Africa Tobacco Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

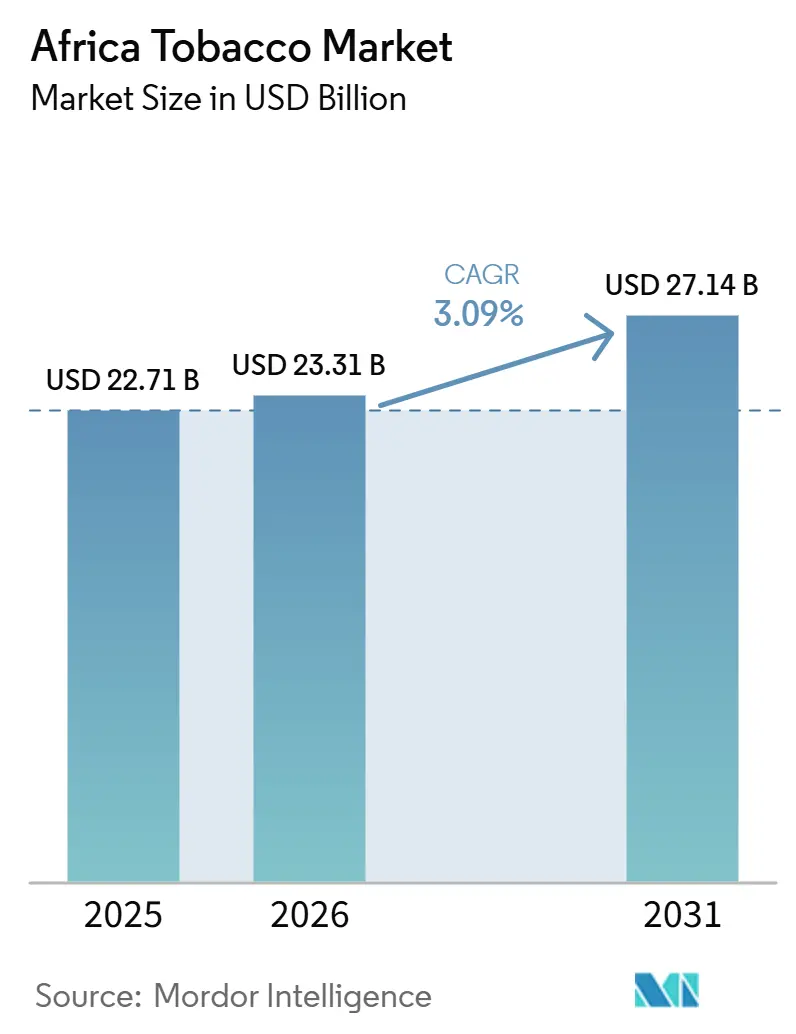

| Base Year Market Size (2025) | USD 22.71 Billion |

| Market Size (2026) | USD 23.31 Billion |

| Market Size (2031) | USD 27.14 Billion |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

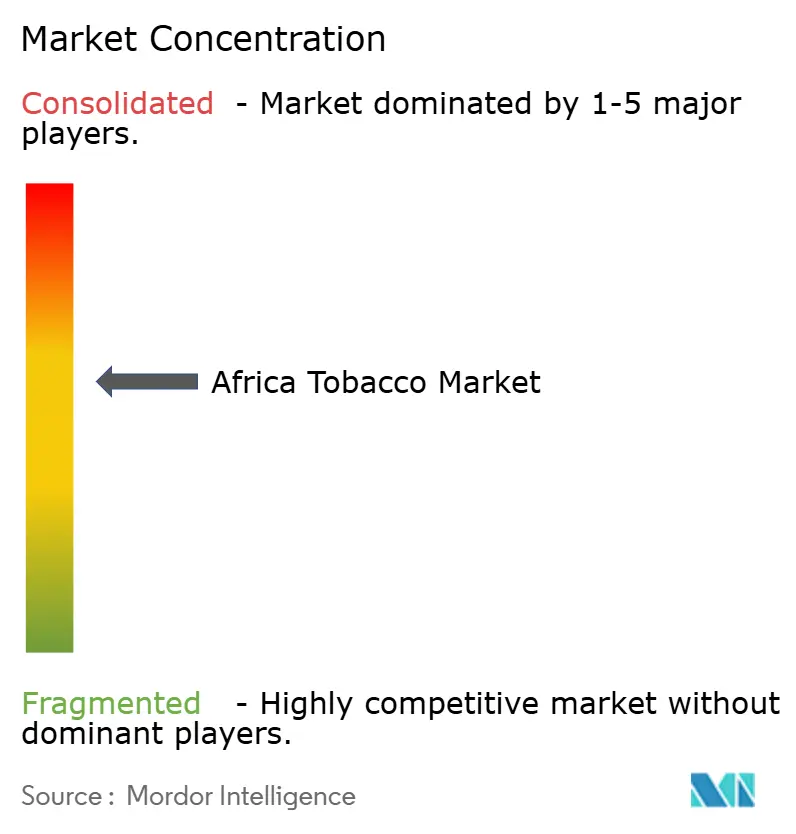

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Tobacco Market Analysis by Mordor Intelligence

The Africa tobacco market size is expected to grow from USD 22.71 billion in 2025 to USD 23.31 billion in 2026 and is forecast to reach USD 27.14 billion by 2031 at 3.09% CAGR over 2026-2031. The market growth is primarily supported by the large adult consumer base across countries such as South Africa, Egypt, Nigeria, and Algeria, where tobacco consumption remains relatively stable despite increasing regulatory oversight. Rising urbanization, expanding retail distribution networks, and the availability of affordable tobacco products continue to sustain demand across several African economies. In addition, multinational tobacco manufacturers are strengthening their regional presence through product portfolio expansion, localized manufacturing, and wider distribution partnerships. However, increasing tobacco taxation, stricter advertising restrictions, and growing public health awareness campaigns are expected to moderate long-term consumption growth, resulting in steady but moderate market expansion over the forecast period.

Key Report Takeaways

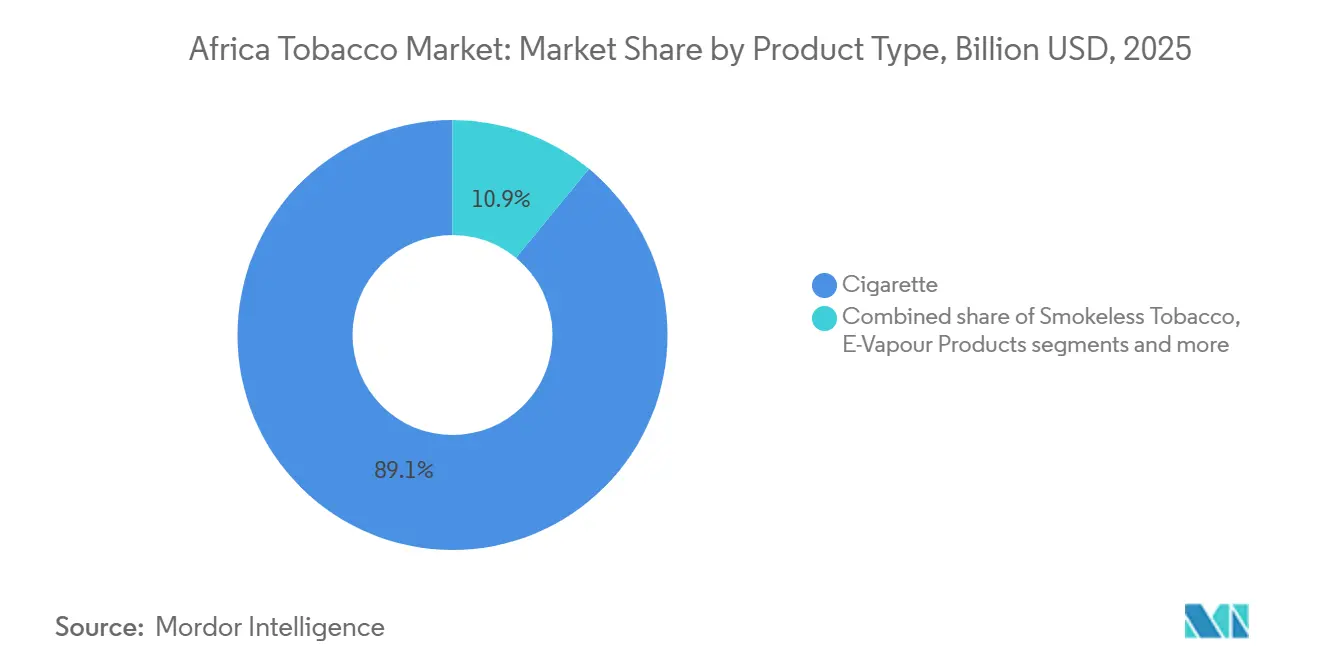

- By product type, cigarettes held 89.06% share in 2025, while e-vapour products are projected to grow at 4.83% CAGR through 2031.

- By end user, males accounted for 91.61% of value in 2025, while females are forecast to expand at 4.08% CAGR through 2031.

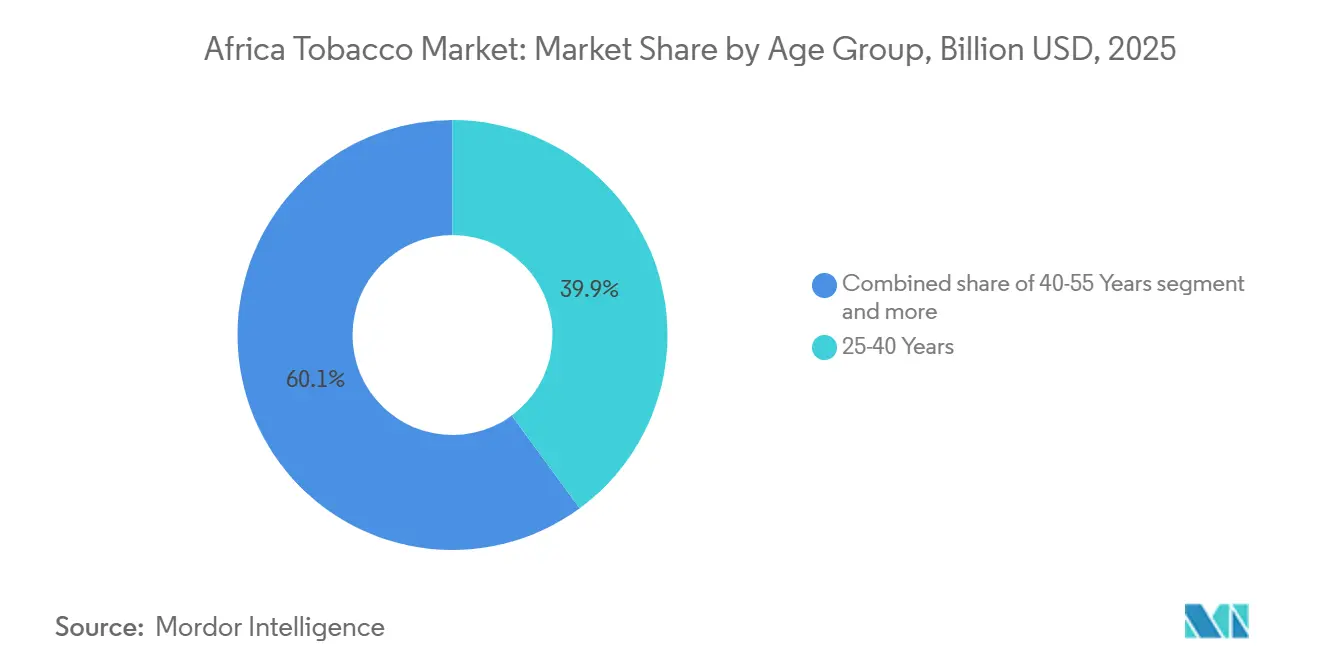

- By age group, 25-40 years held 39.91% share in 2025, while the below 25 years segment is projected to grow at 3.74% CAGR through 2031.

- By distribution channel, convenience and traditional grocery stores accounted for 63.31% of sales in 2025, while specialty and tobacco stores are forecast to advance at 4.14% CAGR through 2031.

- By geography, Egypt held 30.67% share in 2025 and also recorded the highest projected CAGR at 4.29% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Tobacco Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of novel tobacco and nicotine products | +0.7% | South Africa, Nigeria, Kenya, spill-over to Egypt and Morocco | Medium term (2-4 years) |

| Intensifying marketing and promotional strategies by tobacco companies | +0.5% | Sub-Saharan Africa, North Africa | Short term (≤ 2 years) |

| Increasing strategic expansion of global tobacco companies across Africa | +0.6% | Pan-Africa, early gains in Morocco, Zimbabwe, South Africa | Medium term (2-4 years) |

| Rising focus on flavor innovation and product diversification | +0.4% | South Africa, Nigeria, Egypt | Short term (≤ 2 years), Medium term (2-4 years) |

| Growing investments in research and development amid changing market dynamics | +0.3% | Egypt, Nigeria | Long term (≥ 4 years) |

| Regulatory loopholes and limited implementation of tobacco excise taxes | +0.4% | East Africa, West Africa, North Africa | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing adoption of novel tobacco and nicotine products

The Africa tobacco market is no longer shaped solely by combustible tobacco demand, as reduced-risk categories are beginning to influence pricing, retail strategies, and category mix. Philip Morris International is expected to launch its VEEV e-cigarette in South Africa in October 2025, completing a three-product smoke-free portfolio that also includes IQOS and ZYN. This launch would make South Africa one of only 20 markets globally to offer all three categories together. The launch is significant beyond South Africa, as it indicates that leading companies increasingly view selected African markets as viable platforms for multi-category nicotine commercialization, rather than only as cigarette distribution hubs. Around 20% of South Africa’s legal cigarette market has already shifted to smoke-free products, changing merchandising, shelf economics, and how companies defend brand relevance in formal trade. BAT Kenya’s planned reintroduction of VELO nicotine pouches in July 2025 under an import-led model shows that companies are testing oral nicotine formats even in price-sensitive markets, with lower operating risk than local manufacturing. This shift makes the Africa tobacco market more attractive for early movers that can scale reduced-risk categories before retail infrastructure and regulation become more difficult to navigate.

Intensifying marketing and promotional strategies by tobacco companies

Intensifying marketing and promotional strategies by tobacco companies continue to support demand across the Africa tobacco market, particularly in countries where enforcement of advertising restrictions remains inconsistent. While conventional advertising is increasingly regulated, tobacco manufacturers are shifting their focus toward digital platforms, social media engagement, point-of-sale promotions, and indirect brand-building activities to maintain consumer visibility. Marketing efforts are also becoming more targeted, with companies using lifestyle-oriented campaigns and influencer collaborations to reach younger adult consumers. A 2025 peer-reviewed study found that digital media and influencer-led tobacco marketing was widespread across Nigeria, South Africa, Rwanda, Kenya, and Senegal, demonstrating significant exposure among women aged 18-24[1]Source: Biology and Health Science, “The Evolution of Tobacco Marketing to Women and Girls in Sub-Saharan Africa”, bio.org. This highlights how uneven regulatory oversight of digital channels continues to provide opportunities for tobacco companies to engage emerging consumer segments. In addition, promotional activities such as retail branding, product displays, and sponsorships in markets with relatively flexible regulations further strengthen brand recognition and consumer loyalty.

Increasing strategic expansion of global tobacco companies across Africa

Large manufacturers continue to place long-term bets on the Africa tobacco market, despite high short-term volatility related to illicit trade. Japan Tobacco International is expected to officially open its USD 92 million factory in Tétouan, Morocco, in January 2025. The facility will have an initial capacity of 5 billion cigarettes per year, with built-in expansion potential to reach 10 billion cigarettes. The investment is designed to serve 12 North and West African markets, indicating that manufacturers view Africa as an integrated production and distribution region rather than a collection of isolated country-level opportunities. Philip Morris International is expected to re-establish a direct commercial presence in Zimbabwe in February 2026, aligning with the country’s Tobacco Value Chain Transformation Plan and positioning the company closer to a rapidly evolving leaf and processing base. KT&G also uses its Turkey manufacturing base as a regional hub for Africa. The Middle East and Africa are expected to account for 36% of its international cigarette sales mix, while overseas revenues are projected to rise by 24.6% year on year in the first quarter of 2026. These developments indicate that the Africa tobacco market continues to offer sufficient long-term volume, sourcing, and manufacturing advantages to justify new capital investment, despite uneven policy and channel conditions.

Rising focus on flavor innovation and product diversification

The rising focus on flavor innovation and product diversification is emerging as a key driver of the Africa tobacco market as manufacturers seek to attract adult consumers through differentiated product offerings. Tobacco companies are expanding their portfolios with capsule cigarettes, menthol variants, flavored cigars, heated tobacco products, and nicotine pouches to cater to evolving consumer preferences and enhance the overall user experience. Product innovation also enables manufacturers to address demand across different price points, from value brands to premium offerings, thereby broadening their customer base. In urban markets, younger adult consumers are showing greater interest in modern product formats that offer convenience, customization, and perceived novelty. Companies are also introducing limited-edition variants and redesigned packaging where regulations permit, helping strengthen brand appeal and consumer engagement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing environmental and public health concerns over tobacco cultivation | -0.4% | East Africa, Southern Africa, Zimbabwe, Malawi, Mozambique | Long term (≥ 4 years) |

| Rising prevalence and evidence of illicit tobacco trade | -0.8% | Pan-Africa, severe in South Africa, Kenya, Zambia, Uganda | Short term (≤ 2 years), Medium term (2-4 years) |

| Climate variability and extreme weather affecting tobacco leaf production | -0.3% | Zimbabwe, Malawi, Mozambique, Tanzania | Medium term (2-4 years), Long term (≥ 4 years) |

| Rising health awareness and declining social acceptance of tobacco consumption | -0.5% | Urban markets, South Africa, Kenya, Nigeria, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence and evidence of illicit tobacco trade

The rising prevalence of illicit tobacco trade remains a significant restraint on the Africa tobacco market, undermining the growth of the formal tobacco industry and reducing government tax revenues. The widespread availability of smuggled and counterfeit tobacco products allows consumers to access cigarettes at substantially lower prices, intensifying competition for legitimate manufacturers. Illicit trade also weakens the effectiveness of tobacco taxation and public health policies by maintaining the affordability of tobacco products despite higher excise duties. According to WHO Framework Convention on Tobacco Control (WHO FCTC) reporting, fewer than half of African Parties had implemented a track-and-trace system, highlighting persistent gaps in supply chain monitoring and enforcement[2]Source: World Health Organization, “Global Progress Report on Implementation of the Protocol to Eliminate Illicit Trade in Tobacco Products”, who.int. As a result, regulatory authorities continue to face challenges in identifying, tracking, and preventing the movement of illegal tobacco products across borders.

Rising health awareness and declining social acceptance of tobacco consumption

Rising health awareness and the declining social acceptance of tobacco consumption are increasingly restraining the growth of the Africa tobacco market, particularly in urban and middle-income populations. Public health campaigns, greater access to health information, and stronger government initiatives are encouraging consumers to reduce or quit tobacco use due to growing awareness of smoking-related diseases. Social attitudes toward smoking are also evolving, with tobacco use becoming less socially acceptable in workplaces, educational institutions, and public spaces. According to the World Health Organization (WHO), adult tobacco prevalence in Africa stood at 9.5% in 2024, including 16.6% among males and 2.5% among females, even though the overall number of tobacco users continues to increase because of the continent's rapidly expanding population[3]Source: World Health Organization, “WHO global report on trends in prevalence of tobacco use 2000–2024 and projections 2025–2030”, who.int. This indicates that while population growth supports absolute consumption, the proportion of adults using tobacco is under increasing pressure from changing health perceptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combustibles Dominate, But E-Vapour Is Redefining Market Structure

Cigarettes captured 89.06% of the Africa tobacco market share in 2025, confirming their continued dominance across formal and informal retail channels. Their position remains strongest in markets where affordability is critical and single-stick sales are deeply embedded in daily purchasing habits. Nigeria and Ethiopia continue to account for some of the highest cigarette consumption volumes by unit, while Egypt remains the value anchor due to stronger pricing power than many other African markets. Cigars and cigarillos remain concentrated in premium urban and hospitality settings, particularly in South Africa, Egypt, and Morocco, where specialized demand is more visible. Smokeless tobacco also retains a meaningful presence across rural areas of southern and eastern Africa, although a large share of consumption occurs outside tightly measured formal channels.

The Africa tobacco market size for e-vapour products is projected to grow at a CAGR of 4.83% through 2031, making it the fastest-growing product segment during the report period. This growth reflects the rising availability of disposable formats in South Africa, Nigeria, and Kenya, where both modern retail and informal distribution support faster product trial. However, growth remains uneven because countries such as Ethiopia, Rwanda, and Uganda have imposed outright bans, while Nigeria continues to operate without a formal regulatory framework for these products. As a result, the Africa tobacco industry has a product segment with strong urban momentum but limited regulatory consistency for smooth continent-wide scaling.

By End User: Male Segment Anchors Volume, Female Cohort Drives Growth Premium

The male end-user segment dominated the Africa tobacco market, accounting for 91.61% of the market value in 2025. This leadership is primarily driven by significantly higher smoking prevalence among men across most African countries, supported by long-standing cultural and social acceptance of tobacco use among male consumers. Cigarettes remain the most widely consumed tobacco product within this demographic, particularly among working-age adults in countries such as South Africa, Egypt, Nigeria, and Algeria. Higher disposable incomes among male consumers in many African economies also contribute to greater spending on both premium and value tobacco products.

The female end-user segment is projected to register the fastest CAGR of 4.08% during 2026-2031. Growth is being supported by increasing urbanization, rising female workforce participation, and changing social attitudes toward tobacco consumption in several African countries. Greater exposure to international lifestyles, expanding retail accessibility, and the introduction of products with modern packaging and alternative formats are also contributing to higher adoption among female consumers. In addition, tobacco manufacturers are introducing slimmer cigarette formats and reduced-odor or flavored alternatives in selected markets to appeal to evolving consumer preferences where regulations permit.

By Age Group: 25-40 Years Holds Core Volume, Youth Cohort Reshapes Future Demand

The 25-40 years cohort held 39.91% of the Africa tobacco market in 2025, which made it the largest age-based value segment. This group combines working-age income, routine purchase behavior, and strong exposure to urban retail networks, which supports dependable volume in mainstream cigarette formats. It also benefits from the expansion of middle-income consumers in countries such as Egypt, Nigeria, and Morocco, where city-based demand remains more organized and easier to monetize. The 40-55 years and above 55 years cohorts still contribute important revenue because they contain legacy smokers with more established use patterns and lower switching urgency. In rural settings, older users remain more closely linked to smokeless and hand-rolled products, which keeps part of their consumption outside the most visible formal market channels.

The below 25 years segment is forecast to grow at 3.74% CAGR through 2031, which keeps it below e-vapour growth but still firmly above many mature demographic cohorts. Africa’s population profile is central here because nearly 60% of the continent’s population is under 25, which creates one of the world’s largest pools of potential new nicotine users. A 2024 multi-country study estimated that 8.7 million school-going adolescents aged 13-15 in 53 African countries currently use some form of tobacco. The same youth base is more exposed to flavored vaping products, pouches, and digitally promoted entry formats than older cohorts were at the same age. For the Africa tobacco market, this means the next wave of users may not start with a traditional cigarette, even if many later migrate into broader nicotine consumption. That shift matters because it changes the future category mix, retail training needs, and the balance between formal and informal product routes.

By Distribution Channel: Informal Channels Anchor Volume, Specialty Retail Drives Value

Convenience and traditional grocery stores accounted for 63.31% of value in 2025, which kept them at the center of the Africa tobacco market. Their lead reflects proximity, high purchase frequency, and the resilience of single-stick transactions in dense urban and peri-urban areas. These outlets remain critical because they connect the product to everyday consumer traffic in markets where modern trade is still uneven. Supermarkets and hypermarkets held a smaller but stable role, especially in South Africa, Egypt, Morocco, and Nigeria, where structured merchandising and stronger compliance practices are more common. Other channels, including kiosks, mobile vendors, and informal digital routes, continue to act as major access points for illicit and counterfeit products.

The Africa tobacco market size for specialty and tobacco stores is projected to rise at 4.14% CAGR through 2031, which makes them the fastest-growing channel in the report. This growth is tied to premiumization and to the need for dedicated retail settings that can explain smoke-free products more clearly than a general convenience outlet can. Philip Morris has already used IQOS-led specialty environments in South Africa to support category education and controlled product experience, which mirrors its approach in more developed markets.

Geography Analysis

Egypt dominated the Africa tobacco market, accounting for 30.67% of the market value in 2025, and is also projected to register the fastest CAGR of 4.29% during 2026-2031. The country's leadership is supported by its large adult population, well-established tobacco manufacturing industry, and widespread cigarette consumption across both urban and rural areas. Egypt is home to one of Africa's largest tobacco processing and distribution networks, ensuring extensive product availability through traditional retail stores and modern trade channels. Strong domestic production, combined with the presence of leading international and local tobacco companies, continues to strengthen market growth.

South Africa and Nigeria represent two of the most significant tobacco markets in Sub-Saharan Africa, supported by their large populations and established retail infrastructure. South Africa has a mature tobacco industry with well-developed manufacturing capabilities and a broad distribution network, although stricter regulations, plain packaging discussions, and higher excise taxes continue to influence market dynamics. Nigeria, on the other hand, offers strong long-term growth potential due to its rapidly expanding adult population, increasing urbanization, and improving retail accessibility.

Algeria and Morocco collectively contribute a notable share of the African tobacco market, supported by steady domestic demand and expanding organized retail channels. Algeria remains an important market due to its relatively high smoking prevalence and consistent demand for manufactured cigarettes, while Morocco benefits from a stable consumer base and ongoing modernization of retail distribution. Across other African countries, tobacco consumption patterns vary depending on income levels, demographic trends, regulatory frameworks, and cultural preferences.

Competitive Landscape

The Africa tobacco market is moderately consolidated in the organized sector, with British American Tobacco, Philip Morris International, and Japan Tobacco International accounting for a substantial share of formal cigarette sales across key markets. These multinational companies leverage extensive manufacturing facilities, established distribution networks, and strong brand portfolios to maintain their competitive positions in countries such as South Africa, Egypt, Nigeria, and Algeria. Their competitive advantage is further supported by long-standing relationships with wholesalers, retailers, and duty-paid distribution channels. Companies continue to invest in product innovation, premium cigarette offerings, and next-generation nicotine products in selected African markets.

Competition is further shaped by the presence of national tobacco manufacturers and regional players that compete primarily in the value-priced cigarette segment. Domestic companies benefit from strong local market knowledge, established retail relationships, and the ability to offer competitively priced products suited to regional consumer preferences. In several African countries, local manufacturers also receive advantages from domestic production capabilities and lower distribution costs compared with imported brands.

The competitive landscape is also influenced by varying regulatory environments, taxation policies, and the presence of illicit tobacco trade across several African markets. While formal manufacturers compete through branding, product quality, and distribution reach, illegal cigarette sales continue to exert pricing pressure in some countries, particularly where tax differentials are significant. In response, leading companies are increasingly focusing on regulatory compliance, anti-illicit trade initiatives, and digital supply chain monitoring to protect market share.

Africa Tobacco Industry Leaders

British American Tobacco PLC

Eastern Company S.A.E.

Philip Morris International Inc.

Japan Tobacco, Inc.

Imperial Brands PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Philip Morris International re-established a direct commercial presence in Zimbabwe for the first time in nearly two decades, entering a market that recorded tobacco production of 354,000 tonnes in the 2024/25 season. The move aligns with Zimbabwe's Tobacco Value Chain Transformation Plan, which targets USD 5 billion in sector revenues, and positions PMI ahead of local beneficiation policy mandates.

- October 2025: Philip Morris South Africa launched its VEEV e-cigarette, completing the company's smoke-free product trilogy alongside IQOS heated tobacco and ZYN nicotine pouches. South Africa became one of only 20 markets globally to offer all three smoke-free categories, underscoring PMI's intent to use the country as the continent's regulatory testbed for harm reduction policy advocacy.

- January 2025: Japan Tobacco International officially opened its USD 92 million green factory in Tétouan, Morocco, with an initial production capacity of 5 billion cigarettes per year. The facility is designed to serve the North and West Africa cluster of 12 markets and includes pre-planned expansion capacity to reach 10 billion cigarettes per year, supporting future export growth into West African markets.

Africa Tobacco Market Report Scope

Tobacco is a commercial agricultural crop derived from the leaves of plants belonging to the Nicotiana genus, primarily Nicotiana tabacum. The Africa tobacco market is segmented by product type, end user, age group, distribution channel and geography. Based on product type, the market is segmented into cigarette, cigars and cigarillos, smokeless tobacco, e-vapour products and others. Based on end user, the market is segmented into male and female. Based on age group, the market is segmented into below 25 years, 25-40 years, 40-55 years, and above 55 years. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/traditional grocery stores, specialty/tobacco stores and other distribution channels. Based on geography, the market is segmented into South Africa, Nigeria, Egypt, Algeria, Morocco and Rest of Africa. For each segment, the market sizing and forecasting have been done in value terms (USD).

| Cigarette |

| Cigars and Cigarillos |

| Smokeless Tobacco |

| E-Vapour Products |

| Others |

| Male |

| Female |

| Below 25 Years |

| 25-40 Years |

| 40-55 Years |

| Above 55 Years |

| Supermarkets/Hypermarkets |

| Convenience/Traditional Grocery Stores |

| Specialty/Tobacco Stores |

| Other Distribution Channels |

| South Africa |

| Nigeria |

| Egypt |

| Algeria |

| Morocco |

| Rest of Africa |

| By Product Type | Cigarette |

| Cigars and Cigarillos | |

| Smokeless Tobacco | |

| E-Vapour Products | |

| Others | |

| By End User | Male |

| Female | |

| By Age Group | Below 25 Years |

| 25-40 Years | |

| 40-55 Years | |

| Above 55 Years | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Traditional Grocery Stores | |

| Specialty/Tobacco Stores | |

| Other Distribution Channels | |

| By Geography | South Africa |

| Nigeria | |

| Egypt | |

| Algeria | |

| Morocco | |

| Rest of Africa |

Key Questions Answered in the Report

What is the projected value of the Africa tobacco market by 2031?

The Africa tobacco market is forecast to reach USD 27.14 billion by 2031, up from USD 23.31 billion in 2026, at a 3.09% CAGR over 2026-2031.

Which product segment is growing fastest across Africa?

E-vapour products are the fastest-growing product segment, with a projected 4.83% CAGR through 2031, supported by rising urban distribution and broader smoke-free commercialization.

Which country leads tobacco sales in Africa?

Egypt led the region in 2025 with 30.67% share and also posted the highest projected country CAGR at 4.29% through 2031.

Why is illicit trade such a major issue in Africa?

Illicit trade reduces formal company revenue, tax collection, and plant utilization even when consumer demand remains stable, with severe pressure visible in South Africa, Kenya, and Uganda.

What distribution channel matters most for tobacco sales in Africa?

Convenience and traditional grocery stores remain the largest channel with 63.31% of 2025 sales because they fit single-stick purchasing and dense informal retail patterns.

Page last updated on: