Activewear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

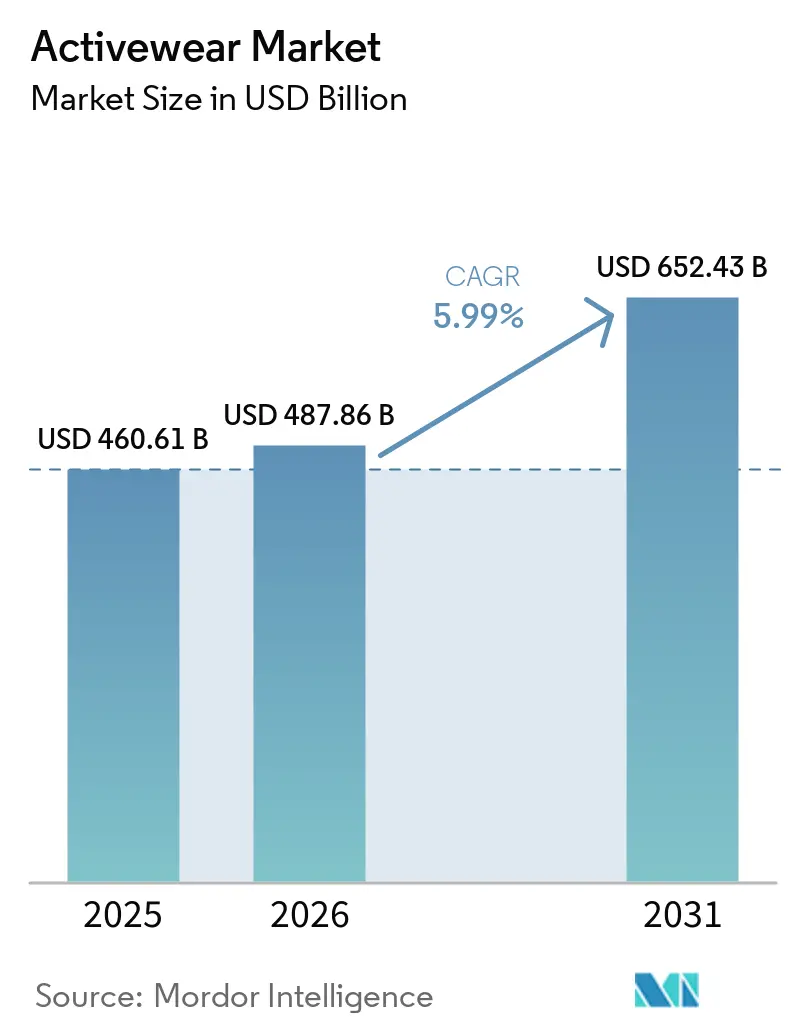

| Market Size (2026) | USD 487.86 Billion |

| Market Size (2031) | USD 652.43 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Activewear Market Analysis by Mordor Intelligence

The activewear market size is expected to grow from USD 460.61 billion in 2025 to USD 487.86 billion in 2026 and is forecast to reach USD 652.43 billion by 2031 at a 5.99% CAGR over 2026-2031. The global activewear market is driven by changing lifestyle habits, increasing health awareness, and the integration of fitness into daily routines. Consumers are prioritizing versatile apparel that combines comfort, performance, and style for activities such as gym workouts, outdoor sports, and casual wear, contributing to the growth of athleisure trends. The rise of digital fitness platforms, social media influence, and celebrity endorsements has further enhanced consumer engagement with activewear brands and fitness-focused lifestyles. Technological advancements in fabrics, including moisture-wicking, breathable, stretchable, and sustainable materials, are fostering product innovation and premiumization within the industry. Additionally, the growing participation of women in sports and fitness activities, rising demand for inclusive and gender-neutral designs, and the rapid growth of e-commerce channels are enabling brands to access broader consumer segments worldwide.

Key Report Takeaways

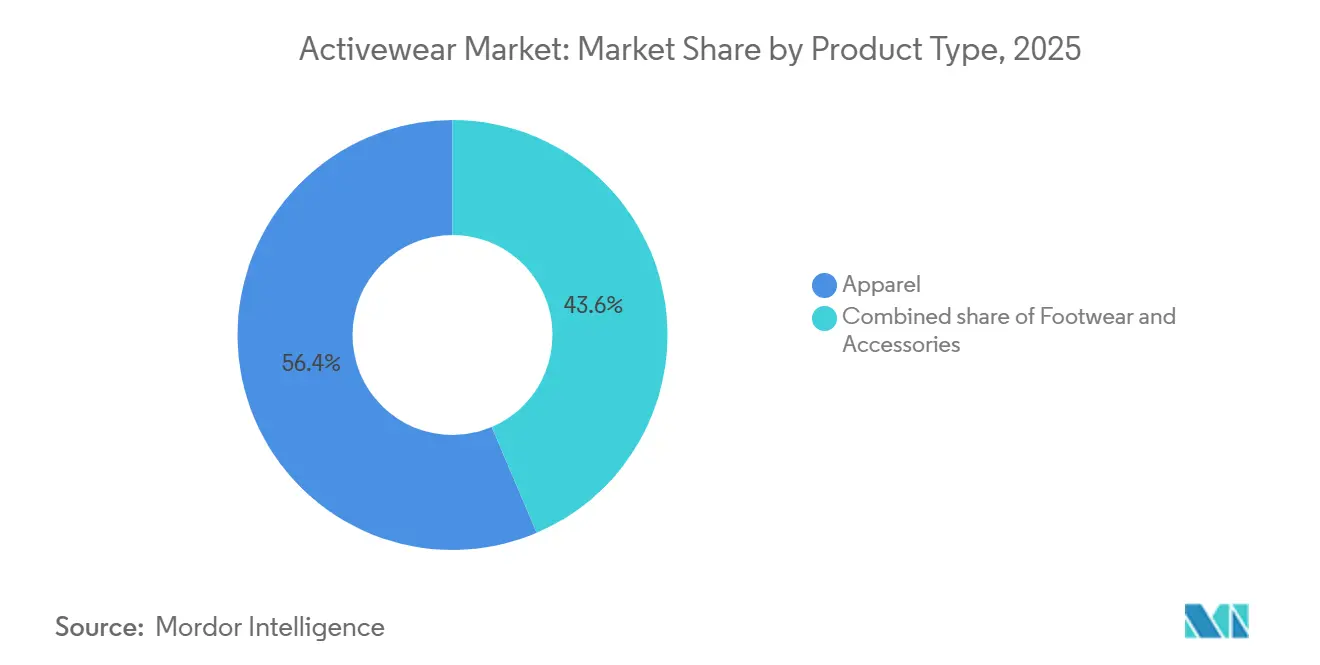

- By product type, apparel held 56.41% of 2025 revenue, while footwear is projected to grow at 6.92% CAGR during 2026-2031.

- By activity, gym and fitness accounted for 36.42% of 2025 revenue, while yoga and Pilates is forecast to expand at 6.81% CAGR during 2026-2031.

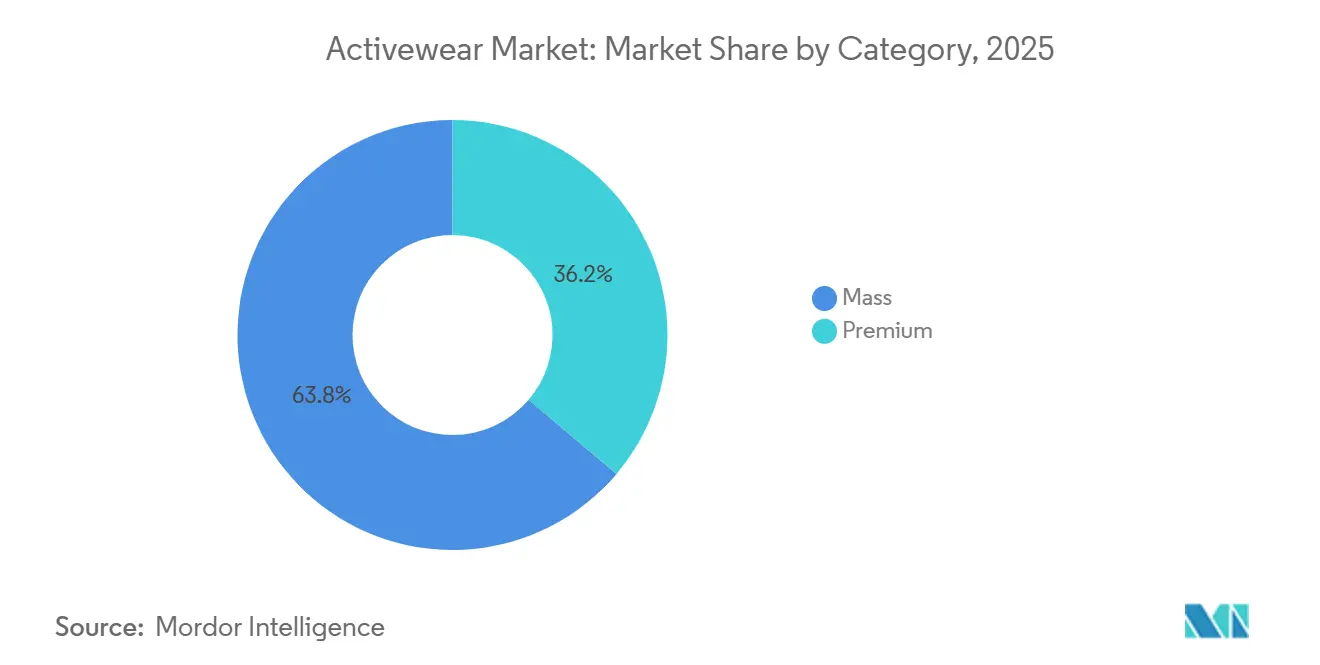

- By category, mass held 63.81% of 2025 revenue, while premium is projected to grow at 7.53% CAGR during 2026-2031.

- By end user, men represented 48.85% of 2025 revenue, while women is forecast to expand at 7.13% CAGR during 2026-2031.

- By distribution channel, sporting goods retailers and specialty stores held 44.63% of 2025 revenue, while online retail is projected to grow at 8.46% CAGR during 2026-2031.

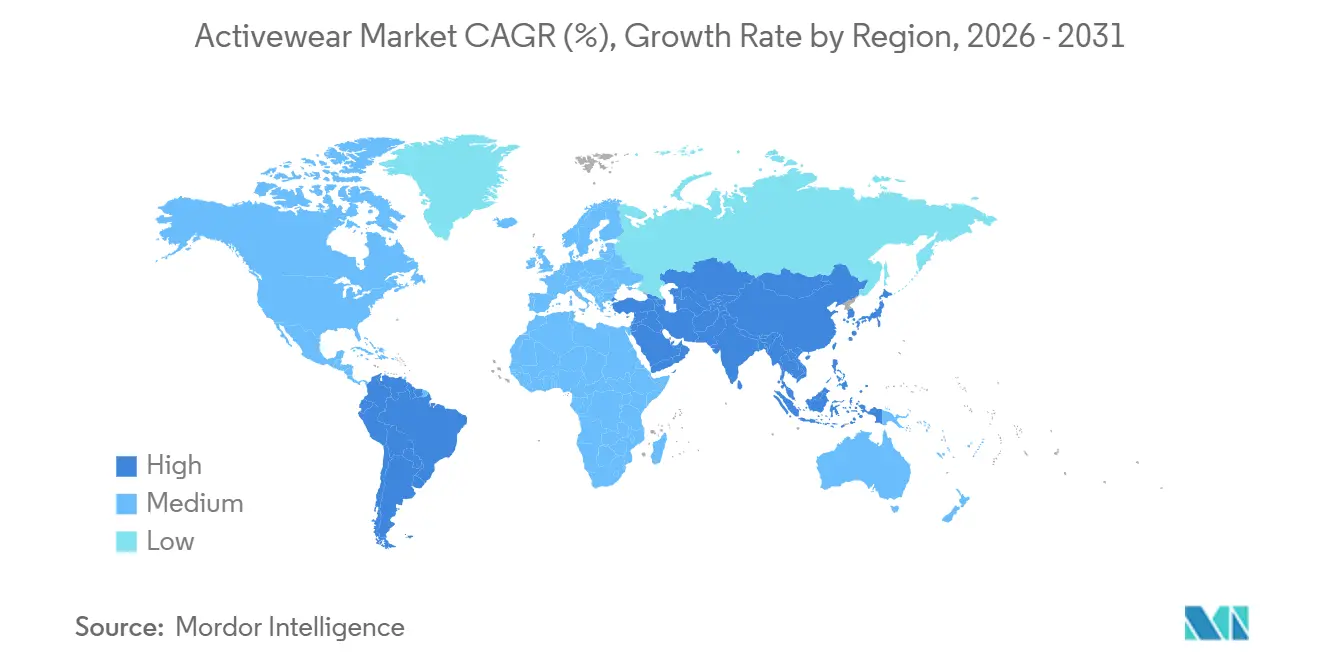

- By geography, North America held 37.64% of 2025 revenue, while Asia-Pacific is forecast to expand at 7.65% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Activewear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing health and wellness awareness | +1.1% | Global | Long term (≥ 4 years) |

| Expansion of athleisure fashion trends | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing participation in fitness and recreational activities | +1.0% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Advancements in performance fabric technologies | +0.8% | Global, with R&D concentrated in the United States, Japan, and Germany | Medium term (2-4 years) |

| Rising influence of social media and fitness influencers | +0.6% | Global, with highest impact in Asia-Pacific and North America | Short term (≤ 2 years) |

| Increasing female participation in sports and fitness | +0.8% | Global, with early-stage gains in South Asia and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing health and wellness awareness

Increasing health and wellness awareness is a key factor driving the global activewear market, as consumers across various age groups are placing greater emphasis on physical fitness, preventive healthcare, and active lifestyles. The rising participation in activities such as gym workouts, yoga, running, cycling, and recreational sports has led to higher demand for comfortable, functional, and performance-oriented apparel suitable for both exercise and casual wear. This trend is further bolstered by the growing popularity of athleisure, where consumers seek versatile clothing that blends style with functionality. The adoption of fitness routines is evident in the expanding membership base of fitness centers worldwide. According to the Health & Fitness Association, the United States fitness industry achieved record levels in 2024, with gyms, studios, and other fitness facilities attracting 77 million members. Membership further increased to 81 million Americans in 2025, representing a 5.2% growth from the previous year[1]Source: Health & Fitness Association, "81 Million Americans Were Members of a Fitness Facility in 2025, New HFA Report Finds," healthandfitness.org. This heightened engagement in fitness and wellness activities is driving consumers to invest more frequently in activewear products that provide enhanced comfort, flexibility, breathability, and moisture-management features, thereby contributing to the global market's growth.

Expansion of athleisure fashion trends

The growth of athleisure fashion trends is a key factor driving the global activewear market, as consumers increasingly seek clothing that combines athletic functionality with casual style. Activewear has transitioned from being limited to gyms, sports, or fitness routines to becoming a mainstream fashion category, widely used for work-from-home settings, travel, social outings, and everyday wear. This shift in consumer preferences toward comfortable, versatile, and stylish apparel has prompted brands to create products that integrate performance features such as stretchability, breathability, and moisture control with contemporary fashion designs. The rising influence of social media, celebrity endorsements, and fitness influencers has further fueled the popularity of athleisure by promoting sporty and wellness-focused lifestyles as fashionable choices. Additionally, evolving workplace dress codes and the growing demand for multifunctional clothing have increased the acceptance of activewear in non-athletic settings. Consequently, consumers are purchasing activewear more frequently for both functional and lifestyle needs, driving ongoing product innovation, brand partnerships, and market growth across global regions.

Increasing participation in fitness and recreational activities

Increasing participation in fitness and recreational activities is a key driver of the global activewear market. More consumers are engaging in sports, exercise routines, outdoor activities, and wellness-focused lifestyles. Growing awareness of physical health, stress management, and overall well-being has encouraged individuals across various age groups to take part in activities such as running, cycling, gym workouts, yoga, hiking, and team sports. This has led to a higher demand for functional and performance-enhancing apparel. Activewear products that provide comfort, flexibility, breathability, and moisture-wicking capabilities are increasingly preferred to support these activities and enhance performance. The scale of sports and recreational participation is highlighted in the Sports & Fitness Industry Association’s (SFIA) 2026 Topline Participation Report, which noted that nearly 250 million Americans participated in at least one sport, fitness, or leisure activity in 2025[2]Source: Sports & Fitness Industry Association, "Participation Hits New High, but Majority of Americans Not Yet Meeting Recommended Guidelines of Weekly Activity, SFIA’s 2026 Topline Report Finds," sfia.org. This growing consumer engagement in active lifestyles is driving frequent purchases of sportswear, footwear, and accessories, while also encouraging brands to develop innovative and activity-specific product lines, thereby fueling the growth of the global activewear market.

Advancements in performance fabric technologies

Advancements in performance fabric technologies are driving the growth of the global activewear market by improving the functionality, comfort, and durability of sports apparel. Consumers are increasingly seeking activewear that supports high-performance activities while ensuring superior comfort for workouts, sports, and daily wear. In response, manufacturers are investing in innovative textile technologies such as moisture-wicking fabrics, temperature-regulating materials, compression technology, anti-odor treatments, lightweight stretch fibers, and quick-drying textiles. These innovations enhance athletic performance by regulating body temperature, reducing sweat-related discomfort, and improving flexibility and movement during physical activities. Furthermore, the adoption of sustainable fabric solutions, including recycled polyester, biodegradable fibers, and eco-friendly dyeing processes, is appealing to environmentally conscious consumers and boosting brand competitiveness. The integration of smart textiles, such as wearable sensors and adaptive fabrics, is also creating opportunities in premium activewear segments. As consumers increasingly prioritize functionality and comfort in fitness and lifestyle apparel, ongoing advancements in fabric technologies are driving product premiumization, encouraging higher replacement rates, and expanding activewear adoption globally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality imitation products | -0.7% | Global, concentrated in Asia-Pacific and Middle East and Africa | Medium term (2-4 years) |

| Volatility in raw material availability and fabric sourcing | -0.6% | Global, concentrated in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Sizing inconsistencies and product return challenges | -0.4% | North America and Europe, with high e-commerce penetration | Medium term (2-4 years) |

| High dependency on seasonal and trend-based demand | -0.5% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and low-quality imitation products

Counterfeit and low-quality imitation products pose a significant challenge to the global activewear market by undermining brand reputation, eroding consumer trust, and reducing overall market revenue. The growing demand for premium activewear brands has led to a notable rise in counterfeit activewear apparel, particularly distributed through online marketplaces and unauthorized retail channels. These imitation products often fail to meet the required standards for quality, durability, and performance, leading to negative consumer experiences and diminished confidence in authentic brands. Furthermore, counterfeit products intensify price competition, making it challenging for established companies to sustain profit margins while continuing to invest in product innovation and marketing efforts. According to U.S. Customs and Border Protection, wearing apparel ranks among the most frequently seized counterfeit products in 2024, with nearly 1 million units confiscated[3]Source: U.S. Customs and Border Protection, "The Truth Behind Counterfeits," cbp.gov. The prevalence of counterfeit activewear not only results in financial losses for manufacturers but also diminishes brand exclusivity and hinders the growth of premium and technologically advanced activewear segments in the global market.

Volatility in raw material availability and fabric sourcing

Volatility in raw material availability and fabric sourcing poses a significant challenge for the global activewear market. Manufacturers depend heavily on specialized textiles such as polyester, nylon, spandex, cotton blends, and performance-enhancing synthetic fibers to produce high-quality activewear. Fluctuations in the supply and pricing of these materials, driven by factors like geopolitical tensions, supply chain disruptions, transportation issues, environmental regulations, and evolving trade policies, can increase production costs and create operational uncertainties for apparel companies. Additionally, the rising demand for sustainable and recycled fabrics has heightened competition for eco-friendly raw materials, often resulting in limited availability and higher procurement costs. Delays in fabric sourcing and shortages of performance textiles can disrupt manufacturing schedules, reduce inventory levels, and hinder brands' ability to adapt quickly to changing fashion and fitness trends. Smaller manufacturers are particularly affected due to their limited supplier networks and lower purchasing power. Consequently, ongoing instability in raw material sourcing and fabric supply chains can adversely impact profit margins, pricing strategies, and product innovation in the global activewear market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Footwear Gaining Ground Against Apparel's Dominance

Apparel remains the largest product segment, accounting for 56.41% of the 2025 market. This dominance is driven by the growing adoption of athleisure fashion, increasing health consciousness, and rising participation in fitness and recreational activities. Consumers are prioritizing apparel that combines comfort, functionality, and style, enabling activewear to be worn not only during workouts but also in casual, travel, and work-from-home settings. Innovations in fabric technologies, such as moisture-wicking, stretchable, breathable, and temperature-regulating materials, are enhancing the appeal of activewear by improving both comfort and performance. Additionally, the influence of social media, fitness influencers, and celebrity collaborations has fueled demand for fashionable sportswear collections across diverse consumer groups. Factors such as the increasing participation of women in fitness activities, a growing preference for sustainable apparel, and rising demand for inclusive sizing and gender-neutral designs are further driving segment growth. The rapid expansion of e-commerce platforms and direct-to-consumer strategies has also improved product accessibility, encouraging frequent purchases of activewear apparel globally.

Footwear is the fastest-growing product segment, with a forecasted CAGR of 6.92% during 2026-2031. This growth is attributed to the increasing popularity of sports, fitness routines, outdoor recreational activities, and lifestyle-oriented athletic fashion trends. Rising consumer awareness about physical fitness and the importance of proper footwear for performance, comfort, and injury prevention has driven demand for specialized athletic shoes designed for activities such as running, training, hiking, and cycling. Technological advancements in footwear design, including lightweight materials, enhanced cushioning systems, shock absorption, ergonomic soles, and smart performance features, are attracting both professional athletes and everyday consumers. The influence of sneaker culture, celebrity endorsements, and limited-edition product launches has elevated athletic footwear into a significant fashion category beyond sports applications. Furthermore, factors such as rising urbanization, growing participation in marathons and fitness events, and increasing consumer preference for versatile footwear suitable for both athletic and casual wear are supporting continuous segment growth. The strong presence of global sportswear brands and the rapid expansion of online retail channels are further accelerating footwear sales in the activewear market worldwide.

By Activity: Gym and Fitness Anchors Volume While Mind-Body Formats Accelerate

The gym and fitness segment accounted for 36.42% of the 2025 market, driven by a growing global emphasis on physical health, weight management, strength training, and overall wellness. Factors such as rising gym memberships, the expansion of fitness center networks, and increased participation in activities like cardio workouts, high-intensity interval training (HIIT), functional fitness, and bodybuilding are encouraging consumers to invest in performance-oriented apparel. These garments are designed for comfort and durability, with consumers favoring activewear made from moisture-wicking, breathable, stretchable, and lightweight fabrics that enhance flexibility and support intense workout sessions. Additionally, the influence of fitness influencers, digital workout platforms, and social media fitness communities has heightened interest in stylish and branded gym apparel. The growing popularity of athleisure trends has further extended the use of gym activewear beyond fitness settings, making it suitable for casual and everyday wear. Technological advancements in compression fabrics, odor-control materials, and seamless garment construction are enhancing product appeal, while the expansion of e-commerce and direct-to-consumer channels is increasing the accessibility of gym-focused activewear globally.

The yoga and Pilates segment is projected to grow at a CAGR of 6.81% over 2026-2031, driven by increasing consumer focus on holistic wellness, mental health, flexibility, and low-impact fitness activities. Greater awareness of stress management, mindfulness, posture improvement, and body balance has significantly boosted participation in yoga and Pilates across various age groups worldwide. This has led to rising demand for specialized activewear that provides superior stretchability, softness, comfort, and freedom of movement during exercise sessions. Consumers prefer apparel made from lightweight, breathable, and non-restrictive fabrics that ensure comfort during prolonged wear and support flexibility-focused movements. The growing popularity of home-based wellness routines, virtual fitness classes, and boutique yoga studios has further accelerated demand for yoga and Pilates apparel. Additionally, the influence of wellness influencers, social media trends, and celebrity-endorsed yoga lifestyles has positioned yoga activewear as both functional and fashion-oriented. Increasing consumer interest in sustainable and eco-friendly fabrics, such as organic cotton and recycled materials, is driving innovation in this segment. Furthermore, the adoption of athleisure fashion continues to expand the use of yoga and Pilates apparel in everyday casual wear.

By Category: Mass Segment Sustains Volume as Premium Reshapes Margins

The mass segment accounted for 63.81% of the 2025 market, driven by the increasing adoption of fitness-oriented lifestyles among mainstream consumers and the rising demand for affordable, comfortable, and versatile sportswear. Consumers across various income groups are seeking budget-friendly activewear suitable for gym workouts, walking, yoga, running, and casual everyday use. This trend has prompted retailers and brands to expand their mass-market product offerings. The growing popularity of athleisure trends has further fueled demand for low- to mid-priced activewear that combines functionality with fashionable designs. Additionally, the expansion of organized retail channels, including supermarkets, hypermarkets, discount stores, and e-commerce platforms, has enhanced product accessibility and availability in urban and semi-urban markets. Fast-fashion companies and private-label brands are increasingly launching cost-effective activewear collections, enabling consumers to purchase trendy sportswear at competitive prices. Factors such as growing health awareness, increased participation in recreational fitness activities, and frequent product replacement cycles due to changing fashion preferences are further driving the global growth of the mass activewear segment.

The premium segment is projected to outpace the mass tier with a 7.53% CAGR over 2026-2031, driven by growing consumer preference for high-performance apparel, brand value, and technologically advanced sportswear products. Consumers are increasingly willing to invest in premium activewear that offers superior comfort, durability, ergonomic fit, and advanced fabric technologies, including moisture management, compression support, temperature regulation, and sustainable materials. The influence of fitness culture, luxury athleisure trends, celebrity endorsements, and designer collaborations has elevated premium activewear into a lifestyle and status-oriented category beyond traditional sports applications. Furthermore, rising participation in specialized fitness activities such as marathon running, high-intensity training, Pilates, and outdoor sports is boosting demand for premium apparel and footwear designed for enhanced performance and injury prevention. Premium brands' strong focus on innovation, exclusivity, sustainability, and personalized shopping experiences is attracting health-conscious and fashion-oriented consumers. The expansion of digital retail channels, limited-edition product launches, and direct-to-consumer strategies are also strengthening brand engagement and accelerating the global growth of the premium activewear segment.

By End User: Women's Growing Engagement Reshapes Product Priorities

Men accounted for the largest end-user share in 2025 at 48.85%, driven by increasing participation in fitness activities, sports, outdoor recreation, and health-focused lifestyles. Growing awareness of physical fitness, muscle training, endurance building, and overall wellness has significantly boosted demand for performance-oriented apparel and footwear tailored for male consumers. Activities such as gym workouts, running, cycling, and high-intensity training are driving frequent purchases of activewear products that prioritize comfort, flexibility, sweat management, and durability. The influence of fitness influencers, professional athletes, and sports sponsorships has further strengthened consumer interest in branded sportswear and athletic fashion. Additionally, the expansion of athleisure trends has led to increased adoption of men’s activewear in casual and work-from-home settings, creating demand for versatile and stylish clothing suitable for both exercise and daily wear. Technological advancements in performance fabrics, ergonomic designs, and lightweight materials, coupled with the rapid growth of online retail channels, are further contributing to the global expansion of the men’s activewear segment.

Women represent the fastest-growing end-user segment, with a CAGR of 7.13% over 2026-2031. This growth is driven by increasing participation in fitness, sports, yoga, Pilates, and wellness-focused activities, alongside the rising influence of athleisure fashion trends. Women are prioritizing health, self-care, and active lifestyles, resulting in higher demand for functional and stylish activewear that supports both performance and everyday comfort. The growing popularity of gym memberships, boutique fitness studios, home workout programs, and wellness communities has accelerated purchases of leggings, sports bras, tank tops, training shoes, and other women’s activewear products. Fashion-forward designs, inclusive sizing, body-positive marketing, and celebrity collaborations have further enhanced consumer engagement in this segment. Additionally, advancements in fabric technologies, including moisture-wicking, stretchable, breathable, and seamless materials, are improving product comfort and functionality, encouraging repeat purchases. The strong presence of social media influencers and digital fitness content has increased awareness of fitness apparel trends, while the growing availability of women-focused collections through e-commerce platforms continues to drive the rapid expansion of the global women’s activewear market.

By Distribution Channel: Specialty Retail Leads as Digital Commerce Accelerates

Sporting goods retailers and specialty stores accounted for the largest distribution share in 2025, at 44.63%. This dominance is attributed to consumers' preference for expert product guidance, personalized shopping experiences, and access to high-performance athletic apparel and footwear. These retail channels provide a broad selection of sports-specific products tailored for activities such as running, training, yoga, hiking, and team sports, enabling consumers to evaluate features, fit, and functionality before purchasing. The availability of trained staff, in-store product trials, gait analysis services, and specialized recommendations enhances consumer confidence, particularly for premium and performance-focused activewear. Additionally, these stores often feature exclusive product launches, limited-edition collections, and collaborations with leading sportswear brands, attracting fitness enthusiasts and loyal brand customers. The increasing popularity of fitness culture, outdoor recreation, and organized sports participation is further driving foot traffic to these outlets. Experiential retail strategies, such as interactive fitness zones and brand engagement events, are also strengthening customer relationships and supporting the growth of activewear sales through sporting goods retailers and specialty stores worldwide.

Online retail is the fastest-growing distribution channel, with a CAGR of 8.46% projected for 2026-2031. This growth is driven by the rising adoption of e-commerce platforms, the convenience of digital shopping, and expanded consumer access to a diverse range of brands and products. Consumers increasingly favor online channels due to the ability to compare prices, explore extensive product options, read customer reviews, and shop from any location at any time. The proliferation of smartphones, digital payment systems, and social commerce platforms has further accelerated online purchasing, particularly among younger, tech-savvy consumers. Activewear brands are enhancing their direct-to-consumer strategies through branded websites and mobile applications, offering personalized shopping experiences, targeted promotions, and loyalty programs. Social media marketing, influencer collaborations, and digital advertising campaigns are also significantly boosting online sales by increasing product visibility and consumer engagement. Additional factors such as fast delivery services, easy return policies, virtual fitting technologies, and frequent online discounts are encouraging consumers to purchase activewear through e-commerce platforms, driving the rapid growth of online retail sales globally.

Geography Analysis

North America remains the largest activewear market globally, accounting for 37.64% of the 2025 market share. This dominance is attributed to the region's strong fitness culture, high participation in sports and recreational activities, and widespread adoption of athleisure fashion trends. Consumers in the United States and Canada are increasingly prioritizing health, wellness, and active lifestyles, driving demand for performance-oriented apparel and footwear suitable for gym workouts, running, yoga, outdoor activities, and everyday wear. The region benefits from the presence of leading global sportswear brands, continuous product innovation, and the rapid adoption of advanced fabric technologies that enhance comfort and functionality. Additionally, celebrity endorsements, fitness influencers, and social media-driven fashion trends significantly influence consumer purchasing behavior. The growing popularity of home fitness programs, premium activewear collections, and sustainable sportswear products further supports market growth. A well-developed e-commerce infrastructure, organized retail networks, and strong consumer spending on lifestyle and fitness products continue to accelerate activewear sales in North America.

Asia-Pacific is the fastest-growing activewear market, with a projected CAGR of 7.65% from 2026 to 2031. This growth is driven by rapid urbanization, increasing health awareness, and rising participation in fitness and sports activities across countries such as China, India, Japan, South Korea, and Australia. Greater exposure to global fitness trends, expanding middle-class populations, and growing interest in gym memberships, yoga, running, and outdoor recreation are encouraging more frequent purchases of activewear products. The rising influence of social media platforms, fitness influencers, and international sports events is strengthening consumer awareness of athletic fashion and wellness-focused lifestyles. Additionally, the growing popularity of athleisure apparel among younger consumers is driving the use of activewear for both fitness and casual wear. The region's rapidly expanding e-commerce sector, increasing smartphone penetration, and availability of both affordable and premium activewear brands are further contributing to market growth. Local manufacturing capabilities and significant investments by international sportswear companies in Asia-Pacific markets are enhancing product availability and competitive pricing.

The activewear markets in Europe, South America, and the Middle East and Africa are growing due to increasing consumer interest in health, fitness, and sports participation, along with the rising influence of athleisure fashion. In Europe, heightened awareness of wellness, sustainability, and outdoor recreational activities such as cycling, hiking, and running is driving demand for technologically advanced and eco-friendly activewear products. In South America, expanding participation in gym workouts, dance fitness, and outdoor sports, particularly among younger consumers, is supporting market growth. In the Middle East and Africa, increasing urbanization, rising fitness club memberships, and growing adoption of Western fashion and wellness trends are fueling demand for modern sportswear and athleisure apparel. Across these regions, social media influence, celebrity endorsements, and the expansion of international sportswear brands are enhancing consumer engagement with activewear products. Furthermore, improving retail infrastructure, rising penetration of online shopping platforms, and the increasing availability of both affordable and premium activewear collections are contributing to the continued growth of the market in these regions.

Competitive Landscape

The global activewear market is characterized by a moderate concentration level. Leading multinational sportswear companies dominate significant portions of the market but face increasing competition from emerging challenger brands and evolving consumer preferences. Major players are restructuring operations to enhance profitability, optimize supply chains, strengthen direct-to-consumer distribution channels, and focus on core performance categories such as running, training, and team sports. Additionally, companies are adjusting pricing and channel strategies to address inflationary pressures, tariff challenges, and changing retail dynamics. Direct-to-consumer platforms, proprietary digital ecosystems, and exclusive product launches are becoming essential tools for improving customer engagement, pricing control, and brand positioning in a rapidly changing market environment.

Competition in the activewear market is intensifying through strategic investments, acquisitions, and technological advancements. Many sportswear companies are expanding internationally by establishing flagship retail stores, enhancing digital commerce initiatives, and leveraging AI-driven consumer engagement models to increase market penetration in high-growth regions. Product differentiation is increasingly focused on proprietary fabric technologies, functional apparel innovations, and sport-specific performance features that enhance comfort, sweat management, flexibility, and recovery support.

Emerging brands with a focus on premium lifestyle positioning, fitness communities, and digital-native engagement models are rapidly gaining market share in specific consumer and activity segments. These challenger brands are capitalizing on the growing demand for athleisure, wellness-oriented lifestyles, and fashion-forward activewear, particularly among younger consumers seeking authenticity and exclusivity. Companies are also investing in community-driven ecosystems, ambassador programs, fitness applications, and experiential events to build consumer loyalty and create long-term switching barriers beyond product differentiation.

Activewear Industry Leaders

-

Nike Inc.

-

Under Armour Inc.

-

Lululemon Athletica Inc.

-

Adidas AG

-

Puma SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Lululemon launched its e-commerce platform in Mexico (lululemon.mx) and announced plans to open over 30 stores in the country by the end of FY2026. Of the 15 new stores planned for North America, 8 will be located in Mexico. This geographic expansion aims to establish the brand in the world's second-largest Spanish-speaking market, aligning with expected growth in the mid-income consumer segment.

- April 2026: On Holding AG, in collaboration with actress and cultural figure Zendaya, introduced their first co-created apparel and footwear collection. The launch was accompanied by a film directed by Academy Award-winning director Spike Jonze.

- April 2026: Anta Sports introduced the PG7 3.0 globally, marking the first activewear footwear to incorporate Haina Yarn 3.0 with Sorona hollow-yarn technology. This innovation achieves a 25% hollow ratio, enhancing breathability. The earlier PG7 2.0 model sold over 4 million pairs in 2025, demonstrating strong commercial demand for technically advanced, affordably priced running footwear.

Global Activewear Market Report Scope

| Apparel |

| Footwear |

| Accessories |

| Running and Cycling |

| Gym and Fitness |

| Yoga and Pilates |

| Dance Fitness |

| Others |

| Mass |

| Premium |

| Men |

| Women |

| Kids |

| Supermarkets and Hypermarkets |

| Sporting Goods Retailer and Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Apparel | |

| Footwear | ||

| Accessories | ||

| By Activity | Running and Cycling | |

| Gym and Fitness | ||

| Yoga and Pilates | ||

| Dance Fitness | ||

| Others | ||

| By Category | Mass | |

| Premium | ||

| By End User | Men | |

| Women | ||

| Kids | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Sporting Goods Retailer and Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the activewear market by 2031?

The activewear market is forecast to reach USD 652.43 billion by 2031, rising from USD 487.86 billion in 2026 at a 5.99% CAGR over 2026-2031.

Which product segment leads global revenue?

Apparel remains the largest product segment, holding 56.41% of 2025 revenue because it spans gym use, running, yoga, and everyday wear.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 7.65% during 2026-2031, supported by urbanization, rising fitness participation, and expanding brand investment.

Why is online retail becoming more important for brands?

Online retail is the fastest-growing channel at 8.46% CAGR, and brands use it to improve margins, gather first-party data, and connect digital expansion with store growth.

Page last updated on: