Africa ESIM Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

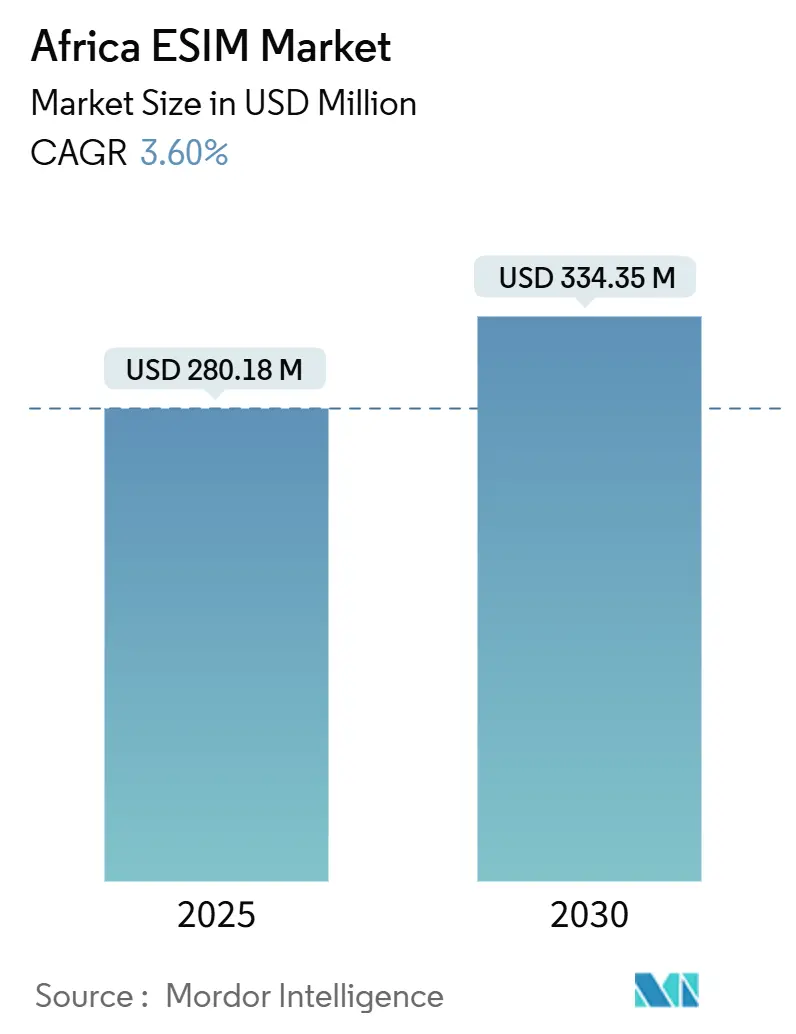

| Market Size (2025) | USD 280.18 Million |

| Market Size (2030) | USD 334.35 Million |

| Growth Rate (2025 - 2030) | 3.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa ESIM Market Analysis by Mordor Intelligence

The Africa ESIM Market size is estimated at USD 280.18 million in 2025, and is expected to reach USD 334.35 million by 2030, at a CAGR of 3.60% during the forecast period (2025-2030).

Rising 5G site density in 16 countries, rapid digital-only SIM launches by tier-1 operators, and recurring revenue from subscription-management platforms underpin steady expansion. The bulk of revenue still comes from hardware because automotive and industrial users demand high-temperature MFF2 chips, yet the fastest growth shifts to cloud-native provisioning services that collect a fee each time a device switches carriers. Dual-SIM smartphones below USD 200 sustain volume momentum, while wearables, utility meters, and vehicle telematics widen the addressable base. Competitive tension increases as smaller carriers deploy eSIM to differentiate on cross-border roaming, although patchy regulatory frameworks in Nigeria, Ghana, and Tanzania delay mass onboarding.

Key Report Takeaways

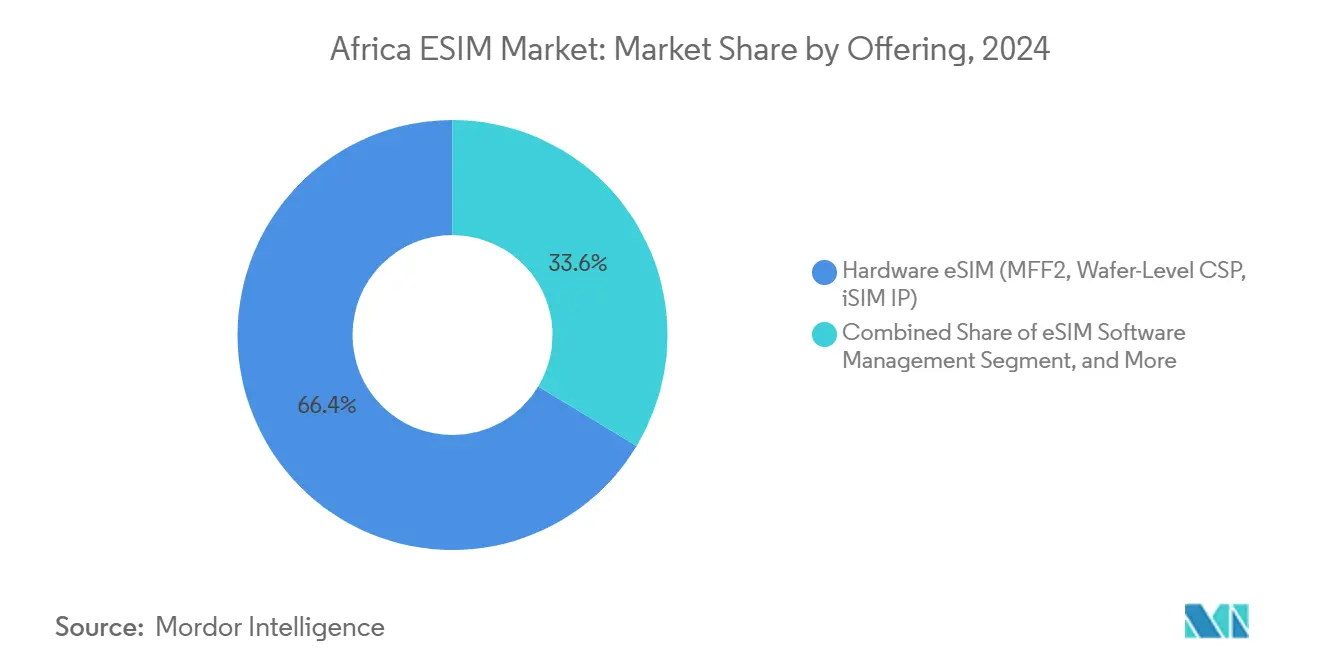

- By offering, hardware commanded 66.37% of Africa eSIM market share in 2024, while remote SIM provisioning services are set to post an 11.10% CAGR through 2030.

- By device type, smartphones and feature phones held 76.66% of Africa eSIM market share in 2024, whereas wearables are projected to expand at a 12.19% CAGR to 2030.

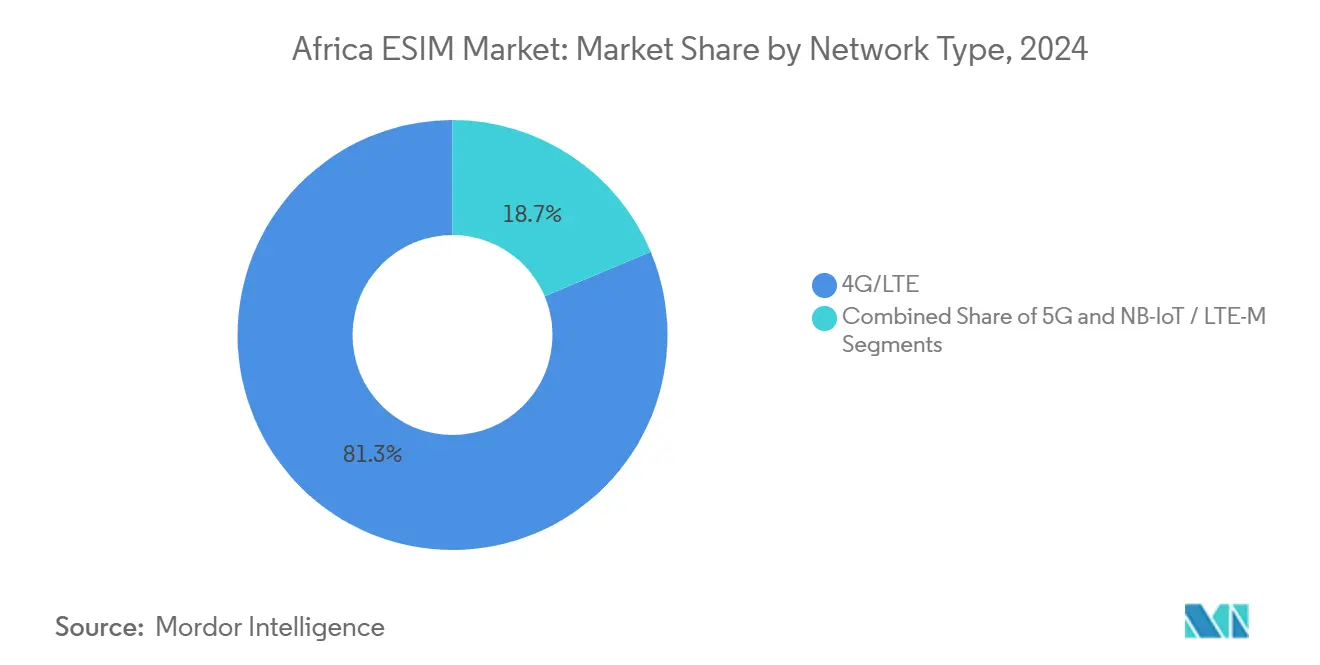

- By network type, 4G and LTE accounted for 81.32% share of the Africa eSIM market size in 2024, and NB-IoT + LTE-M connections will rise at a 16.17% CAGR through 2030.

- By end-user industry, consumer electronics captured 71.48% share of the Africa eSIM market size in 2024, while industrial and manufacturing exhibits a 15.58% CAGR to 2030.

- By geography, South Africa led with 19.20% of Africa eSIM market share in 2024, whereas Kenya records the highest growth at 6.90% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa ESIM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G network coverage | +0.9% | South Africa, Kenya, Nigeria, Egypt, Morocco | Medium term (2-4 years) |

| IoT-based utility metering and smart cities | +0.8% | South Africa, Kenya, Nigeria, Ghana, Tanzania | Long term (≥ 4 years) |

| Digital-identity programs for remote onboarding | +0.6% | Egypt, Kenya, South Africa, Morocco | Medium term (2-4 years) |

| OEM push for sub-USD 200 dual-SIM devices | +0.7% | Nigeria, Kenya, Ghana, Tanzania, Rest of Africa | Short term (≤ 2 years) |

| Roaming-cost optimisation for diaspora travel | +0.4% | South Africa, Nigeria, Kenya | Short term (≤ 2 years) |

| Satellite–cellular convergence in mining | +0.3% | South Africa, Tanzania, Zambia, Rest of Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5G Network Coverage Across Key African Metros

Safaricom has deployed 1,114 5G base stations, which now reach 14% of Kenya’s population, while MTN Nigeria covers 11.3% of its market.[1]Ericsson, “Mobility Report,” ericsson.com The GSMA counts 27 operators with commercial 5G in 16 African states, yet fewer than 10 offer eSIM, showing that radio upgrades alone do not trigger digital SIM take-up. Urban centers such as Johannesburg, Nairobi, and Lagos enable eSIM-based cloud gaming and augmented-reality services, whereas rural zones remain anchored to 4G, capping premium addressable demand. Operators prioritize fixed-wireless broadband because home internet ARPUs exceed smartphone data by 40%, which slows consumer eSIM inflection. Orange completed the national 4G rollout in the Central African Republic in early 2025, focusing on subscriber scale first, and deferring the deployment of dense 5G layers that would spur eSIM monetization.[2]Orange Business, “Smart Metering in Africa,” orangebusiness.com

Growing Adoption of IoT-Based Utility-Metering and Smart-City Projects

Orange Energies installed 300,000 prepaid smart meters across 12 African countries and reduced electricity theft losses by 18% through an eSIM-enabled pay-as-you-go service. Sigfox South Africa won a 15 million smart water meter mandate under regulation RT29, converting compliance into a growth engine for eSIM sensors. Ethio Telecom’s Smart Bahir Dar pilot connects traffic lights and waste bins; however, the absence of an eSIM forces factory pre-provisioning, which adds six weeks to the deployment. MTN manages 2.3 million IoT connections, but only 12% of these use eSIM, as smaller municipalities often lack the necessary subscription-management software. Fragmented procurement keeps each ministry tied to its own carrier, blunting economies of scale that would justify wider eSIM use.

Government-Backed Digital-Identity Programs Enabling Remote eSIM Onboarding

Egypt’s regulator approved eSIM in 2024 and linked activation to the national ID database, allowing Orange Egypt to onboard subscribers using facial recognition. Kenya’s Huduma Namba system supports Safaricom’s remote provisioning, although it currently covers only 38 million of the 54 million residents. South Africa is piloting a digital ID card that embeds eSIM credentials, potentially consolidating identity checks and SIM issuance into a single token; however, civil-liberty concerns may slow the rollout. Morocco registered 12 million citizens on its eID platform in 2024; however, operators have not yet completed integrating remote provisioning, underscoring the difference between regulatory readiness and commercial execution.

OEM Push for Dual-SIM and eSIM-Only Smartphones Below USD 200

Huawei introduced Watch Fit 4 at KES 19,999 (USD 154) with a standalone eSIM, whereas the entry Band 10 omits cellular to hit KES 6,999 (USD 54). Airtel Africa reports a 41.4% smartphone penetration across 14 markets, yet 68% of new handsets still retail for under USD 150, a range where OEMs often skip eSIM to contain the bill of materials. Telkom South Africa reaches 70% smartphone penetration because contract subsidies pair eSIM phones with 24-month data plans, a credit model that Nigeria and Kenya lack. STMicroelectronics achieved a wafer-level cost of USD 0.80 with its ST4SIM-300 in 2024, clearing the price hurdle for sub-USD 100 eSIM feature phones. Operator hesitation also suppresses awareness, as only three in ten subscribers recognize the benefits of eSIM in recent GSMA surveys.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited eSIM support among Tier-2 and Tier-3 MNOs | −0.5% | Ghana, Tanzania, Uganda, Zambia, Senegal | Medium term (2-4 years) |

| Fragmented regulatory approaches | −0.4% | Nigeria, Ghana, Tanzania, Algeria | Short term (≤ 2 years) |

| Low handset-replacement cycle | −0.6% | Nigeria, Kenya, Ghana, Tanzania | Long term (≥ 4 years) |

| Cyber-security concerns around RSP platforms | −0.2% | South Africa, Kenya, Nigeria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited eSIM Provisioning Support Among Tier-2 and Tier-3 MNOs

Zamtel introduced eSIM in September 2024 for 3.2 million subscribers, representing only 8% of Zambia’s market, leaving most users with Airtel or MTN, which still rely on plastic SIMs. MTN South Sudan followed in January 2025, yet conflict limits handset imports that would unlock scale. Workz charges USD 0.15 per profile download, so a five-million-subscriber carrier pays USD 750,000 yearly before marketing outlays, a hurdle many Tier-2 players cannot clear.[3]Workz, “eSIM Cost Model,” workz.com Ghana’s smaller operators Glo and Expresso remain outside the eSIM ecosystem, which forces device makers to preload physical SIMs and locks users into incumbents. Only 18 of the 240 eSIM Discovery providers listed by the GSMA operate in sub-Saharan Africa, and most focus on enterprise IoT rather than mass-market smartphones.

Fragmented Regulatory Approaches to Remote SIM Provisioning

Egypt mandates that eSIM profiles include dual-line support tied to its national ID, while Nigeria has no framework, leaving operators unsure if remote onboarding conflicts with in-person SIM registration rules. Tanzania’s regulator has yet to publish guidelines, delaying launches by Vodacom and Airtel despite readiness from their parent companies, and costing each approximately 120,000 high-value subscribers per year who migrate to Kenyan or South African profiles. Ghana enforces biometric SIM registration but gives no clarity on whether facial recognition meets the standard for eSIM, exposing operators to legal risk. Algeria still blocks eSIM, forcing Orange to distribute plastic cards that clash with its pan-African digital strategy. The lack of harmonised GSMA standards forces OEMs to certify eSIMs country by country, adding nine months to product cycles and deterring smaller brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering – Hardware Dominates as Services Accelerate

Hardware contributed 66.37% of Africa eSIM market share in 2024, led by MFF2 chips and wafer-level packages that meet automotive and industrial temperature standards. Remote SIM provisioning services are expected to register an 11.10% CAGR to 2030 as operators pivot to subscription-management revenue streams that trigger fees with every profile switch. The Africa eSIM market size for hardware will still rise because vehicle telematics and industrial sensors embed tamper-proof silicon; however, the growth delta clearly favors cloud platforms. Giesecke+Devrient achieved GSMA SGP.32 v1.2 compliance in April 2025, removing vendor lock-in for IoT devices and accelerating service uptake. Kigen integrated its eIM framework into Vodafone’s IoT portal, showing how carrier-agnostic orchestration moves value from silicon to software.

The shift mirrors broader telecom models, where connectivity becomes software-defined and monetization migrates toward lifecycle management. BICS eSIM Hub offers multi-IMSI profiles across 700 networks, allowing African travelers to sidestep premium roaming tariffs. Workz exceeded 100 partner telcos with pay-as-you-grow pricing that matches carrier economics, lowering entry barriers for mid-tier operators. As pay-per-use paradigms spread, services will narrow but not completely close the revenue gap with hardware through the forecast window.

By Device Type – Wearables Outpace Smartphones

Smartphones and feature phones accounted for 76.66% of Africa eSIM market share in 2024 because dual-SIM handsets under USD 200 let users separate work and personal lines without swapping cards. Wearables are projected to post the strongest 12.19% CAGR to 2030 as urban consumers adopt cellular smartwatches for health tracking and contactless payments. Africa's eSIM market for wearables is expected to benefit from declining component costs and increasing wellness awareness among the middle class. Netstar operates a fleet of over 2 million vehicle telematics units that utilize eSIM to switch between MTN and Vodacom, demonstrating how enterprise devices extend beyond phones. Tablets and rugged laptops remain niche, but they are gaining traction in logistics and field service, thanks to improving 4G coverage across 71.6% of Airtel Africa’s footprint.

The replacement cycle remains a constraint because 91 million Airtel subscribers still carry feature phones that lack embedded SIM slots. STMicroelectronics pushed chip costs below USD 0.80, so low-end handsets are likely to add eSIM within the forecast period, shortening the lag between carrier capability and device availability.

By Network Type – NB-IoT Gains Despite Sparse Deployments

4G and LTE formed 81.32% of Africa eSIM market share in 2024 given operator focus on data-heavy smartphones. NB-IoT and LTE-M are projected to record a robust 16.17% CAGR to 2030, as utilities, mining companies, and municipalities adopt always-on sensors for metering and remote monitoring. Only Safaricom and Vodacom currently operate NB-IoT in Africa, highlighting a mismatch between 5G marketing narratives and the low-power backhaul that enterprises need. Sigfox secured a 15 million smart water meter contract with a proprietary network, proving that utilities will use non-cellular options when carriers lag.

High 5G capex favors metro smartphone coverage over machine-type communications. The GSMA estimates eSIM will account for 37% of African IoT connections by 2030, yet that assumes NB-IoT deployments triple by 2027—a projection contingent on spectrum policy reform. Until then, enterprises blend 2G fallback, satellite overlays, and proprietary LPWA to bridge the gap.

By End-User Industry – Industrial IoT Accelerates

Consumer electronics dominated with 71.48% of Africa eSIM market size in 2024, driven by handset and wearable shipments. Industrial and manufacturing exhibits a 15.58% CAGR as factories adopt predictive-maintenance sensors that depend on reliable, low-latency links. Africa eSIM market size for industrial use rises in parallel with programs such as Vodacom IoT’s asset monitoring across South Africa and Mozambique. Automotive telematics remains a key niche, with Netstar showing that eSIM-based carrier switching can cut downtime by 18%. Logistics companies leverage multi-IMSI profiles from CommsCloud to reduce cross-border roaming by 70%.

Utilities continue to lead machine-to-machine volume. Orange Energies uses eSIM to curb electricity theft and support pay-as-you-go solar plans, demonstrating measurable ROI that encourages further deployments. Healthcare contributes modest volume today, yet eSIM-connected glucometers and blood-pressure cuffs enhance telemedicine programs, hinting at future growth once reimbursement models mature.

Geography Analysis

South Africa held 19.20% of Africa eSIM market share in 2024, powered by Vodacom and MTN dual consumer–IoT offerings and Telkom’s 70% smartphone penetration among 17.5 million customers. The Independent Communications Authority allows email verification for activation, eliminating store visits and widening adoption. Vodacom reported USD 3.63 billion revenue in H1 FY2025 and operates 588 5G sites that enable cloud gaming and augmented-reality apps reliant on eSIM. Government mandates also stimulate volume, as regulation RT29 drives 15 million eSIM smart water meters through Sigfox.

Kenya grows fastest at 6.90% CAGR to 2030, benefiting from Safaricom’s 1,114 5G and two national NB-IoT sites plus January 2025 eSIM launch. Huduma Namba digital identity enables remote onboarding, although rural gaps persist. Huawei’s Watch Fit 4 at USD 154 targets Nairobi’s middle class and exemplifies how wearables broaden demand. Nigeria hosts Africa’s largest subscriber base at 78 million for MTN, but eSIM uptake lags because the regulator has not finalized remote provisioning rules.

Egypt approved eSIM in 2024 and Orange Egypt now supports up to 10 lines per device, focusing on expatriates and business users. Morocco rolled out digital IDs to 12 million citizens, yet operators have not integrated remote onboarding fully. Zamtel’s September 2024 launch made Zambia the first in its region, though market impact is limited by 3.2 million subscribers. MTN South Sudan introduced eSIM in January 2025 but faces logistical hurdles from ongoing conflict. Collectively, rest-of-continent markets expand as proof-of-concept deployments push incumbents to follow.

Competitive Landscape

Africa eSIM market sits at moderate concentration. Tier-1 operators MTN, Vodacom, Orange, Airtel Africa, and Safaricom hold scale advantages in provisioning platforms and subscriber bases. Smaller entrants such as Zamtel and MTN South Sudan chip away at niches like freight corridors and diaspora travel, adding fragmentation. Giesecke+Devrient secured first GSMA SGP.32 compliance in April 2025, which slashes sensor deployment cycles by six weeks and shifts negotiation power toward hardware-agnostic subscription platforms. Thales integrated eSIM Discovery into Android, giving one-click activation across 240 providers and raising the bar for user experience.

Three white-space arenas stand out. Satellite–cellular hybrid offers from emnify keep mining and energy sites connected beyond terrestrial reach. Wearables appeal to urban professionals seeking untethered health tracking, with Huawei and Apple poised to ramp local SKUs. Smart-meter mandates create volume for IoT modules where Quectel and Kigen supply silicon to MTN and Vodacom. Workz leads the platform race among independents by pricing per profile, which aligns with operator economics as they try to contain up-front capex. Standardization under SGP.32 reduces vendor lock-in and lets enterprises switch carriers based on coverage matrices, eroding the defensive moat that operators held for decades.

Africa ESIM Industry Leaders

MTN Group Limited

Vodacom Group Limited

Thales Group

IDEMIA Group

Giesecke+Devrient GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Giesecke+Devrient gained GSMA SGP.32 v1.2 compliance for IoT eUICC, enabling faster profile switches for industrial sensors.

- January 2025: MTN South Sudan launched eSIM for 2.1 million subscribers, targeting expatriates and business users.

- December 2024: Orange Egypt introduced eSIM with up to 10 lines per device, integrated with national ID verification.

- December 2024: Vodacom South Africa expanded eSIM holiday roaming across 36 African destinations.

Africa ESIM Market Report Scope

| Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software |

| Remote SIM Provisioning Services |

| Smartphones and Feature Phones |

| Tablets and Laptops |

| Wearables |

| M2M/IoT Modules |

| 5G |

| 4G/LTE |

| NB-IoT/LTE-M |

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Logistics and Asset Tracking |

| Energy and Utilities |

| Healthcare and Wearables |

| Algeria |

| Kenya |

| Morocco |

| South Africa |

| Nigeria |

| Ghana |

| Egypt |

| Tanzania |

| Rest of Africa (Tunisia, Uganda, Zambia, Senegal, Others) |

| By Offering | Hardware eSIM (MFF2, Wafer-Level CSP, iSIM IP) |

| eSIM Management Software | |

| Remote SIM Provisioning Services | |

| By Device Type | Smartphones and Feature Phones |

| Tablets and Laptops | |

| Wearables | |

| M2M/IoT Modules | |

| By Network Type | 5G |

| 4G/LTE | |

| NB-IoT/LTE-M | |

| By End-user Industry | Consumer Electronics |

| Automotive and Transportation | |

| Industrial and Manufacturing | |

| Logistics and Asset Tracking | |

| Energy and Utilities | |

| Healthcare and Wearables | |

| By Country | Algeria |

| Kenya | |

| Morocco | |

| South Africa | |

| Nigeria | |

| Ghana | |

| Egypt | |

| Tanzania | |

| Rest of Africa (Tunisia, Uganda, Zambia, Senegal, Others) |

Key Questions Answered in the Report

How much is the Africa eSIM market worth in 2025 and what is its CAGR to 2030?

Africa eSIM market size stands at USD 280.18 million in 2025 and is projected to grow at a 3.60% CAGR to reach USD 334.35 million by 2030.

Which country leads eSIM revenue in Africa?

South Africa held 19.20% of total revenue in 2024 due to high smartphone penetration and clear onboarding rules.

Which segment grows fastest within the Africa eSIM space?

NB-IoT and LTE-M connections rise at a 16.17% CAGR as utilities and mining firms deploy low-power sensors.

Why do wearables matter for African operators?

Wearables record a 12.19% CAGR because urban consumers adopt cellular smartwatches for health tracking and contactless payments.

What is the biggest barrier to eSIM in Africa?

Fragmented regulation and limited Tier-2 carrier support slow remote provisioning across key markets such as Nigeria and Tanzania.

Which companies dominate provisioning platforms?

MTN, Vodacom, Orange, Airtel Africa, and Safaricom control most platforms, though new entrants like Workz and Kigen are gaining ground.

Page last updated on: