Agent Of Record (AOR) For Contractors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

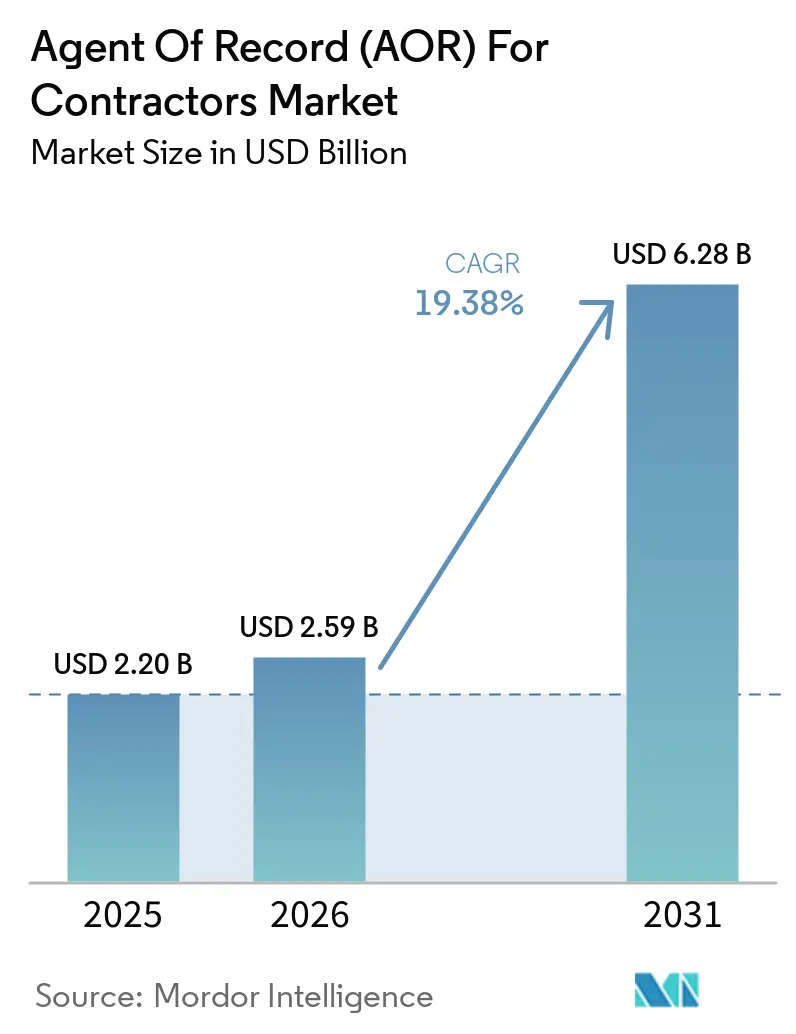

| Market Size (2026) | USD 2.59 Billion |

| Market Size (2031) | USD 6.28 Billion |

| Growth Rate (2026 - 2031) | 19.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agent Of Record (AOR) For Contractors Market Analysis by Mordor Intelligence

The Agent of Record (AOR) for contractors market is expected to grow from USD 2.20 billion in 2025 to USD 2.59 billion in 2026, and is forecast to reach USD 6.28 billion by 2031 at a 19.38% CAGR over 2026-2031. The Agent of Record (AOR) for contractors market is expanding faster than many adjacent workforce technology categories because enterprises now treat contractor compliance as a legal and operational need, not only a payment task. Cross-border hiring is pushing buyers into jurisdictions where local contractor rules, tax treatment, and documentation standards vary sharply, which raises demand for platforms that can stand between the enterprise and the contractor. Tightening enforcement on worker classification and permanent establishment risk is also moving AOR adoption from optional coverage to a formal part of global talent infrastructure. At the same time, country-level e-invoicing rules are making contractor payment workflows more structured, thereby increasing the value of platforms that combine onboarding, tax, invoicing, and payment in a single system. Competition is becoming more intense as larger workforce platforms bundle AOR services with adjacent offerings, while providers with stronger local legal depth and broader workflow coverage still have room to win larger enterprise programs.

Key Report Takeaways

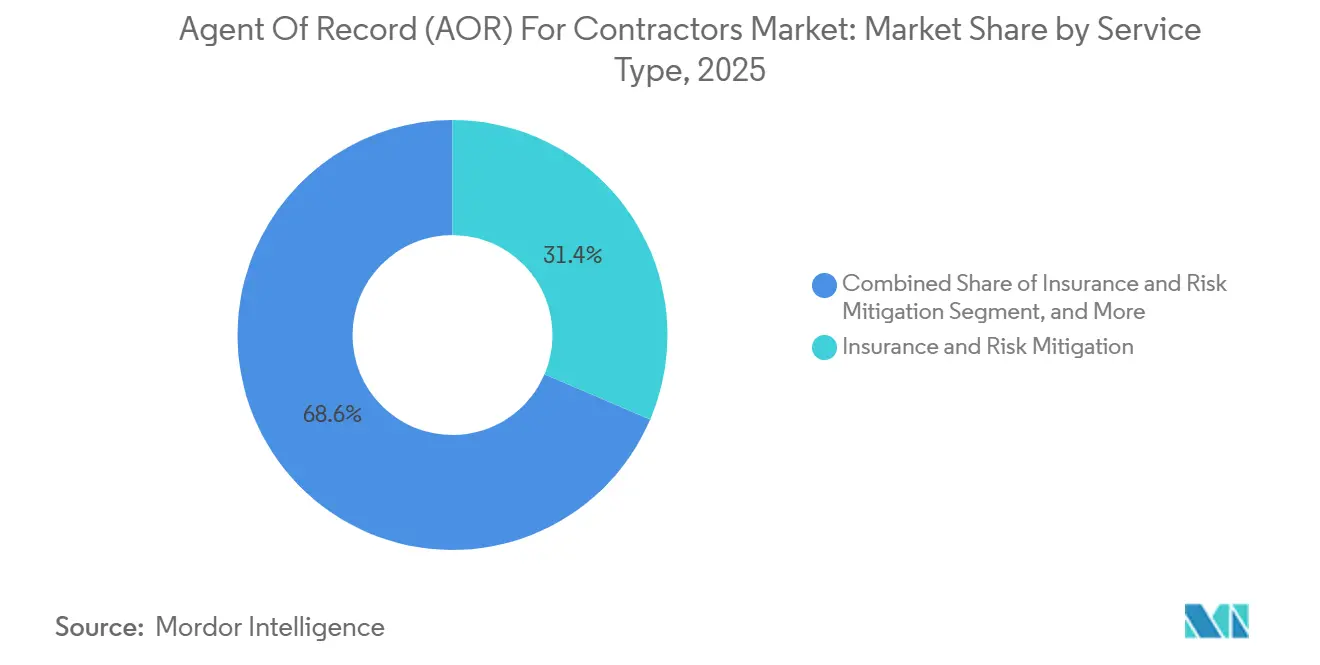

- By service type, Insurance, Liability, and Risk Mitigation led with 31.42% revenue share in 2025, while Contractor Onboarding and Contract Administration are projected to expand at a 21.47% CAGR through 2031 in the agent of record (AOR) for contractors market.

- By end-user enterprise size, SMEs accounted for 58.27% of revenue in 2025, while Large Enterprises are projected to record the highest CAGR of 22.63% through 2031.

- By deployment model, cloud-based deployment accounted for 63.88% of the market in 2025, while hybrid deployment is projected to grow at a 20.19% CAGR through 2031.

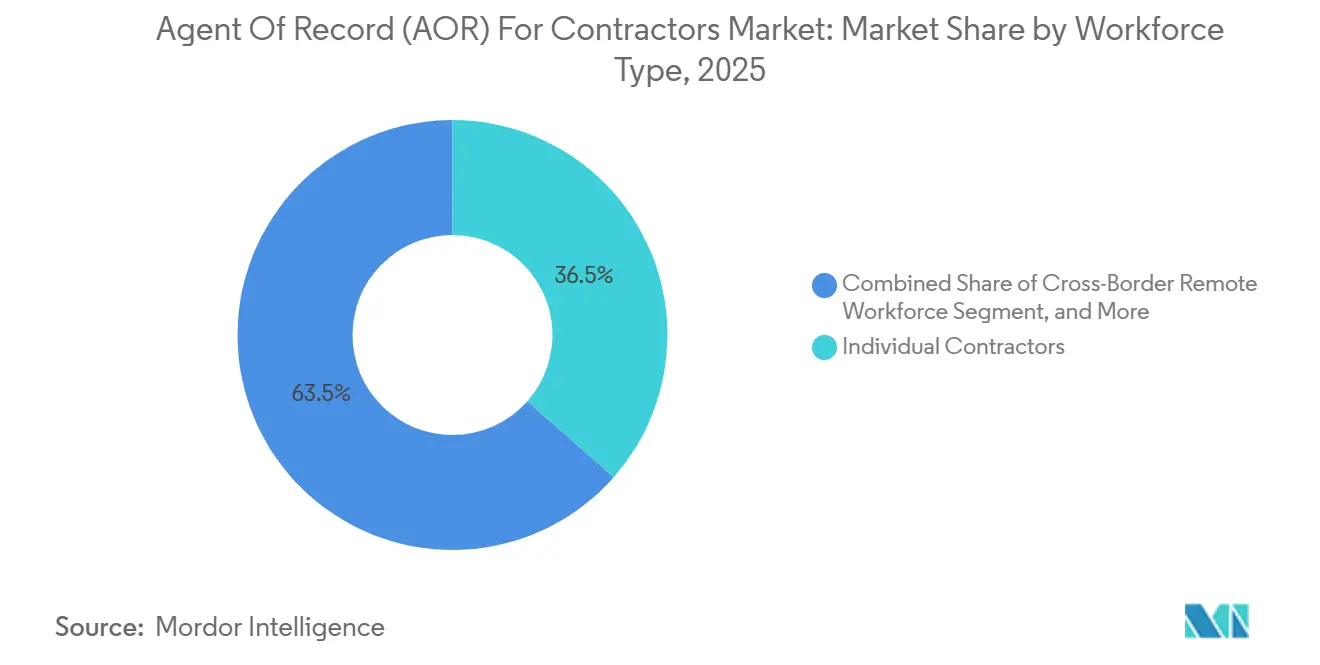

- By workforce type, Independent Contractors and Freelancers held 36.51% share in 2025, while Cross-border Contractors are projected to expand at a 23.14% CAGR through 2031.

- By end-user industry, Information Technology and Telecom accounted for 24.73% share in 2025, while BFSI is projected to grow at a 19.89% CAGR through 2031.

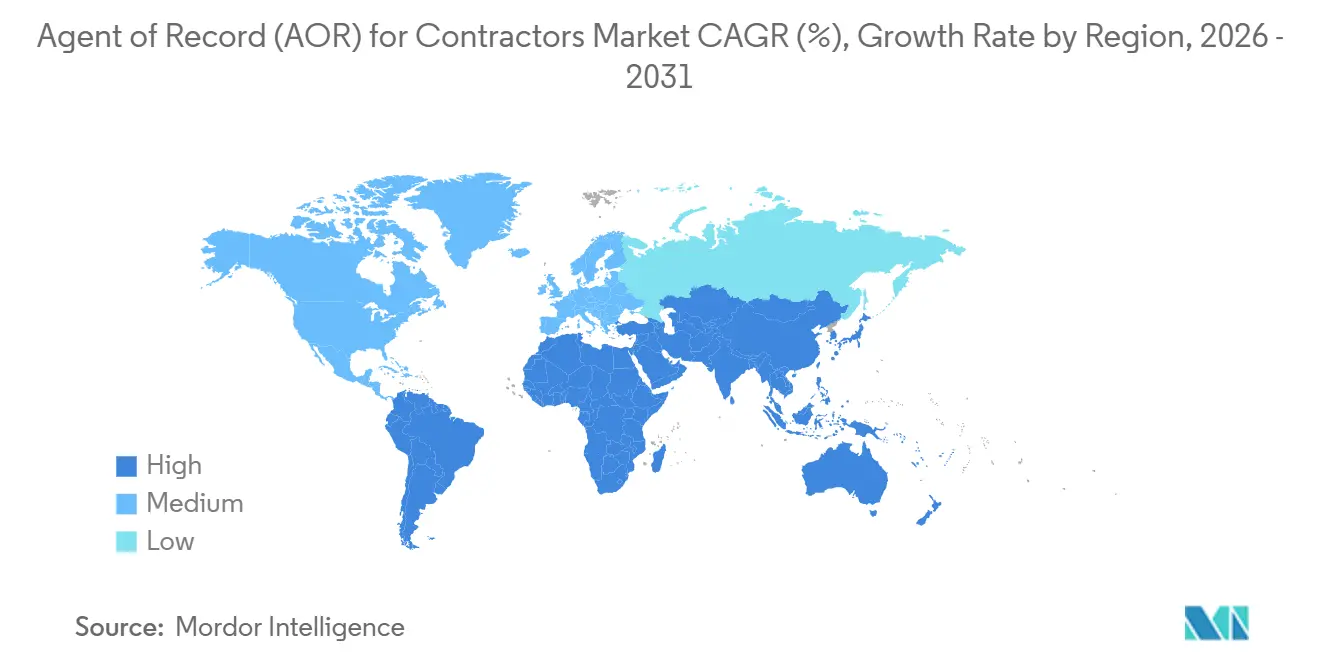

- By geography, North America held 47.19% of the Agent of Record (AOR) for Contractors market share in 2025, while Asia-Pacific is projected to expand at a 24.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agent Of Record (AOR) For Contractors Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cross-Border Remote Contractor Hiring | +5.2% | Global, concentrated in North America, APAC, and EU | Short term (≤ 2 years) |

| Tighter Worker Misclassification Enforcement | +4.1% | North America and EU core, spill-over to APAC | Short term (≤ 2 years) |

| Enterprise Shift Toward Blended Workforce Models | +3.3% | Global | Medium term (2-4 years) |

| Demand for Unified Contractor Onboarding, Tax, and Payment Workflows | +2.8% | Global, early traction in North America and EU | Medium term (2-4 years) |

| OECD Permanent Establishment Monitoring for Borderless Workforces | +1.9% | Global, particularly OECD member states | Long term (≥ 4 years) |

| Country-Level E-Invoicing and Tax Documentation Complexity | +1.6% | EU core, Germany, Belgium, France, spill-over to Middle East and Africa and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Cross-Border Remote Contractor Hiring

Cross-border contractor hiring has shifted from a niche practice to a standard operating model for fast-scaling companies. 88% of the top-funded startups operated across multiple countries within 18 months of founding, and AI trainer roles grew 283% in cross-border engagements in 2025.[1]Deel, “State of Global Hiring Report 2025,” Deel, deel.com This changes the buying problem because enterprises are now hiring in countries where they do not know the local contractor rules or tax processes. AOR platforms fill that gap by acting as the legal intermediary for contracts, withholding, and compliance handling across jurisdictions. As a result, the Agent of Record (AOR) for contractors market is being driven as much by legal complexity as by hiring volume.

Tighter Worker Misclassification Enforcement

Misclassification risk now sits much higher on finance and legal agendas than it did a few years ago. The Internal Revenue Service said the employment tax gap was USD 119 billion per year in Revenue Procedure 2025-10, which signaled a clear intent to tighten oversight.[2]Internal Revenue Service, “Revenue Procedure 2025-10,” Internal Revenue Service, irs.gov The U.S. Department of Labor also issued its final rule on independent contractor status on January 9, 2024, which narrowed the room for aggressive classification practices. Even though Field Assistance Bulletin 2025-1 paused direct enforcement in May 2025, it did not remove the underlying uncertainty for buyers. That uncertainty makes self-managed contractor programs harder to defend once the activity spans many states or countries. This continues to support the Agent of Record (AOR) for Contractors market because liability transfer is now a purchasing priority.

Enterprise Shift Toward Blended Workforce Models

Blended workforce models are changing how enterprises plan project delivery and skills access. Companies now combine employees, contractors, and outside specialists to gain capabilities on an as-needed basis, rather than keeping every function in-house. That shift creates governance gaps because most internal systems were built for payroll workers, not for non-payroll talent spread across several jurisdictions. In the Agent of Record (AOR) for Contractors market, initial adoption often starts with compliance needs, but retention depends more on lifecycle visibility and performance tracking. Providers that connect onboarding, approvals, reuse, and reporting are better positioned to retain larger accounts over time.

Demand for Unified Contractor Onboarding, Tax, And Payment Workflows

Enterprises are moving away from separate tools for onboarding, tax forms, and contractor payments. Contractor Onboarding and Contract Administration is the fastest-growing service type in the Agent of Record (AOR) for contractors market, with a high growth from 2026 to 2031. This shows that buyers want the compliance process handled at the start of the engagement, not corrected after invoices are issued. The spread of structured invoice rules across several countries is also raising the standard for platforms that still depend on manual document handling. That is why unified workflow design is becoming a practical buying requirement for the Agent of Record (AOR) for contractors market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Buyer Confusion Between AOR, EOR, and Payment-Only Tools | -2.4% | Global, most acute in North America and EU | Short term (≤ 2 years) |

| Fragmented Local Labor and Tax Rules Across Jurisdictions | -2.1% | Global, highest friction in APAC and Middle East and Africa | Medium term (2-4 years) |

| EU Platform Work Directive Compliance Spillover | -1.7% | EU core, spill-over to UK and APAC regulatory copycat risk | Long term (≥ 4 years) |

| IP Assignment, Data Residency, and AML Friction in Contractor Onboarding | -1.2% | BFSI and regulated industries globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Buyer Confusion Between AOR, EOR, and Payment-Only Tools

Buyer confusion remains a real sales barrier in the Agent of Record (AOR) for contractors market. Many procurement and legal teams still treat AOR, EOR, and payment-only tools as if they solve the same problem. That leads to under-scoped purchases, slower conversions, and higher switching costs after a compliance review or audit. The New York State Department of Financial Services added another layer in October 2025 by asking financial institutions to strengthen third-party risk review, which makes product differences more material in regulated buying cycles.[3]U.S. Department of Labor, “Employee Or Independent Contractor Classification Under the Fair Labor Standards Act,” Federal Register, federalregister.govProviders that clearly explain legal-principal status, classification coverage, and indemnification terms are converting better than payment-first vendors with retrofitted compliance language.

Fragmented Local Labor and Tax Rules Across Jurisdictions

Fragmented labor and tax rules across jurisdictions continue to slow execution in the Agent of Record (AOR) for contractors market. Providers must interpret local tests on worker status, withholding, social contributions, invoicing, and document retention, country by country. This favors platforms with deep local counsel networks because legal interpretation matters as much as software features in cross-border programs. In regulated sectors, data residency, anti-money laundering checks, and IP assignment rules can stretch onboarding timelines and frustrate in-demand contractors. The result is selective growth, where global coverage claims matter less than real operating depth in each jurisdiction.

Segment Analysis

By Service Type: Risk Coverage Keeps The Core Position While Workflow Services Expand

Insurance, Liability, and Risk Mitigation accounted for 31.42% of service revenue in 2025, giving it the largest position within the Agent of Record (AOR) for contractors market. That lead reflects a clear buyer preference: enterprises want providers that absorb compliance exposure rather than only document it. When misclassification penalties rise in a country, demand for insurance-backed coverage usually rises with them. Contractor Onboarding and Contract Administration is projected to grow at a 21.47% CAGR through 2031, as buyers seek to accelerate contractor activation without repeating legal review at every step.

Compliance and Worker Classification Management and Global Contractor Payments and Tax Documentation remain the operational center of most platform stacks. These functions matter more as tax documentation and invoice rules become harder to manage across multiple countries simultaneously. Contractor Lifecycle Management and Workforce Analytics and Reporting are still smaller service lines, but they are gaining more attention from enterprises with large contractor populations. In the Agent of Record (AOR) industry, vendors that can extend from liability coverage into analytics are building a stickier position than compliance-only providers.

By End User Enterprise Size: SMEs Still Lead, But Large Enterprises Are Scaling Faster

SMEs held 58.27% of the Agent of Record (AOR) for contractors market share in 2025, while Large Enterprises are projected to expand at a 22.63% CAGR through 2031. SMEs often depend on contractors as a core staffing model, so each engagement carries more visible compliance risk at the company level. Large enterprises moved faster into this category after internal reviews linked contractor governance to tax and permanent establishment exposure. Many multinationals now prefer AOR procurement over broad reclassification because it preserves workforce flexibility while closing the most exposed gaps.

Vendors serving larger accounts are differentiating through integration with major HCM and finance systems rather than through standalone dashboards. Procurement teams want synchronized records across legal, finance, and workforce functions, not duplicate data layers. Speed of rollout across India, Vietnam, and the Philippines also matters because global contractor programs are now launched across several countries at once. This gives full-stack providers an advantage when the Agent of Record (AOR) for Contractors market shifts from local use cases to enterprise-wide governance.[4]Organisation for Economic Co-operation and Development, “Model Tax Convention on Income and on Capital, 2025 Update,” OECD, oecd.org

By Deployment Model: Cloud Leads On Scale While Hybrid Gains In Regulated Environments

Cloud-based deployment accounted for 63.88% of the Agent of Record (AOR) for contractors market size in 2025, while hybrid deployment is projected to grow at a 20.19% CAGR through 2031. Cloud adoption stayed high because digital-native buyers wanted rule updates and workflow changes delivered quickly across all users. A shared cloud model also reduces regulatory lag because each jurisdiction update can be applied once and rolled out broadly. Hybrid deployment is gaining popularity because some sectors still want sensitive contractor data held inside auditable internal environments.

The New York State Department of Financial Services strengthened that preference in 2025 by urging financial institutions to deepen oversight of third-party arrangements. On-premises deployment still exists among government contractors and defense-adjacent enterprises with tighter data controls. Even so, most new growth is coming from architectures that combine internal data control with cloud-based payment and documentation workflows. This suggests the Agent of Record (AOR) for contractors market will not move in a single direction on deployment, as compliance rules vary too much by sector and country.

By Workforce Type: Cross-Border Demand Is Redefining The Growth Path

Independent Contractors and Freelancers held 36.51% of workforce demand in 2025, while Cross-border Contractors are forecast to grow at a 23.14% CAGR through 2031. This large base reflects the original use case for the Agent of Record (AOR) for the contractors market, which centered on project-based freelancers hired for defined work. The mix is shifting because companies now source more specialized talent across borders where they lack local entities. AI trainer and machine learning annotation roles grew 283% in cross-border engagements in 2025, indicating that new technical work is fueling this segment.

Contingent Workforce and SOW Contractors sit in the middle of the market, where AOR platforms often need to connect with vendor management systems and procurement tools. Distributed Project Teams remain smaller today, but they are becoming more important for technology and professional services firms. The OECD updated its Model Tax Convention in November 2025, raising concerns about permanent establishment issues arising from borderless work arrangements. That change makes the Agent of Record (AOR) for contractors market more relevant for companies running multinational project teams without a compliant intermediary.

By End-User Industry: IT And Telecom Holds The Lead While BFSI Moves Up Faster

Information Technology and Telecom held 24.73% of revenue in 2025, while BFSI is projected to grow at a 19.89% CAGR through 2031. Technology buyers rely on contractors for software development, product launches, infrastructure work, and specialized AI programs that rise and fall with each project cycle. BFSI is expanding faster because regulated firms need cleaner documentation on third-party workers, stronger onboarding controls, and clearer vendor accountability. The SEC provided clarity in November 2025 with a no-action letter on broker-dealer contractor arrangements, which supports a more formal approach to contractor status in financial services.

Healthcare and Life Sciences also remain a meaningful adopter group because contractor access often touches sensitive data and tightly controlled workflows. Retail, e-commerce, and industrial manufacturing are earlier in adoption, but project-based contractor use is broadening as operations become more digitized. Government and public sector demand moves more slowly because procurement cycles are longer and contracting rules are stricter. Even so, the Agent of Record (AOR) for Contractors market has room to deepen its presence in these industries as compliance needs expand beyond technology-led buyers.

Geography Analysis

North America held 47.19% of the Agent of Record (AOR) market share for contractors in 2025, making it the largest regional contributor. The United States anchors that position because contractor engagement has been common for years, and enforcement pressure is high. Revenue Procedure 2025-10 heightened visibility into classification risk by updating Section 530 safe-harbor standards for the first time in decades. The 2024 federal rule on independent contractor status and the 2025 enforcement pause together kept the legal environment unsettled rather than relaxed. Canada and Mexico added to regional demand as gig-work regulation evolved and nearshore contractor use expanded.

Asia-Pacific is the fastest-growing region in the Agent of Record (AOR) for contractors market, with a projected 24.37% CAGR through 2031. India stands out because Quess Corp said the country had around 2,000 global capability centers in 2026, and 24% of its workforce was in contract arrangements. The Indian Staffing Federation reported a flexi-workforce population of 1.91 million in Q2 FY2026, indicating a large formal contractor base, even before informal hiring is counted. Australia and New Zealand are more mature adopters, while Southeast Asian markets reward providers that can quickly adjust pay, tax, and documentation logic.

Europe is the second-largest regional market, and its regulatory maturity both supports demand and raises the bar for providers. The EU Platform Work Directive set a December 2026 transposition deadline, which increases the need for documented contractor relationships and clearer legal structures. The United Kingdom remains adjacent through IR35-style scrutiny, while South America, the Middle East, and Africa are earlier-stage regions with growing demand pockets in Brazil, the UAE, and South Africa. E-invoicing mandates in Germany, Belgium, and France also push contractor payment workflows toward structured data, favoring vendors with stronger compliance infrastructure.

Competitive Landscape

The Agent of Record (AOR) for the contractors market remains moderately fragmented, with no single provider holding a dominant global position across services and regions. Buyers usually compare vendors on two practical points: how many countries they can truly support and how well their systems connect with payroll, finance, and workforce tools. Full-stack platforms are gaining ground because enterprise procurement teams prefer fewer vendors across contractor compliance, payroll, and reporting. Beeline's June 2025 acquisition of MBO Partners showed that vendor management providers now want AOR capability built into their own stacks rather than through outside partners. That move increased pressure on standalone specialists in larger sales cycles.

Product differentiation is also moving toward better intelligence, faster onboarding, and clearer spend visibility. SafeGuard World International launched its Intelligent Workforce platform in April 2026 to combine AOR, EOR, and contractor analytics into a single interface. Papaya Global announced a strategic alliance with Tech Mahindra in April 2026 to connect compliance infrastructure with enterprise technology delivery for global clients. These moves show that the Agent of Record (AOR) for the contractors market is increasingly being sold as part of a broader workforce operations platform.

Smaller regional providers such as Wisemonk, Transformify, and INS Global continue to win business where country knowledge and localized pricing matter more than global brand scale. That two-tier structure slows consolidation because niche providers remain useful in markets where global players lack sufficient depth. Oyster HR's September 2024 funding round also supported continued expansion across EOR and AOR offerings, which kept competitive pressure elevated as the category matured. YunoJuno's April 2026 leadership recognition strengthened its profile among enterprise clients evaluating structured contractor management platforms.

Agent Of Record (AOR) For Contractors Industry Leaders

Global Contractor Management Solutions Pty Ltd

MBO Partners, Inc.

Papaya Global Ltd.

Worksome ApS

Worksuite Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SafeGuard World International launched the Intelligent Workforce platform (April 9, 2026), an AI-driven workforce management solution integrating AOR, EOR, and contractor analytics into a unified compliance interface, positioning the company as a full-stack workforce intelligence provider for enterprise blended workforce programs.

- April 2026: Papaya Global announced a strategic alliance with Tech Mahindra (April 12, 2026), combining Papaya's global payroll and AOR infrastructure with Tech Mahindra's enterprise technology delivery capabilities to target large enterprise clients across BFSI and IT and Telecom sectors globally.

- April 2026: YunoJuno was named a Leader in the Everest Group FEMS PEAK Matrix 2026 at the highest tier (April 13, 2026), validating its capability positioning among enterprise clients evaluating freelancer and contractor management platforms.

- June 2025: Beeline acquired MBO Partners (June 12, 2025), consolidating VMS and AOR capabilities under a single enterprise workforce management platform, a transaction that signals VMS providers are absorbing AOR functionality to expand their contractor compliance value proposition rather than partnering for it.

Global Agent Of Record (AOR) For Contractors Market Report Scope

The Agent of Record (AOR) for contractors market refers to specialized services and technology platforms that act as the legal and administrative representative for organizations engaging independent contractors, freelancers, contingent workers, cross-border contractors, SOW contractors, and distributed project teams. These solutions manage critical functions such as compliance and worker classification, contractor onboarding and contract administration, global payments and tax documentation, insurance and liability coverage, risk mitigation, contractor lifecycle management, and workforce analytics and reporting. Delivered through cloud-based, hybrid, and on-premises deployment models, they serve both large enterprises and small and medium-sized enterprises across industries, including BFSI, healthcare and life sciences, information technology and telecom, retail and e-commerce, industrial manufacturing, government and public sector, and other end-user industries. The core purpose of this market is to simplify contractor engagement, ensure compliance with labor and tax regulations, reduce organizational risk, and enhance the efficiency of managing flexible, distributed workforces.

The Agent of Record (AOR) for contractors market report is segmented by Service Type (Compliance and Worker Classification Management, Contractor Onboarding and Contract Administration, Global Contractor Payments and Tax Documentation, Insurance, Liability and Risk Mitigation, Contractor Lifecycle Management, and Workforce Analytics and Reporting), Enterprise Size (Small and Medium-Sized Enterprises, and Large Enterprises), Deployment Model (Cloud-Based, Hybrid, and On-Premises), Workforce Type (Independent Contractors and Freelancers, Cross-border Contractors, Contingent Workforce, SOW Contractors, and Distributed Project Teams), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Compliance and Worker Classification Management |

| Contractor Onboarding and Contract Administration |

| Global Contractor Payments and Tax Documentation |

| Insurance, Liability and Risk Mitigation |

| Contractor Lifecycle Management |

| Workforce Analytics and Reporting |

| Small and Medium-Sized Enterprises |

| Large Enterprises |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Independent Contractors and Freelancers |

| Cross-border Contractors |

| Contingent Workforce |

| SOW Contractors |

| Distributed Project Teams |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Service Type | Compliance and Worker Classification Management | |

| Contractor Onboarding and Contract Administration | ||

| Global Contractor Payments and Tax Documentation | ||

| Insurance, Liability and Risk Mitigation | ||

| Contractor Lifecycle Management | ||

| Workforce Analytics and Reporting | ||

| By End User Enterprise Size | Small and Medium-Sized Enterprises | |

| Large Enterprises | ||

| By Deployment Model | Cloud-Based | |

| Hybrid | ||

| On-Premises | ||

| By Workforce Type | Independent Contractors and Freelancers | |

| Cross-border Contractors | ||

| Contingent Workforce | ||

| SOW Contractors | ||

| Distributed Project Teams | ||

| By End-user Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the Agent of Record (AOR) for contractors market?

The Agent of Record (AOR) for contractors market stood at USD 2.59 billion in 2026 and is forecast to reach USD 6.28 billion by 2031, growing at a 19.38% CAGR over 2026-2031.

What is driving growth in contractor compliance platforms globally?

Cross-border hiring, tighter misclassification enforcement, and demand for unified onboarding, tax, and payment workflows are the main growth drivers.

Which region leads today and which region is growing fastest?

North America led with 47.19% share in 2025, while Asia-Pacific is projected to grow the fastest at a 24.37% CAGR through 2031.

Which service category is the largest and which one is expanding the fastest?

Insurance, Liability and Risk Mitigation led with 31.42% share in 2025, while Contractor Onboarding and Contract Administration is projected to grow the fastest at 21.47% CAGR.

Which buyer group is creating the strongest expansion opportunity?

SMEs held 58.27% share in 2025, but large enterprises are expanding faster at a projected 22.63% CAGR as they centralize contractor governance across more jurisdictions.

Which end-user sectors matter most for platform vendors?

Information Technology and Telecom led with 24.73% share in 2025, while BFSI is expected to grow the fastest at 19.89% CAGR because regulated firms need stronger contractor controls.

Page last updated on: