Afghanistan Data Center Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

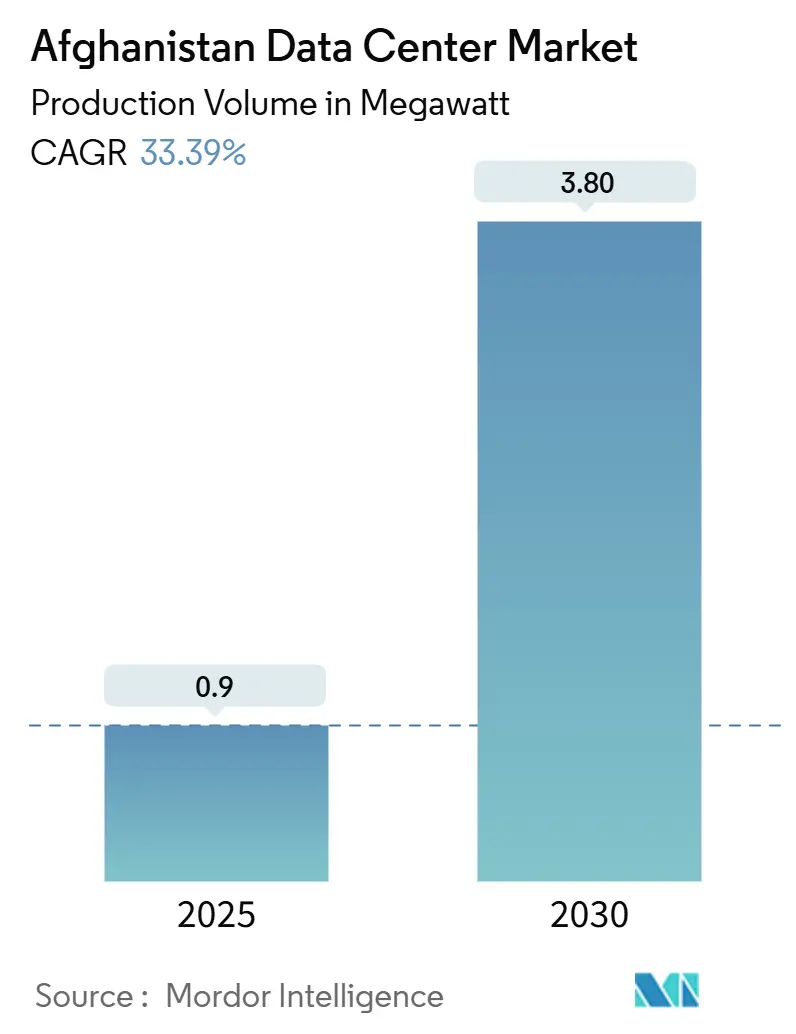

| Market Volume (2025) | 0.9 megawatt |

| Market Volume (2030) | 3.80 megawatt |

| Growth Rate (2025 - 2030) | 33.39% CAGR |

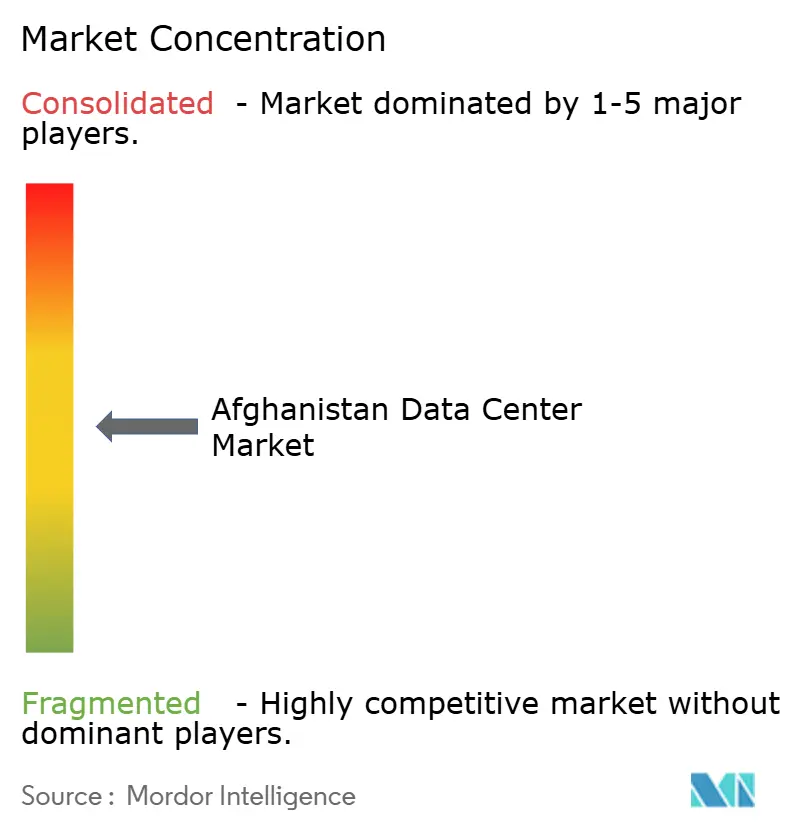

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Afghanistan Data Center Market Analysis by Mordor Intelligence

The Afghanistan data center market size reached 0.9 MW in 2025 and is forecast to climb to 3.8 MW by 2030, reflecting a CAGR of 33.39% and underscoring the country’s accelerating digital-first agenda. A confluence of sizable international funding for backbone networks, rapid 4G uptake, and early preparations for 5G is reshaping national connectivity patterns and creating sustained demand for new white-space capacity. Government programs such as Digital Afghanistan and Digital CASA are anchoring data-localization rules that compel critical workloads to remain onshore, while cross-border fiber corridors are lowering latency and positioning the country as an emerging transit hub between Central and South Asia. Financial settlements with power-exporting neighbors, expanding renewable imports, and targeted investments in back-up generation are gradually mitigating electricity-reliability concerns that previously impeded facility uptime. Meanwhile, telecom operators are densifying edge points of presence to manage exploding mobile-data traffic, prompting cloud providers and hyperscalers to explore in-country availability zones and interconnection partnerships.

Key Report Takeaways

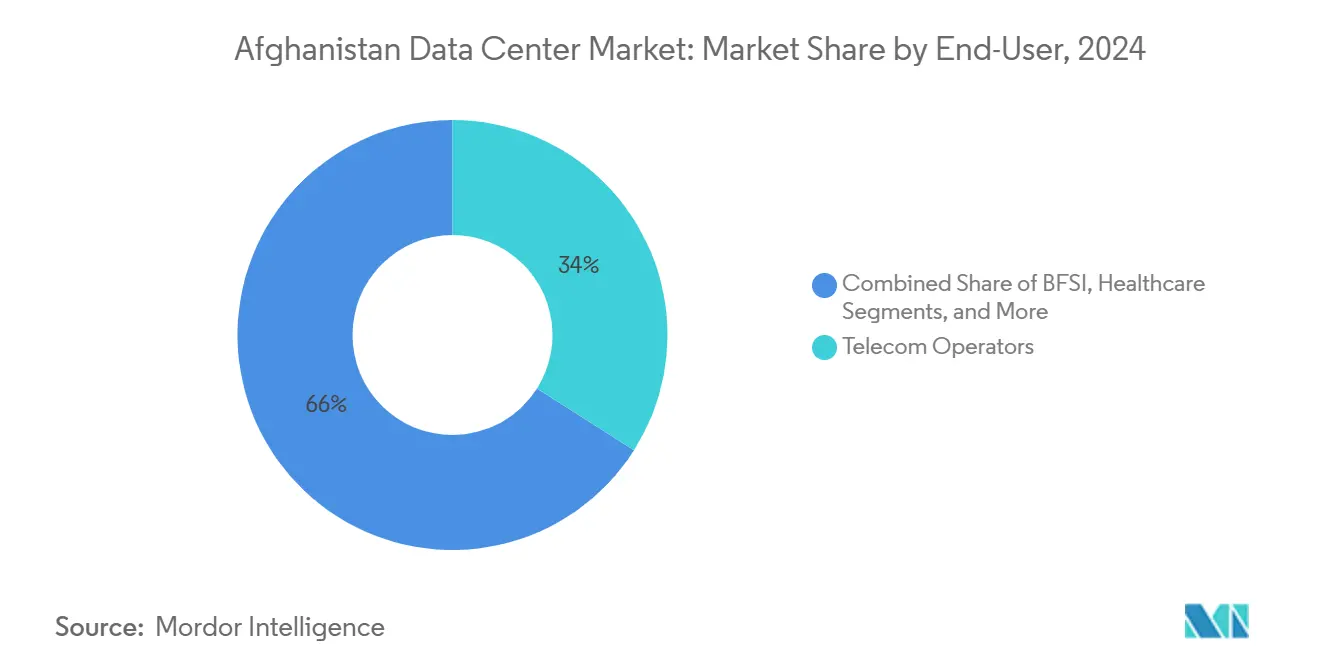

- By end-user, telecom operators held 34% of the Afghanistan data center market share in 2024, while cloud service providers and hyperscalers are projected to post the fastest 18.80% CAGR through 2030.

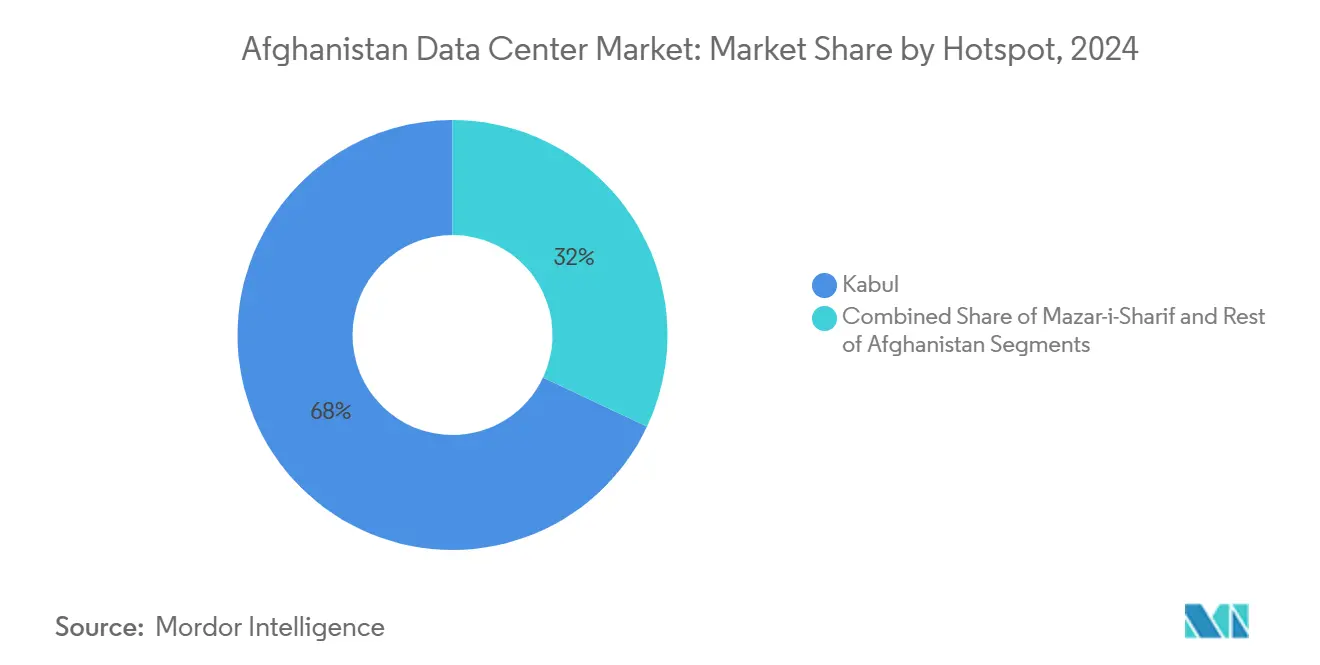

- By hotspot, Kabul commanded 68% of the Afghanistan data center market share in 2024; Mazar-i-Sharif is forecast to register the highest 20.20% CAGR to 2030.

Afghanistan Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive mobile-data growth and 4G/5G preparations | +8.50% | National, concentrated in Kabul and Mazar-i-Sharif | Medium term (2-4 years) |

| Digital CASA and Digital Afghanistan strategies driving data-localization | +7.20% | National, early gains in Kabul, Herat, Mazar-i-Sharif | Long term (≥ 4 years) |

| Cross-border fiber corridors slash latency | +6.80% | Regional corridors with national spill-over | Long term (≥ 4 years) |

| Starlink and other LEO gateway rollout enables nationwide edge compute | +4.30% | National, especially rural areas | Medium term (2-4 years) |

| IFC/MIGA de-risking for greenfield Tier III builds | +3.10% | Urban centers, chiefly Kabul and Mazar-i-Sharif | Short term (≤ 2 years) |

| Diaspora-backed fintech/OTT localization surge | +2.60% | Urban clusters nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Mobile-Data Growth and 4G/5G Preparations

Roshan’s USD 700 million network program has expanded 4G coverage to 91% of the population, and Afghan Telecom’s recent 2x5 MHz 1800 MHz spectrum win underscores operators’ intent to improve average throughput and latency benchmarks.[1]Roshan Corporate Communications, “About Roshan,” Roshan, roshan.af With smartphone penetration edging toward the 50% mark, national peak-hour traffic has doubled in two years, forcing operators to position micro-data centers closer to base-station clusters for content caching and call-detail record analytics. As Etisalat Afghanistan rolls out carrier-grade wholesale services across 21 provinces, customer-experience platforms and VPN gateways are shifting from offshore locations to local racks to satisfy data-sovereignty mandates. These developments necessitate incremental investments in climate-controlled edge booths and Tier III expansions in Kabul, Mazar-i-Sharif, and Herat, thereby securing low-latency paths for emerging 5G use cases, such as mobile gaming and live-video collaboration.

Digital CASA and Digital Afghanistan Strategies Driving Data-Localization

The USD 51 million Digital CASA-1 line of credit finances inland fiber rings, a national Internet Exchange Center, and sector-specific GovCloud blueprints, collectively enhancing the business case for domestic colocation.[2]World Bank Staff, “Afghanistan Digital CASA 1 Project,” World Bank, worldbank.org Under these frameworks, payment settlements processed by the Afghanistan Payments System must reside on Afghan soil, prompting banks to migrate their core banking disaster recovery instances to Kabul facilities. Education-sector e-learning repositories and Ministry of Health telemedicine platforms are also shifting from regional data hubs in the Gulf to in-country cabinets, accelerating rack sales and the uptake of managed services. Inter-operator peering at AFG-IX now allows 23 ISPs to exchange local traffic without rerouting via Frankfurt or Dubai, trimming transit unit costs by up to 60% and freeing opex budgets for new IT loads.

Cross-Border Fiber Corridors Slash Latency

The Wakhan-China spur and the 700 km TAPI fiber bundle are driving round-trip delay from Kabul to Singapore down below 110 ms, making Afghanistan attractive for near-edge content distribution serving Central Asian eyeballs. Redundant paths through CASA-1000 add route diversity toward Europe, a prerequisite for Tier III uptime thresholds. As wholesale bandwidth tariffs fall, enterprise ERP workloads previously hosted in Delhi are repatriating, while gaming publishers contemplate local mirrors to capture a youthful demographic that already spends 4 hours daily on mobile screens.

Starlink and Other LEO Gateway Rollout Enables Nationwide Edge Compute

LEO constellations promise sub-50 ms delays that unlock video consultation, digital cash transfers, and agricultural IoT sensor backhaul for villages cut off from fiber backbones. Pilot clusters powered by rooftop solar arrays demonstrate the feasibility of 40-foot containers hosting micro-racks that support regional hospital information systems and distance-education content stores. Each new gateway converts latent traffic into localized processing demand, encouraging microfinance institutions to launch agent-banking platforms that lean on in-country database replicas rather than offshore cloud instances.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid instability and chronic power deficits | -12.30% | Nationwide, acute in rural zones | Long term (≥ 4 years) |

| Political and security-linked insurance surcharges | -8.70% | Nationwide, conflict-prone districts | Medium term (2-4 years) |

| Acute brain-drain of Tier III/IV O and M engineers | -4.20% | Urban centers | Short term (≤ 2 years) |

| Sovereign credit-rating limits on long-tenor project finance | -3.80% | National, large builds | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Instability and Chronic Power Deficits

Electricity imports account for more than 70% of national consumption, and per-capita usage stands at 173 kWh, which is well below regional peers. This forces operators to deploy diesel gensets rated up to 1,250 kVA for every functional hall.[3]Low Carbon Power Research Team, “Energy Profile: Afghanistan,” Low Carbon Power, lowcarbonpower.org The recent clearance of USD 627 million in arrears has restored a 24-hour supply to Kabul industrial parks; however, sustained voltage fluctuations necessitate investment in double-conversion UPS stacks and modular battery strings sized for 15-minute autonomy. Vertiv SmartCabinet footprints and Schneider Electric Galaxy VS units are now standard in greenfield pods; however, fuel logistics risk continues to weigh on site-selection criteria outside the capital.

Political and Security-Linked Insurance Surcharges

Premiums on construction, marine-cargo, and terrorism cover remain 15-25% higher than benchmarks in neighboring land-locked states, elongating ROI breakeven horizons. MTN’s 2025 exit underlines external investors’ caution and amplifies the importance of IFC/MIGA wraps that backstop greenfield Tier III ventures for tenors beyond seven years. Although sabotage incidents against backhaul towers have fallen since mid-2024, investors still demand layered surveillance and rapid-response teams, adding 2-3 percentage points to total capex.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Telecom operators consolidate mission-critical loads

Telecom operators accounted for 34% of Afghanistan data center market share in 2024, reflecting their status as anchor tenants that operate OSS/BSS systems, customer analytics, and mobile-money switching cores on local racks. The Afghanistan data center market size allocated to cloud service providers and hyperscalers is forecast to expand at an 18.80% CAGR, as domestic data-sovereignty rules obligate hyperscalers to host availability zones within national borders before onboarding public-sector workloads. Growing financial-inclusion initiatives are propelling banks to co-locate disaster-recovery nodes in Tier II cabinets that ride on operator fiber rings, while the defense establishment migrates logistics databases to the GovCloud enclave in Kabul. In parallel, healthcare networks are harnessing edge appliances to stream video libraries and capture EMR traffic, creating new demand curves for micro-colocation enclosures near provincial hospitals.

Cloud-entry costs are moderating as containerized, modular builds cut procurement cycles to under six months, encouraging fintech startups and OTT players to commit to multi-year reserved-instance contracts. The resulting volume discount dynamics are compressing unit prices and prompting operators to bundle cross-connects, managed security, and 24 × 7 NOC services as value-added options further deepening their revenue mix inside the Afghanistan data center market.

By Hotspot: Kabul retains primacy while Mazar-i-Sharif surges

Kabul’s 68% share of the Afghanistan data center market stems from its proximity to the national Internet Exchange Center, the only Tier III-compliant site, and round-the-clock grid coverage of 18 hours daily. The Afghanistan data center market size attributed to Mazar-i-Sharif is growing at the fastest rate, with a 20.20% CAGR, catalyzed by its pivotal role along the Termez-Mazar-i-Sharif-Kabul-Peshawar rail corridor, which accelerates cross-border trade and fintech settlement volumes. Land parcels near Balkh industrial estates now offer lease rates 30% lower than comparable plots inside Kabul, and the CASA-1000 import lines guarantee 300 MW of seasonal hydropower, partially addressing uptime concerns. Rest-of-Afghanistan nodes, primarily Herat, Kandahar, and Jalalabad, are poised to absorb edge traffic via government-sponsored district telecom branches, although the runway for hyperscale builds remains constrained by limited substation-level redundancy.

In Kabul, operators are segmenting footprints into high-density zones optimized for AI inference clusters, which demand 20+ kW per rack, while traditional compute racks typically hover at 5-7 kW. Mazar-i-Sharif facilities, in contrast, market lower pPUE targets of 1.6 owing to cooler ambient temperatures, giving them a power-cost edge that resonates with latency-tolerant backup and archiving workloads. This evolving two-node hierarchy underpins the hybrid deployment strategies many enterprises pursue within the Afghanistan data center market.

Geography Analysis

Afghanistan straddles pivotal Eurasian freight lanes, and each new fiber spur enriches carrier route diversity. Kabul sits on the convergence of three international cables, TAPI, Wakhan, and Turkmenistan Fiber, making it the country’s de facto peering point. Because bandwidth tariffs into the capital have decreased by 40% since 2023, SaaS providers find it commercially viable to deploy mirrors within the city, sparking localized traffic that reduces dependency on Gulf hosting hubs. Mazar-i-Sharif leverages CASA-1000 and Uzbek power trade to lure workload migrations that can tolerate sub-20 ms incremental latency to Kabul. Herat and Kandahar connect to Iran and Pakistan, respectively, creating additional failover paths valuable to disaster-recovery architects operating within the Afghanistan data center market.

Rural districts historically bypassed by terrestrial links are now establishing their first micro-edge stations using solar-powered LEO gateways, enabling e-health consultations for nomadic communities in Badakhshan and opening new telemetry channels for agri-tech pilots in Helmand. While grid reliability outside urban clusters remains a barrier, modular battery vaults coupled with propane gensets are narrowing availability gaps to within Tier II thresholds. Government commitments to roll fiber to every provincial capital by 2027 promise to raise the addressable pie of enterprises that can realistically consume colocation, pushing cumulative installed capacity beyond 6 MW by 2032 if funding stays on track.

Competitive Landscape

Market structure is fragmented, with no single player commanding more than one-third of installed white-space. Afghan Telecom, Roshan, Etisalat Afghanistan, and ATOMA (ex-MTN) each manage proprietary facilities sized below 1 MW but occupy strategically distinct footprints. Afghan Telecom primarily hosts state workloads and rents cross-connects to ISPs, while Roshan monetizes excess space by offering managed NOC services tailored to SaaS and payment-gateway operators. Etisalat Afghanistan concentrates on enterprise rack leasing bundled with MPLS connectivity and recently issued tenders for 750 DC rectifiers to harden its Tier II halls. ATOMA’s 2025 entry injects fresh capex pledges aimed at overlaying 4G densification with containerized edge micro-pods sited at tower bases in peri-urban belts.

Chinese vendors Huawei and ZTE provide turnkey modules financed via export-credit lines, compressing build schedules to under eight months and disrupting local EPC contractors. Meanwhile, U.S.-based generator OEMs and European UPS suppliers sense volume upside as energy-redundancy ratios climb in new designs. ESA-registered satellite broadband integrators, buoyed by ADB studies, are partnering with domestic ISPs to stitch LEO gateway farms onto the Kabul-Mazar-i-Sharif transport spine, carving out a nascent edge-hosting niche. These overlapping ecosystems create vigorous price competition yet keep barriers to entry high because spectrum licenses, construction permits, and insurance coverage remain administratively complex.

Afghanistan Data Center Industry Leaders

Afghan Telecom (ANDC)

Afghan Wireless Communication Co. (AWCC)

ATOMA (Telecom Development Co. Afghanistan)

Roshan (TDCA)

Etisalat Afghanistan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: MTN exited Afghanistan, transferring operations to M1 Group under the ATOMA brand; new leadership pledged network modernization and 4G expansion.

- April 2025: TAPI pipeline advanced 14 km inside Afghanistan with 24 km prepared, reaffirming the USD 10 billion project’s twin roles in gas transit and 700 km fiber rollout.

- February 2025: Taliban administration settled USD 627 million in electricity debt with Tajikistan, Uzbekistan, and Turkmenistan, securing higher import quotas for 2024.

- July 2024: MCIT launched a 700 km fiber link aligned to TAPI, integrating with the national backbone to bolster redundancy.

- July 2024: Afghan Post commenced a USD 900,000 digitalization project linking postal branches to fiber for live parcel tracking and future wallet services.

Afghanistan Data Center Market Report Scope

The Afghanistan Data Center Market Report is Segmented by End-User (BFSI, Cloud Service Providers and Hyperscalers, Telecom Operators, Government and Defence, E-Commerce and Retail, Media and Entertainment, Healthcare, Other End-Users), and Hotspot (Kabul, Mazar-I-Sharif, Rest of Afghanistan). The Market Forecasts are Provided in Terms of Volume (MW Capacity).

| BFSI |

| Cloud Service Providers and Hyperscalers |

| Telecom Operators |

| Government and Defence |

| E-commerce and Retail |

| Media and Entertainment |

| Healthcare |

| Other End-Users |

| Kabul |

| Mazar-i-Sharif |

| Rest of Afghanistan |

| By End-User | BFSI |

| Cloud Service Providers and Hyperscalers | |

| Telecom Operators | |

| Government and Defence | |

| E-commerce and Retail | |

| Media and Entertainment | |

| Healthcare | |

| Other End-Users | |

| By Hotspot | Kabul |

| Mazar-i-Sharif | |

| Rest of Afghanistan |

Key Questions Answered in the Report

How fast is the Afghanistan data center market projected to grow?

Installed capacity is forecast to jump from 0.9 MW in 2025 to 3.8 MW by 2030, translating into a robust 33.39% CAGR.

Which city holds the largest share of national capacity?

Kabul accounts for 68% of installed white-space thanks to its fiber density, government workloads, and higher grid reliability.

What end-user segment currently drives the most rack demand?

Telecom operators lead with 34% market share as their OSS/BSS and mobile-money platforms remain anchor tenants.

Why is Mazar-i-Sharif emerging as a hotspot?

Its location on new rail and fiber corridors, combined with CASA-1000 power imports, supports a 20.20% CAGR for local capacity additions.

How are power-supply challenges being addressed?

The government has cleared overdue electricity debts and is tapping hydropower imports while operators deploy high-efficiency UPS and mobile gas turbines for backup.

What impact will LEO satellites have on facility deployment?

Sub-50 ms latency from Starlink-class networks enables micro-edge pods in rural areas, broadening the addressable customer base for localized processing.

Page last updated on: