Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

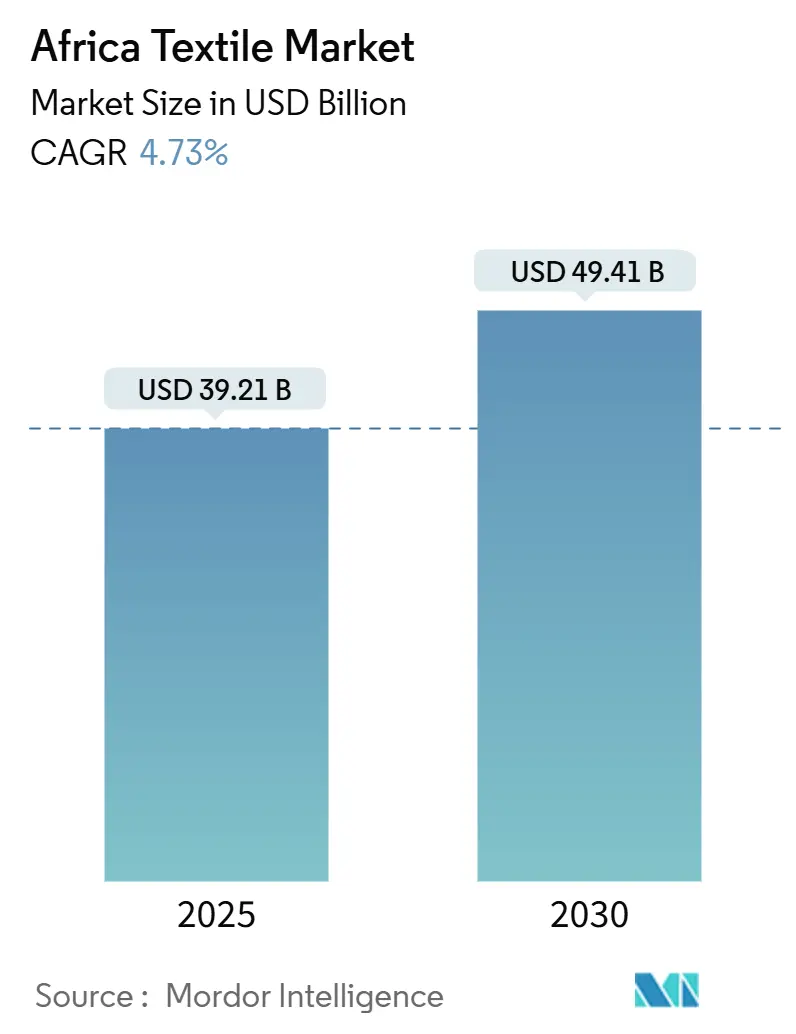

| Market Size (2025) | USD 39.21 Billion |

| Market Size (2030) | USD 49.41 Billion |

| Growth Rate (2025 - 2030) | 4.73% CAGR |

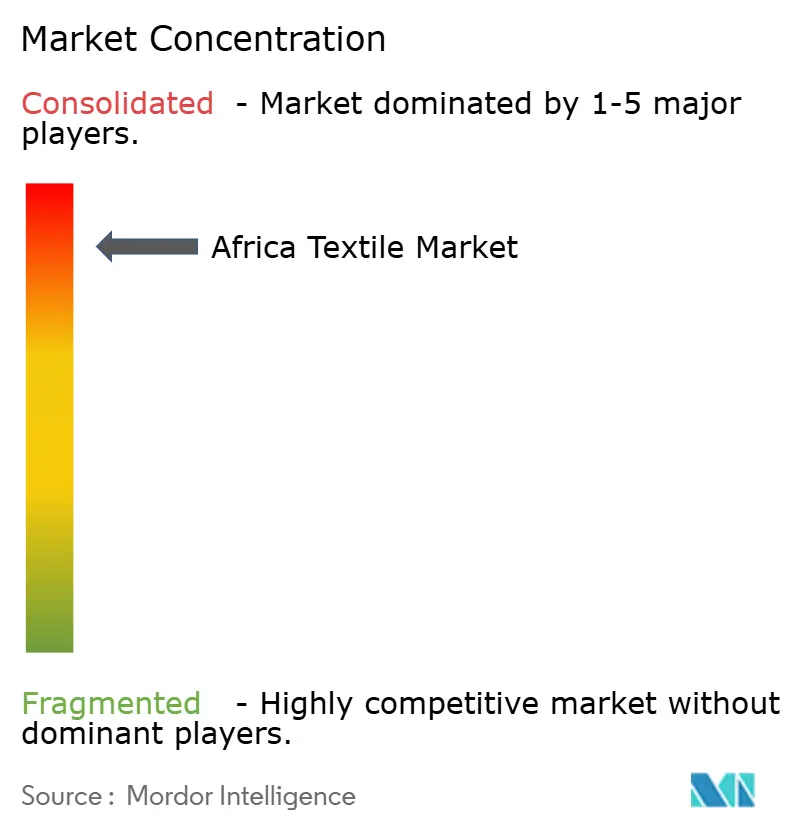

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Textile Market Analysis by Mordor Intelligence

The Africa Textile Market size is estimated at USD 39.21 billion in 2025, and is expected to reach USD 49.41 billion by 2030, at a CAGR of 4.73% during the forecast period (2025-2030). Demographic momentum, rapid urbanization, and the gradual dismantling of intra-African tariffs are stimulating demand for ready-to-wear apparel, medical disposables, and technical fabrics. Foreign investors are responding with selective projects clustered in industrial parks that guarantee low-cost power and streamlined customs, yet the continent’s competitiveness still trails Asian hubs because of fragile logistics, fragmented supply chains, and skills gaps. Polyester remains the dominant raw material, but recycled fiber projects in Kenya, South Africa, and Ghana signal a pivot toward circular sourcing. Nigeria leads consumption, Ethiopia anchors export-oriented clusters, and South Africa retains niche strengths in wool and automotive textiles.

Key Report Takeaways

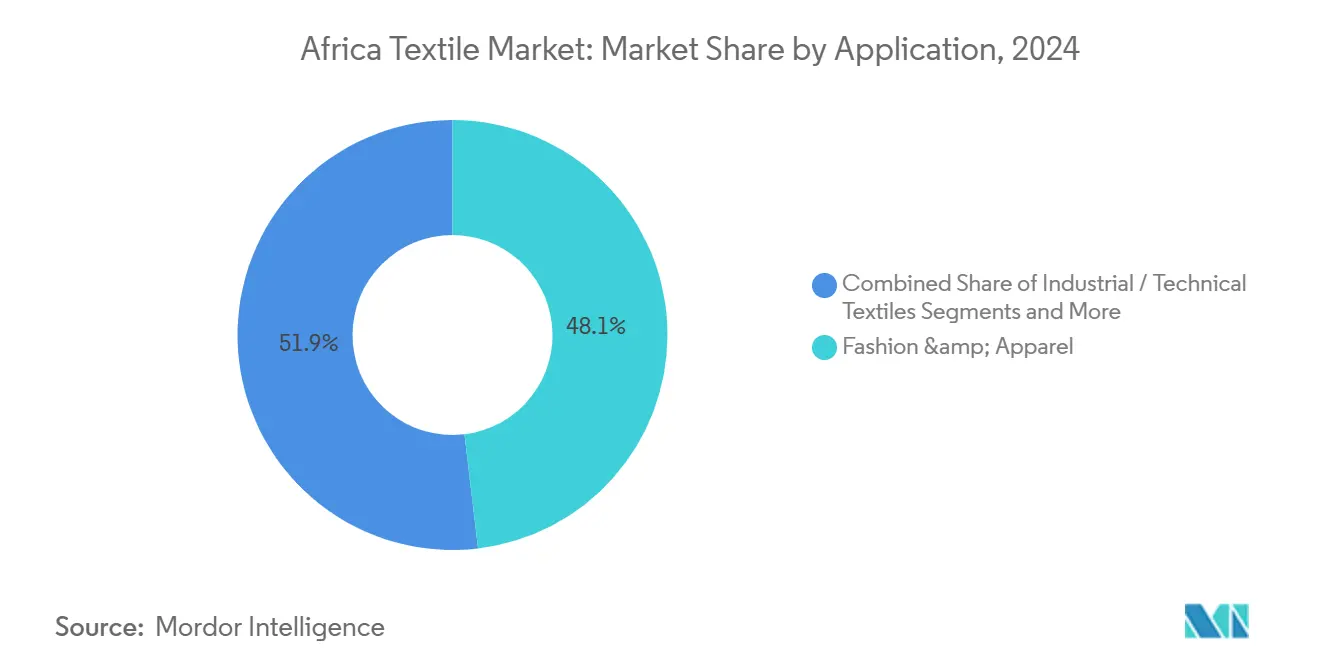

- By application, fashion & apparel captured 48.1% of the Africa textile market share in 2024, whereas medical & healthcare textiles are projected to grow the fastest at a 5.71% CAGR through 2030.

- By raw material, synthetic fibers commanded 46.8% of the Africa textile market size in 2024, while recycled fibers are slated to expand at a 6.02% CAGR to 2030.

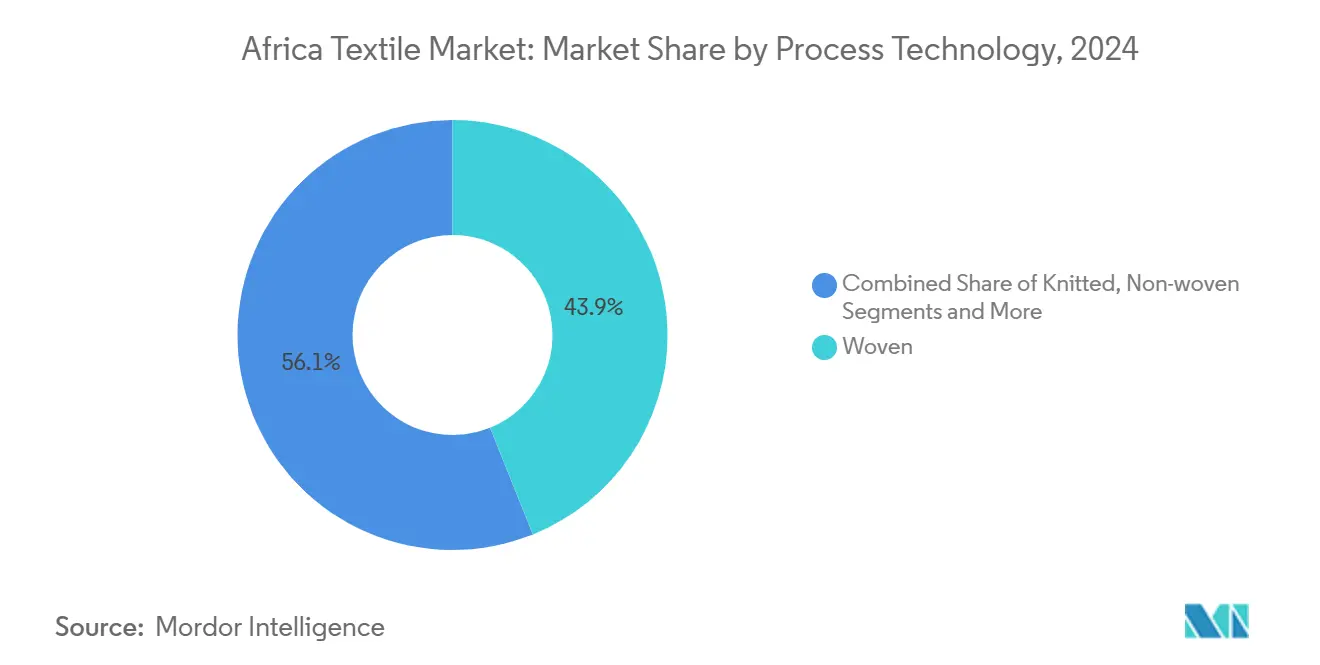

- By process, woven fabrics held 43.9% of the Africa textile market share in 2024 and 3-D weaving & spacer fabrics are advancing at a 5.98% CAGR through 2030.

- By geography, Nigeria accounted for 29.1% of the Africa textile market size in 2024 and is also the fastest-growing major country at a 6.34% CAGR to 2030.

Africa Textile Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Apparel demand growth from young, urbanizing population boosting domestic consumption | +1.2% | Nigeria, Kenya, Ethiopia, Tanzania, Ghana, Egypt | Medium term (2-4 years) |

| AfCFTA reducing trade barriers and enabling regional value chains for yarn, fabric, and garments | +0.9% | Continent-wide with early gains in East and West Africa | Long term (≥ 4 years) |

| Nearshoring/China+1 opening opportunities in basics, workwear, and fast-turnaround orders | +0.7% | Ethiopia, Kenya, Lesotho, Madagascar, Egypt, Tunisia | Medium term (2-4 years) |

| Cotton cultivation potential and agro-processing initiatives supporting upstream integration | +0.5% | Benin, Burkina Faso, Mali, Côte d’Ivoire, Tanzania, Uganda, Nigeria | Long term (≥ 4 years) |

| Industrial parks/SEZs with incentives attracting FDI in spinning, weaving, and CMT | +0.8% | Ethiopia, Kenya, Ghana, Togo, Nigeria, Egypt | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Apparel Demand Growth From Young, Urbanizing Population Boosting Domestic Consumption

Africa’s median age hovers below 20 years and urban centers are expanding quickly, creating a structural rise in discretionary spending on clothing and footwear. Real GDP growth above 4% in Ethiopia, Tanzania, and Uganda is translating into higher per-capita textile outlays as households pivot from informal tailoring to branded ready-to-wear[1]International Cotton Advisory Committee, “World Textile Demand 2024,” icac.org . Nigeria’s near-term macro headwinds have dampened demand, but its 220 million consumers and widening e-commerce penetration underpin medium-term upside once currency stability returns. Kenya’s urban population crossed 30% in 2024, and mobile payments are lowering retail frictions, letting micro-merchants replenish inventory faster. Digital channels, combined with youthful demographics, anchor a consumption story that is difficult to replicate in aging developed markets.

AfCFTA Reducing Trade Barriers and Enabling Regional Value Chains for Yarn, Fabric, and Garments

The African Continental Free Trade Area began tariff-free trading in 2021 and its rules of origin for textiles now allow yarn, fabric, and garments to circulate duty-free among signatories[2]Africa Finance Corporation, “AFC Signs Joint Declaration with UNIDO,” africafc.org . Benin’s Glo-Djigbé zone already turns local cotton into leggings shipped to French retailer Kiabi, illustrating a regional loop once dominated by Asian intermediaries. East African garment makers are shifting fabric sourcing from China to Tanzania and Kenya, trimming lead times by several weeks. Full benefit hinges on digitized customs and north-south freight corridors, but early adopters are already pocketing procurement savings and faster time-to-market.

Nearshoring/China+1 Opening Opportunities in Basics, Workwear, and Fast-Turnaround Orders

Geopolitical tension and tariff risk are nudging global buyers to place a slice of orders outside China, and industrial parks such as Hawassa in Ethiopia are vying for that flow. PVH sources USD 100 million of apparel annually from Hawassa, leveraging renewable power priced at USD 0.03 per kWh and duty-free access to the EU and U.S.. IFC has financed new factories in Togo and Kenya that will jointly add more than 8,000 jobs and focus on basics and workwear where quick replenishment is priceless[3]International Finance Corporation, “IFC Partners With Kenya’s Royal Apparel EPZ,” ifc.org . While logistics costs restrain higher-margin fashion categories, the China+1 trend is carving a realistic niche for Africa in fast-turnaround programs.

Cotton Cultivation Potential and Agro-Processing Initiatives Supporting Upstream Integration

West Africa ships roughly 1.5 million t of cotton lint each year yet converts less than 10% locally, surrendering most of the value chain. Contract farming pilots in Benin and Burkina Faso show that aggregator models can lift yields and assure mill feedstock. Ethiopia has over 3 million ha of suitable land but cultivates just a fraction; policy now prioritizes improved seed and ginning efficiency to widen raw-material security. Retailers seeking fully traceable supply are funding pre-harvest inputs and sustainability certifications, inching the region closer to integrated spinning-to-garment ecosystems.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics and energy costs plus unreliable power undermining competitiveness | -0.6% | Ethiopia, Uganda, Rwanda, Zambia, Zimbabwe, Nigeria, Ghana | Short term (≤ 2 years) |

| Skills gaps, limited machinery modernization, and QA/certification hurdles for exports | -0.5% | Kenya, Tanzania, Ethiopia, Nigeria, Ghana | Medium term (2-4 years) |

| Policy volatility, customs delays, and second-hand imports pressuring formal manufacturers | -0.4% | Kenya, Uganda, Tanzania, Ghana, Nigeria, South Africa, Zimbabwe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Logistics and Energy Costs Plus Unreliable Power Undermining Competitiveness

A 40-ft container from Kampala to Mombasa can cost more than USD 2,000, erasing margin for yarn and fabric imports. Customs paperwork still averages 44 days in Ethiopia, missing fast-fashion lead-time windows. Nigerian mills run diesel generators for up to 40% of operating hours, inflating conversion costs by 15-25%. South African factories install rooftop solar to dodge brownouts, but smaller firms lack the capital for such fixes. Without grid upgrades and transport corridors, the Africa textile market will continue paying a competitiveness tax versus Asian rivals.

Skills Gaps, Limited Machinery Modernization, and QA/Certification Hurdles for Exports

Seven in ten Kenyan textile employers cannot source multi-skilled machine operators, and most vocational institutes still train on outdated domestic machines. Ethiopia’s accreditation body lacks global recognition, limiting exporter credibility for OEKO-TEX and GOTS audits. Modern looms and dyeing equipment are scarce, prolonging learning curves and elevating defect rates. South Africa’s wool sector shows certification can scale—43% of output met RWS criteria in 2024—but replicating that success elsewhere demands coordinated curriculum design, equipment grants, and subsidized audit fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Medical Textiles Scale Up From a Small Base

Fashion & apparel claimed 48.1% of the Africa textile market share in 2024 as rising incomes funneled discretionary spending toward branded garments and footwear. Medical & healthcare textiles, though starting from a smaller base, are forecast to log the fastest 5.71% CAGR to 2030. Nigeria, Kenya, and Ethiopia are building hospitals under public-private frameworks that standardize demand for surgical drapes, fluid-repellent gowns, and certified wound dressings. Pandemic-era reforms further institutionalized bulk procurement of PPE, prompting IFC-backed factories in Ghana and Kenya to add clean-room lines targeting ISO 13485 compliance. As donor-funded health programs embed strict quality thresholds, local manufacturers that invest in testing labs and sterile environments can capture higher margin than commodity apparel makers.

Technical and industrial fabrics power the second growth vector. Automotive seat-cover orders in South Africa require abrasion-resistant 3-D woven structures, and mining firms across Zambia and Botswana specify flame-retardant filtration media. Hotel construction in Mauritius and coastal Kenya lifts household bedding and upholstery demand, while protective sportswear edges upward with greater athlete visibility at global events. Collectively, these niches diversify the revenue mix and raise average selling prices, cushioning the sector against fast-fashion volatility.

By Raw Material: Recycled Fibers Edge Into Mainstream

Synthetic fibers, chiefly polyester, represented 46.8% of consumption in 2024, reflecting price advantage and established supply chains. Recycled fibers are on track for a 6.02% CAGR through 2030, catalyzed by brand sustainability pledges and PET-to-fiber plants under construction in Nairobi, Johannesburg, and Accra. DTRT Apparel in Ghana, with IFC advisory support, plans a polymerization unit that will spin recycled yarn for its own garment lines, reducing dependence on Asian imports. Cotton retains cultural relevance, and West Africa’s 1.5 million t lint output positions the region as a potential upstream anchor, but translating raw lint into local yarn remains limited by ginning inefficiencies and high power tariffs.

Global retailers now demand certified inputs such as Responsible Wool Standard wool, which 43% of South African output already holds, enabling premium pricing. Chemical recycling technologies—glycolysis for PET and hydrolysis for nylon—are maturing, yet capital costs and solvent recovery hurdles delay scale-up. As a result, the Africa textile market operates a dual-track system in which low-margin virgin synthetics coexist with premium, certified, or recycled fibers that offer better economics for compliant exporters.

By Process/Technology: 3-D Weaving Finds Automotive Sweet Spot

Woven fabrics accounted for 43.9% of 2024 output, anchored by cotton shirting and household linens produced on shuttle and rapier looms across Nigeria, Ethiopia, Kenya, and Egypt. The 3-D weaving & spacer fabric segment will outpace the field at a 5.98% CAGR through 2030 as South African OEMs shift to lightweight seat architecture. Spacer fabrics deliver breathability, weight savings, and flame resistance essential for electric vehicle platforms and therefore command higher margins than standard knits.

Circular knitting dominates T-shirts and underwear in Kenya’s EPZs, prized for rapid line changeovers that suit fast-fashion replenishment. Nonwovens see brisk growth in medical disposables; Ontex’s diaper plant in Hawassa sources spun-melt polypropylene webs to satisfy East African hygiene demand. Capital intensity limits the spread of melt-blown lines, but where polymer feedstock and cheap power intersect—such as Ethiopia’s hydropower corridor—projects become bankable. Overall, process diversification is shifting value away from commodity weaves toward engineered structures that integrate function and sustainability.

Geography Analysis

Nigeria led the Africa textile market in 2024 with 29.1% share and is projected to expand at a robust 6.34% CAGR through 2030, buoyed by cotton incentives and the phased rollout of Aba and Kano clusters. Execution risks remain—smuggling, erratic power, and foreign-exchange shortages—but domestic demand from 220 million people offers unmatched scale once macro stability returns.

Egypt combines long-staple cotton heritage with proximity to Europe, leveraging the EU-Egypt Association Agreement to sustain spinning and finishing exports. Machinery modernization is underway, but Turkish and Asian imports still pressure local mills on cost. South Africa’s sector has shrunk yet occupies premium niches in wool, mohair, and automotive textiles; 43% of national wool output held RWS certification in 2024, supporting European luxury contracts.

Rest-of-Africa markets are splitting into export enclaves and consumption hubs. Ethiopia’s Hawassa park targets USD 1 billion in annual exports at full capacity, employing 25,000 workers and leveraging near-zero-cost hydropower. Kenya’s EPZs, backed by IFC lending, added 3,700 new jobs in 2025, while Ghana’s DTRT Apparel secured USD 8 million to integrate recycled fiber spinning. Togo, Lesotho, Madagascar, and Eswatini capitalize on AGOA and EU duty-free windows, though high freight costs curb scale. Without seamless AfCFTA corridors, the continent risks perpetuating isolated pockets of excellence rather than cohesive value chains.

Competitive Landscape

Competition is highly fragmented: no firm controls more than 5% of continental turnover, and thousands of informal tailors coexist with vertically integrated parks. Export-oriented enclaves in Ethiopia, Kenya, and Ghana display early buyer-driven consolidation because WRAP, OEKO-TEX, and LEED certifications are non-negotiable for audits, favoring larger, well-capitalized operators. Domestic fabric markets in Nigeria and Ghana remain atomized, with quality differentiation minimal and price wars common.

Strategic plays revolve around vertical integration and anchor-buyer models. ARISE IIP’s Glo-Djigbé zone compresses ginning, spinning, weaving, and garment assembly on a single campus, letting U.S. retailers source fully traceable Benin-made leggings. PVH’s USD 100 million annual commitment at Hawassa attracted 18 suppliers, proving that guaranteed offtake unlocks foreign direct investment. IFC-backed factories in Togo and Kenya are bundling automation and renewable energy to trim lead times and achieve EDGE certification, positioning themselves for near-shoring programs.

Technology adoption is uneven. Ethiopia’s zero-liquid-discharge plant sets an environmental benchmark, while many Nigerian mills still rely on open-ditch effluent disposal. South Africa’s wool and mohair producers leverage RWS and RMS certification for luxury premiums, but most Sub-Saharan spinners lack ISO 9001 or OEKO-TEX accreditation, curbing EU market access. This bifurcation is expected to widen as extended producer responsibility laws and retailer traceability portals gain traction.

Africa Textile Industry Leaders

CIEL Textile Ltd

Mediterranean Textile Company SAE

Almeda Textile Factory Plc

Truworths International Ltd

Rivatex East Africa Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: IFC extended a USD 15 million package to Kenya’s Royal Apparel EPZ to build an EDGE-certified factory that will create 3,700 jobs and adopt renewable power.

- November 2024: IFC loaned USD 8 million to DTRT Apparel in Ghana to expand capacity and pilot recycled-fiber spinning.

- July 2024: Star Garments secured USD 15 million from IFC to construct Togo’s first large-scale apparel plant, projected to add 4,520 jobs and tap local cotton.

- June 2024: Africa Finance Corporation signed a pact with UNIDO, WTO, and others to establish regional textile hubs that leverage West African cotton.

Africa Textile Market Report Scope

By Application

| Fashion & Apparel |

| Industrial / Technical Textiles |

| Household & Home Textiles |

| Medical & Healthcare Textiles |

| Automotive & Transport Textiles |

| Others (Protective, Sports, etc.) |

By Raw Material

| Natural Fibres | Cotton |

| Wool | |

| Silk | |

| Synthetic Fibres | Polyester |

| Nylon | |

| Rayon / Viscose | |

| Acrylic | |

| Polypropylene | |

| Recycled Fibres | |

| Others (Aramid, Carbon, UHMWPE) |

By Process / Technology

| Woven | |

| Knitted | |

| Non-woven | Spun-laid (Spunbond / Melt-blown) |

| Dry-laid Hydro-entangled | |

| Wet-laid | |

| Needle-punched | |

| 3-D Weaving & Spacer Fabrics |

By Country

| Nigeria |

| Egypt |

| South Africa |

| Rest of Africa |

| By Application | Fashion & Apparel | |

| Industrial / Technical Textiles | ||

| Household & Home Textiles | ||

| Medical & Healthcare Textiles | ||

| Automotive & Transport Textiles | ||

| Others (Protective, Sports, etc.) | ||

| By Raw Material | Natural Fibres | Cotton |

| Wool | ||

| Silk | ||

| Synthetic Fibres | Polyester | |

| Nylon | ||

| Rayon / Viscose | ||

| Acrylic | ||

| Polypropylene | ||

| Recycled Fibres | ||

| Others (Aramid, Carbon, UHMWPE) | ||

| By Process / Technology | Woven | |

| Knitted | ||

| Non-woven | Spun-laid (Spunbond / Melt-blown) | |

| Dry-laid Hydro-entangled | ||

| Wet-laid | ||

| Needle-punched | ||

| 3-D Weaving & Spacer Fabrics | ||

| By Country | Nigeria | |

| Egypt | ||

| South Africa | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa textile market?

The sector was valued at USD 39.21 billion in 2025 and is forecast to reach USD 49.41 billion by 2030.

Which country leads consumption within Africa’s textile arena?

Nigeria accounted for 29.1% of 2024 demand and is projected to maintain the lead with a 6.34% CAGR through 2030.

Which application is expanding the fastest?

Medical & healthcare textiles will grow at a 5.71% CAGR, outpacing all other end-use segments.

How significant are recycled fibers in the raw-material mix?

While still small, recycled fibers are expected to record a 6.02% CAGR, the quickest among raw-material groups.

What are the main challenges limiting Africa’s textile competitiveness?

High logistics costs, unstable power, skills shortages, and policy volatility collectively subtract up to 1.5 percentage points from potential CAGR.

How is AfCFTA influencing the regional textile landscape?

The trade pact is lowering tariffs and lead times, enabling yarn and fabric to move duty-free among member states, which strengthens intra-African value chains.

Page last updated on: