Aerospace And Defense Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

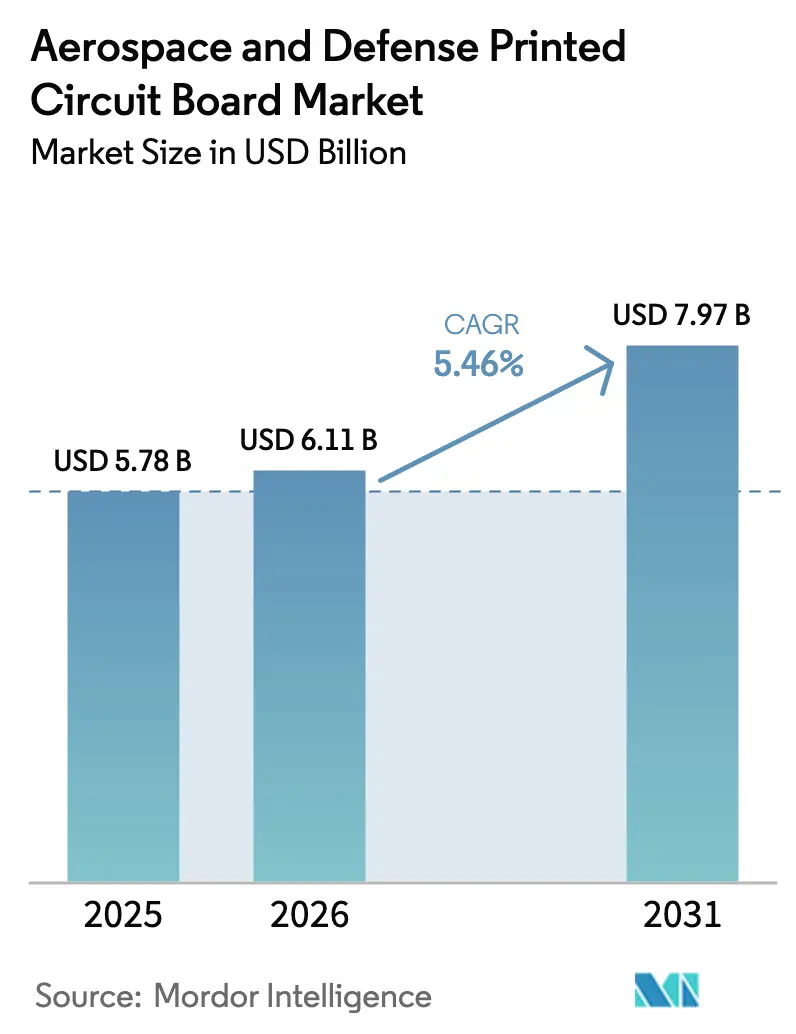

| Market Size (2026) | USD 6.11 Billion |

| Market Size (2031) | USD 7.97 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

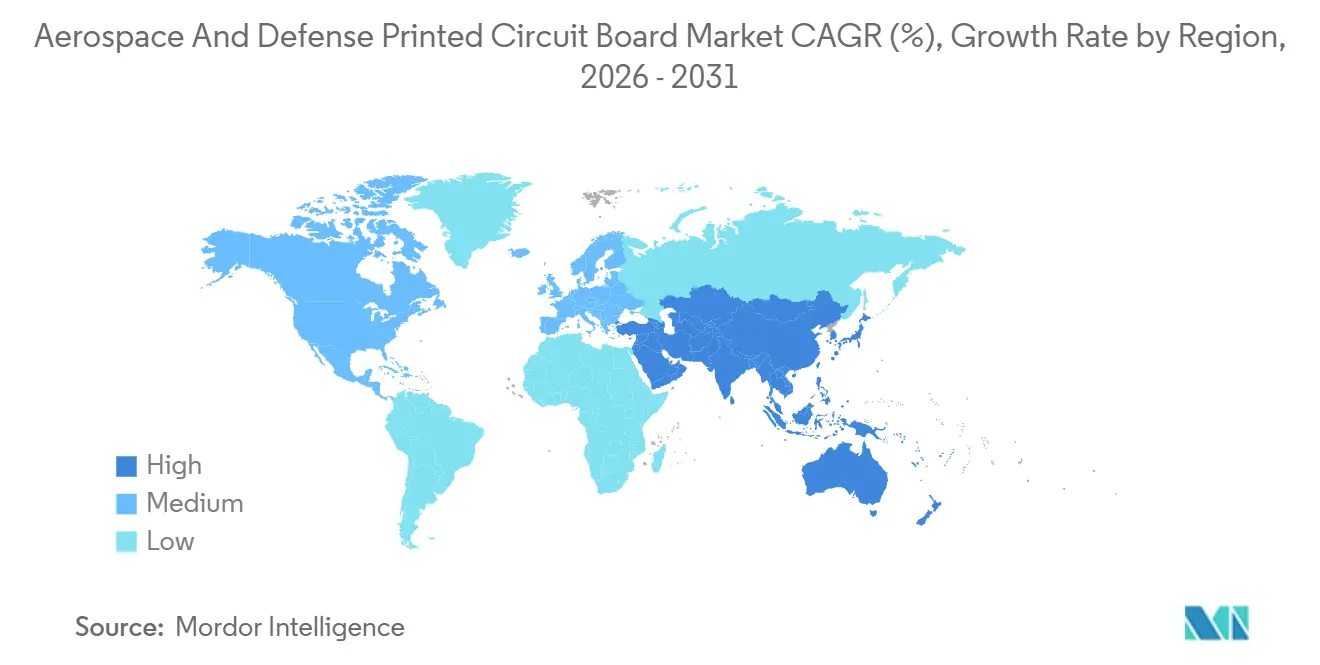

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace And Defense Printed Circuit Board Market Analysis by Mordor Intelligence

The Aerospace And Defense Printed Circuit Board Market size is projected to be USD 5.78 billion in 2025, USD 6.11 billion in 2026, and reach USD 7.97 billion by 2031, growing at a CAGR of 5.46% from 2026 to 2031.

This growth reflects the steady migration from analog electronics to digital, power-dense architectures that place strict demands on trace widths, thermal budgets, and regulatory compliance. Prime contractors are reshoring fabrication lines to meet International Traffic in Arms Regulations and AS9100 requirements, while sovereign artificial-intelligence mandates and hypersonic-weapon programs are boosting demand for trusted domestic capacity. Increased radar bandwidth, satellite proliferation, and the More Electric Aircraft concept are all funneling investment toward high-density interconnect boards, heavy-copper constructions, and metal-core substrates. Simultaneously, prolonged export-license reviews and lingering shortages of polyimide resins lengthen lead times, prompting vertically integrated suppliers to secure laminate chemistry in-house and to accelerate qualification of alternate materials.

Key Report Takeaways

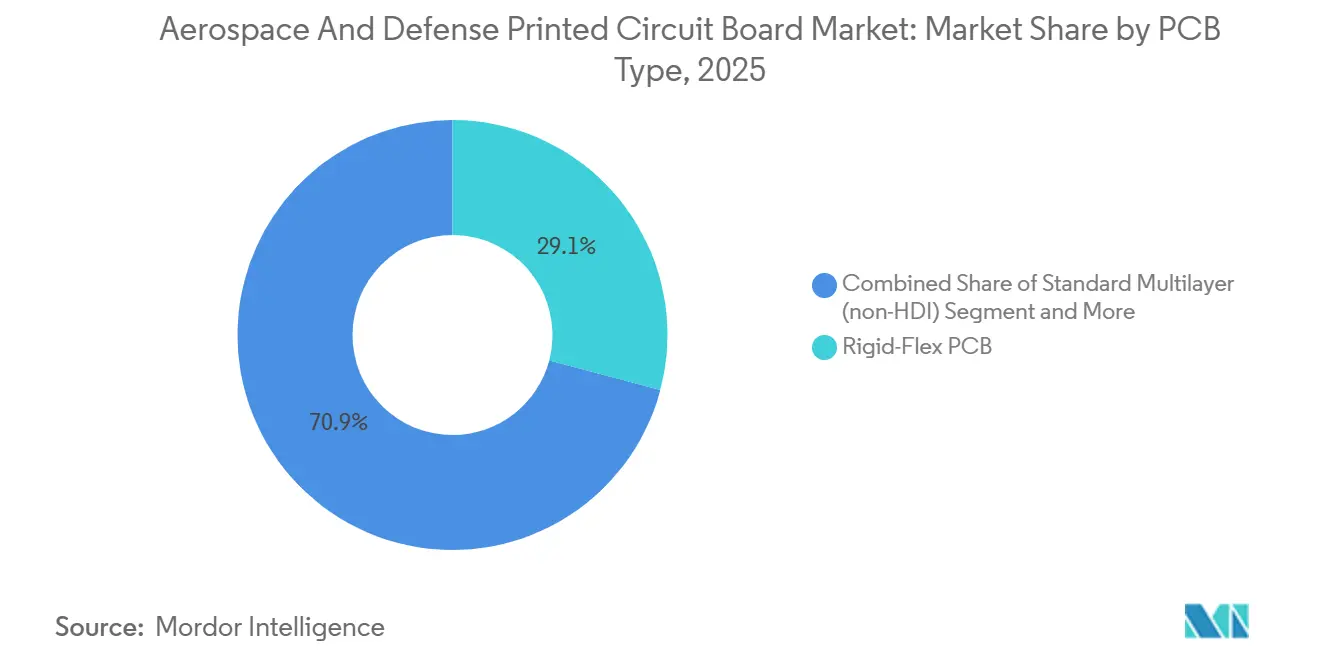

- By PCB type, rigid-flex captured 29.12% of the Aerospace and Defense PCB market share in 2025, while flexible circuits are forecast to expand at a 6.93% CAGR to 2031.

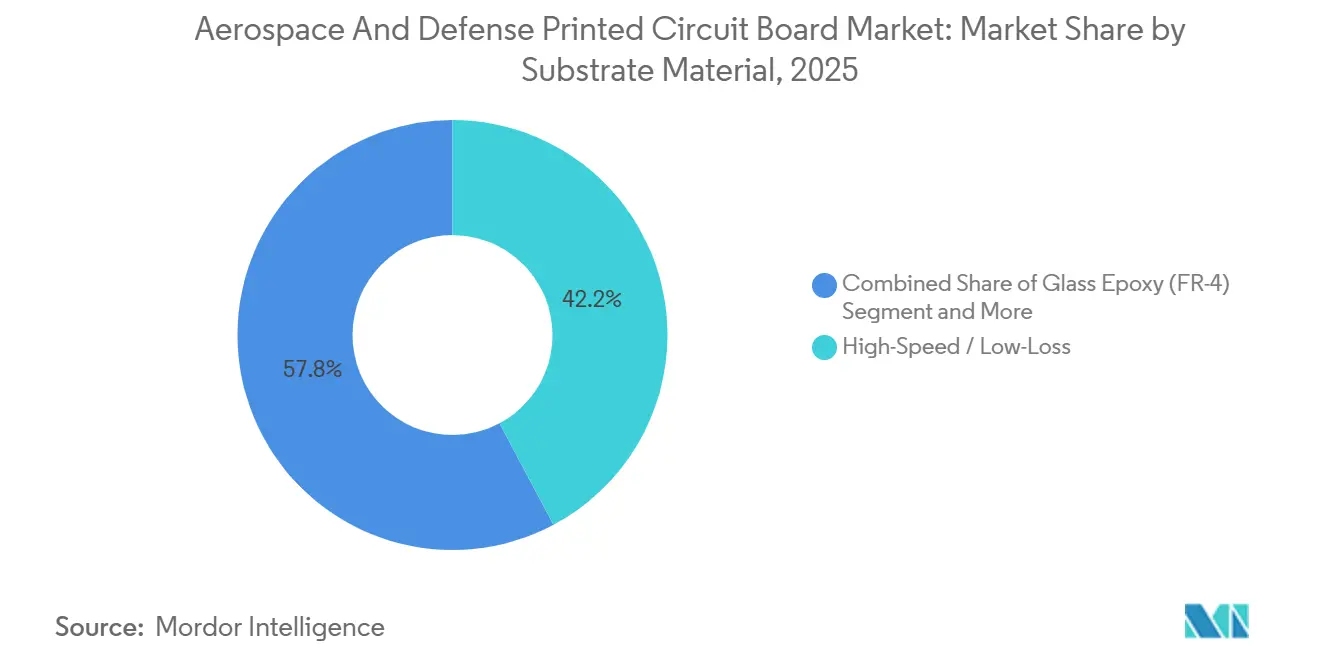

- By substrate material, high-speed and low-loss laminates accounted for 42.21% of the Aerospace and Defense PCB market size in 2025 and are projected to grow at a 6.12% CAGR through 2031.

- By geography, the Asia Pacific accounted for 87.43% of global volume in 2025 and is expected to post a 6.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerospace And Defense Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| More Electric Aircraft Trend Driving Power Electronics PCBs | +1.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Rising Defense Electronics Upgrades in NATO Fleets | +1.0% | North America and Europe, spillover to Asia Pacific | Medium term (2-4 years) |

| Growing Adoption of HDI Boards in Avionics | +0.9% | Global | Short term (≤ 2 years) |

| Spacecraft Miniaturization Requiring High-Density Interconnects | +0.7% | Global, led by North America and Asia Pacific | Long term (≥ 4 years) |

| Domestic Content Mandates Boosting Local PCB Supply Chains | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Demand for High-Temperature PCBs in Hypersonic Weapons | +0.5% | North America, China, Russia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

More Electric Aircraft Trend Driving Power Electronics PCBs

Airframers are replacing hydraulic and bleed-air circuits with electrically driven actuators, ice protection, and environmental control units. These modules channel kilowatts through boards clad with 6-ounce to 10-ounce copper foils, necessitating heavy-copper or metal-core substrates rated for sustained 175°C junction temperatures. Silicon-carbide inverters are already being embedded directly onto metal-core boards in regional jets and urban air-mobility demonstrators, cutting parasitic inductance and trimming cooling hardware mass by 22% according to Horizon Europe’s ORCHESTRA test program.[1]ORCHESTRA Project, “More Electric Aircraft Power Electronics Research,” orchestra-project.eu Military rotorcraft amplify the requirement: the United States Army’s Future Vertical Lift specification demands redundant PCB channels with built-in test logic that sustain fault-tolerant tail-rotor control. Polyimide laminates with glass-transition temperatures above 280°C have therefore displaced FR-4 in high-power positions, effectively narrowing the global supplier base to a handful of resin formulators.

Rising Defense Electronics Upgrades in NATO Fleets

NATO’s Digital Backbone initiative mandates interoperable data links and software-defined radios by 2030, triggering cockpit retrofits across F-16, Eurofighter and Rafale fleets.[2]North Atlantic Treaty Organization, “Digital Backbone Initiative,” nato.int The United States Air Force’s USD 2.4 billion E-7A Wedgetail award illustrates scale, requiring multilayer boards populated with thousands of gallium-nitride TR modules and stacked microvias on 0.8 mm pitch. European sixth-generation fighter programs adopt similar any-layer HDI processes that allow via formation on each copper plane, a capability still limited to roughly a dozen qualified fabricators worldwide. System-in-package avionics integrate passives within the board core, dropping assembly height by 60% and enabling conformal installation in wing leading edges.

Growing Adoption of HDI Boards in Avionics

Flight-management, synthetic-vision, and terrain-awareness functions have migrated to system-on-chip devices with 400-plus ball-grid-array connections that cannot be fanned out on conventional through-hole vias. Laser-drilled microvias with 75 µm capture pads provide escape routing for 0.4 mm packages while holding 100 Ω differential impedance at 28 Gb/s. ESA’s Hera mission used this approach to trim its autonomous navigation computer mass by 35%, and the MQ-25 Stingray tanker drone validated microvia boards for 15-G maneuvers under salt-fog exposure. Each prototype demands destructive cross-sections and ionic-contamination tests that consume 8-12 weeks, straining ITAR-qualified capacity and elongating design cycles.

Spacecraft Miniaturization Requiring High-Density Interconnects

Smallsat buses under 250 kg require boards with areal densities below 2.5 kg/m² and total-ionizing-dose tolerance beyond 100 krad. Rigid-flex constructions remove bulky harnesses and cut assembly labor by 40% in solar-array drives and star-tracker interfaces. Starlink V2 satellites employ polyimide flex with rolled-annealed copper that survives 200 thermal cycles between −180 °C and +120 °C, performance verified at NASA’s Goddard Space Flight Center.[3]NASA Goddard Space Flight Center, “Materials Testing and Evaluation,” nasa.gov/goddard Fewer than eight global fabricators hold the dual AS9100 and ITAR credentials needed for such builds, pushing lead times for space-grade boards to 32 weeks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclic Defense Procurement Budgets | -0.8% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| ITAR and Export Compliance Complexities | -0.6% | Global, with primary impact on North America and Europe | Medium term (2-4 years) |

| Limited Availability of Aerospace-Grade Laminate Materials | -0.4% | Global | Short term (≤ 2 years) |

| High Certification Costs for New PCB Suppliers | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyclic Defense Procurement Budgets

Continuing resolutions delayed United States fiscal-year 2025 appropriations until March 2025, freezing new-start electronics and deferring USD 18 billion of defense procurement. Germany’s 2025 defense budget, EUR 53.3 billion (USD 57.2 billion), rose only 1.2%, trailing inflation.[4]German Federal Ministry of Finance, “Federal Budget 2025,” bundesfinanzministerium.de Such volatility depresses order visibility for PCB suppliers with shelf-life-limited inventory and discourages new entrants forced to invest USD 4-6 million for AS9100 and MIL-PRF-55110 certification.

ITAR and Export Compliance Complexities

Boards designed for missile guidance, radar or electronic warfare qualify as defense articles, restricting foreign nationals from accessing design data without a Technical Assistance Agreement. Fabricators in Taiwan or Europe must establish Foreign-Owned, Foreign-Controlled or Foreign-Influenced mitigation plans, a process that can take up to 18 months. Dedicated ITAR material streams raise laminate costs by roughly 15% versus commercial equivalents, and a 2024 violation that drew a USD 3.2 million penalty heightened industry vigilance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Gain Altitude

Rigid-flex boards captured 29.12% Aerospace and Defense PCB market share in 2025, retaining dominance in cockpit displays, mission computers and engine-control units that benefit from connector-free three-dimensional packaging. Flexible circuits, favored for weight-critical unmanned aerial vehicles and LEO satellites, are advancing at a 6.93% CAGR, the fastest pace among all form factors. Multilayer and rigid one-to-two sided boards continue to support legacy upgrades, yet their combined portion is slipping as primes specify any-layer HDI designs to compress volume and boost reliability. Heavy-copper boards underpin More Electric Aircraft power distribution, carrying hundreds of amperes on 10-ounce foils without exceeding 175°C junction temperatures. Metal-core and ceramic substrates fill niche thermal-management roles in directed-energy weapons where silicon-carbide amplifiers dissipate 300 W/cm², but high cost and limited via density constrain widespread use. The tilt toward flex and rigid-flex also simplifies export documentation, because eliminating connectors reduces the number of serialized components subject to license filings.

Second-order effects reinforce this shift. Colony-size satellite constellations require roll-to-roll production of long-span polyimide flex that folds around solar-array hinges, an operation incompatible with conventional panel-based lines. Prime contractors erect in-house rigid-flex capability to protect intellectual property and avoid multi-year qualification delays at external shops. Start-ups offering embedded-passive HDI prototypes shrink design loops from 12 weeks to 6 weeks, appealing to avionics engineers wrestling with compressed schedules. These customer expectations amplify demand volatility as low-rate initial production can pivot to full-rate orders within a single quarter, rewarding fabricators that can re-tool within days rather than weeks.

By Substrate Material: High-Speed Laminates Dominate Signal Integrity

High-speed and low-loss materials held 42.21% of the Aerospace and Defense PCB market size in 2025 and are forecast to grow 6.12% annually, powered by phased-array radar retrofits and Ka-band data links above 40 GHz. Rogers RO4000 and Isola Astra MT77 laminate families deliver dissipation factors below 0.004 with dielectric constants stable to ±0.02 across −55°C to +125°C sweeps, a property verified using IPC-TM-650 tests. Polyimide substrates defend engine-mounted sensors where FR-4 would delaminate after 500 thermal cycles, while Ajinomoto build-up films enable flip-chip IC substrates with sub-0.4 mm pitches.

Commodity FR-4 still serves power-supply daughtercards and relay panels, yet its high loss tangent (>0.020 at 10 GHz) precludes millimeter-wave routing. Metal-core substrates see limited uptake beyond LED arrays and power baseplates because their single-to-double-sided routing cannot support dense control logic. Ceramic boards, notably aluminum nitride, provide unmatched thermal conductivity for hybrid microwave integrated circuits but require laser drilling and thus carry a prohibitive cost for volume avionics. Innovation accelerates: Panasonic released a laminate with a 0.002 dissipation factor at 28 GHz that targets satellite transponders and airborne ISR payloads. Suppliers that can co-develop resin chemistries with customers gain strategic advantage, particularly when export licenses or short supply windows constrain material substitutions.

Geography Analysis

Asia Pacific generated 87.43% of 2025 production volume, reflecting entrenched high-mix, low-volume infrastructure in Taiwan, Japan and South Korea. Regional governments continue to bankroll aerospace-grade lines, exemplified by Japan’s JPY 45 billion (USD 300 million) 2025 subsidy that seeks to claw back share lost during earlier disruptions.[5]Ministry of Economy, Trade and Industry, “Aerospace Industry Support Programs,” meti.go.jp China, India and South Korea channel domestic-content rules into avionics procurement, insulating supply chains from Western export controls yet exposing programs to single-point-of-failure risks if geopolitical tension throttles substrate shipments.

North America, while smaller in volume, is scaling rapidly as the CHIPS and Science Act triggers capacity additions. TTM Technologies opened a 40,000 ft² clean room in Wisconsin for HDI and rigid-flex boards serving F-35 and Next Generation Interceptor builds. Mexico’s Querétaro and Baja California clusters attract final assembly under USMCA rules, although ITAR regulations still centralize laminate fabrication within the United States.

Europe’s footprint remains fragmented among Germany, France, the United Kingdom, and Austria. AT&S operates the continent’s largest aerospace-qualified plant in Leoben, leveraging EUR 3.2 billion (USD 3.4 billion) in European Chips Act incentives. Brexit-related customs frictions have prompted BAE Systems to dual-source rigid-flex boards from German and French partners to protect Tempest timelines. Outside these hubs, South America relies primarily on Brazil’s Embraer ecosystem, which still imports high-reliability laminates for defense programs.

Competitive Landscape

The Aerospace and Defense PCB market shows moderate concentration: the five leading suppliers captured roughly 38% of 2025 revenue, yet program-level tooling, multi-year qualifications and stringent audits limit economies of scale. TTM Technologies, AT&S and Amphenol Printed Circuits maintain vertical integration from laminate procurement through final test, allowing rapid design iterations for classified platforms. Smaller specialists such as Summit Interconnect and APCT leverage co-location near prime-contractor engineering centers, pruning prototype cycles to 48 hours and winning early design-ins.

Strategic moves focus on geographic diversification and embedded-component technology. Sanmina’s 2024 purchase of a Guadalajara facility offers near-shore capacity under USMCA while retaining AS9100 and ITAR compliance. Patent filings indicate accelerated deployment of laser direct imaging systems capable of 25 µm line-and-space geometries, essential for next-generation avionics processors.[6]United States Patent and Trademark Office, “Patent Search and Database,” uspto.gov Compliance remains a formidable moat: NADCAP audits and AS9100 renewals run on multi-year cycles, discouraging customers from shifting mid-program and effectively locking in incumbents for the 15-25 year life of defense platforms.

White-space opportunities persist. Heavy-copper boards for More Electric Aircraft and radiation-hardened substrates for LEO constellations remain under-served. Firms mastering laminate chemistry plus via reliability at 200°C stand to capture disproportionate share as hypersonic-weapon and all-electric rotorcraft programs transition from prototype to low-rate production.

Aerospace And Defense Printed Circuit Board Industry Leaders

TTM Technologies Inc.

NCAB Group AB

WUS Printed Circuit Co. Ltd.

Summit Interconnect Inc.

APCT Inc.

- *Disclaimer: Major Players sorted in no particular order

Global Aerospace And Defense Printed Circuit Board Market Report Scope

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| North America | United States |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By PCB Type | Standard Multilayer (non-HDI) | |

| Rigid 1-2 Sided | ||

| High-Density Interconnect (HDI) | ||

| Flexible Circuits (FPC) | ||

| IC Substrates (Package Substrates) | ||

| Rigid-Flex | ||

| Other PCB Types | ||

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

How fast is the Aerospace and Defense PCB market expected to grow through 2031?

The market is projected to advance at a 5.46% CAGR, climbing from USD 6.11 billion in 2026 to USD 7.97 billion by 2031.

Which PCB type is showing the quickest expansion?

Flexible circuits lead growth with a 6.93% CAGR forecast through 2031, driven by unmanned aircraft and satellite constellations.

What material segment commands the largest share?

High-speed and low-loss laminates held 42.21% of 2025 revenue and are poised to grow 6.12% per year on radar and electronic-warfare demand.

Why is Asia Pacific so dominant in production?

Decades of investment by Taiwanese, Japanese and South Korean fabricators create 87.43% of global output, though geopolitical risks are prompting select re-shoring.

What is the primary regulatory hurdle for new suppliers?

Achieving ITAR compliance and AS9100 certification can cost USD 4-6 million and take up to 18 months, deterring smaller entrants.

Where do new market opportunities lie?

Heavy-copper boards for More Electric Aircraft and radiation-hardened substrates for smallsat constellations remain under-served niches with high entry barriers.

Page last updated on: