Actinium-225 Therapeutic Radioisotope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 298.55 Million |

| Market Size (2031) | USD 582.35 Million |

| Growth Rate (2026 - 2031) | 14.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Actinium-225 Therapeutic Radioisotope Market Analysis by Mordor Intelligence

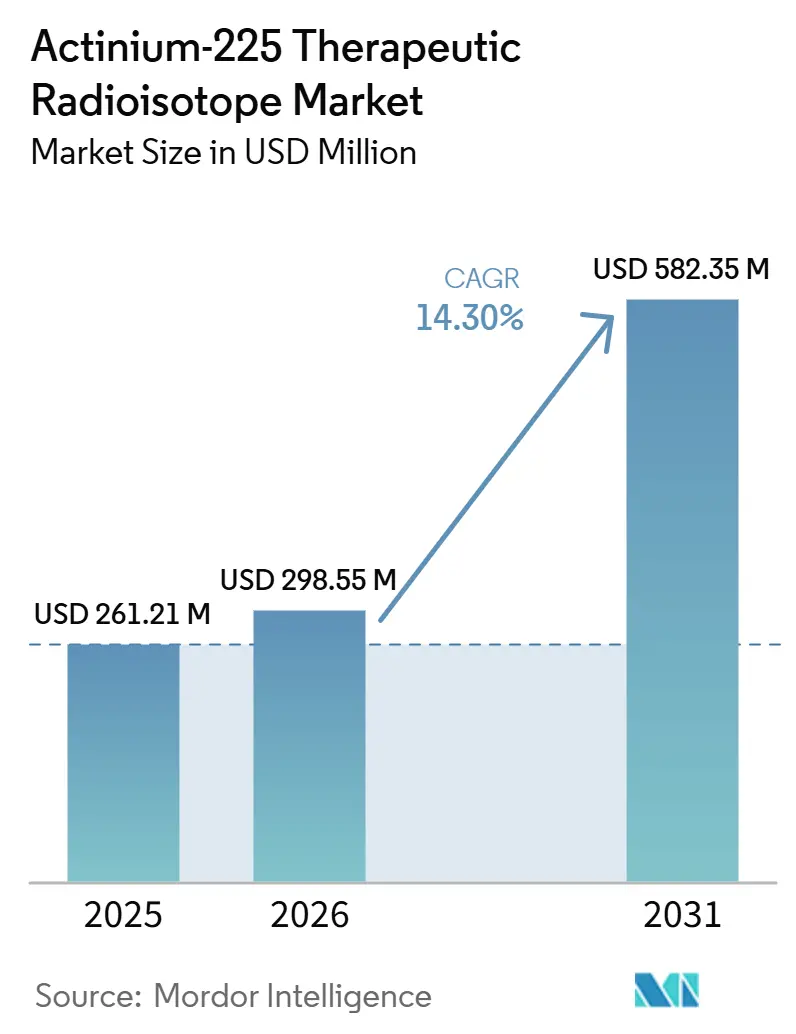

The Actinium-225 Therapeutic Radioisotope Market size was valued at USD 261.21 million in 2025 and is estimated to grow from USD 298.55 million in 2026 to reach USD 582.35 million by 2031, at a CAGR of 14.30% during the forecast period (2026-2031).

The market is moving forward as targeted alpha therapy gains stronger clinical backing in oncology, especially in settings where patients have already progressed after lutetium-177 treatment and still need a next treatment option. The actinium-225 therapeutic radioisotope market is also being shaped by a shift in competitive behavior, because supply access now matters as much as drug design, and producers with scalable output or controlled feedstock are becoming central partners in clinical development. Another important factor is the move away from reliance on a narrow production base, as governments and private producers continue to back cyclotron, accelerator, and hybrid routes that can spread supply more widely across treatment networks. Regional expansion is becoming more balanced, with North America holding the lead through its established isotope infrastructure while Asia-Pacific advances quickly through domestic manufacturing efforts and new research-driven supply plans. Near-term conditions still reflect a supply-constrained actinium-225 therapeutic radioisotope market, but announced production investments, commercial scale-up programs, and facility additions create a clearer path for broader availability later in the forecast period.

Key Report Takeaways

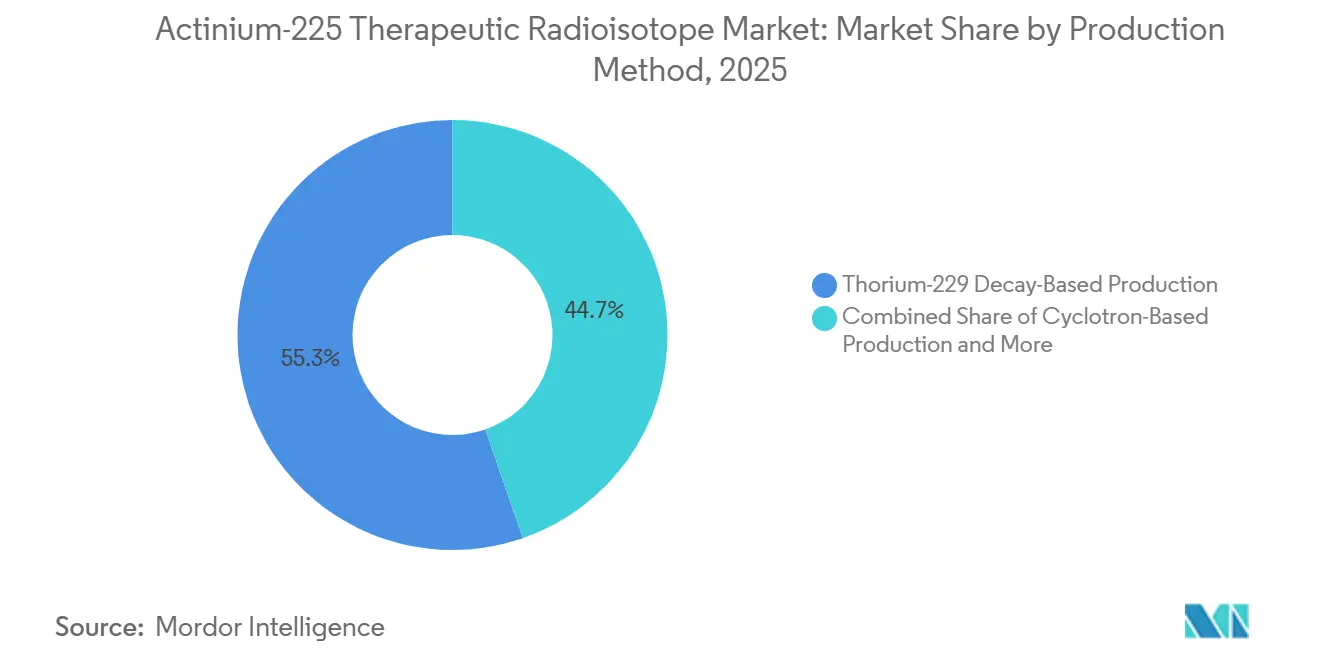

- By production method, thorium-229 decay-based production held 55.31% share in 2025, while cyclotron-based production is forecast to expand at 17.38% CAGR through 2031.

- By application, prostate cancer accounted for 38.24% share in 2025, while research and development is projected to grow at 20.52% CAGR through 2031.

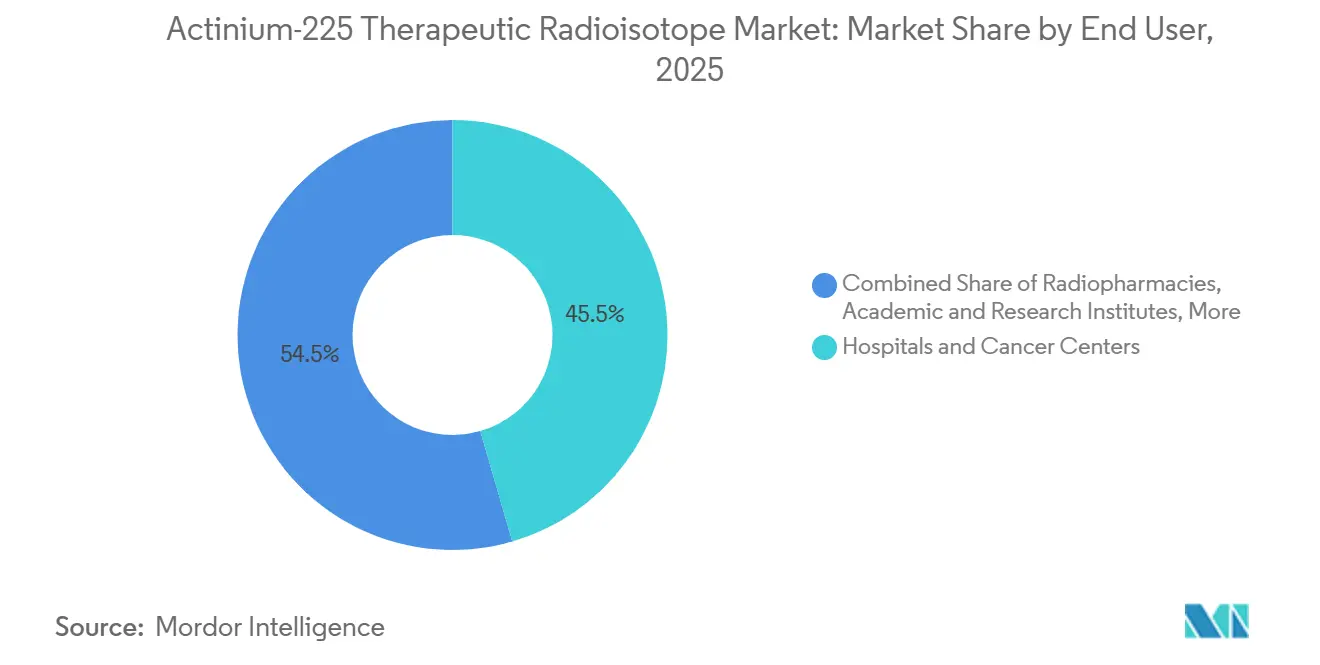

- By end user, hospitals and cancer centers held 45.52% of the actinium-225 therapeutic radioisotope market share in 2025, while radiopharmacies are expected to record the highest CAGR at 18.25% through 2031.

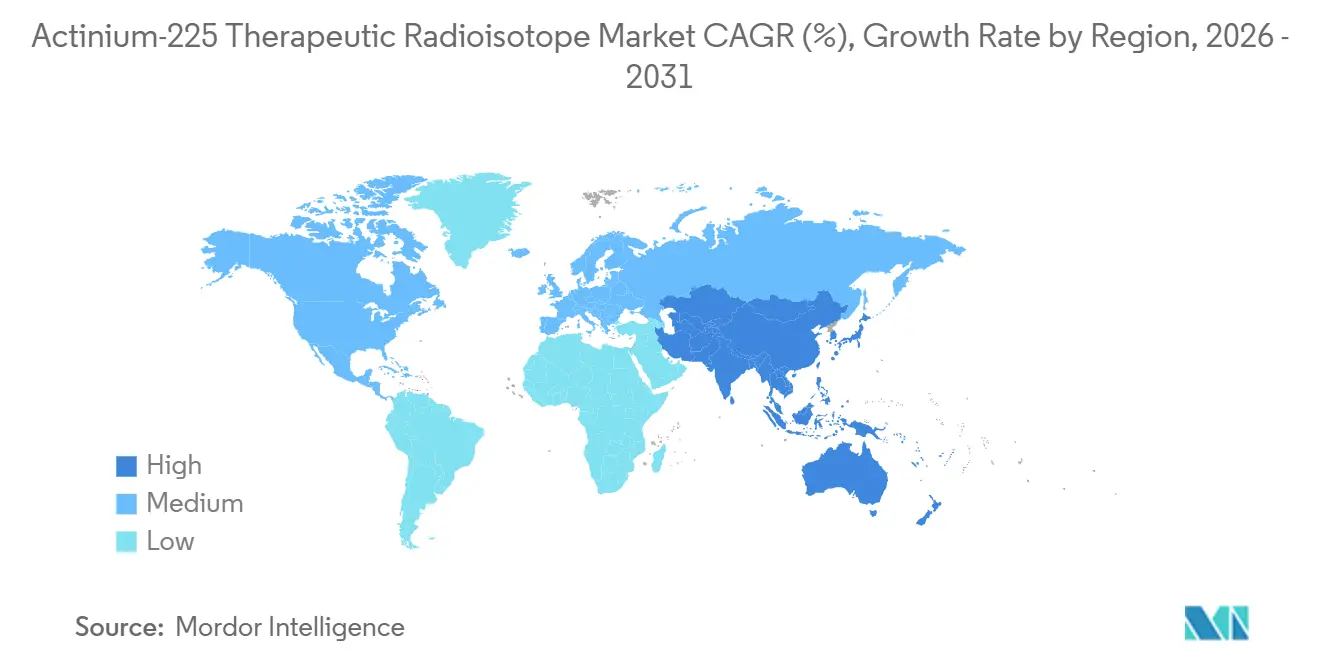

- By geography, North America represented 36.22% share in 2025, while Asia-Pacific is expected to expand at 20.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Actinium-225 Therapeutic Radioisotope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Clinical Adoption in Targeted Alpha Therapy Oncology | +4.2% | Global | Short term (≤ 2 years) |

| Expansion of Late-Stage Radiopharmaceutical Pipelines | +3.1% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Long-Term Supply Agreements Reducing Procurement Uncertainty | +2.4% | Global, with early gains in North America & EU | Medium term (2-4 years) |

| Government Funding for Isotope Production Infrastructure | +1.8% | North America, APAC core, spill-over to EU | Medium term (2-4 years) |

| Decentralized Radiopharmacy and Hospital Access Models | +1.2% | North America & EU, early-stage in APAC | Long term (≥ 4 years) |

| Isotope Recycling, Yield Improvement, and Feedstock Recovery | +0.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Clinical Adoption in Targeted Alpha Therapy Oncology

The actinium-225 therapeutic radioisotope market is benefiting from stronger clinical confidence in targeted alpha therapy, especially in prostate cancer programs that now report meaningful response activity with better-managed toxicity profiles. Phase 1 findings from Bayer’s PAnTHa study, presented at the 2026 ASCO Genitourinary Cancers Symposium, showed PSA50 responses in 83% of patients at the recommended expansion dose of 125 kBq/kg, and the study also reported no grade 3 or 4 salivary toxicities at that dose level. A 2026 clinical landscape review from Nucleus RadioPharma identified 28 active Phase I and Phase I/II alpha therapy trials worldwide, with actinium-225 programs accounting for a large share of that early development base[1]“The Alpha Era: How 2026 Could Be the Breakthrough Year for Targeted Alpha Therapies,” Nucleus RadioPharma, nucleusrad.com. The clinical role of actinium-225 is also broadening because published reviews show activity in patients who are refractory to lutetium-177 PSMA therapy, which means the actinium-225 therapeutic radioisotope market can grow alongside lutetium-177 rather than only against it. Regulatory support is also reinforcing demand expansion, as the FDA granted Fast Track designation to Aktis Oncology’s AKY-1189 in January 2026 for urothelial cancer, extending visible pipeline interest beyond prostate cancer and supporting broader clinical use cases for the actinium-225 therapeutic radioisotope market.

Expansion of Late-Stage Radiopharmaceutical Pipelines

The actinium-225 therapeutic radioisotope market is being supported by a visible move from exploratory work into later-stage radiopharmaceutical programs, and that shift raises isotope demand per study as patient cohorts expand. AstraZeneca’s Phase 2 study of FPI-2265 in PSMA-positive metastatic castration-resistant prostate cancer is already positioned as a registration-enabling program for patients who previously received lutetium-177 PSMA therapy, which shows that development activity is no longer limited to early proof-of-concept work[2]“FPI-2265 (225Ac-PSMA-I&T) for Patients With PSMA-Positive Metastatic Castration-Resistant Prostate Cancer,” ClinicalTrials.gov, clinicaltrials.gov. In March 2026, the FDA cleared the IND for Aktis Oncology’s [225Ac]Ac-AKY-2519 to move into Phase 1b trials across prostate, lung, and other solid tumors, which widened the tumor mix under active evaluation. As more programs move toward larger and more complex study designs, isotope procurement becomes part of development planning much earlier than before, and that changes how companies sequence their clinical operations within the actinium-225 therapeutic radioisotope market. The practical result is a faster connection between pipeline maturity and supply planning, which keeps the actinium-225 therapeutic radioisotope market closely tied to execution speed in radiopharmaceutical development.

Long-Term Supply Agreements Reducing Procurement Uncertainty

The actinium-225 therapeutic radioisotope market increasingly rewards companies that secure material access early, because supply planning now shapes whether clinical programs can proceed on schedule and at the intended scale. In this setting, long-duration supply arrangements do more than reduce procurement uncertainty, because they also help sponsors protect timelines, support dose scheduling, and limit the risk that a later-stage study will compete for scarce output with other programs already in motion. This behavior is reinforced by the IAEA Global Radium-226 Management Initiative, which had 14 participating countries as of January 2026 and added a broader international layer to feedstock movement and recovery efforts[3]“Radium Sources Yield Cancer-Fighting Ac-225 in IAEA Program,” ANS Nuclear Newswire, ans.org. The larger effect is that committed supply becomes a competitive filter within the actinium-225 therapeutic radioisotope market, because developers with earlier access can move from preclinical work into human studies with less disruption. That leaves a smaller pool of flexible supply for later entrants and raises the strategic value of every scalable production relationship in the actinium-225 therapeutic radioisotope market.

Government Funding for Isotope Production Infrastructure

Government backing remains an important support for the actinium-225 therapeutic radioisotope market because isotope scale-up still depends on specialized equipment, licensed facilities, and long construction timelines that private developers do not always fund alone. The US Department of Energy’s FY2025 budget request included USD 45.9 million in total estimated cost funding for isotope research and production activities, and the plan specifically included actinium-225 production scale-up at Brookhaven National Laboratory’s new medical cyclotron. Pennsylvania also supported TerraPower Isotopes with USD 10 million in state incentives for its USD 450 million Bellwether Laboratory in Philadelphia, a facility that broke ground in May 2026 and is designed to raise production capacity 20-fold when completed in 2029. In Canada, the Canadian Medical Isotope Ecosystem awarded CAD 500,000 to the Sylvia Fedoruk Canadian Centre for Nuclear Innovation in 2026 to help scale actinium-225 production with low-energy cyclotrons. Japan is pursuing the same direction through a national push to demonstrate actinium-225 production in the fast reactor Joyo by FY2026, which shows that the actinium-225 therapeutic radioisotope market is now tied to industrial policy as much as biomedical research.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Global Supply Bottlenecks | -2.1% | Global, most acute in APAC, South America, and MEA where no domestic production exists | Short term (≤ 2 years), partially easing as new facilities come online post-2028 |

| High Regulatory Burden Across Nuclear and Drug Authorities | -1.4% | Global, with highest compliance complexity in North America (dual FDA + NRC oversight) and EU (country-level variation) | Medium term (2-4 years) |

| Cold-Chain, Shielding, and Last-Mile Logistics Complexity | -1.0% | Global, most acute in APAC, MEA, and South America, spill-over to any geography relying on centralized production with long transit distances | Medium term (2-4 years) |

| Uneven Reimbursement Readiness for Alpha Therapy Procedures | -0.8% | Europe (fragmented billing codes across member states), APAC, and South America, early-stage gaps in North America for non-approved indications | Medium term (2-4 years), easing toward Long term as payer frameworks mature |

| Source: Mordor Intelligence | |||

Persistent Global Supply Bottlenecks

Supply remains the clearest operational restraint on the actinium-225 therapeutic radioisotope market because the installed production base is still small relative to the number of clinical and pre-commercial programs that are already moving forward. The current supply structure still leans heavily on legacy thorium-229 resources, while alternative production routes are only now moving into more dependable commercial or near-commercial operation. Large capacity additions are underway, but several of the most important projects are still being built or scaled, which means the actinium-225 therapeutic radioisotope market is likely to remain tight until those facilities begin contributing at a meaningful level. This also creates a practical imbalance between developers with secured access and developers that still depend on spot or short-notice material availability, and that imbalance slows broader participation in the actinium-225 therapeutic radioisotope market. Until more distributed output becomes routine, supply tightness will continue to influence study pacing, commercial readiness, and the bargaining position of established producers.

High Regulatory Burden Across Nuclear And Drug Authorities

The actinium-225 therapeutic radioisotope market also faces a demanding regulatory path because production and clinical use require compliance that goes beyond the standards applied to conventional oncology products. Each site must manage radioactive material handling, manufacturing quality systems, product documentation, and transfer readiness in ways that extend timelines and raise fixed costs. PanTera’s simultaneous GMP qualification work and FDA type II Drug Master File submission in Q1 2026 show how much front-end preparation is needed before new capacity can support clinical or commercial demand at scale. The burden is heavier for smaller suppliers, because they must build the same compliance foundation without the balance sheet flexibility available to larger isotope or pharmaceutical groups. This slows the pace at which new entrants can ease bottlenecks in the actinium-225 therapeutic radioisotope market and helps explain why scale and regulatory readiness increasingly move together.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Method: Thorium-229 Generators Hold Ground While Cyclotrons Scale

Thorium-229 decay-based production held 55.31% of the actinium-225 therapeutic radioisotope market size in 2025, reflecting its long-standing role as the most established and most clinically familiar source of actinium-225. This route continues to benefit from a history of use and a high level of confidence around output quality, which explains why it remains the reference point for supply discussions across the actinium-225 therapeutic radioisotope market. At the same time, the method is tied to a finite feedstock base, and that creates a natural ceiling that cannot fully match the long-term needs of expanding radiopharmaceutical programs. That ceiling is one reason producers, governments, and research centers are putting more effort into scalable alternatives that can distribute production risk more widely across the actinium-225 therapeutic radioisotope market.

Cyclotron-based production is forecast to grow at 17.38% CAGR through 2031, making it the fastest-growing production route as suppliers move toward larger and more repeatable output. Eckert and Ziegler and the Nuclear Physics Institute of the Czech Academy of Sciences transitioned their joint initiative into high-volume cyclotron production in February 2026, which marked a practical step from development work into a more industrial supply model. NorthStar also confirmed successful routine commercial-scale actinium-225 production in January 2026 and later secured FDA acceptance of its Drug Master File for no-carrier-added actinium-225, adding another credible route to commercial supply. Hybrid and accelerator-linked approaches are also gaining relevance, with the DOE tri-lab effort and the first FDA-approved clinical trial using exclusively accelerator-produced actinium-225 helping reduce the earlier hesitation around non-generator supply. The overall mix is therefore shifting from dependence on one dominant route toward a broader supply base, which makes the actinium-225 therapeutic radioisotope market less exposed to a single feedstock or facility network.

By Application: Prostate Cancer Anchors Revenue While R&D Diversifies Pipeline

Prostate cancer accounted for 38.24% share of the actinium-225 therapeutic radioisotope market size in 2025, supported by PSMA overexpression in metastatic castration-resistant disease and by the clinical groundwork already laid by lutetium-177 PSMA treatment. The application continues to lead because it combines a known targeting biology with a patient population that still needs new options after progression on prior radioligand therapy. Bayer’s Phase 1 PAnTHa data presented at ASCO GU 2026 showed an objective response rate of 71% and PSA50 responses in 83% of patients at the recommended Phase 2 expansion dose, which supports continued investment in this part of the actinium-225 therapeutic radioisotope market. This position is strengthened further by published evidence that actinium-225 can show activity in beta-refractory patients, which means prostate cancer remains both the current revenue anchor and a continuing source of follow-on development opportunity.

Research and development is forecast to expand at 20.52% CAGR through 2031, making it the fastest-growing application as the pipeline spreads into additional tumor settings and more experimental targeting approaches. Neuroendocrine tumors remain an important next application because their receptor biology already supports radiopharmaceutical targeting logic that the field understands well. Leukemia and pancreatic cancer are also receiving attention, with programs such as [Ac-225]RTX-2358 showing that developers are pairing actinium-225 with new target classes and manufacturing partnerships as they broaden the treatment map. PharmaLogic and Ratio Therapeutics expanded their manufacturing collaboration in 2026 to support clinical development of [Ac-225]RTX-2358, which shows how research growth in the actinium-225 therapeutic radioisotope market depends on both scientific design and dependable production execution. This widening application base helps the actinium-225 therapeutic radioisotope industry move beyond a single cancer focus and improves the long-run value of each incremental supply improvement.

By End User: Hospitals Lead Volume While Radiopharmacies Drive Access Expansion

Hospitals and cancer centers held 45.52% of the actinium-225 therapeutic radioisotope market share in 2025 because they concentrate the nuclear medicine staff, radiation safety procedures, and oncology patient throughput needed for alpha-emitting therapies. Their lead reflects where treatment can be delivered most reliably today, especially as product handling and patient administration still require a high level of institutional control. Academic and research institutes remain important because they support early translational work and trial execution, while pharmaceutical and biotechnology companies account for a meaningful share of direct isotope demand tied to manufacturing and development programs. This makes hospitals the present volume anchor of the actinium-225 therapeutic radioisotope market, even as the structure of access begins to widen.

Radiopharmacies are projected to grow at 18.25% CAGR through 2031, the fastest rate among end users, because shorter transit paths help preserve usable dose, reduce waste, and improve scheduling around a 9.9-day half-life. Their role matters more as the actinium-225 therapeutic radioisotope market moves from isolated specialist use toward broader treatment network coverage. The segment also benefits from the wider use of decentralized manufacturing and dispensing models, which are better suited to time-sensitive isotope delivery than a heavily centralized approach. As more production sites become qualified and more regions build nearby handling capacity, radiopharmacies should take a larger role in connecting upstream isotope output with downstream treatment demand in the actinium-225 therapeutic radioisotope market.

Geography Analysis

North America captured 36.22% of the actinium-225 therapeutic radioisotope market size in 2025, supported by long-established isotope infrastructure, national laboratory capabilities, and a dense base of radiopharmaceutical developers and suppliers. The United States remains central to this position because the Department of Energy continues to fund isotope expansion, including actinium-225 scale-up work at Brookhaven National Laboratory. The region is also adding future capacity through TerraPower Isotopes’ Bellwether Laboratory in Philadelphia, a USD 450 million project designed to increase production capacity 20-fold by 2029. Canada adds depth through production activity connected to TRIUMF and through targeted funding for cyclotron-linked expansion, which helps preserve North America’s lead in the actinium-225 therapeutic radioisotope market.

Europe remains the second-largest regional base in the actinium-225 therapeutic radioisotope market, with strength in both production capability and clinical use. Germany has an important position because it combines supplier activity with clinical treatment expertise, while the Czech Republic supports the region’s emerging cross-border production cluster. In February 2026, Eckert and Ziegler and UJF increased production volume through their joint actinium-225 initiative, giving Europe a more visible industrial supply role. The European Commission’s Joint Research Centre is also developing a liquid radium-226 target method that supports radium recycling, improved yield economics, and lower waste burden, which strengthens the region’s technical diversity inside the actinium-225 therapeutic radioisotope market.

Asia-Pacific is the fastest-growing regional segment at 20.15% CAGR through 2031, which gives the actinium-225 therapeutic radioisotope market its strongest growth runway outside North America. Japan leads this regional acceleration through an explicit domestic manufacturing push. The Quantum Science and Technology Research and Development Organization began supplying actinium-225 to the National Cancer Center Research Institute in March 2025 under a cooperation framework signed in December 2024, showing that the region is moving from planning into operating supply relationships. Japan is also targeting an actinium-225 production demonstration in the fast reactor Joyo by FY2026, while NovAccel plans to begin sample supply from Hiroshima University in Q4 2026 using its compact superconducting accelerator platform. The Middle East and Africa remain early-stage participants, though South Africa’s role in the IAEA Global Radium-226 Management Initiative shows that feedstock and capability building are already underway. South America is still nascent in the actinium-225 therapeutic radioisotope market, but it remains strategically relevant because any future regional growth will depend on whether local nuclear medicine systems can connect with international isotope supply and therapy delivery standards.

Competitive Landscape

The actinium-225 therapeutic radioisotope market has 2 connected competitive layers, one centered on isotope production and the other centered on drug development. The upstream group includes suppliers such as TerraPower Isotopes, NorthStar Medical Radioisotopes, Eckert and Ziegler, BWXT Medical, Niowave, ITM and Actineer, Cardinal Health, and PanTera, while the downstream group includes developers such as AstraZeneca and Fusion, Bayer, Eli Lilly and Point Biopharma, Bristol Myers Squibb and RayzeBio, Actinium Pharmaceuticals, Aktis Oncology, and Cellectar Biosciences. These groups are becoming more interdependent because the actinium-225 therapeutic radioisotope market no longer treats supply as a background input, and developers increasingly need early production relationships to keep pipelines moving. The result is a competitive structure where supply security, regulatory readiness, and technical output quality now sit beside clinical performance as the main tools of differentiation.

The producer side of the actinium-225 therapeutic radioisotope market is moderately concentrated because only a limited set of companies can deliver clinically relevant quantities, yet the developer side remains more fragmented across tumor types and platform designs. NorthStar strengthened its position in 2026 by confirming routine commercial-scale production in January and securing FDA acceptance of its Drug Master File in April, which gave it stronger credibility with developers seeking compliant commercial supply. Eckert and Ziegler also advanced its standing through higher-volume cyclotron production and by signaling in its Q1 2026 investor presentation that it sees actinium-225 as the next major therapy isotope and expects the first commercial drug approval tied to the area in 2028. TerraPower’s May 2026 groundbreaking in Philadelphia is another important move because it aims to turn future scale into a competitive advantage before the actinium-225 therapeutic radioisotope market fully commercializes.

The most important competitive behavior is still the search for a durable supply moat, because secure isotope access can determine whether a program reaches trial milestones on time. This is why the actinium-225 therapeutic radioisotope market is seeing closer alignment between producers, developers, and specialized manufacturing partners. White-space opportunities remain for companies that can support frequent, smaller-batch delivery into decentralized radiopharmacy and hospital networks, because logistics still shape dose usability and treatment scheduling. Technology quality is also becoming a more visible differentiator, and research from CERN-MEDICIS published in Nature Scientific Reports showed that mass separation can achieve far better actinium-225 and actinium-227 selectivity than conventional separation methods. That kind of quality advantage could support a premium supply position in the actinium-225 therapeutic radioisotope market, especially when regulators and developers place more weight on impurity control. Competitive pressure is therefore likely to increase from both scale and precision, rather than from scale alone.

Actinium-225 Therapeutic Radioisotope Industry Leaders

Bayer AG

NorthStar Medical Radioisotopes, LLC

ITM Isotope Technologies Munich SE

Eckert and Ziegler Strahlen- und Medizintechnik AG

Telix Pharmaceuticals Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: TerraPower Isotopes broke ground on the 250,000 sq ft Bellwether Laboratory in Philadelphia, Pennsylvania, representing a USD 450 million investment to increase Ac-225 production capacity 20-fold by 2029. Pennsylvania provided USD 10 million in state incentives. The facility is designed to position TerraPower as the premier global distributor of cGMP Ac-225.

- April 2026: Cardinal Health announced a significant expansion of Ac-225 production capabilities at its Center for Theranostics Advancement in Indianapolis. The company had quadrupled its weekly Ac-225 output since the end of 2024 and added a high-capacity production line to its Drug Master File, expanding cGMP-compliant supply for investigational and future commercial programs.

Global Actinium-225 Therapeutic Radioisotope Market Report Scope

As per the scope of the report, Actinium-225 (Ac-225) is a radioactive isotope used in targeted cancer therapy. It is a therapeutic radioisotope that emits alpha particles, which have high energy and a very short range, making it effective for destroying cancer cells while minimizing damage to surrounding healthy tissue. Ac-225 is commonly employed in radiopharmaceuticals for treating various types of cancers, particularly those resistant to other treatments. Its ability to deliver potent radiation directly to tumor sites makes it a promising agent in targeted alpha therapy (TAT).

The actinium-225 therapeutic radioisotope market is segmented by production method into thorium-229 decay-based production, cyclotron-based production, reactor and accelerator hybrid production, and other production methods; by application into prostate cancer, neuroendocrine tumors, leukemia, pancreatic cancer, research and development, and other applications; by end user into hospitals and cancer centers, academic and research institutes, pharmaceutical and biotechnology companies, radiopharmacies, and other end users; and by geography into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Thorium-229 Decay-Based Production |

| Cyclotron-Based Production |

| Reactor and Accelerator Hybrid Production |

| Other Production Methods |

| Prostate Cancer |

| Neuroendocrine Tumors |

| Leukemia |

| Pancreatic Cancer |

| Research and Development |

| Other Applications |

| Hospitals and Cancer Centers |

| Academic and Research Institutes |

| Pharmaceutical and Biotechnology Companies |

| Radiopharmacies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Production Method | Thorium-229 Decay-Based Production | |

| Cyclotron-Based Production | ||

| Reactor and Accelerator Hybrid Production | ||

| Other Production Methods | ||

| By Application | Prostate Cancer | |

| Neuroendocrine Tumors | ||

| Leukemia | ||

| Pancreatic Cancer | ||

| Research and Development | ||

| Other Applications | ||

| By End User | Hospitals and Cancer Centers | |

| Academic and Research Institutes | ||

| Pharmaceutical and Biotechnology Companies | ||

| Radiopharmacies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2031 outlook for actinium-225 therapeutic radioisotopes?

The actinium-225 therapeutic radioisotope market is projected to reach USD 582.35 million by 2031 from USD 298.55 million in 2026, growing at a 14.30% CAGR over 2026-2031.

Which region leads global demand and supply activity?

North America led with a 36.22% share in 2025, supported by DOE infrastructure, commercial producers, and a dense radiopharmaceutical development base.

Which region is expanding the fastest through 2031?

Asia-Pacific is forecast to grow at a 20.15% CAGR through 2031, driven mainly by Japan's domestic manufacturing and demonstration programs.

Which production route currently dominates, and which is growing fastest?

Thorium-229 decay-based production held 55.31% share in 2025, while cyclotron-based production is projected to grow fastest at 17.38% CAGR through 2031.

Why is prostate cancer the largest application area?

Prostate cancer held 38.24% share in 2025 because PSMA targeting is already well established and actinium-225 is showing activity even after lutetium-177 exposure.

What is the main constraint on wider clinical adoption?

Supply remains the main bottleneck, because the number of scalable and qualified production sources is still limited even as clinical programs continue to expand.

Page last updated on: