Advanced Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

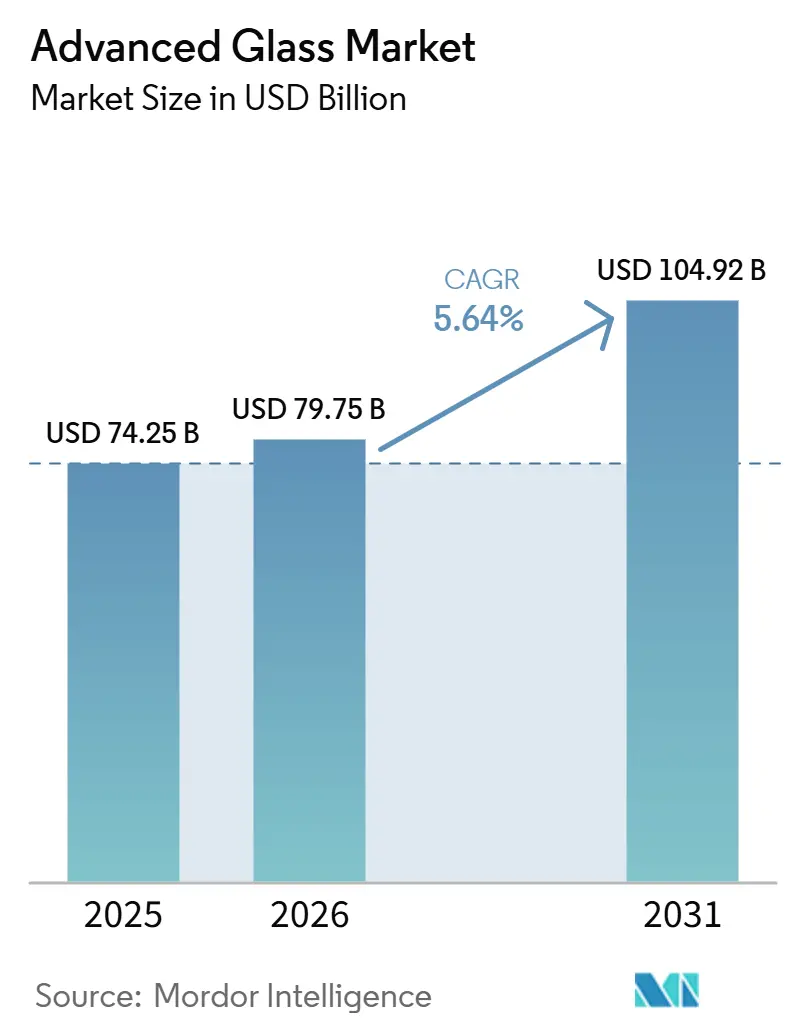

| Market Size (2026) | USD 79.75 Billion |

| Market Size (2031) | USD 104.92 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Glass Market Analysis by Mordor Intelligence

The Advanced Glass Market size was valued at USD 74.25 billion in 2025 and is estimated to grow from USD 79.75 billion in 2026 to reach USD 104.92 billion by 2031, at a CAGR of 5.64% during the forecast period 2026-2031. Growth is supported by stricter building energy regulations, wider deployment of photovoltaics, and broader use of multifunctional glass across construction, mobility, and electronics. Building operations account for 30% of global final energy consumption, underscoring the importance of high-performance glazing to efficiency and decarbonization programs rather than treating it as an optional upgrade. This broad demand base gives the advanced glass market a more balanced demand profile than markets tied to a single downstream sector. Competitive positioning centers on coating capability, manufacturing reach, and the ability to reduce production emissions, while AGC's FY2025 sales and FY2026 guidance indicate that large producers continue to invest in scale and portfolio quality. The main pressure points remain energy cost volatility, high furnace investment requirements, and softer construction cycles in some markets, although healthcare and specialty electronics continue to provide demand support for the advanced glass market.

Key Report Takeaways

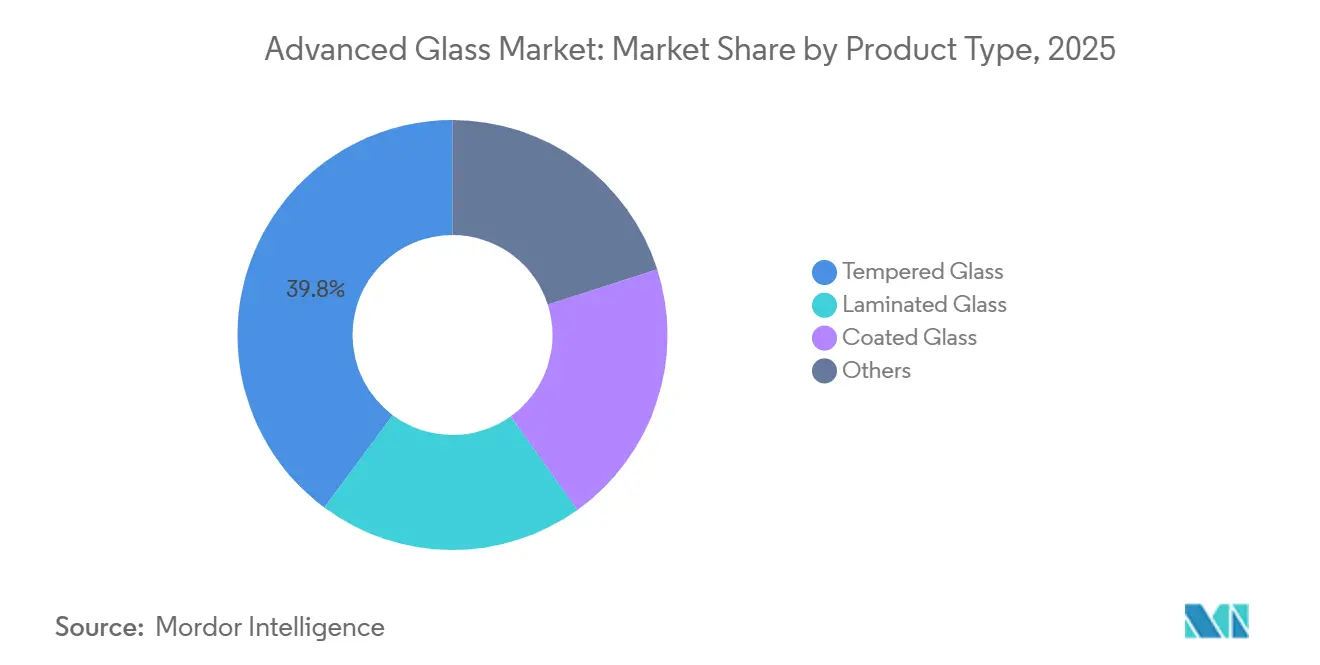

- By product type, tempered glass led with 39.82% revenue share in 2025, while coated glass is forecast to expand at 6.33% CAGR through 2031.

- By function, safety and security glass held 42.66% of the advanced glass market in 2025, while solar control glass is forecast to have the highest projected CAGR at 6.57% through 2031.

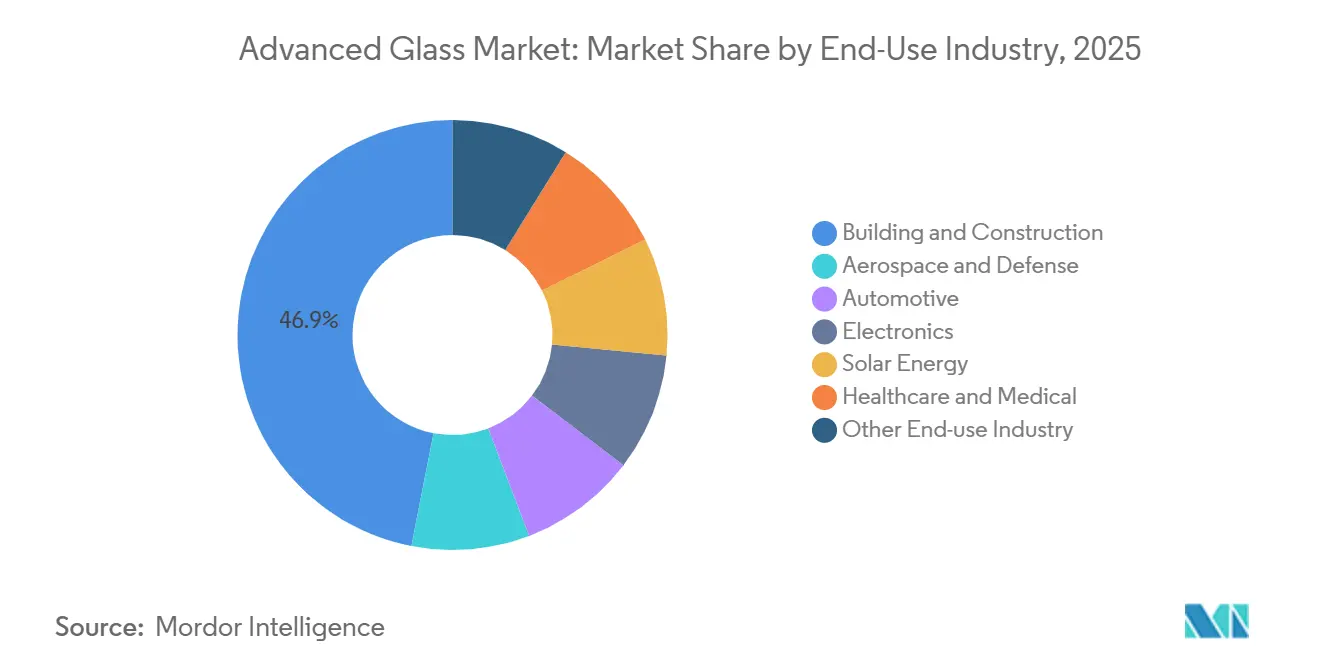

- By end-use industry, building and construction accounted for 46.95% of the advanced glass market in 2025, while solar energy is forecast to expand at a 7.13% CAGR through 2031.

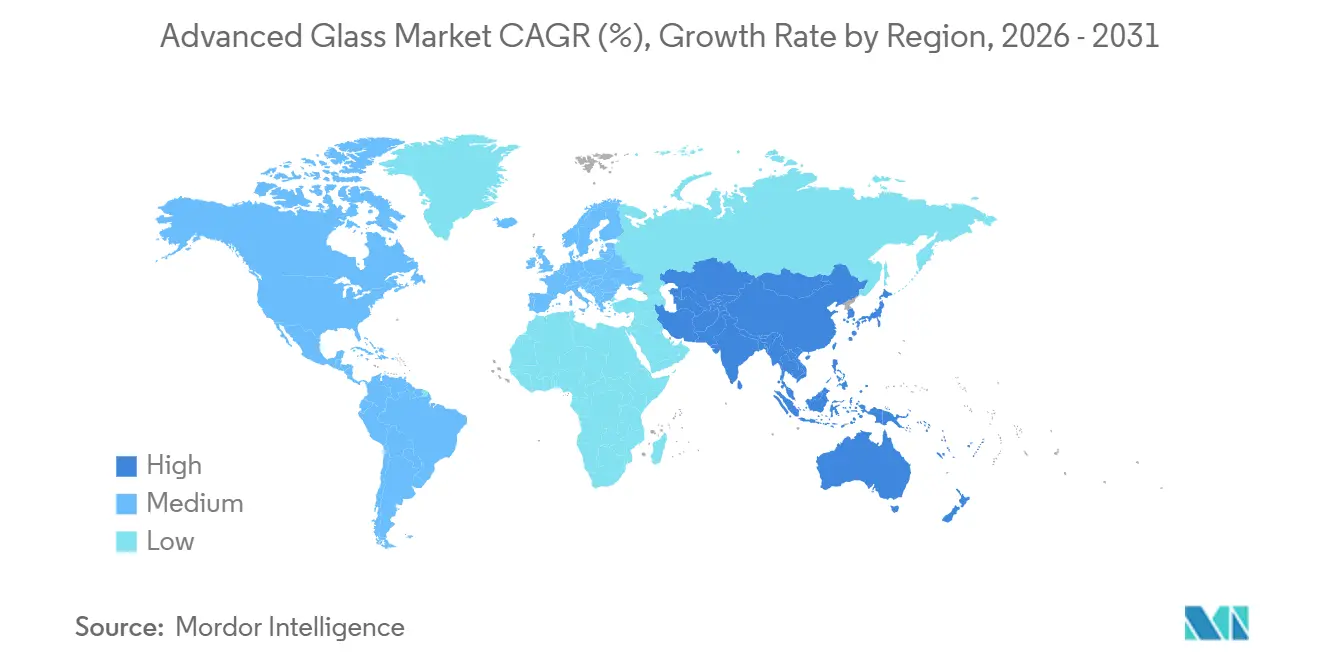

- By geography, Asia-Pacific held 47.51% of the advanced glass market in 2025 and posted the fastest projected CAGR at 6.44% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Lightweight and High-Performance Glass in Automotive and Electronics | +0.6% | Global, strongest in China, Germany, South Korea, Japan, and the United States | Medium term (2-4 years) |

| Stringent Energy Efficiency Regulations for Buildings | +1.2% | Europe, North America, China, Japan, and South Korea | Short term (≤ 2 years) |

| Increasing Building and Construction Activity in Urban Markets | +1.4% | Asia-Pacific, with spillover into the Middle East and Africa | Medium term (2-4 years) |

| Growing Integration of Smart Glass and Electrochromic Technologies | +0.9% | North America, Europe, and East Asia | Medium term (2-4 years) |

| Expanding Demand for Solar Energy Applications and BIPV | +0.7% | Asia-Pacific, Europe, the United States, India, and the Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Energy Efficiency Regulations for Buildings

The revised Energy Performance of Buildings Directive entered into force in May 2024, making the building envelope, including windows and glazing systems, a central part of energy performance calculations[1]European Commission, “Energy Performance of Buildings Directive Recast,” European Commission, energy.ec.europa.eu. That shift moved glazing selection away from architectural preference and into compliance practice for a growing share of commercial building decisions across Europe. Similar performance thresholds in other major construction markets mean buyers now evaluate glass using certified thermal and solar performance data, rather than visual or structural characteristics alone. Peer-reviewed research published in 2026 found that electrochromic windows can reduce building energy consumption by up to 35.6%, providing dynamic glazing with a clearer operating case for procurement teams. This supports wider adoption of low-emissivity, insulated, and smart glazing across both new construction and retrofit programs in the advanced glass market. It also narrows approved supplier lists, as producers that can demonstrate performance data are more likely to hold specification positions, while products that cannot meet these standards lose access with little notice.

Increasing Building and Construction Activity

Urbanization across Asia-Pacific, the Middle East, and Africa continues to drive architectural glass demand beyond energy-efficiency regulations alone. Construction activity in India and infrastructure programs across Gulf markets are creating concentrated demand for safety, structural, and insulating glass. Newer commercial designs use larger glazed facades, which raises glass intensity per square meter of completed space. This changes the value mix because developers purchase more processed, coated, and laminated formats instead of relying on standard clear glass. In hotter climates, products that limit solar heat gain have a stronger payback case because cooling costs remain a major operating expense for building owners. As a result, the advanced glass market captures a larger share of project budgets, even as builders remain disciplined about total project spending.

Growing Integration of Smart Glass and Electrochromic Technologies

Smart glass is moving from a premium feature toward a standard option in Grade-A commercial buildings and premium vehicle platforms. The electrochromic smart glass segment is estimated at USD 2.3 billion in 2026 and is growing at 12.3%, a rate faster than the broader advanced glass market. That growth gap reflects how buyers are placing greater value on solar control, privacy control, and building automation compatibility within the same glazing system. In June 2026, researchers at the Korea Institute of Materials Science demonstrated a formulation that can switch between three distinct color states, indicating stronger commercial potential. In 2026, ZEISS Microoptics joined the QuadAlliance consortium to support mass production of holographic windshield displays by 2029, with smart glass serving as the optical substrate. This expands the role of advanced glass in vehicles from a passive surface into a platform for display, sensing, and acoustic functions.

Expanding Demand for Solar Energy Applications and Building-Integrated Photovoltaics (BIPV)

The IEA Photovoltaic Power Systems Programme (IEA PVPS) reported that global photovoltaic capacity reached nearly 3 TW in 2025, up from 2.3 TW in 2024, with 698 GW of new installations recorded in a single year. Each new block of installed capacity requires specialized tempered or coated cover glass, and bifacial modules increase glass use because they require glass on both faces. Building-integrated photovoltaics reached 4.2 GW of cumulative installed capacity by the first quarter of 2026, growing 28% year over year, with glass-glass curtain wall formats expanding the fastest. Japan's Seventh Strategic Energy Plan targets solar at 23% to 29% of the national power mix by fiscal 2040, up from 9.8% in fiscal 2023. That policy direction supports domestic demand for photovoltaic glass and favors suppliers with consistent coating quality. As bifacial adoption rises, producers that can verify anti-reflection performance should hold better pricing and specification positions within the advanced glass market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Requirements for Furnace Construction and Advanced Coatings | -0.6% | Global, most pronounced in emerging markets with limited capital access | Long term (≥ 4 years) |

| Volatility in Energy and Raw Material Prices Affects Production Economics | -0.5% | Global, with the highest sensitivity in energy-import-dependent markets | Medium term (2-4 years) |

| Quality Control Challenges in Advanced Coatings and Specialty Glass Manufacturing | -0.3% | Global, concentrated in markets, scaling new product lines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements

Float glass furnace construction costs range from USD 100 million to more than USD 300 million per line, and advanced coating lines require additional capital expenditure. These thresholds restrict major capacity additions to producers with strong balance sheets and long planning horizons. Fédération Européenne du Verre d'Emballage (FEVE) stated in its 2025 decarbonization report that the European glass industry will require EUR 20 billion, or USD 21.4 billion, of cumulative investment over the coming decades, alongside more than 150 active projects and an annual investment of EUR 600 million (USD 642 million)[2]Fédération Européenne du Verre d'Emballage, “European Glass Industry Accelerates Energy Transition, 150+ Projects Engaged,” FEVE Decarbonization Report 2025, fedeverre.fr. Smaller processors in India and Southeast Asia face greater difficulty when attempting to move into coated or higher-specification products, as equipment financing remains constrained. The advanced glass market also faces a timing challenge, as furnace projects are typically committed 3 to 5 years before the related revenue is generated. This long asset cycle increases exposure to demand fluctuations and slows the pace of new entry into the advanced glass market.

Volatility in Energy and Raw Material Prices

Glass production remains highly energy-intensive, and changes in natural gas, oxygen, and electricity costs directly affect producer margins. Soda ash and silica sand prices also shift when freight costs rise or supply is disrupted in key source regions. This makes cost control a strategic priority for participants in the advanced glass market. Larger integrated producers respond through hybrid furnace investments, efficiency upgrades, and longer-term energy arrangements that reduce exposure to spot prices. Smaller independent processors have less capacity to hedge and therefore absorb more price volatility. This difference is widening the operating gap between large-scale players and smaller converters during periods of unstable energy prices in the advanced glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tempered Glass Anchors Safety-Driven Demand

Tempered glass held 39.82% of the advanced glass market share in 2025, reflecting its widespread use in facades, vehicles, and other safety-focused applications. Its position is supported by regulatory and liability considerations, as many building and mobility applications treat higher-strength glass as a minimum requirement rather than an upgrade. This gives tempered glass a more stable demand profile than product groups driven primarily by appearance or optional features. Laminated glass retained strong relevance in high-rise commercial projects and transport applications, as sound reduction, impact resistance, and security continue to shape specification choices. The other category included ultra-thin glass for foldable displays and glass substrates for semiconductor packaging, indicating that specialty uses were expanding beyond traditional flat glass.

Coated glass is forecast to record the fastest growth in the advanced glass market, with a 6.33% CAGR from 2026 to 2031. This growth is driven by the combined effect of energy codes, retrofit activity, and photovoltaic adoption, all of which reward better thermal or optical performance. Low-emissivity variants are moving closer to standard specification in commercial projects as developers increasingly treat cooling and heating performance as a lifecycle issue. Anti-reflective coatings are also benefiting from bifacial solar modules, where tighter product specifications support a sustained premium over basic float glass. As this product mix shifts upward, producers with reliable coating capabilities and processing scale are better positioned to protect margins across the advanced glass market.

By Function: Solar Control Reshapes Advanced Glass Specifications

Safety and security applications accounted for 42.66% of the advanced glass market in 2025. Their scale reflected the significant role of building and construction, where fire-rated, blast-resistant, and intrusion-resistant glazing is tied to code compliance and project risk management. This gives the segment a dependable volume base even when parts of the construction cycle weaken. Optics and aesthetics remain important in consumer electronics and specialty display applications, where clarity, thinness, and surface quality shape purchasing decisions. In that niche, producers such as Corning, SCHOTT AG, and Nippon Electric Glass compete more on material science and process control than on output volume.

Solar control glass is expected to deliver the fastest growth in the advanced glass market, with a 6.57% CAGR through 2031. Rising urban temperatures and stricter building performance regulations are pushing solar heat gain control into core design decisions for offices, retail centers, and institutional buildings. High-performance thermal-insulation glass is also gaining ground in colder climates, as better-coated systems deliver heating savings that justify the higher upfront cost. Renovation programs in Europe add another layer of demand, as replacement projects follow a different timing pattern than new construction. As a result, the function mix of the advanced glass market is shifting toward products that improve energy performance while meeting safety and design requirements.

By End-Use Industry: Construction Anchors Demand, Solar Energy Accelerates Fastest

Building and construction accounted for 46.95% of the advanced glass market size in 2025 and remained the anchor segment for total demand. Urban densification and curtain wall design keep volume high, particularly in commercial buildings across Asia-Pacific and the Middle East. At the same time, energy-efficiency regulations are shifting the product mix toward coated, laminated, and insulated formats that offer higher value per square meter. Automotive remains the third-largest end-use, and its mix is shifting as electric vehicle platforms adopt acoustic, solar control, and digitally enabled glazing. This raises value per vehicle even when physical glass volumes do not change significantly.

Solar energy is projected to post the fastest growth in the advanced glass market, with a 7.13% CAGR through 2031. Record photovoltaic installations are driving strong demand for tempered, coated, and glass-glass module formats across utility, commercial, and building-integrated systems. Electronics and healthcare are smaller in volume but remain attractive because quality requirements and qualification cycles support better margins than commodity architectural lines. Aerospace also contributes, even at low volume, as optical-grade and protective glass programs can sustain premium pricing and deepen process expertise. Producers that maintain a presence in aerospace and electronics strengthen their innovation pipelines, which can later support broader offerings across the advanced glass market.

Geography Analysis

Asia-Pacific held 47.51% of the advanced glass market share in 2025 and is expected to record the fastest growth at a 6.44% CAGR through 2031. This reflects the region's strength in construction, photovoltaic manufacturing, and vehicle production. In China, tighter building standards and decarbonization goals are driving greater adoption of coated and insulating glass in mainstream specifications. India adds further demand as commercial and residential development expands and buyers shift toward higher-value glass products. Southeast Asia is also growing in importance, with countries such as Vietnam and Indonesia adding capacity to serve both domestic construction demand and export supply.

North America and Europe present different growth profiles but remain important for the advanced glass market. In January 2025, the U.S. Department of Commerce awarded Creating Helpful Incentives to Produce Semiconductors (CHIPS) incentives to Corning to support expanded production of high-purity fused silica and ultra-low-expansion glass for Extreme Ultraviolet (EUV) semiconductor lithography, signaling that specialty glass had become a national technology priority. In May 2026, Corning and NVIDIA announced a multi-year partnership that will increase U.S. optical connectivity manufacturing capacity tenfold and expand fiber production by more than 50% through new facilities in North Carolina and Texas. In Europe, renovation demand remains central, as the Energy Performance of Buildings Directive (EPBD) recast accelerates upgrades to older building stock. Saint-Gobain reported 2025 revenue of EUR 46.5 billion (USD 49.8 billion) and an operating margin of 11.4%, reflecting demand across its glass and construction portfolio.

South America, the Middle East, and Africa are smaller markets in absolute terms but remain relevant for suppliers able to match project specifications and climate requirements. In South America, Brazil's construction activity and growing interest in solar installations are supporting demand for architectural and photovoltaic glass in selected projects. In the Middle East and Africa, high solar irradiance makes solar control and reflective-coated glass an operational necessity in many buildings rather than a discretionary sustainability feature. Large urban developments, airports, and renewable energy projects in the region also favor glass-intensive designs, supporting value capture for suppliers that secure approved positions early.

Competitive Landscape

The advanced glass market is moderately consolidated globally, with a limited group of vertically integrated producers, including AGC Inc., Compagnie de Saint-Gobain, NSG Group, Guardian Industries, Xinyi Glass Holdings, Fuyao Glass, and Corning Incorporated, controlling much of the value-added capacity. Downstream processing is more fragmented, as regional fabricators convert flat glass into finished products close to end markets. This creates a two-tier structure in which large producers compete on furnace scale, coatings, and geographic reach, while local players compete on finishing, logistics, and specification support. Bargaining power in this market depends on the product step, with upstream advantage strongest in coated, solar, and specialty formulations. High furnace costs, long amortization cycles, and proprietary coating knowledge continue to limit new entry into the advanced glass market.

Competition is divided between scale-oriented and technology-oriented suppliers. Xinyi, CSG, and Fuyao are positioned in cost- and volume-driven segments, while Corning, SCHOTT, and Gentex defend margins through proprietary formulations, coatings, and integrated hardware. In February 2026, AGC reported FY2025 net sales of JPY 2,058.8 billion (USD 13.7 billion) and guided FY2026 net sales of JPY 2,200 billion (USD 14.7 billion), reflecting continued focus on scale and product mix management. In 2026, ZEISS Microoptics joined the QuadAlliance to support the industrialization of holographic windshield displays, illustrating how smart glass is becoming part of a broader in-vehicle electronics stack.

The most visible white space exists in Building-Integrated Photovoltaics (BIPV) glass for curved or non-planar applications and in glass substrates for advanced semiconductor packaging. These areas are attracting research and product development activity, as pricing is materially higher than in standard architectural flat glass, and qualification barriers are greater. At the same time, competitive pricing by Chinese producers continues to pressure European and Japanese manufacturers in price-sensitive applications, encouraging a shift toward specialty glass and higher-value automotive programs. As a result, competition in the advanced glass market remains centered on portfolio mix, process capability, and the ability to exit segments where price competition is most intense.

Advanced Glass Industry Leaders

AGC Inc.

Saint-Gobain

Nippon Sheet Glass Co., Ltd

Guardian Industries

Sisecam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Corning Incorporated and NVIDIA announced a multi-year commercial partnership for optical connectivity manufacturing in the United States. Under the arrangement, Corning will increase optical connectivity capacity tenfold and fiber production capacity by over 50%, with three new manufacturing facilities to be constructed in North Carolina and Texas. The partnership includes an NVIDIA equity stake of up to USD 3.2 billion and a multi-billion-dollar prepayment for future optical infrastructure supply.

- March 2026: Apollo Global Management's funds announced a strategic investment in NSG Group, a manufacturer of architectural, automotive, and functional glass. The investment is expected to accelerate NSG Group's strategic restructuring across its three business areas and strengthen its competitive position in solar panel glass and display cover glass.

Global Advanced Glass Market Report Scope

Advanced glass refers to engineered glazing materials designed with specific optical, thermal, or structural properties. These materials are used in architecture, electronics, and automotive industries, offering benefits such as noise reduction, UV control, temperature regulation, and privacy control.

The advanced glass market is segmented by product type, function, end-use industry, and geography. By product type, the market is segmented into laminated glass, tempered glass, coated glass, and others. By function, the market is segmented into safety and security, solar control, optics and lighting, and high performance. By end-use industry, the market is segmented into building and construction, aerospace and defense, automotive, electronics, solar energy, healthcare & medical, and other end-use industry. The report also covers market size and forecasts for advanced glass across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Laminated Glass |

| Tempered Glass |

| Coated Glass |

| Others |

| Safety and Security |

| Solar Control |

| Optics and Lighting |

| High Performance |

| Building and Construction |

| Aerospace and Defense |

| Automotive |

| Electronics |

| Solar Energy |

| Healthcare & Medical |

| Other End-use Industry |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Laminated Glass | |

| Tempered Glass | ||

| Coated Glass | ||

| Others | ||

| By Function | Safety and Security | |

| Solar Control | ||

| Optics and Lighting | ||

| High Performance | ||

| By End-Use Industry | Building and Construction | |

| Aerospace and Defense | ||

| Automotive | ||

| Electronics | ||

| Solar Energy | ||

| Healthcare & Medical | ||

| Other End-use Industry | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Advanced Glass Market?

The Advanced Glass Market size was valued at USD 74.25 billion in 2025 and is estimated to grow from USD 79.75 billion in 2026 to reach USD 104.92 billion by 2031, at a CAGR of 5.64% during the forecast period 2026-2031.

What is driving growth in demand for advanced glass?

Building energy regulations, stronger solar installations, and higher use of multifunctional glass in construction, vehicles, and electronics are the main growth supports.

Which product type leads advanced glass sales?

Tempered glass led with a 39.82% share in 2025, as it remains a standard material for safety-focused applications in buildings and the automotive industry.

Which functional category is growing fastest?

Solar control glass is the fastest-growing function, with a projected 6.57% CAGR through 2031 as cooling performance becomes more important in buildings.

Page last updated on: