ADC Drug CDMO Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 6.21 Billion |

| Growth Rate (2026 - 2031) | 25.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ADC Drug CDMO Service Market Analysis by Mordor Intelligence

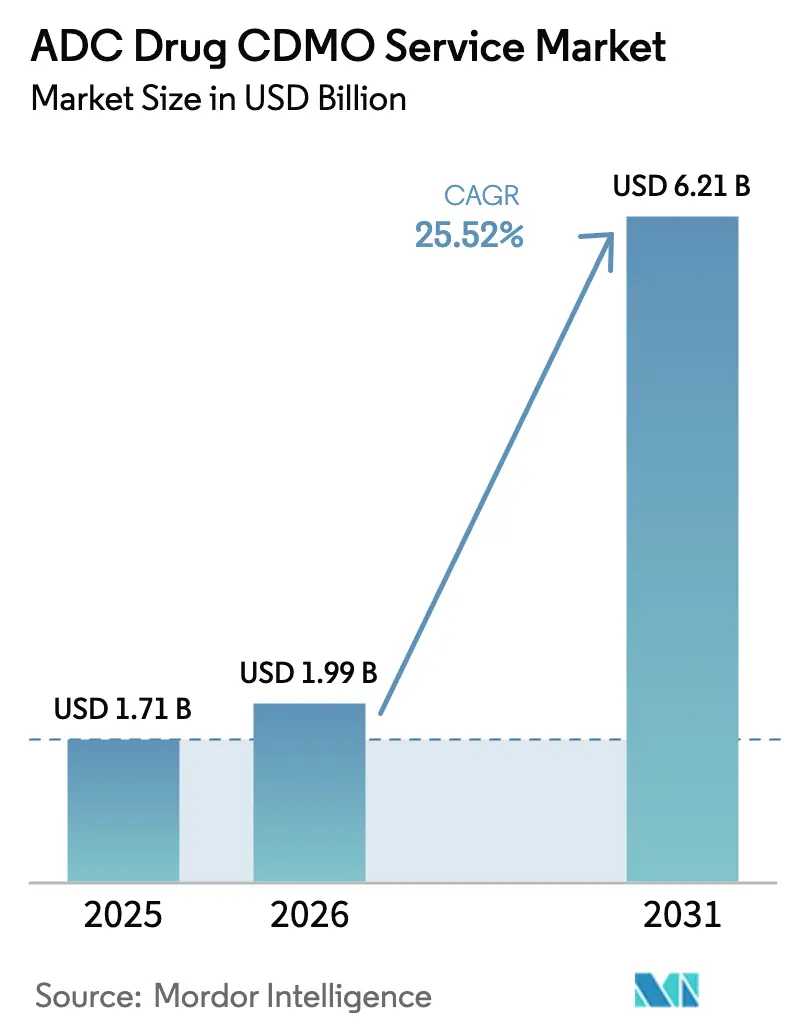

The ADC Drug CDMO Service Market size is projected to expand from USD 1.71 billion in 2025 and USD 1.99 billion in 2026 to USD 6.21 billion by 2031, registering a CAGR of 25.52% between 2026 to 2031.

Favorable regulatory momentum and a steady shift by sponsors toward outsourcing high-containment operations are accelerating project flow across preclinical, clinical, and commercial stages. The strongest near-term lift comes from the record pace of ADC regulatory designations and sponsors’ preference to avoid capital-heavy HPAPI builds, which supports sustained bookings and higher utilization of purpose-built suites. Capacity expansions by leading CDMOs are smoothing bottlenecks in conjugation and fill-finish, while specialized capabilities in linker chemistry and site-specific conjugation are emerging as key differentiators. Geographic investment patterns are also reshaping supply options as North America anchors approvals and Asia-Pacific broadens multi-product ADC footprints through new suites and integrated offerings.

Key Report Takeaways

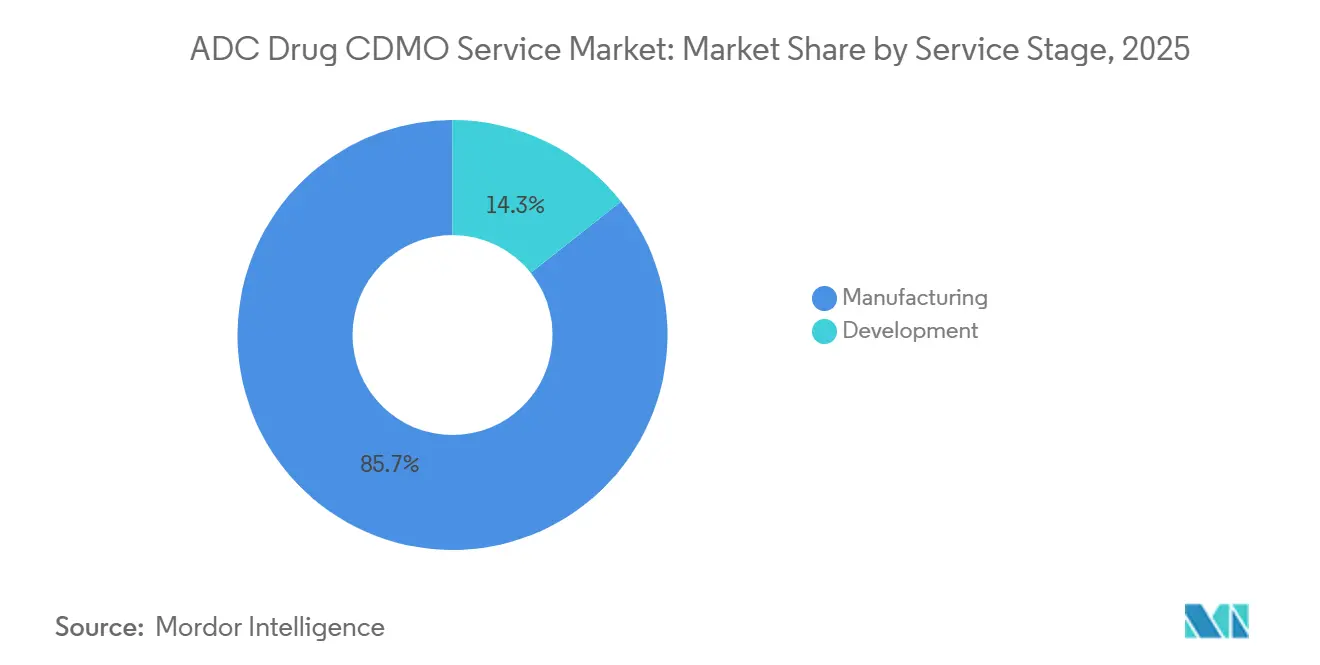

- By service stage, manufacturing services accounted for 85.67% in 2025. Development services are projected to grow at a 27.10% CAGR through 2031.

- By linker type, cleavable linkers led with a 66.23% share in 2025. Cleavable linkers are forecast to expand at a 26.41% CAGR through 2031.

- By therapeutic area, multiple myeloma accounted for 45.10% of the market in 2025. Lymphoma applications are projected to record a 28.10% CAGR through 2031.

- By component, antibody manufacturing accounted for 40.23% of the market in 2025. Antibody manufacturing is projected to grow at a 27.14% CAGR through 2031.

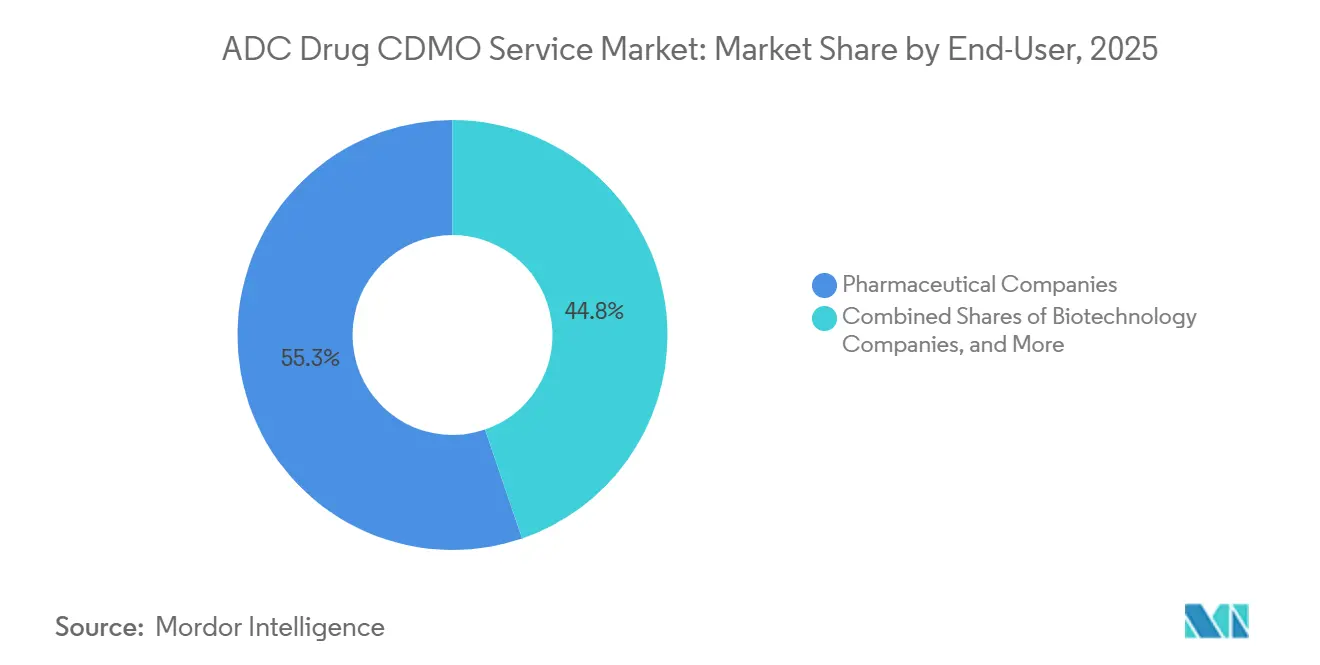

- By end-user, pharmaceutical companies accounted for 55.25% of 2025 revenue. Biotechnology companies are projected to grow at a 27.65% CAGR through 2031.

- By region, North America accounted for 41.25% in 2025. Asia-Pacific is projected to expand at a 28.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ADC Drug CDMO Service Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Robust clinical-stage ADC pipeline expansion | +6.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Outsourcing trend to avoid HPAPI capital expenditure | +5.2% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Rising demand for targeted oncology therapies | +4.9% | Global | Long term (≥ 4 years) |

| Regulatory support and expedited pathway | +4.3% | North America, Europe, with spillover to APAC | Medium term (2-4 years) |

| Technical advances in ADC technologies | +3.7% | North America, Europe, APAC advanced markets | Medium term (2-4 years) |

| Government biodefense subsidies for domestic HPAPI | +3.1% | North America and EU, with emerging focus in Japan and South Korea | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust Clinical-Stage ADC Pipeline Expansion

By 2025, the clinical pipeline will feature more than 200 ADC candidates targeting over 50 antigens, with 41 assets already in Phase III, intensifying CDMO demand for tox batches, Phase I material, and commercial conjugation.[1]Asher Mullard, “FDA Approvals in 2024: A Surge in Antibody-Drug Conjugates,” Nature Reviews Drug Discovery, nature.com The breadth of antigens and late-stage programs is compressing timelines under expedited pathways, which increases the value of CDMOs that can scale across phases without revalidation. Large sponsors continue to rely on multiple CDMO partners to reduce supply risk across parallel trials, as highlighted by portfolio redeployments after recent acquisitions and trial clustering for key ADCs. The emergence of bispecific constructs and dual payloads is increasing analytical complexity, pushing method development and validation cycles to 10 months for specific programs. These shifts are driving higher utilization across high-containment suites and favoring CDMOs with orthogonal conjugation chemistries, robust DAR control, and late-stage readiness.

Outsourcing Trend to Avoid HPAPI Capital Expenditure

Building OEB 5 HPAPI facilities with dedicated air-handling systems costs USD 150 million to USD 200 million. It takes 30 months to achieve GMP readiness, which many venture-backed developers cannot absorb within financing windows. This cost and time profile drives a clear preference for multi-product suites at established CDMOs and supports premium pricing for conjugation and fill-finish slots. Sponsors in North America and Europe face strict cross-contamination controls, which further elevate the advantage of CDMOs with proven containment and electronic records compliance. Providers are bundling antibody production, payload synthesis, conjugation, and drug product under a single quality framework to streamline oversight and accelerate tech transfer from 9 months to 6 months in well-characterized platforms. The result is steady demand across the ADC drug CDMO service market, as integrated offerings reduce sponsor risk and capital intensity while improving speed to clinic.

Rising Demand for Targeted Oncology Therapies

Global cancer incidence is projected to reach 35 million new cases in 2050, up 77% from 20 million cases in 2022, which underscores persistent demand for targeted therapies that balance efficacy and tolerability.[2]American Chemical Society, “ACS Workforce Survey 2025: Chemical Professionals in Biopharmaceuticals,” ACS, acs.org ADCs enable targeted delivery of cytotoxic payloads through antigen-specific antibodies, which is widening payer acceptance as real-world outcomes strengthen in broader subpopulations. Medicare coverage decisions have expanded access to specific agents, lifting treatment-eligible groups and reinforcing near-term demand for commercial-scale conjugation and fill-finish. Growth in HER2-low and other biomarker-defined populations also increases process requirements, including higher antibody titers during conjugation to meet volume needs for expanding labels. Combination regimens, including ADCs alongside checkpoint inhibitors, are improving response rates in priority indications, further increasing the CDMO workload for dual-supply and coordinated release.

Technical Advances in ADC Technologies

Transitioning from stochastic to site-specific conjugation reduces heterogeneity. It improves the therapeutic index, thereby reducing batch-to-batch DAR variability from legacy ranges toward tighter control windows that regulators now expect. Engineered cysteines and non-native amino acids enhance DAR precision and improve stability profiles, which are essential for late-stage and commercial runs. Advances in cleavable linkers, including tumor microenvironment-responsive constructs, have reduced off-target toxicity in preclinical settings and prompted sponsors to switch mid-development to improve safety margins. CDMOs are investing in modular platforms that accommodate multiple linkers and payloads while maintaining strict segregation and analytical depth. Providers that combine high-resolution mass spectrometry, hydrophobic interaction chromatography, and orthogonal methods for DAR and impurity control are winning new awards as programs move to pivotal studies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent global HPAPI/ADC GMP regulations | -3.2% | Global, most acute in North America and EU | Short term (≤ 2 years) |

| Cytotoxic precursor supply-chain bottlenecks | -2.8% | Global, with acute shortages in APAC | Medium term (2-4 years) |

| High development and operational cost | -2.4% | North America, Europe | Medium term (2-4 years) |

| Shortage of skilled bioconjugation chemists | -1.9% | Global, most severe in South America and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global HPAPI/ADC GMP Regulations

Recent revisions to sterile manufacturing expectations require continuous environmental monitoring and heightened particulate controls, which force retrofits to isolator-based transfer and closed-loop sampling across HPAPI workflows. Health-based exposure limits and risk-based frameworks raise the bar for containment efficacy, including stringent expectations for OEB 5 operations that stress air-handling performance and validation depth. North American and European facilities undergo more frequent inspections and must maintain electronic batch records compliant with 21 CFR Part 11 and related controls, which intensifies compliance investment. CDMOs unable to meet new standards face constrained eligibility for Western sponsor audits, which concentrates late-stage work among providers with current credentials. These dynamics push up fixed costs and consolidate awards within the ADC Drug CDMO Service market among top-tier operators with proven quality systems.

Cytotoxic Precursor Supply-Chain Bottlenecks

Payload precursor supply tightened as demand for auristatin and maytansinoid classes increased faster than capacity additions at a small set of qualified API producers. Novel payload classes, such as topoisomerase I and RNA polymerase II inhibitors, face even narrower supplier pools, with only a handful of manufacturers having the synthesis expertise and containment to operate at scale. CDMOs are pursuing backward integration to secure payload and linker availability and to reduce qualification cycles that delay tech transfer and scale-up. Geopolitical measures affecting chemical exports have extended lead times and forced qualification of alternative sources, adding months to program schedules and increasing analytical comparability work. Sponsors are dual-sourcing to mitigate risk, but even minor differences in impurity profiles across suppliers can affect conjugation kinetics and stability, adding workload to CMC programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Stage: Development Services Gain as Biotechs Front-Load Risk Mitigation

Development services are projected to grow at a 27.10% CAGR through 2031, while manufacturing services held an 85.67% share in 2025, reflecting the weight of commercial supply against faster early-stage outsourcing. This split reflects a consistent pattern in which venture-backed ADC developers preserve capital by outsourcing IND-enabling packages, toxicology testing, and Phase I materials to accelerate clinical entries. The ADC drug CDMO service market benefits as integrated providers match development work with late-stage scale, reducing the risk of revalidation or process drift at tech transfer. In North America, many pre-IND sponsors have embraced complete externalization of development activities, while larger European sponsors often retain selected upstream capabilities. Platform allowances for repeat linker-payload combinations simplify specific validation steps and shorten timelines for programs that reuse proven conjugation chemistries.

By Linker Type: Cleavable Constructs Lead, Yet Non-Cleavable Gains in Solid Tumors

Cleavable linkers accounted for a 66.23% share in 2025 and are forecast to grow at a 26.41% CAGR through 2031, driven by their efficacy in hematologic malignancies, where rapid intracellular release remains central to clinical outcomes. Sponsors are also evaluating glucuronide-based linkers to improve tumor-selective activation, thereby lowering off-target toxicity while preserving on-target potency in preclinical models. In parallel, the ADC drug CDMO service market is seeing a pivot to non-cleavable constructs for select solid tumors that demand stability in circulation before lysosomal degradation. Non-cleavable thioether linkers have shown lower off-target effects in trials such as HER2-low breast cancer, which is influencing pipeline choices at several large sponsors. This trend shifts CDMO selection toward providers with click-chemistry and analytics tailored for non-cleavable formats and solid tumor programs.

By Therapeutic Area: Lymphoma Surges as BCMA and CD79b Targets Mature

Multiple myeloma applications accounted for 45.10% of the market in 2025, anchored by programs targeting BCMA and related antigens that translate well to scalable manufacturing. Lymphoma programs are projected to expand at a 28.10% CAGR as targets such as CD79b and CD19 advance into later stages, increasing the need for consistent DAR and optimized linker choices. Breast cancer remains an important indication as labels broaden into HER2-low and HR-positive populations, although growth is normalizing as the largest patient pools become served. The ADC drug CDMO service market will continue to benefit from solid tumor combinations, which will raise aggregate drug substance demand across combination partners. Pipeline depth across hematologic malignancies supports consistent lot scheduling and endorses the use of established conjugation platforms at scale.

By Component Service: Conjugation and Purification Capture Premium Pricing

Antibody manufacturing accounted for 40.23% in 2025 and is growing at a 27.14% CAGR, supported by repurposing existing CHO capacity at established biologics CDMOs. Payload synthesis, conjugation, and fill-finish carry greater pricing power because they depend on specialized containment systems, analytical instrumentation, and sterile drug product expertise. CDMOs with end-to-end offerings from cell line through commercial fill-finish increasingly win first-in-class programs where continuity and oversight simplicity are valued. The ADC drug CDMO service market shows an apparent bottleneck in fill-finish, where limited ADC-specific lines and specialized lyophilization or light-protection protocols constrain availability. These constraints reinforce premium pricing for late-stage conjugation and drug product campaigns with validated ADC-specific processes.

By End-User: Biotech Clients Drive Development Demand

Pharmaceutical companies accounted for 55.25% of 2025 CDMO revenue, while biotechnology companies are projected to grow at a 27.65% CAGR as they outsource early-stage activities to preserve cash. This split shapes the service mix: biotech clients emphasize development services, tox batches, and Phase I materials, whereas large pharma prioritizes commercial-scale manufacturing and tech transfer. The ADC drug CDMO service market supports milestone-based pricing for biotech sponsors to balance cash outlays with key clinical events. In contrast, large pharma often negotiates multi-year supply to reduce the cost per gram at scale. Contract structures are therefore adapting to end-user profiles and to the phase of the molecule.

Geography Analysis

North America accounted for 41.25% in 2025, supported by a concentration of ADC developers, expedited regulatory pathways, and funding for domestic high-containment capacity. Sustained use of expedited pathways, including breakthrough therapy designations, has created a predictable path for late-stage programs and faster commercial transitions. The region’s policy focus on resilient supply of critical medicines supports investments in HPAPI capacity, benefiting providers with compliant facilities and scalable footprints. Canada and Mexico are gaining attention for selected services that meet quality expectations at lower cost, including analytics and sterile drug products for specific use cases. Sponsors also adopt dual-source policies in the United States to mitigate disruption risk from payload intermediates and cross-border controls.

Asia-Pacific is projected to expand at a 28.63% CAGR through 2031 as multi-product ADC suites come online in South Korea, China, and Japan. Major CDMOs have commissioned or expanded ADC-specific lines, blending antibody production, conjugation, and fill-finish offerings within integrated campuses. China leads regional capacity growth with dedicated ADC facilities providing end-to-end services at cost positions that attract both domestic and global biotech clients. India is extending HPAPI synthesis capacity and is increasingly present in Phase I and Phase II campaigns that require cost-effective tox and early clinical materials. Japan and South Korea continue to emphasize high-value services, including site-specific conjugation and analytical development with strong quality credentials.

Europe remains a core region for ADC payload synthesis and conjugation under stringent EMA expectations for sterile operations and health-based exposure limits. Switzerland, Germany, and the United Kingdom host anchor sites that supply European sponsors and global programs with Western-audited capabilities. Emerging locations across the rest of Europe offer cost-competitive services and are developing expertise in sterile drug products, stability, and analytics. Sponsors balancing cost and regulatory requirements often combine continental providers for payload synthesis with Swiss and German capacity for conjugation and release. The region’s compliance-driven delivery complements North American approvals and Asia-Pacific cost positions within the ADC drug CDMO service market.

Competitive Landscape

The ADC drug CDMO Service market exhibits moderate concentration in commoditized molecules but fragmentation in specialty niches. The top players are Lonza Group AG, WuXi XDC, Samsung Biologics, Piramal Pharma Solutions, and Sterling Pharma Solutions Limited. These companies dominate due to their scale, integrated capabilities, and specialized expertise in antibody-drug conjugates.

Competition has intensified as CDMOs announced ADC capacity expansions and investments in high-containment suites that support shorter lead times for conjugation slots. Providers with legacy peptide-synthesis strengths are winning cleavable-linker contracts, while platforms built for click-chemistry and non-cleavable constructs are capturing solid-tumor programs. In parallel, CDMOs are scaling analytical depth for control with high-resolution mass spectrometry and hydrophobic interaction methods to strengthen late-stage readiness. Several leaders are building geographic redundancy to enable sponsors to dual-source conjugation and drug product under harmonized quality systems. These moves underpin a steady flow of awards as the ADC drug CDMO service market shifts toward higher complexity programs.

ADC Drug CDMO Service Industry Leaders

Lonza Group AG

WuXi XDC

Samsung Biologic

Piramal Pharma Ltd.

Sterling Pharma Solutions Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Biologics inaugurated a fourth ADC manufacturing facility in Songdo, South Korea, with an annual capacity of 300 kilograms of conjugated drug substance and integrated antibody production suites. The USD 450 million investment positions Samsung as the largest single-site ADC CDMO globally and reflects surging demand from Asian biotech clients.

- October 2025: LOTTE Biologics and SK Pharmteco have signed a strategic partnership to strengthen their global capabilities as CDMOs for antibody-drug conjugates. The collaboration aims to provide integrated, one-stop services covering antibody drug substance, linker–payload production, and bioconjugation, supported by joint marketing efforts.

- August 2025: Cohance Lifesciences announced a USD 10 million investment in NJ Bio to expand antibody-drug conjugate CDMO capabilities, strengthening specialized services in bioconjugation and payload-linker chemistry.

- July 2025: Simtra BioPharma Solutions expanded facilities to bring commercial-scale ADC drug product manufacturing to the United States, positioning the company with specialized fill-finish capabilities for oncology therapies.

Global ADC Drug CDMO Service Market Report Scope

According to the scope of the report, an ADC drug CDMO service refers to specialized contract development and manufacturing services that support the entire lifecycle of antibody-drug conjugates (ADCs). These complex oncology therapeutics combine a monoclonal antibody with a cytotoxic payload. These services cover everything from early-stage development to commercial-scale production.

The segmentation of the ADC drug CDMO service market is based on service stage, linker type, therapeutic area, component services, end user, and geography. By service stage, the market is segmented into manufacturing and development. By linker type, the market is segmented into cleavable linkers and non-cleavable linkers. By therapeutic area, the market is segmented into multiple myeloma, lymphoma, breast cancer, and other therapeutic areas. By component service, the market is segmented into antibody manufacturing, payload synthesis (HPAPI), conjugation & purification, and fill & finish. By end user, the market is segmented into pharmaceutical companies, biotechnology companies, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Manufacturing |

| Development |

| Cleavable Linkers |

| Non-Cleavable Linkers |

| Multiple Myeloma |

| Lymphoma |

| Breast Cancer |

| Other Therapeutic Area |

| Antibody Manufacturing |

| Payload Synthesis (HPAPI) |

| Conjugation & Purification |

| Fill & Finish |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Other End-User |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Stage | Manufacturing | |

| Development | ||

| By Linker Type | Cleavable Linkers | |

| Non-Cleavable Linkers | ||

| By Therapeutic Area | Multiple Myeloma | |

| Lymphoma | ||

| Breast Cancer | ||

| Other Therapeutic Area | ||

| By Component Service | Antibody Manufacturing | |

| Payload Synthesis (HPAPI) | ||

| Conjugation & Purification | ||

| Fill & Finish | ||

| By End-User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Other End-User | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the ADC Drug CDMO Service sector?

The ADC Drug CDMO Service market size is USD 1.99 billion in 2026 and is forecast to reach USD 6.20 billion by 2031 at a 25.52% CAGR.

Which service stage is expanding fastest in the ADC Drug CDMO Service space?

Development services are projected to grow at a 27.10% CAGR through 2031 as biotechs outsource IND-enabling work and early clinical materials.

Which linker category leads current adoption in ADC Drug CDMO Service programs?

Cleavable linkers led with 66.23% share in 2025, supported by strong use in hematologic malignancies, and are forecast to grow at a 23.41% CAGR through 2031.

Which therapeutic areas are shaping demand for ADC Drug CDMO Service providers?

Multiple myeloma held a 45.10% share in 2025, while lymphoma is projected to record a 28.10% CAGR as CD79b and CD19 pipelines advance.

What regions are most important for ADC Drug CDMO Service capacity?

North America held 41.25% in 2025 due to approvals and funding support, while Asia-Pacific is projected to grow at a 28.63% CAGR with new multi-product ADC suites.

What are the main bottlenecks for ADC Drug CDMO Service delivery today?

Constraints include payload precursor supply, limited ADC-specific fill-finish lines, and a shortage of trained bioconjugation chemists, which raises costs and extends timelines.

Page last updated on: