Advanced Bipolar Direct Energy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.30 Billion |

| Market Size (2031) | USD 4.94 Billion |

| Growth Rate (2026 - 2031) | 8.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

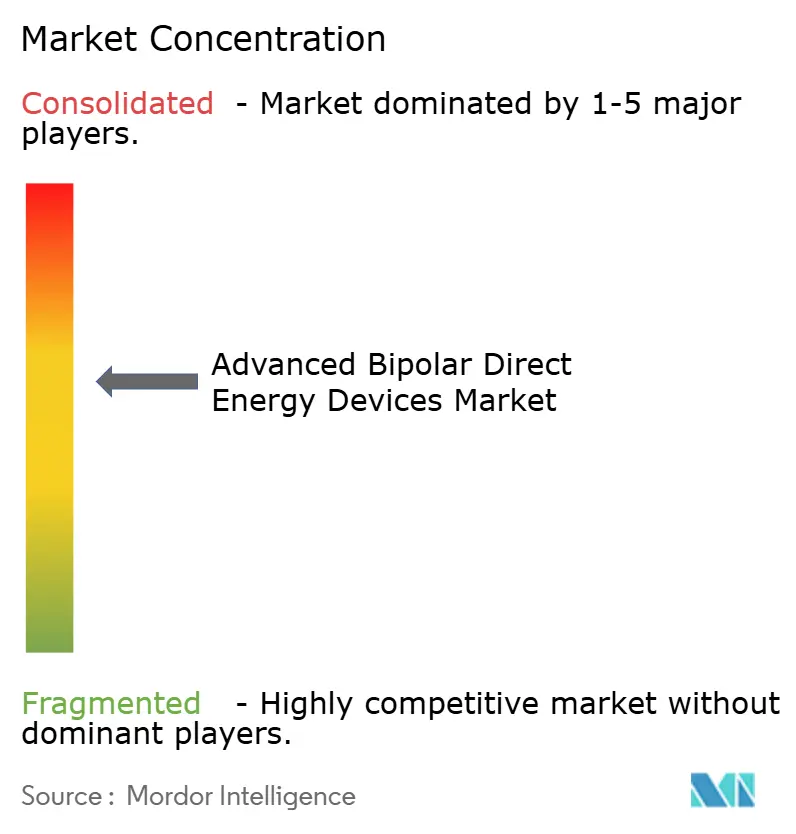

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Bipolar Direct Energy Devices Market Analysis by Mordor Intelligence

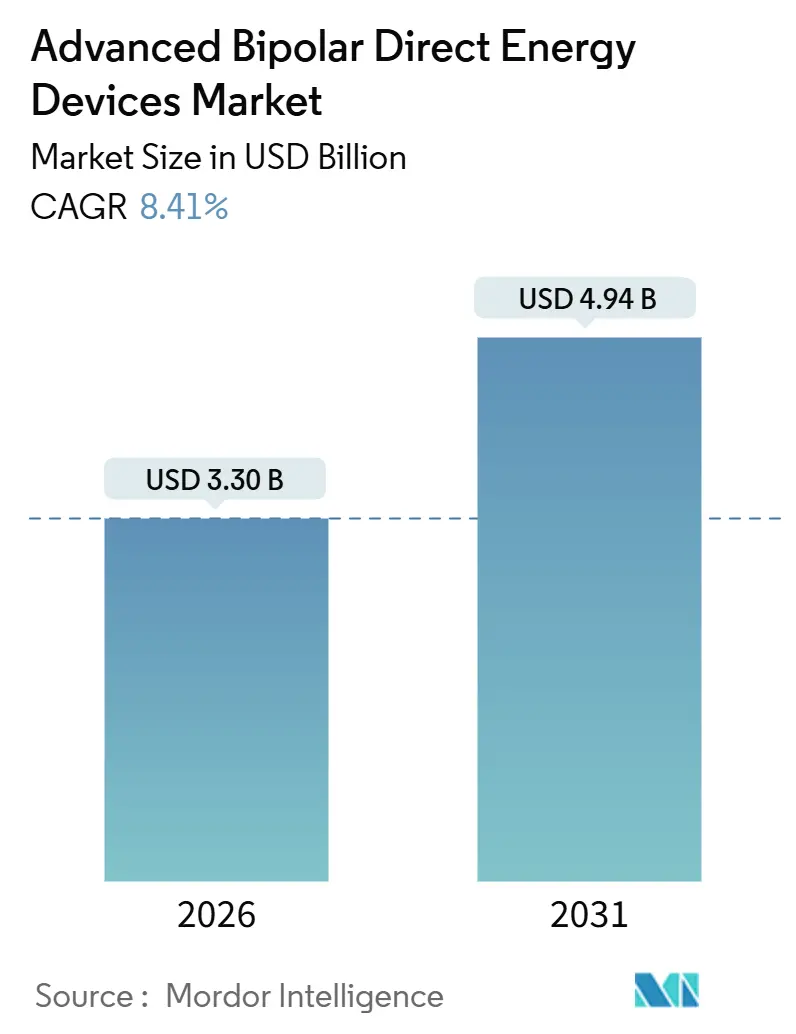

The Advanced Bipolar Direct Energy Devices Market size is estimated at USD 3.30 billion in 2026, and is expected to reach USD 4.94 billion by 2031, at a CAGR of 8.41% during the forecast period (2026-2031).

Momentum stems from hospitals replacing legacy fixed-power generators with impedance-controlled platforms, ambulatory surgery centers (ASCs) absorbing high-volume laparoscopic work, and robotic-surgery vendors bundling proprietary bipolar instruments for premium pricing. Electrosurgical generator systems, though a smaller base, are expanding at 12.25% annually as buyers favor modular consoles that drive multi-modality compatibility, lower OR footprint, and reduce device skew counts. Meanwhile, neurosurgery’s demand for sub-millimeter precision accelerates uptake of ceramic-insulated forceps that cut collateral heat by 55%, a clinically significant reduction when working near eloquent cortical regions. Asia-Pacific shows the steepest regional climb at 11.51% CAGR, due to India’s Production-Linked Incentive (PLI) scheme and China’s Healthy China 2030 policy, both subsidizing domestic Class III device production and thereby shrinking import markups. Competitive intensity remains moderate; Intuitive Surgical still captures roughly one-quarter of segment revenue by locking its 9,500-system installed base into exclusive vessel sealers and curved bipolar forceps, yet Johnson & Johnson and Olympus are eroding that moat with multi-energy consoles cleared in 2025.

Key Report Takeaways

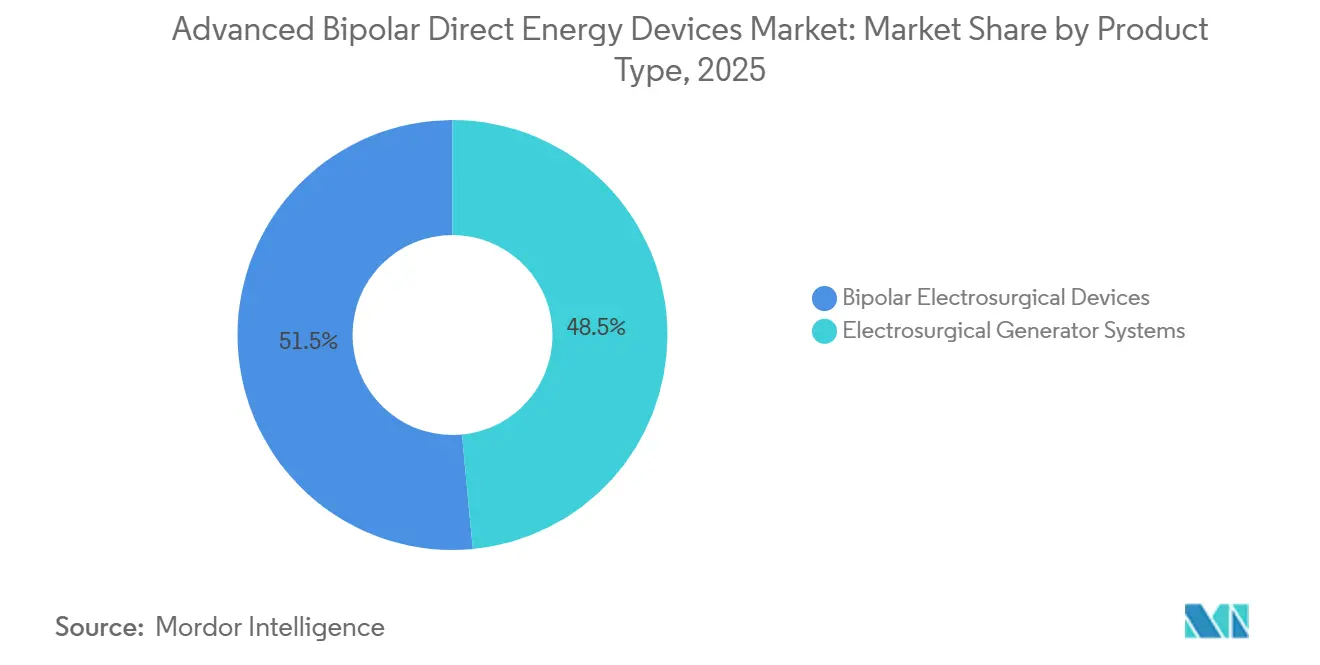

- By product type, bipolar electrosurgical devices contributed 51.55% of 2025 revenue, while generator systems booked the fastest 12.25% CAGR through 2031.

- By end user, hospitals held 59.53% share in 2025; ASCs are expanding at an 11.85% CAGR on the back of payer-mandated site-of-care migration.

- By application, general surgery delivered 45.23% of 2025 revenue, whereas neurosurgery is advancing at a 12.15% CAGR owing to precision demand.

- By geography, North America accounted for 38.15% of 2025 sales, yet Asia-Pacific is rising at 11.51% CAGR as PLI and Healthy China 2030 funding compress device prices.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Bipolar Direct Energy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of minimally-invasive surgeries | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Aging population and chronic disease burden | +1.8% | Global, particularly North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Technology advances in precision and safety | +1.5% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Expansion of ambulatory surgery centers | +1.3% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Robotic-surgery integration creating premium demand | +1.0% | North America, Europe, and select Asia-Pacific markets | Medium term (2-4 years) |

| Outcome-based reimbursement accelerating capital refresh | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally-Invasive Surgeries

More than 85% of surgical cases in developed health systems now rely on minimally-invasive techniques, and robotic-assisted volumes grew 21.9% year-over-year in 2025, a trend that steers hospitals toward robotic-compatible bipolar instruments carrying 40%-plus price premiums[1]U.S. FDA, “510(k) K251234 Vessel Sealer Curved,” fda.gov. Intuitive Surgical’s July 2025 clearance for its wristed Vessel Sealer Curved highlights this shift, since buyers value single-use tips that pair seamlessly with existing robotic wrists to shorten docking time. Inventory complexity rises because facilities must stock both handheld and robotic consumables, nudging procurement teams toward modular generator platforms that power either style without additional cart space. That interoperability allows perioperative managers to standardize preventive-maintenance schedules, lowering mean time between failure and securing better scorecards under outcome-based reimbursement. Consequently, suppliers offering unified energy stacks are squeezing out niche vendors limited to single-function handpieces.

Aging Population and Chronic Disease Burden

By 2030, 1 in 6 people globally will be aged 60 or older, an epidemiologic swing that drives higher volumes of cardiovascular and oncologic resections requiring meticulous hemostasis. Silver-tipped bipolar forceps with ceramic insulation cut collateral thermal spread by 55% versus stainless-steel predecessors, crucial when coagulating vessels adjacent to neural or cardiac tissue. Johnson & Johnson’s VARIPULSE pulsed-field platform, approved in November 2024, exemplifies movement toward non-thermal tissue effects that spare surrounding anatomy and broaden eligibility for elderly, co-morbid patients. India’s PLI program earmarked INR 3,420 crore (USD 411 million) for domestic device manufacturing, lowering import duties that previously stacked 30%-plus onto advanced bipolar equipment costs. As populations age, the case-mix skews to chronic disease surgeries, meaning demand elasticity hinges less on volume and more on device performance that reduces re-operation risk.

Technology Advances in Precision and Safety

Next-generation consoles employ real-time impedance sensing that adjusts power output 3,333 times per second, shrinking seal failures and stray-current burns. Machine-learning algorithms, reviewed in a July 2025 Sensors study, optimized electrode geometry to cut tissue sticking by 40% and improved seal reliability in vessels up to 7 mm, a proof point that software-driven design is eclipsing purely mechanical differentiation. Olympus’s POWERSEAL line, released in May 2025, reduces squeeze force, allowing surgeons to sustain precision during lengthy laparoscopic procedures without grip fatigue. Hospitals upgrading 10-year-old generators reported 15%-20% drops in surgical-site infections and 10% quicker case throughput, directly boosting bundled-payment margins. Because software updates can be pushed over existing hardware, facilities now factor lifecycle firmware support into purchasing decisions alongside capital cost.

Expansion of Ambulatory Surgery Centers

ASCs conduct more than 65% of outpatient procedures in the United States yet operate with 30%-40% slimmer capital budgets than hospital outpatient departments. CMS’s October 2024 pass-through codes allow separate payment for advanced energy systems, letting ASCs recoup generator amortization over higher volume and shorter stay cycles. Hologic’s CoolSeal console illustrates an ASC-tailored design, enabling sub-2-second vessel seals and accommodating both reusable and disposable handpieces so directors can fine-tune supply costs per specialty. Vendor service contracts now include virtual troubleshooting; Olympus partnered with Proximie in October 2024 so remote engineers can diagnose generator alarms without dispatching onsite talent, cutting downtime that would otherwise cripple tight ASC block schedules. Consequently, manufacturers offering tiered feature bundles and cloud-supported maintenance gain a procurement edge in price-sensitive outpatient settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and lifecycle costs | -1.2% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Stringent regulatory pathway | -0.8% | Global, most stringent in North America and Europe | Short term (≤ 2 years) |

| RF component supply-chain bottlenecks | -0.6% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Surgeon training gaps in advanced energy use | -0.5% | Global, more pronounced in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Costs

Generator list prices span USD 45,000-USD 80,000, but disposable handpieces add USD 200-USD 400 per case and annual service contracts consume 8%-12% of purchase value, pushing five-year ownership beyond USD 150,000 for high-volume sites. ASCs, reimbursed at roughly 60% of hospital outpatient rates, frequently defer replacements; a 2024 Ambulatory Surgery Center Association survey found 42% of members delaying capital purchases amid payment uncertainty. In India, 18% customs duty plus 12% GST inflates imported bipolar devices by nearly one-third, deterring tier-2 city adoption until PLI-subsidized local production scales up. Leasing programs and refurbished-equipment offerings fill the gap but prolong the installed base of earlier-generation consoles that lack adaptive energy control, diluting clinical benefits projected in value-based care models. Vendors must therefore prove total-cost-of-ownership advantages, not just sticker discounts, to accelerate replacement cycles.

Stringent Regulatory Pathway

IEC 60601-2-2:2017+AMD1:2023 layers fresh electromagnetic-compatibility testing onto high-frequency surgical equipment, extending European time-to-market by 6-9 months and adding USD 500,000-USD 1 million in compliance costs per product family. The FDA’s January 2025 shortage list now requires electrosurgical manufacturers to carry six-month component buffers, tying up working capital and complicating just-in-time manufacturing. Smaller German OEM Pro Med Instruments exited its DORO non-stick forceps portfolio in April 2024 because the incremental cost of meeting updated standards eroded margins. These hurdles consolidate share toward deep-pocketed incumbents but slow innovation cadence, especially for niche applications requiring bespoke tip geometries. Regulatory harmonization initiatives under the International Medical Device Regulators Forum may streamline dual submissions, yet in the interim, medium-sized firms face longer cash-burn runways before revenue capture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Generators Outpace Handpieces as Hospitals Consolidate Platforms

Electrosurgical generator systems are logging a 12.25% CAGR through 2031, markedly faster than the broader advanced bipolar direct energy devices market, as value-based purchasing pushes hospitals to retire decade-old consoles lacking impedance feedback. Within this cohort, Johnson & Johnson’s Dualto console combines monopolar, bipolar, and advanced bipolar modes, enabling procurement teams to condense three standalone units into one rack and thereby free 1.5 m² of OR floor space—an overlooked but monetizable metric for ambulatory build-outs. In 2025, bipolar electrosurgical devices still generated 51.55% of category turnover, yet rising generator attachment rates signal an inflection wherein capital replacements pull through corresponding handpiece sales.

Recurring consumables keep bipolar vessel-sealing systems the revenue anchor, with single-use tips priced at USD 300-USD 400 yet delivering 15%-20% shorter theater time in laparoscopic hysterectomy. Forceps innovation centers on metallurgy; silver-tipped variants dissipate heat faster, cutting post-op edema scores in neurosurgery by half, while rose-gold alloys from B. Braun drive conductivity gains without nickel allergenicity. Advanced scissors remain niche but shine in robotic contexts where instrument exchanges impose three-minute delays under tight pneumoperitoneum windows. Over 2026-2031, generator upgrades will continue to lift the overall advanced bipolar direct energy devices market size, whereas consumable vendors must defend margins against lower-priced entrants courting budget-sensitive ASCs.

By End User: ASC Penetration Accelerates Under Payer Site-Shift Mandates

Hospitals commanded 59.53% spend in 2025, yet ASCs are forecast to grow 11.85% annually, reshaping channel dynamics as payers cut inpatient reimbursement for routine laparoscopy. CMS pass-through codes now let ASCs bill separately for advanced bipolar consumables, equating to USD 140 per colorectal case, sufficient to break even on generator leases within 28 months[2]Centers for Medicare & Medicaid Services, “Medicare Physician Fee Schedule 2024,” cms.gov. Because ASCs run lean, vendors win deals by bundling 24-hour hot-swap service and remote calibration that eliminates in-house biomed staffing.

Large academic medical centers remain the early adopters of robotic bipolar instrumentation, creating a walled-garden revenue model for Intuitive Surgical and, by 2026, Johnson & Johnson as OTTAVA units ship in volume. Clinics and office-based labs, a nascent slice, gravitate toward compact bipolar consoles with intuitive touchscreen presets; gains here will expand the advanced bipolar direct energy devices market share in dermatology and ophthalmology where monopolar burn risk runs high. Overall, the hospital sector will sustain absolute dollar dominance, but volume growth tilts toward outpatient sites, compelling manufacturers to triage feature sets across two distinct economic buyers.

By Application: Neurosurgery Sets the Pace While General Surgery Retains Breadth

General surgery’s wide procedural base yielded 45.23% revenue in 2025, keeping it the backbone of the advanced bipolar direct energy devices market; however, neurosurgery is compounding at 12.15% CAGR thanks to ceramic insulation that confines thermal spread within a 500-micron halo, acceptable for work near eloquent cortex. B. Braun’s rose-gold forceps, adopted by 300 U.S. centers in 2025, exemplify material science driving premium tiering.

Gynecology benefits from ASC migration, where vessel-sealing consoles support same-day myomectomies with 120 mL lower mean blood loss compared with clip ligation. Cardiovascular use cases are pivoting toward pulsed-field ablation; the VARIPULSE platform eliminates esophageal fistula risk, widening eligibility among elderly atrial fibrillation patients. Orthopedic and thoracic segments remain fragmented but will ride the coattails of robotic expansion into joint arthroplasty and lobectomy. Over the horizon, AI-guided energy dosing could open new cranial and spinal indications, further elevating neurosurgery’s contribution to the advanced bipolar direct energy devices market size.

Geography Analysis

North America retained 38.15% of 2025 turnover, anchored by roughly 9,500 da Vinci robotic systems that guarantee steady consumable uptake across 3.8 million annual MIS procedures. Capital refresh cycles shortened from 10 years to 7 years after value-based penalties ramped in 2025, prompting Level I trauma centers to retire fixed-power consoles ahead of depreciation schedules. CMS pass-through incentives are siphoning laparoscopic gallbladder and hernia repairs into ASCs, fracturing purchasing influence and forcing vendors to deploy tiered price ladders and remote service to protect share. Canada’s single-payer provinces earmarked CAD 500 million for operating-room modernization in 2025, directing funds toward energy consoles compatible with future robotic expansion, while Mexico leveraged USD 1.2 billion in 2024 infrastructure funding to outfit 18 tertiary hospitals with dual-mode generators, partly financed via Banobras low-interest loans.

Asia-Pacific is the growth engine, forecast at 11.51% CAGR to 2031 as India’s medical-device market scales toward USD 50 billion by 2030, assisted by PLI grants that slash import dependence from 75% to 55%. Domestic contract manufacturers are pivoting from commodity monopolar pens to advanced bipolar handpieces under technology-transfer deals with Japanese OEMs, yielding 18% ex-factory savings for public hospitals. China’s volume-based procurement caps price escalation, but Healthy China 2030 funnels CNY 200 billion into surgical-infrastructure upgrades, underwriting generator buys that meet the strict IEC update. Japan and South Korea remain technology early adopters; however, shrinking procedure volumes from demographic decline temper unit growth, channeling supplier focus toward software upgrades and extended warranties.

Europe faces MDR headwinds that drag 510(k)-equivalent approvals by 12-18 months and inflate per-SKU recertification costs. Germany, France, and the United Kingdom still represent a signficaint percentage of regional spend, but reimbursement heterogeneity complicates launch sequencing. Olympus exploited its European home-court advantage by debuting THUNDERBEAT II in October 2025, bundling ultrasonic and advanced bipolar energy into a single handpiece that hospitals adopted to pare instrument trays by 15 SKUs on average[3]Olympus Corporation, “THUNDERBEAT II Europe Launch,” olympus-europa.com. In the Middle East, the United Arab Emirates commissioned Cleveland Clinic Abu Dhabi’s new robotic center in 2025, introducing bundled bipolar-instrument contracting, while South Africa’s private Netcare network signed a master lease for 40 impedance-sensing generators to differentiate cardiovascular service lines. Latin America’s growth polarizes around Brazil and Argentina, yet exchange-rate volatility delays tenders; Brazil’s 2025 budget prioritized primary care, deferring 60 generator replacements across state hospitals.

Competitive Landscape

Competitive intensity is moderate, with the five leading manufacturers controlling a significant share of 2025 global sales. Intuitive Surgical defends a 25% stake in the electrosurgical-instrument niche by bundling vessel sealers and curved bipolar forceps into every da Vinci procedural kit, yielding 70%-plus gross margin on disposables. Johnson & Johnson’s Dualto console, FDA-cleared in March 2025, anchors its pivot toward modularity, allowing surgeons to toggle between monopolar, bipolar, and advanced bipolar without swapping towers, locking institutions into multiyear service engagements. Olympus leverages its 4,000-unit European laparoscopic camera install base to cross-sell POWERSEAL handpieces, and a July 2025 joint venture with Swan EndoSurgical channels USD 458 million into next-gen flexible endoscopy energy tools.

Medtronic maintains deep relationships in cardiac surgery via its merger with Covidien, yet lagged in robotic integration, a gap it aims to bridge through its Hugo platform slated for CE roll-out in 2026. B. Braun focuses on neurosurgical forceps, offering 300 SKUs with proprietary rose-gold tips that now hold 18% of European OR share. New entrants exploit software niches; startups are embedding RFID tags in reusable forceps to count autoclave cycles and signal end-of-life, mitigating latent seal-failure risk. AI-based energy-dosing algorithms are intellectual-property hotbeds; patent families filed in 2025 rose 38% year-over-year, suggesting that data analytics rather than hardware alone will anchor future pricing power. Component shortages persist—RF capacitors for impedance circuits remain on FDA’s shortage list—favoring vertically integrated companies that dual-source silicon dies.

White-space persists in office-based labs where portable, tablet-controlled generators priced under USD 25,000 could displace basic monopolar pens. Durability also differentiates; Olympus offers 40-cycle guaranteed handpieces, twice the reusable lifespan of generic options, shaving USD 14 per case after sterilization cost offsets. As hospitals scrutinize carbon footprints, manufacturers marketing handpieces with recyclable polymer housings may tap ESG-linked procurement funds, another dimension of competition beyond fee schedules and capital discounts.

Advanced Bipolar Direct Energy Devices Industry Leaders

Medtronic

Johnson & Johnson

B. Braun Melsungen AG

Olympus Corporation

Conmed Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Erbe Elektromedizin released the VIO 3n, a specialty-configured generator family, alongside VIO seal, its first console dedicated solely to bipolar applications.

- March 2025: Johnson & Johnson launched the Dualto multi-energy generator, compatible with its forthcoming Ottava robotic platform and capable of powering monopolar, bipolar, ultrasonic, and advanced bipolar instruments.

Global Advanced Bipolar Direct Energy Devices Market Report Scope

As per the scope of the report, advanced bipolar direct energy devices are sophisticated medical or aesthetic tools that utilize bipolar radiofrequency or similar energy modalities to deliver targeted electrical energy to tissues.

The segmentation of the advanced bipolar direct energy devices market is categorized by product type, end user, application, and geography. By product type, the market includes electrosurgical generator systems, bipolar electrosurgical devices, vessel-sealing systems, bipolar forceps, and advanced bipolar scissors. By end user, it is segmented into hospitals, ambulatory surgical centers, clinics, and others. By application, the market covers general surgery, gynecology, cardiovascular, neurosurgery, and others. By geography, the segmentation includes North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Electrosurgical Generator Systems | |

| Bipolar Electrosurgical Devices | Vessel-Sealing Systems |

| Bipolar Forceps | |

| Advanced Bipolar Scissors |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Others |

| General Surgery |

| Gynecology |

| Cardiovascular |

| Neurosurgery |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Electrosurgical Generator Systems | |

| Bipolar Electrosurgical Devices | Vessel-Sealing Systems | |

| Bipolar Forceps | ||

| Advanced Bipolar Scissors | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Others | ||

| By Application | General Surgery | |

| Gynecology | ||

| Cardiovascular | ||

| Neurosurgery | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What revenue is expected for advanced bipolar direct energy devices in 2031?

The segment is projected to reach USD 4.94 billion by 2031, expanding at an 8.41% CAGR from its 2026 baseline.

Which product type is growing fastest?

Electrosurgical generator systems are advancing at 12.25% CAGR because hospitals favor modular consoles that power multiple energy modalities.

Why are ambulatory surgery centers important buyers?

ASCs secure separate CMS pass-through payments for advanced energy devices, letting them finance capital purchases despite tighter budgets.

Which application is forecast to lead growth?

Neurosurgery is set to post a 12.15% CAGR to 2031, driven by precision forceps that minimize thermal injury in delicate neural tissue.

How will Asia-Pacific influence market dynamics?

Asia-Pacific is rising at 11.51% CAGR, propelled by India's PLI subsidies and China's Healthy China 2030 funding that lower acquisition costs.

Who are the key competitors to watch through 2031?

Johnson & Johnson, Olympus, Medtronic, and B. Braun will remain pivotal as they roll out multi-energy generators and robotic-compatible instruments.

Page last updated on: