.org

Payer-Provider Trust Gap in Black-Box Models

The AI-based prior authorization market is also constrained by a trust gap between payers and providers, because interoperability can expose clinical criteria while leaving the internal weighting and sequencing logic of the AI engine difficult to understand. AMA reported in 2025 that 61% of physicians were concerned that unregulated AI was increasing prior authorization denial rates by overriding clinical judgment, which shows that resistance is tied to care quality concerns rather than to general skepticism about automation. KFF reported that 75% of health plans used AI in prior authorization approvals, while 8% to 12% used it in denial decisions, a small share that still carries outsized scrutiny because adverse determinations are where reputational risk is highest. KFF also noted that 9 states, including California, Illinois, Texas, and Maryland, had enacted laws by April 2026 requiring human review, individual clinical circumstance assessment, or regulator audit authority over AI-driven determinations. A 2026 study in npj Digital Medicine found that poor oversight of AI in prior authorization was contributing to physician burnout, and 89% of surveyed physicians said prior authorization requirements worsened burnout. For the AI-based prior authorization market, these pressures do not stop adoption, but they do slow multi-state rollouts and raise the bar for explainability, auditability, and human-in-the-loop design.[3]Nature Publishing Group, “Medicare Advantage Becoming a Disadvantage with Use of Artificial Intelligence in Prior Authorization Review,” npj Digital Medicine, nature.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Closing the Gap as Compliance Complexity Rises

Software platform held 51.44% of revenue in 2025, giving it the leading position in the AI-based prior authorization market as large commercial payers and pharmacy benefit managers continued to favor licensed platforms that fit established utilization management teams. That lead reflected buying behavior built around scale, integration control, and the ability to configure clinical pathways inside long-standing payer operations. At the same time, services is projected to advance at a 19.67% CAGR through 2031, showing that the AI-based prior authorization market is shifting toward implementation support, workflow redesign, and governance-heavy delivery rather than software licensing alone. This pattern fits the current stage of the AI-based prior authorization industry, where compliance complexity is rising faster than many organizations can absorb through internal teams.

The services expansion is being reinforced by a practical gap in capabilities, because many mid-tier payers and administrators lack the staff needed to interpret new CMS rules, configure FHIR APIs, maintain criteria libraries, and document how automated decisions are governed. As a result, the AI-based prior authorization market size for services is rising as managed services, implementation support, model monitoring, and compliance reporting are bundled into longer recurring contracts around the core platform. GenAI copilots are adding to this effect, because organizations now need support for audit logs, de-identification controls, model testing, and business associate oversight before putting conversational or ambient tools into live clinical workflows.

By Deployment Mode: Cloud Leads on Both Share and Growth

Cloud-based deployment accounted for 55.76% of revenue in 2025, which made it the largest deployment model in the AI-based prior authorization market and showed that buyers are already moving beyond older on-premise utilization management stacks. Cloud is also projected to grow at a 20.17% CAGR through 2031, so the same model that leads today is also widening its position as new compliance and interoperability requirements take effect. This combination is unusual in a more mature software category, because top-share segments often slow first, yet the AI-based prior authorization market remains early enough in migration that cloud still has room to pull share from legacy environments. The deployment trend also reflects the operating needs of modern prior authorization programs, where transaction volumes shift with enrollment cycles, reporting requirements are continuous, and multi-entity connectivity cannot be handled efficiently through static local infrastructure.

On-premise deployments still matter for government buyers and integrated delivery networks with strict residency or control requirements, but even those organizations are moving toward hybrid models that separate core clinical storage from scalable inference and routing functions. In the AI-based prior authorization market, cloud architecture supports API uptime measurement, auditability, and payer-to-payer data exchange in ways that are harder to reproduce economically on premises. Waystar reinforced this direction in January 2026 when it introduced agentic AI capabilities through its AltitudeAI platform to combine clinical, financial, and administrative intelligence and generate stronger justification at submission.

By Application: Specialty Drugs Gaining Share as Medical Benefit Reforms Take Hold

Inpatient and outpatient procedures represented 47.55% of 2025 revenue, which made them the largest application segment in the AI-based prior authorization market because medical benefit claims still carry the greatest structural volume across commercial and Medicare Advantage plans. Advanced imaging, elective surgeries, infusion therapies, and procedure-linked medical necessity reviews continue to drive this leadership, since they sit at the center of payer utilization controls and provider reimbursement timing. Pharmacy and specialty drugs, however, are projected to grow at a 19.64% CAGR through 2031, making them the fastest-moving application area as treatment complexity rises across biologics, oncology, and high-cost chronic therapies. This makes the AI-based prior authorization market size for pharmacy and specialty drugs one of the clearest future expansion pools, especially as evidence requirements become more layered and less workable through manual channels.

Growth in this segment is being reinforced by benefit design complexity, because specialty therapies often require step edits, disease activity scores, prior treatment history, and payer-specific documentation that is difficult to assemble consistently under time pressure. Diagnostics and imaging approvals remain meaningful within the AI-based prior authorization market as well, particularly where payers are using clinical criteria libraries to automate appropriateness checks and shorten review cycles before a formal submission stalls care.

By End-User: Providers Accelerating Adoption Under Value-Based Risk

Healthcare payers held 49.64% of revenue in 2025, which gave them the largest buyer position in the AI-based prior authorization market because they remain the entities with direct utilization management responsibility and the clearest obligation to comply with CMS interoperability rules. Their lead also reflects existing spending power, existing integration footprints, and the operational need to manage approval volumes, denial logic, reporting, and audit response at scale. Healthcare providers are projected to grow at a 20.36% CAGR through 2031, which makes them the fastest-growing end-user group as value-based contracts and Medicare Advantage risk arrangements increase the financial cost of delayed or denied care. This is where the AI-based prior authorization market share is beginning to spread, because adoption is no longer limited to the decision-maker on the payer side and is expanding toward the submitting party that needs faster throughput and cleaner documentation.

Third-party administrators still occupy a meaningful place because they provide access to mid-market employer plans that do not always buy directly from platform vendors, yet they rarely carry the same level of technical and compliance capacity as large national plans. The AI-based prior authorization market is also becoming easier for providers to access because EHR-connected workflows reduce the need for separate portals and allow clinicians or staff to work inside systems they already use. That change matters because the provider side of the AI-based prior authorization market now values low-friction integration just as much as algorithmic performance, especially when authorization work competes with staffing shortages and burnout pressure.

Geography Analysis

North America held 52.23% of revenue in 2025, which gave it the leading regional position in the AI-based prior authorization market and reflected the unusually high administrative burden of the U.S. healthcare system. The region’s scale is tied to a mix of private insurance complexity, Medicare Advantage utilization controls, large provider network variation, and a regulatory calendar that turned prior authorization modernization into an urgent operating need rather than a discretionary upgrade. CMS-0057-F pushed that urgency further when the January 1, 2026 deadlines made turnaround times, denial specificity, and performance reporting active obligations for covered entities. The AI-based prior authorization market in North America is also being shaped by a second policy wave, because the April 2026 CMS-0062-P proposal would extend electronic prior authorization rules to drugs billed under both medical and pharmacy benefits and widen the universe of transactions subject to digital processing. Canada and Mexico remain smaller opportunities, but both sit within a regional environment where payers and public systems are under pressure to lower administrative drag and improve approval consistency.

Asia-Pacific is projected to grow at a 21.32% CAGR through 2031, which makes it the fastest-growing regional pocket in the AI-based prior authorization market even though it starts from a smaller base than North America. The regional growth case rests on digital health infrastructure build-out, expanding claims digitization, and the fact that several countries are now creating the policy and data conditions needed for workflow automation in reimbursement review. Japan offers one of the more structured regulatory pathways for adaptive health AI products, while India’s digital health push is widening the foundation for claims-linked automation as insurance penetration grows. The AI-based prior authorization market in Asia-Pacific is therefore being defined less by legacy replacement and more by the ability to build authorization workflows on top of newer digital health rails, which gives vendors room to shape process design earlier in the adoption cycle.

Europe and the Middle East & Africa show a more mixed pattern in the AI-based prior authorization market, because institutional interest in claims and workflow automation is rising while privacy and cross-border data rules remain stricter than in the United States. Europe has structurally similar approval and referral processes in several countries, but automation remains uneven and vendors must navigate tighter consent, governance, and secondary data use expectations when building scalable models. In the Middle East, GCC health systems are investing in claims management and broader digital transformation programs, which creates a longer-cycle opening for vendors with interoperable and compliance-ready platforms. South America remains more gradual, with Brazil and Argentina shaped by distinct public and private payer structures that can slow uniform rollout but still support targeted adoption where regulatory modernization improves claims workflow readiness. The AI-based prior authorization market across these regions is therefore expanding through uneven pathways, with policy clarity and data governance carrying more weight than pure technology readiness in determining adoption speed.

Competitive Landscape

The AI-based prior authorization market shows a moderately concentrated structure with a clear long tail, because a limited group of scaled platforms benefits from established payer and provider relationships while many smaller vendors compete through narrower specialty depth and workflow focus. Optum, Waystar, Cognizant through TriZetto, Surescripts, and Cohere Health are positioned near the center of the market conversation because existing integration footprints still matter more than feature breadth alone when buyers need fast deployment and lower switching friction. Even so, the AI-based prior authorization market is not tightly locked up by a few firms, since specialized vendors continue to compete on explainability, clinical criteria logic, and readiness for complex use cases that large platforms do not always address evenly. This keeps competitive intensity elevated and pushes product development toward workflow coverage rather than single-function automation.

Differentiation in the AI-based prior authorization market has moved beyond basic rules automation and now centers on how well a platform can generate clinical justification, map evidence to payer criteria, and fit into regulated data exchange. Waystar illustrated this shift in January 2026 when it launched agentic AI capabilities that used clinical, financial, and administrative data to support authorization workflows more proactively at the point of submission. UnitedHealthcare showed another type of strategic move in May 2026 when it announced plans to remove prior authorization requirements for 30% of remaining services by year-end, a decision that changes where automation value sits by taking simpler cases out and leaving harder cases in scope.

White space remains visible in several parts of the AI-based prior authorization market. Rare disease and ultra-orphan drug reviews are still underserved because low patient counts limit training depth and make automation less reliable than in high-volume claims categories. Pharmacy-benefit drug prior authorization remains another opening because much of that workflow still depends on manual communication even as federal policy moves toward standardized electronic exchange. TPA-focused tools also remain less mature, since many current products were designed for large payer environments and do not always fit the cost and workflow needs of self-insured employer plans served by administrators. The AI-based prior authorization market also carries higher diligence standards after AHA cited a Senate investigation that found meaningful increases in denial rates at some health plans alongside greater use of automated tools, which means buyers now ask harder questions about explainability, bias review, and governance before signing new contracts.

AI-Based Prior Authorization Industry Leaders

Optum

Availity

Cohere Health

Olive AI

PriorAuthNow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cognizant launched a headless API model that enables AI agents to directly interact with its TriZetto Unify payer-provider platform, with Electronic Prior Authorization becoming the first solution available through the framework. The initiative is designed to help payers prepare for the January 2027 FHIR API mandate and accelerate AI-driven prior authorization workflows.

- May 2026: Surescripts expanded its Prior Authorization Automation network to 68,000 prescribers across 42 health systems, representing a 50% increase since December 2025. The platform reported a median approval time of 18 seconds, supported 104 medications, and achieved a 34% automated approval rate for eligible medications.

- April 2026: The Centers for Medicare & Medicaid Services proposed extending electronic prior authorization requirements to drugs under both medical and pharmacy benefits for the first time, with an October 1, 2027 compliance target. The proposal elevates FHIR to HIPAA-mandated standard status for PA transactions and introduces mandatory API endpoint reporting to CMS.

Global AI-Based Prior Authorization Market Report Scope

According to the report’s scope, the AI-based prior authorization market refers to the industry focused on the use of artificial intelligence technologies to automate, streamline, and optimize the prior authorization process between healthcare providers, payers, and patients. These solutions leverage AI, machine learning, and predictive analytics to accelerate approval decisions, reduce administrative burden, improve accuracy, and enhance access to medically necessary treatments and services.

The AI-based prior authorization market is segmented into component, deployment mode, application, end-user, and geography. By component, the market is segmented into software platform and services. By deployment mode, the market is segmented into cloud-based and on-premise. By application, the market is segmented inpatient and outpatient procedures, pharmacy and specialty drugs, durable medical equipment, and diagnostics and imaging approvals. By end-user, the market is segmented into healthcare payers, healthcare providers, and third-party administrators (TPAs). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software Platform |

| Services |

| Cloud-Based |

| On-Premise |

| Inpatient and Outpatient Procedures |

| Pharmacy and Specialty Drugs |

| Durable Medical Equipment |

| Diagnostics and Imaging Approvals |

| Healthcare Payers |

| Healthcare Providers |

| Third-party Administrators (TPAs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platform | |

| Services | ||

| By Depolyment Mode | Cloud-Based | |

| On-Premise | ||

| By Application | Inpatient and Outpatient Procedures | |

| Pharmacy and Specialty Drugs | ||

| Durable Medical Equipment | ||

| Diagnostics and Imaging Approvals | ||

| By End-User | Healthcare Payers | |

| Healthcare Providers | ||

| Third-party Administrators (TPAs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI-based prior authorization through 2031?

Growth is being driven by federal interoperability rules, faster decision deadlines, stronger denial transparency, and the push to reduce administrative burden across payers and providers. The market is projected to rise from USD 1.74 billion in 2026 to USD 4.21 billion by 2031 at a 19.38% CAGR.

Why is North America leading adoption of AI-based prior authorization tools?

North America held 52.23% of revenue in 2025 because the U.S. system carries a high administrative burden and now faces active CMS compliance deadlines for turnaround times, reporting, and API-based exchange.

Which application area is expanding fastest?

Pharmacy and specialty drugs is the fastest-growing application at a 19.64% CAGR through 2031, helped by rising therapy complexity and the proposed extension of electronic prior authorization requirements to pharmacy-benefit drugs.

Why is cloud deployment outperforming on-premise systems?

Cloud held 55.76% share in 2025 and is growing at 20.17% because it is better suited for FHIR APIs, continuous compliance updates, uptime reporting, and cross-entity connectivity than legacy on-premise architectures.

Page last updated on: