AI-Based Nursing Assistant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 15.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Nursing Assistant Market Analysis by Mordor Intelligence

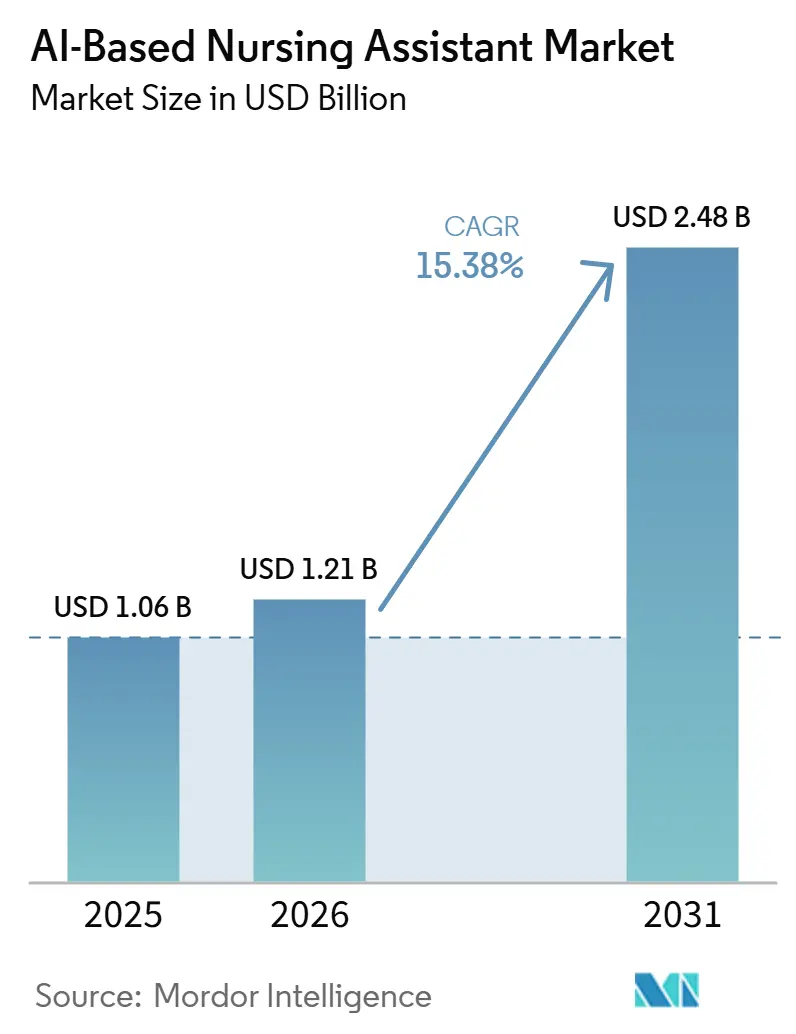

The AI-based nursing assistant market is expected to grow from USD 1.06 billion in 2025 to USD 1.21 billion in 2026 and is forecasted to reach USD 2.48 billion by 2031 at 15.38% CAGR over 2026-2031. The AI-based nursing assistant market is expanding because health systems are treating nursing automation as a response to a lasting labor shortage rather than as a narrow software upgrade, with the global nursing gap still measured in millions and workforce exits staying elevated in major care markets. The AI-based nursing assistant market is also gaining support from hospital demand to reduce documentation load, standardize handovers, and recover nursing time inside existing EHR workflows. Another growth layer comes from broader use of AI-enabled monitoring outside intensive care, where falls prevention, ward surveillance, and long-term observation are moving closer to baseline safety operations in understaffed settings. The AI-based nursing assistant market remains open across most use cases, but stronger compliance obligations and deeper EHR integration needs are raising the advantage of well-resourced vendors that can combine clinical utility with governance discipline. White space still remains visible in falls prevention workflows, rehabilitation settings, and multilingual patient interaction, which leaves room for new entrants even as platform competition becomes more intense.

Key Report Takeaways

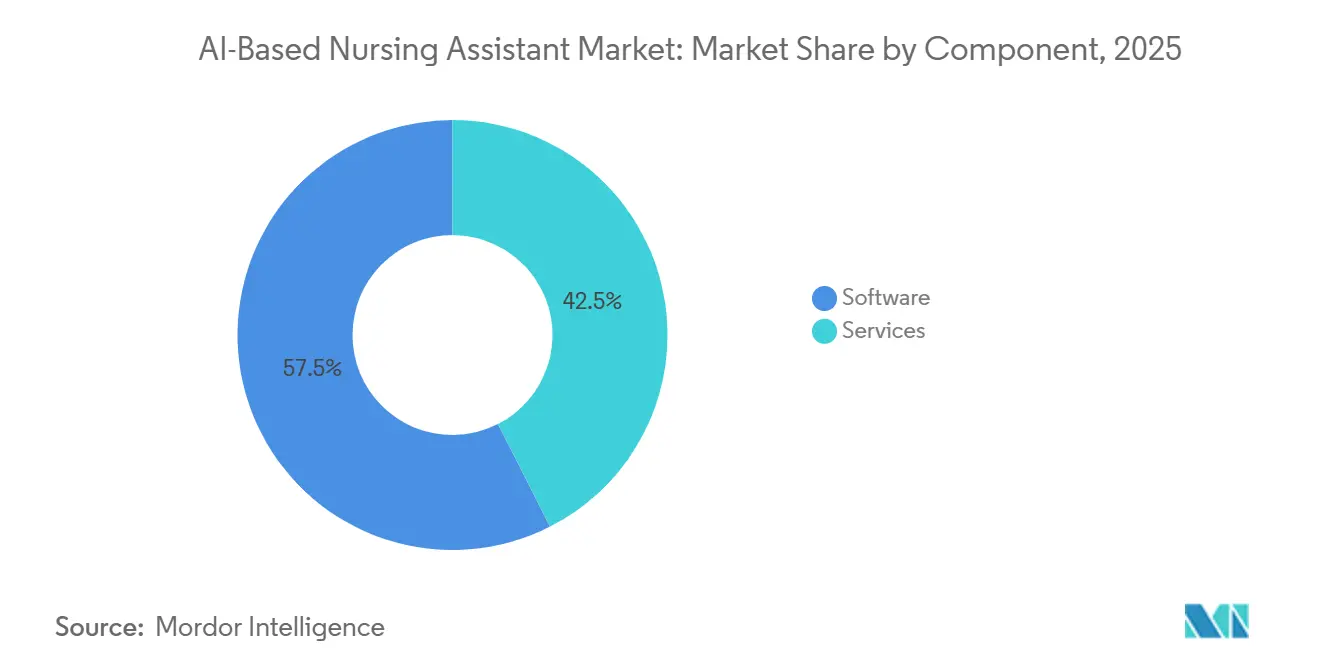

- By component, software held 57.47% of the AI-based nursing assistant market share in 2025, while services are projected to expand at a 15.59% CAGR through 2031.

- By deployment mode, cloud-based solutions led with a 48.38% share in 2025, while hybrid deployment is forecasted to grow at a 15.76% CAGR through 2031.

- By AI capability, natural language processing accounted for 40.26% of revenue in 2025, while speech recognition is expected to advance at a 16.18% CAGR through 2031.

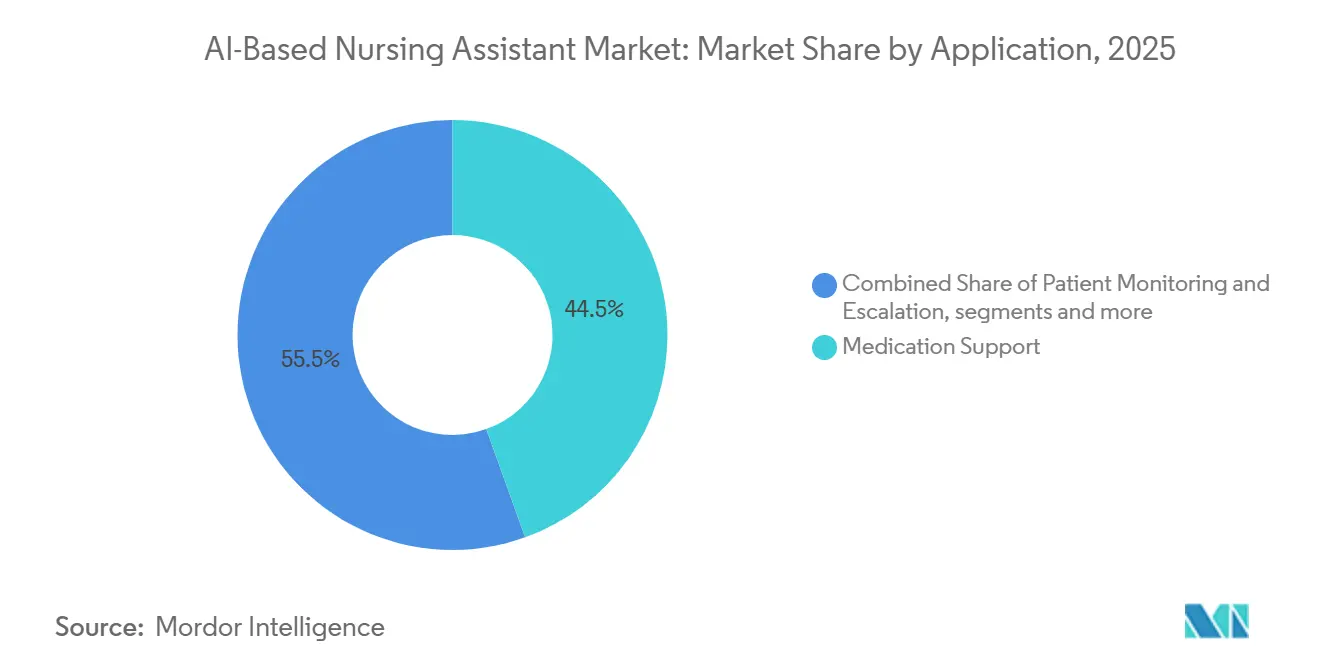

- By application, patient monitoring accounted for 44.51% of the AI-based nursing assistant market size in 2025, while medication support is projected to grow at a 17.22% CAGR through 2031.

- By end-user, hospitals and clinics represented 50.02% of demand in 2025, while long-term care facilities are expected to record a 16.42% CAGR through 2031.

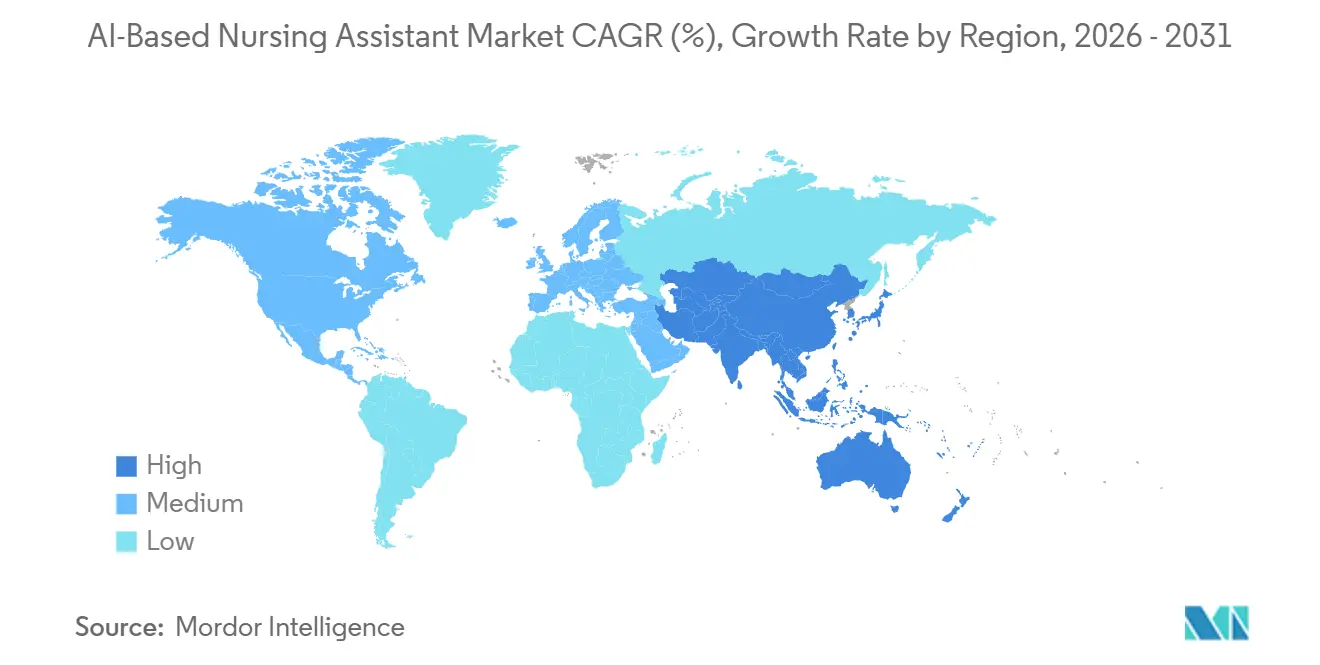

- By geography, North America held 43.41% share in 2025, while Asia-Pacific is forecasted to expand at an 18.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Nursing Assistant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Nursing Shortages and Care Delivery Bottlenecks | +3.5% | Global, acutest in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Need for Continuous Patient Monitoring and Escalation | +2.8% | Global, intensive deployment in North America and Asia-Pacific | Medium term (2-4 years) |

| Hospital Interest in Workflow Automation and Time Savings | +3.2% | North America and Europe, early gains spreading to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Home-Based and Remote Care Models | +2.5% | North America, Asia-Pacific, spillover to Western Europe | Long term (≥ 4 years) |

| Liability-Reduction Through Standardized Digital Triage | +1.9% | North America, emerging relevance in Europe | Medium term (2-4 years) |

| Under-Documented Demand from Night-Shift Coverage Gaps | +2.1% | North America, Europe, Japan, Australia; emerging signals in GCC and Singapore | Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Rising Nursing Shortages and Care Delivery Bottlenecks

The AI-based nursing assistant market continues to draw its strongest support from a labor gap that remains structurally difficult to close across both advanced and emerging healthcare systems. The World Health Organization reported a global nursing shortage of 5.8 million in 2023 and projected only a partial improvement to 4.1 million by 2030, with the burden still concentrated in regions that are also trying to expand care access and hospital capacity.[1]World Health Organization, “Nursing Workforce Grows, But Inequities Threaten Global Health Goals,” WHO News, who.int The National Council of State Boards of Nursing also found that more than 138,000 nurses left the workforce since 2022 and that nearly 40% of the remaining workforce intend to leave by 2029, which reinforces the pressure on hospitals to find alternatives that extend staff capacity without waiting for labor supply to normalize.[2]National Council of State Boards of Nursing, “National Nursing Workforce Study,” NCSBN, ncsbn.org In this setting, the AI-based nursing assistant market is being evaluated less as a convenience layer and more as a source of usable nursing time inside each shift. That is why providers are paying close attention to tools that can absorb education, discharge, and intake tasks that do not always need direct manual repetition from bedside staff.

Hospital Interest in Workflow Automation and Time Savings

The AI-based nursing assistant market is also being pushed forward by hospital demand to recover time now lost to charting, handovers, and repetitive administrative work. Microsoft stated in October 2025 that nurses can spend 25% to 41% of their shift on documentation and administrative tasks, which has made workflow improvement central to purchasing decisions rather than a side benefit. This pressure is changing procurement in the AI-based nursing assistant market from isolated pilots toward platform decisions tied to the broader EHR environment. Dragon Copilot for nurses, launched with Epic Rover integration, showed how ambient AI is moving into the core clinical stack rather than staying in a standalone application category. A 2026 JMIR study across three hospitals in Taiwan found that an LLM-based handover documentation system saved 474 to 981 nursing hours per month, which gave finance and operations teams a direct way to compare AI deployment with agency staffing and overtime costs.[3]JMIR, “Integrating a Large Language Model to Streamline Nursing Handover Documentation Across Multiple Hospitals in Taiwan,” Journal of Medical Internet Research, jmir.org As more of these gains are proven inside live hospital settings, the AI-based nursing assistant market is likely to favor vendors that can show measurable time recovery at enterprise scale instead of only offering narrow feature improvements.

Need for Continuous Patient Monitoring and Escalation

The AI-based nursing assistant market is widening because AI-supported monitoring is no longer limited to intensive care units and high-acuity beds. Health systems are extending monitoring use cases into general wards, long-term care facilities, and other settings where manual observation is harder to sustain with current staffing levels. A 2025 study in Frontiers in Digital Health found that the Verso Vision computer-vision system reduced accidental falls in hospitalized patients by 78% compared with standard care, which supports the case for AI as a practical safety layer rather than an experimental upgrade.[4]Frontiers in Digital Health, “Prevention of Falls in Hospitalized Patients, Evaluation of the Effectiveness of a Monitoring System Developed with Artificial Intelligence,” Frontiers in Digital Health, frontiersin.org The American Hospital Association also described health systems that are combining virtual nursing, fall prevention, documentation support, and remote patient oversight, which shows how monitoring is being folded into broader nursing workflow redesign rather than treated as a separate device category. This pattern matters for the AI-based nursing assistant market because it expands the number of beds, sites, and workflows that can justify adoption. It also shifts demand toward tools that can stay active continuously, surface actionable alerts, and support nurses before staffing strain turns into delayed response or preventable harm.

Expansion of Home-Based and Remote Care Models

The AI-based nursing assistant market is also gaining a new demand layer from care models that are moving away from traditional facilities and into patient homes. Axxess reported in January 2026 that 60% of care-at-home leaders expect AI to have the greatest sector impact by 2030, while fewer than 1 in 4 organizations had made AI-specific investments at that point, which signals an adoption gap with room to close. That gap matters because home-based care creates a different product requirement set than hospital deployment. Solutions in this part of the AI-based nursing assistant market need to work on lighter devices, tolerate inconsistent connectivity, and support clinical tasks without the tightly supervised environment that exists inside an inpatient unit. Those conditions tend to favor documentation tools, language interfaces, and voice-driven patient guidance ahead of more infrastructure-heavy formats. As policy and reimbursement continue to pull care outward from hospitals, vendors that can adapt nursing AI for lower-control environments are positioned to reach a broader but still underpenetrated part of the care continuum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Clinical Governance Concerns | -2.2% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Integration Friction with EHR and Nursing Workflows | -1.8% | Global, particularly fragmented in the Middle East and Africa, parts of Asia-Pacific, and South America | Medium term (2-4 years) |

| Reimbursement Uncertainty for AI-Augmented Nursing Services | -1.6% | North America and Europe | Medium term (2-4 years) |

| Limited Acceptance in High-Acuity and Safety-Critical Use Cases | -1.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Clinical Governance Concerns

The AI-based nursing assistant market faces a slower rollout path when solutions handle protected health information through ambient listening, chart summarization, or patient-facing voice interaction. These tools sit close to real clinical documentation and real patient communication, which raises the standard for auditability, governance, and accountability inside the procurement process. The American Nurses Association stated in 2025 that the ethical use of AI in nursing requires transparency, oversight, and an ongoing approach to governance because opaque systems are difficult to evaluate and supervise in practice. This slows the AI-based nursing assistant market because product value alone is not enough when hospitals also need clear policies for data handling, human review, and clinical accountability. It also creates a wider separation between vendors that treat compliance as a core product design principle and those that try to address governance after deployment. As regulation of clinical AI becomes more defined, buyers are likely to place greater weight on documentation controls, audit support, and traceability before scaling any nursing AI program.

Integration Friction with EHR and Nursing Workflows

The AI-based nursing assistant market also faces friction when new tools must connect to older healthcare IT environments that were not built for continuous AI-supported workflows. Most nursing AI applications need reliable two-way exchange with the EHR, and that requirement becomes harder to meet when hospitals are operating with mixed systems, uneven interfaces, or older application layers. This problem is especially relevant for smaller providers and more fragmented regional markets, where modernization budgets are limited and internal IT teams already have to balance security, maintenance, and reporting demands. It is one reason the AI-based nursing assistant market often moves faster inside large integrated delivery networks than inside providers with a patchwork of legacy systems. Until interoperability becomes less burdensome, deployment speed will continue to depend not only on clinical interest but also on how ready each provider is to connect AI into everyday nursing workflows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates, Services Revenue Scaling Fast

Software held 57.47% of AI-based nursing assistant market share in 2025, while services are projected to grow at a 15.59% CAGR through 2031. Software leads the AI-based nursing assistant market because documentation platforms, predictive analytics engines, and decision-support modules are the products that sit closest to daily nursing work. This lead also reflects the fact that many providers want capabilities that can plug into existing EHR workflows instead of adding a separate operating layer for staff to manage. The AI-based nursing assistant market is, therefore, still anchored by software value capture, especially where hospitals want immediate impact on charting time, handovers, and clinical coordination.

Providers are moving from one-time software procurement toward implementation support, change management, staff training, workflow redesign, and model tuning that stay active after go-live. This makes sense because nursing AI usually changes routines, documentation habits, and supervision structures rather than simply adding a new digital feature. As a result, service revenue is rising not because software is weakening, but because the AI-based nursing assistant market is moving from pilot activity into operational deployment that needs ongoing support.

By Deployment Mode: Cloud Leads, Hybrid Gains on Clinical Security Grounds

Cloud deployment held 48.38% of revenue in 2025, which keeps it at the center of the AI-based nursing assistant market because cloud systems support continuous model updates, lower upfront infrastructure demands, and easier scaling across multi-site provider networks. Cloud also fits well with health systems that have already moved large portions of their clinical data stack into modern hosted environments. This has made cloud the default starting point for many vendors competing in the AI-based nursing assistant market. At the same time, on-premises deployment still matters in systems with tighter data residency expectations or stricter internal control preferences. That ongoing relevance prevents the market from settling into a single infrastructure model.

Hybrid deployment is forecasted to grow at a 15.76% CAGR through 2031, which shows that speed and security needs are pushing the AI-based nursing assistant market toward blended architecture rather than pure cloud dependence. The reason is practical, because ambient listening, fall detection, and vital-sign alerting lose value if latency delays a clinically meaningful response. That gives edge processing and local inference a larger role in workflows that are time-sensitive and data-sensitive at the same time. That is why the AI-based nursing assistant market is likely to keep cloud in the lead while allowing hybrid models to gain faster traction where clinical responsiveness and privacy controls must be managed together.

By AI Capability: NLP Anchors Documentation, Speech Recognition Emerges as the Fastest Mover

Natural language processing accounted for 40.26% of revenue in 2025, which made it the largest capability area in the AI-based nursing assistant market. NLP holds that position because it supports the tasks that are already central to nursing work, including chart summarization, handover creation, record review, documentation support, and medication reconciliation prompts. This part of the AI-based nursing assistant market is relatively mature because vendors have spent years adapting language systems to clinical terminology and structured record environments. That maturity explains why NLP remains the default capability layer for products trying to show value quickly inside hospital workflows.

Speech recognition is projected to grow at a 16.2% CAGR through 2031, which reflects the operational reality that nurses often need to capture information while moving between patients and tasks. Predictive analytics and computer vision continue to serve narrower but high-value use cases such as deterioration scoring, fall surveillance, and pressure injury detection. The next step in the AI-based nursing assistant market may come from systems that combine language, speech, and task orchestration inside a single clinical environment, which is why Epic’s 2026 Agent Factory announcement drew attention as a sign that custom AI agents could become a larger part of nursing workflow design.

By Application: Patient Monitoring Anchors Revenue, Medication Support Sets the Pace for Growth

Patient monitoring and alert management held 44.51% of application revenue in 2025, which keeps it as the broadest use case in the AI-based nursing assistant market. This position comes from the fact that monitoring already sits close to established device infrastructure, safety protocols, and inpatient nursing routines. Hospitals can often connect AI monitoring more directly to known workflows than they can with newer forms of conversational or autonomous task support. That gives the AI-based nursing assistant market a stable application base in surveillance, escalation, and patient observation.

Medication support is forecasted to grow at a 17.22% CAGR through 2031, which makes it the fastest rising application in the AI-based nursing assistant market. The commercial logic is strong because medication errors carry high clinical risk and nurses still shoulder major verification and administration responsibilities. Across the AI-based nursing assistant market, documentation support is already embedded in most leading platforms, while virtual patient interaction remains earlier in commercialization outside established telehealth use cases.

By End User: Hospitals and Clinics Form the Core, Long-Term Care is the Key Growth Frontier

Hospitals and clinics accounted for 50.02% of demand in 2025, which made them the largest end-user base in the AI-based nursing assistant market. This lead reflects concentration of budget, EHR infrastructure, governance processes, and deployment support that larger provider organizations can bring to clinical AI programs. It also reflects the breadth of nursing tasks inside hospitals, where documentation, monitoring, patient education, medication workflows, and handovers all create room for automation or assistance.

Long-term care facilities are projected to expand at a 16.42% CAGR through 2031, which reflects stronger nurse-to-resident pressure and high need for continuous observation in elder care. This makes long-term care the most important growth frontier in the AI-based nursing assistant market after hospitals. Home healthcare providers also represent a meaningful growth path as aging populations, documentation burden, and distributed care delivery create a clearer return case for lighter AI tools. Ambulatory care and rehabilitation centers remain smaller within the AI-based nursing assistant market, but they still matter because medication adherence, episodic patient interaction, and progress tracking create targeted use cases that vendors have not fully covered.

Geography Analysis

North America held 43.41% of AI-based nursing assistant market share in 2025, while Asia-Pacific is forecasted to grow at an 18.43% CAGR through 2031. North America leads the AI-based nursing assistant market because it combines acute nurse staffing pressure with mature EHR ecosystems and a provider base willing to operationalize AI inside standard workflows. The United States remains the center of this regional position, supported by documented workforce strain and faster movement from evaluation into active deployment. Microsoft’s work with Mercy hospitals on Dragon Copilot and Suki’s October 2025 nursing consortium with health systems on Epic, MEDITECH, and Oracle Health showed that the AI-based nursing assistant market in North America is moving toward enterprise commitment rather than isolated trials. Canada and Mexico are also participating in the AI-based nursing assistant market, though adoption remains more measured because governance and EHR fragmentation create a slower path to scale.

Europe remains the second-largest regional cluster in the AI-based nursing assistant market, with activity concentrated in markets such as Germany, the United Kingdom, and France. The region’s progress is tied to digital infrastructure improvement and a gradual move from experimentation toward structured clinical AI strategy. NHS Grampian’s partnership with Corti in 2025 also showed that the AI-based nursing assistant market is gaining traction in public health settings that have traditionally moved more cautiously on commercial AI tools.

Asia-Pacific is the fastest-growing region in the AI-based nursing assistant market because hospital digitization is accelerating across China, Japan, South Korea, and India. The region is attractive because providers are expanding digital infrastructure while also facing staffing strain, aging populations, and pressure to improve clinical throughput. The Middle East and Africa remain earlier in development, with Gulf markets showing the clearest institutional budget support while other areas still face infrastructure gaps. South America is also earlier in the AI-based nursing assistant market, with demand centered in major urban providers and private hospital groups as EHR modernization gradually improves the base for wider deployment.

Competitive Landscape

The AI-based nursing assistant market is moderately fragmented, with competition spread across EHR-native vendors, dedicated documentation specialists, and patient-interaction AI developers. Epic and Oracle Health sit in a strong position because health systems already rely on their enterprise platforms and prefer to limit workflow disruption when adding new clinical tools. That creates an advantage in the AI-based nursing assistant market for vendors that can extend existing contracts into new AI functions rather than asking providers to add an entirely separate platform. The AI-based nursing assistant market therefore still rewards integration depth as much as product novelty.

Dedicated specialists remain important because they move faster in targeted workflows and can focus product design more directly on nursing use cases. Hippocratic AI also tried to separate itself in the AI-based nursing assistant market by positioning Polaris 5.0 around clinical accuracy, HIPAA compliance, and patient interaction quality, which shifted competition toward trust and governance as well as automation performance.

White space remains visible in falls prevention workflows that go beyond early alerts, multilingual virtual patient interaction, and rehabilitation-focused nursing support. Those gaps matter because the AI-based nursing assistant market still lacks a single vendor with broad dominance across every major use case. Smaller players can therefore gain traction by proving measurable value in one workflow before expanding into adjacent categories. At the same time, larger platform vendors are widening their reach quickly, which means the AI-based nursing assistant market is likely to become more competitive before it becomes more consolidated. Buyers are increasingly looking for clear nurse-time savings, dependable integration, and strong governance, which keeps the competitive field active across both incumbents and newer specialists.

AI-Based Nursing Assistant Industry Leaders

Microsoft Corporation

Suki AI, Inc.

Oracle

IBM

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hippocratic AI launched Nurse Co-Pilot and AI Front Door, two first-of-kind voice AI products co-developed with Cincinnati Children's Hospital Medical Center, OhioHealth, and Cleveland Clinic. Nurse Co-Pilot automates inpatient workflows including admission education, discharge preparation, and medication adherence, returning an estimated 1 to 4 hours per nurse per shift.

- April 2026: Ambience Healthcare launched Chart Chat for Nursing, the first EHR-integrated conversational AI tool for inpatient nursing, with Cleveland Clinic as the inaugural pilot site. The tool enables nurses to ask plain-language questions about patient charts, pulling from physician progress notes, hospital policy, and recent labs in real time.

- April 2026: Hippocratic AI launched Polaris 5.0, a 5-trillion-parameter constellation healthcare AI model benchmarked against Claude, GPT, and Gemini on clinical accuracy, HIPAA compliance, and empathy in patient interaction. New clinical skills include contextual ASR, cough detection, drug safety protocols, and clinical escalation pathways.

Global AI-Based Nursing Assistant Market Report Scope

According to the report’s scope, the AI‑based nursing assistant is a virtual healthcare tool that uses artificial intelligence to support nurses by automating routine tasks, providing clinical decision support, enabling patient monitoring, and assisting with documentation. It improves efficiency, reduces workload, and enhances patient care through intelligent, nursing‑specific applications.

The AI‑based nursing assistant market is segmented into component, deployment mode, AI capability, application, end-user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based, on-premises, and hybrid. By AI capability, the market is segmented into natural language processing, predictive analytics, computer vision, speech recognition, and other AI capabilities. By application, the market is segmented into medication support, patient monitoring and escalation, virtual patient interaction, falls and safety management, and documentation assistance. By end-user, the market is segmented into hospitals and clinics, long-term care facilities, home healthcare providers, ambulatory care centers, and rehabilitation centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Natural Language Processing |

| Predictive Analytics |

| Computer Vision |

| Speech Recognition |

| Other AI Capabilities |

| Medication Support |

| Patient Monitoring and Escalation |

| Virtual Patient Interaction |

| Falls and Safety Management |

| Documentation Assistance |

| Hospitals and Clinics |

| Long-Term Care Facilities |

| Home Healthcare Providers |

| Ambulatory Care Centers |

| Rehabilitation Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By AI Capability | Natural Language Processing | |

| Predictive Analytics | ||

| Computer Vision | ||

| Speech Recognition | ||

| Other AI Capabilities | ||

| By Application | Medication Support | |

| Patient Monitoring and Escalation | ||

| Virtual Patient Interaction | ||

| Falls and Safety Management | ||

| Documentation Assistance | ||

| By End-User | Hospitals and Clinics | |

| Long-Term Care Facilities | ||

| Home Healthcare Providers | ||

| Ambulatory Care Centers | ||

| Rehabilitation Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI-based nursing assistant solutions through 2031?

Growth is driven by persistent nurse shortages, stronger hospital focus on documentation efficiency, and wider use of AI monitoring across inpatient and long-term care settings. The overall value is projected to rise from USD 1.06 billion in 2025 to USD 1.21 billion in 2026 to USD 2.48 billion by 2031 at a 15.38% CAGR.

Which component leads revenue in 2025?

Software leads revenue with a 57.47% share in 2025 because documentation, decision support, and predictive tools are the most established use cases in provider workflows.

Which application is growing the fastest?

Medication support is the expected to be the fastest-growing application, with a projected 17.22% CAGR through 2031, supported by hospital interest in safer and more automated medication workflows.

Which end-user group offers the largest demand base?

Hospitals and clinics account for 50.02% of demand in 2025 because they have the budgets, governance structures, and EHR environments needed for enterprise deployment.

Page last updated on: