Adenomyosis Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

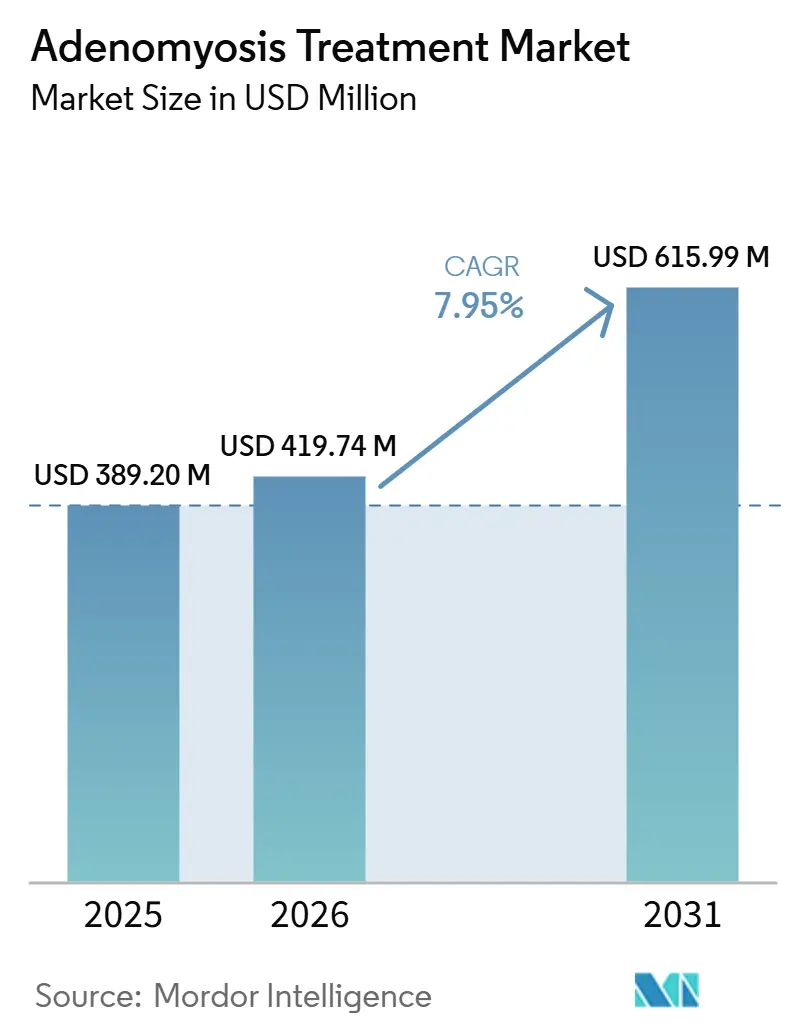

| Market Size (2026) | USD 419.74 Million |

| Market Size (2031) | USD 615.99 Million |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

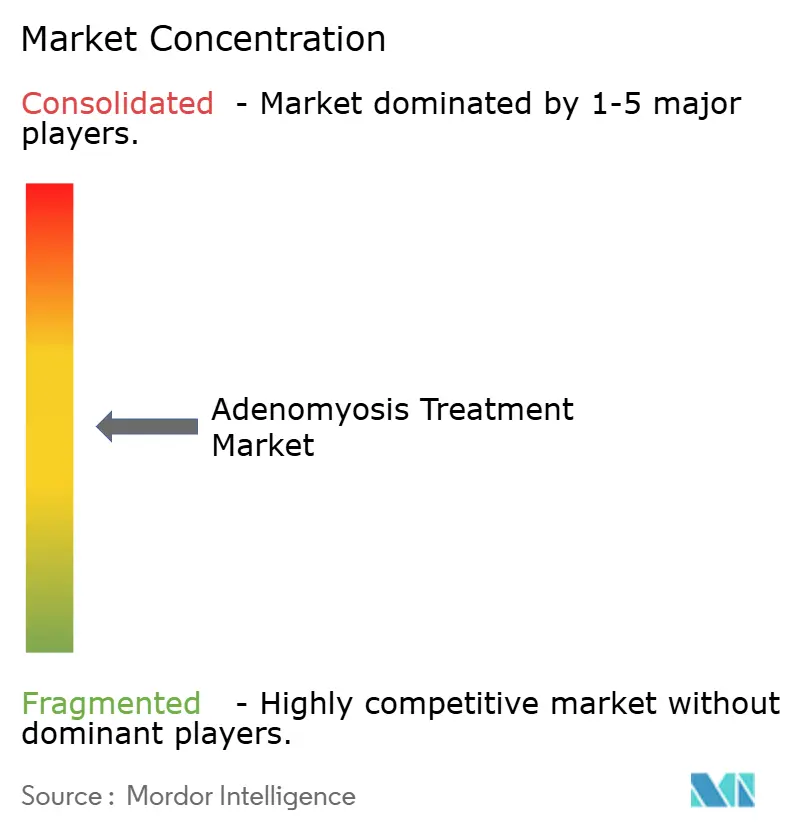

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adenomyosis Treatment Market Analysis by Mordor Intelligence

The Adenomyosis Treatment Market size is projected to expand from USD 389.20 million in 2025 and USD 419.74 million in 2026 to USD 615.99 million by 2031, registering a CAGR of 7.95% between 2026 to 2031.

The adenomyosis treatment market is expanding because diagnosed case volumes are rising faster than underlying recognition has historically allowed, and that keeps the treated patient pool well below the actual clinical burden even now. A 2025 systematic review covering 198.9 million women across 127 studies found prevalence at 41% to 49% in symptomatic gynecological populations and 31% among women with infertility, which supports the view that the adenomyosis treatment market still has meaningful room to grow as diagnosis improves.[1]Wang MH et al., “Global Prevalence of Adenomyosis and Endometriosis, A Systematic Review and Meta-Analysis,” Reproductive Biology and Endocrinology, pmc.ncbi.nlm.nih.gov The adenomyosis treatment market is also benefiting from a clear care model change, as treatment is moving away from hysterectomy as the default endpoint and toward hormonal suppression, uterus-sparing procedures, and more tailored sequencing based on patient profile. Competitive activity is rising because pharmaceutical companies are extending long-term safety evidence for GnRH antagonists while procedural players are strengthening uterus-sparing portfolios through targeted investments and acquisitions. The adenomyosis treatment market also has a durable opportunity base because the absence of disease-specific regulatory labels in major markets still limits prescribing confidence, which means better evidence and clearer pathways can unlock additional demand rather than only redistribute existing demand.

Key Report Takeaways

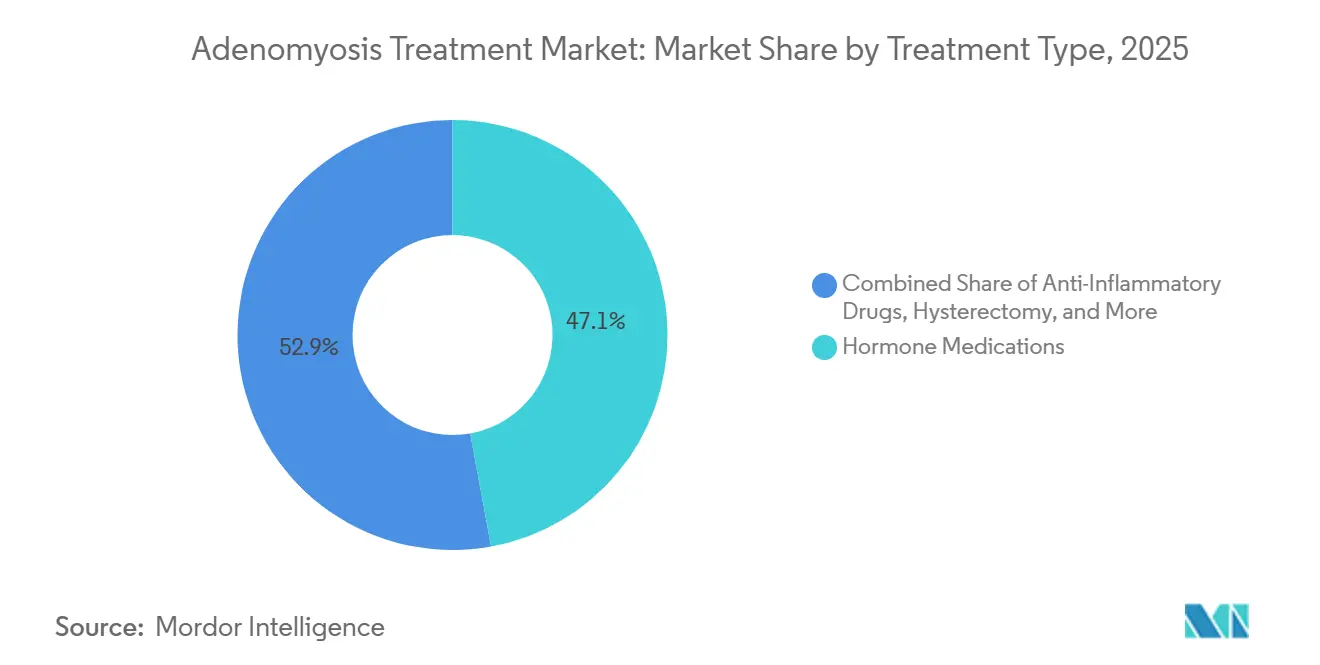

- By treatment type, Hormone Medications held 47.14% of the adenomyosis treatment market share in 2025, while Anti-Inflammatory Drugs are projected to expand at an 8.77% CAGR through 2031.

- By disease type, Diffuse Adenomyosis accounted for 68.13% share in 2025 and is also forecast to record the fastest growth at an 8.63% CAGR through 2031.

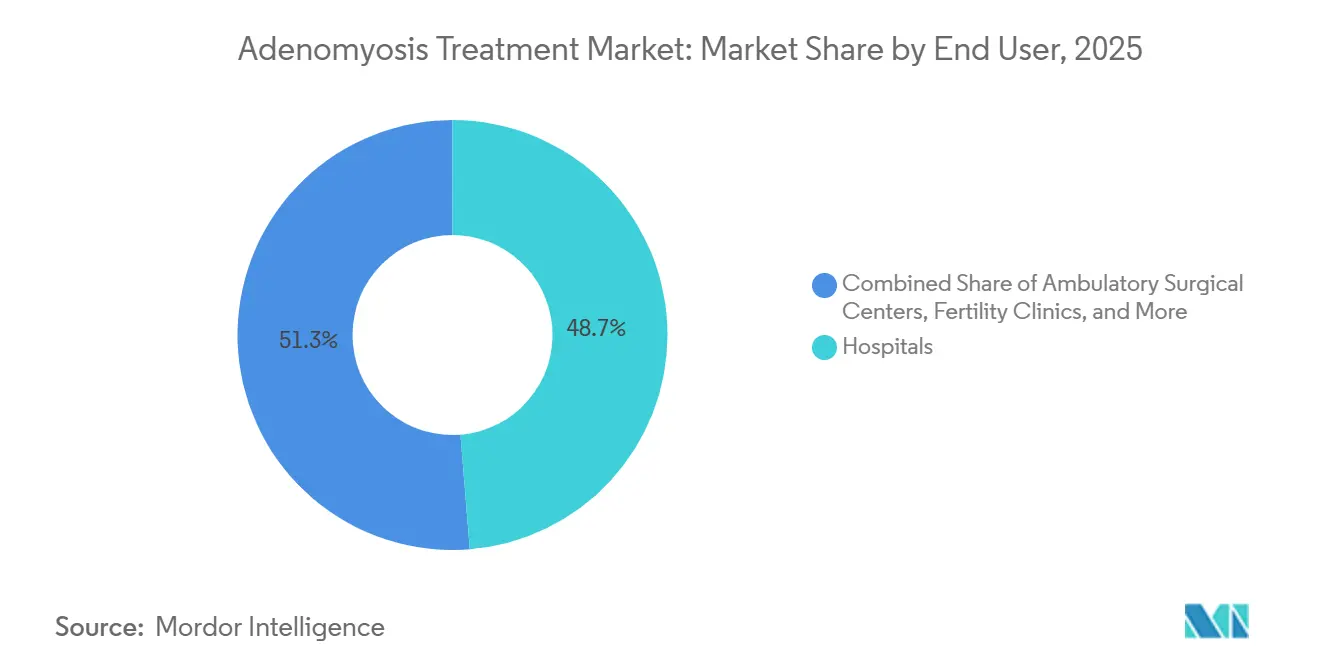

- By end user, Hospitals captured 48.73% share in 2025, while Specialty Gynecology Centers are expected to grow at a 9.03% CAGR through 2031.

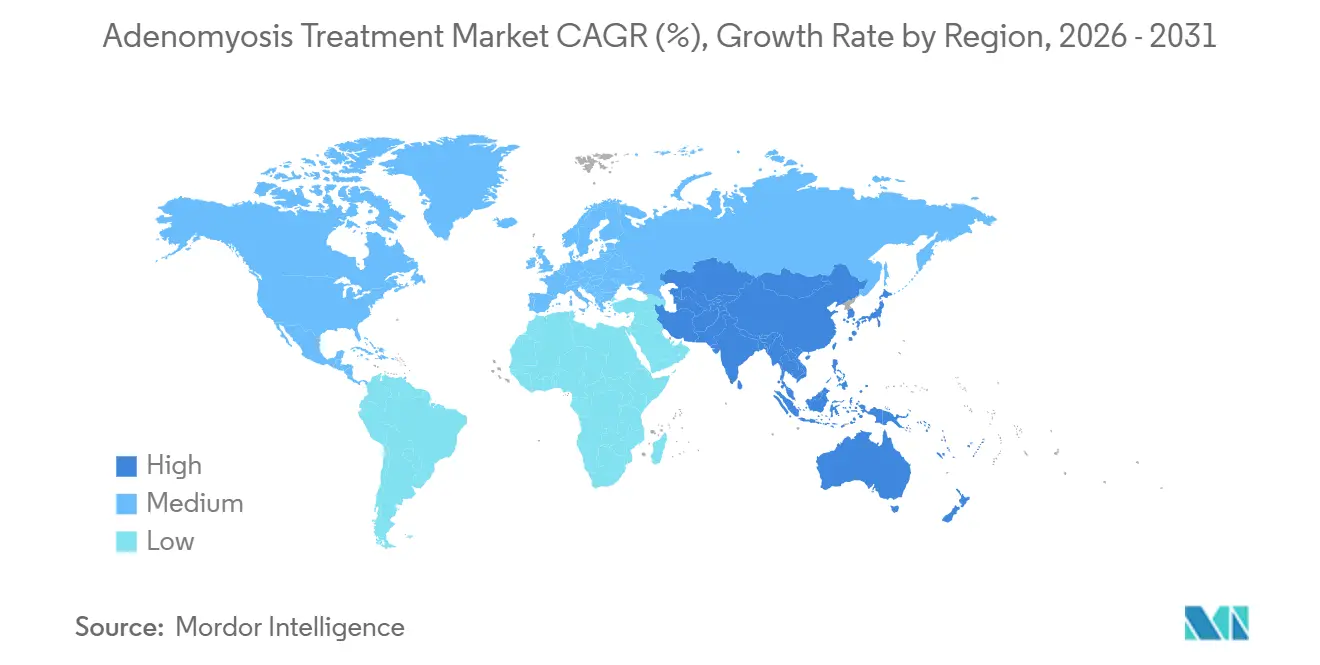

- By geography, North America held 38.12% share of the adenomyosis treatment market in 2025, while Asia-Pacific is projected to advance at a 9.16% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Adenomyosis Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Detection of Underdiagnosed Cases | +1.6% | Global | Short term (≤ 2 years) |

| Fertility-Preserving Hormonal Therapy Adoption | +1.4% | North America & EU | Medium term (2-4 years) |

| Shift Toward Uterus-Sparing Minimally Invasive Procedures | +1.1% | APAC & North America | Medium term (2-4 years) |

| Expansion of Specialty Women’s Health Referral Networks | +0.9% | North America & EU | Medium term (2-4 years) |

| AI-Assisted Pelvic Imaging Triage and Phenotyping | +0.7% | Global | Long term (≥ 4 years) |

| Outpatient Care Migration for Symptom Control Pathways | +0.6% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diagnostic Detection of Previously Underdiagnosed Cases

The adenomyosis treatment market is gaining from a diagnosis shift because adenomyosis was long identified after hysterectomy rather than through routine outpatient workup. Transvaginal ultrasound protocols aligned with the Morphological Uterus Sonographic Assessment criteria are now making non-invasive diagnosis more practical in everyday gynecology settings, which is widening the treatable patient pool beyond historically recognized volumes. This matters for the adenomyosis treatment market because low reported prevalence in many countries does not signal low burden; it more often signals low detection and inconsistent imaging workflows. As structured imaging training spreads and secondary cities gain better access to gynecological ultrasound infrastructure, more symptomatic women are likely to enter treatment earlier rather than remain untreated for years. The commercial effect is important because growth in treated volumes can continue even before any major therapy breakthrough arrives, simply through better identification of existing cases. That is why the adenomyosis treatment market has stronger underlying support than prescription counts alone might suggest, especially where current diagnosis rates still trail real-world symptom burden.

Fertility-Preserving Hormonal Therapy Adoption

The adenomyosis treatment market is also advancing because oral GnRH antagonists are changing the profile of long-term hormonal management for women who want symptom control without immediate definitive surgery. Compared with older GnRH agonist use, newer antagonists allow more controlled estrogen management, which supports longer treatment duration and broadens the group of women who can remain on therapy. A 2025 phase 3 analysis of elagolix with add-back therapy reported stable bone mineral density across 60 months, and that materially improves the risk discussion around prolonged hormonal use in premenopausal women.[2]Sanjay K. Agarwal et al., “Bone Mineral Density with Elagolix Plus Add-Back Therapy in Women with Heavy Menstrual Bleeding and Uterine Fibroids, Open-Label and Post-Treatment Results of a 60-Month Phase 3 Trial,” AJOG Global Reports, doi.org The adenomyosis treatment market benefits because longer safe treatment windows can raise both therapy persistence and physician willingness to escalate from symptomatic control to more structured disease management. This dynamic is becoming more relevant in Asia as well, since Kissei initiated a Phase III linzagolix trial for endometriosis and adenomyosis in Japan in March 2025 after regulatory progress around the compound, showing that regional development activity is converging with Western programs. The result is a broader fertility-aware treatment pathway in which hormonal therapy is no longer framed only as a short bridge before surgery.

Shift Toward Uterus-Sparing Minimally Invasive Procedures

The adenomyosis treatment market is being reshaped by the growing acceptance of uterus-sparing interventions for patients who decline hysterectomy or are not good candidates for it. High-intensity focused ultrasound, uterine artery embolization, and radiofrequency ablation have moved closer to routine use because multiple clinical and guideline sources now recognize their role in symptom control and uterus preservation. This has practical importance for the adenomyosis treatment market because it expands the care pathway rather than replacing one product class with another, and that supports revenue across devices, imaging, follow-up care, and adjunctive drugs. Hologic strengthened this area in January 2025 by completing the USD 350 million acquisition of Gynesonics, adding the Sonata System and signaling a stronger strategic commitment to incisionless or low-incision gynecologic treatment platforms.[3]Hologic, Inc., “Hologic Completes Acquisition of Gynesonics, Inc.,” BusinessWire, businesswire.com Better fertility outcome evidence after HIFU is also improving physician confidence in recommending procedure-based care to reproductive-age patients who once faced a narrow choice between symptom relief and future fertility. As a result, the adenomyosis treatment market is seeing a more balanced split between medical and interventional pathways, which helps sustain demand across a wider treatment mix.

AI-Assisted Pelvic Imaging Triage and Phenotyping

The adenomyosis treatment market is beginning to feel the effect of AI-enabled imaging because classification tools are moving beyond basic detection and toward treatment-relevant phenotyping. Deep learning studies in ultrasound imaging have shown strong potential for more standardized identification of adenomyosis, which reduces dependence on highly variable observer interpretation. A multicenter model development study registered on ClinicalTrials.gov is advancing this approach through structured ultrasound datasets and formal validation design, which indicates that workflow integration is moving from concept to clinical testing. The adenomyosis treatment market stands to benefit because more reliable first-contact triage can reduce long empirical treatment cycles, shorten the time to effective therapy, and improve patient retention in specialty care pathways. This is commercially relevant because centers that pair advanced imaging with treatment selection can differentiate themselves on efficiency, outcomes, and patient experience rather than only on procedure availability. Over time, the adenomyosis treatment market could see a prescription cascade that starts with phenotyped referral rather than generalized trial-and-error care, and that would favor companies aligned with imaging-led treatment protocols.a

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Disease-Specific Treatment Guidelines and Standardized Pathways | -0.7% | Global | Medium term (2-4 years) |

| Symptom Recurrence After Conservative Therapy | -0.6% | Global | Short term (≤ 2 years) |

| Limited Access to Specialized Gynecology and Interventional Capacity | -0.5% | APAC, MEA, South America | Long term (≥ 4 years) |

| High Cost and Fertility Trade-Offs of Procedural Interventions | -0.4% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Disease-Specific Treatment Guidelines and Standardized Pathways

The adenomyosis treatment market still faces a basic structural limit because no drug carries a regulatory label specifically for adenomyosis in major markets, and hormonal use remains largely off-label. A 2025 systematic review and network meta-analysis found no harmonized treatment ranking across the available randomized evidence, with outcomes varying depending on whether the focus was pain, bleeding, or uterine size reduction. That uncertainty slows the adenomyosis treatment market because general gynecologists may hesitate to initiate or escalate therapy when treatment sequencing is not standardized. Germany’s updated S2k guidance in 2025 moved practice toward imaging-first diagnosis and more personalized sequencing, but broader community adoption still depends on how quickly payers and routine practice absorb those recommendations. Until clearer disease-specific pathways are widely embedded, the adenomyosis treatment market is likely to continue showing uneven uptake across providers, even where therapeutic options themselves are available. This restraint is especially important because it affects initiation rates, reimbursement discussions, and confidence in higher-cost or longer-duration therapy plans at the same time.

Symptom Recurrence After Conservative Therapy

The adenomyosis treatment market is also constrained by clinically meaningful symptom recurrence after hormonal management or uterus-sparing ablation. Recurrence keeps many patients in a repeated cycle of symptom control, escalation, and re-intervention, which maintains healthcare contact but weakens confidence in non-definitive treatment pathways. The problem is more visible in progesterone-resistant groups, where first-line options such as LNG-IUS or dienogest may not deliver durable control and later escalation becomes necessary. Studies in 2024 and 2025 showed that HIFU combined with hormonal adjuncts can lower recurrence versus HIFU alone, but the added cost and treatment complexity remain real barriers to broader use. For the adenomyosis treatment market, this creates a mixed picture in which long-term patient engagement supports volume, yet payers and clinicians still question whether repeated therapy cycles deliver enough value. That tension is likely to keep outcome scrutiny high, especially in systems that rely on centralized or benchmarked reimbursement reviews.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Hormone Medications Lead, Anti-Inflammatories Grow Faster

Hormone Medications held 47.14% of the adenomyosis treatment market size in 2025, reflecting the deep use of progestins, combined oral contraceptives, and newer GnRH receptor antagonists across routine care. This leading position in the adenomyosis treatment market rests on the fact that medical therapy often remains the first structured option before physicians consider procedural intervention or definitive surgery. Dienogest continues to hold a strong prescribing position because it combines once-daily dosing with a tolerability profile that supports repeat use and physician familiarity. The same 2025 network meta-analysis reinforced that preference by identifying dienogest as the most effective hormone therapy for adenomyosis-associated pelvic pain at 3 and 6 months.[4]A. Etrusco et al., “Efficacy and Safety of Hormone Therapies for Treating Adenomyosis-Associated Pelvic Pain, A Systematic Review and Network Meta-Analysis of Randomized Controlled Trials,” Frontiers in Endocrinology, frontiersin.org LNG-IUS remains an important part of the segment as well because it offers long-acting symptom control with limited systemic estrogen suppression and retains guideline support across multiple clinical settings.

Anti-Inflammatory Drugs are the fastest-growing treatment type in the adenomyosis treatment market, with an 8.77% CAGR through 2031, largely because they remain widely used as co-prescriptions for acute symptom relief. Their role is especially relevant where reimbursement delays, physician preference, or patient hesitation around endocrine treatment constrain access to hormonal agents. Hysterectomy still occupies a stable place in the adenomyosis treatment market. Still, its role has narrowed because fertility-preserving and uterus-sparing options now cover more of the treatment pathway than before. That means hysterectomy is increasingly reserved for women who have completed childbearing or for those whose conservative care has failed after multiple attempts. The Others category also deserves attention because pipeline activity, such as the registered nintedanib trial for adenomyosis-associated infertility, shows that the adenomyosis treatment industry is beginning to test mechanisms that go beyond symptom suppression.

By Disease Type: Diffuse Adenomyosis Anchors Volume and Growth

Diffuse Adenomyosis represented 68.13% of the adenomyosis treatment market size in 2025 and is expected to record the fastest 8.63% CAGR through 2031. That dual position is unusual, because the same subtype that already leads the adenomyosis treatment market is also the one advancing the fastest. The explanation lies in disease burden, since diffuse disease is tied to broader myometrial infiltration, heavier bleeding, larger uterine volume, and a higher chance of treatment failure than more localized forms. Those clinical features translate into more treatment attempts, longer care journeys, and greater need for sequencing between hormonal and procedural interventions. For the adenomyosis treatment market, that means diffuse disease generates both higher patient intensity and stronger repeat engagement with the healthcare system than focal disease typically does.

Focal Adenomyosis remains smaller in the adenomyosis treatment market, but it is gaining attention because it is often more responsive to targeted intervention. Conservative surgical management literature in 2025 supported focal excision in appropriately selected women and highlighted the relevance of careful pre-operative evaluation when fertility outcomes matter. This makes focal disease more suitable for centers that combine imaging strength with specialized procedural capability, particularly when patients are seeking a uterus-preserving path. The practical value for the adenomyosis treatment market is that better subtype differentiation can sharpen therapeutic triage and reduce the mismatch between patient profile and treatment selection. As imaging-led stratification improves, the adenomyosis treatment industry is likely to see more focused interventional demand in focal cases while diffuse disease continues to dominate overall volume and longitudinal care needs.

By End User: Hospitals Lead, Specialty Gynecology Centers Set the Growth Pace

Hospitals captured 48.73% of the adenomyosis treatment market share in 2025 because they remain the main access point for complex cases that require integrated imaging, inpatient support, interventional management, or surgery. Their leadership in the adenomyosis treatment market is still supported by procedural volumes, especially where hysterectomy and uterine artery embolization are concentrated in hospital-based gynecology departments. Hospitals also benefit from referral patterns in severe bleeding, pain, infertility overlap, and treatment-refractory disease, all of which raise the need for multidisciplinary evaluation. Fertility Clinics are smaller in value terms, but they hold strategic weight because adenomyosis is strongly linked with subfertility and therefore continues to generate referrals from reproductive medicine specialists. That connection keeps the adenomyosis treatment market closely tied to IVF preparation, uterine receptivity management, and patient selection for more intensive symptom control before assisted reproduction.

Specialty Gynecology Centers are the fastest-growing end-user category in the adenomyosis treatment market, with a 9.03% CAGR through 2031, because they are well placed to consolidate diagnosis, counseling, and tailored care. These centers are often better positioned than general outpatient departments to invest in dedicated ultrasound capability, structured treatment planning, and higher-value follow-up services. The end-user mix in the adenomyosis treatment market is therefore shifting toward settings that can manage both medication sequencing and referral into minimally invasive procedures with less fragmentation. Ambulatory Surgical Centers are also gaining momentum as gynecologic procedures move into lower-acuity settings, which supports greater patient convenience and puts pressure on hospital-centered elective care economics. This gradual migration does not remove hospitals from the care model, but it does broaden where the adenomyosis treatment market can generate procedure volume and patient retention over time.

Geography Analysis

North America held 38.12% of the adenomyosis treatment market share in 2025, making it the largest regional contributor by value. The region’s position in the adenomyosis treatment market reflects established reimbursement pathways for hormonal agents, strong women’s health referral networks, and a dense base of specialty practices that can recognize and manage the condition earlier. The United States remains the key country because long-term safety evidence for GnRH antagonists has strengthened payer and prescriber confidence, especially around extended treatment use.

Europe remains the second-largest regional bloc in the adenomyosis treatment market and shows a more mixed structure because reimbursement and treatment adoption differ materially across countries. Germany plays an outsized role because health technology assessment decisions and pricing review shape how newer hormonal therapies enter practice, as shown by the June 2025 G-BA resolution on linzagolix.[5]G-BA, “Resolution on Linzagolix D-1147,” Federal Joint Committee, g-ba.de The updated German S2k guidance also supports imaging-confirmed diagnosis and gestagen-first sequencing, which helps standardize care but can slow early uptake of premium therapy where comparator expectations remain strict. Across the wider region, the adenomyosis treatment market is therefore shaped less by unmet need alone and more by how quickly guideline alignment turns into routine reimbursement and prescribing behavior.

Asia-Pacific is the fastest-growing region in the adenomyosis treatment market, with a 9.16% CAGR through 2031, driven by large patient pools, maturing hormonal protocols, and rising private and tertiary care investment. Japan is important because multiple GnRH antagonist programs are progressing at the same time, including Kissei’s Phase III work for linzagolix in endometriosis and adenomyosis, which strengthens the region’s therapeutic depth. China supports growth through dedicated endometriosis and adenomyosis care centers and comparatively strong HIFU adoption, which gives the procedural side of the adenomyosis treatment market a stronger footing than in many Western settings.

Competitive Landscape

The adenomyosis treatment market shows moderate concentration in pharmaceuticals and greater fragmentation in devices and procedures. AbbVie, Bayer, Takeda, and Organon hold important positions in the adenomyosis treatment market through established hormonal therapy portfolios. At the same time, Hologic and Medtronic compete more directly in procedure-enabling platforms and adjacent women’s health devices. No single company controls more than one-fifth of total value, and that leaves room for repositioning because most therapies still lack adenomyosis-specific labels. Bayer has one of the strongest fits with current clinical practice through Mirena and Visanne, both of which align well with symptom control pathways already used in routine care. That position gained further strategic support when Bayer initiated the Phase III SUNFLOWER study in December 2025 to expand the clinical evidence base for Mirena in adjacent uterine conditions.

AbbVie remains well placed in the adenomyosis treatment market because long-term safety evidence around elagolix with add-back therapy improves differentiation versus older injectable suppression options. Hologic also strengthened its strategic position when it completed the Gynesonics acquisition in January 2025, adding a real-time ultrasound-guided radiofrequency ablation platform that fits the move toward uterus-sparing intervention. In April 2026, Blackstone and TPG completed the USD 18.30 billion privatization of Hologic, which could support faster product development and investment focus outside public market reporting cycles. These moves show that competition in the adenomyosis treatment market is not limited to drug development; it also includes ownership structure, platform breadth, and procedural ecosystem control.

White-space opportunity in the adenomyosis treatment market remains strongest around disease-specific regulatory submissions and tighter links between imaging phenotyping and treatment selection. Any company that secures a clear adenomyosis label would gain a durable narrative advantage because today’s market still relies heavily on off-label prescribing logic. Kissei’s Phase III linzagolix program in Japan is therefore strategically important, since it signals that competitive positioning is moving closer to indication-focused development rather than only adjacent gynecologic use. The adenomyosis treatment market is also becoming more difficult to enter on the technology side because imaging-linked workflow, precision ablation capability, and specialized referral systems are increasingly connected rather than sold as isolated tools. That combination favors companies that can support a broader care pathway, while smaller entrants may need to compete through focused niches, partnerships, or highly targeted evidence generation.

Adenomyosis Treatment Industry Leaders

AbbVie Inc.

Bayer AG

Ferring B.V.

Organon and Co.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Blackstone and TPG completed the USD 18.3 billion privatization of Hologic, appointing José Almeida as CEO. The transaction, including minority stakes from ADIA and GIC, positions Hologic to accelerate product development and geographic expansion in women's health, including minimally invasive gynecological surgery relevant to adenomyosis and uterine disease.

- June 2025: The German Federal Joint Committee (G-BA) published its resolution on linzagolix for endometriosis, concluding that no additional benefit over appropriate comparator therapy had been proven, a health technology assessment outcome that directly shapes reimbursement negotiations across Europe's largest pharmaceutical market.

- March 2025: Kissei Pharmaceutical initiated a Phase III clinical trial for linzagolix (KLH-2109) in endometriosis/adenomyosis in Japan, following the compound's successful Phase III fibroid readout and a new drug application accepted by Japan's PMDA. Phase III completion is targeted for 2027-2028, with commercial implications for the Asia-Pacific GnRH antagonist market.

- December 2025: Bayer initiated the Phase III SUNFLOWER study evaluating Mirena® 52mg LNG-IUS in nonatypical endometrial hyperplasia across approximately 90 centres in 3 countries, reinforcing its strategy to expand the clinical evidence base for Mirena in adjacent uterine conditions beyond its existing approved indications.

Global Adenomyosis Treatment Market Report Scope

The Adenomyosis Treatment Market comprises pharmaceutical therapies, medical interventions, and surgical procedures used to manage the symptoms and progression of adenomyosis, a benign uterine disorder characterized by the presence of endometrial tissue within the myometrium. The market is driven by the rising prevalence of chronic pelvic pain, heavy menstrual bleeding, and infertility associated with the disease, along with increasing awareness and earlier diagnosis through advanced imaging techniques.

The adenomyosis treatment market is segmented by treatment type, disease type, end user, and geography. By treatment type, it is further divided into anti-inflammatory drugs, hormone medications, hysterectomy, and others. By disease type, it is segmented into diffuse adenomyosis and focal adenomyosis. By end user, the market is segmented into hospitals, specialty gynecology centers, ambulatory surgical centers, fertility clinics, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Hormone Medications |

| Hysterectomy |

| Others (Antifibrinolytics, Analgesics, etc.) |

| Diffuse Adenomyosis |

| Focal Adenomyosis |

| Hospitals |

| Specialty Gynecology Centers |

| Ambulatory Surgical Centers |

| Fertility Clinics |

| Others (Academic and Research Institutes, Homecare Settings, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| Anti-Inflammatory Drugs | Hormone Medications | |

| Hysterectomy | ||

| Others (Antifibrinolytics, Analgesics, etc.) | ||

| By Disease Type | Diffuse Adenomyosis | |

| Focal Adenomyosis | ||

| By End User | Hospitals | |

| Specialty Gynecology Centers | ||

| Ambulatory Surgical Centers | ||

| Fertility Clinics | ||

| Others (Academic and Research Institutes, Homecare Settings, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and outlook for adenomyosis treatment?

The adenomyosis treatment market was valued at USD 389.20 million in 2025, stands at USD 419.74 million in 2026, and is forecast to reach USD 615.99 million by 2031 at a 7.95% CAGR.

Which therapy category leads revenue today?

Hormone Medications led with 47.14% share in 2025 because they remain the most established first-line structured option across symptom control and longer treatment pathways.

Which disease subtype drives the largest demand?

Diffuse Adenomyosis accounted for 68.13% share in 2025 and is also projected to grow the fastest at an 8.63% CAGR, reflecting higher symptom burden and longer treatment engagement.

Which care setting is growing the fastest?

Specialty Gynecology Centers are expected to expand at a 9.03% CAGR through 2031 as they consolidate diagnosis, treatment planning, and referral into minimally invasive care.

Which region offers the strongest growth opportunity?

Asia-Pacific is forecast to grow at a 9.16% CAGR through 2031, supported by large patient pools, rising specialty capacity, and stronger adoption of both hormonal and uterus-sparing approaches.

What is holding back wider adoption of newer therapies?

The biggest barriers are the lack of adenomyosis-specific regulatory labels and persistent symptom recurrence after conservative therapy, both of which slow physician confidence and payer support.

Page last updated on: