AI-Based Care Coordination Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

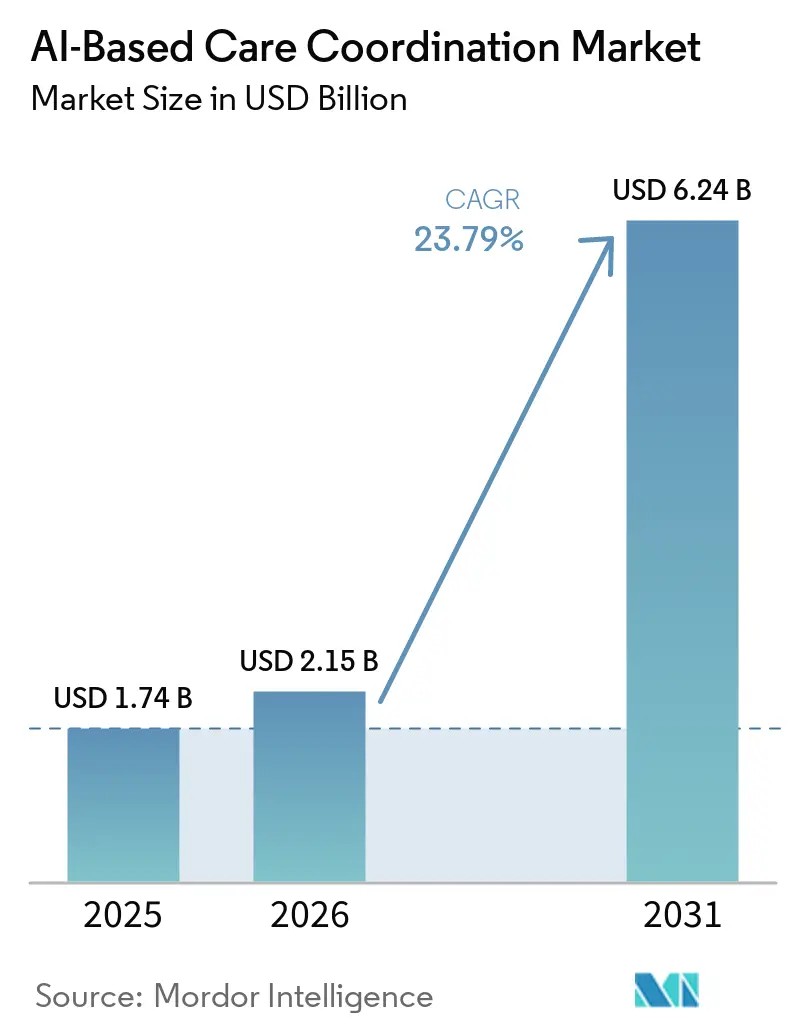

| Market Size (2026) | USD 2.15 Billion |

| Market Size (2031) | USD 6.24 Billion |

| Growth Rate (2026 - 2031) | 23.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Care Coordination Market Analysis by Mordor Intelligence

The AI-Based Care Coordination Market size is projected to expand from USD 1.74 billion in 2025 and USD 2.15 billion in 2026 to USD 6.24 billion by 2031, registering a CAGR of 23.79% between 2026 to 2031.

Growth in the AI-based care coordination market is being shaped by three forces that are reinforcing one another, wider interoperability requirements, a stronger move toward value-based care, and AI tools that now support multi-step coordination work with less manual follow-up. The CMS Interoperability and Prior Authorization final rule has pushed payer and provider workflows toward FHIR-based connectivity, which supports more automated coordination across authorizations, referrals, and care transitions. TEFCA moved from nearly 10 million health records exchanged in January 2025 to nearly 500 million by February 2026, which materially expanded the usable data base for AI-based care coordination market platforms that depend on broader longitudinal records. The commercial center of demand is also moving toward cloud delivery and broader integration, because buyers increasingly want platforms that can coordinate across hospitals, post-acute providers, payers, and community networks rather than optimize a single workflow. Competitive intensity remains moderate, with scale advantages in EHR-embedded platforms and population health suites, while newer growth is shifting toward SDoH coordination, discharge orchestration, and HIE or QHIN-linked models that can operate across fragmented care networks.

Key Report Takeaways

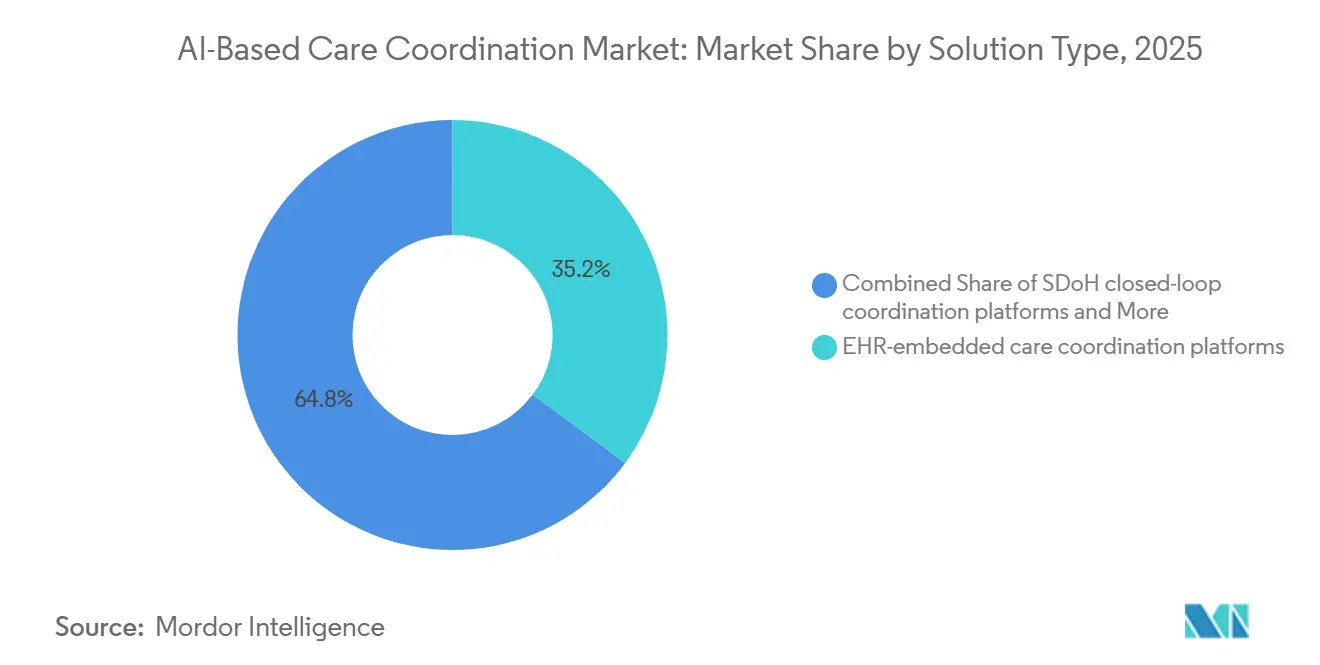

- By solution type, EHR-embedded care coordination platforms held 35.16% of the AI-based care coordination market share in 2025, while SDoH closed-loop coordination platforms are projected to expand at 24.88% CAGR through 2031.

- By care setting, hospitals and health systems accounted for 46.17% of the AI-based care coordination market size in 2025, while home health and hospital-at-home is forecast to grow at 24.12% CAGR through 2031.

- By deployment model, cloud or SaaS captured 65.29% of the AI-based care coordination market size in 2025 and is also the fastest-growing deployment model at 25.19% CAGR through 2031.

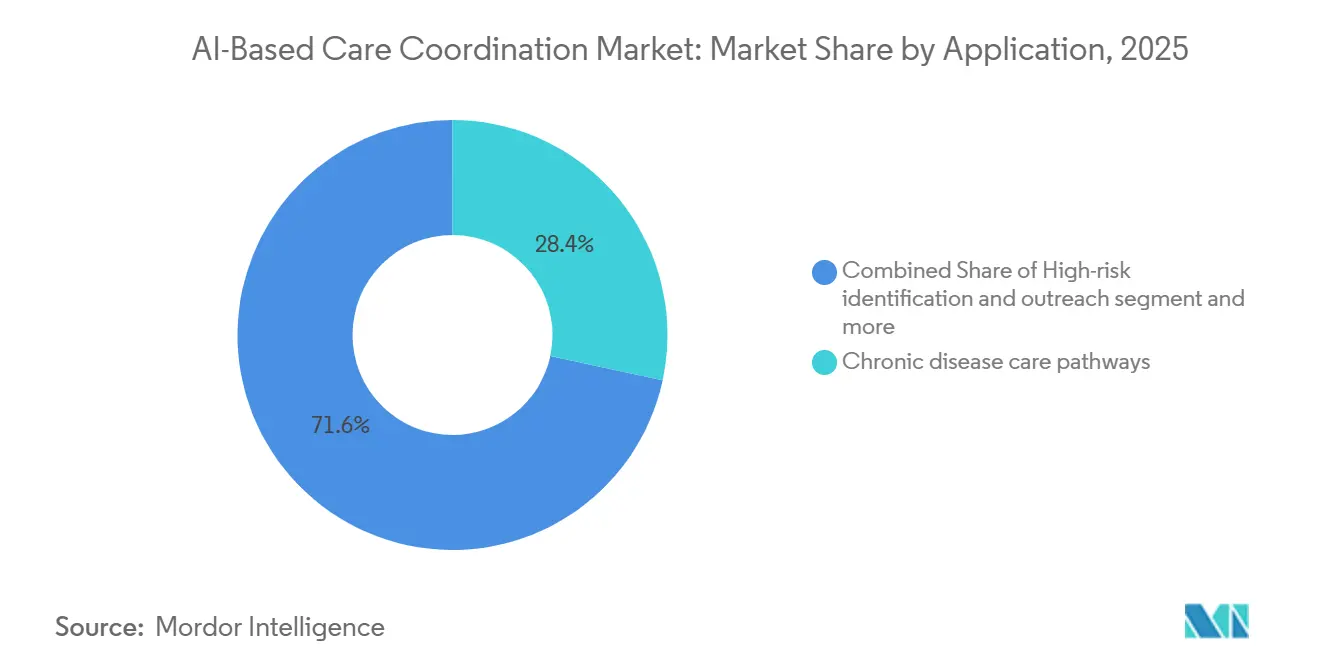

- By application, chronic disease care pathways led with 28.37% share in 2025, while transitions of care and discharge coordination is projected to rise at 26.33% CAGR through 2031.

- By AI technique, predictive analytics and risk stratification held 32.77% share in 2025, while workflow automation, RPA, and agentic AI is forecast to advance at 25.48% CAGR through 2031.

- By integration approach, EHR-integrated solutions held 61.44% share in 2025, while the HIE or QHIN-integrated model is projected to expand at 27.11% CAGR through 2031.

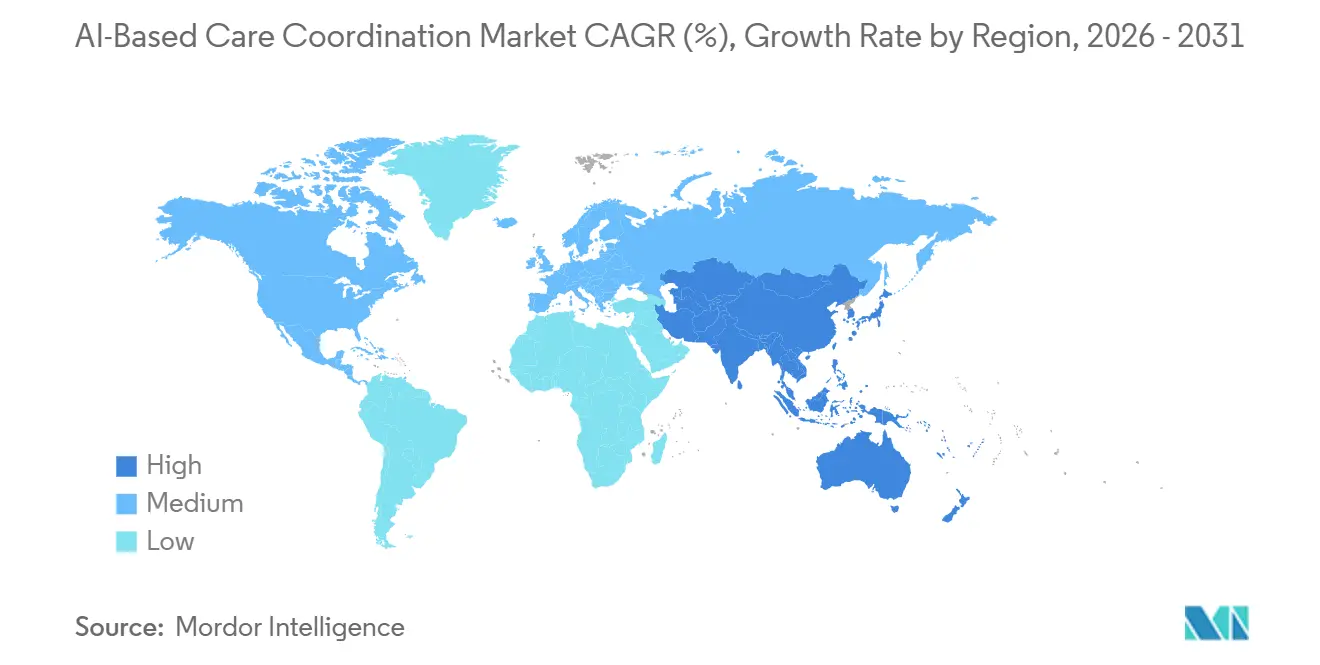

- By geography, North America held 43.18% of the AI-based care coordination market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 27.36% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Care Coordination Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift To Value-Based Care And ACO Models | +3.5% | Global, dominant in North America | Medium term (2-4 years) |

| CMS-0057-F Interoperability Mandate | +4.2% | North America, especially payers, MA plans, and Medicaid | Short term (≤ 2 years) |

| Cloud-First Architectures For AI Coordination | +2.8% | Global, with highest density in North America and Asia-Pacific | Long term (≥ 4 years) |

| TEFCA QHIN-To-QHIN FHIR Exchange | +3.1% | North America, with spillover to FHIR adopters in Asia-Pacific | Medium term (2-4 years) |

| AI-Driven Patient Flow And Discharge Orchestration | +3.6% | North America and Western Europe, with early adoption in Asia-Pacific | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift To Value-Based Care And ACO Models Elevates Analytics-Driven Workflows

The move from fee-for-service reimbursement toward value-based contracting continues to create a direct operating need for the AI-based care coordination market, because success under shared-risk models depends on earlier outreach, tighter follow-up, and fewer avoidable gaps in care. The State and Science of Value-based Care 2025 study found that 50% of surveyed organizations were actively investing in data analytics and AI, while 65% expressed optimism about AI's predictive value in value-based arrangements.

Medicare Shared Savings Program ACOs using AI-enhanced analytics reported 40% higher shared savings distributions, which supports the case that better coordination performance can fund additional technology spending. That pattern matters because the AI-based care coordination market is no longer being bought only as software, it is being evaluated as an operating lever that can improve medical cost control and quality performance under risk contracts. As more ACOs and related provider groups seek repeatable gains in utilization management, discharge planning, and chronic disease follow-up, the commercial pull for automation becomes stronger. The result is a self-reinforcing cycle in which organizations with better coordination tools can post better contract performance, defend their economics, and widen the gap with providers still dependent on manual care management models.

CMS-0057-F Interoperability Mandate Catalyzes API-First Coordination Architectures

The CMS Interoperability and Prior Authorization final rule has accelerated the move toward API-first workflow design in the AI-based care coordination market, because it turns interoperability from a planning goal into a dated compliance requirement. CMS finalized the rule on January 17, 2024, with a January 1, 2026 deadline for certain prior authorization response timelines and a January 1, 2027 deadline for the related FHIR API requirements covering provider access, payer-to-payer exchange, and prior authorization. ONC also tied related interoperability work to lower administrative burden, noting projected savings of USD 19.2 billion over the coming decade from electronic prior authorization standards.

Once provider systems can retrieve more complete payer-side history through standardized interfaces, AI coordination tools can compress work that previously required separate payer portals, manual history checks, and repeated staff follow-up. That change makes the AI-based care coordination market more attractive to health systems and payers that need administrative simplification at scale, especially in referral, authorization, and pre-visit preparation workflows. It also favors vendors that were built for structured data exchange and flexible orchestration rather than those relying on closed interfaces and local custom integrations.

TEFCA QHIN-To-QHIN FHIR Exchange Accelerates Cross-Network Coordination

TEFCA has shifted from a governance concept to an operating data network, and that shift is becoming a meaningful growth driver for the AI-based care coordination market. HHS reported that TEFCA reached nearly 500 million health records exchanged by February 2026, up from nearly 10 million in January 2025, which sharply increased the scale of available cross-network data exchange. The Sequoia Project's FHIR Roadmap also placed QHIN-to-QHIN FHIR exchange infrastructure deployment in 2026, with end-to-end exchange work and pilots moving forward in the same period[1]The Sequoia Project, “FHIR Roadmap for TEFCA Exchange Version 2.0,” The Sequoia Project, sequoiaproject.org.

For the AI-based care coordination market, the practical value lies in broader patient context, because cross-network treatment queries can support more complete risk scoring, cleaner transitions, and better referral routing than isolated EHR views. This changes how procurement teams assess platform value, since integration breadth and event visibility become more important when organizations want coordination tools that work across hospitals, community providers, and post-acute partners. Vendors aligned to TEFCA and QHIN-based data movement therefore gain an advantage in settings where buyers want fewer blind spots at points of handoff.

AI-Driven Patient Flow And Discharge Orchestration Unlocks System Capacity

Discharge planning and patient flow have become one of the clearest operating use cases for the AI-based care coordination market, because these workflows sit directly at the intersection of bed capacity, readmission risk, and post-acute placement speed. The Acute Hospital Care at Home waiver was extended through 2030, and by March 2026 the program covered 366 approved programs across 139 health systems in 37 states, which widened the need for stronger discharge and transition coordination beyond the hospital walls. The same AMA coverage also highlighted Marshfield Clinic's hospital-at-home results, including a 44% reduction in readmissions and a 35% drop in average length of stay, which points to the operational value of better coordinated step-down care.

WellSky expanded its AI activity in post-acute referral intake and in long-term care, skilled nursing, and home health documentation workflows during 2026, which shows that automation demand is spreading across discharge-linked settings rather than staying inside acute hospitals. That widening use case matters because the AI-based care coordination market is being evaluated not only by care management leaders, but also by operating teams that want faster placement, shorter stays, and fewer handoff failures. As a result, discharge orchestration is becoming one of the fastest commercial entry points for vendors that can tie clinical readiness, capacity visibility, and referral execution into one workflow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy, Security, And Integration Complexity | -2.1% | Global, most acute in North America and Europe | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Implementation And Change-Management Costs | -1.8% | Global, with the highest burden in mid-market health systems | Medium term (2-4 years) |

| EU AI Act High-Risk Obligations | -1.4% | European Union member states, with spillover to global vendors serving Europe | Medium term (2-4 years) to Long term (≥ 4 years) |

| Uneven Cross-Network Eventing Until TEFCA FHIR Matures | -1.2% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Security, And Integration Complexity Slow AI Deployment

The AI-based care coordination market still faces a basic deployment challenge, because the same broad data access that improves coordination also widens the operational burden around privacy, consent, identity resolution, and interface reliability. These platforms need to ingest and normalize information from EHRs, payer systems, HIEs, remote monitoring streams, and community resource networks, and each source often carries a different data model and governance expectation. The State and Science of Value-based Care 2025 study found that 69% of surveyed respondents cited regulatory complexities as a primary reason for slower adoption, which shows that the issue extends well beyond technical interface work alone[2]National Association of ACOs and Innovaccer, “The State and Science of Value-based Care 2025,” NAACOS, naacos.com.

Federal TEFCA rulemaking and related interoperability activity continue to expand exchange pathways, but they also make trust, routing, and data-handling practices more visible to buyers that are assessing enterprise AI coordination deployments. Large health systems can usually absorb more of this integration effort through internal digital teams, but smaller providers often struggle to support the same level of data engineering, consent management, and workflow redesign. That imbalance slows broader adoption of the AI-based care coordination market, especially in mid-sized networks, community settings, and rural organizations that need the benefit but have fewer deployment resources.

High Implementation And Change-Management Costs Challenge ROI Realization

The AI-based care coordination market is also restrained by the distance between technical capability and realized workflow value, because implementation requires organizations to redesign daily processes rather than simply install new software. Even when interoperability standards reduce connection work, providers still need to decide who acts on AI suggestions, how exceptions are routed, and what metrics define success across clinical and administrative teams. Company activity in 2025 and 2026 shows that vendors are trying to reduce this burden by cutting integration time and packaging more of the orchestration layer into the platform itself.

Innovaccer stated in January 2026 that its Snowflake partnership reduced data integration timelines by nearly 30% and lowered infrastructure costs by 20% to 25% for joint customers, which shows why buyers are rewarding vendors that reduce deployment friction. Even so, the AI-based care coordination market still demands substantial local change management, because care managers, physicians, utilization teams, and discharge staff must trust and use the recommendations in live workflows. That is why adoption continues to move fastest in large systems and sponsored programs that can justify up-front transformation work across multiple service lines and sites of care.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: SDoH Platforms Accelerating as Social Risk Becomes a Quality Metric

EHR-embedded care coordination platforms led the solution landscape in 2025 with a 35.16% share, which reflected the advantage of staying inside the core workflow already used by clinicians and care managers. In the AI-based care coordination market, that installed-base position matters because switching between systems still slows documentation, follow-up, and exception handling. Care management suites for population health continued to hold an important secondary position, especially where organizations wanted a broader longitudinal view across attributed populations. Referral and network management tools also remained relevant, because post-acute and external handoffs still sit among the least digitized parts of the care journey. Standalone and other solution types continued to attract investment where providers wanted focused functionality without a full suite replacement.

The fastest-growing solution segment is SDoH closed-loop coordination platforms, which are projected to grow at 24.88% CAGR through 2031 as social needs closure becomes more visible in quality and population health workflows. This part of the AI-based care coordination industry is gaining traction because buyers now want evidence that referrals to community-based organizations were completed, tracked, and tied back to patient follow-up. Innovaccer announced in November 2025 a statewide partnership with the PopHealth Learning Center to support care coordination for 2 million Medi-Cal patients across 200 clinics, which illustrates how publicly sponsored programs are pushing broader SDoH-linked deployment. That policy and program pressure is changing the mix of demand inside the AI-based care coordination market, because buyers are no longer treating social screening as sufficient on its own. They are instead looking for auditable closed-loop processes that connect clinical teams, social services, and reporting requirements in one operating chain.

By Care Setting: Post-Acute and Home Health Disrupting Hospital-Centric Workflows

Hospitals and health systems held 46.17% share in 2025, which gave them the leading position across care settings because they control large technology budgets and manage the most complex patients. That scale gives hospital buyers an early advantage in the AI-based care coordination market, since they can spread deployment costs across care management, utilization review, discharge planning, and population health programs. Ambulatory and physician group settings still matter, but their buying patterns are more fragmented and often depend on narrower use cases or shared infrastructure. Post-acute and long-term care settings remained smaller in current share terms, yet they carry some of the highest coordination pain points in day-to-day operations. Other care settings also remained part of the demand mix where local network coordination gaps were large.

Home health and hospital-at-home is projected to record the fastest CAGR at 24.12% through 2031, which shows how quickly coordination demand is moving beyond the traditional inpatient campus. The hospital-at-home waiver extension through 2030 and the spread of approved programs across 139 health systems support that shift by making distributed acute care a more durable operating model rather than a temporary experiment. WellSky stated in February 2026 that its SkySense AI expansion into long-term care and skilled nursing could reduce documentation time by up to 50% in home health workflows, which signals stronger automation demand in post-acute settings. In practical terms, the AI-based care coordination market is moving toward the places where follow-up failures are common and staffing pressure is persistent. That makes home-based and post-acute care a natural growth area, even while hospitals continue to hold the largest current spending base.

By Deployment Model: Cloud/SaaS Dominates and Widens Its Lead

Cloud or SaaS accounted for 65.29% share in 2025, which made it the clear leader among deployment models and gave it the broadest installed footprint. That position reflects a structural reality in the AI-based care coordination market, because continuous scoring, summarization, and workflow execution require computing elasticity that many local environments do not support well. Hybrid deployments still held a role for organizations that needed to keep sensitive identifiers under tighter local governance while still using cloud-based intelligence layers. On-premises systems remained present in high-security or legacy-heavy environments, especially where migration cycles were slow or governance rules were strict. Even so, the direction of demand continued to move toward centralized and managed deployment models that could scale across settings and counterparties.

Cloud or SaaS is also the fastest-growing deployment model, with the AI-based care coordination market size for this segment projected to expand at 25.19% CAGR through 2031. Innovaccer said in January 2026 that its Gravity platform and Snowflake partnership reduced integration timelines by nearly 30% and lowered infrastructure costs by 20% to 25% for joint customers, which supports the argument that cloud design is becoming a cost and speed advantage rather than only a technical choice. Procurement teams are also increasingly treating enterprise security certifications as the basic floor for cloud adoption, which helps established vendors with stronger operating maturity. For the AI-based care coordination market, that means cloud leadership is being reinforced by both technical necessity and buyer preference for faster deployment. It also weakens the long-term case for heavily customized on-premises architectures in workflows that depend on cross-network data movement and real-time orchestration.

By Application: Transitions of Care Outpacing Chronic Disease Management in Growth

Chronic disease care pathways held 28.37% share in 2025 and remained the largest application category because they align closely with mature value-based care programs and long-standing quality measures. In the AI-based care coordination market, this segment benefits from predictable outreach cycles, recurring risk stratification, and measurable quality reporting across diabetes, hypertension, and heart failure populations. High-risk identification and outreach also remained important, especially where payer and provider organizations needed earlier intervention for members with rising utilization risk. Prior authorization and utilization management coordination formed another meaningful part of the application mix, since these tasks connect directly to access, throughput, and administrative burden. SDoH referrals and related closed-loop activity continued to expand alongside equity-oriented care management models.

Transitions of care and discharge coordination is projected to grow at 26.33% CAGR through 2031, making it the fastest-growing application area in the AI-based care coordination market. The hospital-at-home extension and the spread of approved programs across multiple states have made discharge planning and post-acute routing more central to system performance. The same logic is visible in WellSky's March 2026 referral intake expansion, which was designed to streamline hospital-to-post-acute placement across a large national footprint. Buyers are therefore prioritizing applications that can reduce avoidable handoff failures at a predictable point in the patient journey. That is why discharge coordination is growing faster than chronic disease management even though chronic care remains the largest established spending category today.

By AI Technique: Agentic AI Overtaking Predictive Analytics as the Defining Capability

Predictive analytics and risk stratification led the AI technique mix with 32.77% share in 2025, reflecting the long period over which these tools have been used in population health and ACO settings. In the AI-based care coordination market, that legacy matters because risk models are already embedded in outreach planning, utilization review, and gap-in-care management. NLP and information extraction also remained important, especially for summarization and documentation-heavy workflows that need structured outputs from unstructured notes. Recommender systems and computer vision maintained narrower but still useful roles in specific operational settings. The current mix therefore still reflects the earlier era of AI adoption, which focused more on guidance and less on direct task execution.

Workflow automation, RPA, and agentic AI is projected to grow at 25.48% CAGR through 2031, making it the fastest-growing AI technique in the AI-based care coordination industry. UiPath launched healthcare-focused agentic AI solutions in February 2026 for medical record summarization, claim denial prevention, and prior authorization workflows, which illustrates how vendors are packaging task execution rather than only analytics. This shift is important for the AI-based care coordination market because buyers increasingly want visible labor savings in repetitive multi-step workflows that already have defined process rules. As a result, the center of product differentiation is moving from insight generation toward reliable action, orchestration, and exception handling. Predictive models remain essential, but they are increasingly being treated as one layer within a broader automation stack rather than the final product.

By Integration Approach: QHIN-Integrated Architecture Winning the Speed-of-Data Race

EHR-integrated solutions dominated the integration approach mix with 61.44% share in 2025, which reflected the deep reach of large clinical system vendors across hospital and ambulatory environments. That position remains important in the AI-based care coordination market because native workflow placement lowers training friction and keeps decision support close to the clinical record. Standalone open-API approaches also held a place, particularly for smaller practices and specialty vendors that wanted flexibility without full network membership. These models benefited from broader FHIR adoption, but they still depended on the quality and completeness of the upstream data available to them. As a result, integration depth continued to shape how much value a platform could create in live coordination workflows.

The HIE or QHIN-integrated approach is projected to grow at 27.11% CAGR through 2031, making it the fastest-growing integration vector in the AI-based care coordination market. The Sequoia Project's TEFCA FHIR Roadmap placed QHIN-to-QHIN exchange infrastructure deployment in 2026, which supports the case that broader network-based connectivity is moving closer to operational reality. HHS reporting on TEFCA's exchange volume growth reinforces the same point, since the value of coordination software rises when more patient context is available across organizational boundaries. This is why the AI-based care coordination market size for QHIN-linked models is rising faster than EHR-only approaches, even though EHR integration still leads on current share. Buyers are rewarding architectures that can reduce blind spots across post-acute care, behavioral health, community services, and multi-provider networks.

Geography Analysis

North America held 43.18% share in 2025, which kept it as the largest regional block in the AI-based care coordination market. That lead is tied to a stronger regulatory and operating framework, because CMS interoperability deadlines, TEFCA network development, and value-based care adoption are moving in the same direction. The United States also has the densest concentration of scaled vendors, which helps convert product development into live contracts across payer and provider organizations. Within North America, the AI-based care coordination market benefits from a buyer base that is already familiar with risk-based care, utilization controls, and interoperability spending. Canada and Mexico remain at earlier stages, with some digital health foundation in place but less direct policy pressure than in the United States.

Europe presents a different operating profile for the AI-based care coordination market because compliance design plays a larger role in how systems are brought to market and scaled. Official European guidance on the interaction between the AI Act and MDR or IVDR shows why many care coordination tools tied to clinical decision or regulated workflows face heavier oversight requirements[3]Joint Artificial Intelligence Board and Medical Device Coordination Group, “Interplay Between MDR/IVDR and the Artificial Intelligence Act,” European Commission Health, health.europa.eu. France published a national strategy for AI and health data in July 2025, and CNSA also released its 2025-2026 roadmap for AI in autonomy and care coordination, which points to active public-sector support in targeted areas. Germany's applied activity is also visible through Fraunhofer ITWM's ViKI pro work in AI-based care planning for long-term care settings, which shows that the regional opportunity extends beyond hospitals and into broader care delivery models. The region therefore offers real demand, but that demand is filtered through stronger governance, more formal conformity expectations, and closer attention to how tools are classified and supervised.

Asia-Pacific is the fastest-growing region and is projected to expand at 27.36% CAGR through 2031, which gives it the strongest forward growth profile in the AI-based care coordination market. Growth in this region is being supported by aging populations, more active public digital health programs, and a willingness in several countries to use AI as part of system modernization. India published its Strategy for Artificial Intelligence in Healthcare in February 2026 and identified care coordination among the priority use cases, which supports longer-term deployment potential where digital public infrastructure is expanding. Japan is also moving forward, and Fujitsu Japan announced in March 2026 a joint proof of concept with Teikyo University Hospital focused on referred-patient management and data analysis, which shows concrete interest in AI-assisted coordination workflows. Outside the 3 leading regions, the Middle East and Africa and South America remain earlier-stage demand pockets, with activity concentrated in selective smart hospital and digital health programs rather than broad-based adoption.

Competitive Landscape

The AI-based care coordination market is moderately fragmented, with stronger scale in EHR-embedded and population health categories and a much looser structure in SDoH coordination, post-acute transitions, and specialty workflow automation. Epic Systems and Oracle Health remain important anchors in EHR-linked coordination because their installed bases create workflow depth and switching friction inside hospitals and physician organizations. That said, the AI-based care coordination market still leaves room for specialized vendors when cross-network coordination, payer-provider exchange, or community resource routing matters more than deep control inside a single EHR. This is why the competitive field remains broader than it first appears from hospital procurement cycles alone. The practical dividing line is no longer just feature count, but whether a platform can combine data access, workflow execution, and measurable outcomes across more than one care setting.

Innovaccer has been one of the clearest examples of this broader positioning strategy in the AI-based care coordination market. The company announced a statewide partnership in California in November 2025 covering 2 million Medi-Cal patients across 200 clinics, which strengthened its standing in publicly sponsored population health and social care coordination. It also announced a Snowflake partnership in January 2026 and a Databricks validated partner milestone in March 2026, both aimed at operationalizing enterprise AI across healthcare data environments. These moves show how vendors are trying to own more of the operating stack, from data unification to workflow execution, instead of staying in a narrow application lane.

WellSky and UiPath illustrate 2 other competitive patterns shaping the AI-based care coordination market. WellSky expanded AI in long-term care and skilled nursing in February 2026, then broadened post-acute referral intake in March 2026, which reinforced its position around discharge-linked coordination and downstream placement workflows. UiPath launched dedicated healthcare agentic AI solutions in February 2026, which signaled a stronger push from workflow automation vendors into clinical-adjacent administrative bottlenecks such as records summarization and prior authorization. Competition is therefore widening from both sides, incumbent healthcare platforms are extending their reach, while automation and data-platform players are moving into care coordination use cases. That keeps the AI-based care coordination market open to innovation, but it also raises the bar for vendors that cannot prove integration depth, workflow reliability, or a clear economic case across multiple stakeholders.

AI-Based Care Coordination Industry Leaders

Innovaccer

Epic Systems

Oracle Health (Cerner)

Health Catalyst (Lumeon & Twistle)

WellSky (CarePort)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Innovaccer announced a USD 250 million investment over three years in its Gravity Autonomous Healthcare Platform. The goal is to enhance AI capabilities in prior authorization, utilization management, care management, and revenue cycle processes. With clients like Kaiser Permanente, Ascension, and Trinity Health, this move highlights Innovaccer's plan to compete with major EHR providers.

- April 2026: Hippocratic AI introduced two Voice AI products to transform healthcare delivery. AI Front Door replaces fragmented call centers and digital interfaces with a single, always-available AI health agent, ensuring seamless patient care. Nurse Co-Pilot, co-developed with Cincinnati Children's Hospital Medical Center, OhioHealth, and Cleveland Clinic, is designed to save inpatient nurses 1-4 hours per shift.

Global AI-Based Care Coordination Market Report Scope

As per the scope of the report, AI-based care coordination refers to the use of artificial intelligence technologies to organize, manage, and optimize patient care across multiple healthcare providers and settings. It involves leveraging AI algorithms, machine learning, and data analytics to improve communication, streamline workflows, ensure timely interventions, and personalize treatment plans, ultimately enhancing patient outcomes and healthcare efficiency.

The segmentation for the AI-based care coordination market is categorized by solution type, care setting, deployment model, application, AI technique, integration approach, and geography. By solution type, the market includes care coordination platforms embedded in EHRs, population health and care management suites, orchestration of patient flow and discharge, management of referrals and networks including post-acute transitions, closed-loop coordination platforms addressing Social Determinants of Health (SDoH), and other solutions. By care setting, it covers hospitals and health systems, ambulatory groups, physician practices and clinics, post-acute and long-term care settings including skilled nursing facilities (SNF), rehabilitation, and home health, home health services and hospital-at-home models, and other care settings. By deployment model, the segmentation includes cloud-based and Software as a Service (SaaS), on-premises solutions, and hybrid models.

By application, it includes pathways for chronic disease care, care transitions, discharge and post-acute coordination, identification and outreach for high-risk patients, coordination for prior authorization and utilization management, referrals and closed-loop coordination for Social Determinants of Health (SDoH), and other applications. By AI technique, the market is segmented into predictive analytics and risk stratification methods, Natural Language Processing (NLP) for information extraction and summarization, workflow automation, Robotic Process Automation (RPA), and agentic AI, recommender systems and determining the next best action, and computer vision applications and remote monitoring. By integration approach, it includes integration with Electronic Health Records (EHR), integration with Health Information Exchanges (HIE) and Qualified Health Information Networks (QHIN), and standalone solutions with open Application Programming Interfaces (APIs). By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| EHR-embedded care coordination platforms |

| Care management suites (population health / care management) |

| Patient flow & discharge orchestration |

| Referral & network management (including post-acute transitions) |

| SDoH closed-loop coordination platforms |

| Others |

| Hospitals & health systems |

| Ambulatory/physician groups & clinics |

| Post-acute & long-term care (SNF, rehab, home health) |

| Home health & hospital-at-home |

| Others |

| Cloud / SaaS |

| On-premises |

| Hybrid |

| Chronic disease care pathways |

| Transitions of care / discharge & post-acute coordination |

| High-risk identification & outreach |

| Prior authorization & utilization management coordination |

| SDoH referrals & closed-loop coordination |

| Others |

| Predictive analytics & risk stratification |

| NLP & information extraction/summarization |

| Workflow automation, RPA & agentic AI |

| Recommender systems / next best action |

| Computer vision & remote monitoring |

| EHR-integrated |

| HIE/QHIN-integrated |

| Standalone with open APIs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | EHR-embedded care coordination platforms | |

| Care management suites (population health / care management) | ||

| Patient flow & discharge orchestration | ||

| Referral & network management (including post-acute transitions) | ||

| SDoH closed-loop coordination platforms | ||

| Others | ||

| By Care Setting | Hospitals & health systems | |

| Ambulatory/physician groups & clinics | ||

| Post-acute & long-term care (SNF, rehab, home health) | ||

| Home health & hospital-at-home | ||

| Others | ||

| By Deployment Model | Cloud / SaaS | |

| On-premises | ||

| Hybrid | ||

| By Application | Chronic disease care pathways | |

| Transitions of care / discharge & post-acute coordination | ||

| High-risk identification & outreach | ||

| Prior authorization & utilization management coordination | ||

| SDoH referrals & closed-loop coordination | ||

| Others | ||

| By AI Technique | Predictive analytics & risk stratification | |

| NLP & information extraction/summarization | ||

| Workflow automation, RPA & agentic AI | ||

| Recommender systems / next best action | ||

| Computer vision & remote monitoring | ||

| By Integration Approach | EHR-integrated | |

| HIE/QHIN-integrated | ||

| Standalone with open APIs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the AI-based care coordination market by 2031?

The AI-based care coordination market is projected to reach USD 6.24 billion by 2031, up from USD 2.15 billion in 2026.

What is driving growth in AI-based care coordination platforms?

Growth is being supported by interoperability mandates, wider value-based care adoption, TEFCA expansion, and stronger demand for automation in discharge, referral, and authorization workflows.

Which solution type currently leads adoption?

EHR-embedded care coordination platforms led the market in 2025 with a 35.16% share because they fit directly into existing hospital workflows.

Which application is growing the fastest through 2031?

Transitions of care and discharge coordination is the fastest-growing application, with a projected 26.33% CAGR through 2031.

Why does cloud deployment dominate this space?

Cloud or SaaS held 65.29% share in 2025 and is also the fastest-growing model because AI coordination requires scalable computing and broader cross-network connectivity.

Which region has the strongest future growth outlook?

Asia-Pacific has the fastest outlook, with a projected 27.36% CAGR through 2031, supported by public digital health initiatives and expanding AI adoption in healthcare workflows.

Page last updated on: