Acrylic Teeth Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

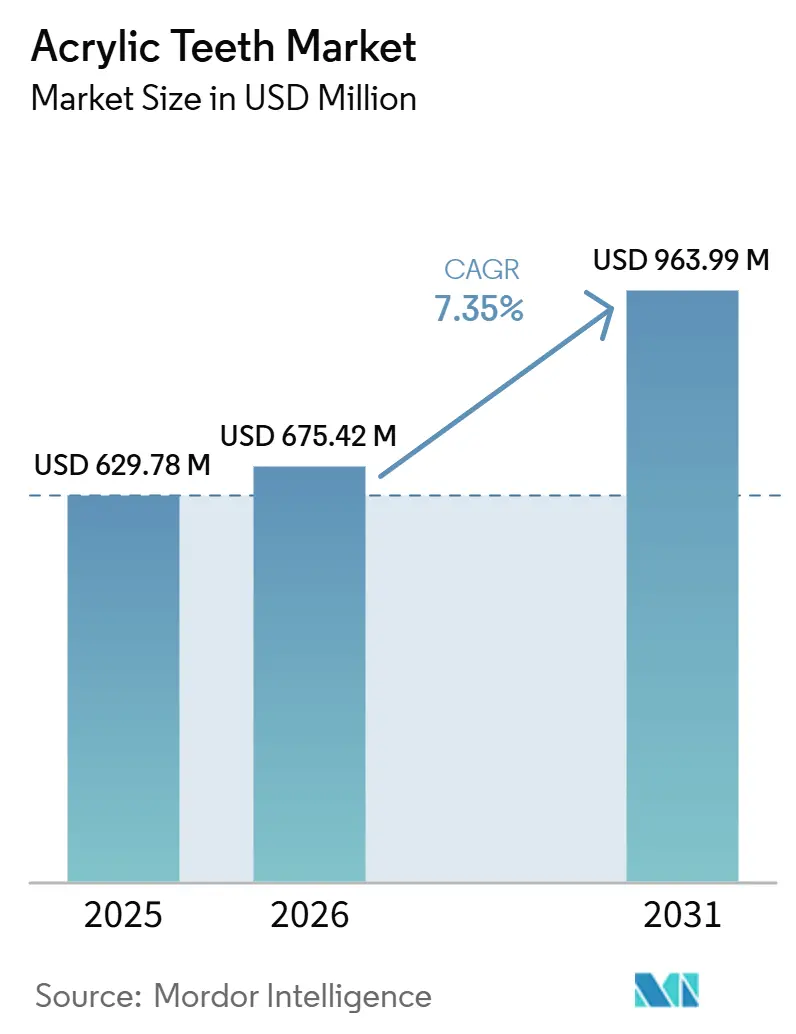

| Market Size (2026) | USD 675.42 Million |

| Market Size (2031) | USD 963.99 Million |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

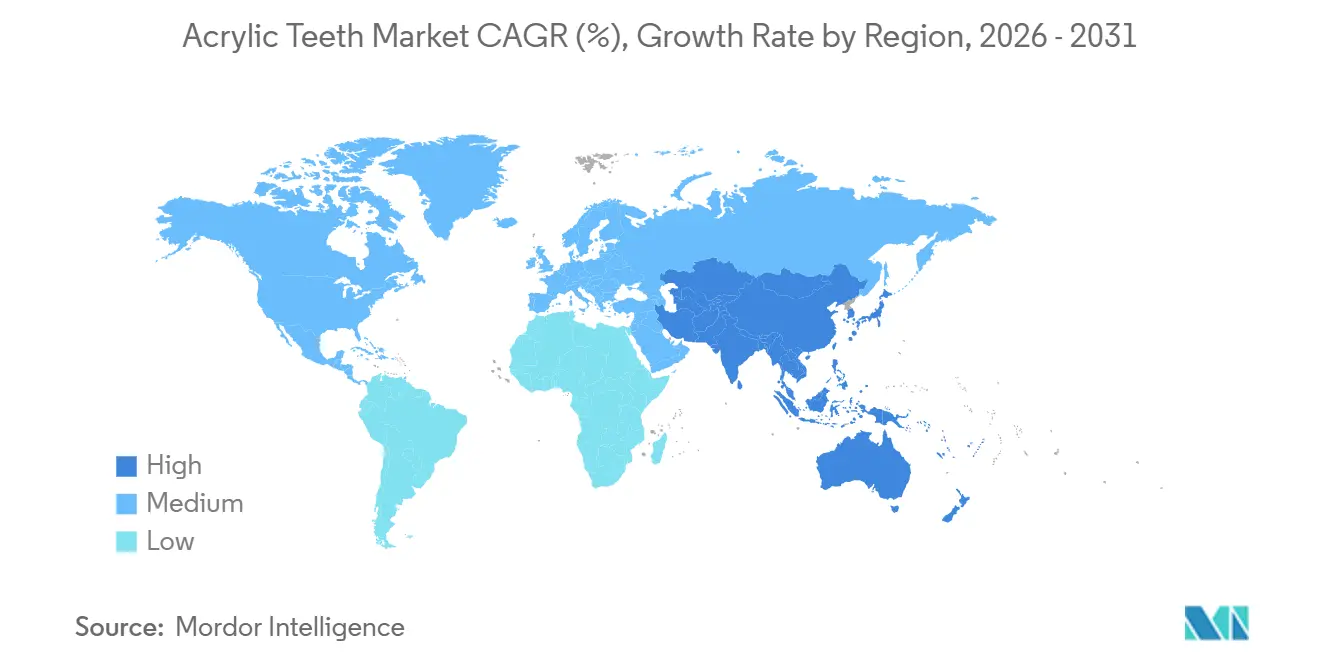

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

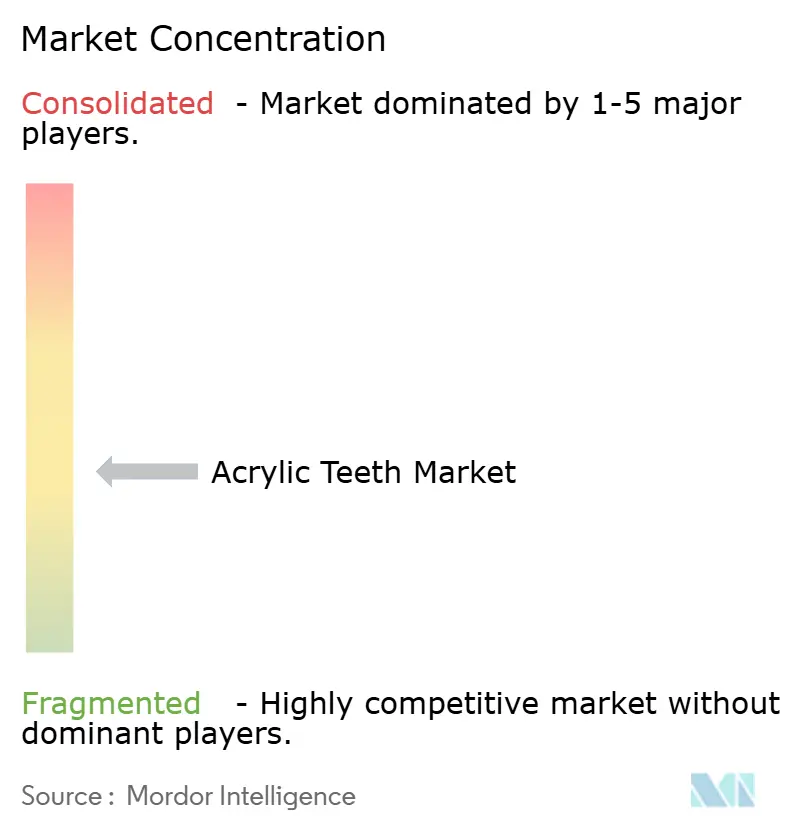

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acrylic Teeth Market Analysis by Mordor Intelligence

The Acrylic Teeth Market size is expected to increase from USD 629.78 million in 2025 to USD 675.42 million in 2026 and reach USD 963.99 million by 2031, growing at a CAGR of 7.35% over 2026-2031.

The Acrylic teeth market is supported by the rising number of edentulous patients worldwide, and the long-term outlook remains tied more to population aging and absolute case growth than to any deterioration in oral health rates. The 50 to 64 age group is expanding fastest among new edentulism cases, which keeps demand visible for removable prosthetics and supports repeat replacement needs over several years. The Acrylic teeth market is also being reshaped by digital denture production, as laboratories and larger clinic networks move toward printed and milled workflows that improve consistency and shorten turnaround times. Product competition is moving toward better shade depth, cross-linked polymers, and digital compatibility, which is why multilayer products and aesthetic applications are gaining ground inside the Acrylic teeth market.

Key Report Takeaways

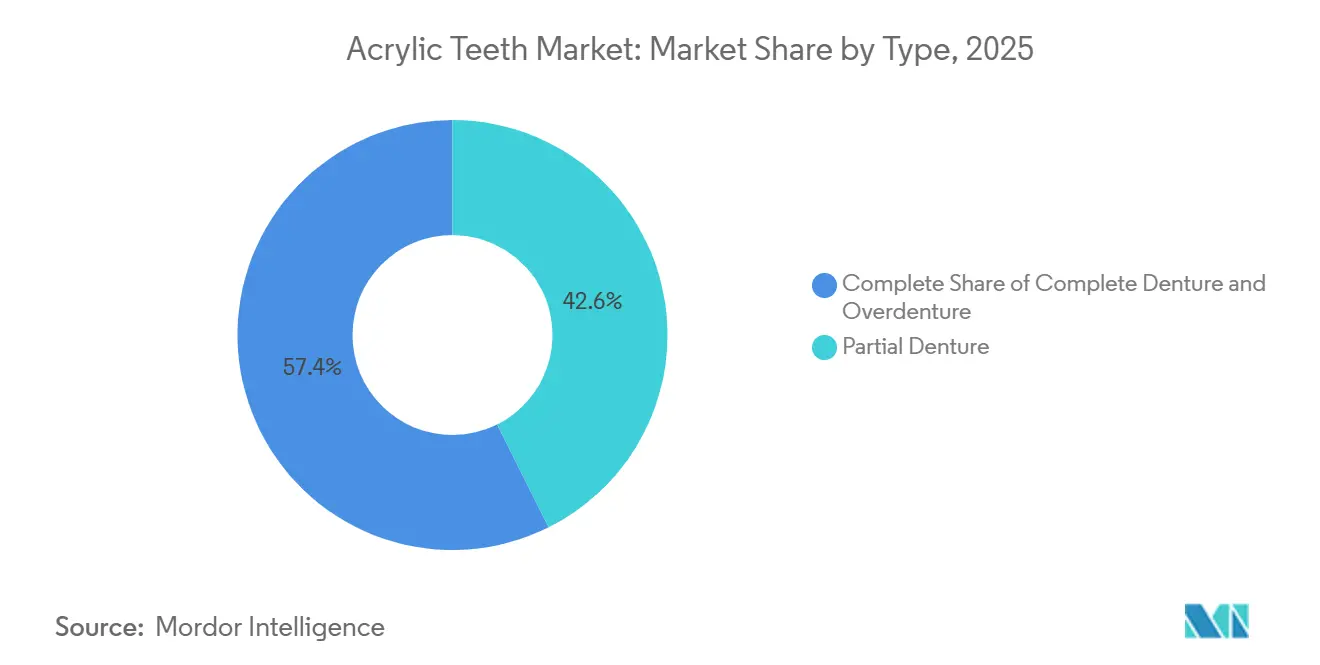

- By type, partial dentures held 42.62% share in 2025, while overdentures are projected to record a CAGR at 8.76% through 2031.

- By layer, three-layer acrylic teeth led with 39.65% share in 2025, while four-layer formats are forecast to expand at 8.47% CAGR through 2031.

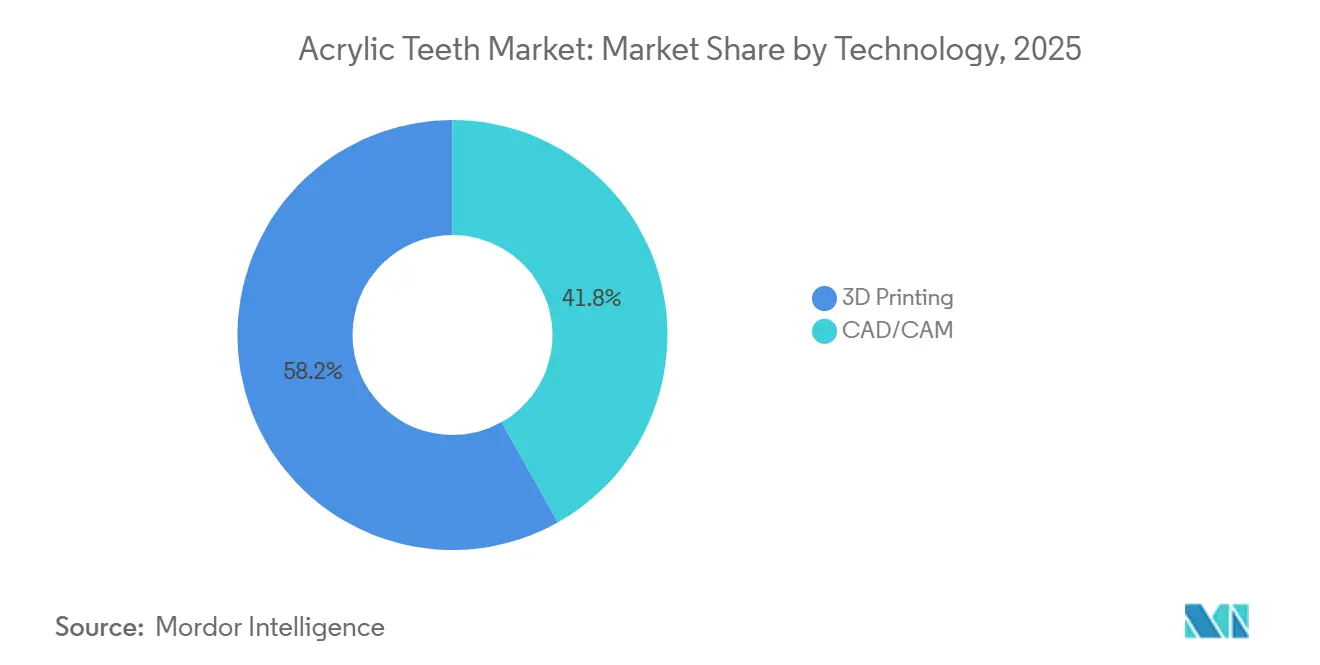

- By technology, 3D printing accounted for 58.17% share in 2025, while CAD/CAM is advancing at 9.15% CAGR through 2031.

- By application, functionality captured 57.42% share in 2025, while aesthetics is forecast to grow at 9.45% CAGR through 2031.

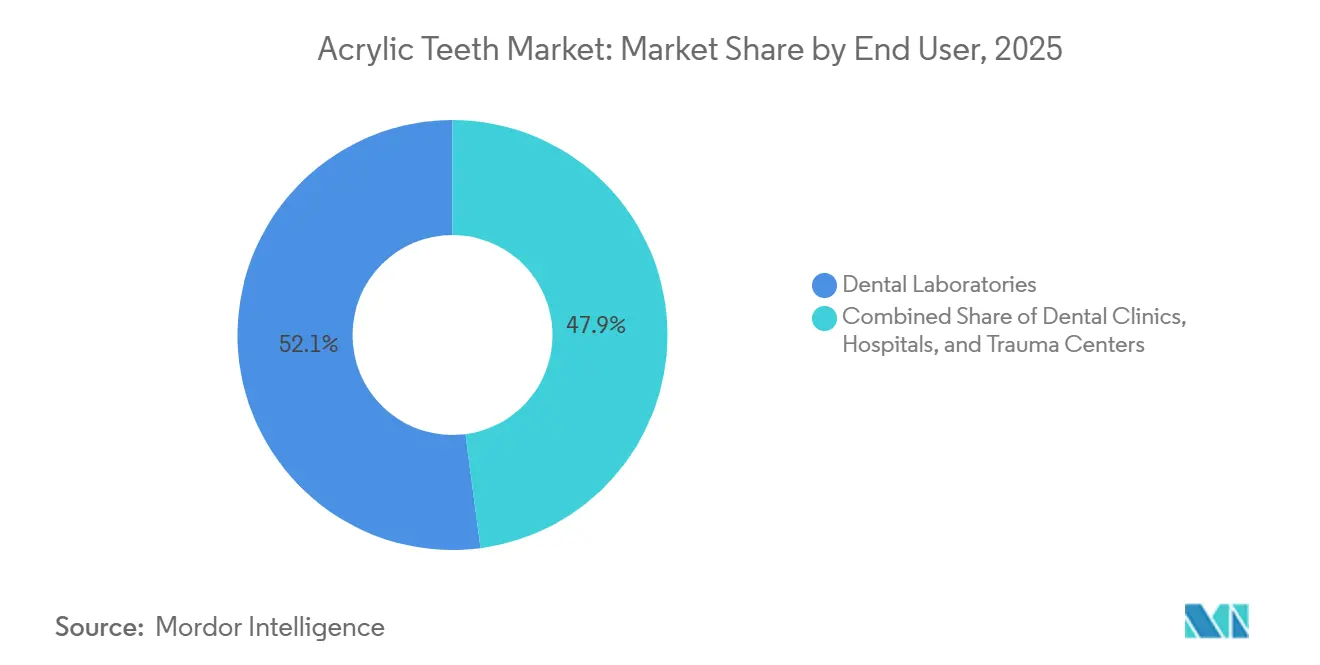

- By end user, dental laboratories held 52.07% share in 2025, while dental clinics posted the highest projected CAGR at 8.91% through 2031.

- By geography, North America retained 42.15% share in 2025, while Asia-Pacific is projected to expand at 8.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acrylic Teeth Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Edentulism and Geriatric Tooth Loss | +2.5% | Global, with concentration in Latin America, East Asia, and Eastern Europe | Long term (≥ 4 years) |

| Cost Advantage Over Ceramic and Zirconia Alternatives | +1.4% | Global, with strongest effect in APAC and Latin America | Medium term (2-4 years) |

| Expansion of Digital Denture Workflows in Dental Labs | +1.8% | North America, Western Europe, China, and Australia | Medium term (2-4 years) |

| Increased Demand for Aesthetic, Shade-Matched Prosthetics | +1.3% | North America, Europe, Japan, and South Korea | Medium term (2-4 years) |

| Growth in Public and Private Dental Care Access in Emerging Markets | +1.1% | India, Southeast Asia, Brazil, and the GCC | Long term (≥ 4 years) |

| Replacement Cycles in High-Wear Partial Dentures | +0.8% | Global, with higher incidence in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Edentulism and Geriatric Tooth Loss

The Acrylic teeth market is growing on the back of a larger global pool of edentulous patients, even though age-standardized rates have not worsened at the same pace as total case counts. Population size contributed 62.2% of the absolute burden increase and aging structure contributed 50.6%, which shows why the Acrylic teeth market is tied closely to demographics rather than short-term treatment cycles.[1]The global, regional, and national patterns of change in the burden of edentulism, 1990–2021: an analysis of the global burden of disease study 2021 and forecast to 2041 Global edentulism affected 353 million people in 2021, and projections point to more than 660 million edentulous individuals by 2050. The 50 to 64 cohort is expanding fastest, which creates a long replacement and maintenance runway for the Acrylic teeth market because these patients may remain in care pathways for many years. China will remain central to future demand, with 130.23 million edentulous people projected by 2050, which keeps Asia relevant to long-term Acrylic teeth market expansion.

Cost Advantage Over Ceramic and Zirconia Alternatives

The Acrylic teeth market keeps its broadest patient reach because removable polymer prosthetics remain a practical option for cost-sensitive treatment settings, especially when compared with more premium restorative materials described in the user draft. Price is only part of the picture, because service life and replacement frequency also shape demand inside the Acrylic teeth market. A 2024 retrospective study covering 1,893 prostheses found a median survival of 45 months for acrylic partial dentures, compared with 73 months for metal-based alternatives.[2]Longevity of acrylic and cobalt-chromium removable partial dentures–A ten-year retrospective survival analysis of 1246 denture-wearing patients That shorter interval creates recurring replacement volume, which supports repeat orders for laboratories, clinics, and manufacturers serving the Acrylic teeth market. The same durability profile also keeps maintenance and follow-up clinically important, which helps sustain ongoing patient interaction rather than a one-time device sale. In practical terms, affordability plus predictable replacement cycles continue to make the Acrylic teeth market resilient across middle-income patient groups and price-sensitive care systems.

Expansion of Digital Denture Workflows in Dental Labs

The Acrylic teeth market is being reshaped by the move from hand-packed production to digital workflows in laboratory settings. In July 2025, 3D Systems commercially released its NextDent Jetted Denture Solution, an FDA-cleared monolithic system that prints teeth and base in a single pass for the United States market. The company stated that the system cuts a conventional five-day process to under one day and lowers manual labor by more than 50%, which improves economics for the Acrylic teeth market, where turnaround time matters. CAD/CAM products are also gaining attention because material suppliers are expanding disc and resin portfolios that fit premium denture workflows. This change favors higher-value materials with stronger shade control and better process consistency, which supports premium tiers within the Acrylic teeth market. As labs add software-linked material libraries and equipment-specific resin systems, the Acrylic teeth market is moving toward a workflow-based competitive model rather than a simple commodity model.

Increased Demand for Aesthetic, Shade-Matched Prosthetics

The Acrylic teeth market is seeing stronger demand for prosthetics that look more natural and fit patient expectations on shade, translucency, and visible smile design. Manufacturers are responding by expanding shade ranges and promoting premium cross-linked materials that improve wear behavior and appearance retention. VITA launched VITA VIONIC RESINS in April 2025 with nine classical shades for denture teeth and a dedicated base resin for digital workflows. Ivoclar’s SR Vivodent S DCL line offers 40 shade options and uses a four-layer Double Cross-Linked process, which fits the premium direction of the Acrylic teeth market. In February 2025, Aspen Dental and Ivoclar launched the Signature Elite Denture and supported the rollout with certification for more than 1,300 lab technicians, which shows that aesthetic upgrades are now moving through larger care networks. As those expectations spread beyond specialist practices, the Acrylic teeth market is likely to keep shifting from basic tooth replacement toward more appearance-led product selection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Material Wear, Staining, and Fracture Risk | -0.9% | Global, with strongest effect in high-use partial denture segments | Medium term (2-4 years) |

| Substitution by Implant-Supported and Fixed Prosthetics | -1.5% | North America, Western Europe, Japan, and South Korea | Long term (≥ 4 years) |

| Skilled Dental Technician Shortage in Lower-Income Markets | -0.7% | Sub-Saharan Africa, South Asia, and rural Southeast Asia | Long term (≥ 4 years) |

| PMMA Feedstock and Input Cost Volatility | -0.5% | North America, Europe, and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Material Wear, Staining, and Fracture Risk

The Acrylic teeth market still faces a clear material limitation because acrylic resin teeth wear faster and remain more vulnerable to staining and fracture than harder alternatives in demanding use cases. Manufacturers are trying to close the gap through reinforced polymer systems, including Kulzer’s NanoPearls concept and Ivoclar’s DCL approach, noted in the user draft. Even so, higher-wear settings still expose intrinsic limits around microcracks, occlusal stress, and appearance changes over time. This means the Acrylic teeth market keeps a solid value case, but it does not fully overcome performance concerns in cases where patients can access more durable options.

Substitution by Implant-Supported and Fixed Prosthetics

The Acrylic teeth market faces its strongest substitution pressure from dental implants and other fixed restorative options in higher-income care settings. The dental implants market places more clinical spending into permanent or semi-permanent treatment paths. That pressure is not uniform across the Acrylic teeth market, because part of implant adoption still supports removable overdentures rather than eliminating acrylic demand outright. North America, Western Europe, Japan, and South Korea remain the most exposed to this restraint because implant access and surgical infrastructure are strongest there, based on the pattern described in the user draft. As a result, the Acrylic teeth market is not losing relevance everywhere, but its mix is shifting toward more hybrid and price-tiered treatment pathways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Partial Dentures Anchor Volume While Overdentures Lead Growth

Partial dentures held 42.62% of the acrylic teeth market share in 2025, which made them the largest type segment by volume. Their lead reflects the broad patient base for partially edentulous treatment, since many patients still retain natural dentition and require transitional or interim restorative support. The Acrylic teeth market benefits from this segment because partial dentures are widely used across age groups, rather than being tied only to advanced geriatric needs. Acrylic remains attractive here because it is easier to adjust chairside and easier to rebase when clinical conditions change during treatment. The 2024 retrospective study also showed that maintenance intervals under 3 months materially improved survival outcomes, which points to recurring service opportunities around the core volume base.

Overdentures are projected to grow at 8.76% CAGR through 2031, which makes them the fastest-growing type within the Acrylic teeth market. Their rise reflects a practical middle path, since patients can gain better retention from implants without paying for a fully fixed bridge in every case. This also shows how the Acrylic teeth industry is adapting rather than retreating when implant care expands. Complete dentures remain the second-largest type and still track aging populations in mature European markets such as Germany, France, and Spain, as stated in the user draft. Replacement demand also keeps type volumes active, because acrylic partial dentures have a median service life of 45 months and therefore return patients to the care cycle on a predictable basis.

By Layer: Three-Layer Products Hold the Base While Four-Layer Products Move Upmarket

Three-layer acrylic teeth retained 39.65% share in 2025, which kept them as the largest layer configuration across the Acrylic teeth market. Their position comes from a balanced mix of esthetic quality and mechanical performance, which has made them a common mid-tier and premium choice for many denture indications. Two-layer products still serve cost-sensitive cases and remain important where laboratories focus on value throughput rather than appearance-led upgrades. Other layer formats hold narrower positions in specialty cases, but they do not shape the main volume structure of the Acrylic teeth market in the same way. This leaves three-layer products as the practical center of the segment, especially where functionality and acceptable aesthetics need to be balanced at scale.

Four-layer products are forecast to grow at 8.47% CAGR through 2031, which makes them the fastest-moving layer segment in the Acrylic teeth market. Their growth is tied to deeper shade gradation, better visual layering, and stronger fit with premium digital denture workflows. Ivoclar’s SR Vivodent S DCL shows this direction clearly, since it combines a four-layer process with 40 shade options and higher compressive strength than conventional PMMA products. Candulor’s TCR milling discs also show that the Acrylic teeth industry is redefining value around cross-link density and abrasion resistance, not only around visible layer count. In practice, layer competition is moving toward premium chemistry and digital compatibility, which keeps four-layer products well placed for the next growth cycle.

By Technology: 3D Printing Leads Current Scale While CAD/CAM Gains Faster

3D printing accounted for 58.17% of the Acrylic teeth market size in 2025, which made it the leading technology path across laboratories using digital denture workflows. That lead reflects how widely resin-based additive production has already spread for denture teeth and base fabrication. The July 2025 commercial release of 3D Systems’ NextDent Jetted Denture Solution marked a visible step change, because the platform prints teeth and base in one pass and cuts labor input by more than 50%.[3]3D Systems Announces Major Milestone in Digital Dentistry with Full Commercial Release of New FDA-cleared Denture Solution Carbon’s FP3D, made commercially available in September 2025, expanded printed workflow relevance into flexible removable partial dentures and broadened the reach of digital fabrication. These developments keep printed production central to the Acrylic teeth market where throughput, speed, and platform standardization matter most.

CAD/CAM is projected to grow at 9.15% CAGR through 2031, which makes it the fastest-growing technology segment in the Acrylic teeth market. Laboratories are moving further into milled PMMA disc workflows because reproducibility and occlusal accuracy matter more as case complexity rises. VITA expanded its VIONIC DENT DISC portfolio in October 2024 with five additional shades, and Candulor continued to position TCR Mono and Multi discs as premium milling options. In June 2026, Dentsply Sirona extended its Lucitone Digital Print Denture ecosystem to the HeyGears UltraCraft MMF printer, which shows how the printed and milled branches of the Acrylic teeth market are starting to converge into shared digital platforms. The result is not a simple winner-takes-all shift, but a broader digital upgrade cycle where both technologies expand with different use priorities.

By Application: Functional Use Holds the Base While Aesthetic Use Expands Faster

Functionality held 57.42% share in 2025, which kept it as the main application across the Acrylic teeth market. This reflects the clinical purpose of most removable prosthetics, since restoring chewing efficiency and practical oral function still comes before cosmetic enhancement in many treatment decisions. In lower reimbursement and lower budget settings, buyers continue to focus on fit, fracture resistance, and dependable day-to-day use rather than extended shade libraries. That is why conventional three-layer products remain important in large-volume applications across the Acrylic teeth industry. The segment’s large share shows that practical restoration still defines the base demand pool for the Acrylic teeth market.

Aesthetics is forecast to grow at 9.45% CAGR through 2031, which makes it the fastest-growing application in the Acrylic teeth market. This shift is being supported by wider shade ranges, better digital visualization, and stronger patient attention to visible appearance during denture selection. Aspen Dental’s February 2025 rollout of the Signature Elite Denture showed that premium esthetic lines are now entering larger chain settings with national scale rather than staying limited to niche prosthodontic practices. That product used SR Vivodent SDCL anterior teeth and an IvoBase heat-injected base, which matched the premium direction already visible across the Acrylic teeth industry. As a result, pricing power and product differentiation are becoming more concentrated in appearance-led offerings than in purely basic restorative lines.

By End User: Dental Laboratories Hold the Largest Base While Dental Clinics Rise Faster

Dental laboratories held 52.07% share in 2025, which made them the largest end-user channel in the Acrylic teeth market. Their lead reflects the continued importance of centralized fabrication, batch workflows, and specialized technical capacity for both partial and complete dentures. Large operators are using digitalization to defend unit economics, which is why investment in milling, printing, and material libraries remains a central feature of the Acrylic teeth market. Modern Dental Group reported a 47.7% net profit surge in 2025 and linked the gain to digitalization-driven operating efficiency, which underlines the scale benefits available to larger laboratory players.[4]Modern Dental Group Announces 2025 Annual Results, Net Profit Surges 47.7% on Digitalization-Driven Operational Efficiency Gains Hospitals and trauma centers remain a distinct sub-segment for institutional and complex restorative cases, but they do not set the overall channel balance of the Acrylic teeth market.

Dental clinics are projected to grow at 8.91% CAGR through 2031, which makes them the fastest-growing end-user category in the Acrylic teeth market. This reflects the spread of in-house milling and chairside printing, which reduces dependence on external laboratory turnaround and supports faster delivery. The June 2026 Dentsply Sirona and HeyGears workflow expansion also supports this direction, because it simplifies monolithic production and makes digital denture fabrication more accessible beyond traditional central labs. The Acrylic teeth industry is also benefiting from the growth of clinic networks in India, Southeast Asia, and the GCC, where standardized digital systems can be deployed across multiple sites, as described in the user draft. That shift does not remove laboratories from the value chain, but it does narrow the gap between where a prosthetic is prescribed and where it can be produced inside the Acrylic teeth market.

Geography Analysis

North America held 42.15% of Acrylic teeth market share in 2025, which kept it as the largest regional segment. The region benefits from dense private laboratory networks, broad private dental coverage, and strong patient demand for immediate-load and same-day restorative pathways, based on the user draft. The July 2025 FDA-cleared commercial release of 3D Systems’ monolithic NextDent denture platform also reinforced North America’s lead in digital adoption and regulatory validation.

Europe remains a major regional base for the Acrylic teeth market because it combines an aging patient profile with one of the deepest clusters of premium material manufacturers. VITA Zahnfabrik, Kulzer, Ivoclar, Candulor, and Merz Dental have shaped the region’s position through material science, established laboratory relationships, and strong digital workflow integration. The region also benefits from steady complete denture demand in mature Western markets, where older patient cohorts continue to support replacement and maintenance volume. Digital denture adoption is visible across both printing and milling, with companies such as Stratasys and VITA extending workflow options for laboratories that want higher throughput and better shade flexibility. That mix keeps Europe important to the Acrylic teeth market not only as a consumption base, but also as a center for premium product design and process standards.

Asia-Pacific is projected to grow at 8.77% CAGR through 2031, which makes it the fastest-growing geography in the Acrylic teeth market. China is central to that outlook because it combines an expanding manufacturing base with the world’s largest future pool of edentulous patients, reaching 130.23 million by 2050 according to the GBD 2021 projections. Japan and South Korea continue to support premium demand through established domestic dental material ecosystems, while India and Southeast Asia add growth through broader care access and expanding clinic networks, as described in the user draft.

Competitive Landscape

The Acrylic teeth market shows moderate concentration in premium products and broader fragmentation in mid-tier and commodity supply. European specialists such as Ivoclar, VITA Zahnfabrik, Kulzer, Candulor, and Merz Dental compete through materials engineering, shade systems, and software-linked workflow compatibility rather than through pure price. Their strategy is to become the default material choice inside digital design systems, which makes software integration as important as standalone tooth performance in the Acrylic teeth market. VITA’s validation of VIONIC resins for RAYSHAPE 3D printers in China and Candulor’s preloaded libraries in 3Shape are clear examples of this workflow-lock approach. Dentsply Sirona’s June 2026 expansion of Lucitone Digital Print Denture compatibility to the HeyGears UltraCraft MMF system followed the same logic at a broader commercial scale.

Asian manufacturers such as Huge Dental Material, Shanghai Pigeon Dental, and Yamahachi Dental remain important on cost and scale, but the user draft shows that they are also pushing into higher-layer and reinforced material formats. This means the Acrylic teeth market is not dividing neatly between low-cost Asia and premium Europe, because product architecture and digital readiness are moving up across both groups. Carbon’s September 2025 commercial release of FP3D added another competitive opening, since flexible partial denture materials extend digital workflow relevance into an adjacent category that traditional prefabricated tooth suppliers did not fully control before. Stratasys also expanded competitive pressure in Europe with the January 2025 launch of TrueDent as a CE Mark Class I device, which widened the installed base for monolithic digital denture production.

Modern Dental Group stands out for geographic expansion, which gives the Acrylic teeth market a different kind of competitive model based on scale, acquisition, and regional manufacturing reach. Its January 2025 acquisition of Hexa Ceram in Thailand added local production capacity in Southeast Asia, while the September 2025 Sindan agreement created an entry point into the UAE and wider MENA laboratory buildout. Aspen Dental and Ivoclar’s February 2025 Signature Elite Denture launch showed a different route, where branded premium denture systems scale through national clinic networks rather than laboratory acquisitions. Together, these moves show that the Acrylic teeth market is being shaped by platform integration, targeted material upgrades, and regional footprint expansion rather than by one dominant global leader.

Acrylic Teeth Industry Leaders

Dentsply Sirona Inc.

Ivoclar Vivadent AG

Kulzer GmbH

SHOFU INC.

VITA Zahnfabrik H. Rauter GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Dentsply Sirona and HeyGears expanded their digital denture workflow ecosystem with the validation of Lucitone Digital Print Denture resins for the HeyGears UltraCraft Multi-Material Fusion (MMF) DLP 3D printer. The collaboration enables bonding-free monolithic one-piece denture production, eliminating the previously required tooth-to-base bonding step and improving lab throughput and structural consistency for full-arch and partial acrylic dentures.

- September 2025: Modern Dental Group signed a Memorandum of Understanding with Sindan (UAE) at Hong Kong's "Belt and Road Summit" to develop the first world-class dental laboratory in the UAE, targeting rapid entry into the MENA market using advanced digital fabrication technologies and Modern Dental's global prosthetics expertise.

- September 2025: Carbon announced full commercial availability of FP3D, an FDA-cleared flexible removable partial denture resin with dual-cure chemistry, developed with Keystone Industries. FP3D is the first dental resin to use Carbon's dual-cure technology, enabling 3D printing of flexible partial dentures with improved durability, translucency, and dimensional accuracy over traditional fabrication methods.

- July 2025: 3D Systems announced full commercial release of the NextDent Jetted Denture Solution for the US market, the first FDA-cleared monolithic jetted denture system. Using the NextDent 300 MultiJet printer, the system prints denture teeth and base in a single pass at 300% faster throughput than analog workflows, reducing manual labor by over 50% and targeting a USD 600 million US denture replacement market. European and Asian market releases are pending regional regulatory approvals.

Global Acrylic Teeth Market Report Scope

The Acrylic Teeth Market refers to the global market for artificial acrylic resin teeth used in the fabrication and restoration of removable dental prostheses to replace missing natural teeth. It encompasses the manufacturing, distribution, and commercialization of acrylic teeth designed to restore oral function, aesthetics, and speech in edentulous and partially edentulous patients.

The acrylic teeth market is segmented by type, layer, technology, application, end user, and geography. By type, it is further divided into partial denture, complete denture, and overdenture. By layer, it is segmented into two-layer acrylic teeth, three-layer acrylic teeth, four-layer acrylic teeth, and other layer configurations. By technology, the market is segmented into CAD/CAM and 3D printing. By application, the market is segmented into functionality and aesthetics. By end user, the market is segmented into dental clinics, dental laboratories, hospitals, and trauma centers. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Partial Denture |

| Complete Denture |

| Overdenture |

| Two-Layer Acrylic Teeth |

| Three-Layer Acrylic Teeth |

| Four-Layer Acrylic Teeth |

| Other Layer Configurations |

| CAD/CAM |

| 3D Printing |

| Functionality |

| Aesthetics |

| Dental Clinics |

| Dental Laboratories |

| Hospitals |

| Trauma Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Partial Denture | |

| Complete Denture | ||

| Overdenture | ||

| By Layer | Two-Layer Acrylic Teeth | |

| Three-Layer Acrylic Teeth | ||

| Four-Layer Acrylic Teeth | ||

| Other Layer Configurations | ||

| By Technology | CAD/CAM | |

| 3D Printing | ||

| By Application | Functionality | |

| Aesthetics | ||

| By End User | Dental Clinics | |

| Dental Laboratories | ||

| Hospitals | ||

| Trauma Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the acrylic teeth market?

The Acrylic teeth market was valued at USD 629.78 million in 2025, is growing to USD 675.42 million in 2026, and is forecast to reach USD 963.99 million by 2031.

How fast is acrylic teeth demand expected to grow through 2031?

The Acrylic teeth market is projected to grow at 7.35% CAGR from 2026 to 2031, supported by rising edentulism, aging populations, and digital denture adoption.

Which product type leads acrylic teeth demand today?

Partial dentures led by type with 42.62% share in 2025, reflecting their broad use in partially edentulous patients and transitional restorative care.

Which part of the business is expanding the fastest?

Aesthetics is the fastest-growing application at 9.45% CAGR, while CAD/CAM is the fastest-growing technology at 9.15% CAGR and dental clinics are growing at 8.91% CAGR.

Which region offers the strongest growth outlook for acrylic teeth?

Asia-Pacific is the fastest-growing region at 8.77% CAGR through 2031, while North America remains the largest regional segment with 42.15% share in 2025.

Page last updated on: