Market Overview

| Study Period | 2019 - 2030 |

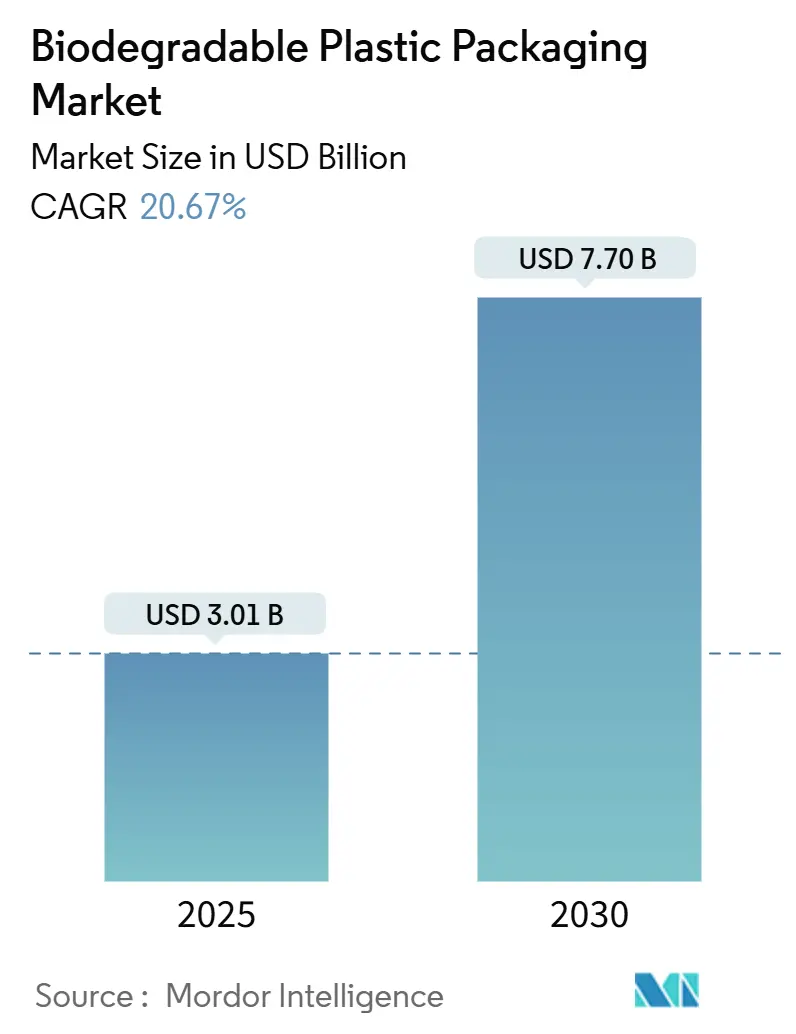

| Market Size (2025) | USD 3.01 Billion |

| Market Size (2030) | USD 7.70 Billion |

| Growth Rate (2025 - 2030) | 20.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Biodegradable Plastic Packaging Market Analysis by Mordor Intelligence

The biodegradable plastic packaging market size stands at USD 3.01 billion in 2025 and is forecast to reach USD 7.70 billion by 2030, expanding at a 20.67% CAGR. The strong trajectory reflects simultaneous regulatory mandates, corporate carbon-pricing policies, and rapid advances in bio-resin processing that together improve economic viability for compostable formats.[1]European Commission, “Single-use plastics,” environment.ec.europa.eu Brand owners now prefer global rather than regional packaging specifications, allowing large volume contracts that lower per-unit costs. Material innovation continues to cut performance gaps with conventional polymers; marine-degradable PHA and heat-resistant PBAT variants now satisfy demanding barrier and temperature requirements. In parallel, municipal waste-diversion targets push food-delivery and retail sectors to adopt certified compost-ready solutions, creating predictable offtake for resin suppliers. The biodegradable plastic packaging market therefore enjoys clear line-of-sight demand that compensates for still-volatile agricultural feedstock pricing.

Key Report Takeaways

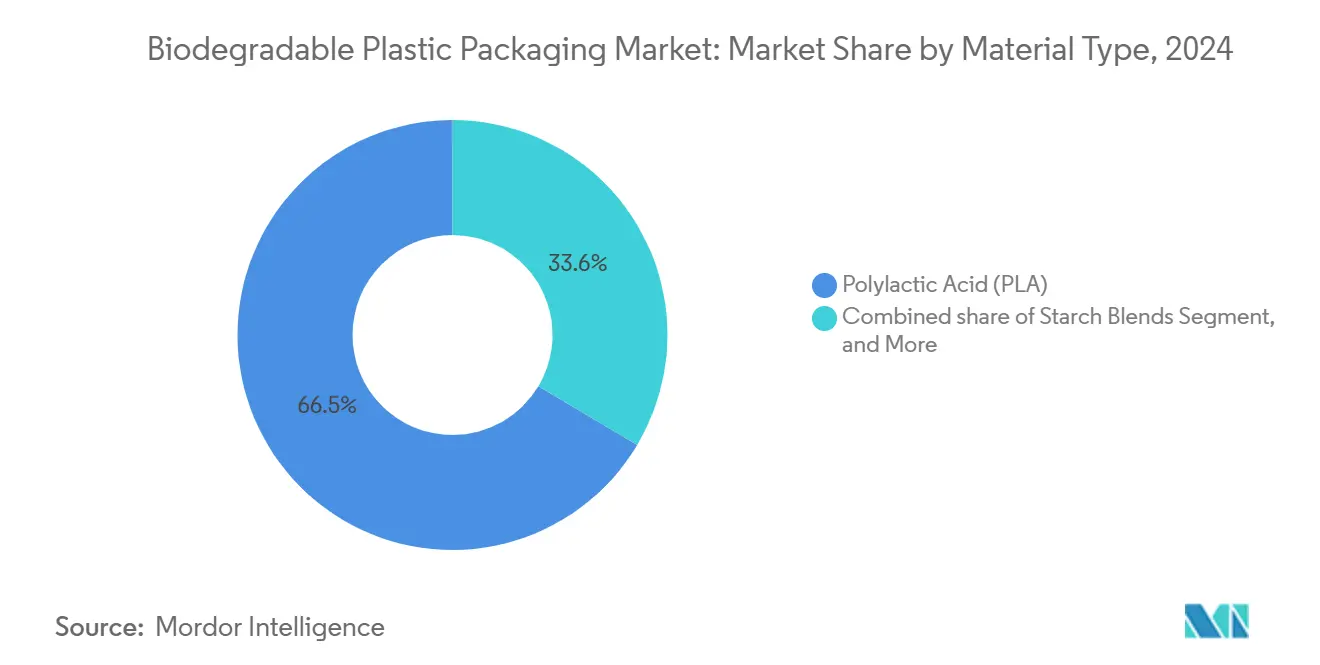

- By material type, Polylactic Acid retained 66.45% of biodegradable plastic packaging market share in 2024, while Polyhydroxyalkanoates are projected to grow at a 25.34% CAGR through 2030.

- By packaging type, flexible formats captured 58.77% revenue share of the biodegradable plastic packaging market size in 2024; rigid formats will post the fastest 23.1% CAGR to 2030.

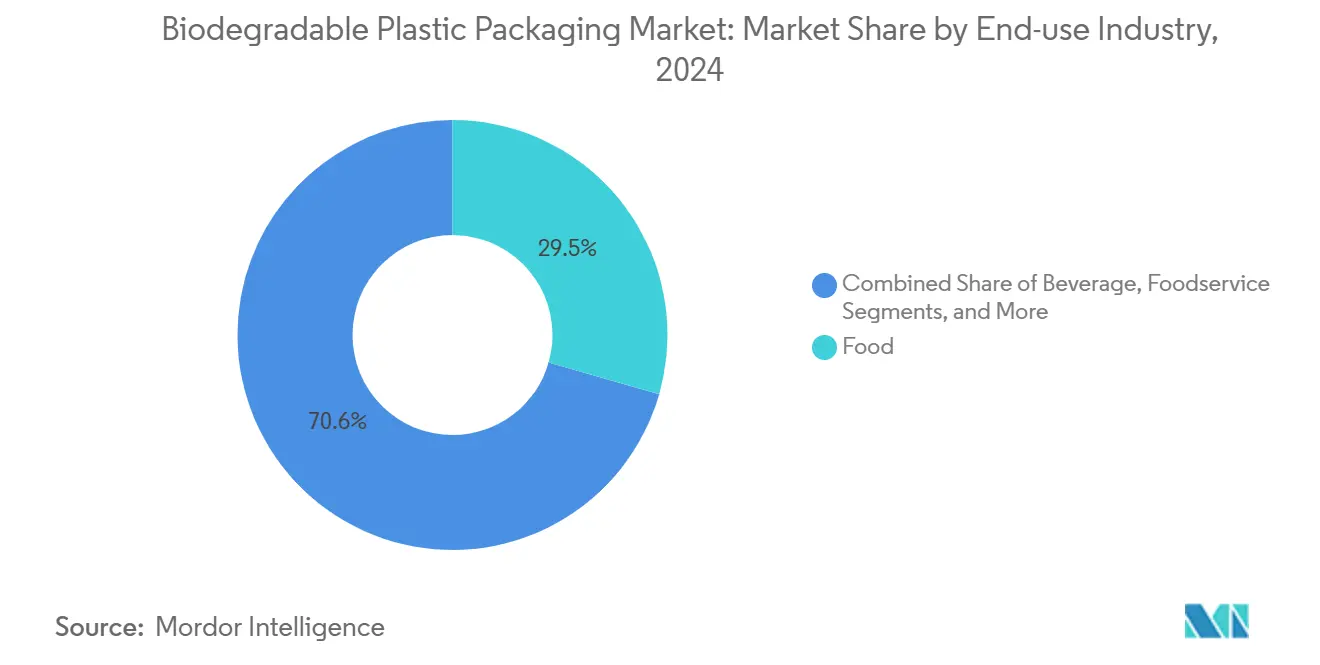

- By end-use industry, foodservice held 29.45% of the biodegradable plastic packaging market size in 2024 and is advancing at a 24.68% CAGR.

- By compostability, industrial-compostable variants commanded 55.78% share of the biodegradable plastic packaging market size in 2024, while home-compostable lines expand at a 22.56% CAGR.

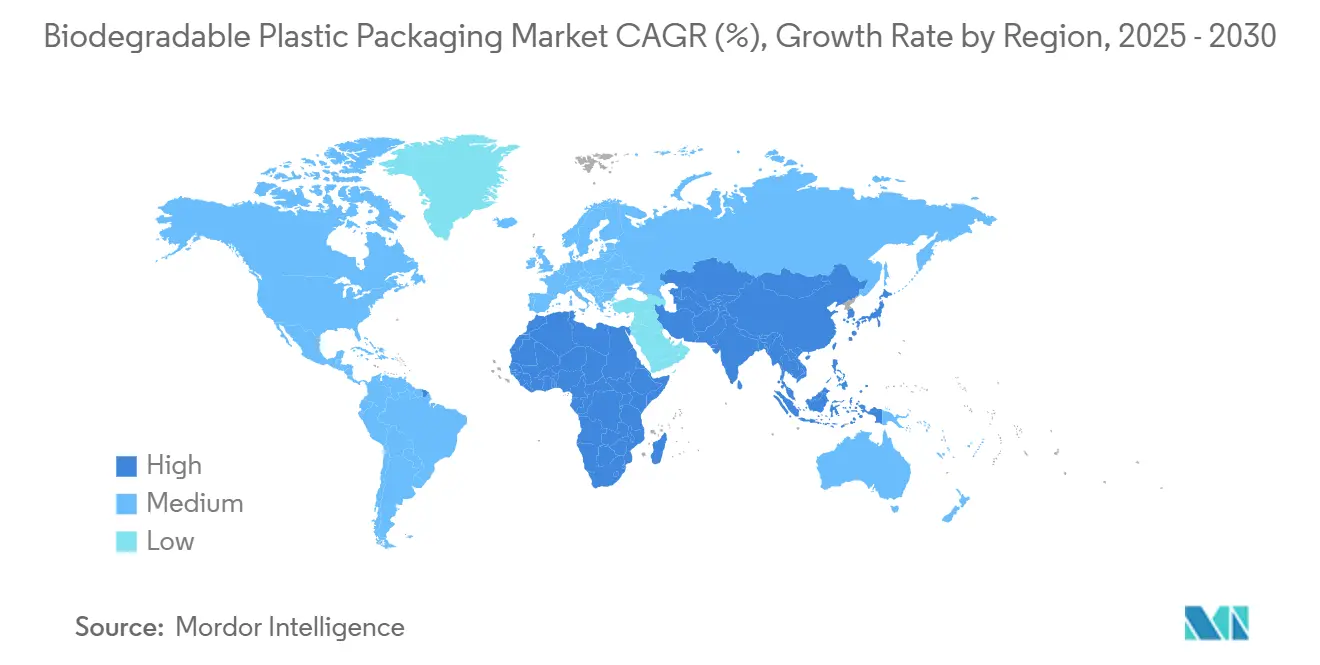

- By geography, Europe led with 35.57% biodegradable plastic packaging market share in 2024; Asia-Pacific represents the fastest-growing region at 24.65% CAGR.

Global Biodegradable Plastic Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated bans on single-use petro-plastic packaging across EU and India | +3.5% | Europe, India, expanding to ASEAN | Short term (≤ 2 years) |

| Food-delivery app proliferation requiring compost-ready formats in North America | +2.8% | North America, expanding to Latin America | Medium term (2-4 years) |

| Retailer "plastic-neutral" pledges boosting demand | +1.9% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Re-tooling of existing film-blowing lines to run bio-resins | +2.1% | Global manufacturing hubs | Short term (≤ 2 years) |

| Brand shift to transparent carbon-labelling on packs | +1.8% | Europe, North America, Japan | Long term (≥ 4 years) |

| Corporate internal carbon-price adoption favouring bio-options | +1.2% | Global Fortune 500 operations | Medium term (2-4 years) |

Source: Mordor Intelligence

Accelerated bans on single-use petro-plastic packaging across EU and India

The European Union’s 2024 Single-Use Plastic Directive immediately raised demand for certified compostable food-contact packs, replacing difficult-to-recycle items such as cutlery and clamshells. India’s statewide prohibitions expose more than 1.8 billion consumers to the same shift, forcing multinationals to harmonize global specifications and unlocking scale economies for resin plants. Penalties that exceed the premium on bio-materials further accelerate adoption. Australia’s 2024 bans reinforce a cascading policy effect that sustains volume visibility for producers.

Food-delivery app proliferation requiring compost-ready formats in North America

Leading aggregators mandate that restaurants use compostable bowls, cups, and cutlery in top metropolitan areas, aligning with municipal diversion goals and consumer preference tracking recorded in 2024. Delivery fee structures hide the material premium, so operators focus on brand perception and landfill fee savings. Chain pilots report 15-20% lower disposal costs and smoother compliance with city ordinances. The requirement has spilled into cloud kitchen networks, amplifying flexible-pack demand for sauces and sides.

Retailer “plastic-neutral” pledges boosting demand

Global retailers such as Walmart and Carrefour now offset residual petro-plastic tonnage with equal volumes of certified compostable packs, guaranteeing long-term offtake agreements that underpin resin plant expansions. Dedicated sustainability sourcing teams pay the bio-premium without procurement pushback because consumer studies confirm measurable preference boosts. Private-label control allows rapid switchovers, influencing nearly one-third of packaged goods in developed markets.

Re-tooling of existing film-blowing lines to run bio-resins

Retrofit kits for PLA and PBAT reduce conversion costs to below 15% of a new line, cutting changeover times to 4-6 weeks and letting converters service both fossil and bio segments with the same assets. Margin uplift of 20-25% on bio runs justifies capital spend, while manufacturing flexibility shields processors from resin price swings. This technical leap removes a historical barrier and widens the addressable converter base for the biodegradable plastic packaging market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight industrial-composting infrastructure outside Western Europe | -1.8% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Feed-stock price volatility for PLA (corn, sugarcane) | -1.4% | Global, concentrated in corn/sugarcane regions | Short term (≤ 2 years) |

| Consumer confusion around "compostable" vs "biodegradable" claims | -0.9% | Global, particularly in emerging markets | Medium term (2-4 years) |

| Mechanical-recycling stream contamination penalties in US and Japan | -0.7% | North America, Japan, expanding to EU | Short term (≤ 2 years) |

Source: Mordor Intelligence

Tight industrial-composting infrastructure outside Western Europe

Adoption in Asia-Pacific and Latin America recently outpaced the build-out of high-temperature composting plants capable of fully degrading bio-resins, risking landfill diversion and methane release that undermine environmental claims . Municipal funding limitations and permitting hurdles delay facility commissioning, while private operators await clearer acceptance rules for mixed food and packaging waste. Until capacity expands, sales into regions without adequate end-of-life options are capped, tempering the otherwise rapid uptake of the biodegradable plastic packaging market.

Feedstock price volatility for PLA

Corn and sugarcane spot prices fluctuated 25-40% during 2024, directly lifting monomer costs and unsettling multi-year supply contracts.[2]Dow, “Dow and New Energy Blue announce collaboration to develop renewable plastic materials from corn residue,” corporate.dow.com Drought-induced yield drops, biofuel policy competition, and regional export restrictions heighten risk relative to naphtha-sourced polymers. Producers hedge via long-term grower agreements and diversification into residue-based sugars, yet procurement teams still cite raw-material unpredictability as the top budgeting challenge.

Segment Analysis

By Material Type: PHA Disrupts PLA Dominance

The biodegradable plastic packaging market size for material types remained skewed toward Polylactic Acid, which held 66.45% share in 2024, yet Polyhydroxyalkanoates posted the strongest 25.34% CAGR outlook. PHA’s ability to biodegrade in marine settings satisfies growing coastal-waste legislation, making it the preferred option for straws, cutlery, and high-barrier pouches targeting island and port cities. Manufacturers exploit its broad melt-flow window to mold thicker pharmaceutical vials and personal-care jars that PLA struggles to handle. The segment also benefits from fresh capacity announcements in the United States and Thailand that leverage agricultural residues instead of food-grade sugar sources, insulating it from feedstock swings.

PLA remains cost-competitive where industrial composting exists, supporting bakery films and thermoformed salad tubs in Western Europe. Continuous R&D produced higher-heat Ingeo grades that withstand 105 °C filling temperatures, narrowing earlier performance gaps. PBAT and PBS serve niche heat-resistant or chemical-contact applications, while starch blends dominate ultra-price-sensitive grocery bag programs. The overall material landscape shows a transition from first-generation cost leadership to second-generation performance leadership, reinforcing the long-term diversification of the biodegradable plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Flexible Dominance Faces Rigid Innovation

Flexible formats commanded 58.77% of the biodegradable plastic packaging market share in 2024, underpinned by light-weighted pouches, wraps, and mailers that minimize freight costs for e-commerce and meal-kit delivery. Films processed on retrofitted lines achieve oxygen transmission rates suitable for fresh produce, extending shelf life without secondary wraps. Premium snack brands emphasize transparent windows made from clarified PLA to showcase product integrity, while laminates incorporating PBAT improve puncture resistance.

Rigid formats accelerate at 23.1% CAGR on the back of coffee pods, hot-cup linings, and microwave-ready trays. NatureWorks and machine supplier IMA released a turnkey pod system that meets Keurig and Nespresso specifications and composts in 90 days, opening high-volume beverage channels. Foodservice chains shift from polystyrene clamshells to PHA-lined fiber bowls compatible with industrial composters, satisfying performance and brand-equity goals. The fast-growing rigid segment illustrates how functionality gains erode legacy dominance and broaden total addressable revenue for the biodegradable plastic packaging market.

By End-use Industry: Foodservice Acceleration Outpaces Food Segment

In 2024, the food segment generated the largest volume yet foodservice now advances faster at a 24.68% CAGR. Chain restaurants leverage compostable disposables to save dishwashing labor and tap green marketing value, while municipal green-bin programs remove landfill tipping fees. Stadiums and event venues replicate the model, specifying single-material PLA cups and beer lids that match local industrial composting standards.

Packaged food makers still rely on bio-films for fresh produce, dairy, and confectionery, but adoption cycles are tied to slower retail re-tooling. Beverage brands experiment with PHA-coated paper bottles for chilled juice, while concentrated cleaning products in refill pouches illustrate cross-industry spill-over. Pharmaceutical trials of barrier-coated tablets show promise, though regulatory validation lengthens timelines. Overall, operational convenience and cost-avoidance explain why foodservice leads near-term demand in the biodegradable plastic packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Compostability: Home Solutions Gain Infrastructure Support

Industrial-compostable grades retained 55.78% of the 2024 biodegradable plastic packaging market size because commercial facilities in Europe and select US states guarantee complete breakdown within 6-12 weeks. Closed-loop collection at corporate campuses and stadiums further supports volume. However, home-compostable SKUs are scaling quickly as suburban municipalities distribute kitchen bins and offer curbside pickup. Brands print prominent “home-OK” logos to minimize consumer confusion and avoid fines for incorrect disposal. PHA and advanced PLA blends meet stricter low-temperature disintegration tests under ASTM D6400 and EN 13432, unlocking garden-compost bin channels and boosting the segment’s 22.56% growth rate.

Geography Analysis

Europe’s mature composting infrastructure and comprehensive regulatory backdrop secured 35.57% biodegradable plastic packaging market share in 2024. Regional resin producers benefit from cohesive EN standards and predictable demand created by extended-producer-responsibility fees, while converters profit from proximity to high-growth food delivery platforms now ubiquitous in Paris, Berlin, and Madrid. Government subsidies for separate organic waste collection further aid pack adoption, cementing Europe’s near-term leadership.

Asia-Pacific generates the strongest 24.65% CAGR as India, China, and Thailand enforce phased bans on difficult-to-recycle packaging formats. Chinese directives targeting “non-degradable” plastics in tier-one cities escalate from carrier bags to takeaway containers by 2027, spawning localized plants using cassava and rice-husk feedstocks. India’s state regulations remain fragmented, yet cumulative population coverage draws multinational quick-service restaurants to standardize compostable coating technologies. Australia and New Zealand also adopted comprehensive single-use plastic prohibitions, driving immediate substitution demand throughout Oceania.

North America leverages food-delivery mandates and internal carbon-pricing at Fortune 500 corporations to propel adoption, although regional coverage of industrial composting remains uneven. Latin American megacities such as São Paulo and Mexico City deploy pilot composting hubs, setting the stage for broader growth. In the Middle East and Africa, landfill scarcity and tourism-driven plastic bans create niche opportunities, especially in Gulf Cooperation Council hospitality sectors. Overall, jurisdictional policy cadence and infrastructure investment patterns explain divergent regional growth in the biodegradable plastic packaging market.

Competitive Landscape

BASF, Amcor, and NatureWorks leverage backward integration into fermentation or polymerization assets, enabling stable output and joint development programs with converters. NatureWorks’ Ingeo upgrades and BASF’s ecovio expansion illustrate investment in differentiated high-heat and barrier grades.[3]BASF, “BASF ecovio innovations,” basf.com Amcor pilots drop-in bio-film solutions on existing pouching lines, marketing speed-to-shelf advantages to multinational brand owners.

Emerging players focus on PHA production from waste oils and agricultural residues, reducing feedstock-cost volatility. United States start-ups backed by venture capital emphasize marine-degradation credentials attractive to coastal states legislating microplastic controls. Asian newcomers supported by rice and cassava processors exploit local biomass availability to build regional supply chains. Strategic alliances dominate: Avantium collaborates with Plastipak to scale FDCA-based polyester bottles, while Pierre Fabre partners with Sorbonne University to target cosmetic applications demanding pharmaceutical-grade purity.

M&A prospects rise as chemical majors seek access to proprietary monomers or anaerobic-digestible additives. Equipment suppliers add bio-compatible retrofits, bundling resins with machinery services to create sticky ecosystems. On the demand side, retailer long-term offtake contracts enhance revenue visibility, encouraging capacity expansions. Competitive dynamics therefore hinge on feedstock security, intellectual-property strength, and ability to validate performance in high-growth end uses of the biodegradable plastic packaging market.

Biodegradable Plastic Packaging Industry Leaders

-

Bio Packaging Films

-

Cortec Corporation

-

Folietec Kunststoffwerk AG

-

Futamara Group

-

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Dow and New Energy Blue agreed to produce bio-ethylene from corn stover at a new Iowa facility, targeting late-2025 start-up and displacing over 1 million t of CO₂ annually.

- February 2025: Mitsui Chemicals, Nan Ya Plastics, and Taiwan Mitsui Chemicals launched joint biomass-based plastics market-development efforts in Asia-Pacific.

- September 2024: Pierre Fabre teamed with Sorbonne University to develop biodegradable bioplastics for cosmetics and pharmaceuticals.

- June 2024: Thailand approved construction of a Braskem–SCGC bio-ethylene plant that will boost Southeast Asian resin supply.

Global Biodegradable Plastic Packaging Market Report Scope

The study provides market revenue (USD) based on material type, packaging type, and end-use industries. This report analyzes the factors that impact geopolitical developments in the market studied based on the prevalent base scenarios, key themes, and end-use industries-related demand cycles.

Industry experts and organizations provide volume data for biodegradable plastic packaging products. This data serves as the basis for tracking the market, with the primary metric being the production volume of raw materials utilized in manufacturing finished biodegradable plastic packaging products. Revenue is calculated by factoring in the raw material price and production volume. The derived cost represents the price of the finished product, excluding additional service costs such as printing, transportation, and other related expenses.

The biodegradable plastic packaging market is segmented by material type (starch blends, polylactic acid (PLA), poly(butylene adipate-co-terephthalate) (PBAT), polybutylene succinate (PBS), polyhydroxyalkanoates (PHA), other material types), by packaging type (flexible packaging [bags and pouches, other flexible packaging types [films, wraps], rigid packaging [tableware, trays and bowls, food containers, coffee cups and pods, other rigid packaging types]), by end-use industries (food, beverage, foodservice packaging, personal care and home care, pharmaceutical, other end-use industries), by Geography (North America [United States, Canada], Europe [France, Germany, Italy, Spain, United Kingdom, Russia, Rest of Europe], Asia Pacific [China, India, Japan, Rest of Asia Pacific], Latin America, Middle East and Africa [United Arab Emirates, Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| By Material Type | Starch Blends | |||

| Polylactic Acid (PLA) | ||||

| Poly(Butylene Adipate-co-Terephthalate) (PBAT) | ||||

| Polybutylene Succinate (PBS) | ||||

| Polyhydroxyalkanoates (PHA) | ||||

| Other Material Types | ||||

| By Packaging Type | Flexible Packaging | Bags and Pouches | ||

| Films and Wraps | ||||

| Labels and Sleeves | ||||

| Rigid Packaging | Tableware | |||

| Trays and Bowls | ||||

| Food Containers | ||||

| Coffee Cups and Pods | ||||

| Other Rigid Packaging | ||||

| By End-use Industry | Food | |||

| Beverage | ||||

| Foodservice | ||||

| Personal Care and Home Care | ||||

| Pharmaceutical | ||||

| Other End - Use Industry | ||||

| By Compostability | Home-Compostable | |||

| Industrial-Compostable | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| Middle East and Africa | Middle East | United Arab Emirates | ||

| Saudi Arabia | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

By Material Type

| Starch Blends |

| Polylactic Acid (PLA) |

| Poly(Butylene Adipate-co-Terephthalate) (PBAT) |

| Polybutylene Succinate (PBS) |

| Polyhydroxyalkanoates (PHA) |

| Other Material Types |

By Packaging Type

| Flexible Packaging | Bags and Pouches |

| Films and Wraps | |

| Labels and Sleeves | |

| Rigid Packaging | Tableware |

| Trays and Bowls | |

| Food Containers | |

| Coffee Cups and Pods | |

| Other Rigid Packaging |

By End-use Industry

| Food |

| Beverage |

| Foodservice |

| Personal Care and Home Care |

| Pharmaceutical |

| Other End - Use Industry |

By Compostability

| Home-Compostable |

| Industrial-Compostable |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the biodegradable plastic packaging market?

The market is valued at USD 3.01 billion in 2025, with expectations of reaching USD 7.70 billion by 2030 at a 20.67% CAGR.

Which material leads the biodegradable plastic packaging market?

Polylactic Acid leads with 66.45% share in 2024, though Polyhydroxyalkanoates are growing fastest at 25.34% CAGR.

Why is foodservice driving demand for biodegradable packs?

Restaurants and delivery platforms cut waste-disposal fees and meet consumer sustainability preferences, resulting in a 24.68% CAGR for foodservice applications.

How do regional regulations influence adoption?

The EU Single-Use Plastic Directive and similar bans in India, China, and Australia mandate compostable substitutes, providing clear growth visibility across geographies.

What restraints could slow market growth?

Insufficient industrial-composting capacity in emerging economies and feedstock price volatility for PLA remain the chief obstacles to consistent global scaling.

Who are the major players in the biodegradable plastic packaging industry?

Key companies include BASF, Amcor, NatureWorks, Avantium, and emerging PHA producers leveraging agricultural residues for cost-stable supply.

Page last updated on: July 3, 2025